Japan’s inflation hit a 40-year high in October, driven by a policy of placing stock market gains above all else.

When Japan first adopted negative interest rates, the argument was that it would help end the country’s deflationary spiral and return inflation to a 2% goal. Now that inflation is nearly twice as high as the goal, one might expect rates to move at least a little higher.

When Japan first adopted negative interest rates, the argument was that it would help end the country’s deflationary spiral and return inflation to a 2% goal. Now that inflation is nearly twice as high as the goal, one might expect rates to move at least a little higher.

Although the BoJ has allowed the 10Y to rise to 0.24%… …they have held short-term rates at -0.1% since 2016.

…they have held short-term rates at -0.1% since 2016. The BoJ’s utter lack of candor is nothing new. Forget about FTX. Japan’s markets are the biggest Ponzi scheme on Earth. Since the Fukushima disaster in 2011, Japan’s stock market has been driven principally by the yen carry trade which relies on an ever-cheaper yen to attract capital into the stock market.

The BoJ’s utter lack of candor is nothing new. Forget about FTX. Japan’s markets are the biggest Ponzi scheme on Earth. Since the Fukushima disaster in 2011, Japan’s stock market has been driven principally by the yen carry trade which relies on an ever-cheaper yen to attract capital into the stock market. The obvious limit to this scheme is that as the yen depreciates, imports become more expensive. And, since Japan imports all of its oil and most of its food, it was simply a matter of time before inflation bit Japan in the お尻.

The obvious limit to this scheme is that as the yen depreciates, imports become more expensive. And, since Japan imports all of its oil and most of its food, it was simply a matter of time before inflation bit Japan in the お尻.

Luckily for Japan, they have no bond market per se. The entirety of Japan’s borrowings are purchased by the BoJ. This monetization of debt has gone on for years without repercussions – until now.

