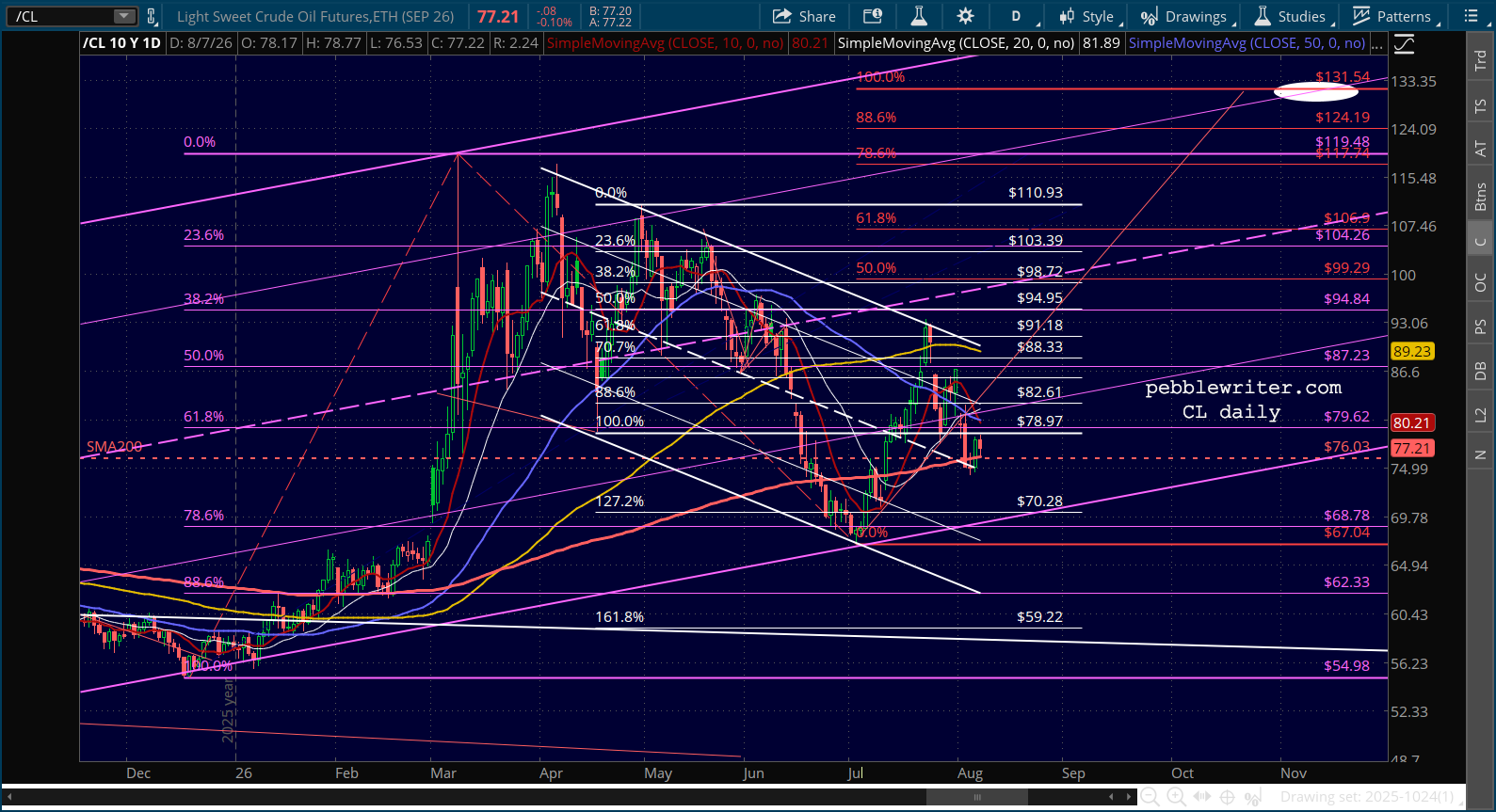

Futures are flat on slightly higher oil prices with a twist on the Iran war: any deal is likely to be between Iran and Oman, and Israel is unlikely to approve.

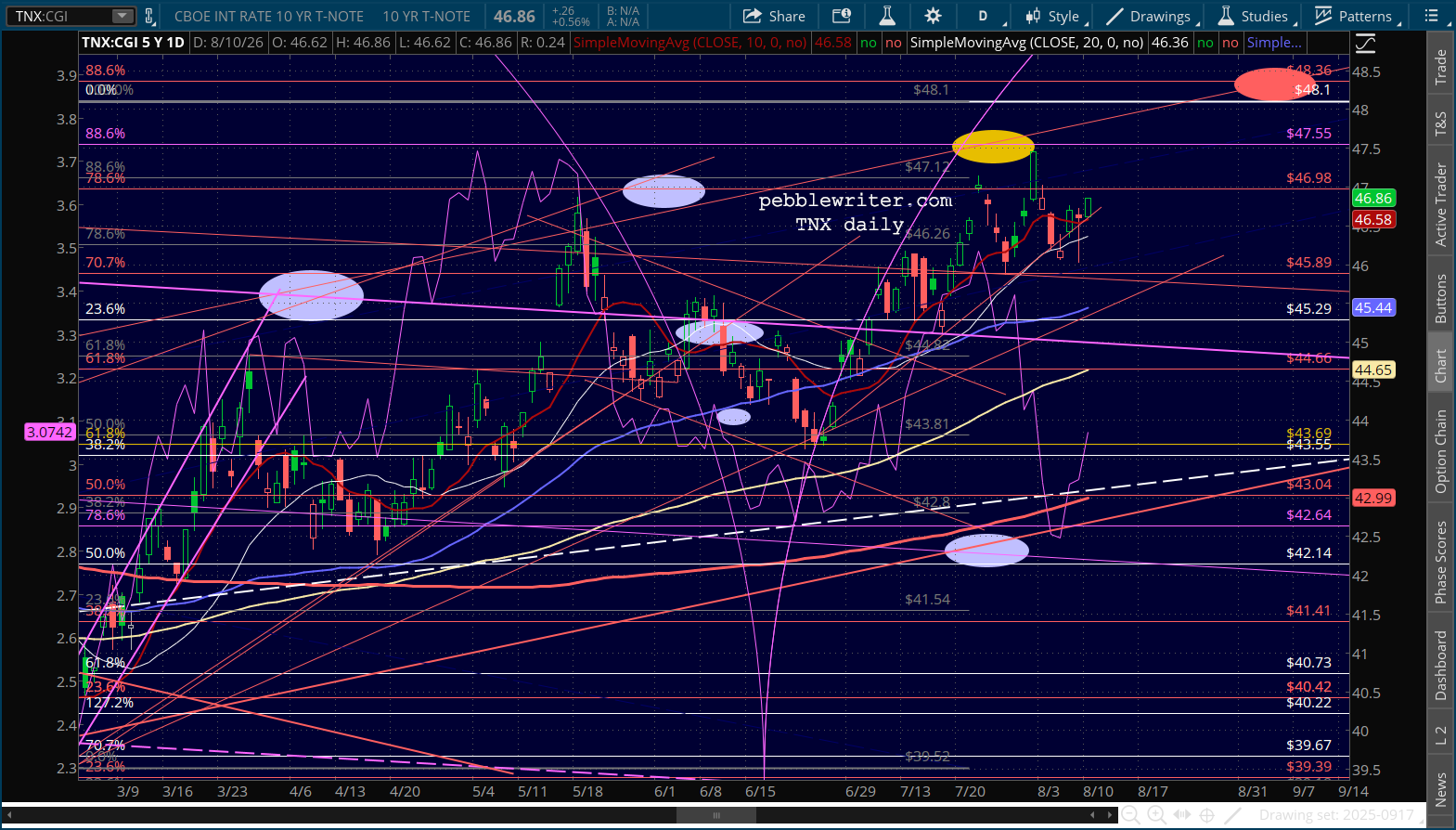

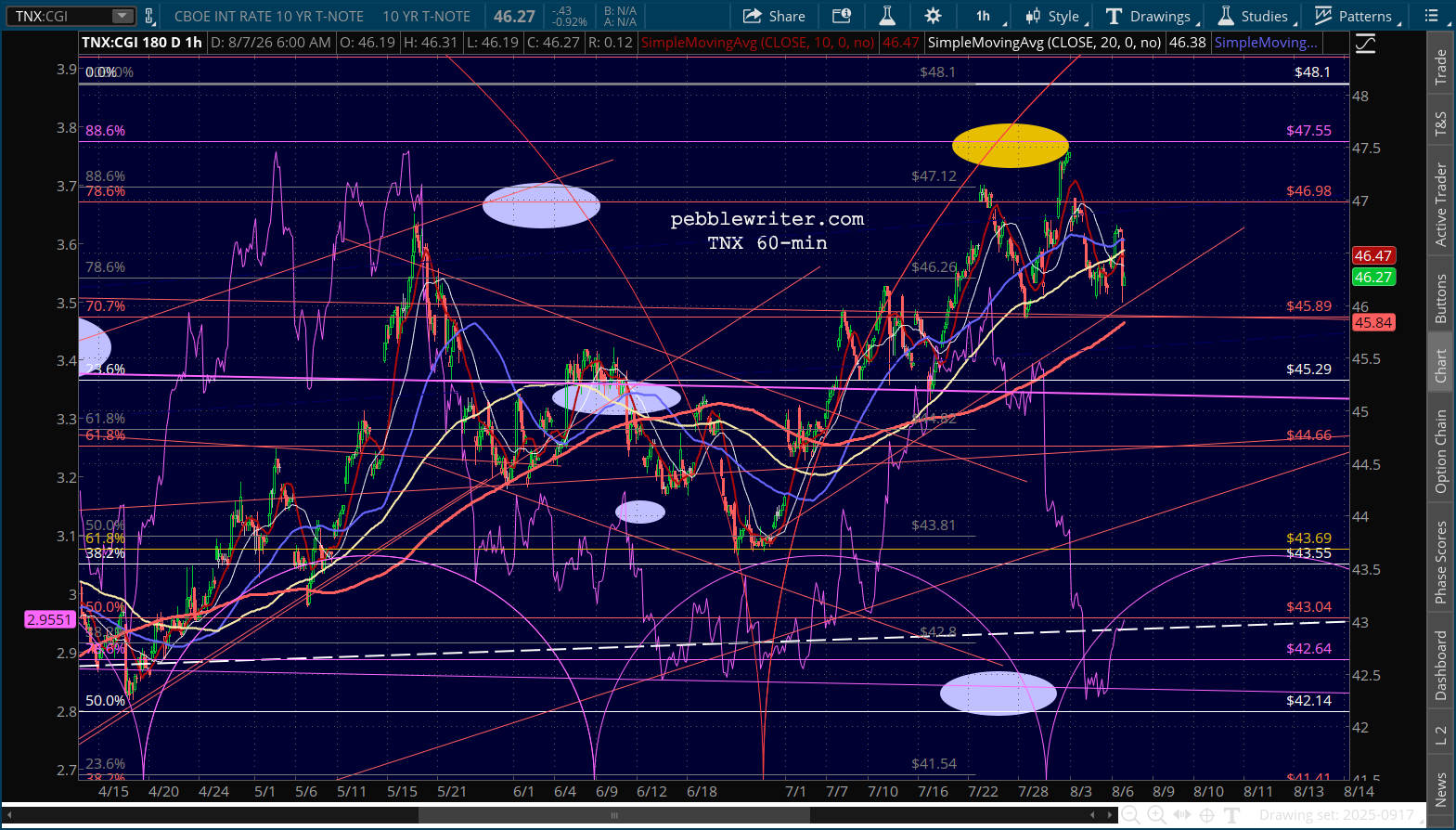

The bond market is not impressed. Last week’s breakdown in yields has been “fixed.”

Futures are flat on slightly higher oil prices with a twist on the Iran war: any deal is likely to be between Iran and Oman, and Israel is unlikely to approve.

The bond market is not impressed. Last week’s breakdown in yields has been “fixed.”

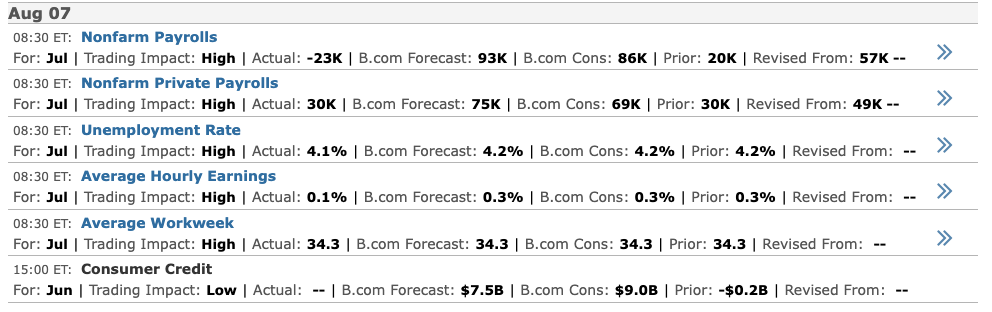

The jobs print came in at a stunning 23K drop (versus a consensus +86K gain.)

It was stunning because it potentially represents a change in strategy by the White House. Are they finally willing to admit a less than stellar job market in order to force interest rates lower and stock prices higher?

