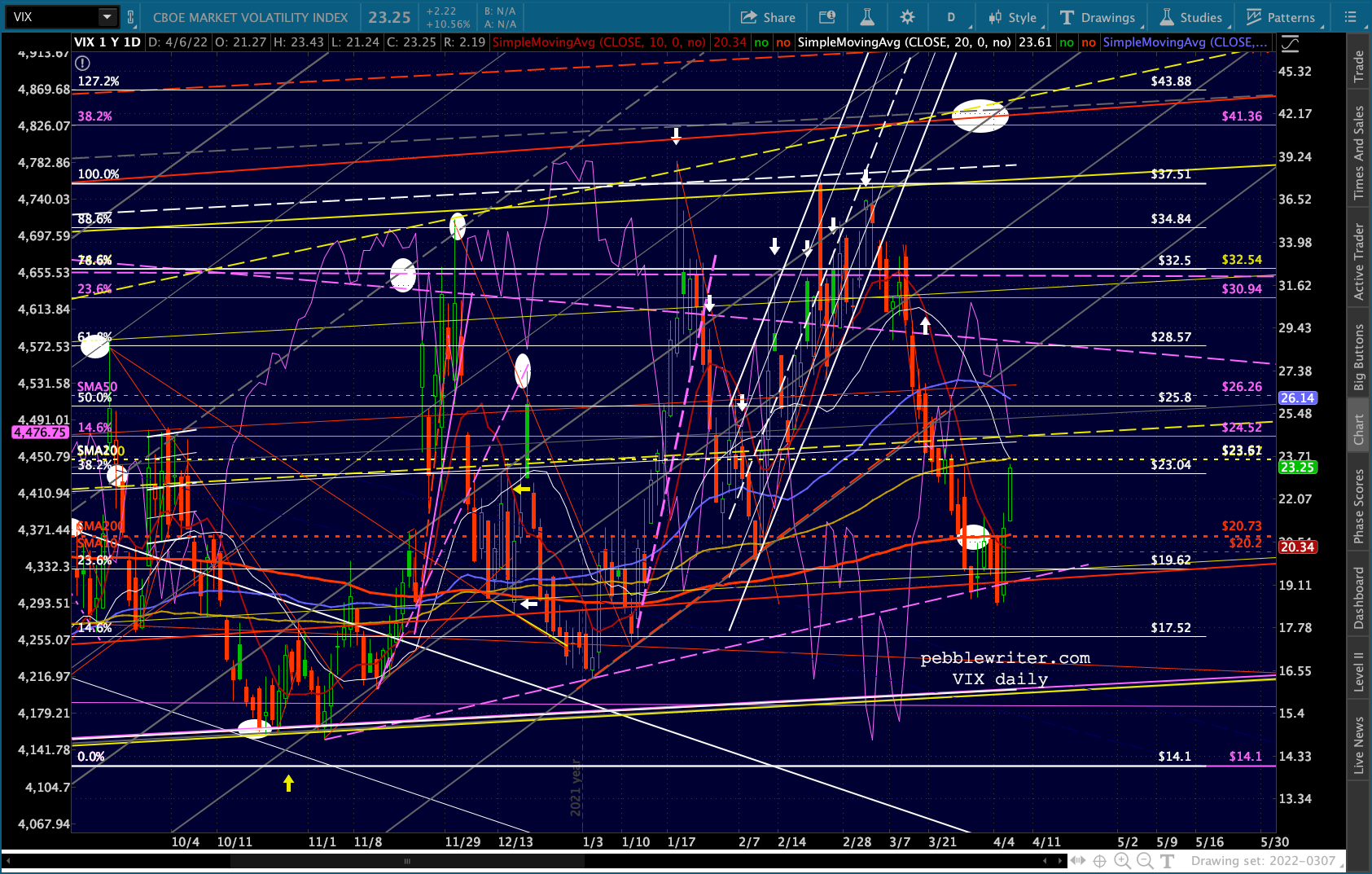

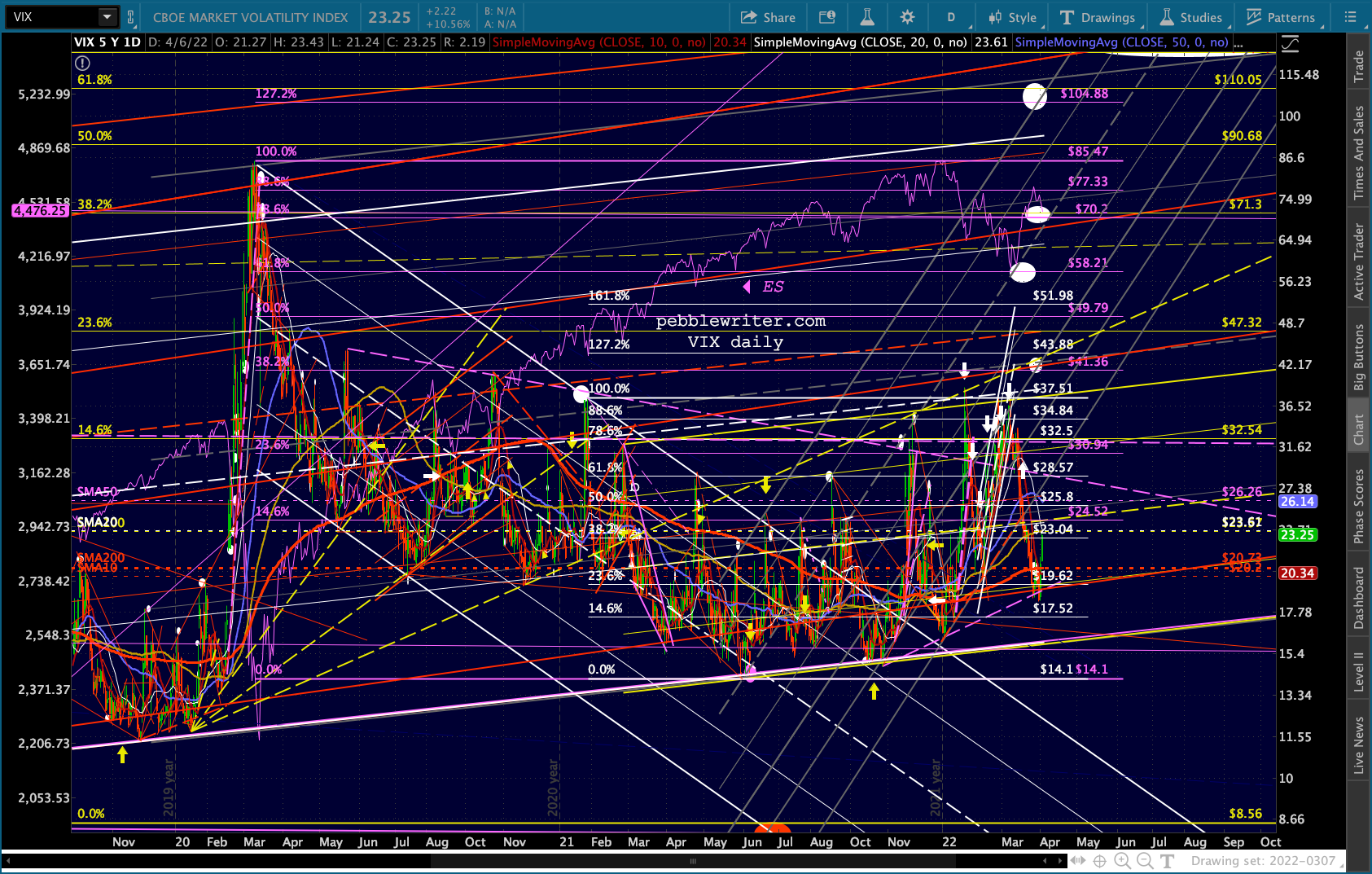

Futures are off sharply as we approach the open. Algos are responding to VIX’s pop back above its 200-DMA and the prospect of increasing Fed hawkishness.