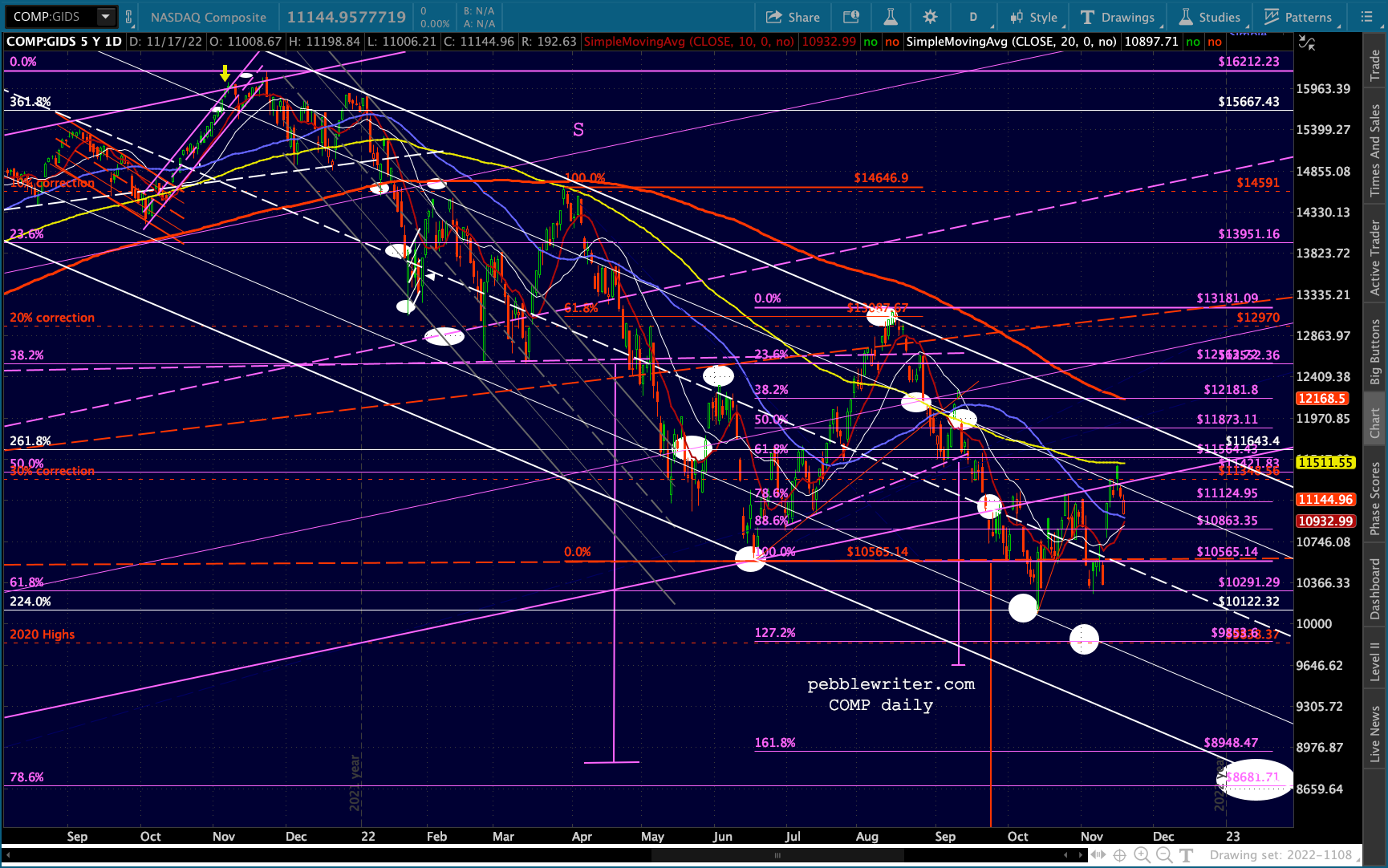

The Nikkei was locked in a falling price channel between Feb 2021 and Mar 2022, when the decline finally reached -20.7%. At that point, it was less than 1% away from its pre-pandemic highs of 24,140. It was no coincidence, then, that USDJPY picked that specific moment to break above both the midline of a channel and a trend line at least 50 years old.

It was no coincidence, then, that USDJPY picked that specific moment to break above both the midline of a channel and a trend line at least 50 years old. Subsequent rises in the USDJPY (declines in the yen) have acted to lift NKD above its SMA200 and out of its falling channel. Everything’s going great – unless you consider rising taxes and plunging consumer confidence problematic.

Subsequent rises in the USDJPY (declines in the yen) have acted to lift NKD above its SMA200 and out of its falling channel. Everything’s going great – unless you consider rising taxes and plunging consumer confidence problematic.

Come to think of it, the US faces similar problems.

* * *

In other news, VIX has sent the all-clear to algos to rally at least a little further – this being OPEX and all. continued for members…