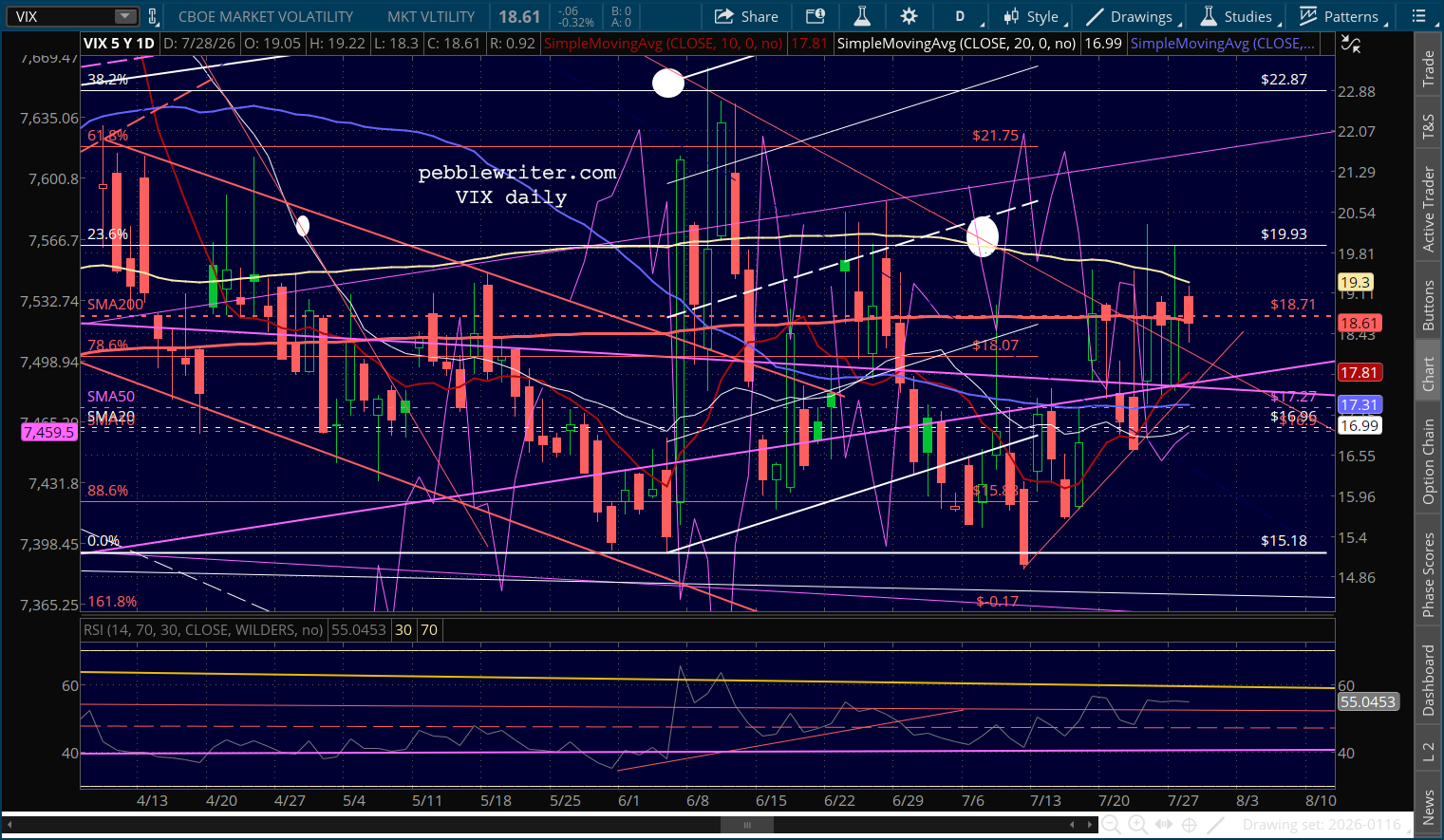

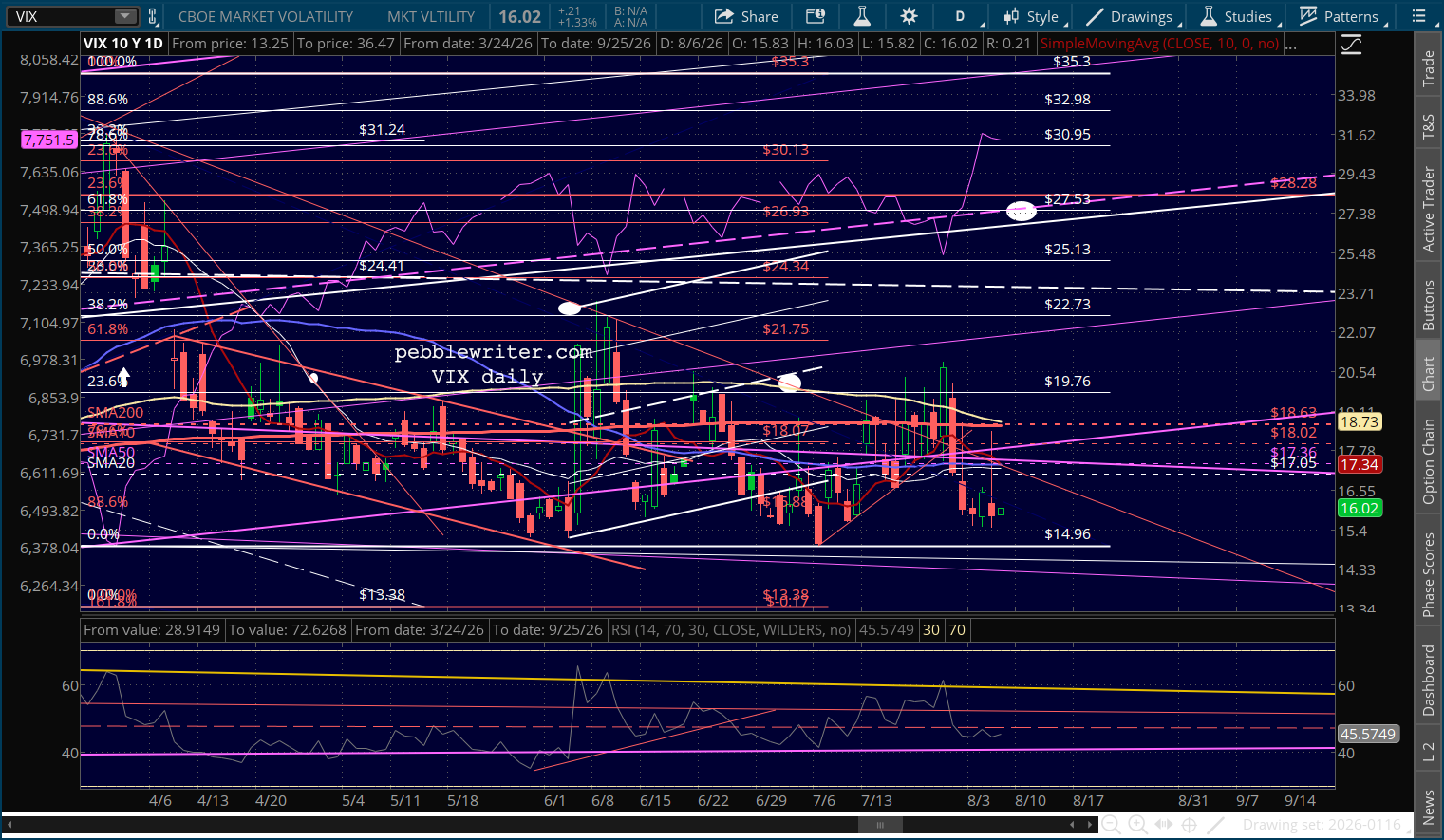

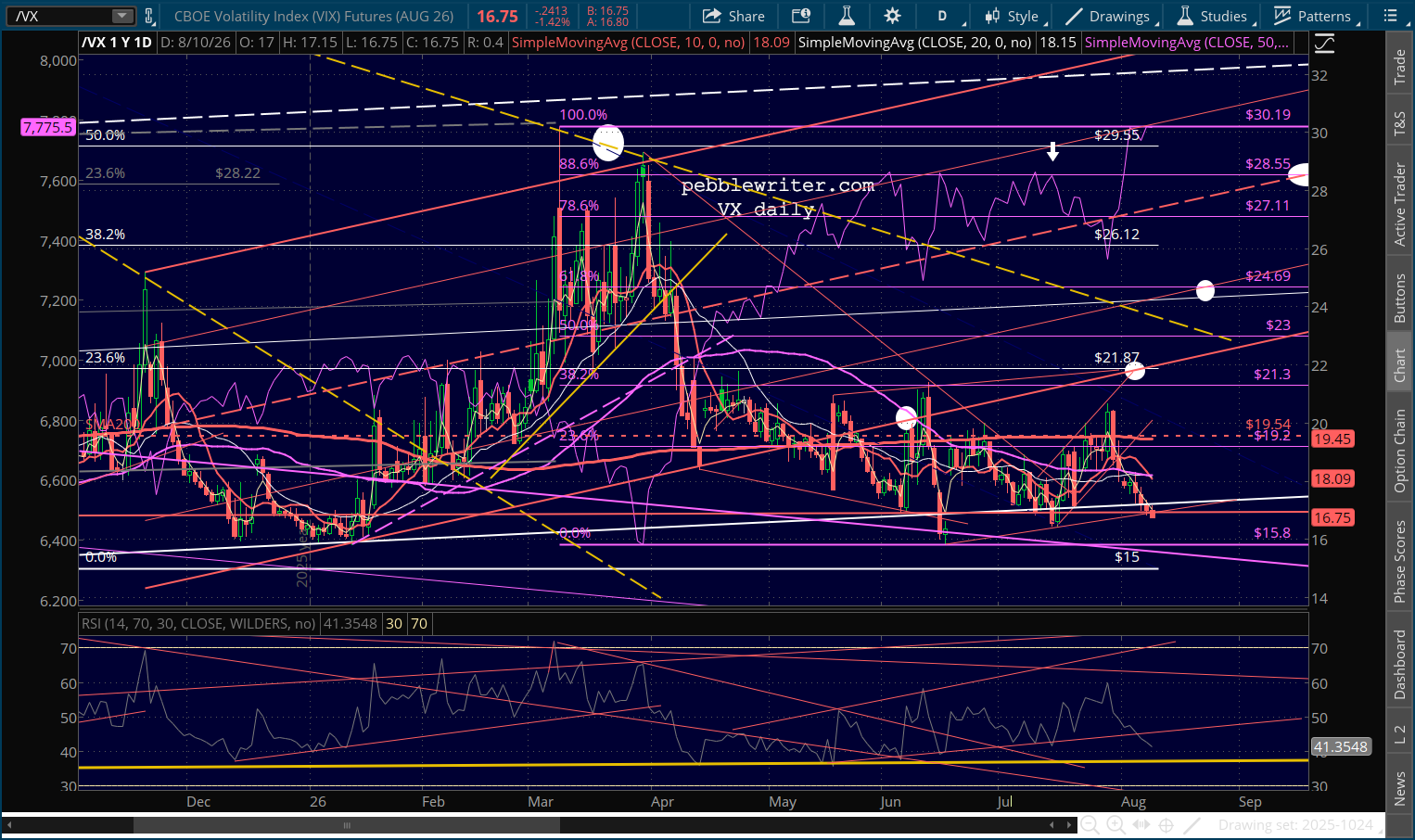

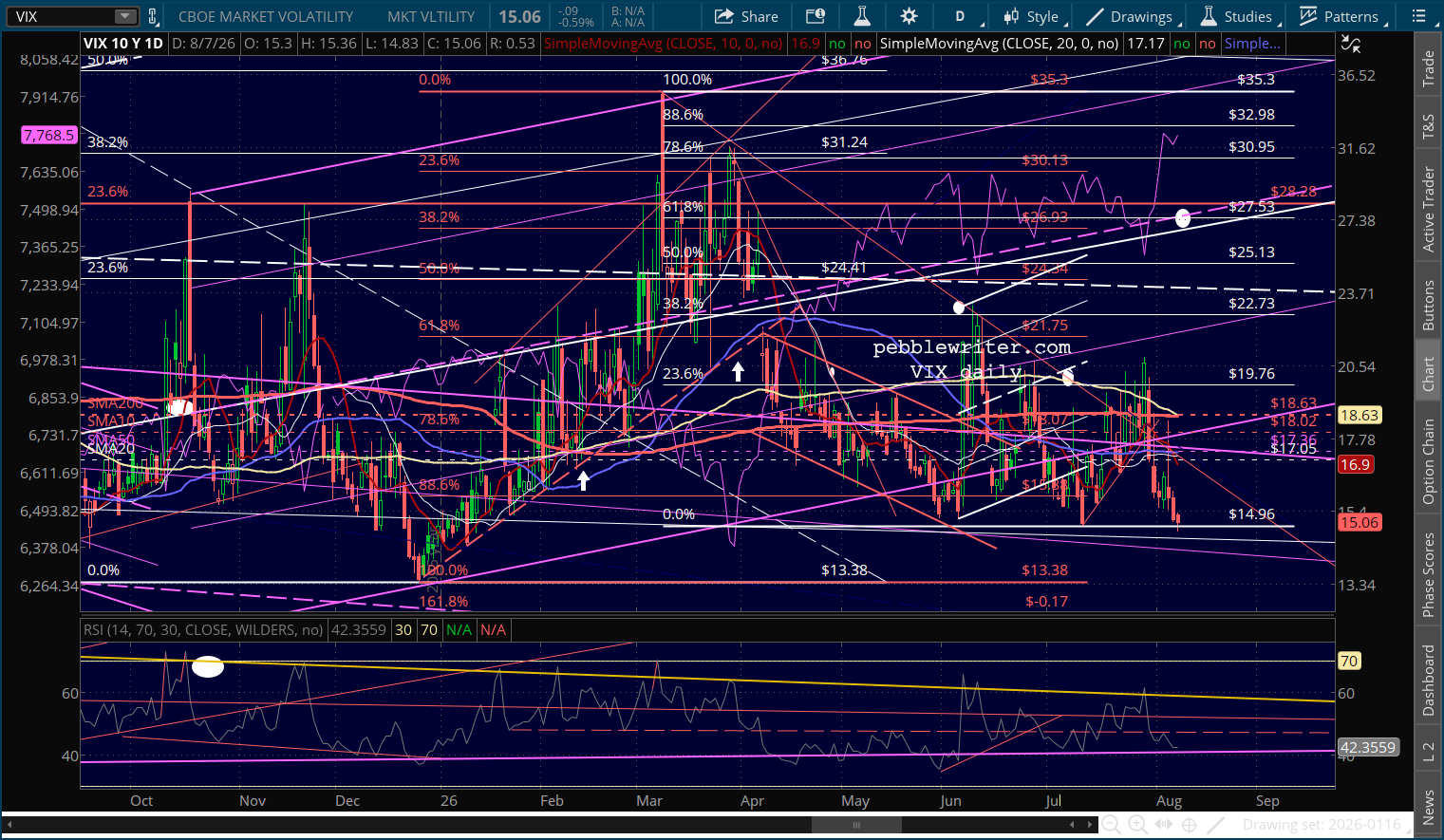

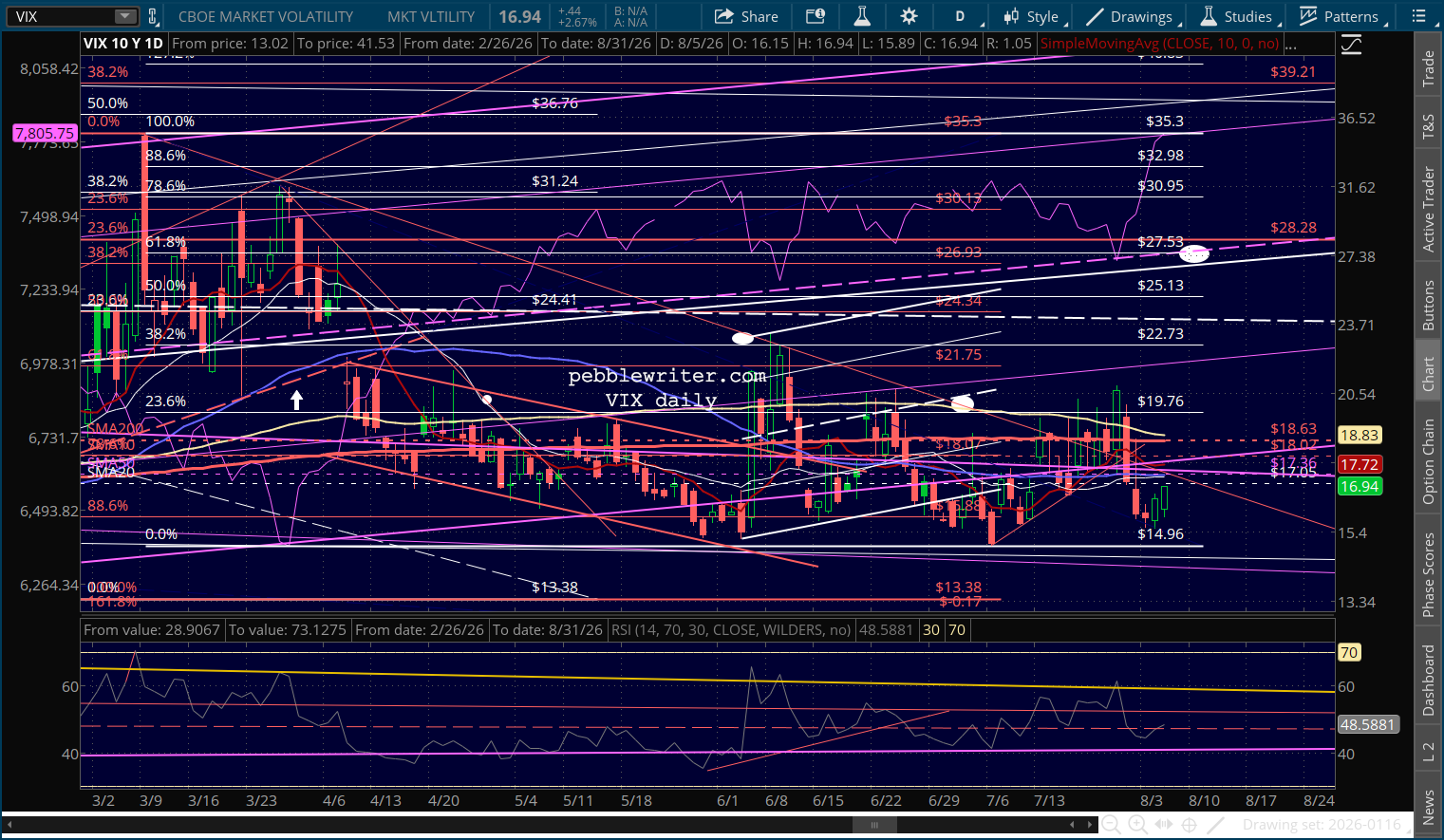

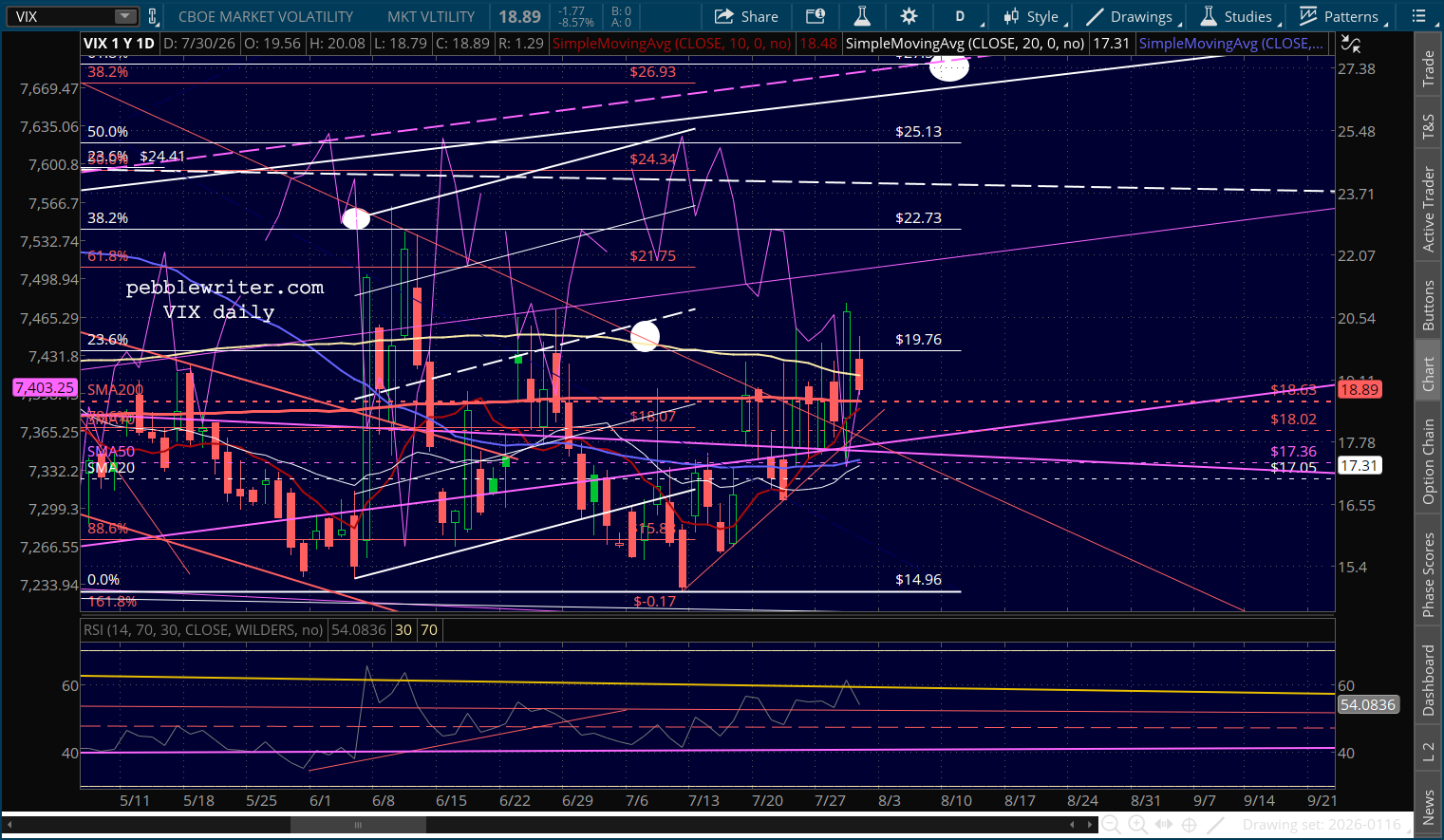

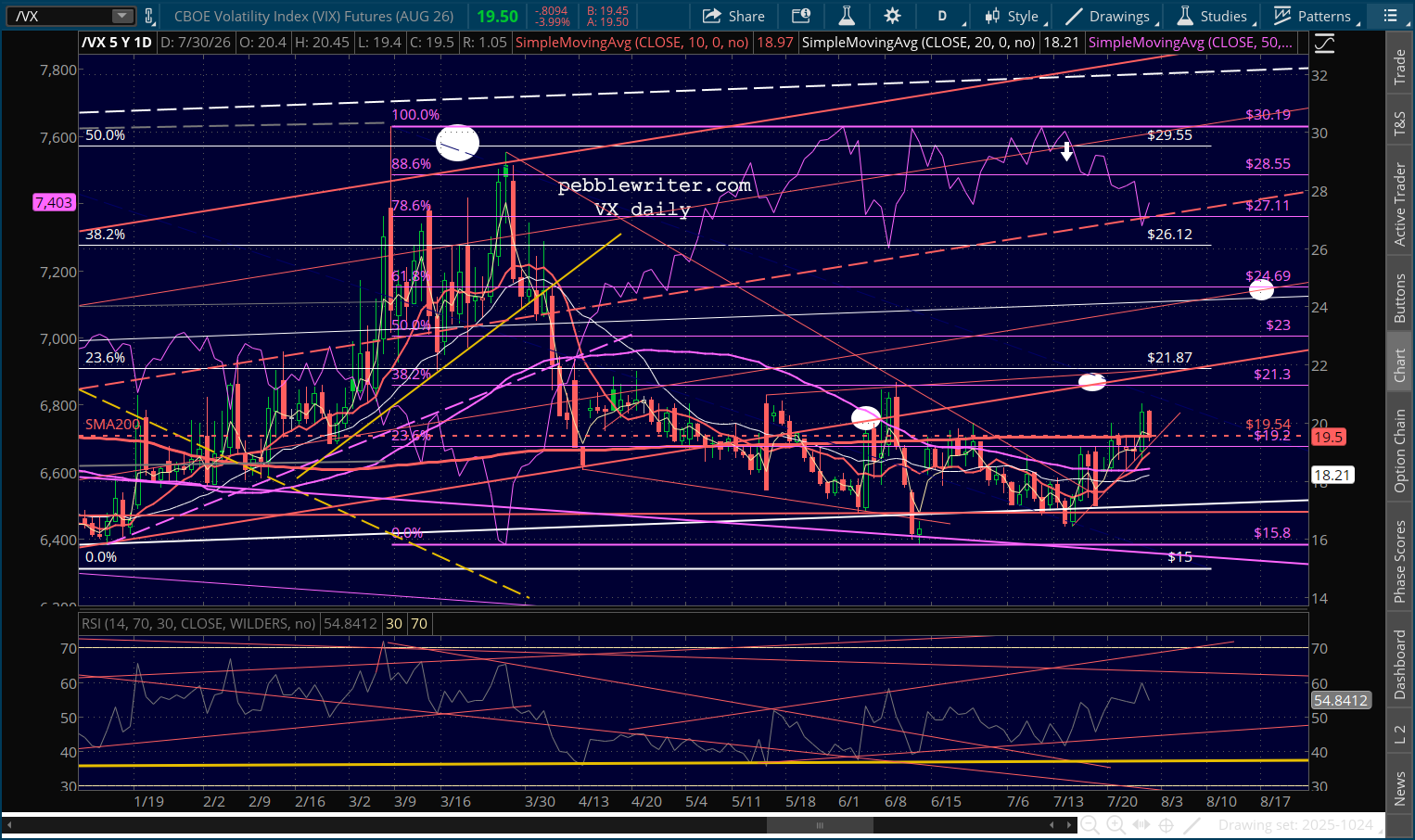

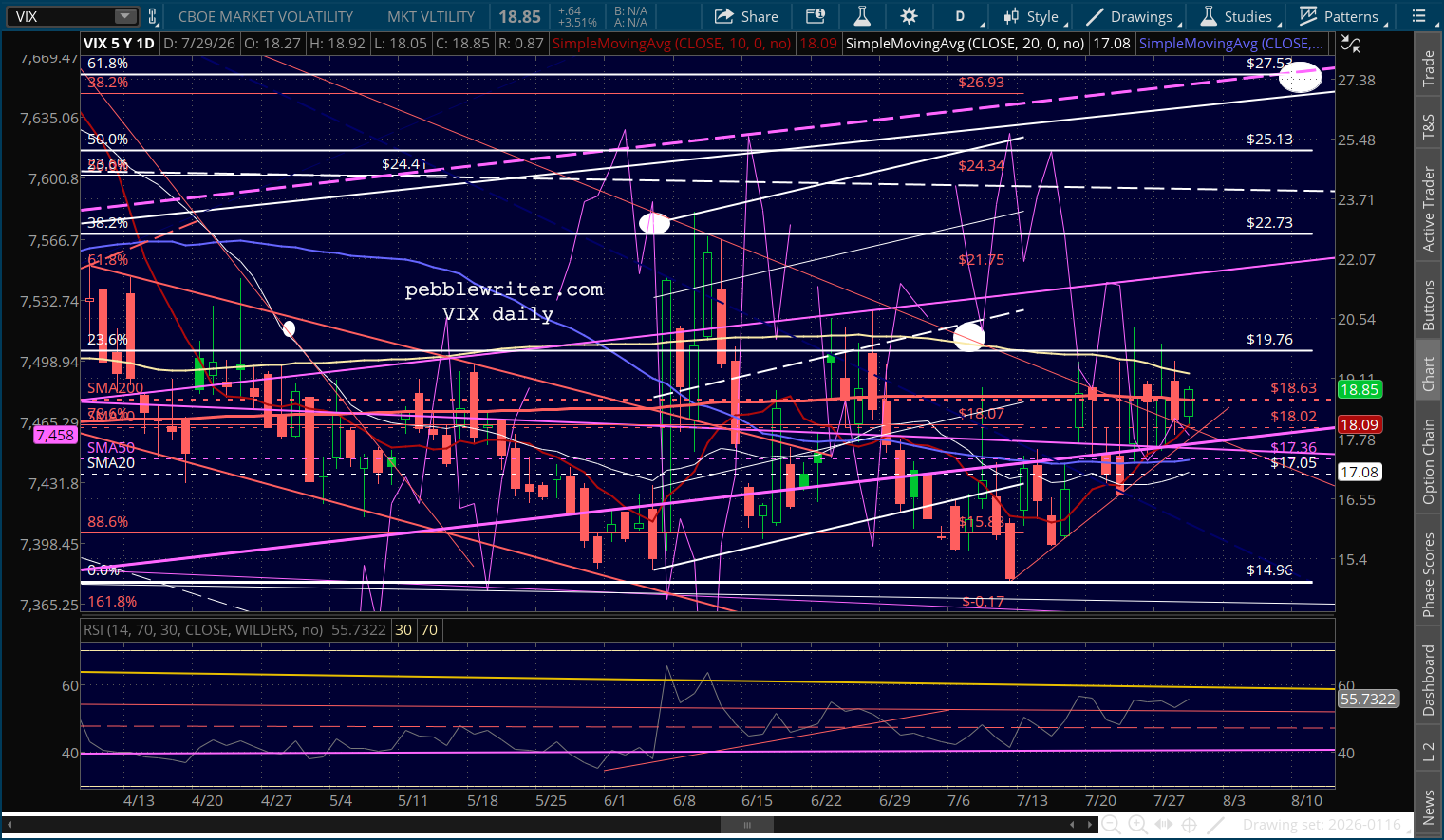

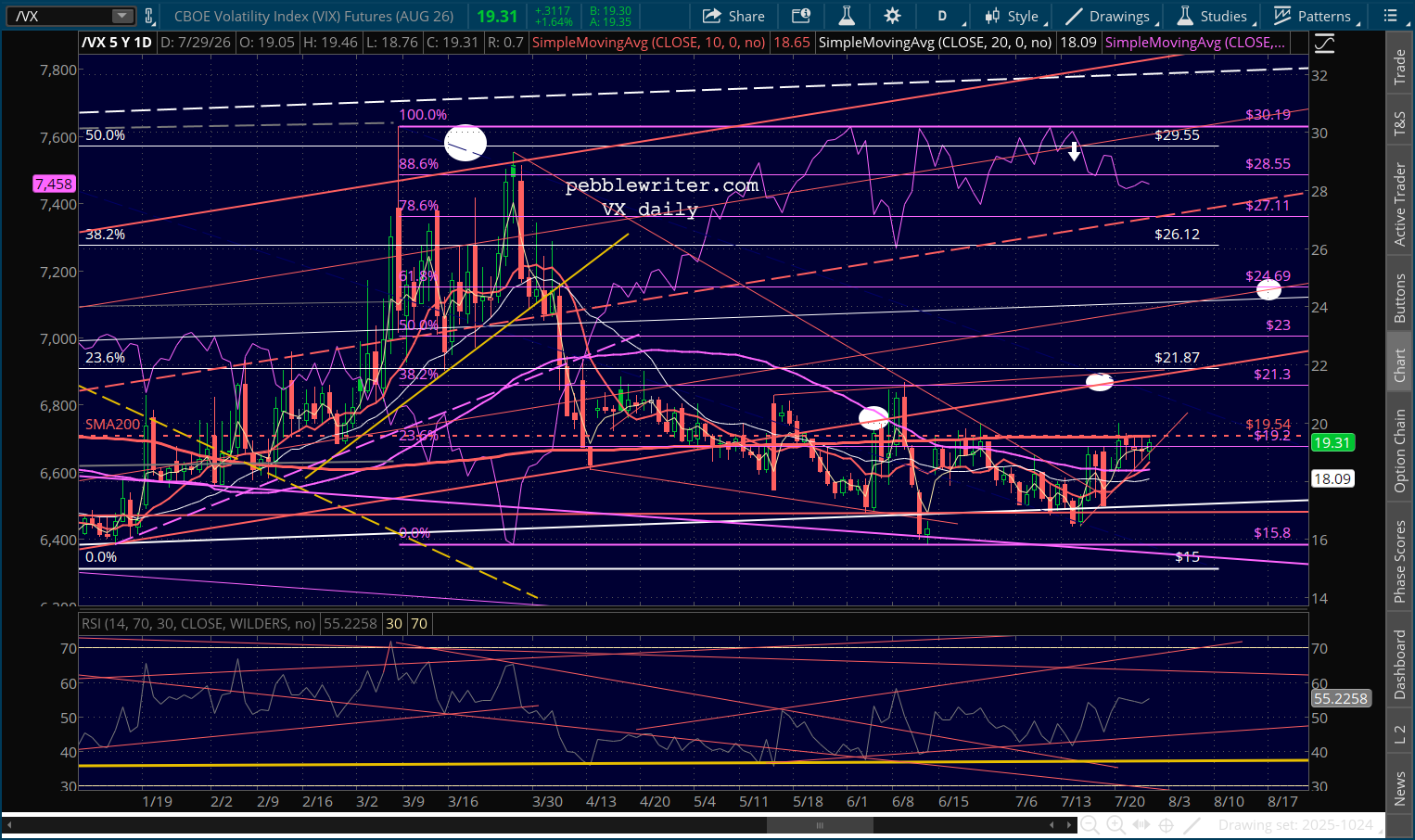

It helped to force VIX to the lowest value since early January. From the 18.43 backtest of the SMA200 two sessions ago to new lows? Yeah, okay. Why not?