As we pointed out yesterday, the 10Y has again reached the top of a well-formed channel dating back over 30 years. Its ongoing decline has provided much of the fuel for increasing stock, bond and real estate prices, though, reversals at the channel top have marked severe downturns. If the Fed prevents the 10Y from breaking out while continuing to raise short-term rates, the 2s10s will become even more inverted, validating recession forecasts. And, as we discussed last week [see: Should We Fear a Yield Curve Inversion?] the aftermath of these inversions has never been good for stocks.

If the Fed prevents the 10Y from breaking out while continuing to raise short-term rates, the 2s10s will become even more inverted, validating recession forecasts. And, as we discussed last week [see: Should We Fear a Yield Curve Inversion?] the aftermath of these inversions has never been good for stocks.

Bottom line, the Fed is damned if they do and damned if they don’t. The real question surrounding today’s minutes is whether members will sound as bewildered on paper as they have in person.

Bottom line, the Fed is damned if they do and damned if they don’t. The real question surrounding today’s minutes is whether members will sound as bewildered on paper as they have in person.

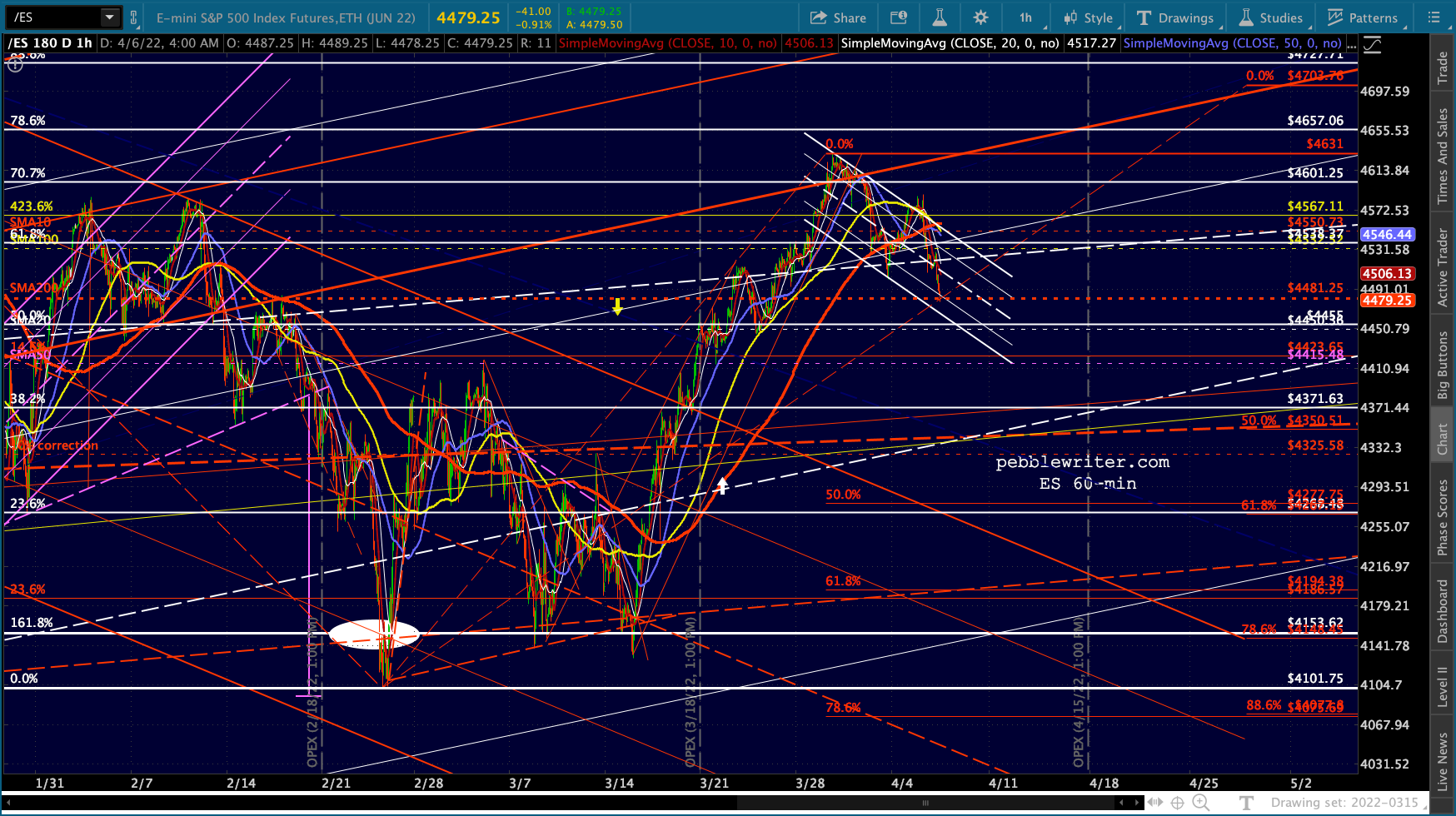

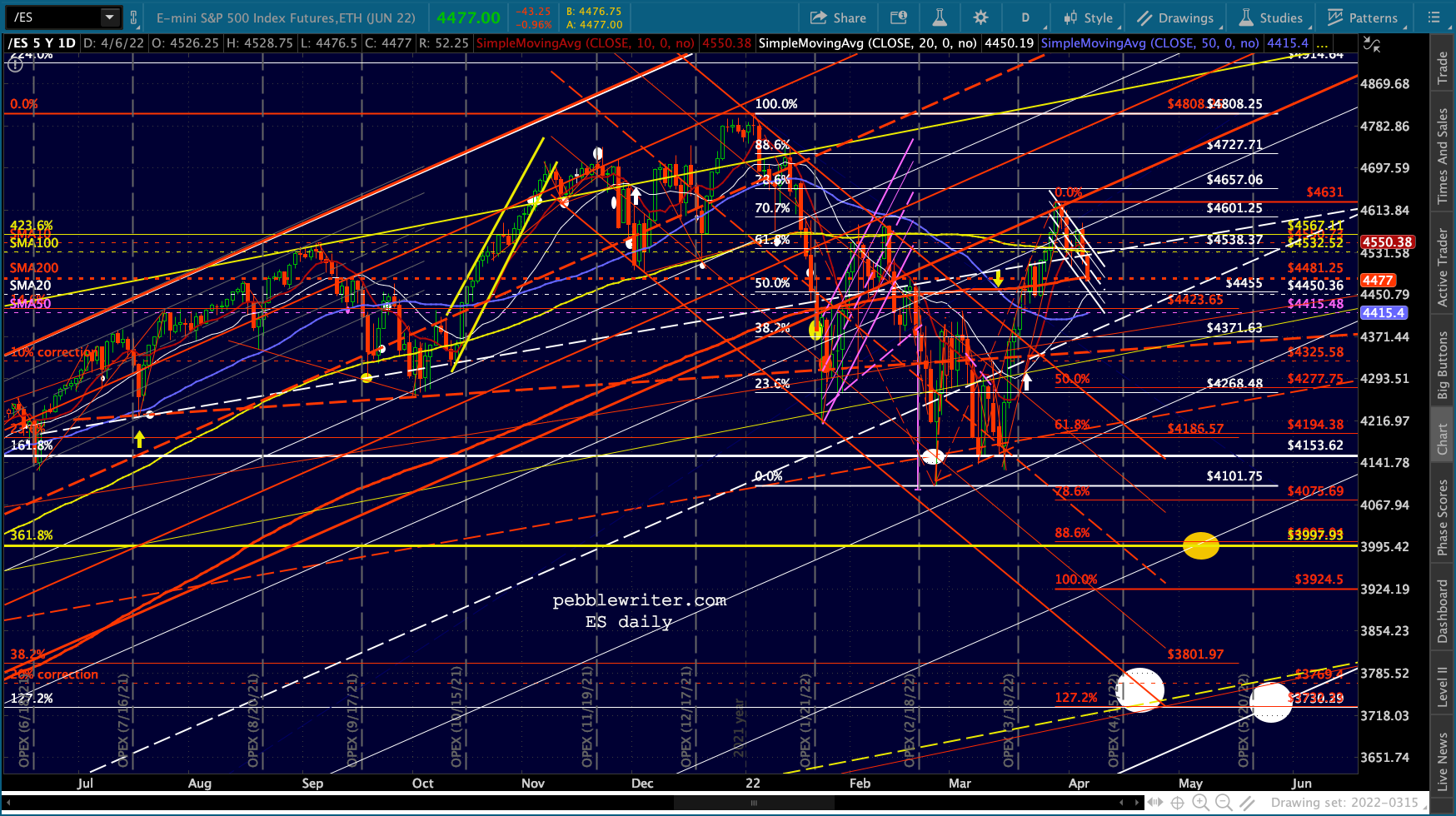

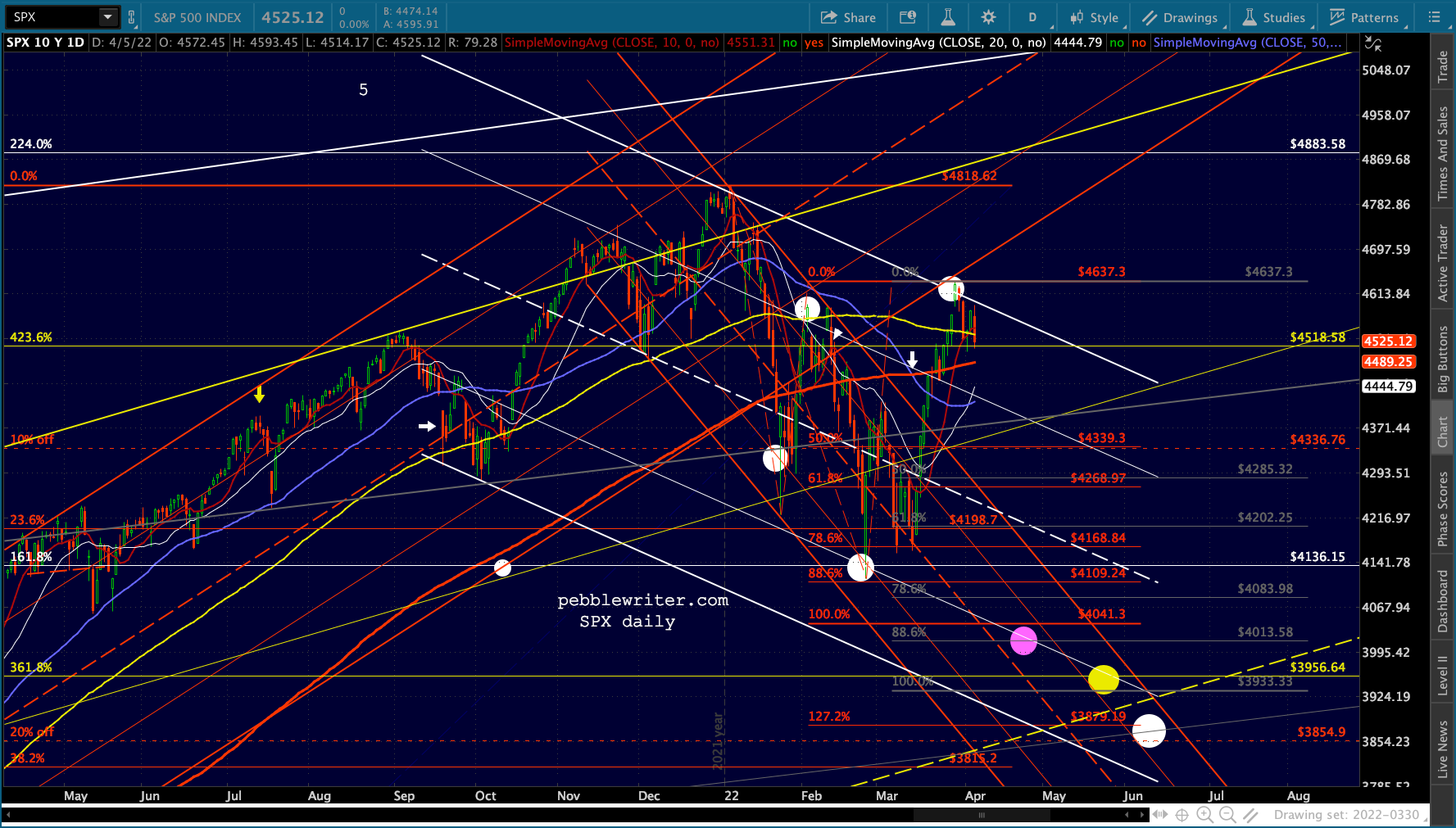

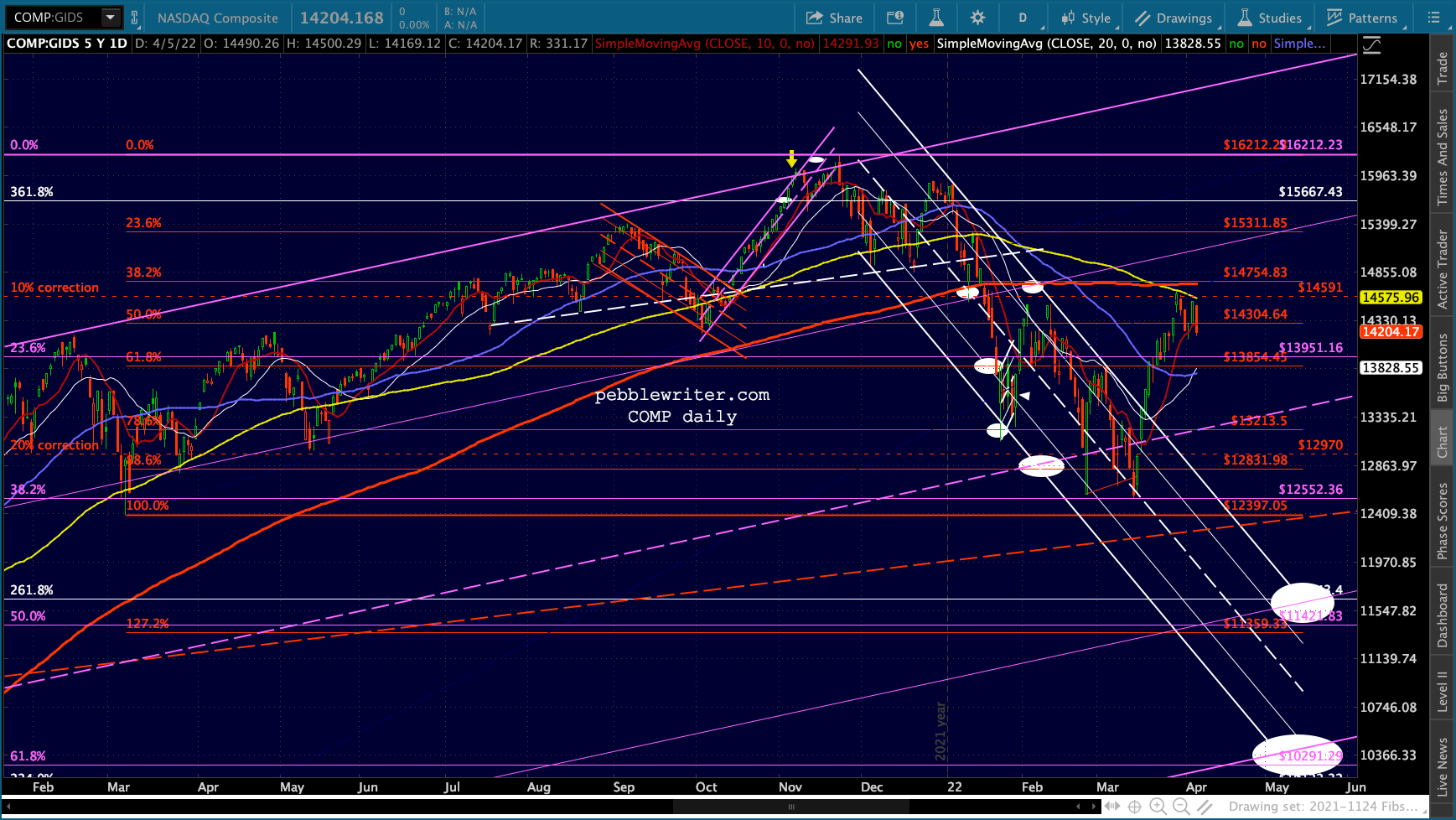

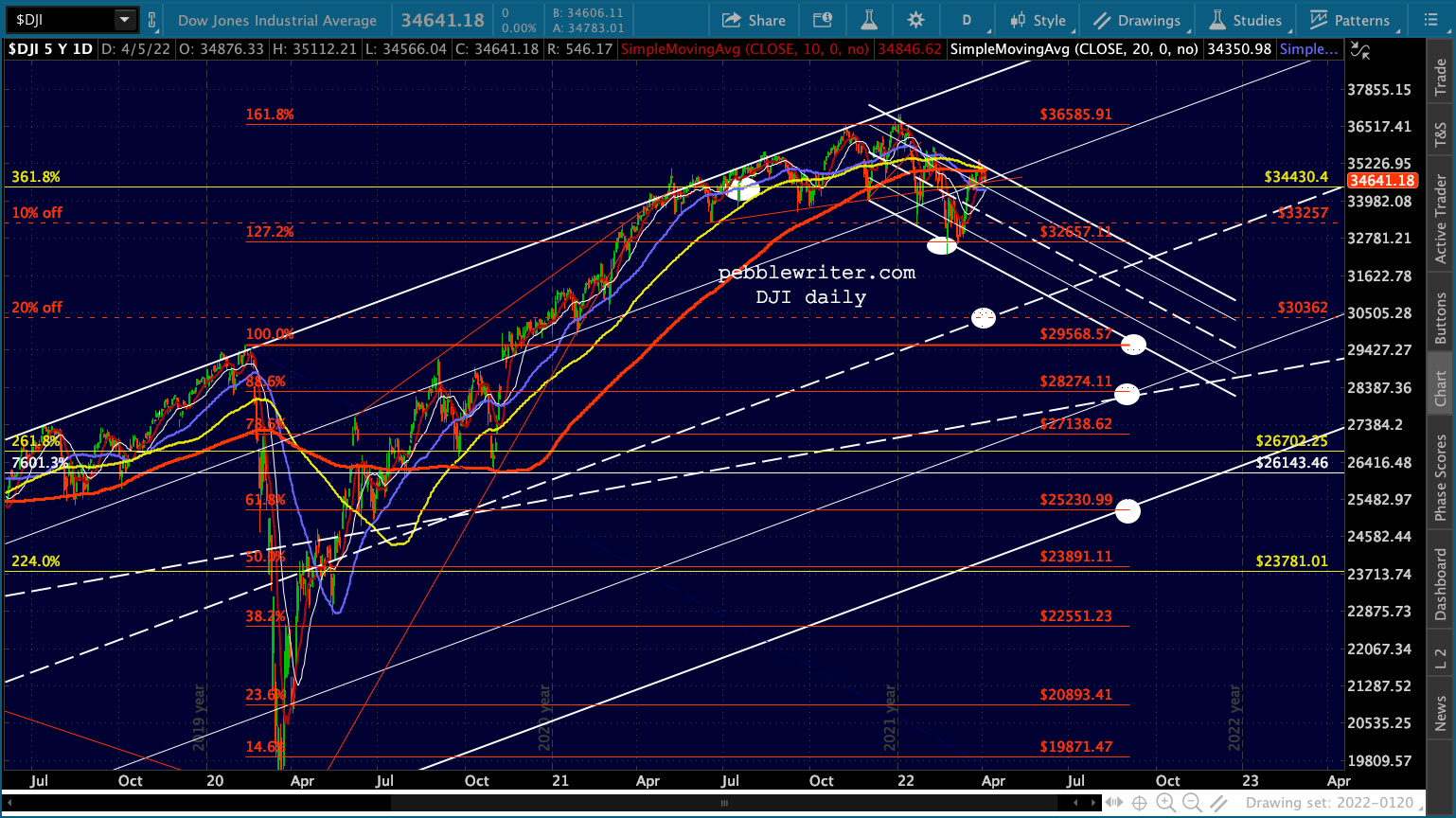

continued for members…The equity picture continues to look bearish, with ES’ test of its SMA200 today’s big event.

SPX already closed below its SMA200 yesterday.

SPX already closed below its SMA200 yesterday.

