The situation is pretty clear. By raising rates, the FOMC could continue to fight inflation but would also exacerbate the banking crisis. By pausing, the FOMC could give banks a little relief but would loosen financial conditions – thereby making it tougher to reduce inflation to target.

The seldom discussed situation is what impact the Fed’s decision would have on equity markets. This unspoken third mandate often weighs more heavily on decisions than do full employment and price stability.

From that standpoint, we look for the Fed to either: (a) pause but stress that the pause is due to rapidly tightening financial conditions which are inherently disinflationary; or, (b) raise 25 bps but stress that this could be the last hike for a while because they believe inflation is headed significantly lower due to tightening financial conditions.

Our own research indicates that this is true. Gas prices, which are very highly correlated with CPI, are slated to fall 18.6% YoY in March. The last time the YoY delta hit this level was in Nov 2021 when CPI registered 1.17%.

Obviously, other stickier factors have usurped the inflation narrative: wages, real estate, cars, etc. But, as we’ve discussed often in these pages, many of these other categories have been fairly flat or have declined over the past year – meaning that their YoY deltas are also falling rapidly.

Obviously, other stickier factors have usurped the inflation narrative: wages, real estate, cars, etc. But, as we’ve discussed often in these pages, many of these other categories have been fairly flat or have declined over the past year – meaning that their YoY deltas are also falling rapidly.

Consider food prices, still elevated at 9.5% YoY in Feb.

Underlying prices, as reflected in the DBA agricultural ETF, have fallen 11.3% over the past year. As long as it remains in the very tight trading range it’s been in since Jun 2022, the YoY decline will reduce inflationary pressures just as oil/gas have.

Underlying prices, as reflected in the DBA agricultural ETF, have fallen 11.3% over the past year. As long as it remains in the very tight trading range it’s been in since Jun 2022, the YoY decline will reduce inflationary pressures just as oil/gas have.

Futures have been vacillating around unch all night. The real action should start at 2PM with the announcement, followed by Powell’s press conference at 2:30.

Futures have been vacillating around unch all night. The real action should start at 2PM with the announcement, followed by Powell’s press conference at 2:30.