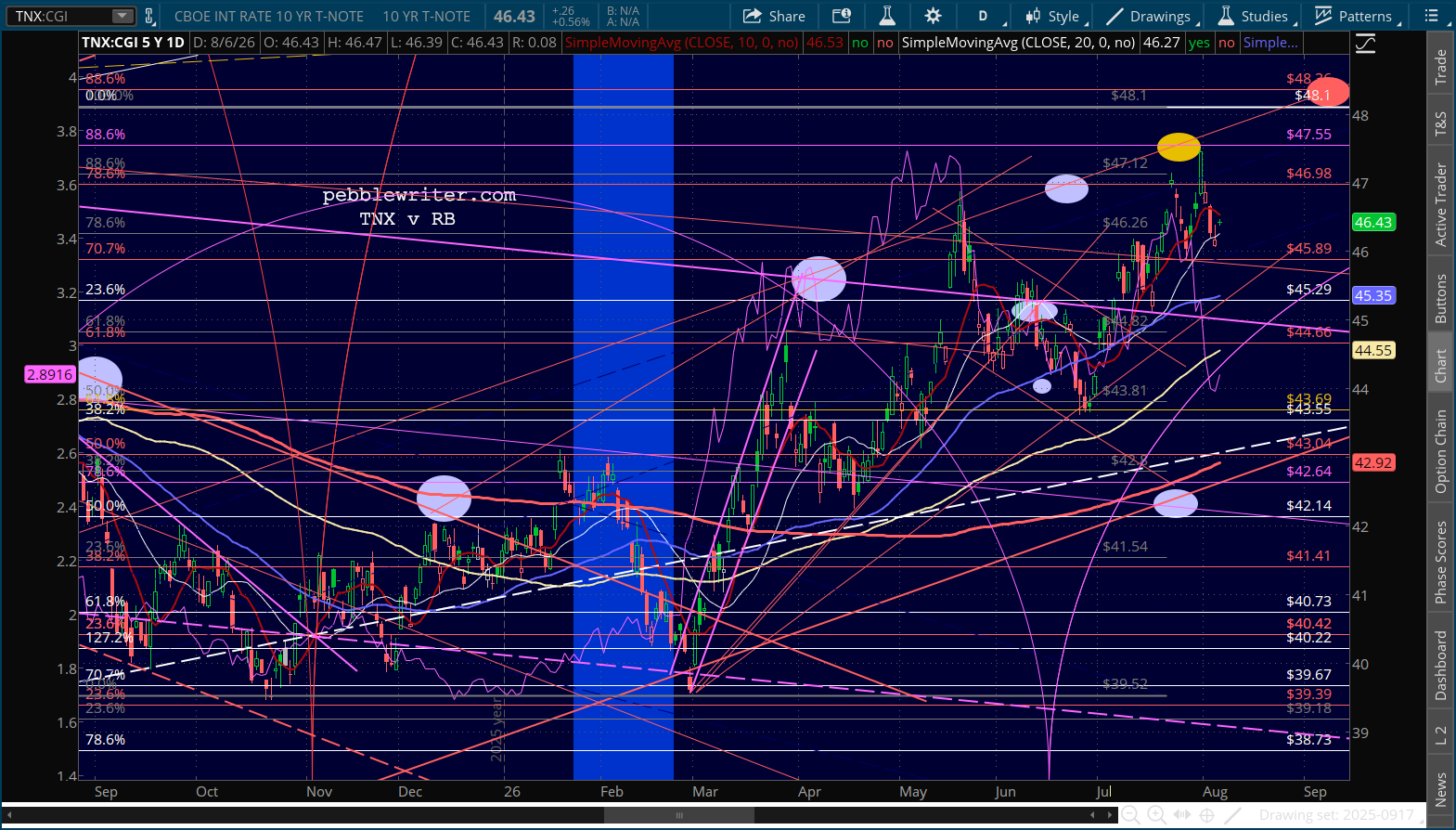

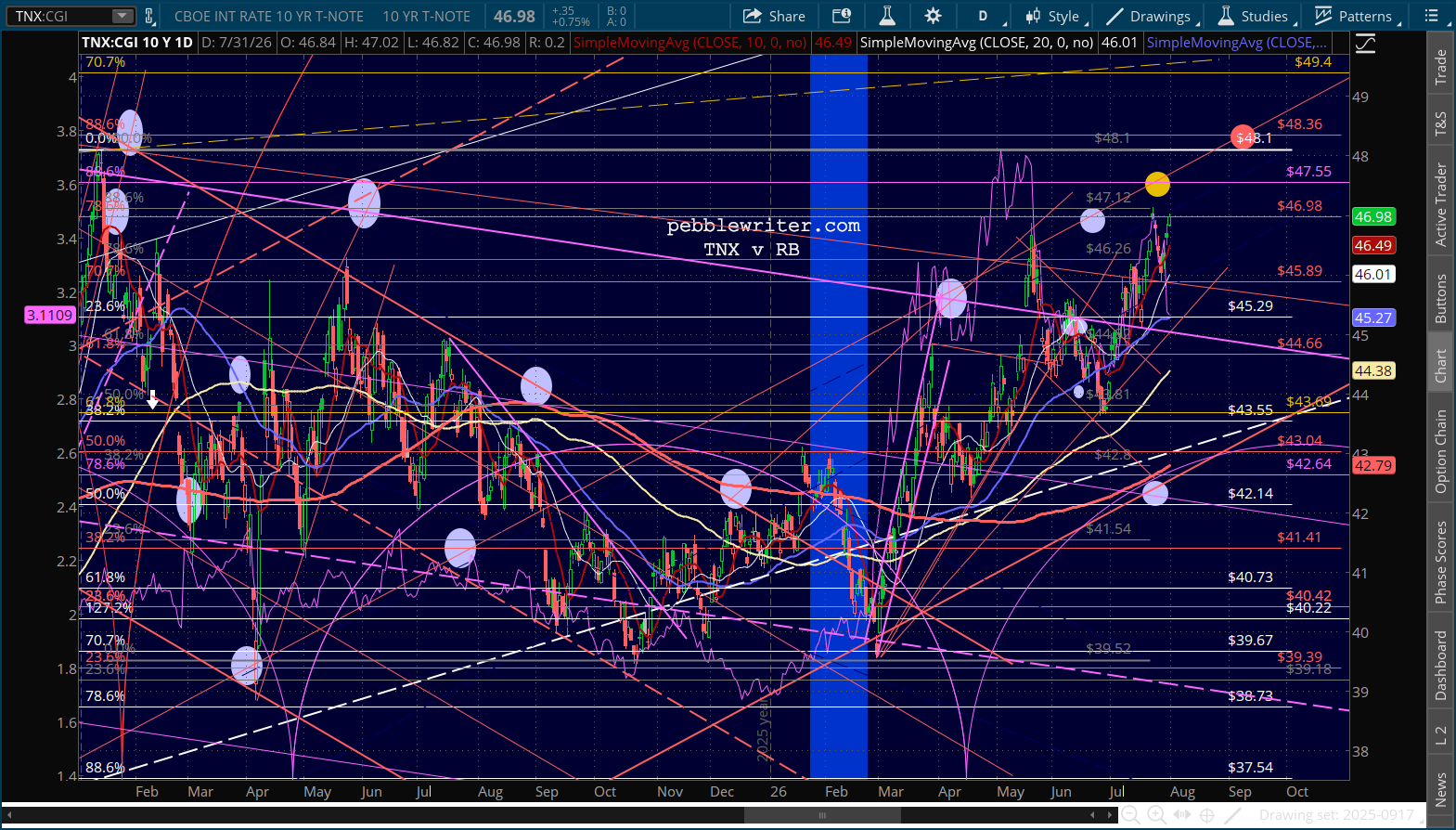

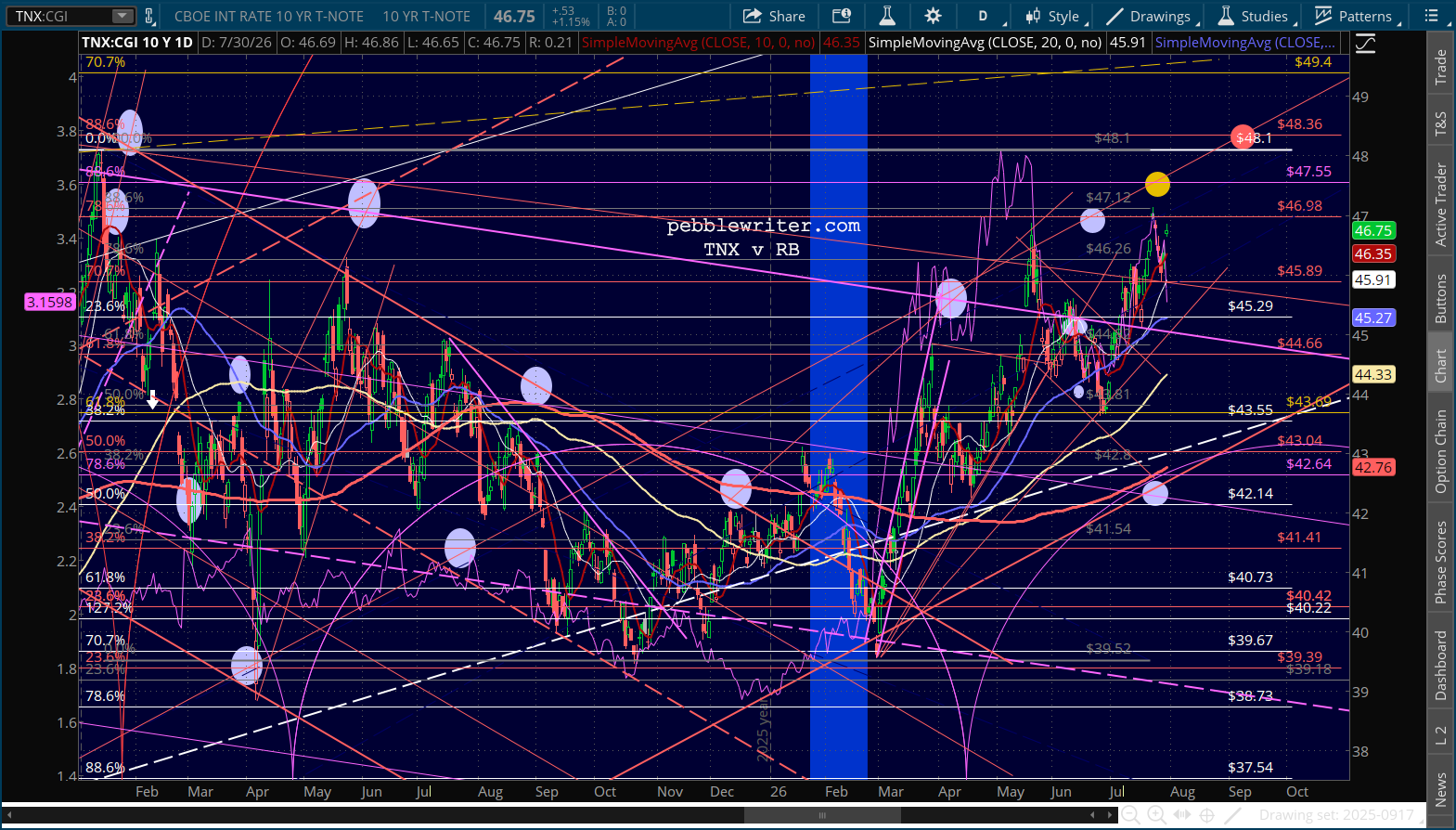

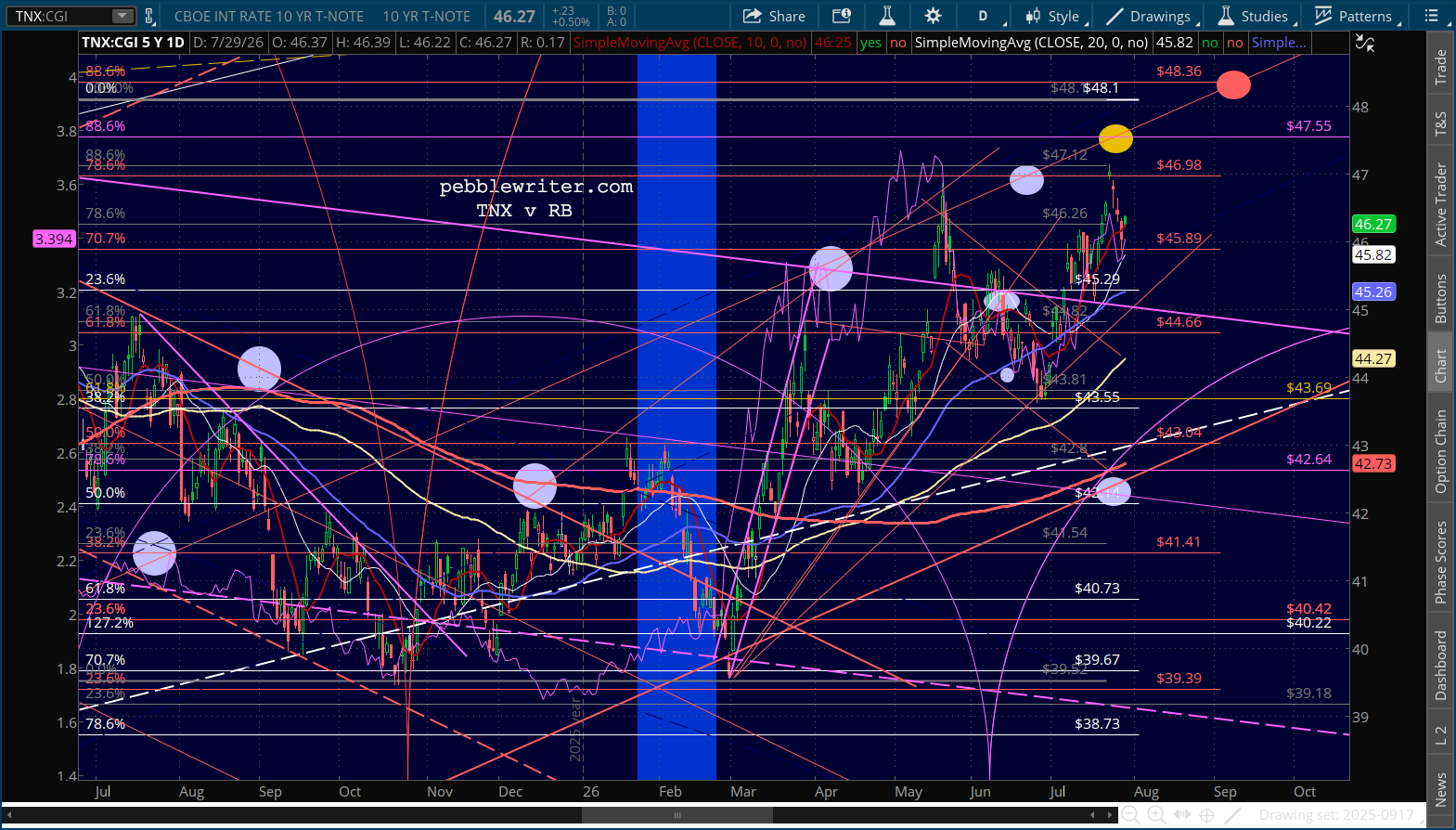

Even though the 10Y cratered on the print, it didn’t break down below the TL from mid-June. Remember, the cycle high was 4.75% at the end of July. So, 4.60 is a nice move. But, even if the trend line fails, we still have the SMA200 support just below at 4.58%.

This being Friday, it wouldn’t be surprising to see some truth about the lack of a deal in Iran sneak out…followed, of course, by a social media post before the market opens on Monday that we are ever so close to a great deal.