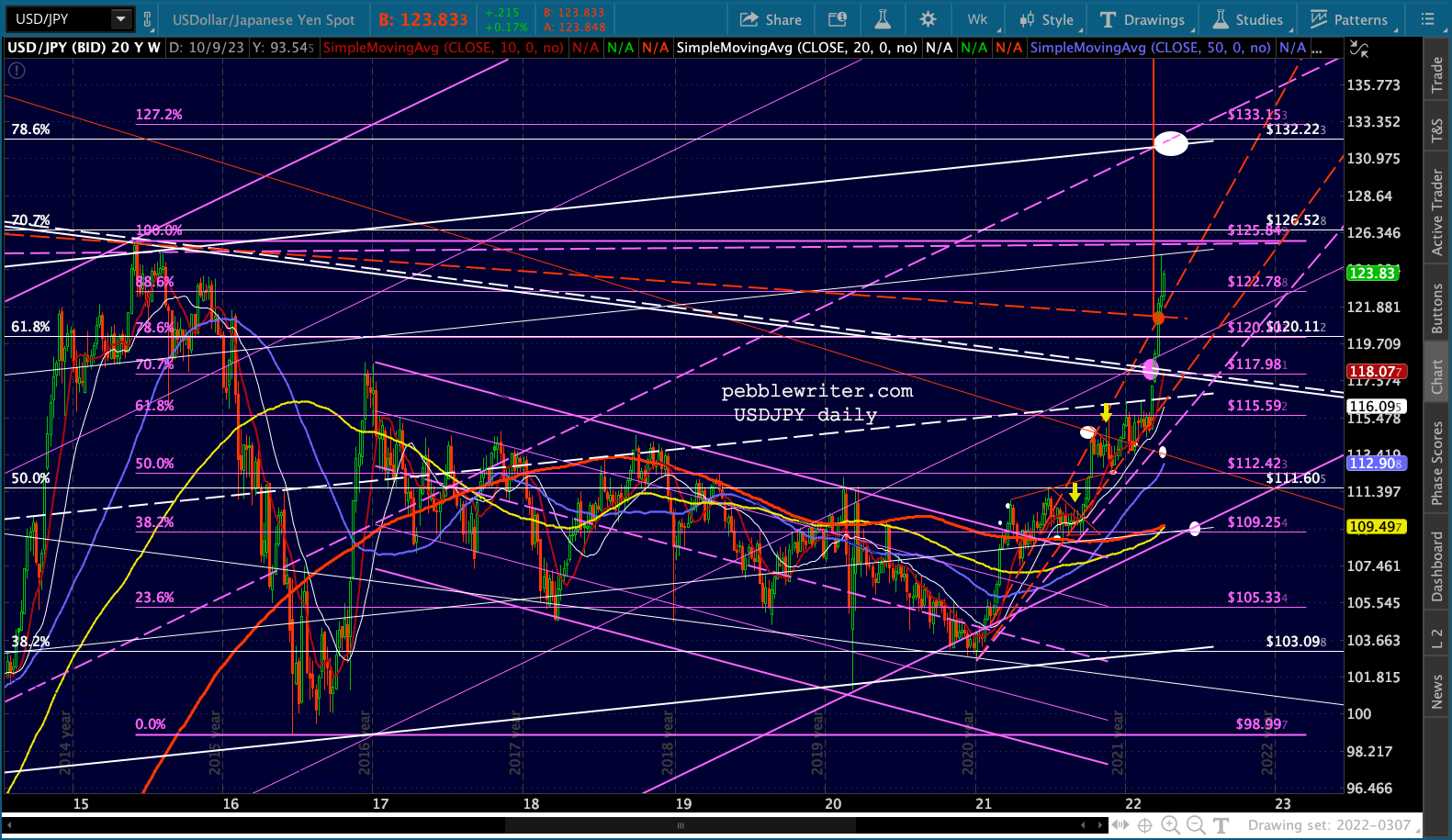

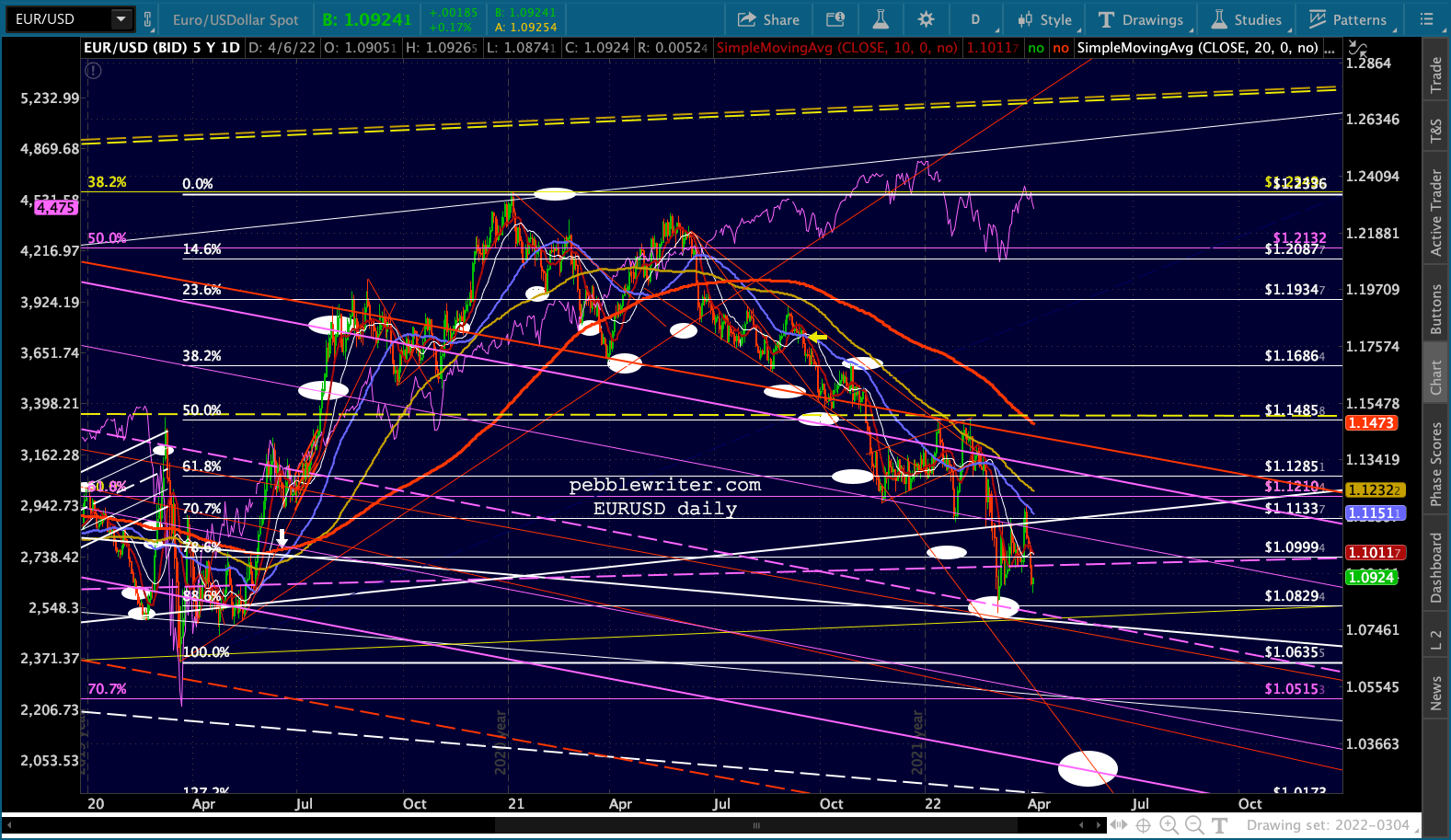

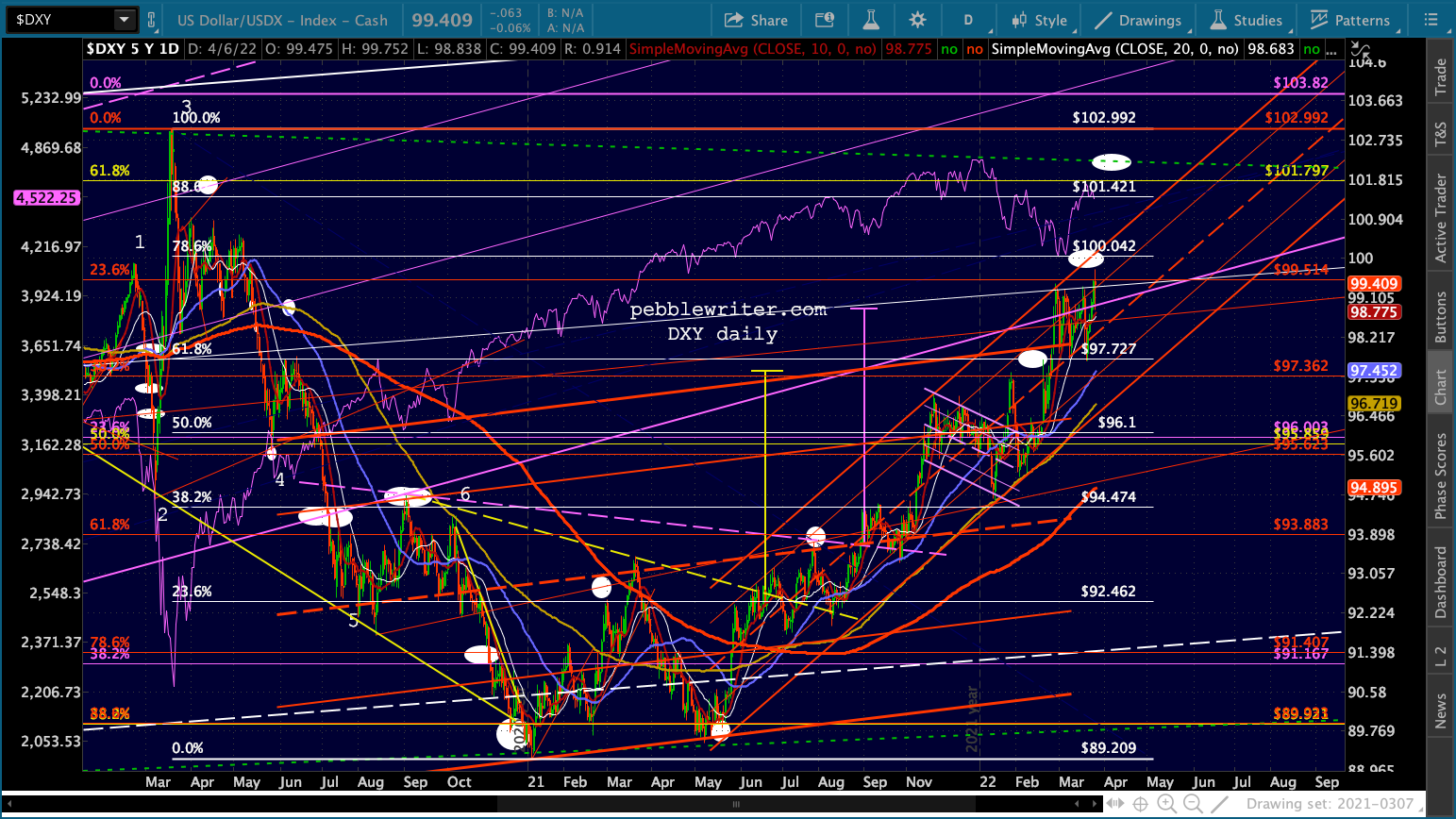

While USDJPY continues higher, EURUSD has not. DXY is closing in on our 100.042 target.

While USDJPY continues higher, EURUSD has not. DXY is closing in on our 100.042 target.