continued for members…

continued for members…

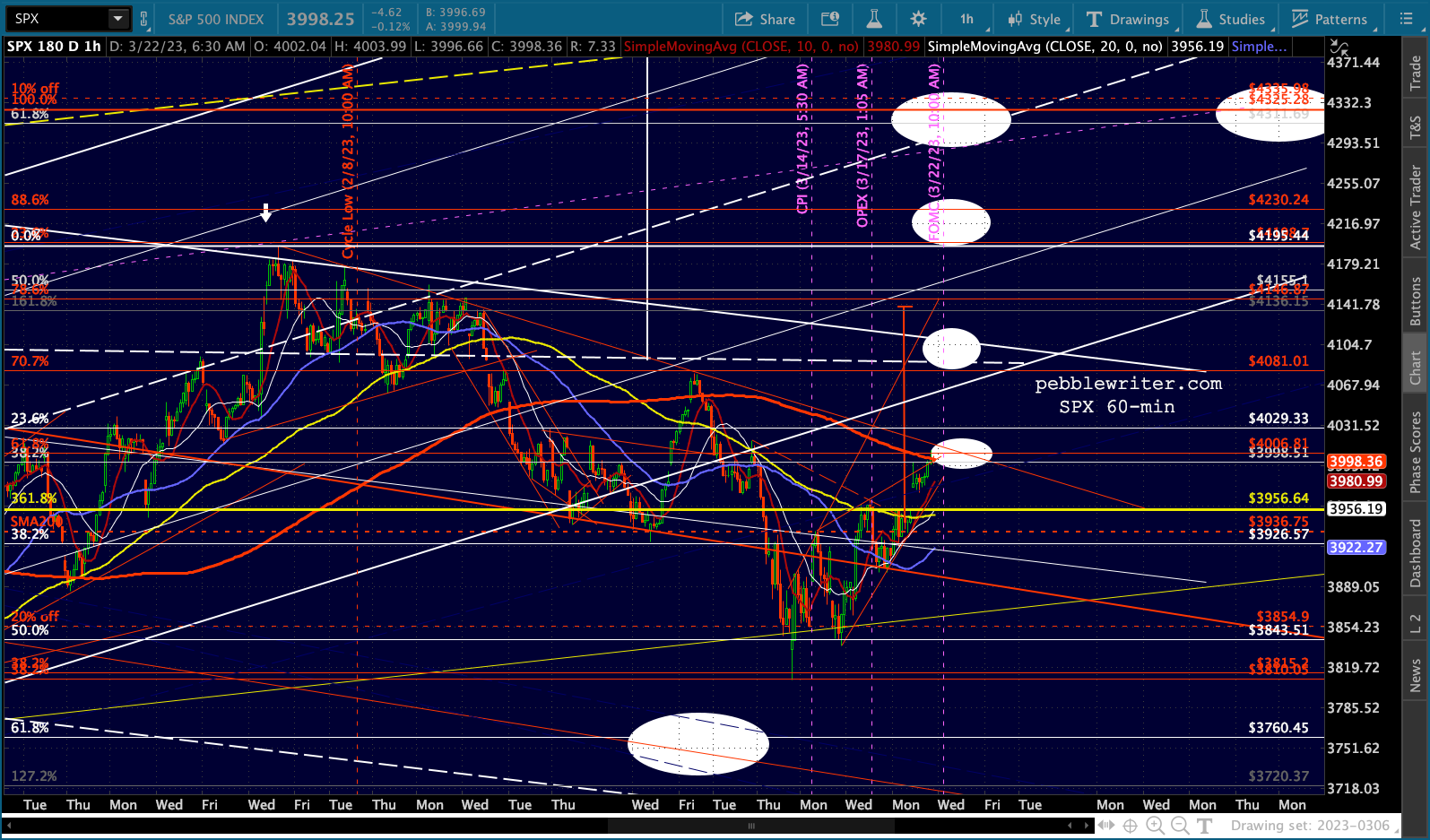

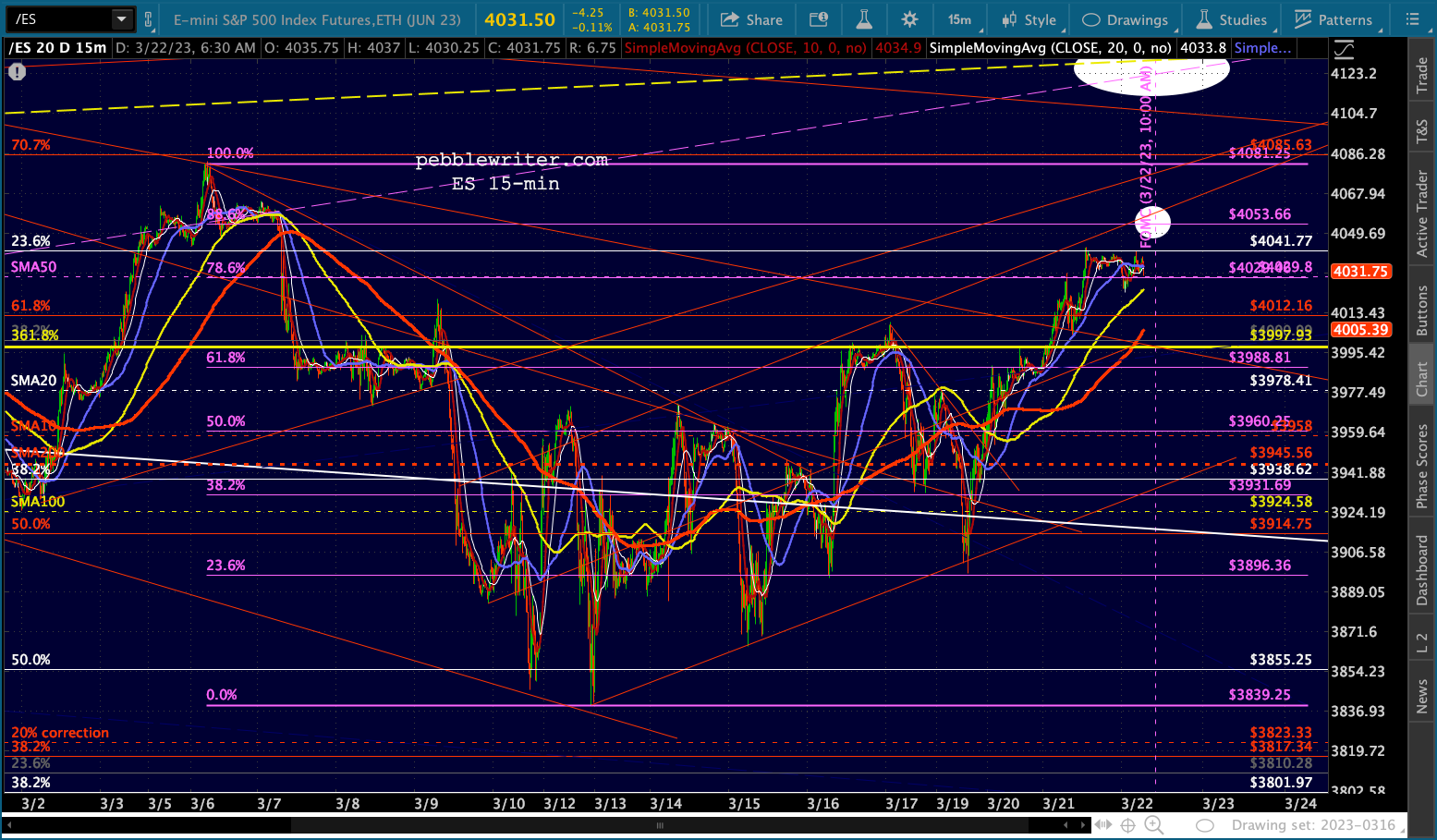

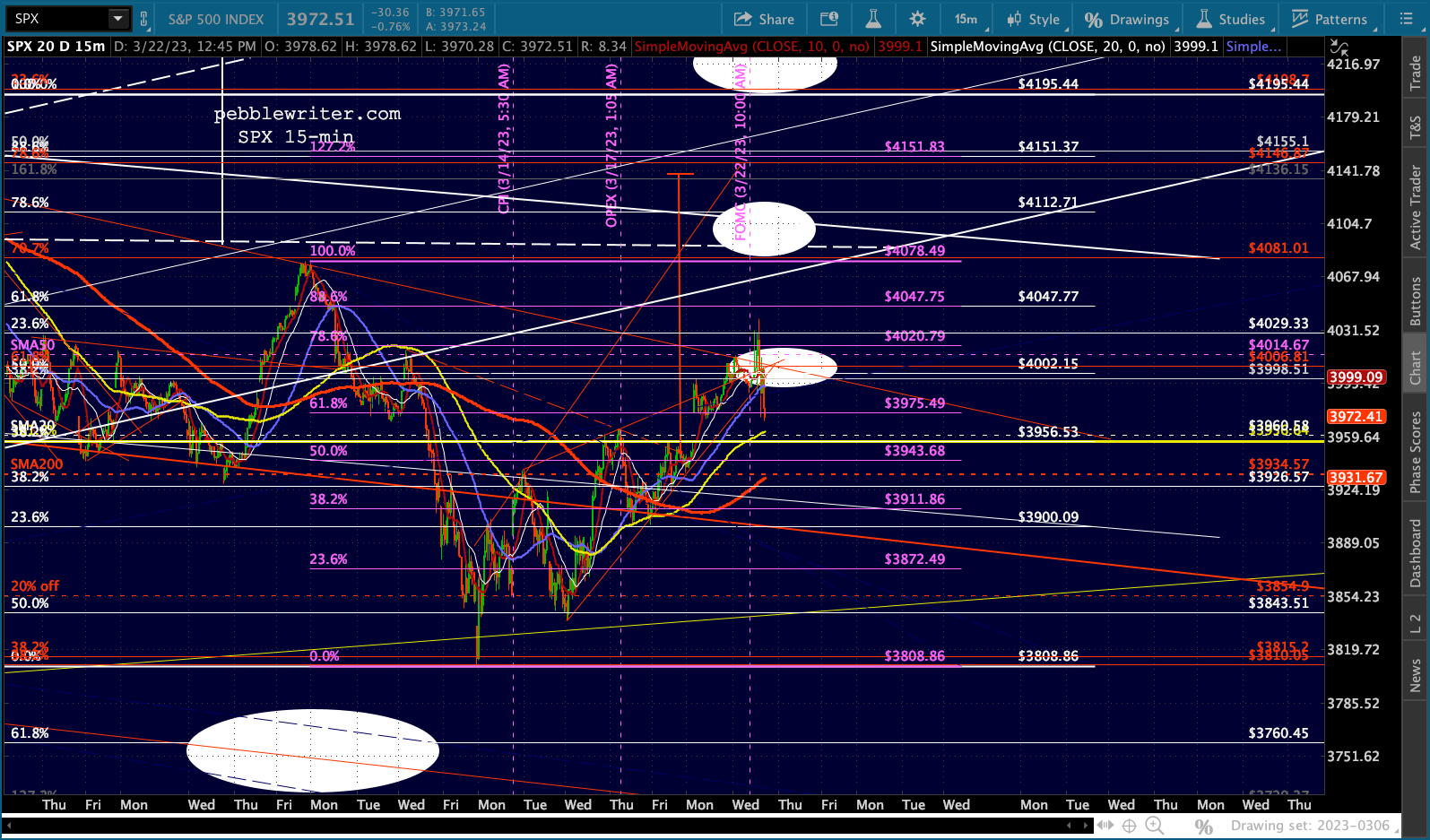

Not much has changed overnight. SPX reached our 4000 target yesterday. Note that it’s also in line with a TL off the Feb 2 highs. The ES equivalent shows it has broken above that same TL and is resting just above the .786 Fib and below the .886 Fib.

The ES equivalent shows it has broken above that same TL and is resting just above the .786 Fib and below the .886 Fib.