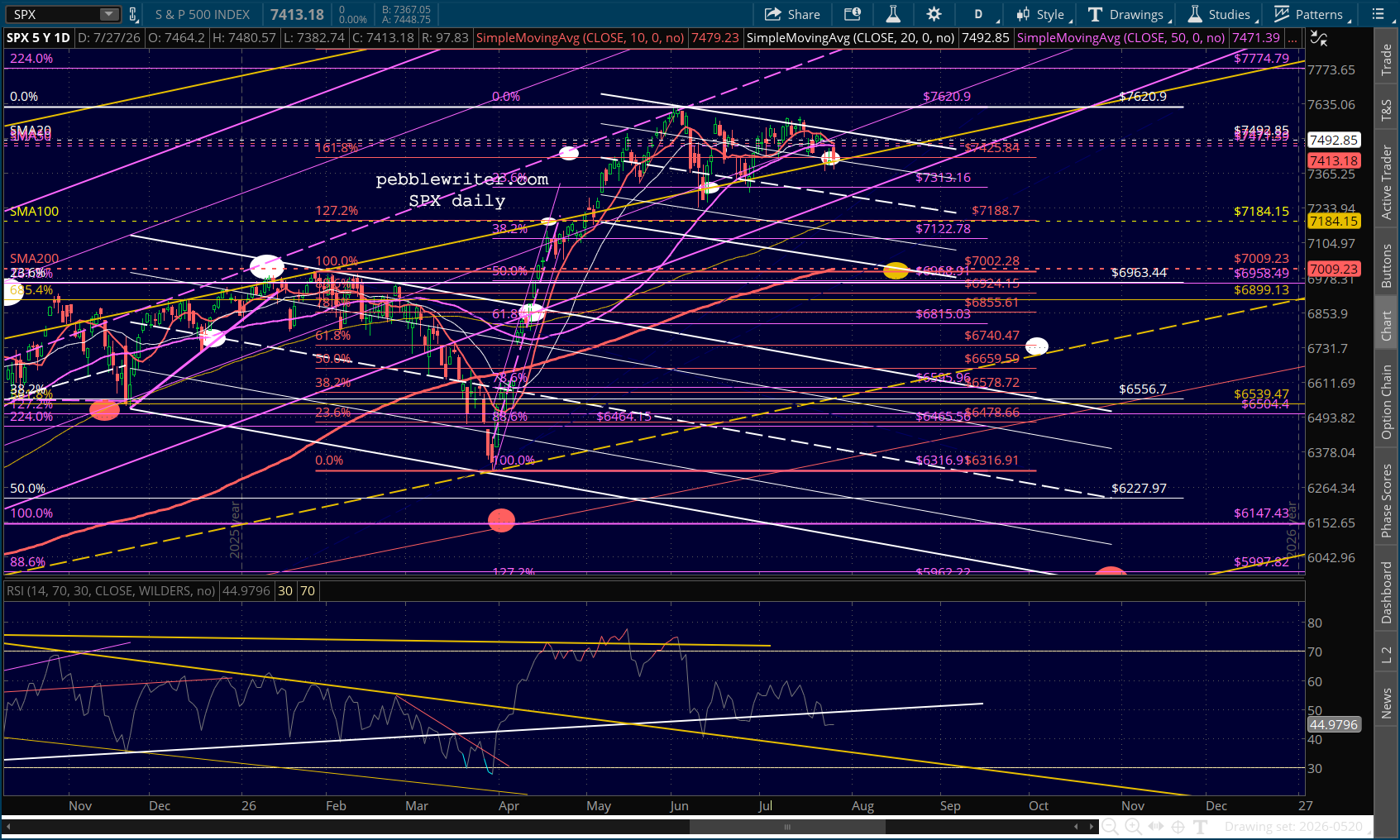

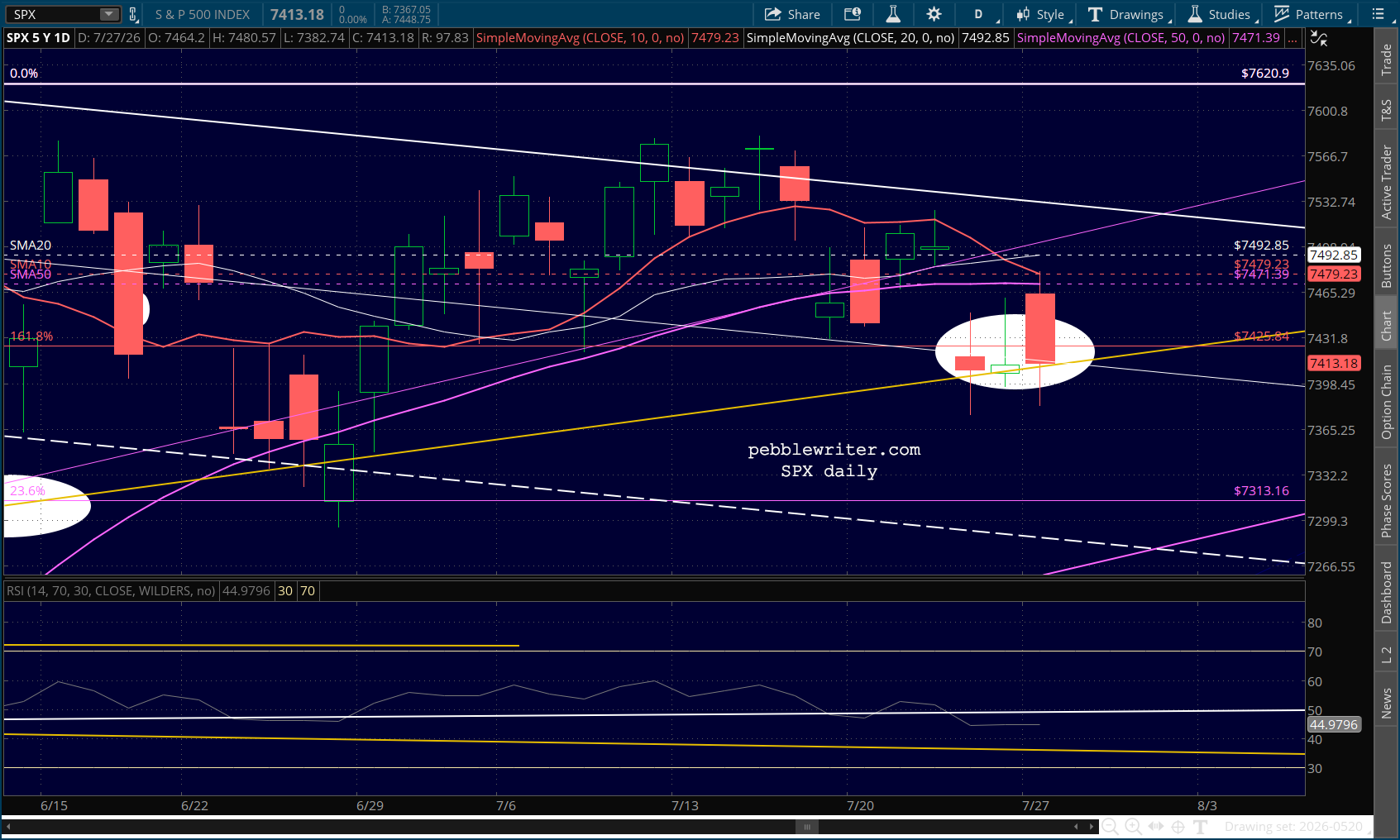

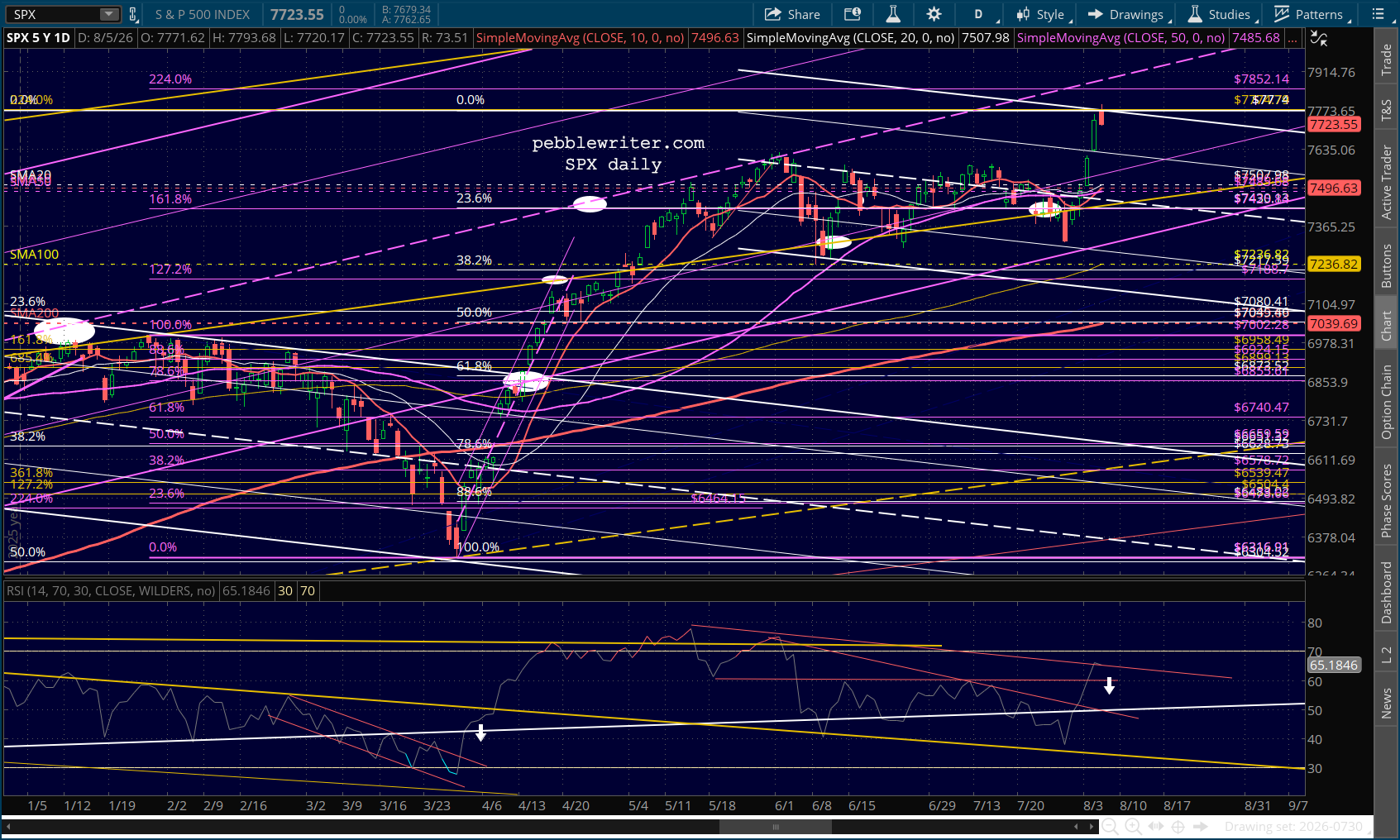

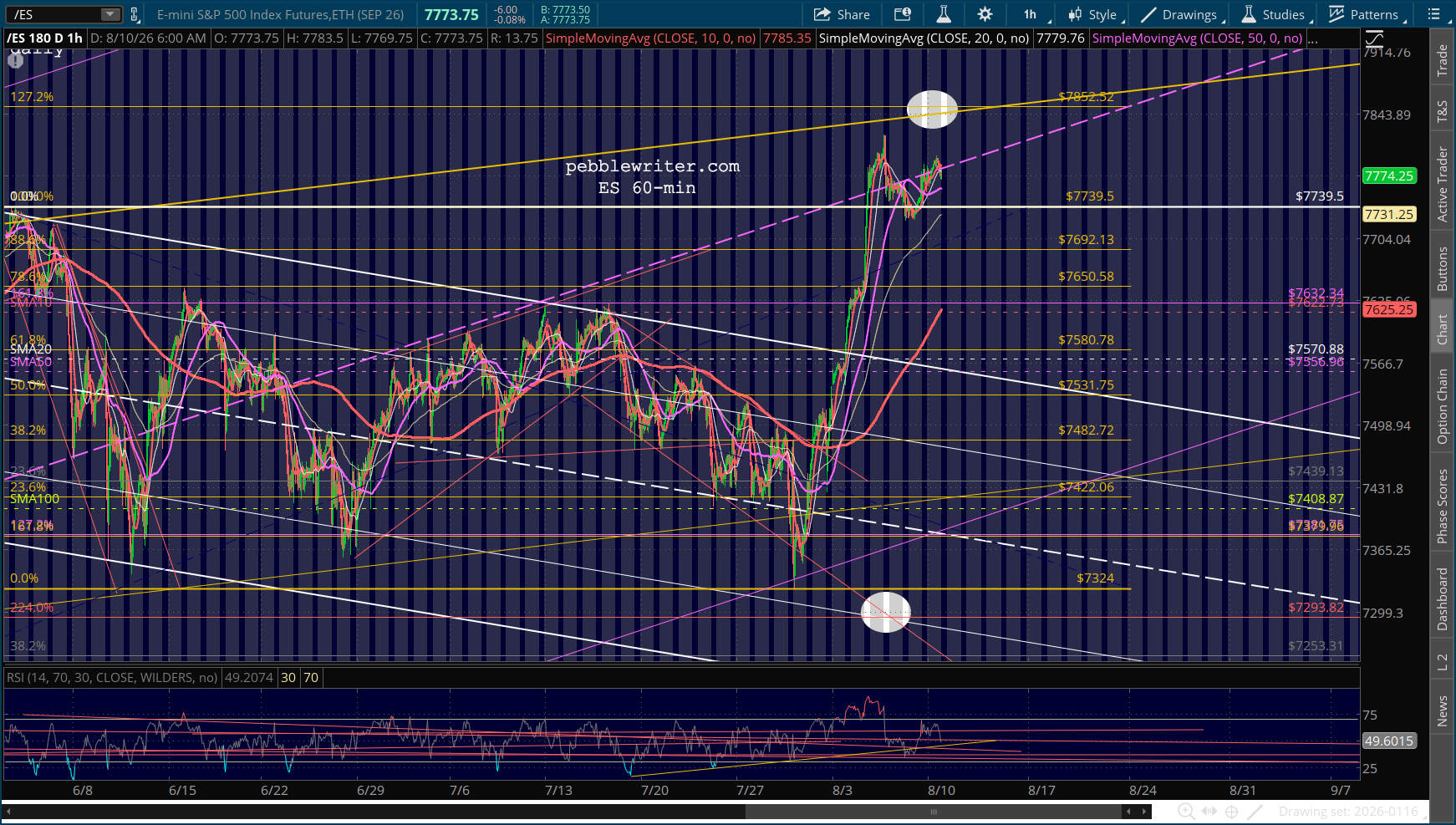

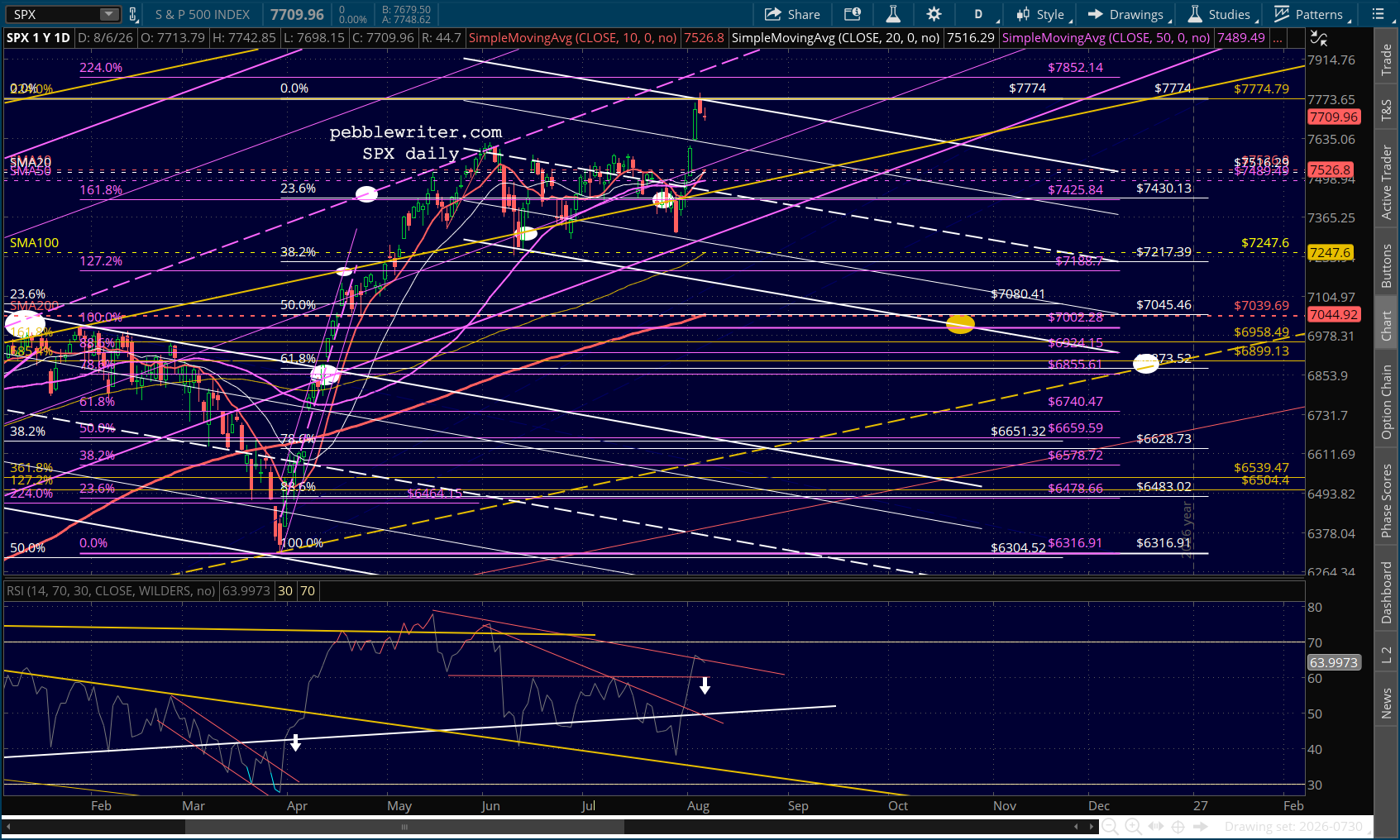

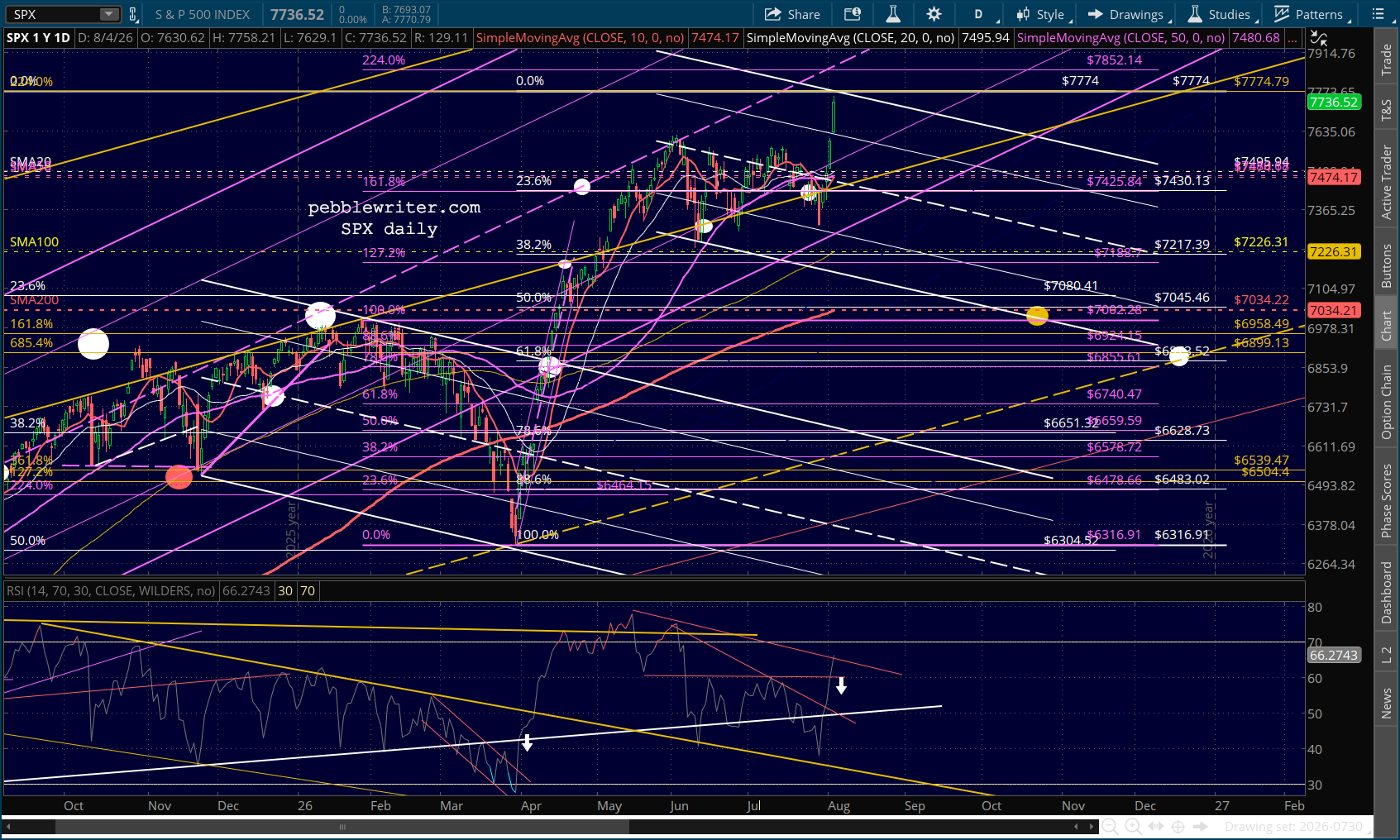

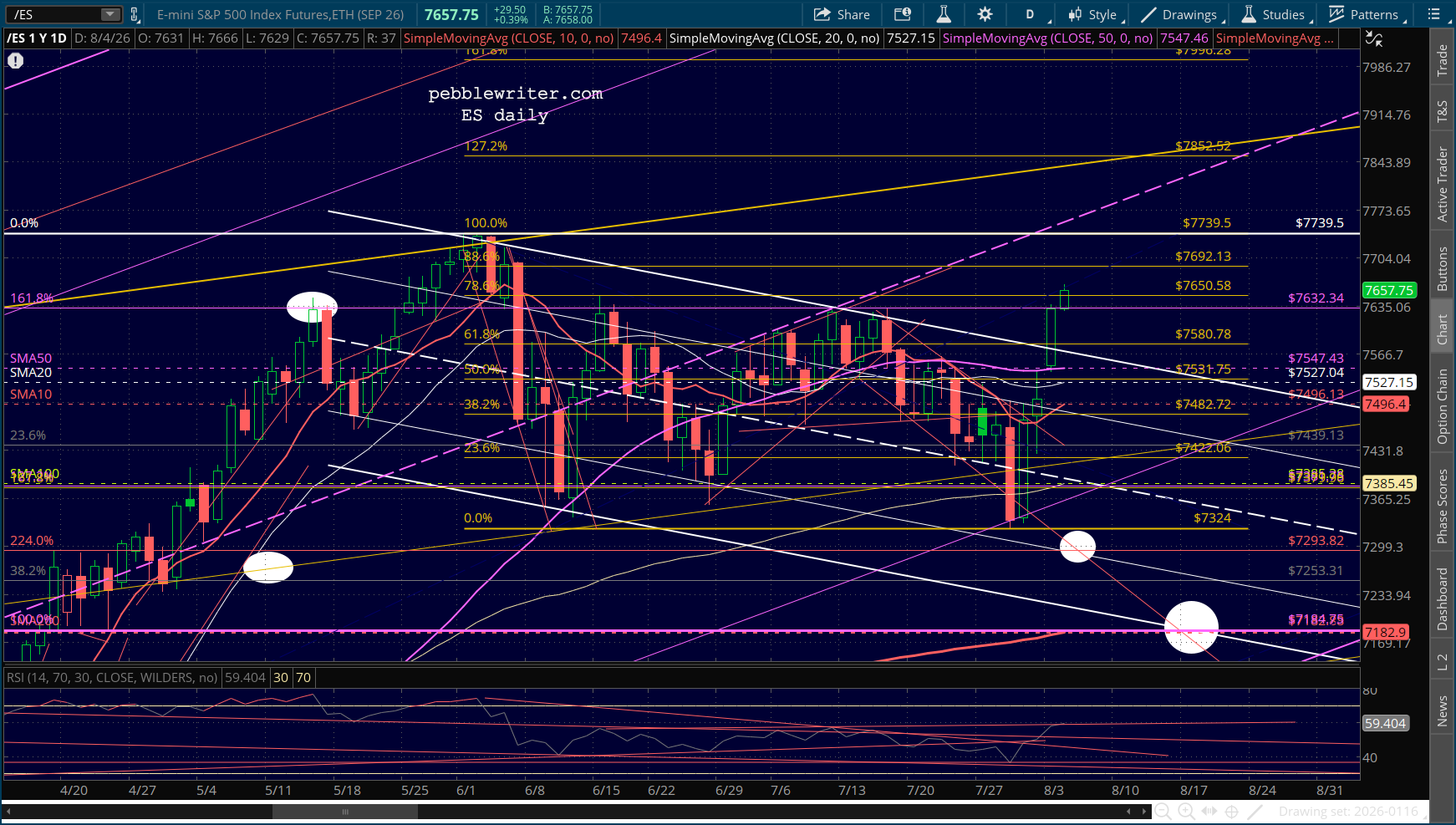

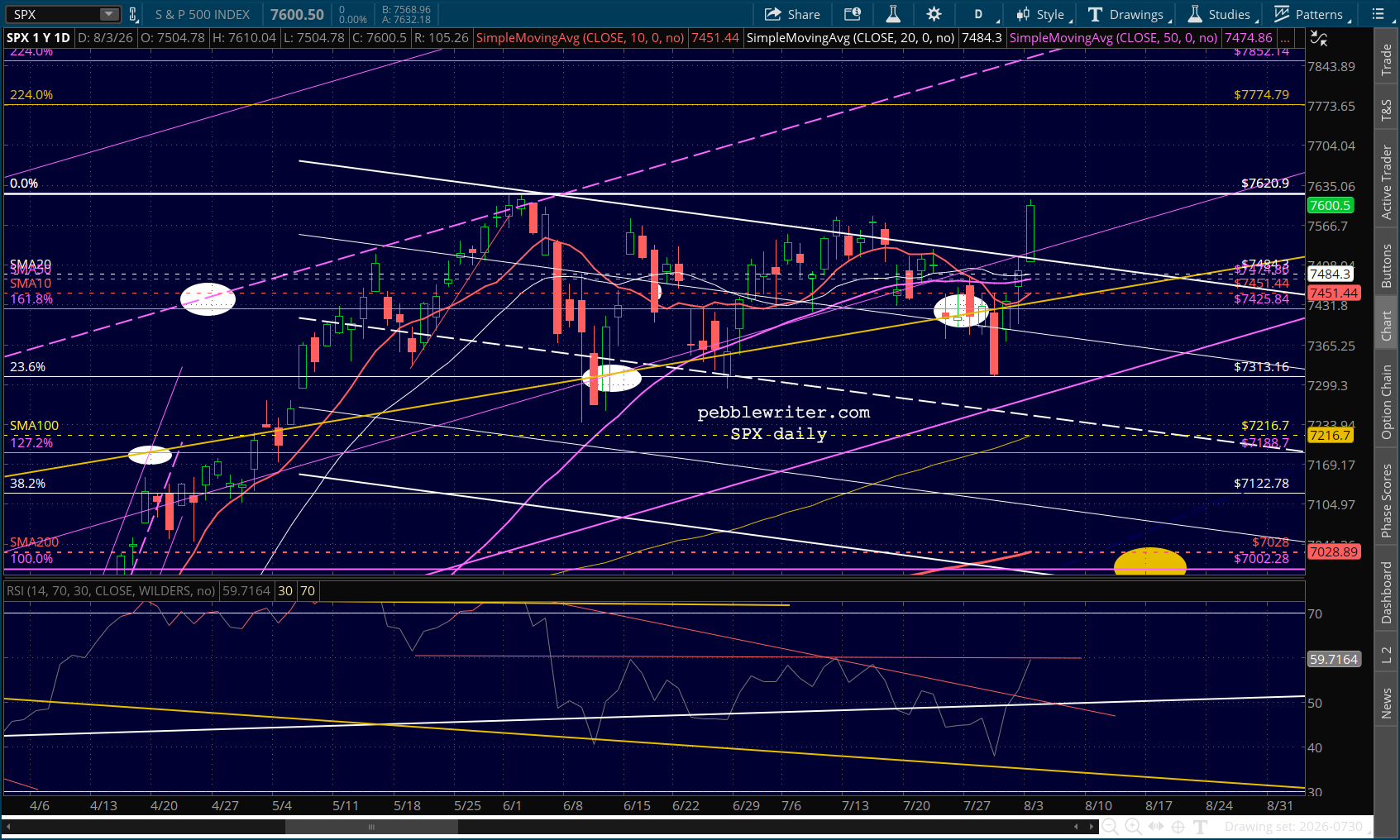

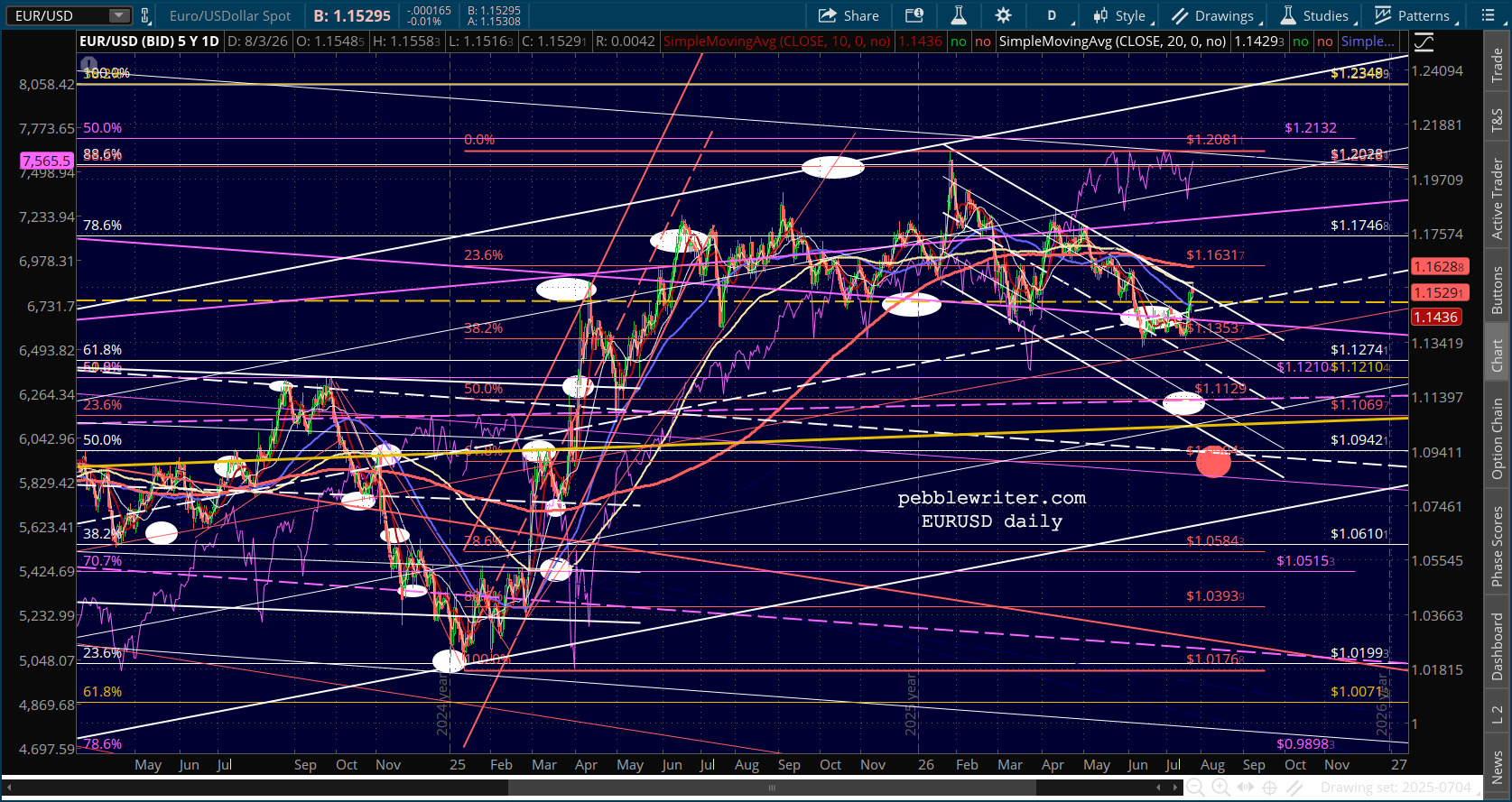

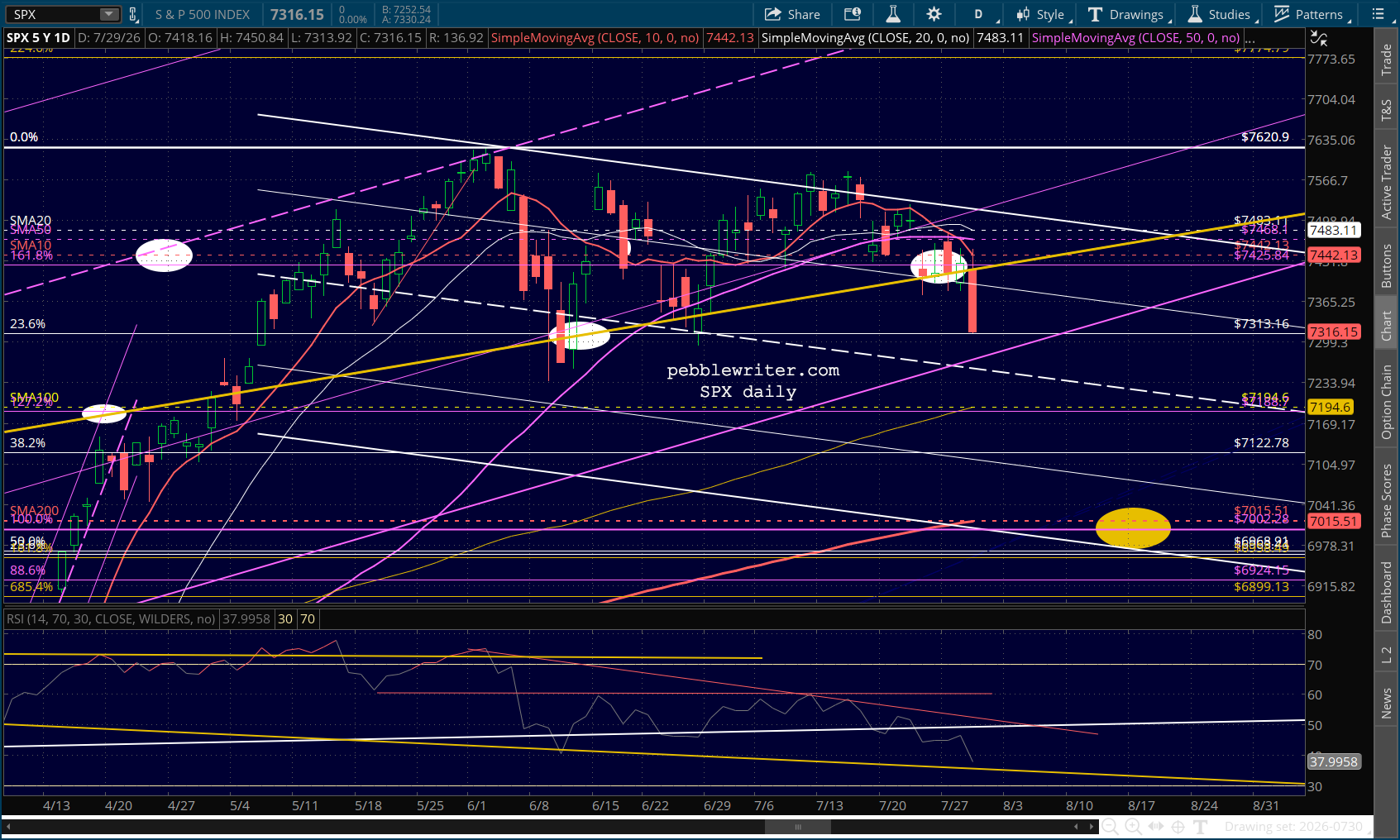

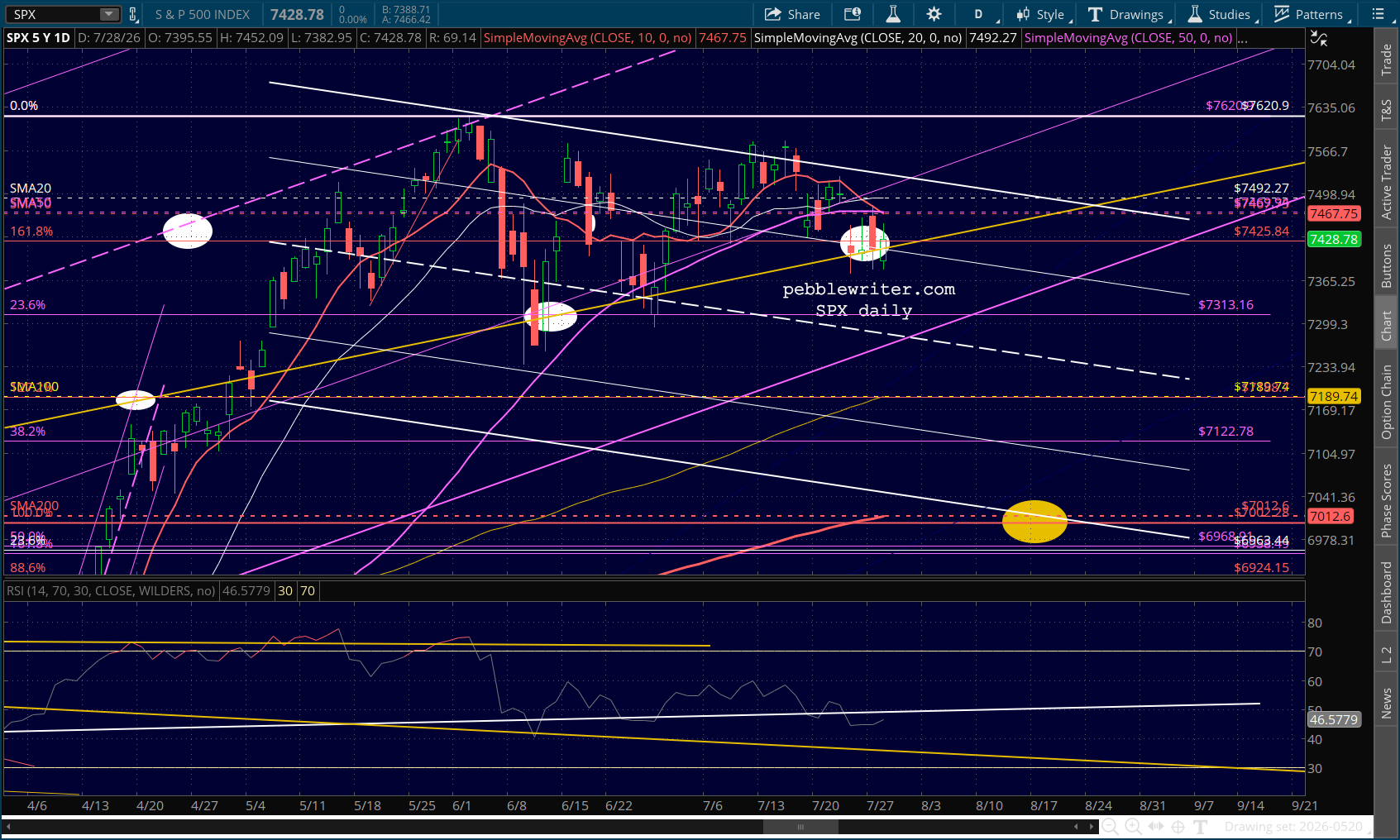

SPX broke out yesterday, driven by a sharp decline in oil prices and in VIX. It landed just shy of the 2.24 Fib extension while exhibiting pretty striking negative divergence. As a result, any disappointment re the supposed “deal” with Iran could result in a sharp pullback.