continued for members…

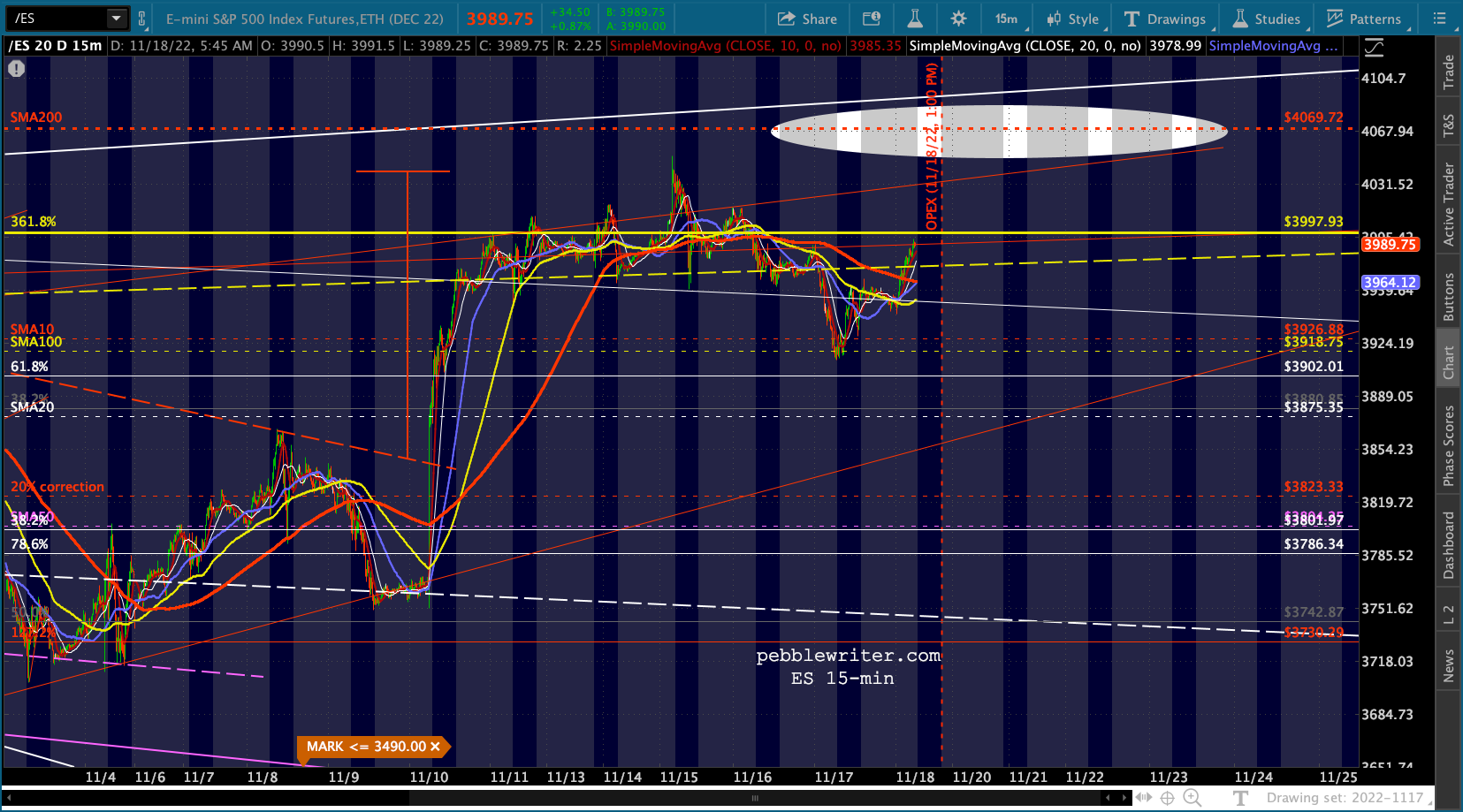

The equity picture is still uncertain as to a SMA200/channel top tag. But, with next week being a low volume holiday week, the possibility remains that we’ll get a breakout to ES 4153. If so, the question will be whether the rise above the SMA200 can hold.

The one constant since Oct 13, the day stocks last bottomed, has been a steady decline in VIX. VIX’s failure to complete its IH&S and subsequent series of lower highs and lower lows has been the biggest factor in the 10% rebound. Remember, the rebound occurred in the face of horrible earnings and outlooks for the biggest, most important stocks in the S&P 500.

The one constant since Oct 13, the day stocks last bottomed, has been a steady decline in VIX. VIX’s failure to complete its IH&S and subsequent series of lower highs and lower lows has been the biggest factor in the 10% rebound. Remember, the rebound occurred in the face of horrible earnings and outlooks for the biggest, most important stocks in the S&P 500.

Meanwhile, the yen isn’t the only currency being manipulated to prop up stocks. EURUSD finally broke out of the channel it’s been in during 18 months of its 23-month old decline.

Meanwhile, the yen isn’t the only currency being manipulated to prop up stocks. EURUSD finally broke out of the channel it’s been in during 18 months of its 23-month old decline. It seems to have stalled at its SMA200, but I’ll reserve judgement for now.

It seems to have stalled at its SMA200, but I’ll reserve judgement for now.

The DXY has stalled at a backtest of the two channels it broke out of – at least for now. It has ostensibly been reacting to interest rate expectations. But, the formula for DXY is driven primarily by the EUR, so even a nonsense rise in the EUR is enough to power DXY lower.

The DXY has stalled at a backtest of the two channels it broke out of – at least for now. It has ostensibly been reacting to interest rate expectations. But, the formula for DXY is driven primarily by the EUR, so even a nonsense rise in the EUR is enough to power DXY lower.

After VIX, the next most important macro factor at the moment is the price of oil and gas. They started the whole inflation ball rolling, and continue to be problematic. When interest rates peaked in 2014 and in 2018, it was a plunge in oil/gas prices that brought inflation and interest rates back down.

After VIX, the next most important macro factor at the moment is the price of oil and gas. They started the whole inflation ball rolling, and continue to be problematic. When interest rates peaked in 2014 and in 2018, it was a plunge in oil/gas prices that brought inflation and interest rates back down.

This was important for the US, but was essential for Japan which needed lower oil prices in order to drastically devalue the yen.

This was important for the US, but was essential for Japan which needed lower oil prices in order to drastically devalue the yen.

With Japan’s inflation reaching 40-year highs, we would expect the BoJ to exert any influence they might have to bring oil/gas prices down. Every other country on earth would benefit as well – except of course for the OPEC+ countries which are benefiting greatly.

The NOPEC countries have thus far been unsuccessful in getting prices back to 2020 levels. But, the decline from the Mar 2022 130 highs has been substantial, and likely has further to go – hence our 70.19 target for CL.

We’ll see.

In the meantime, oil and gas have broken down somewhat and – along with fears that stocks have rallied too much – are keeping rates in check.

I understand the geopolitical risks which have driven oil/gas prices so high. But, I remain bearish on them in the near term.

I understand the geopolitical risks which have driven oil/gas prices so high. But, I remain bearish on them in the near term. Even XLE is ripe for a breakdown.

Even XLE is ripe for a breakdown.  Stay tuned.

Stay tuned.