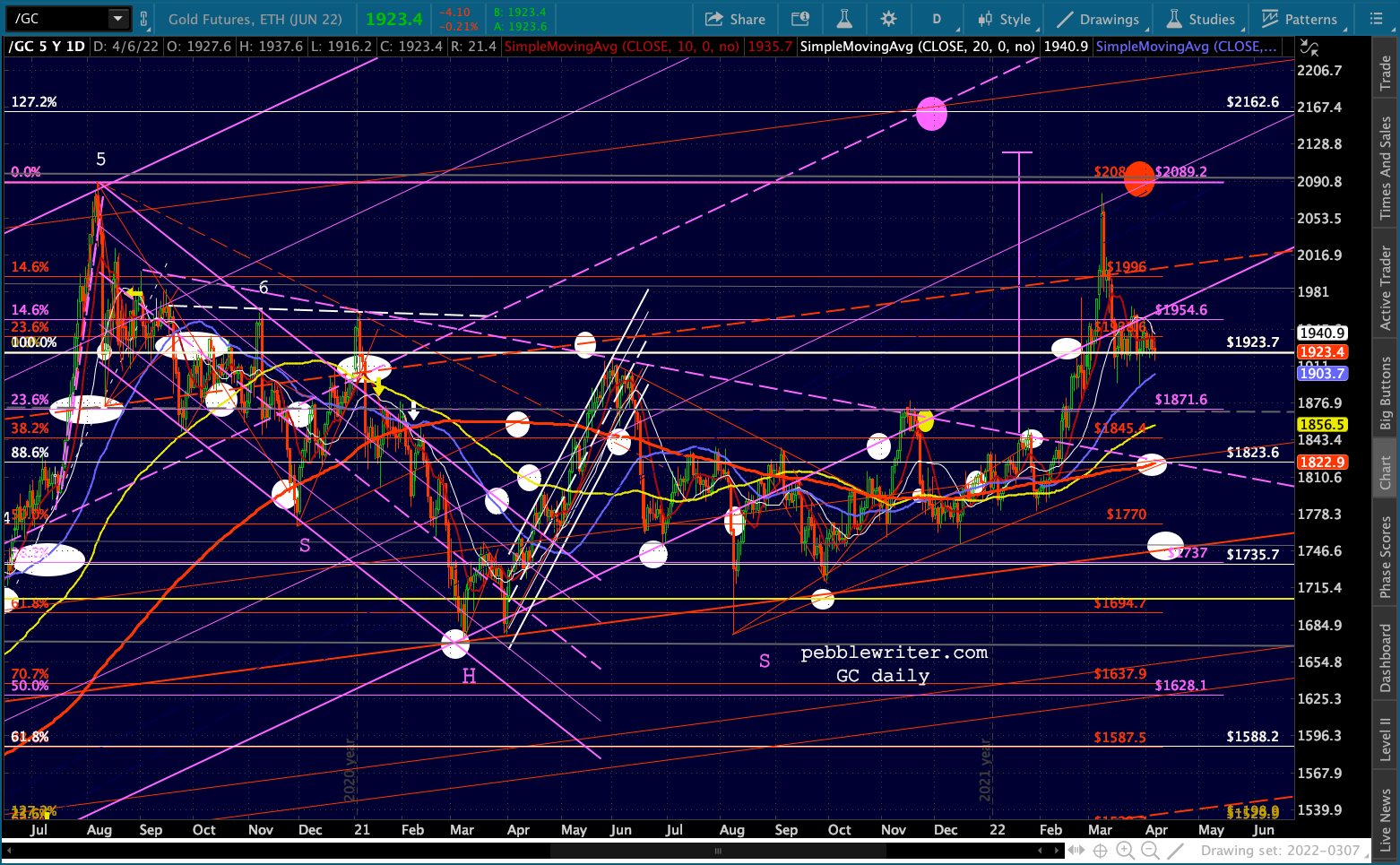

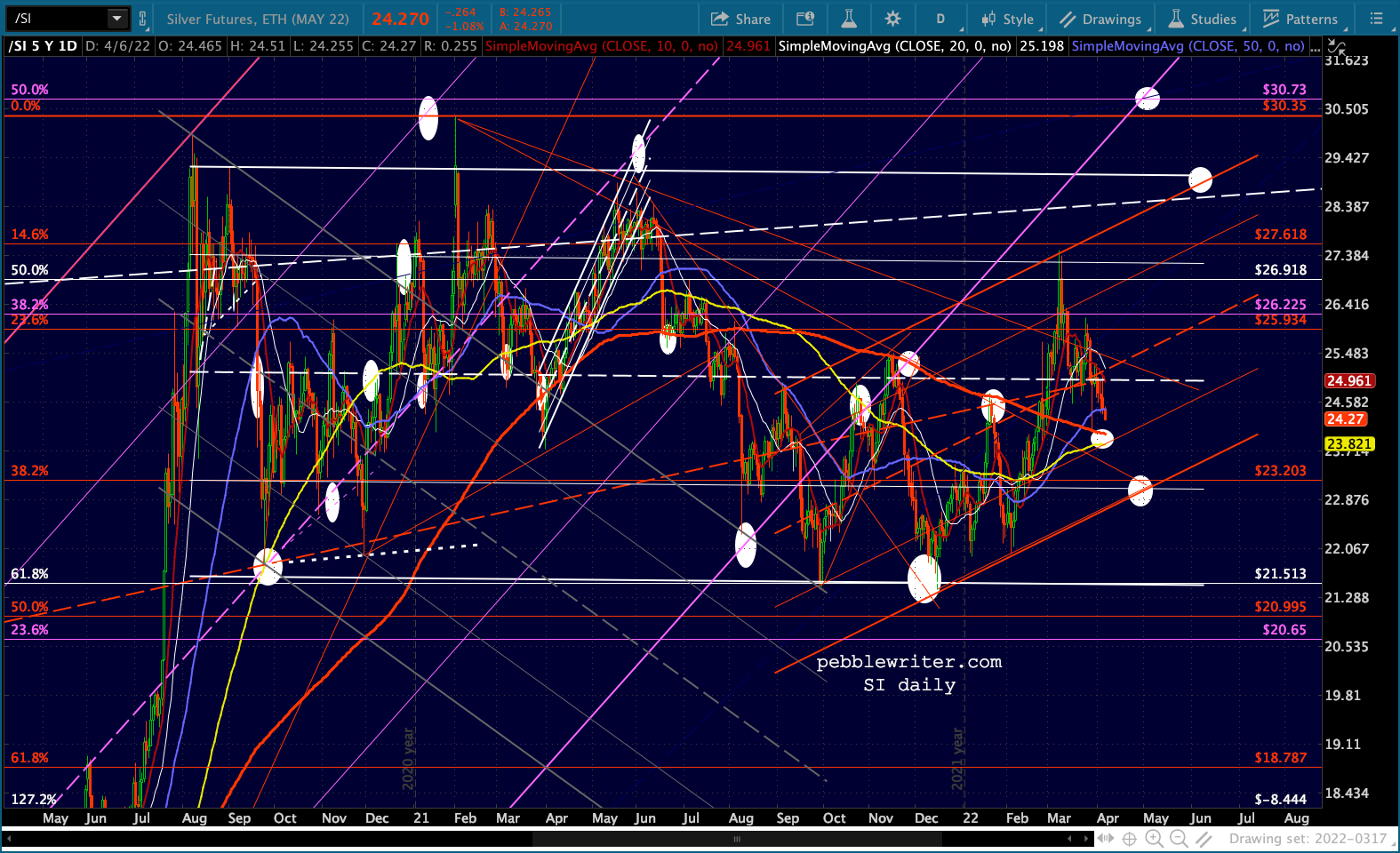

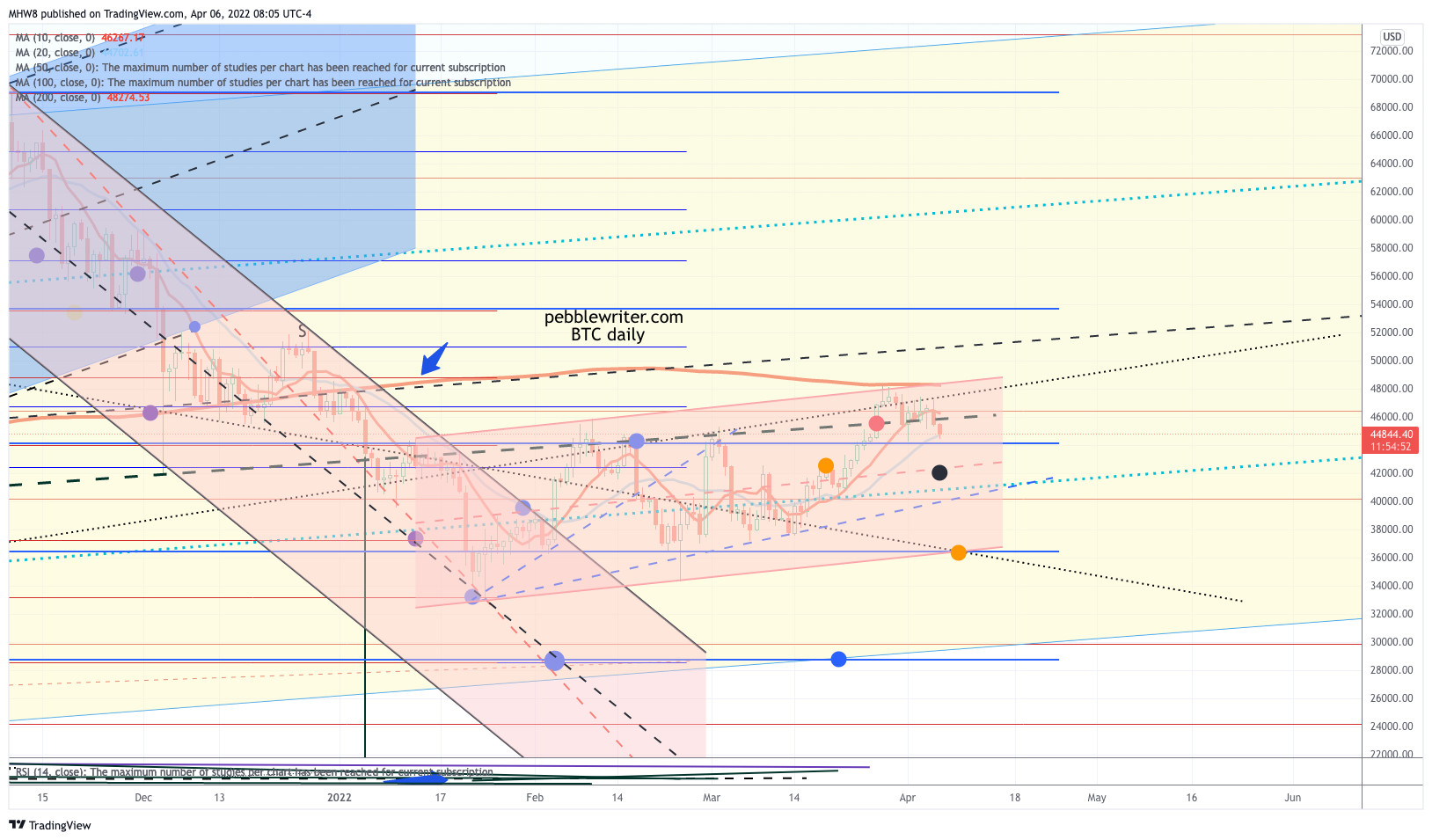

GC, SI and BTC continue to backtest.

GC, SI and BTC continue to backtest.