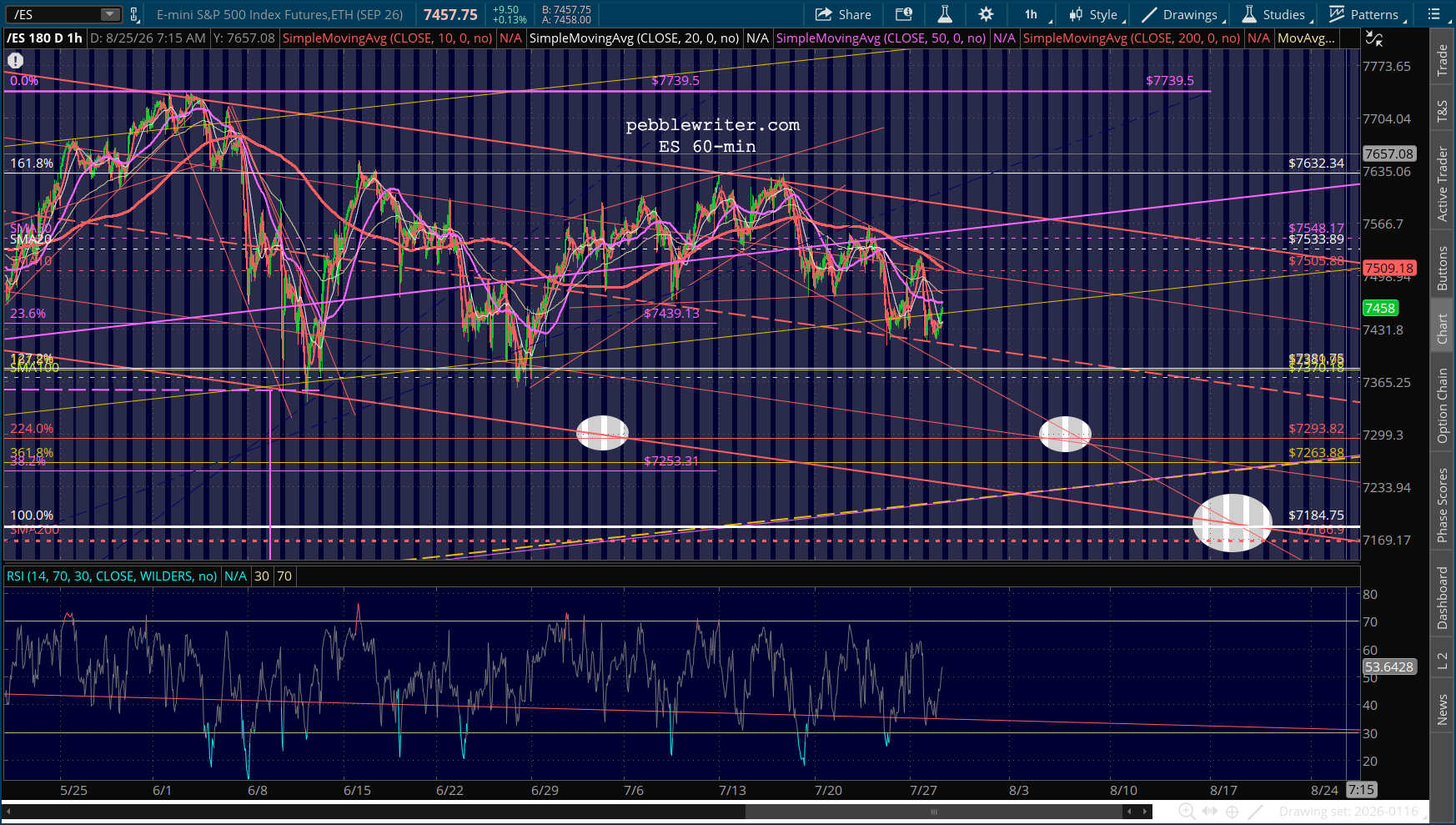

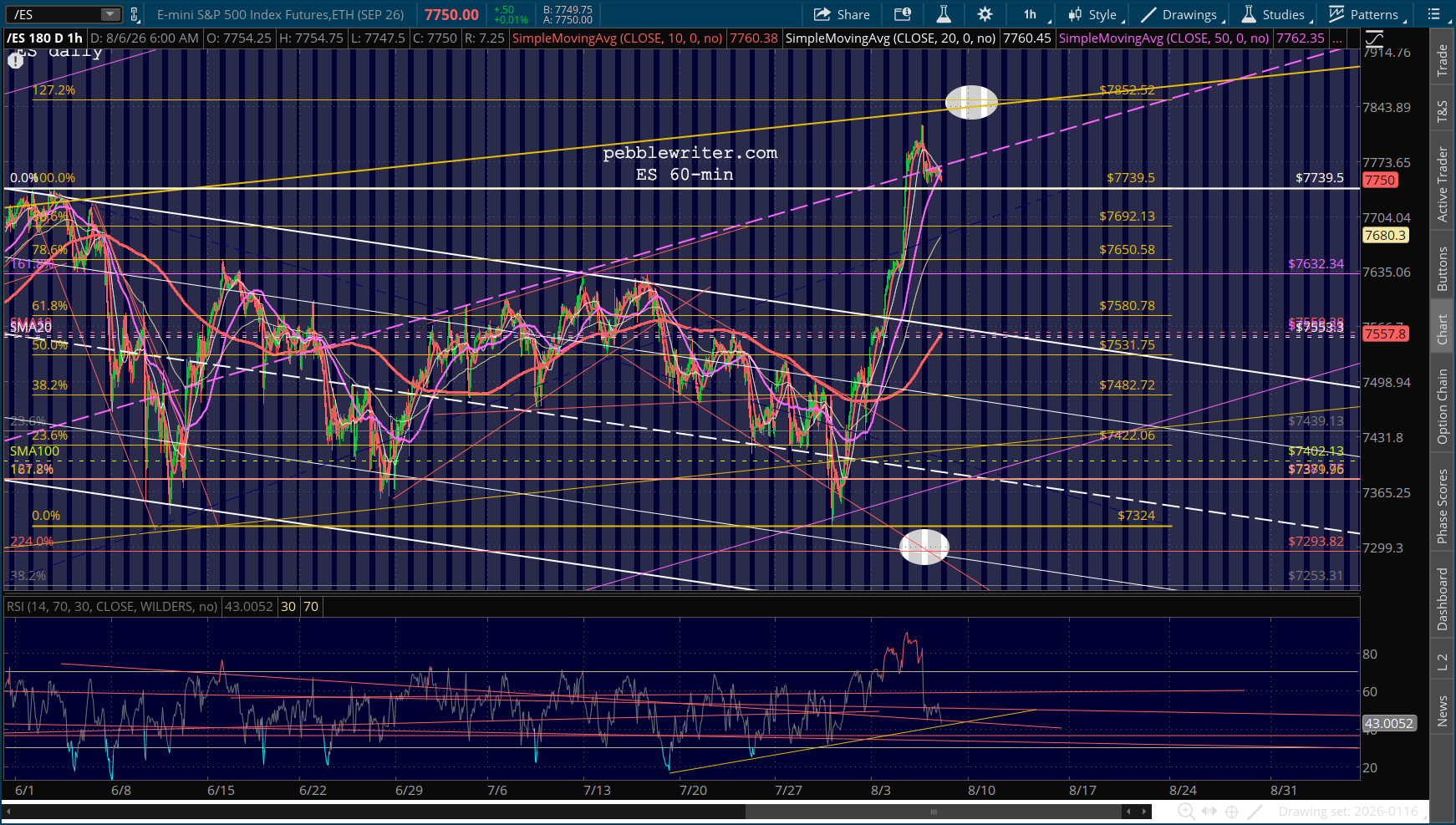

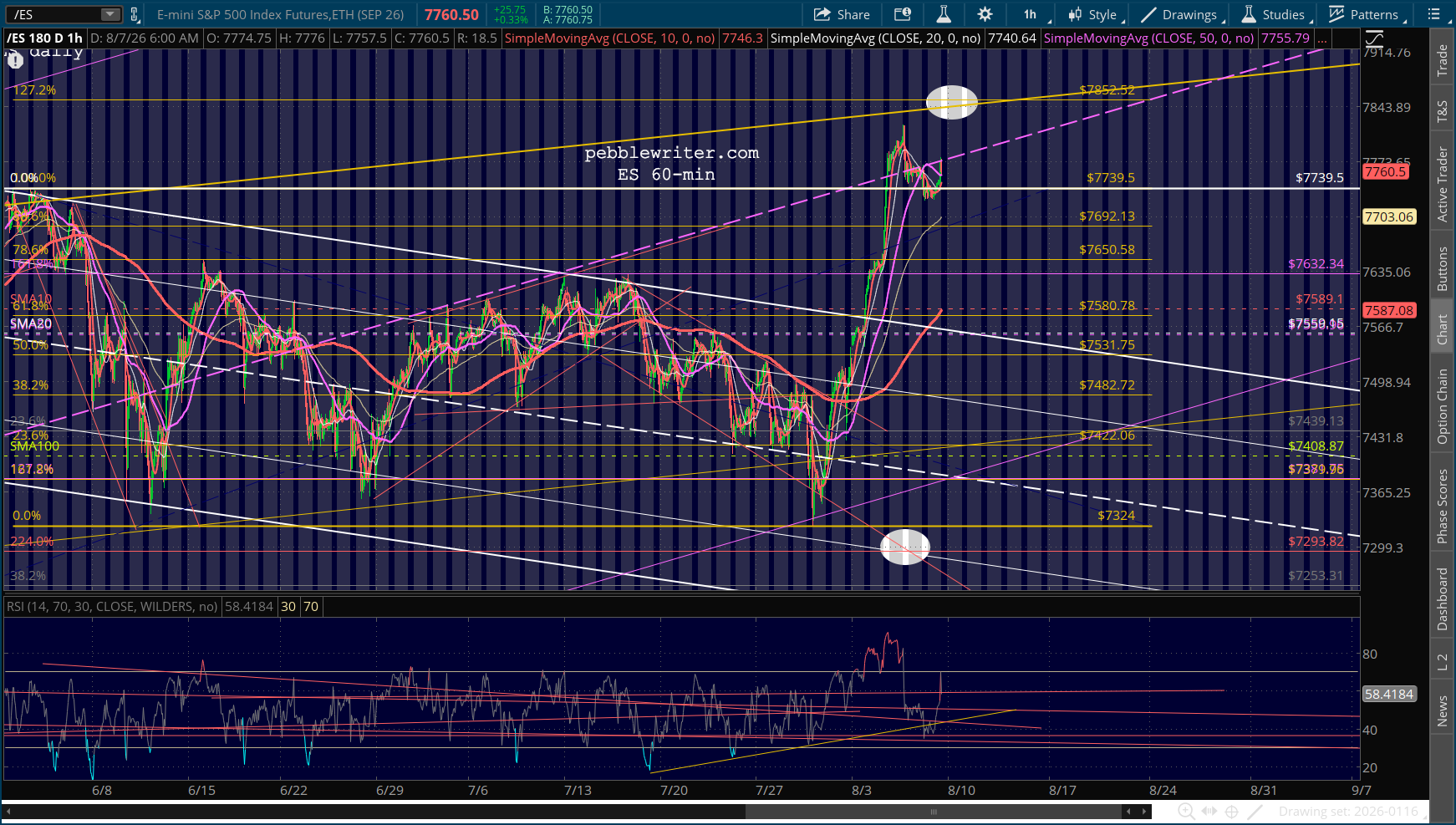

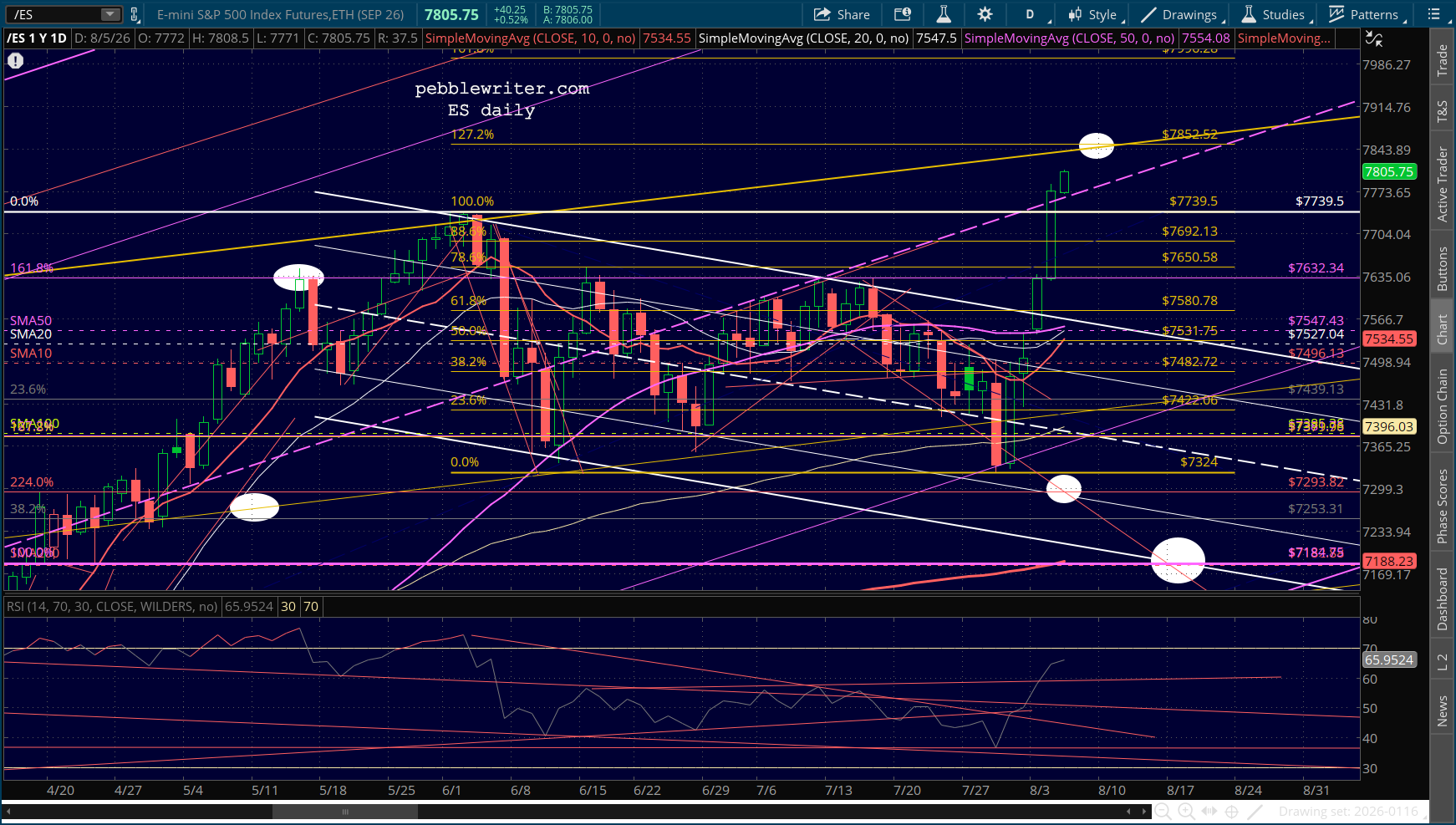

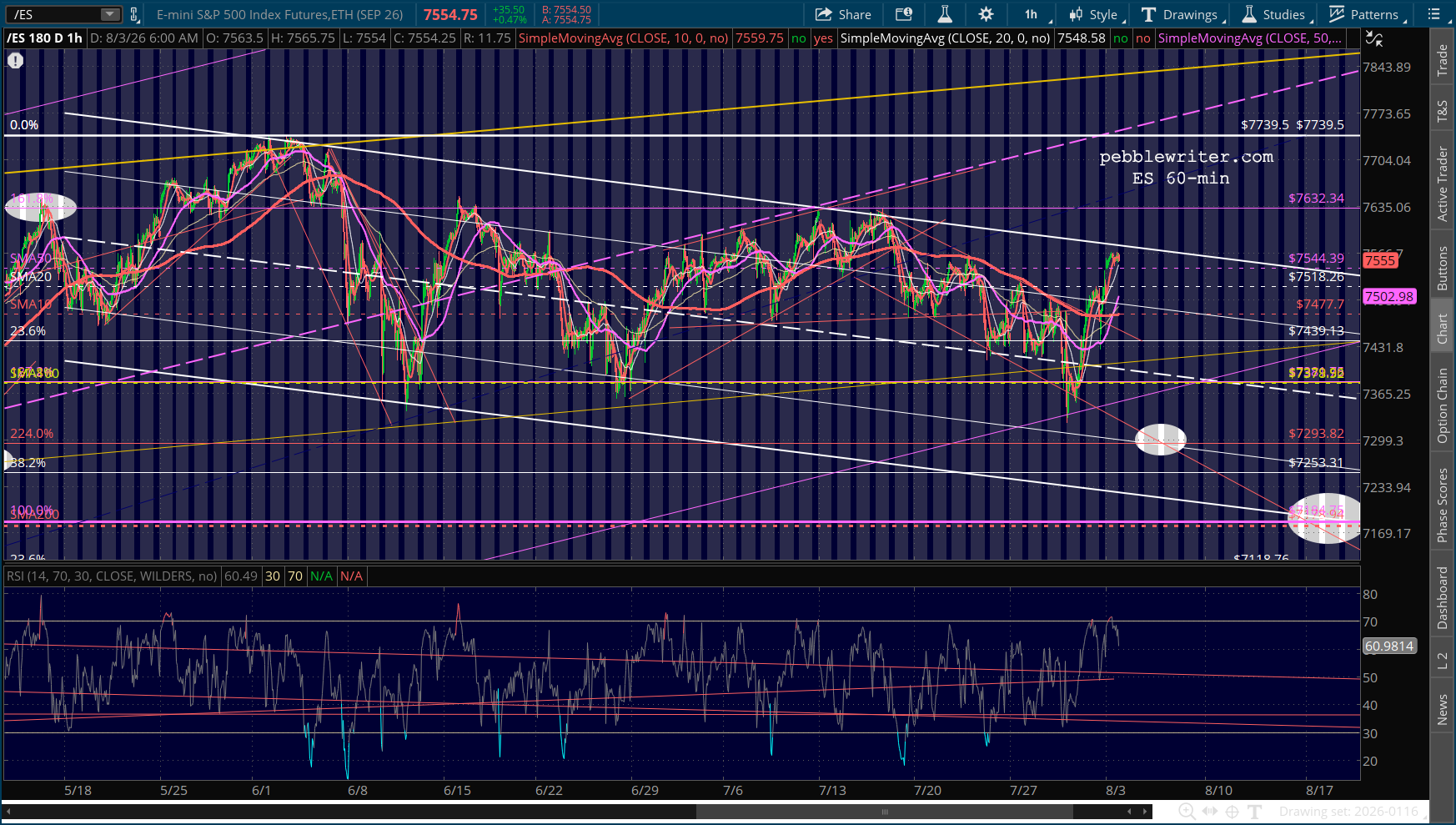

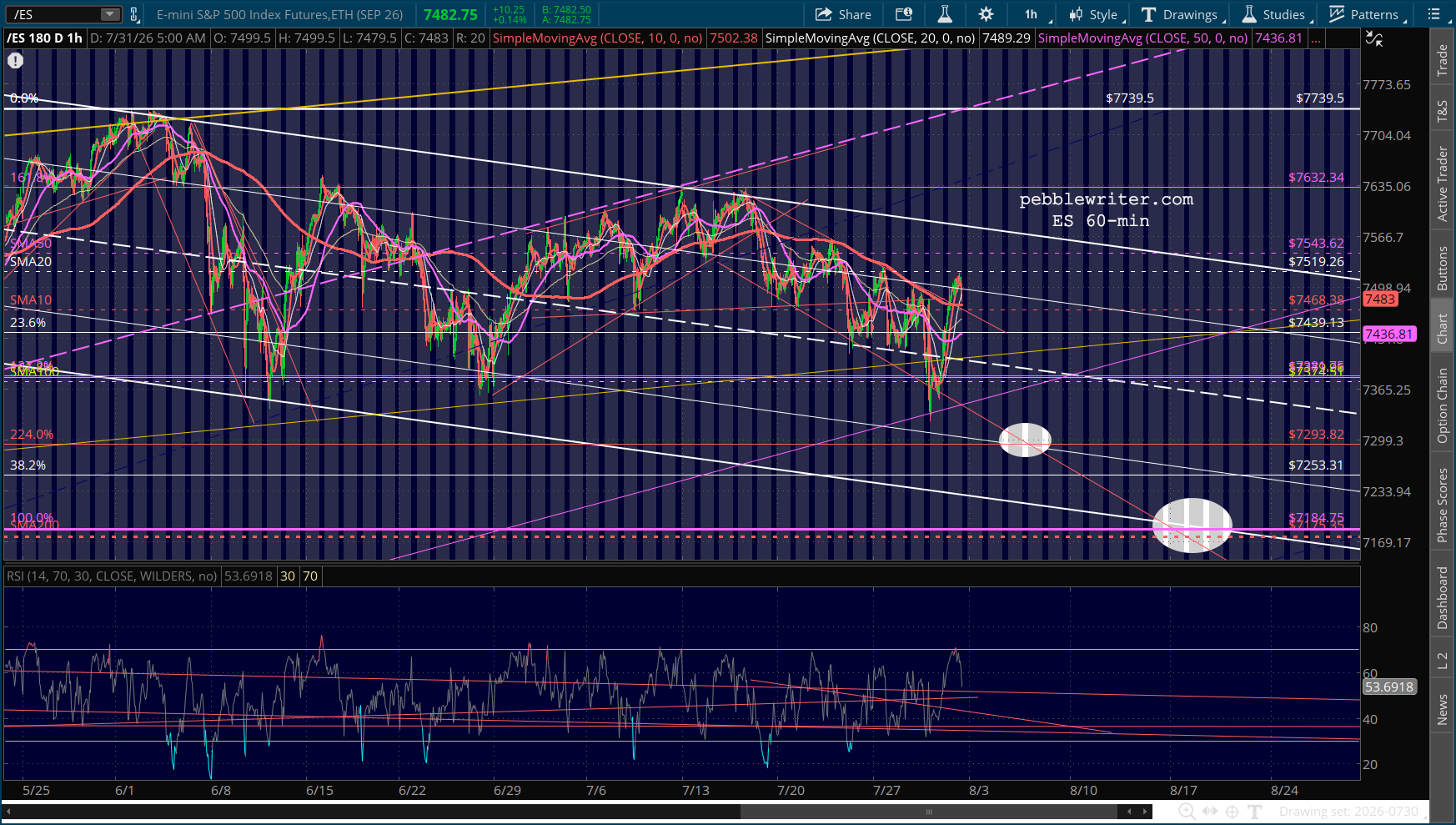

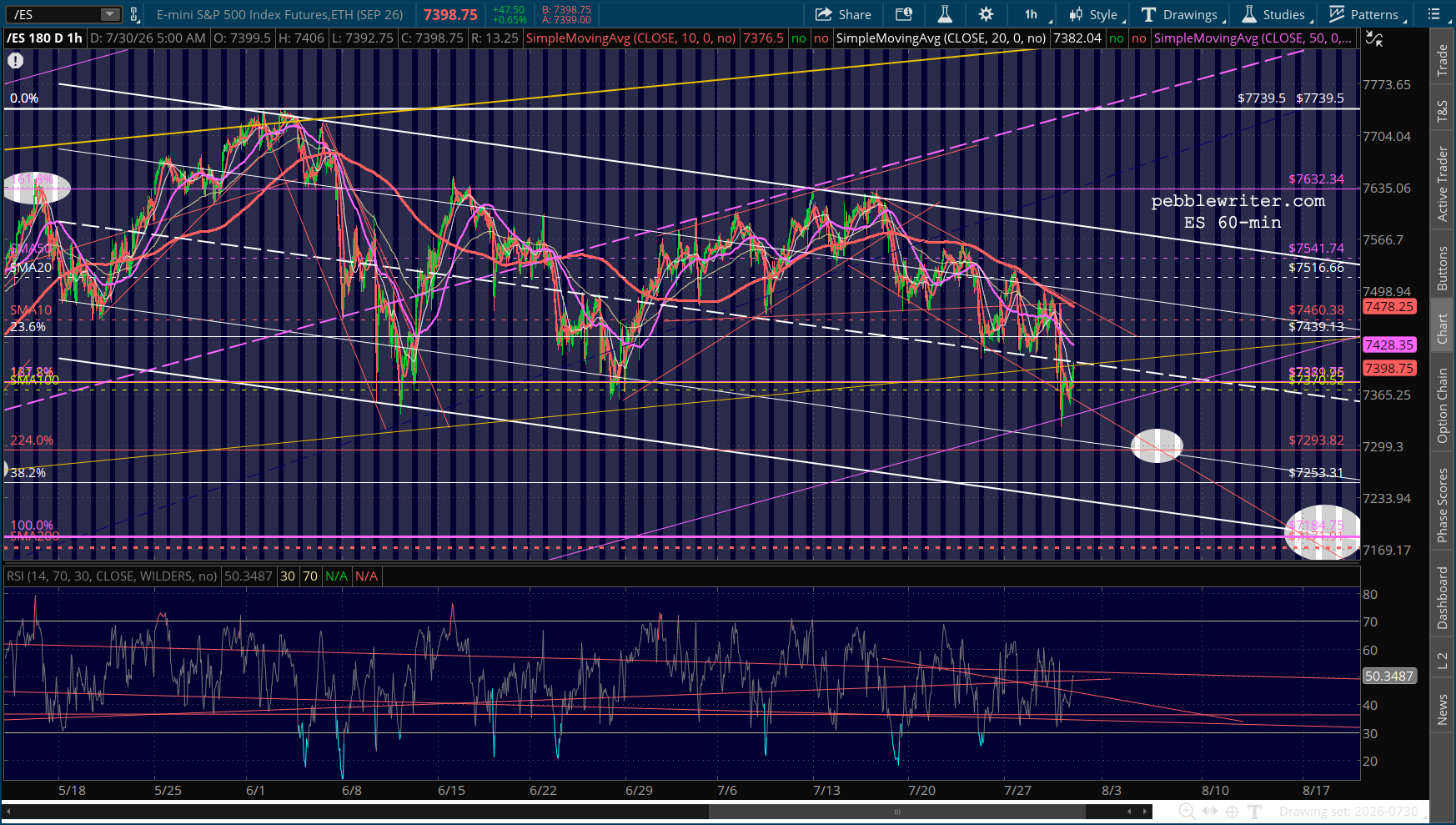

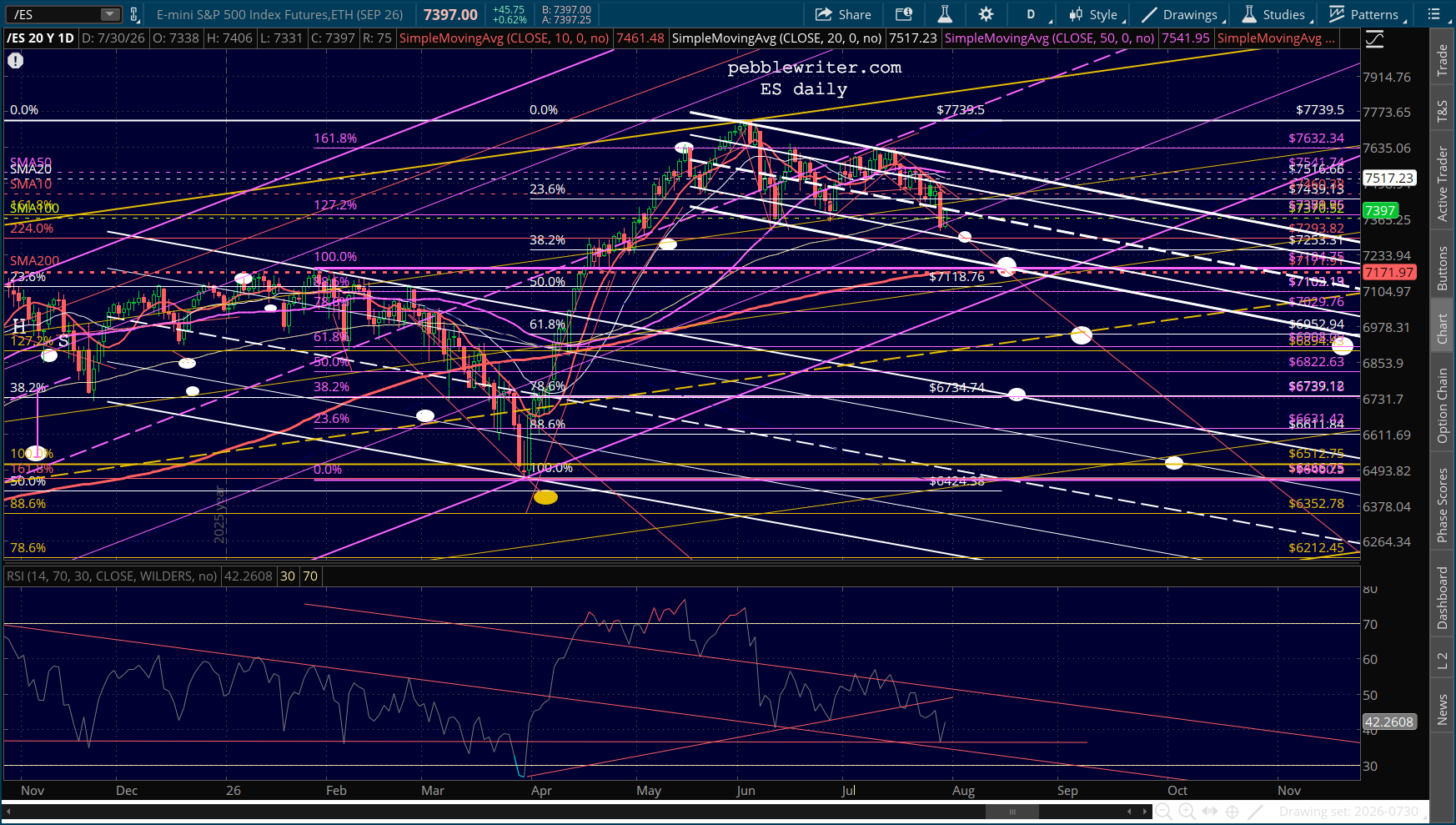

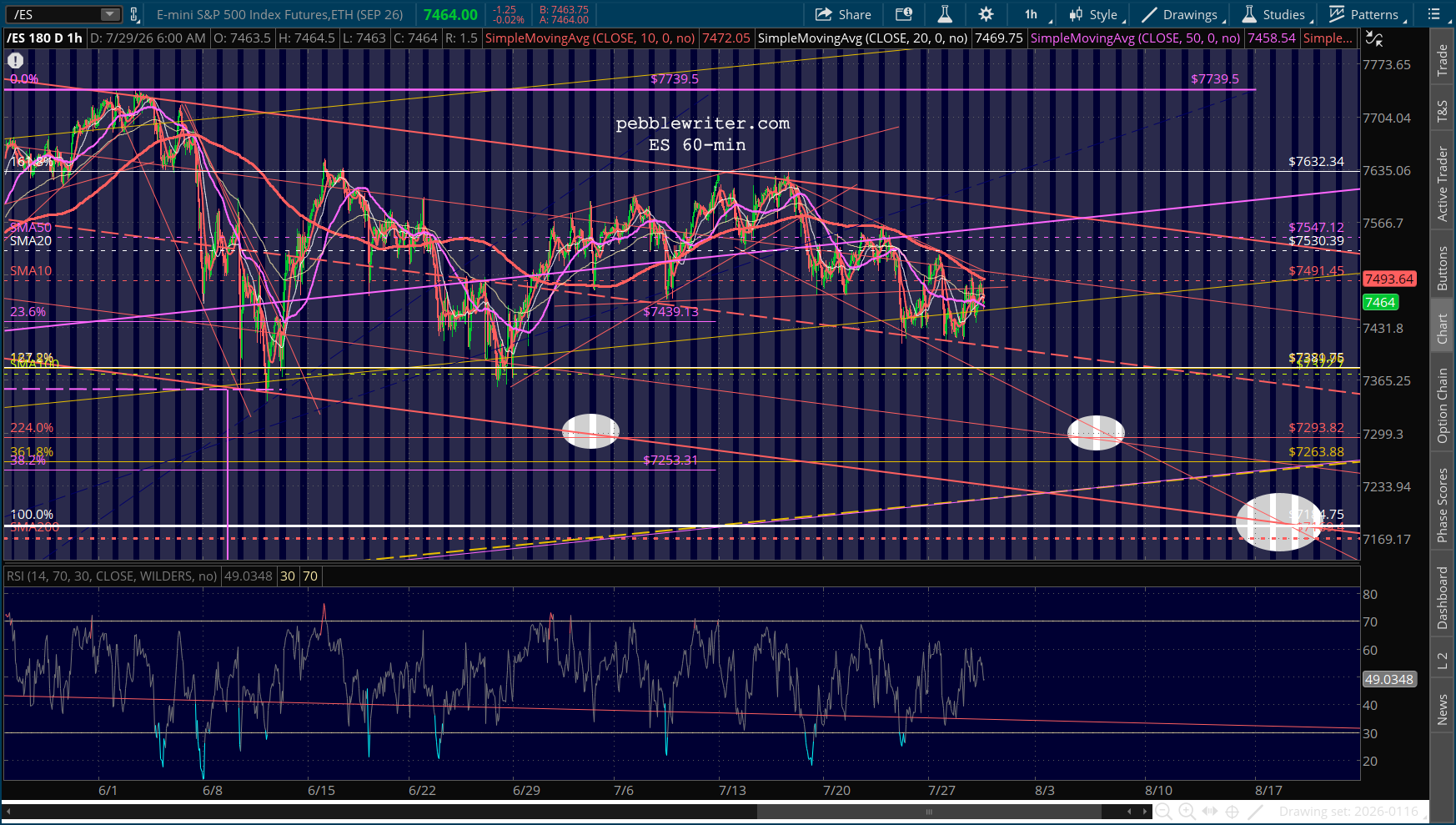

ES, on the other hand, has a ways to go before reaching obvious resistance. Though it is also showing strong negative divergence.