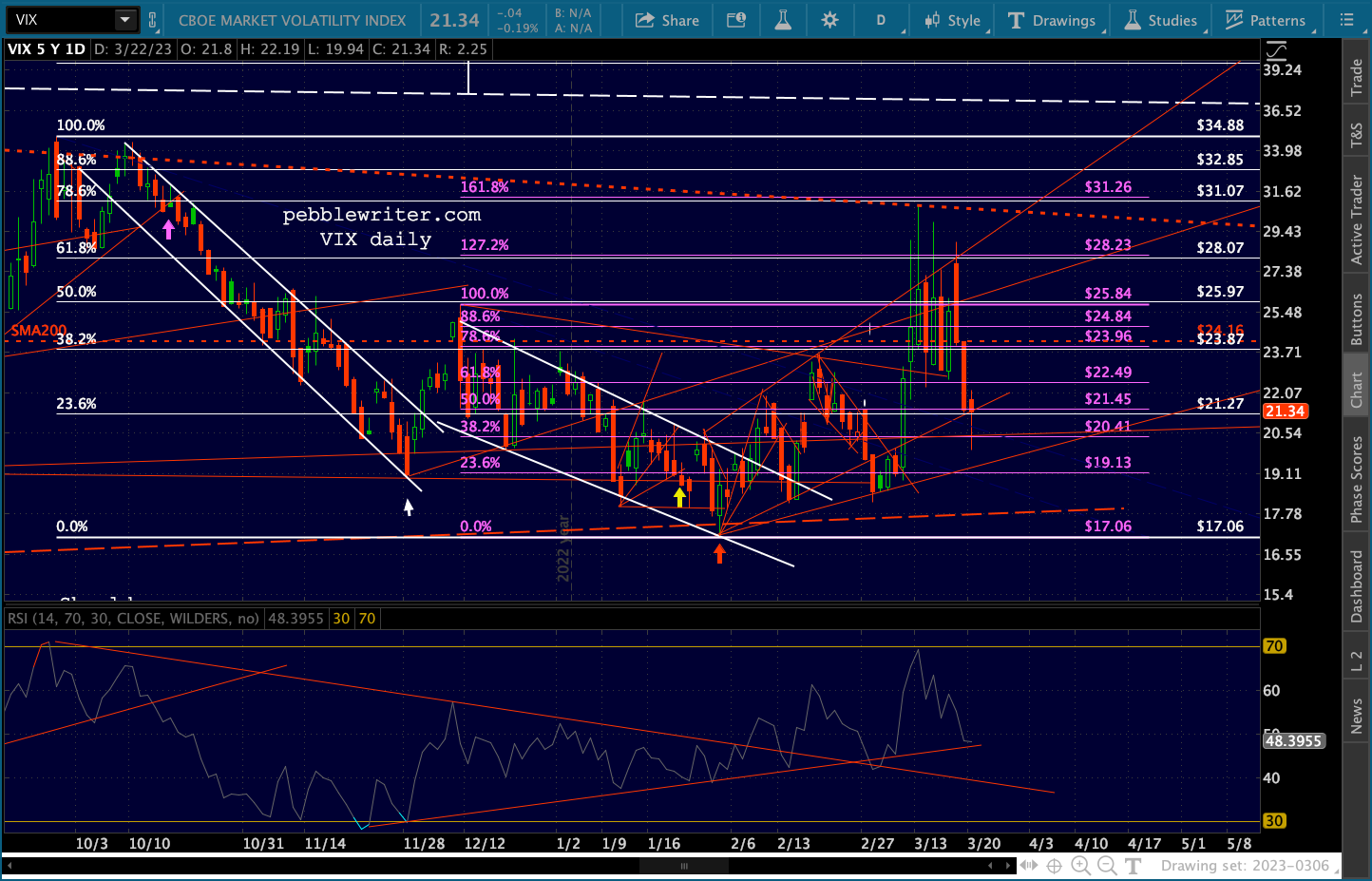

VIX is still clearly being utilized to boost stock prices.

VIX is still clearly being utilized to boost stock prices.