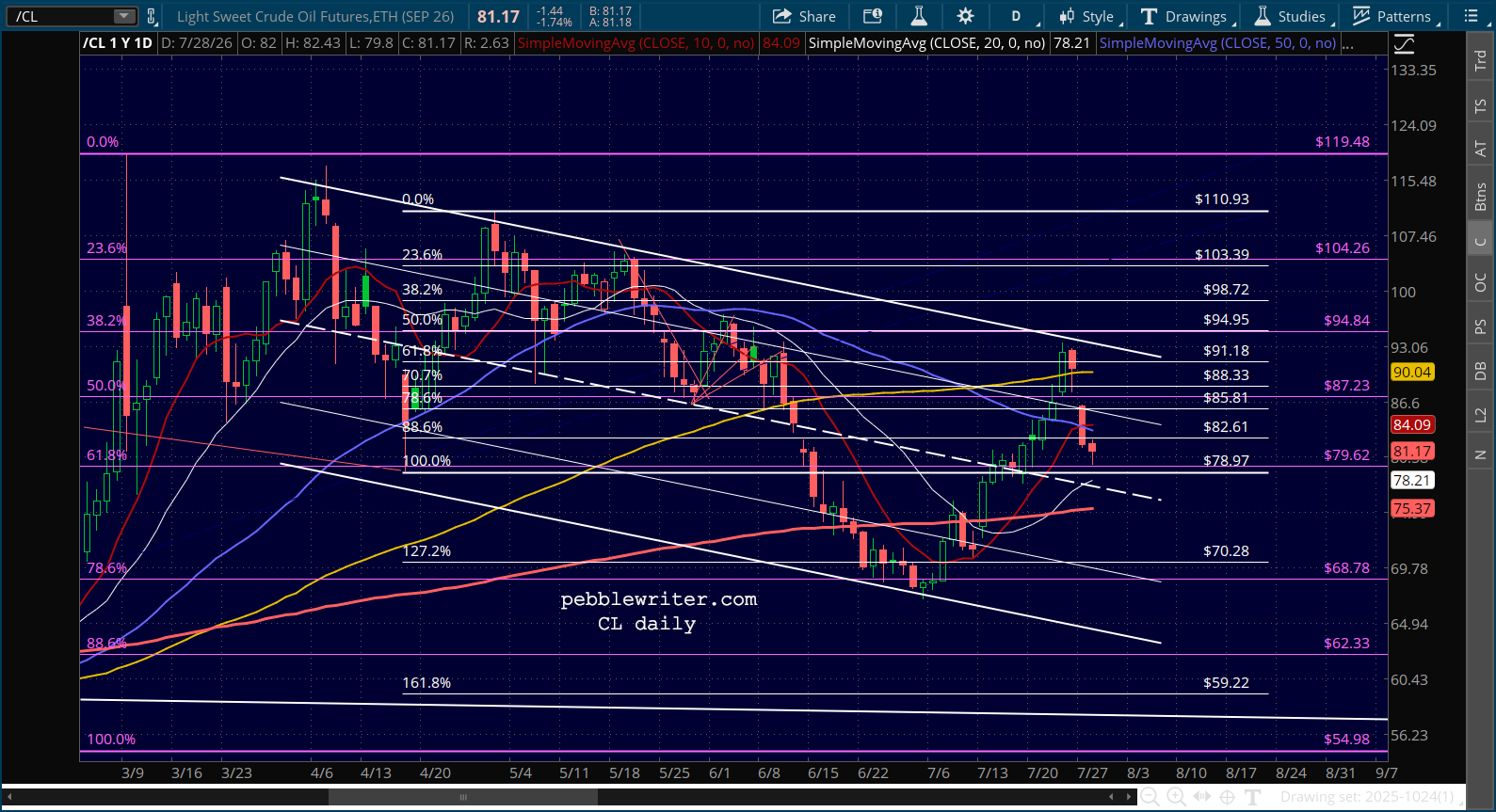

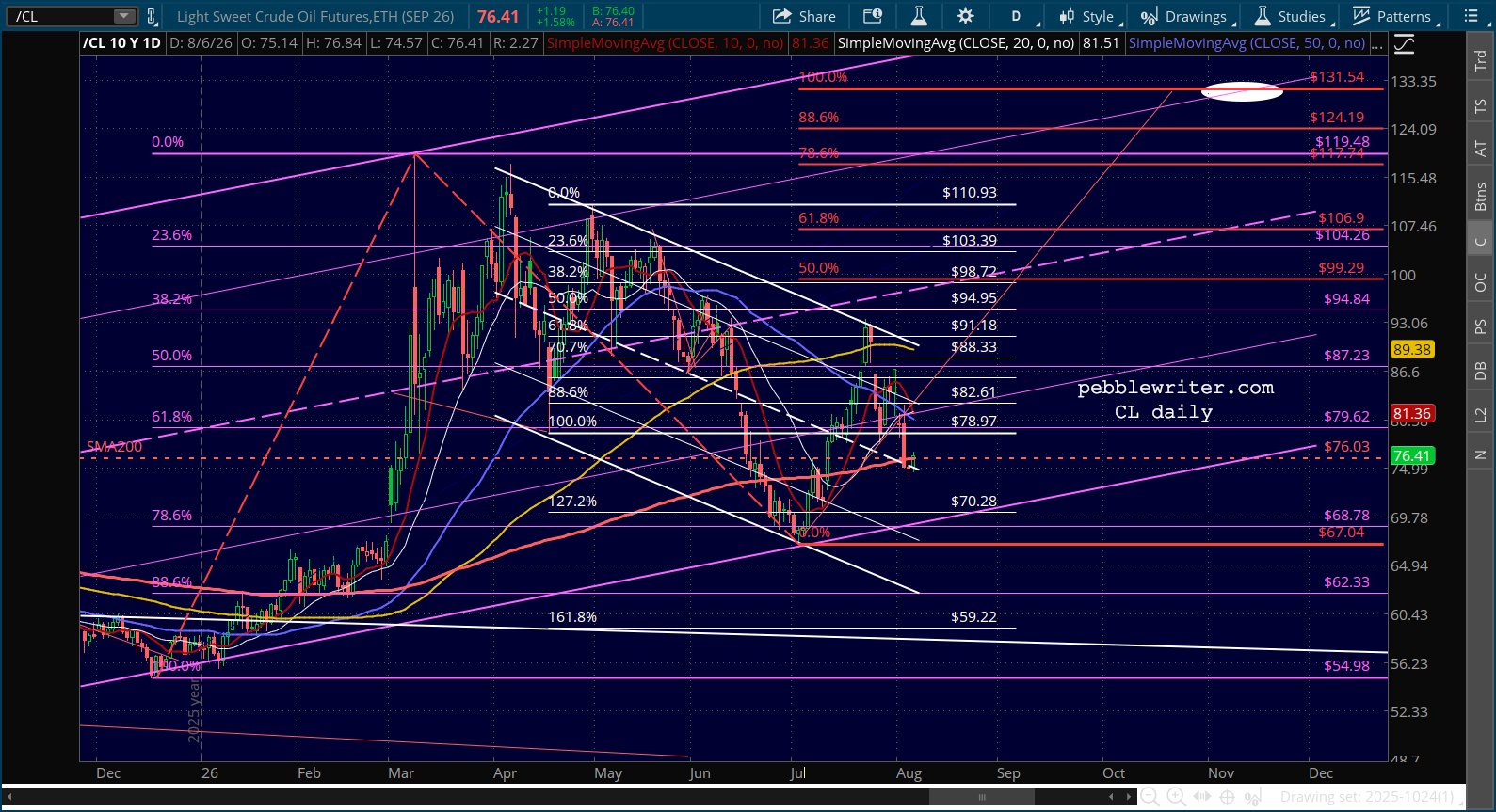

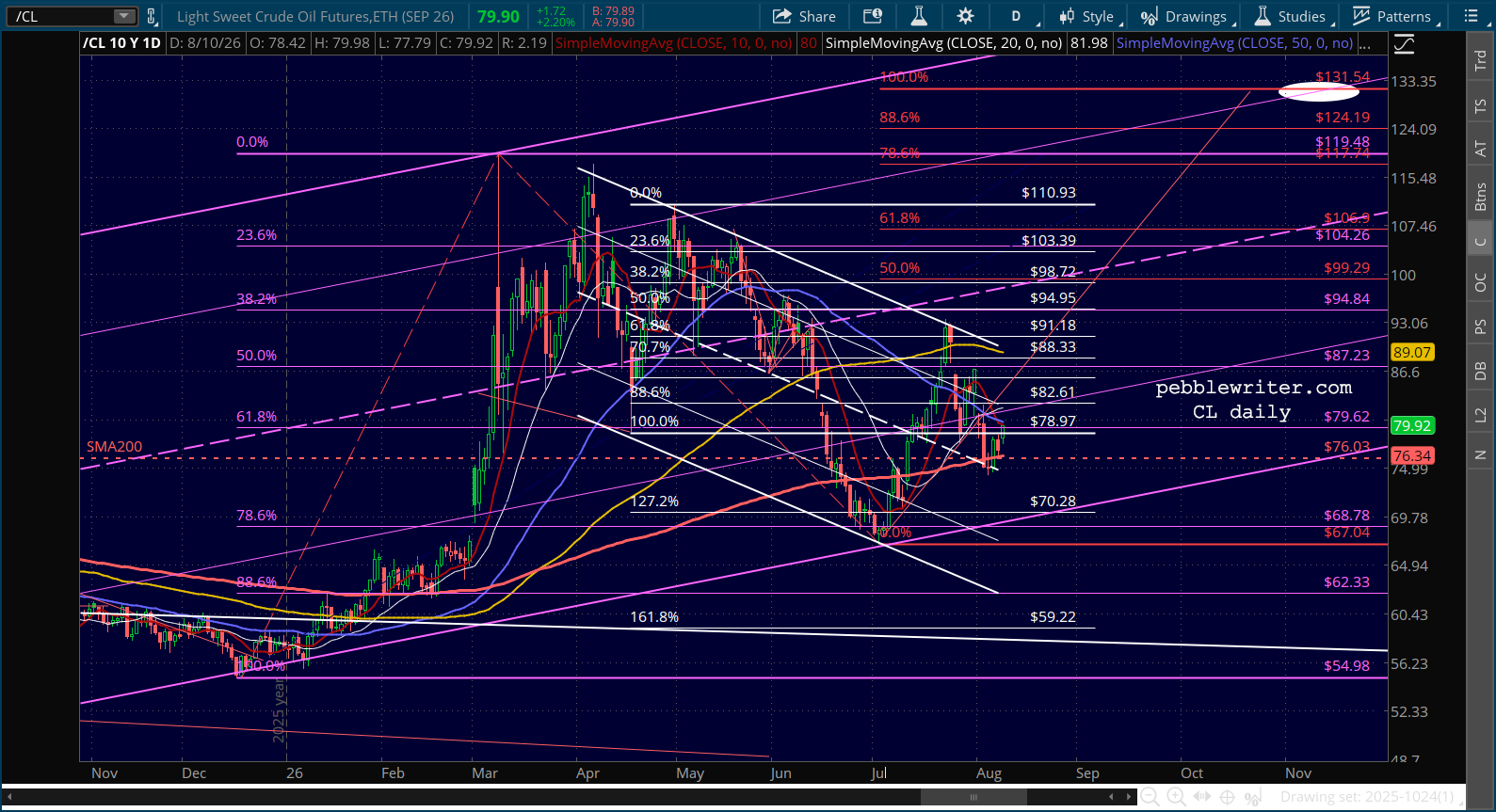

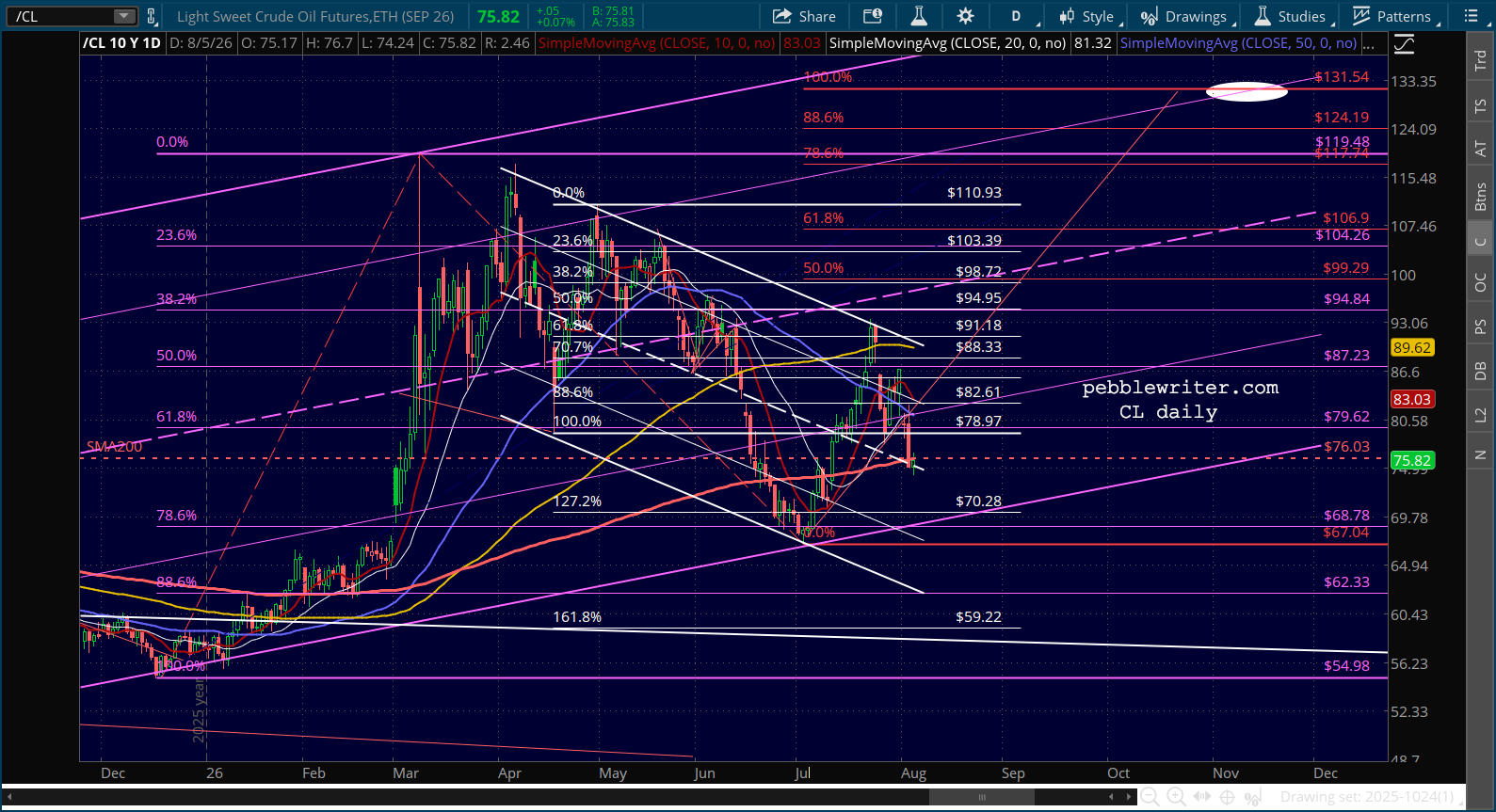

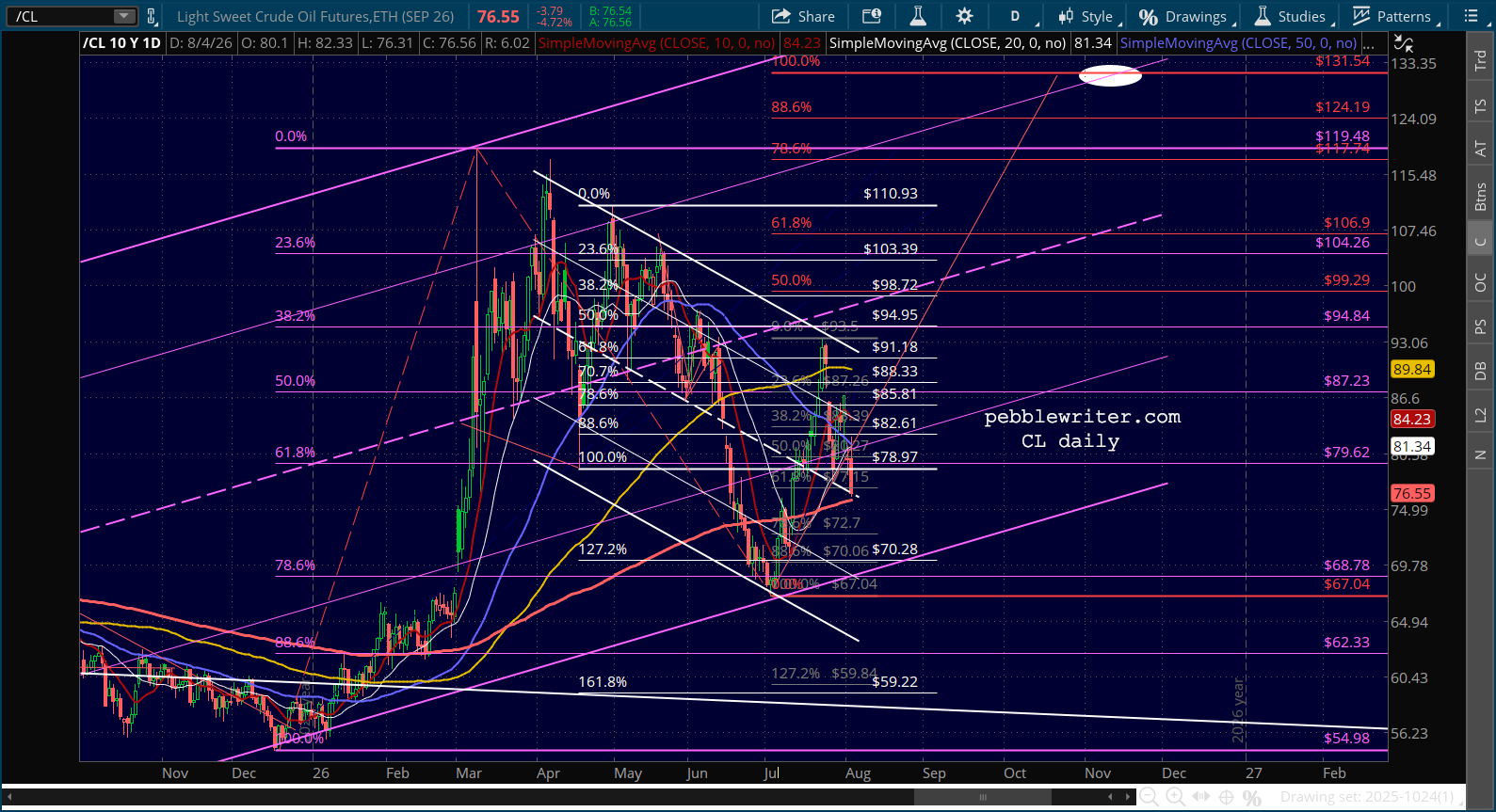

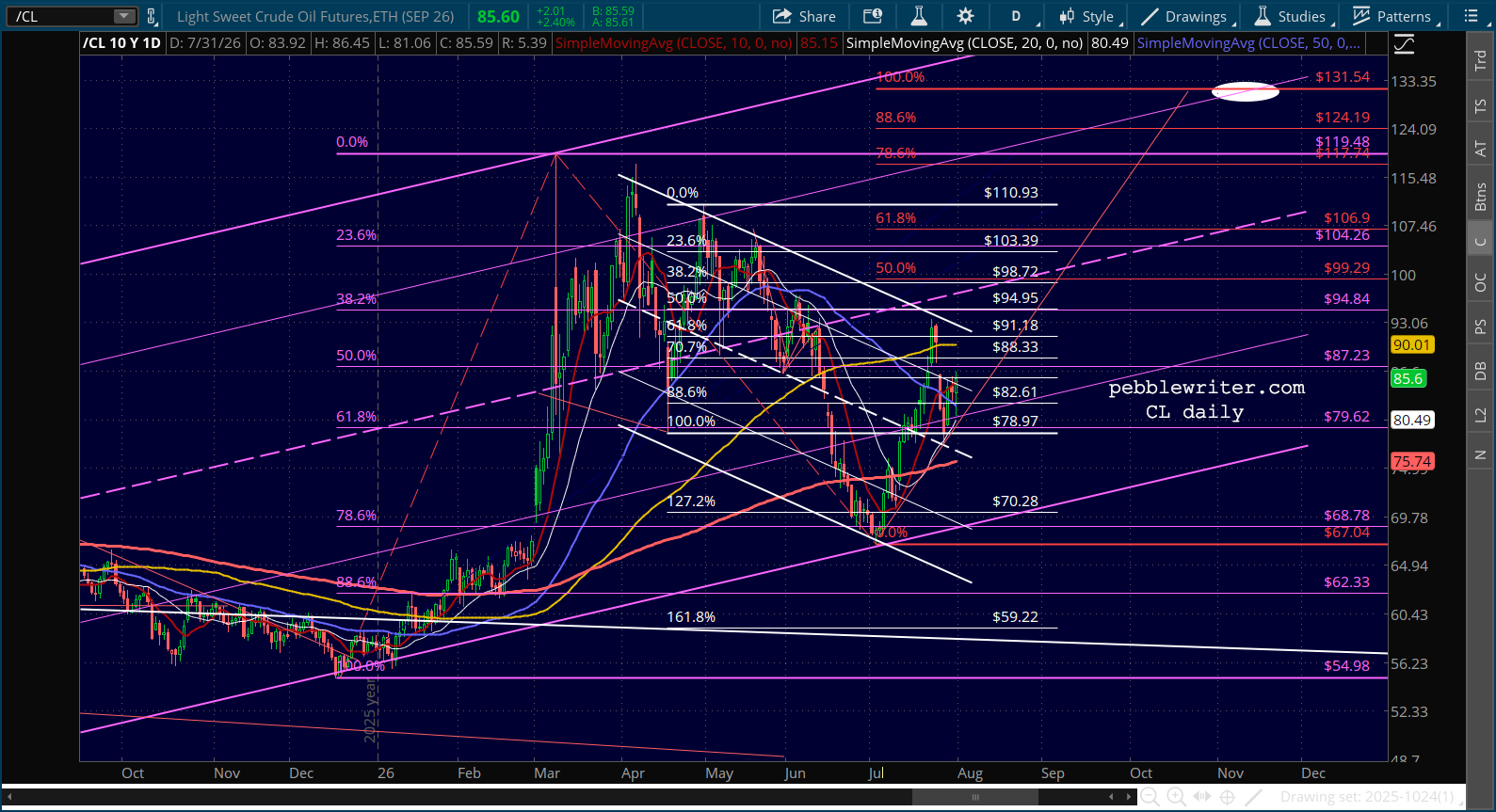

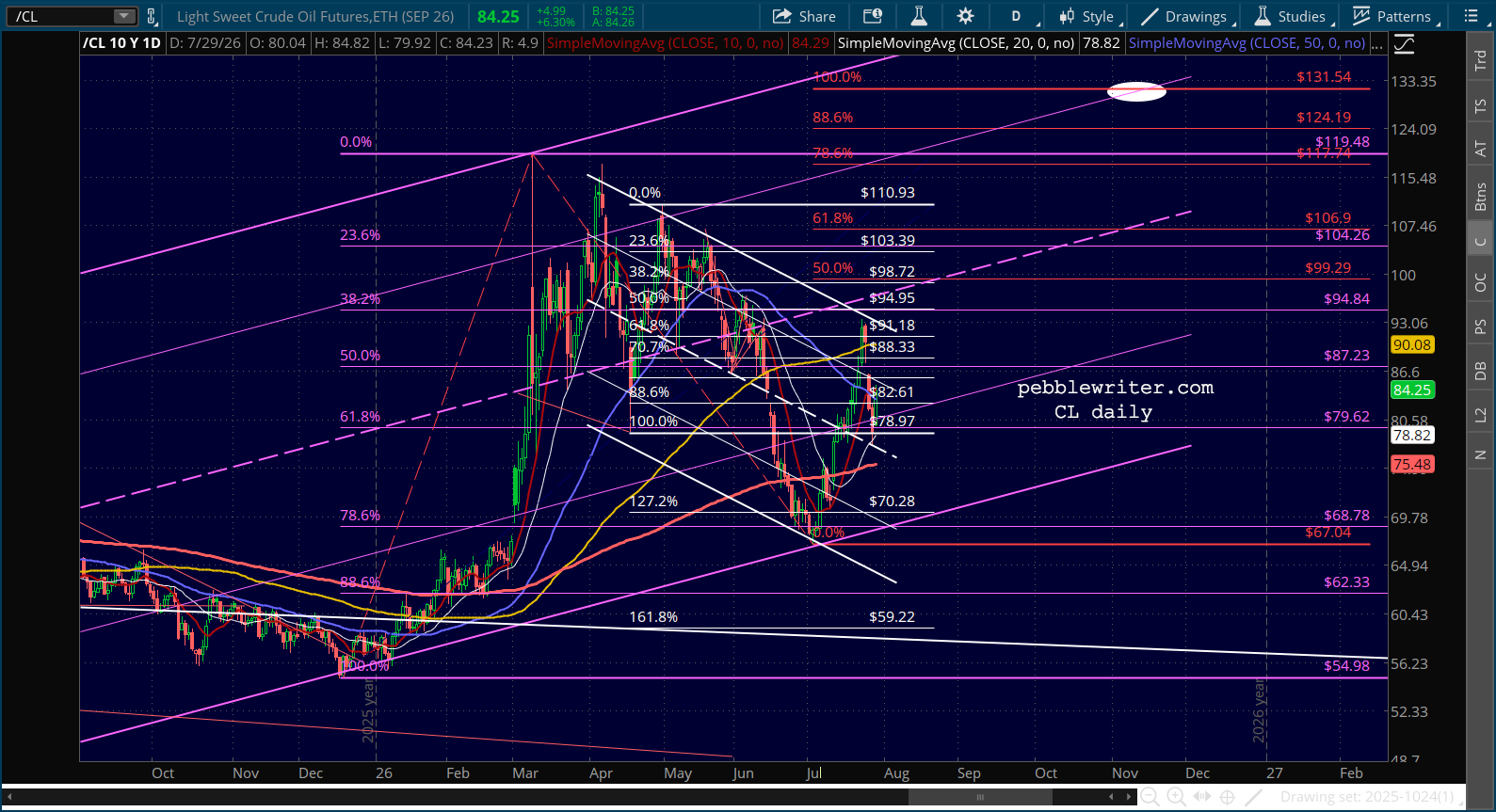

CL appears to be hung up on its SMA200, though this is a tool that the administration has not hesitated to use in the past. The flag pattern is quite clear, suggesting an upside breakout. Again, will the Iranians acquiesce or will they continue to politically punish the Donald? I suspect the latter, though it’s a losing bet at the moment.

Then there’s VIX and the usual games being played with breakdowns of trendlines and the SMA200. FWIW, it’s up over 4% this morning even though ES is up 0.50%.

In watching the financial news this morning, it’s almost impossible to find anyone who’s bearish. This alone is reason to be cautious.

Stay tuned.

Futures are in a position to put SPX at new highs, even as ES itself is still a a little over 1% shy.

We have new lows on VIX – no surprise.

But, the potential trap for equity traders is that CL’s significant drop — thanks entirely to Trump’s and Bessent’s jawboning — is running into a channel midline AND SMA200. It is fairly likely to bounce here, which would put those new equity highs at risk.

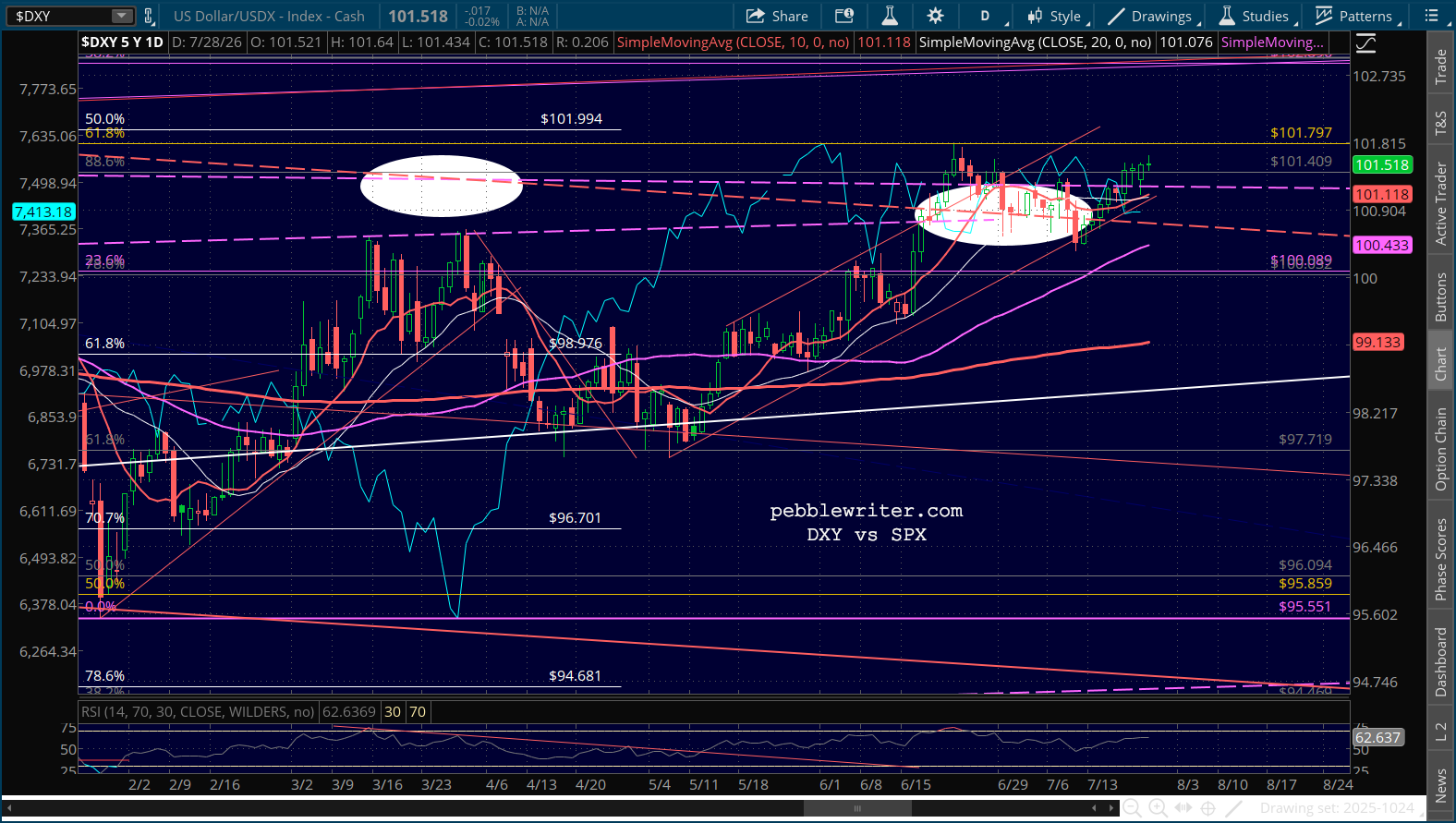

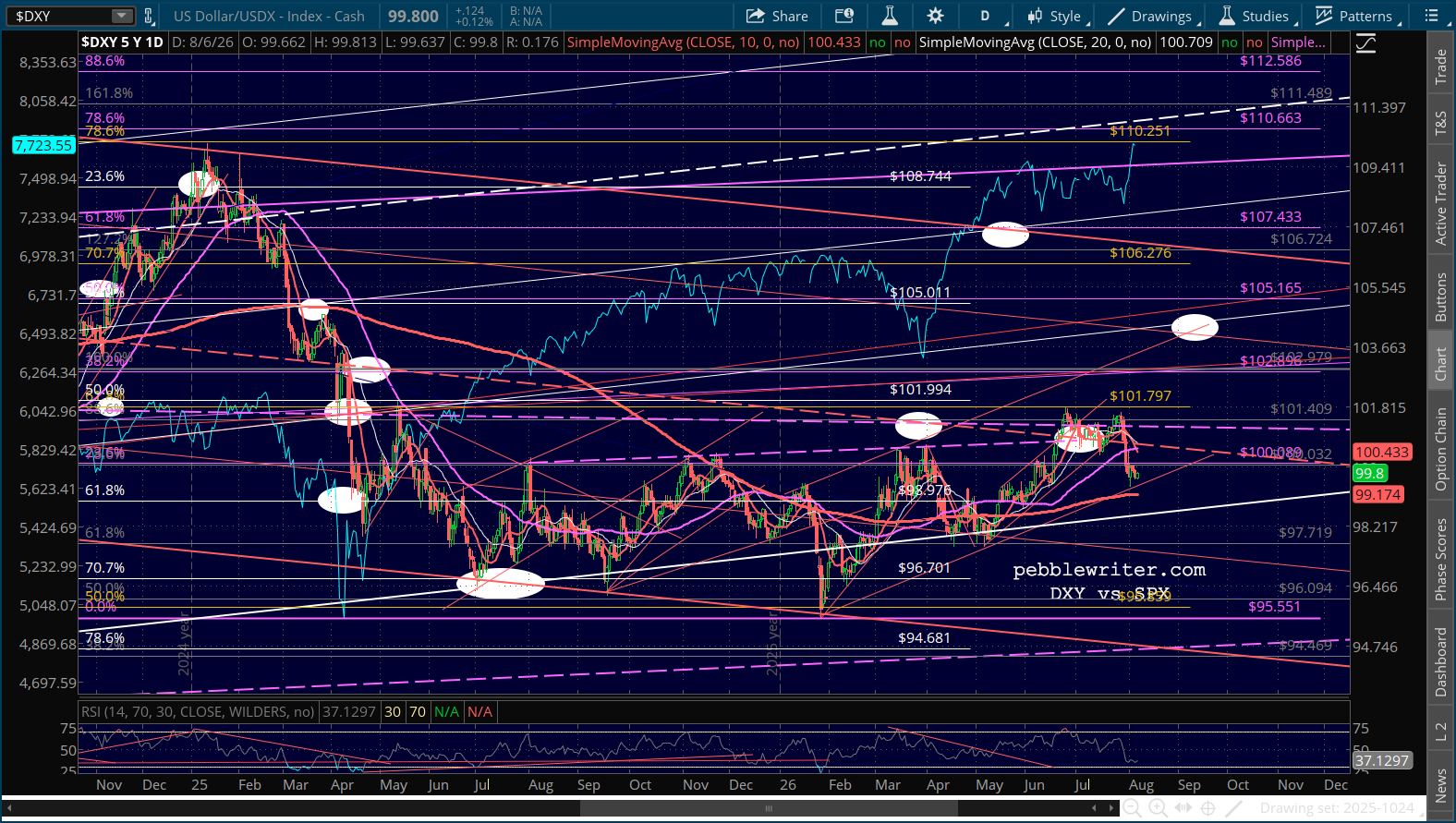

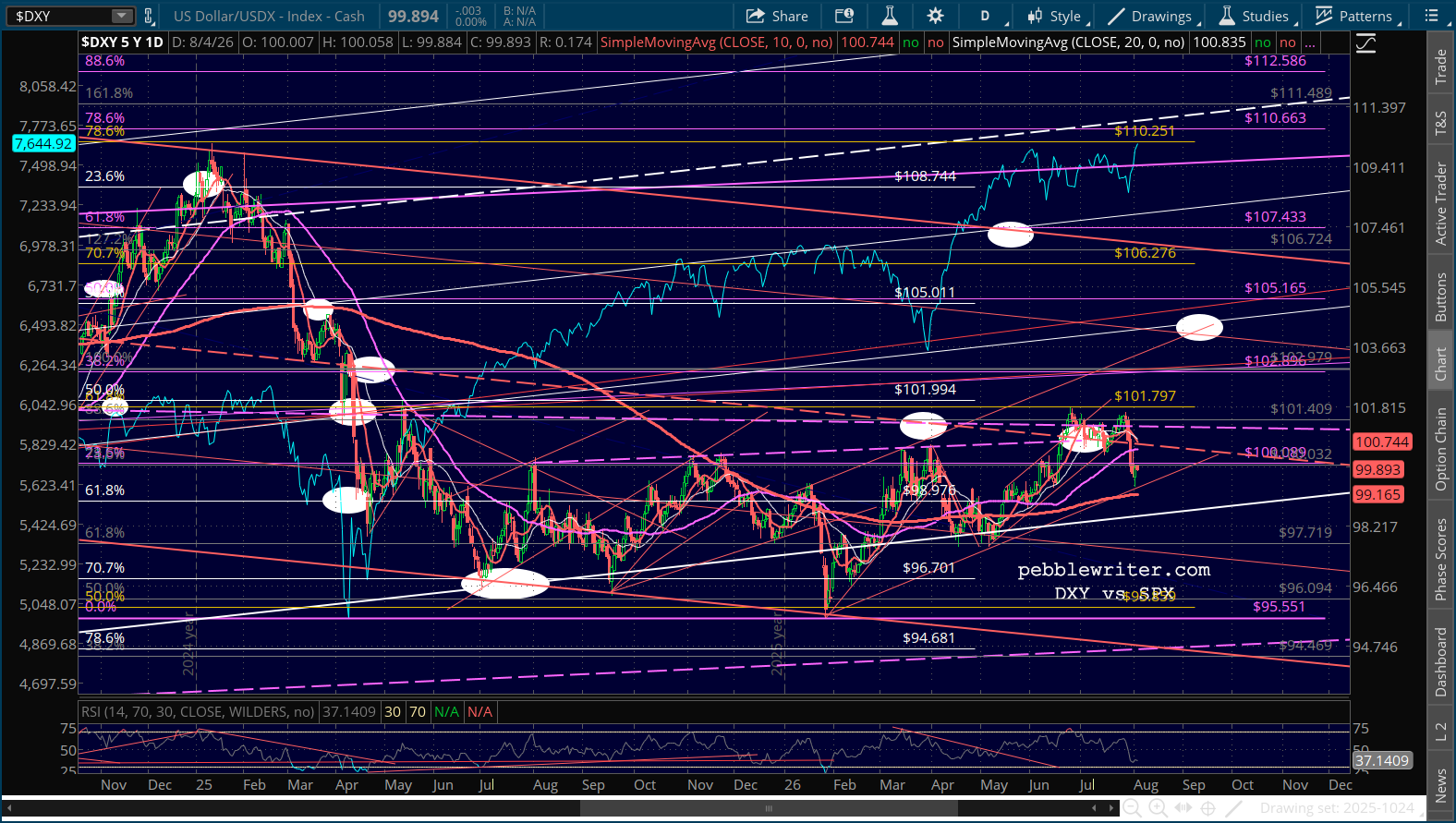

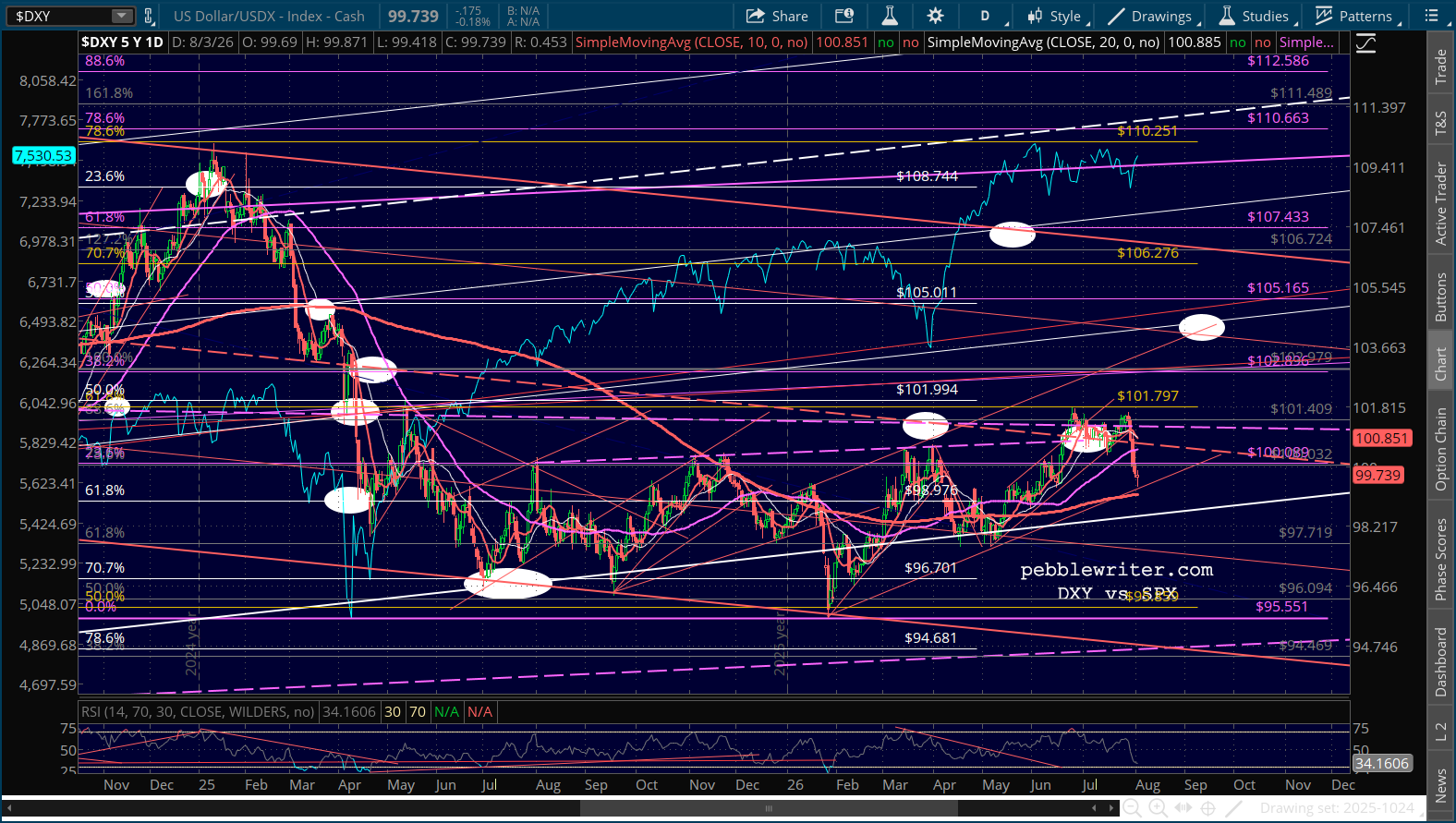

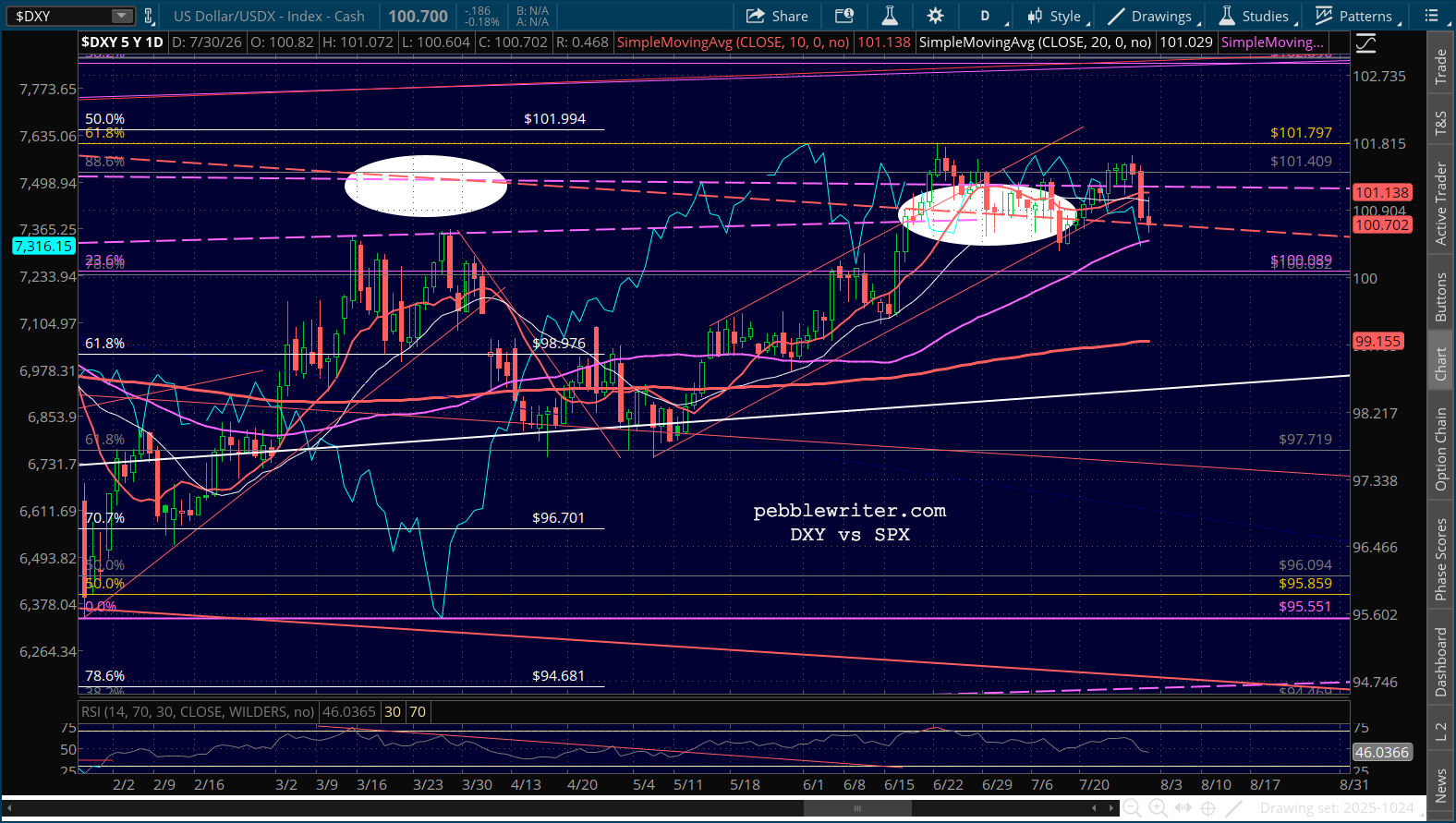

And, DXY is only slightly above strong support.