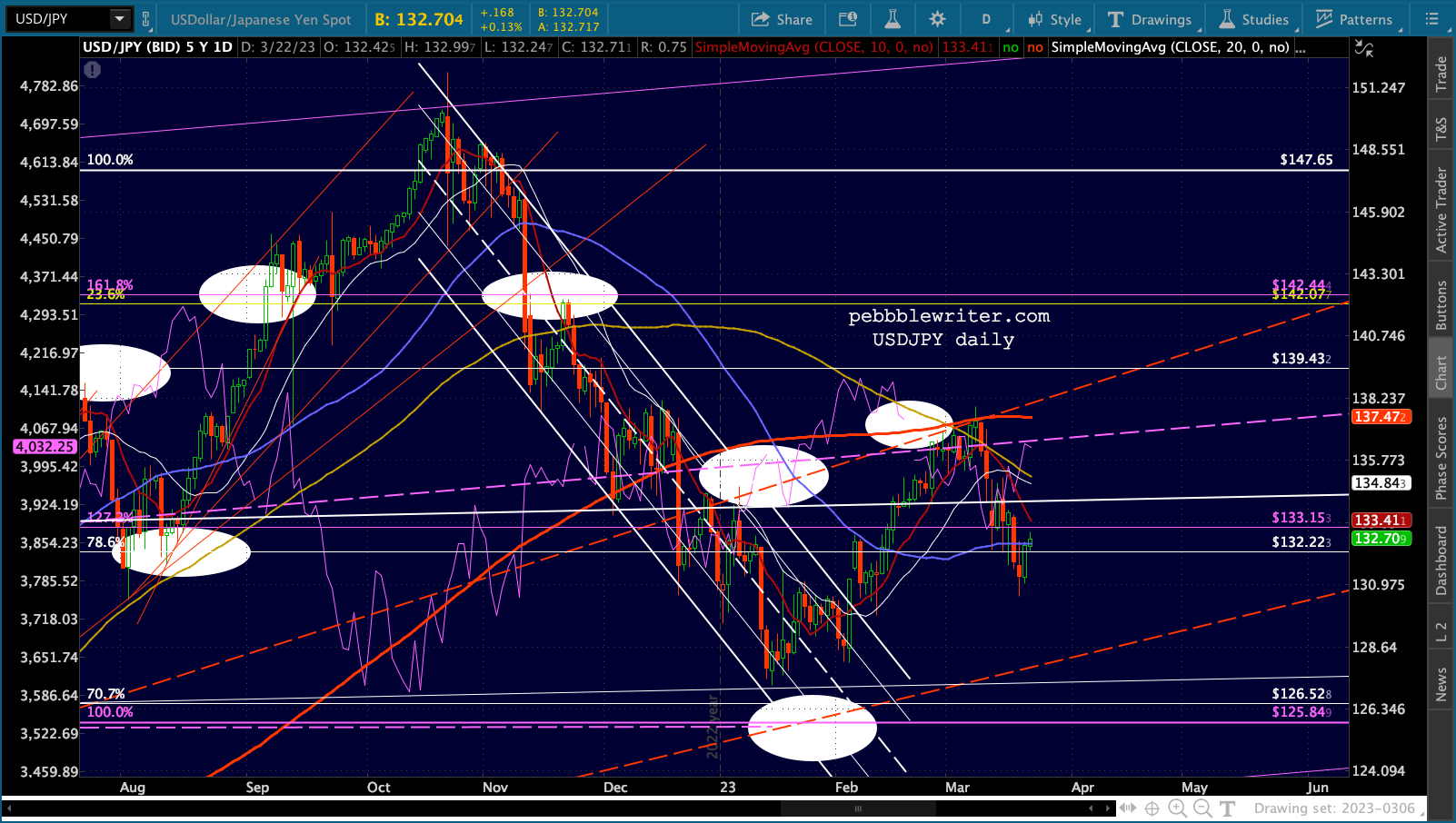

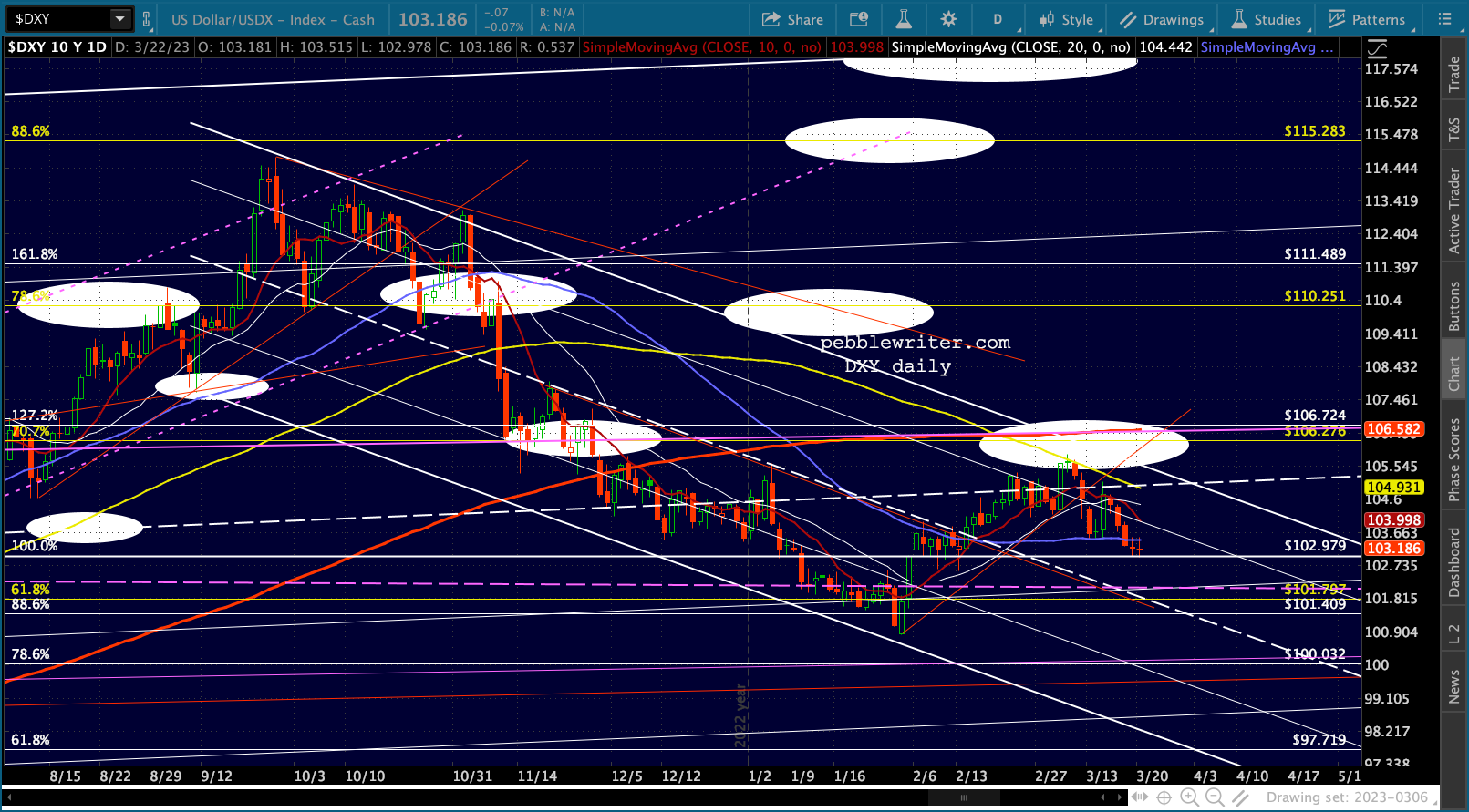

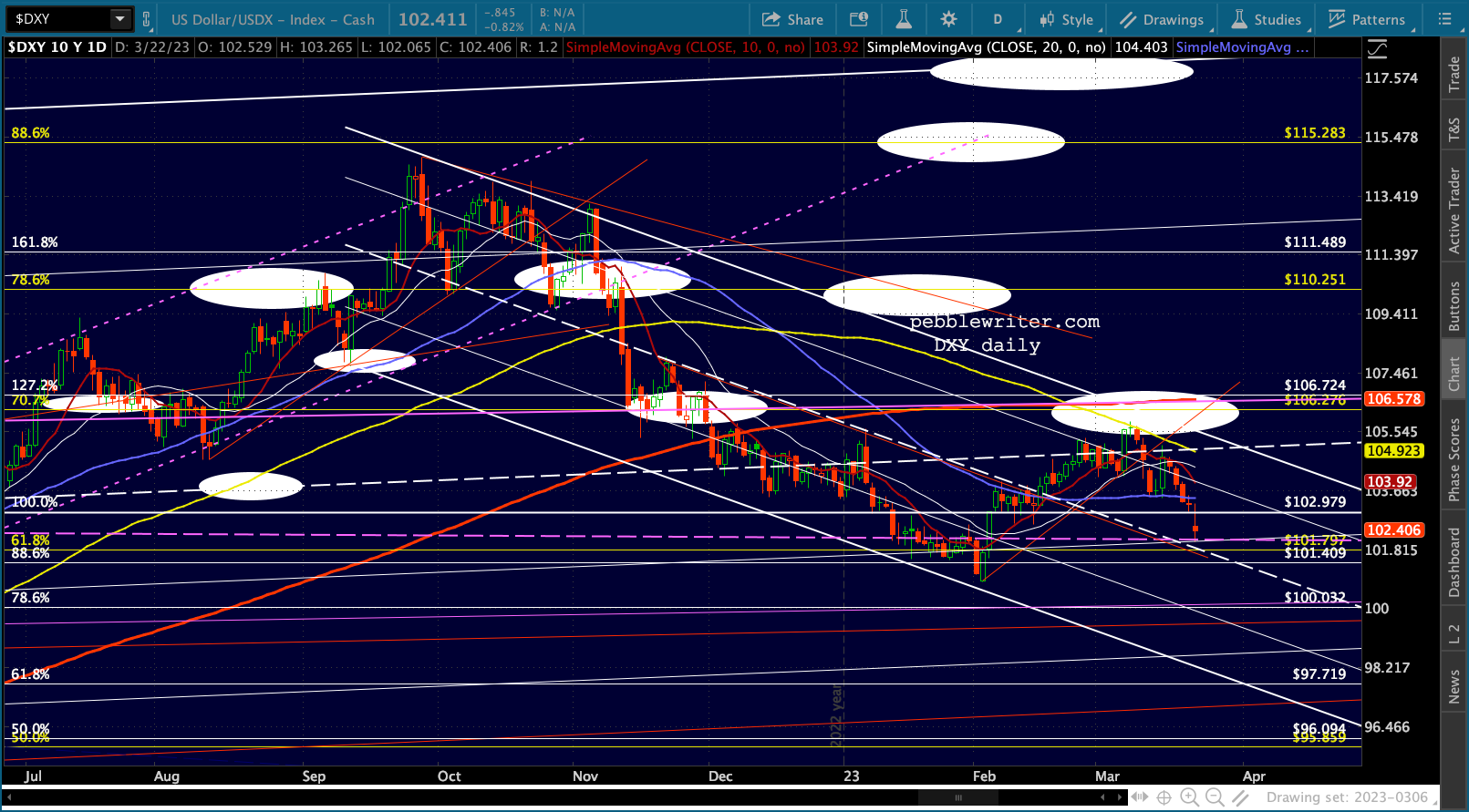

As are currencies, which continue to keep modest pressure on the DXY.

As are currencies, which continue to keep modest pressure on the DXY.