All of these issues could be allayed by more of the same kind of manipulation that got stocks to where they are. But, the risk is real, and will remain so until we get a bullish 10/20 cross.

Stay tuned.

Moment of truth, thanks to another unsupported social media declaration…

…that sent CL tumbling by over 6%.

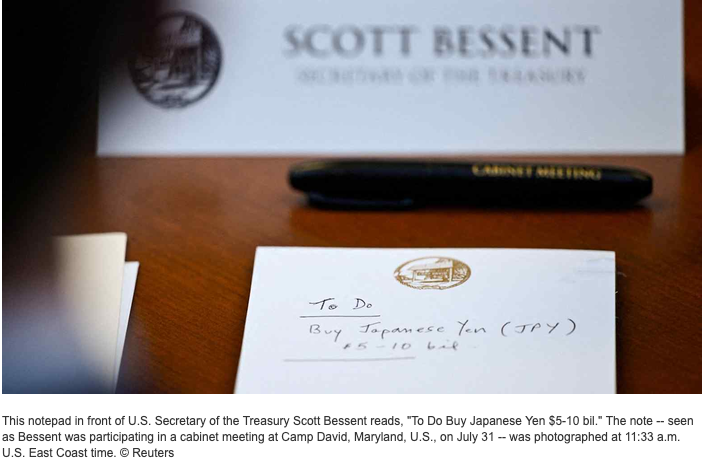

Perhaps the bigger development is the extraordinary intervention in the Japanese yen. Reuters captured this snapshot of Scott Bessent’s To-Do list at Camp David the other day:

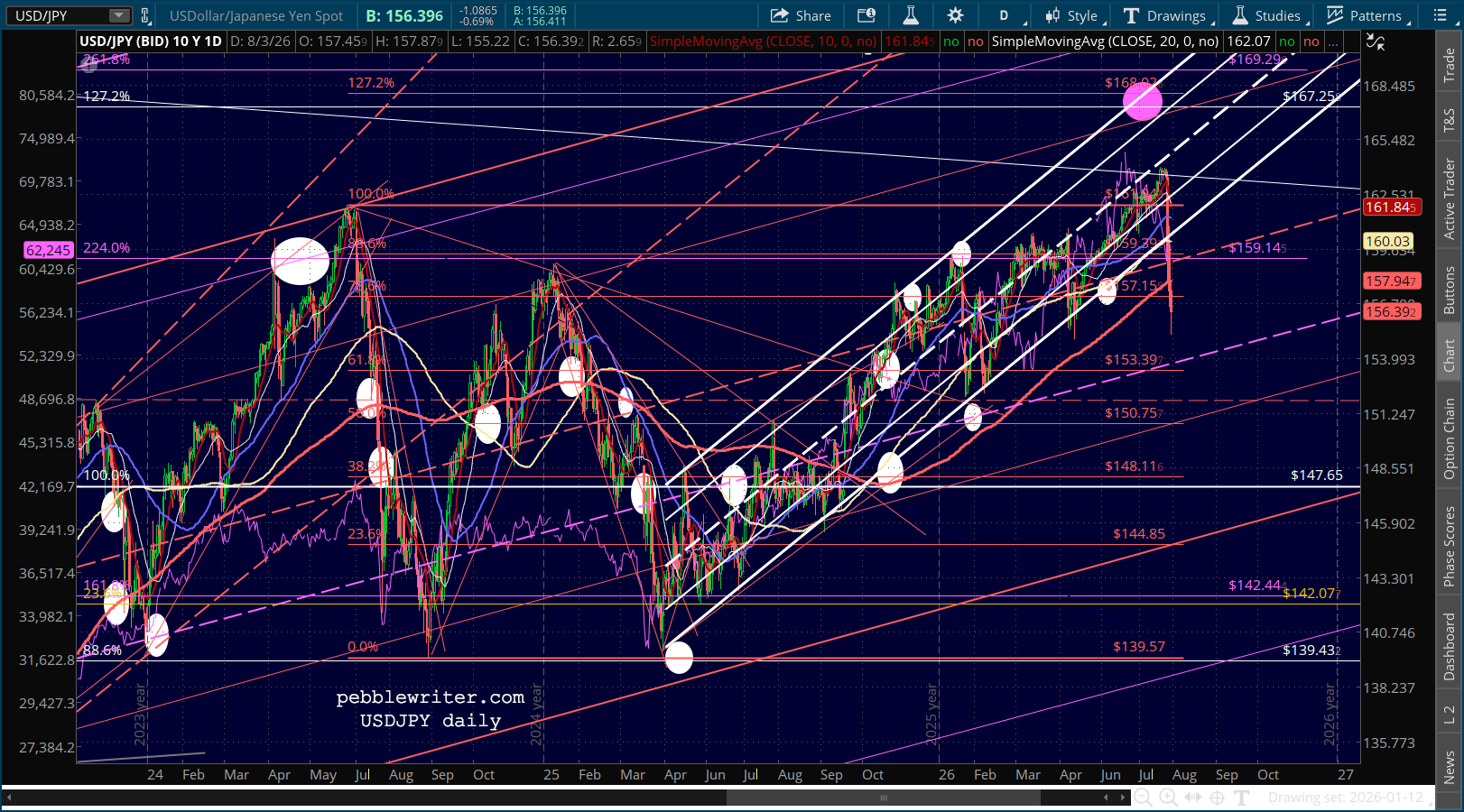

There is some confusion as to how the purchase was financed – with dollars or euros. And, there’s plenty of doubt as to whether the yen strength will last given Japan’s negative real interest rates. But, the USDJPY’s breakdown…

…was mirrored by a breakdown in the DXY. Such declines have been beneficial to stocks of late.

…was mirrored by a breakdown in the DXY. Such declines have been beneficial to stocks of late.

Another correction was averted in the usual way, with investors assured that there’s nothing to worry about. Volatility is under control…

…oil prices are returning to normal…

…inflation is under control…

…and, the market is once again headed to new highs.

The reality is that all of these news flashes are just the lies the wolf wants you to believe. Lies like the weekly proclamations that the Middle East is no longer embroiled in war. We got another one last night. It took a great deal of restraint for Fox News to leave off the exclamation point.

Hamas agrees to complete disarmament under ‘historic’ Gaza agreement

If we dig a little deeper in practically any other news source website, we see that the so-called deal – involving the Board of Peace, no less – is only a draft of a deal, would take up to a year to be consummated, and would involve Hamas placing their most potent weapons in a depository managed by a new Palestinian authority. Not even Israel is rooting for this deal to happen.

It’s another nothingburger dreamed up by the White House to calm the markets and reduce the amount of money the Treasury has to spend to keep a lid on oil futures. They trot these stories out weekly (e.g. the Iran War has ended 15-20 times so far) or whenever the stock market wakes up with a hangover and realizes it drank way too much last night.

By now, it has dawned on everybody that Trump didn’t select Kevin Warsh as FOMC chair in a rare commitment to integrity and fidelity. Just like we all thought, there was an agreement (wink, wink) that interest rates needed to decline — or at least not rise — regardless of the inflation picture, and definitely in time for the midterms.

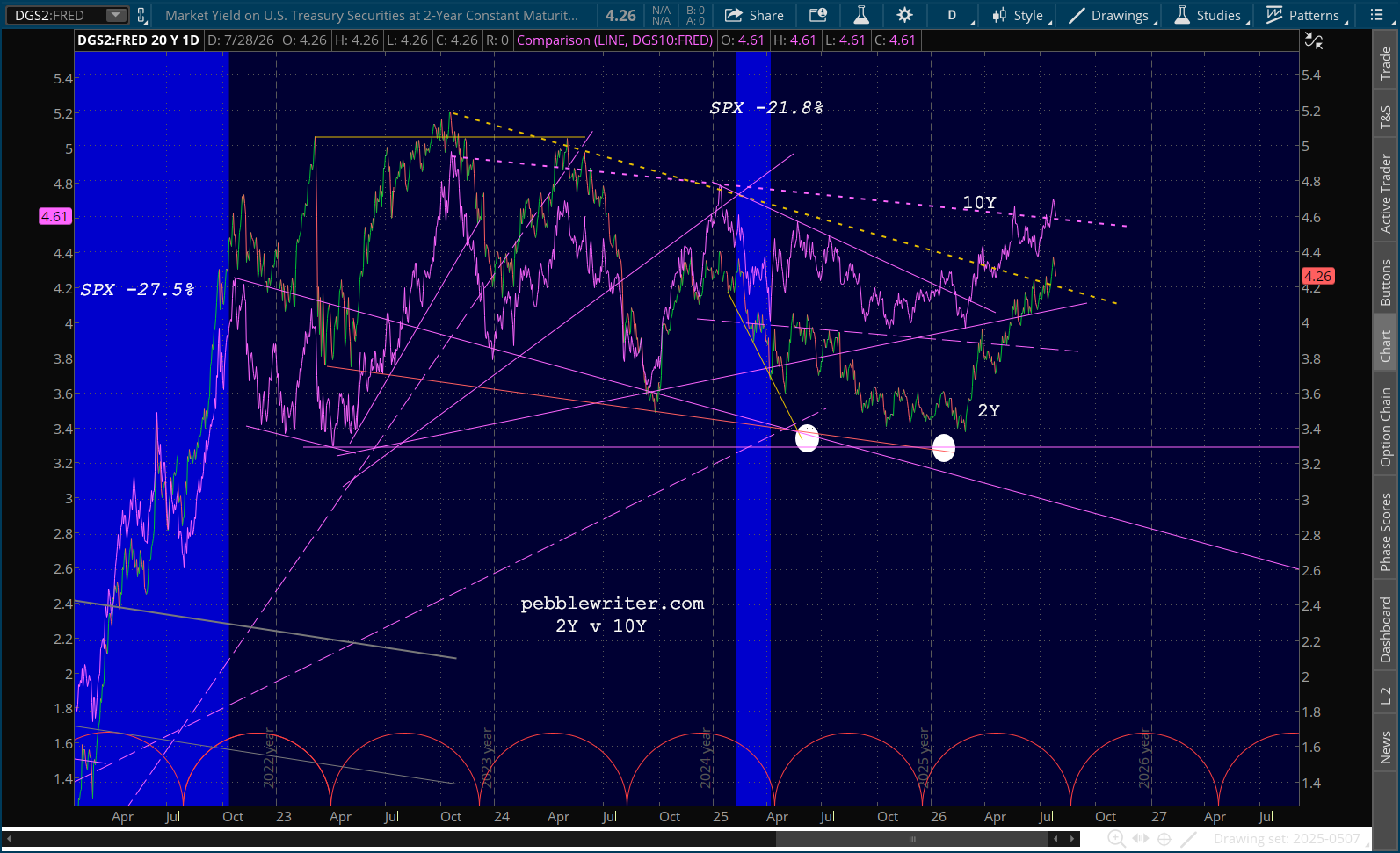

Inflation has been above target for five years. But, Warsh admits it could take months to bring it back down, asserting that last month’s falsified CPI data justifies the Fed sitting on its hands until at least September. The bond market believes otherwise, with the 10Y clearly breaking out while the 2Y drops like a rock as investors like Leopold Aschenbrenner notice the music has stopped. How many other overleveraged prepubescent billionaires are out there?

My read of the economy is that the concentration of wealth and income at the top of the “K” is more than offsetting the lack of the same at the bottom. Likewise, the gains in AI stocks, and previously in the Magnificent Seven, have more than offset the losses in all the rest. In my experience, concentrations typically unwind. It can happen slowly, over time. Or it can happen quickly — which sometimes results in panics.

The Powers That Be have become really good over the years at quelling panics: QE, ZIRP, billions in COVID payments, etc. But, unless this aberration is unlike every other one in history, it will eventually unwind. And, the longer the aberration is perpetuated, the more pain there will be when it does.

Stay tuned.

The expression “all hat, no saddle” was popular in Texas for a minute. It refers to someone who is all talk and no action.

Investors might have been impressed by Warsh’s bold talk yesterday…if only he had offered an equally bold action plan. Instead, he offered the kind of fuzzy, nebulous “trust-us-we’re-smarter-than-you” floridity that seldom convinces skeptics.

Yen strength is producing some dollar weakness this morning. But, there’s a strong cross current from rising yields…

…at least on the 10Y.

The 2Y is reacting more sharply than the 10Y…

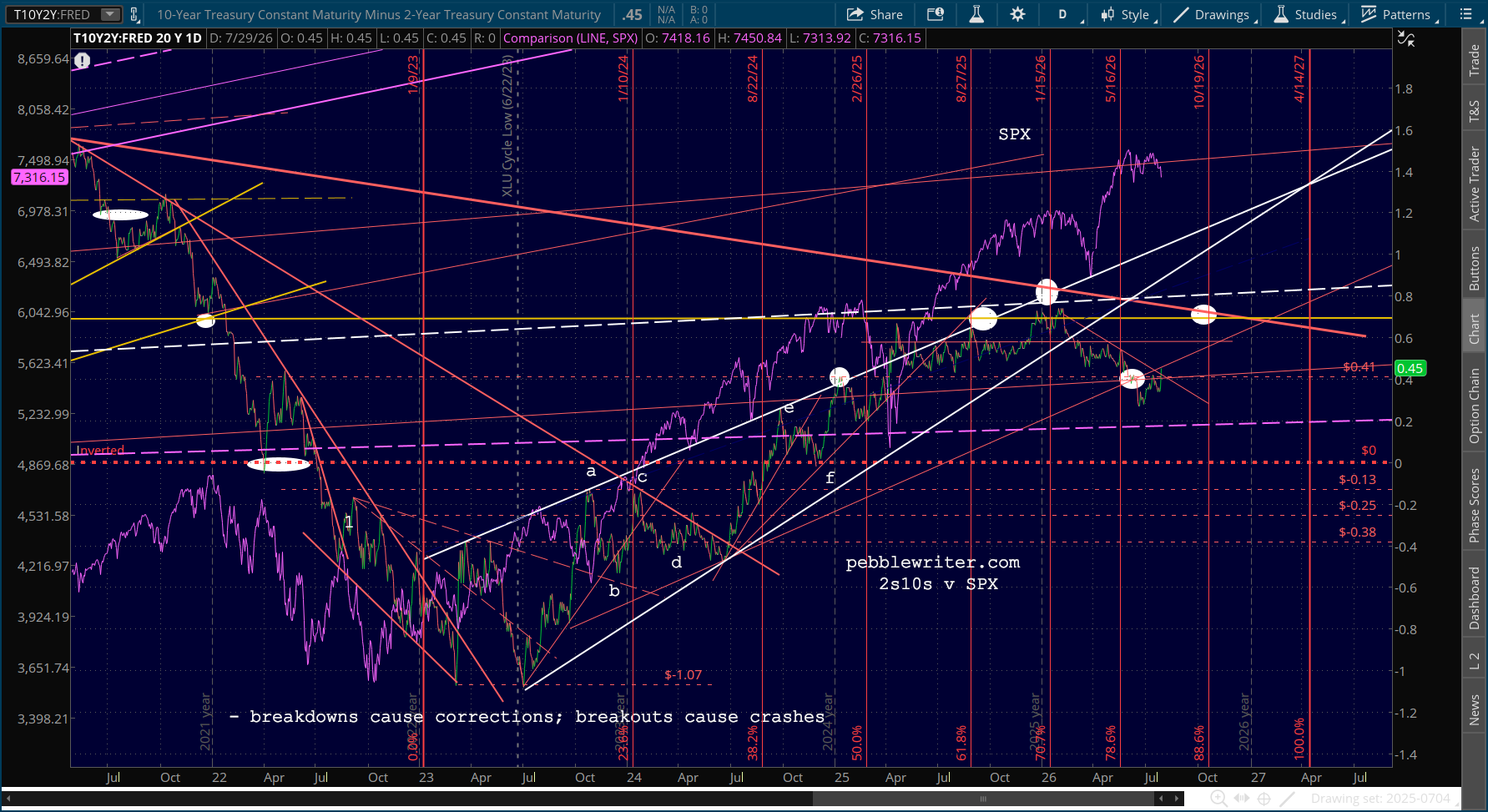

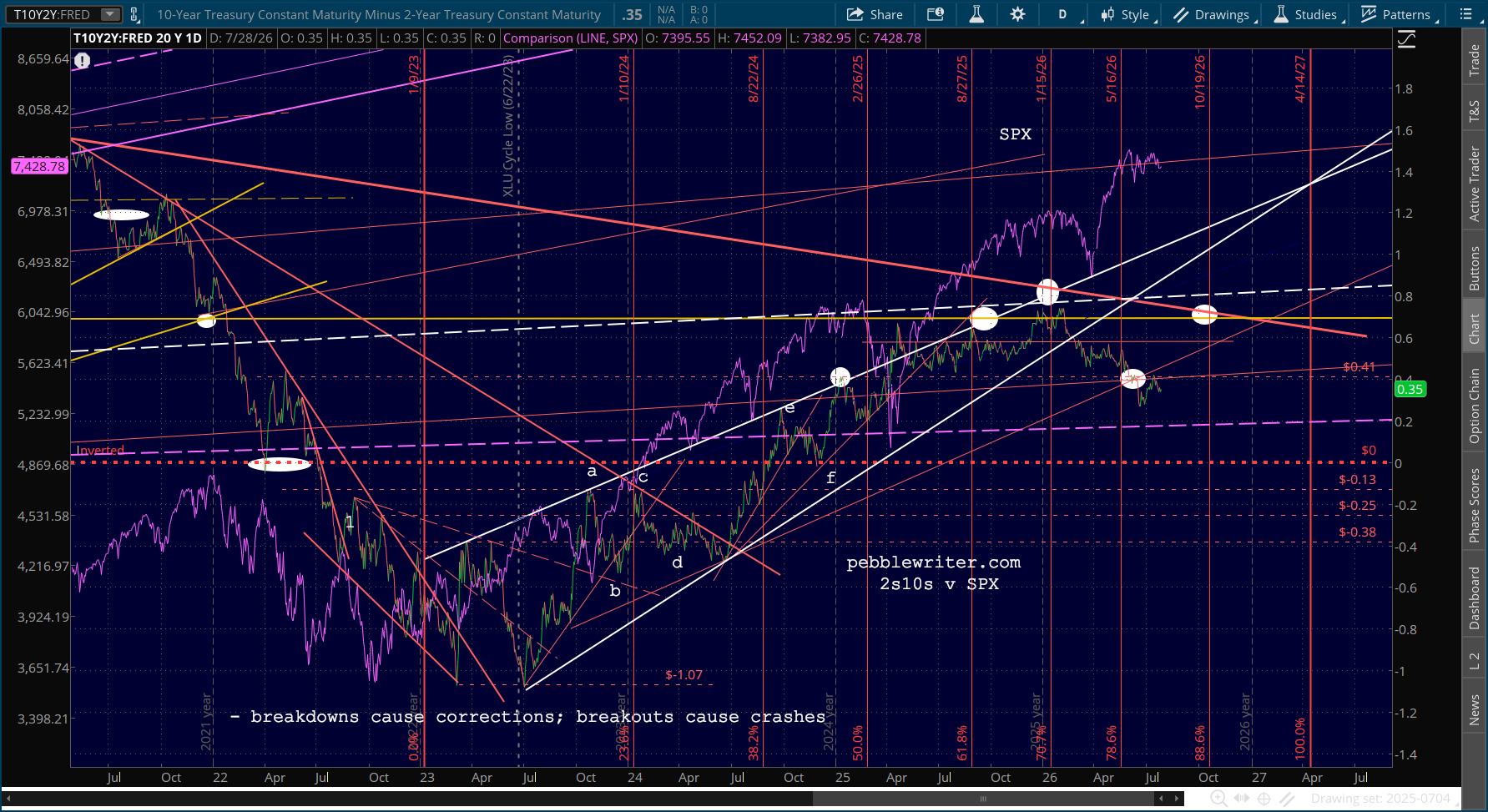

…which has produced a sharp bump in the 2s10s. Is it enough to lift it back above resistance? We’ll see. It means the difference between a correction and a crash.

Speaking of which…things are heating up in the Middle East again. Although WTI reversed off the flag pattern top, the risk of much higher prices hasn’t gone away. The pattern suggests new highs – which is consistent with my long-standing expectation that Iran is playing the long game while Trump desperately searches for an off ramp. Iranian leaders seem perfectly willing to absorb whatever blows may come if it means neutering Trump in the upcoming midterms.

It’s the regime change Trump promised – just not on the regime he was hoping for.

Futures are flat in advance of today’s FOMC announcement. I don’t know whether the FOMC will have the courage to announce a rate hike in the wake of the recent (dubious) CPI print. But, Trump’s inability to put the Middle East back together after single-handedly breaking it has left us with one of the most disastrous economic scenarios since the Great Financial Crisis.

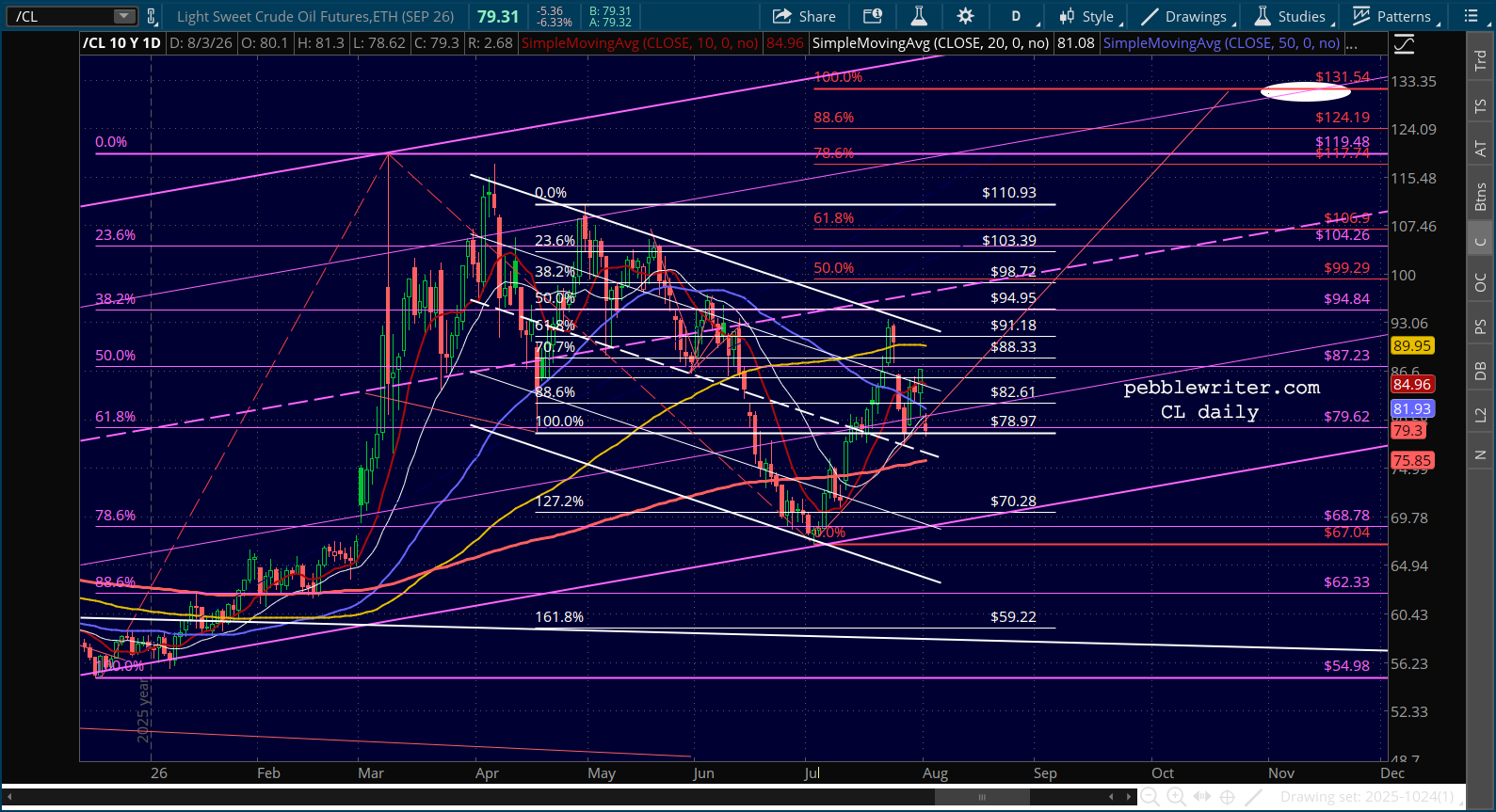

CL has completed a very well-formed Flag Pattern targeting 131.54.

The 2s10s has finished its backtest and is prepped for a sizable downturn.

Both the 2Y and the 10Y have clearly broken out.

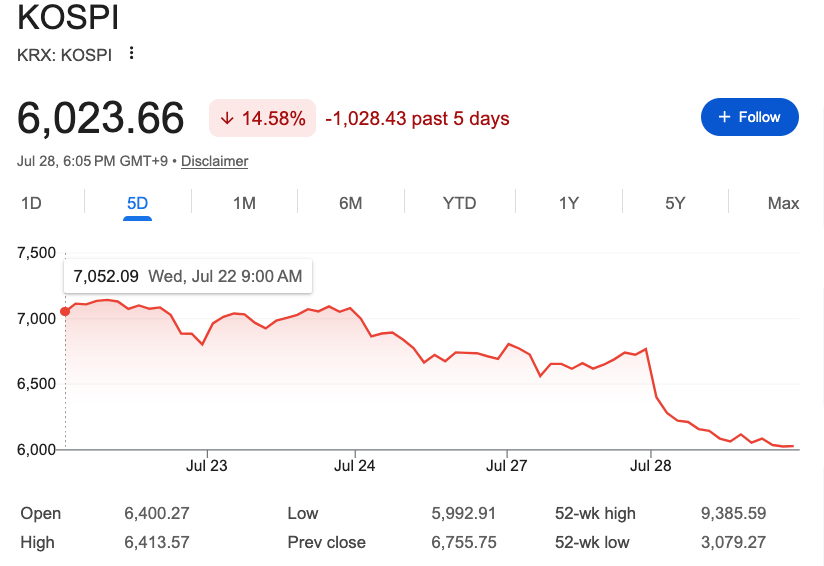

Futures are mixed on the eve of an FOMC meeting where a rate hike is a 35% possibility and a 10% one-day plunge in the Korean chip-heavy KOSPI index is a 100% certainty.