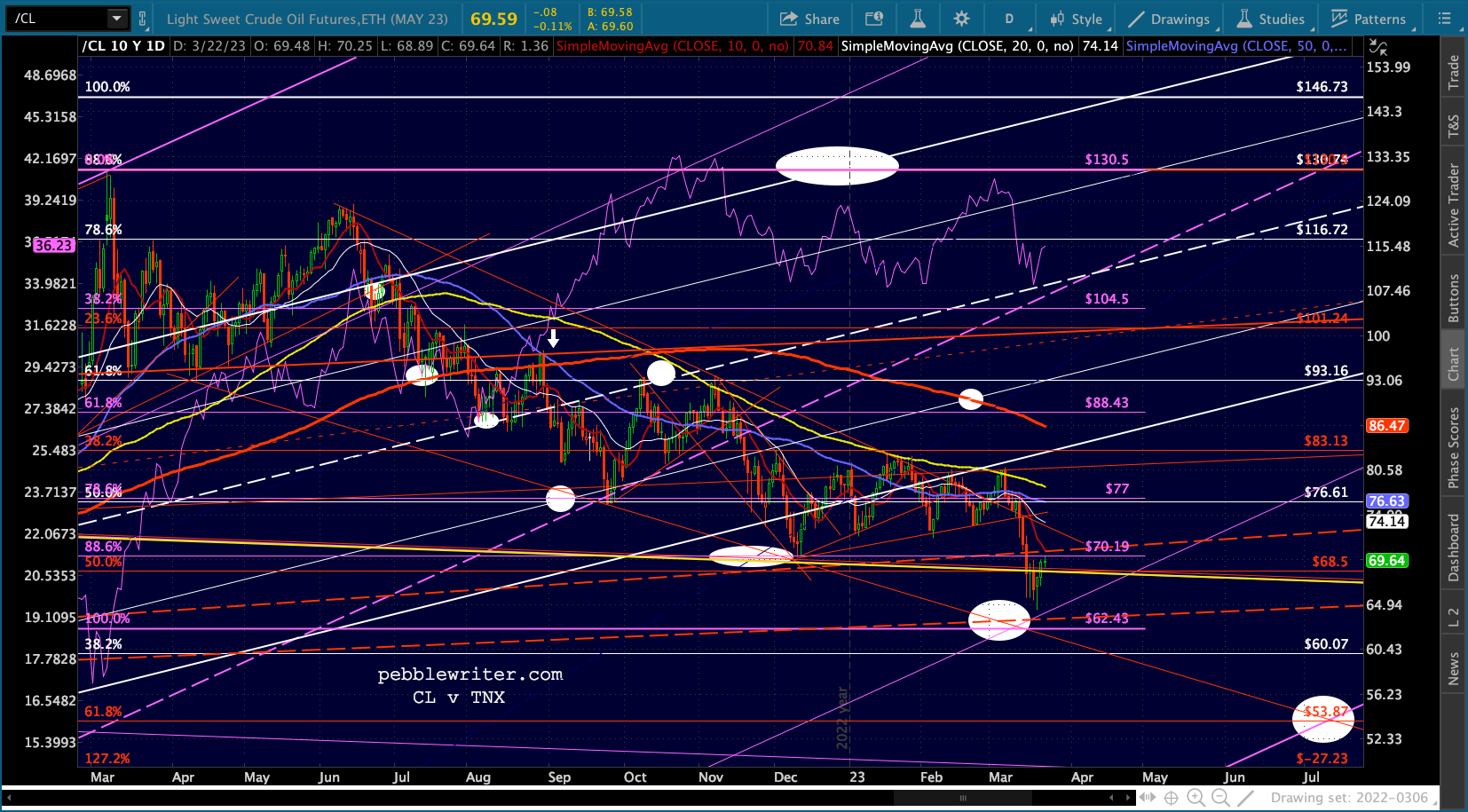

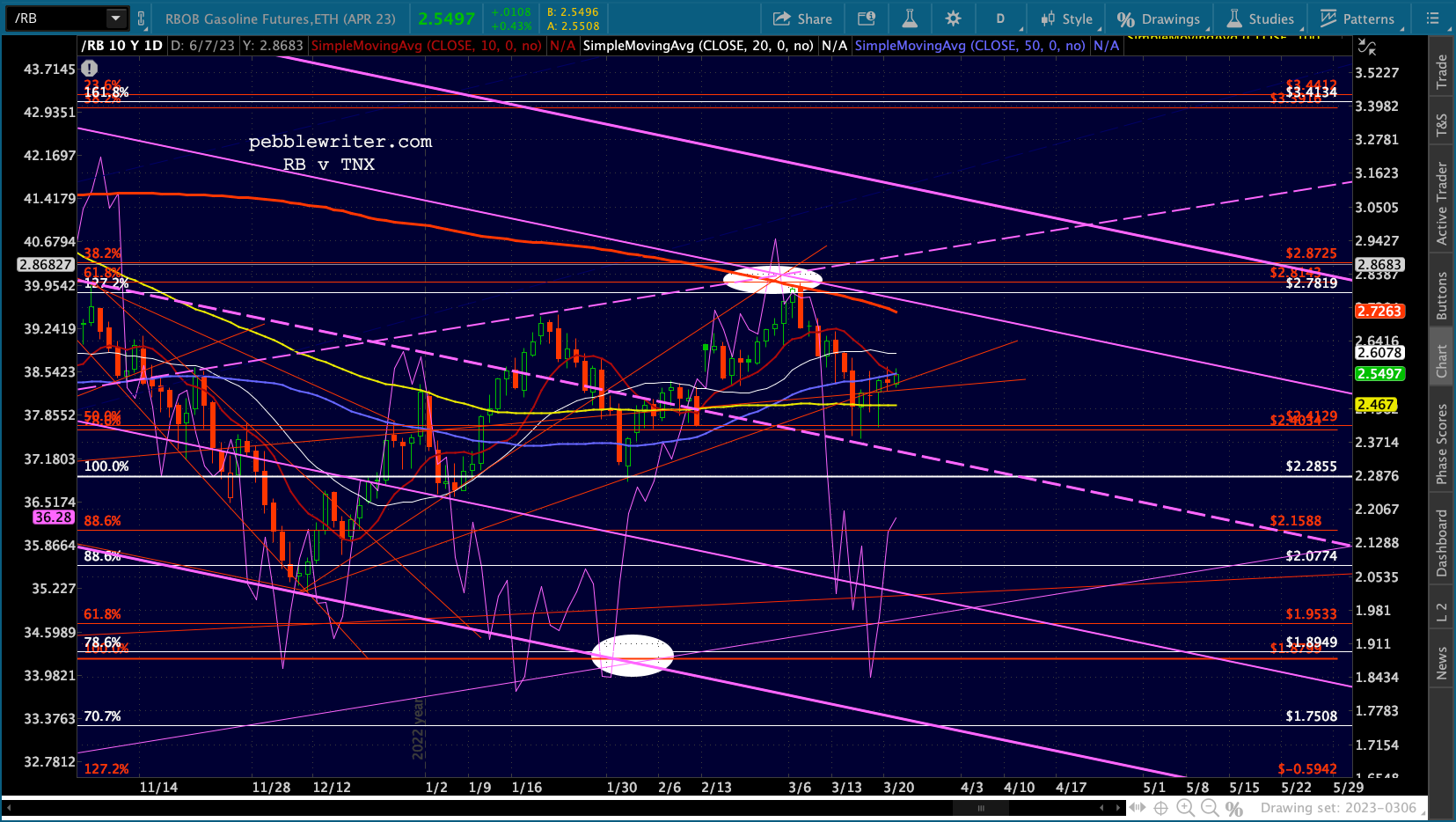

Oil and gas are hanging in there…

Oil and gas are hanging in there…

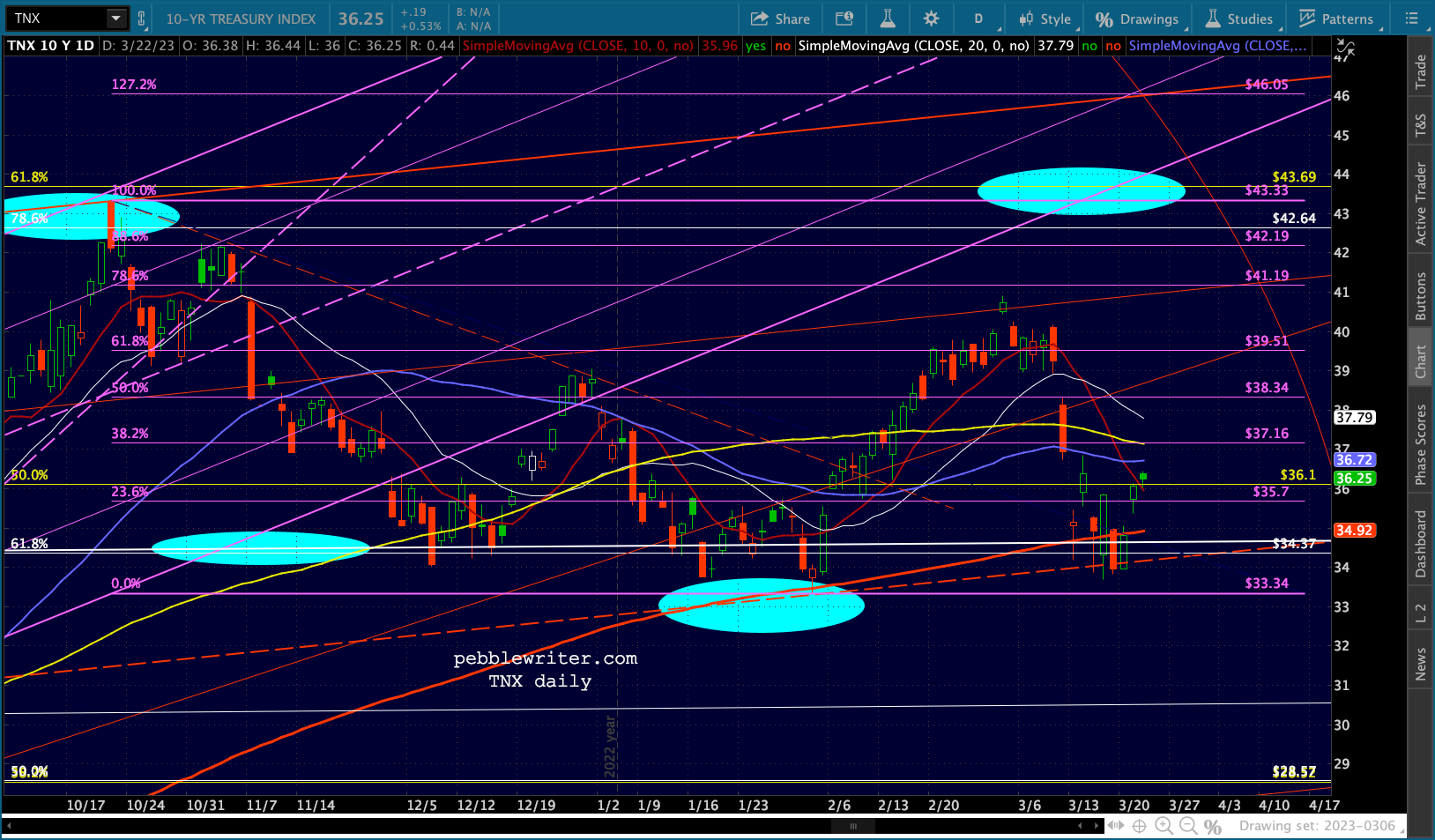

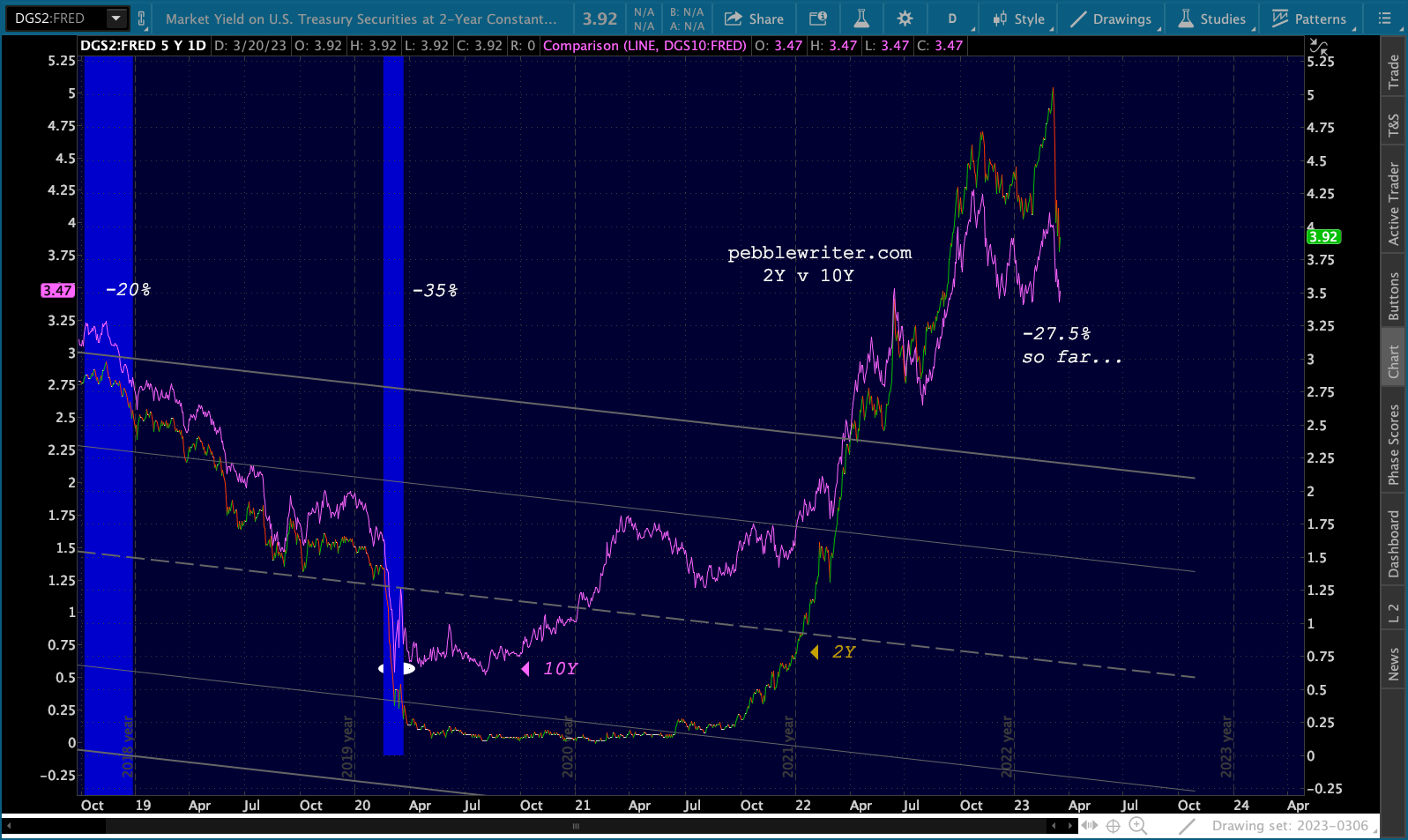

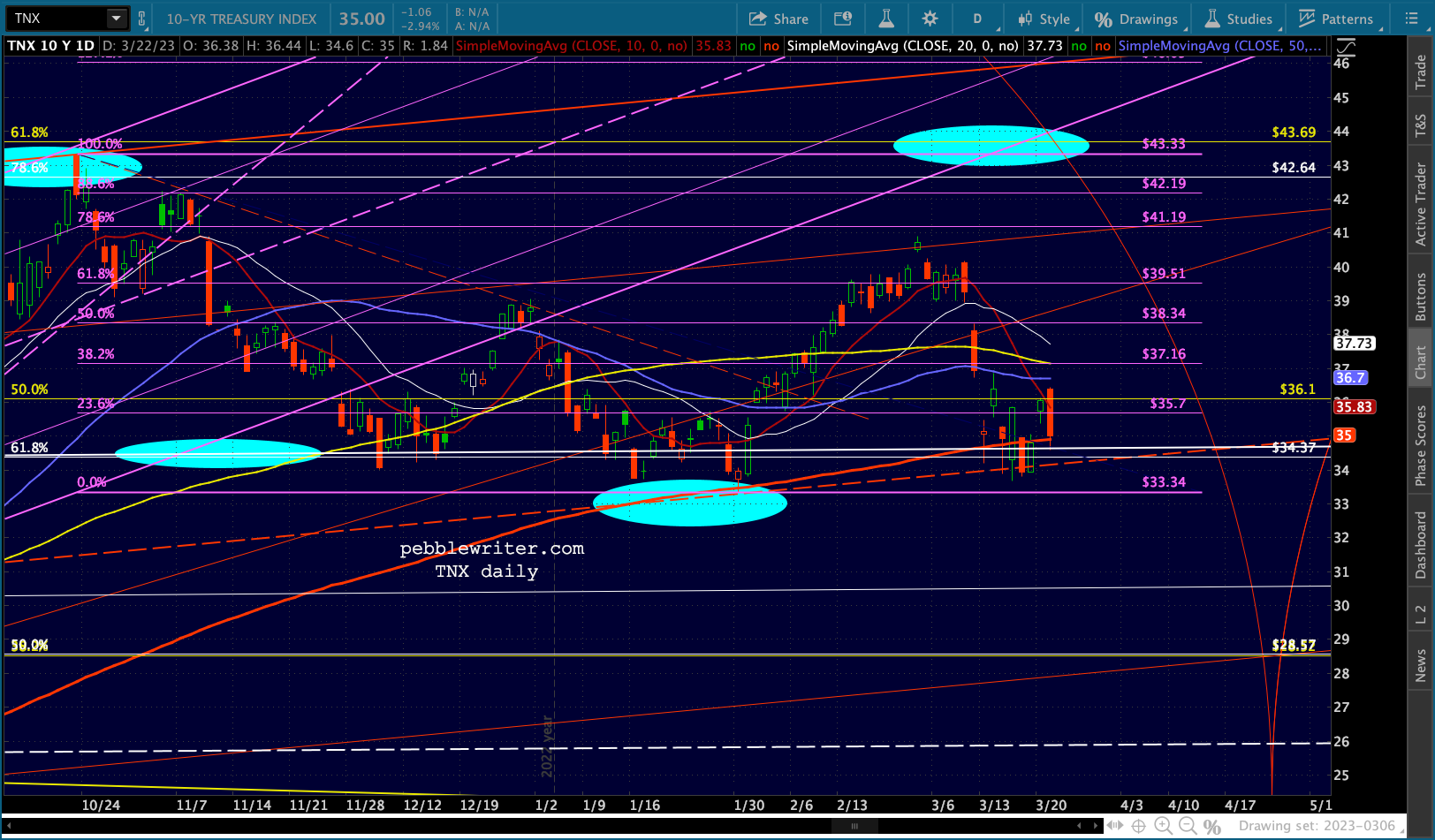

… just enough to prop up the 10Y…

… just enough to prop up the 10Y… …which has managed to avoid a push above 2s10s -42 bps for another day.

…which has managed to avoid a push above 2s10s -42 bps for another day.

Stay tuned…

Stay tuned…

UPDATE: 3:45 PM

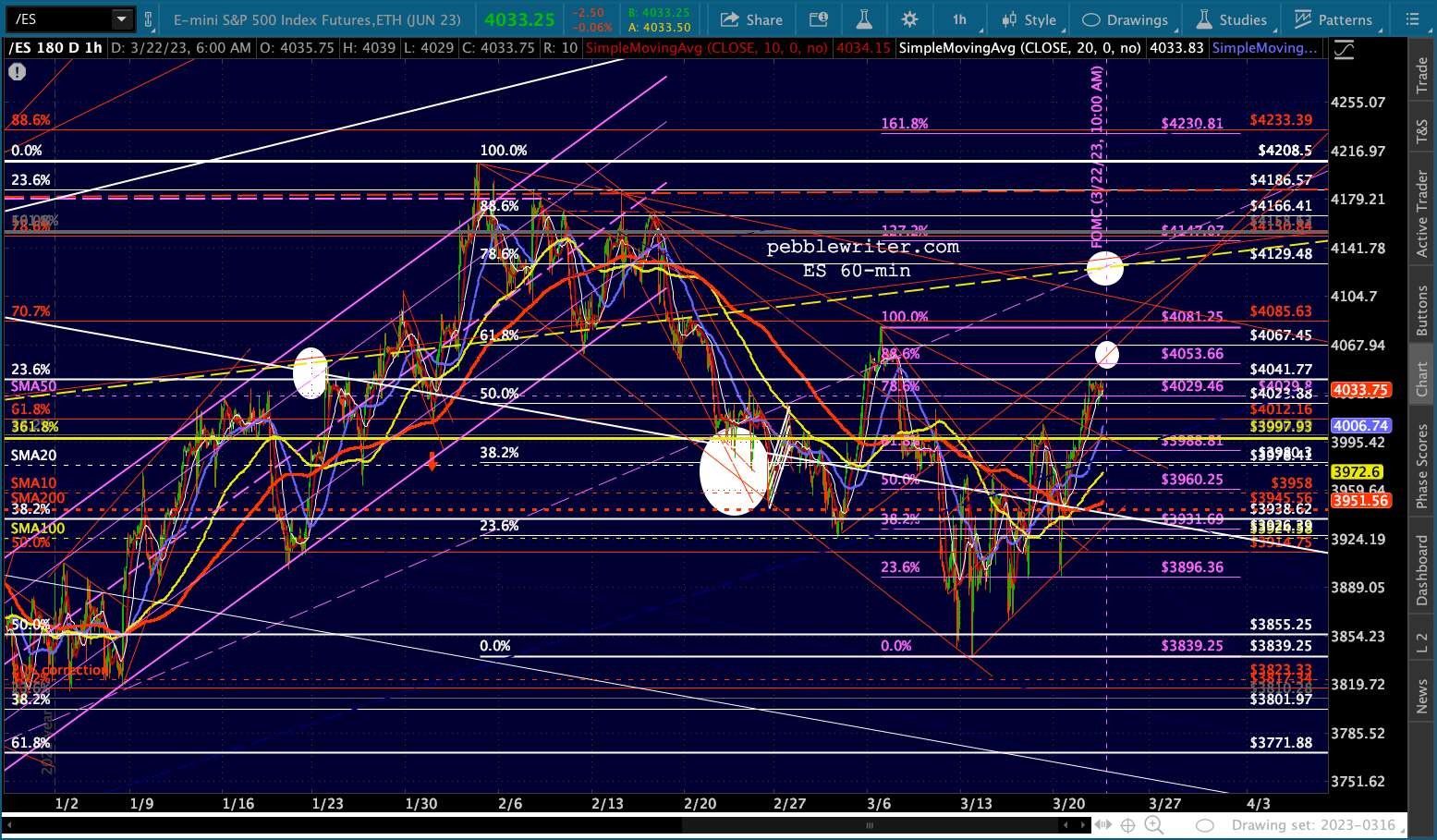

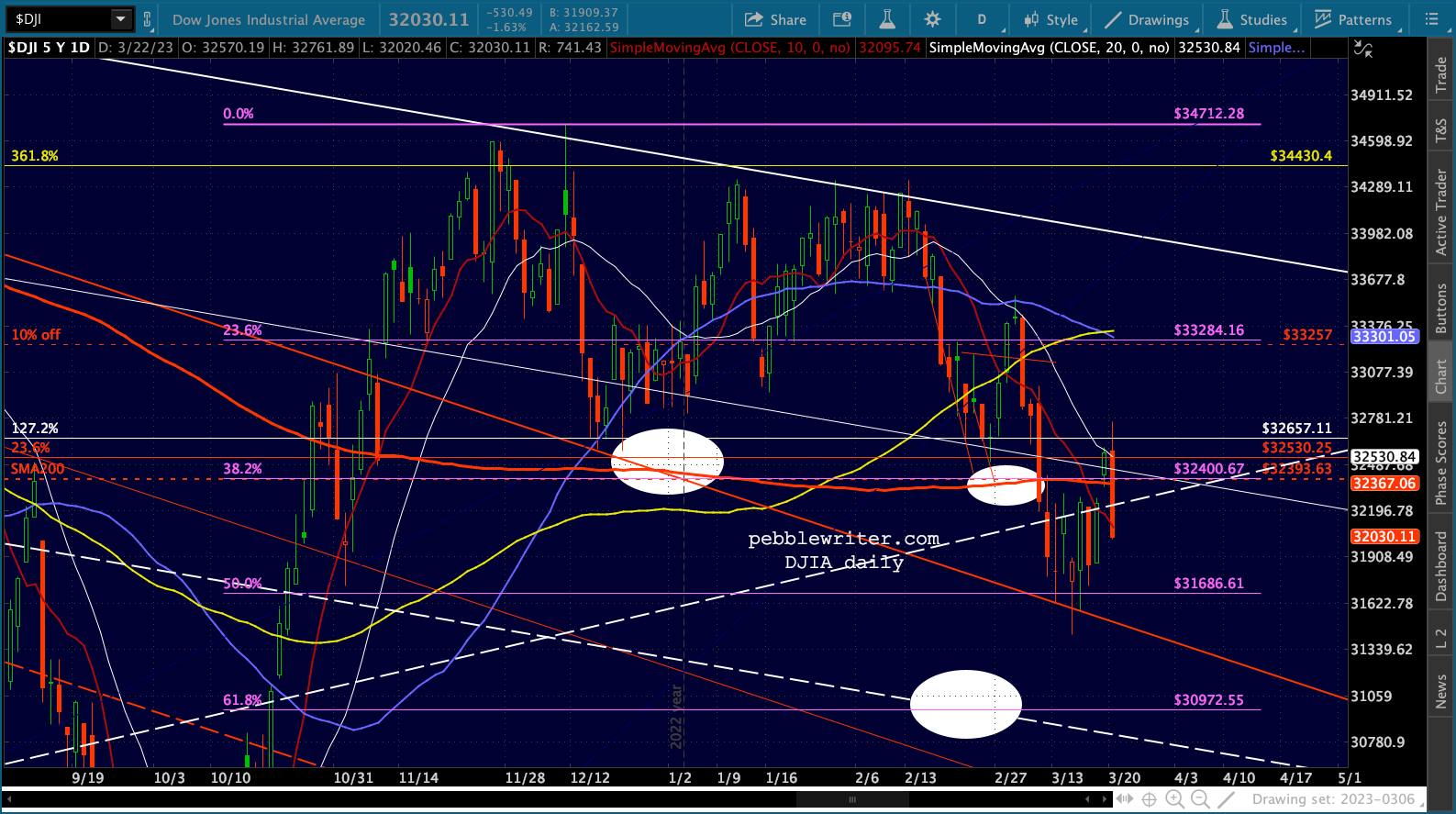

Powell chose the second option. Though SPX initially broke out of the rising wedge, it has now broken down, eyeing its SMA200 for support.

ES has caught a bid at the red channel midline and SMA20.

ES has caught a bid at the red channel midline and SMA20. VIX, which tested and bounced off its SMA50 on a 10%+ dip, is now back to positive.

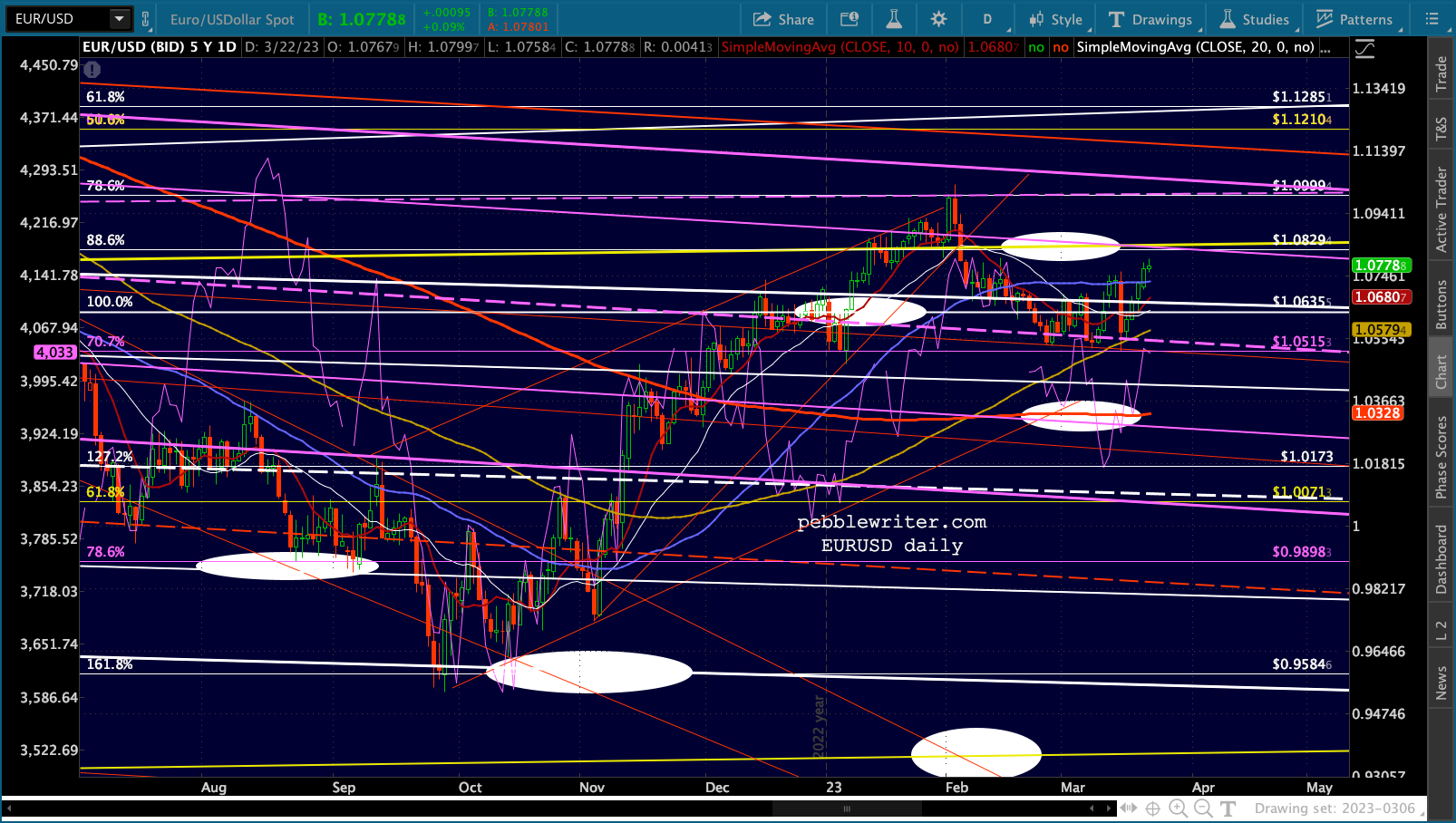

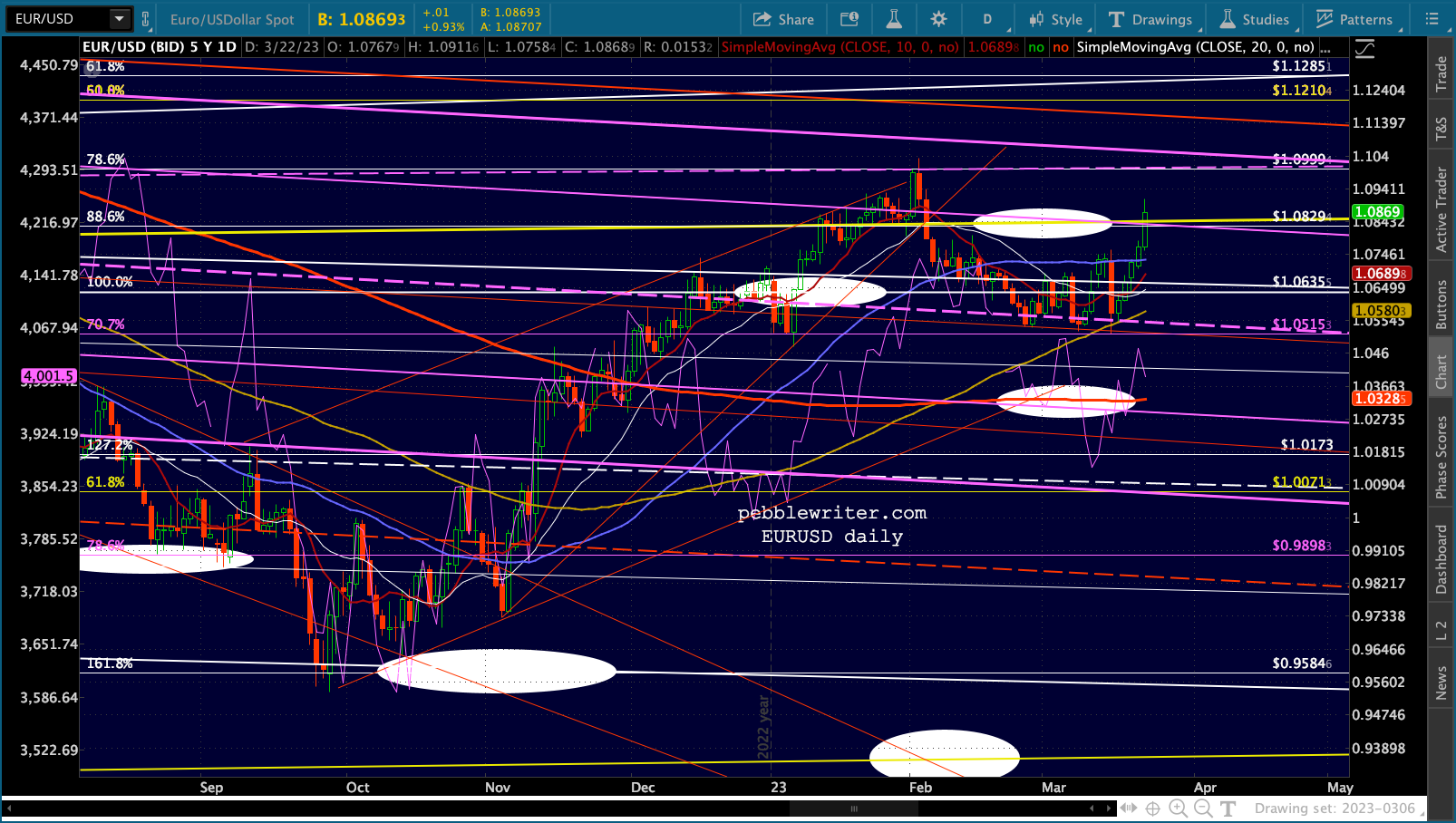

VIX, which tested and bounced off its SMA50 on a 10%+ dip, is now back to positive. EURUSD rallied – legit because the Fed did hike, after all.

EURUSD rallied – legit because the Fed did hike, after all.  The DXY continues to get hammered, but has reached pretty good support.

The DXY continues to get hammered, but has reached pretty good support.  The 10Y got down to 3.46…

The 10Y got down to 3.46… …but the 2Y is back below 4%, leaving the 2s10s at -50bps.

…but the 2Y is back below 4%, leaving the 2s10s at -50bps.

This is shaping up as an ugly close. It’s hard to imagine many investors were surprised by the decision and/or Powell’s dovish comments. Pulling back on expectations of future hikes was beneficial, but it didn’t stick.

This is shaping up as an ugly close. It’s hard to imagine many investors were surprised by the decision and/or Powell’s dovish comments. Pulling back on expectations of future hikes was beneficial, but it didn’t stick.

From a charting standpoint, it’s safe to say that many of the drivers of the latest rally have run into resistance. The key, now, is for SPX and ES to remain above their SMA200s – something the Dow was unable to do.

UPDATE: 18:00

UPDATE: 18:00

Looks like the rally was cut short by Janet Yellen’s announcement that there would be no blanket protection for bank depositors.