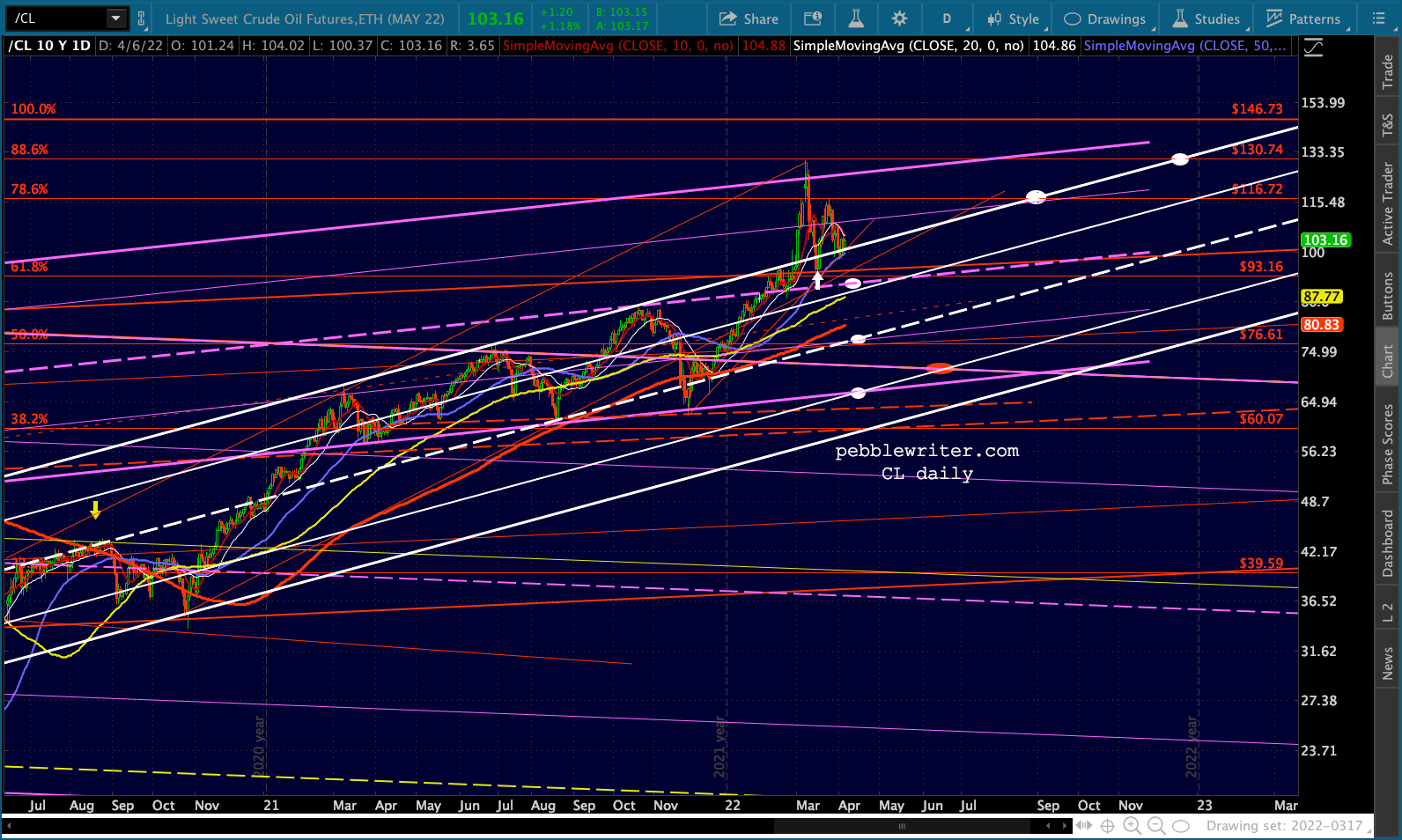

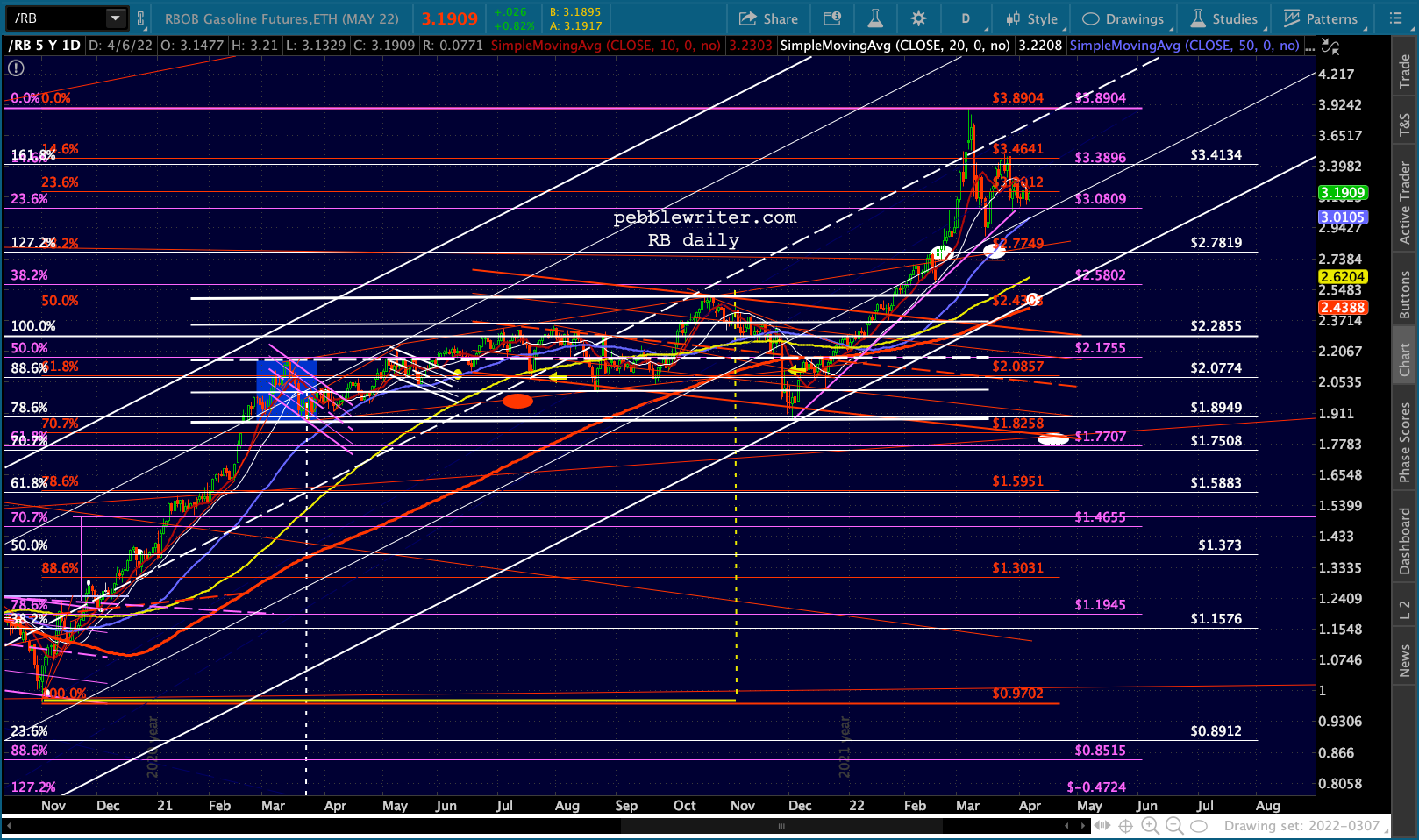

CL and RB are up moderately today, but oil company CEOs are due to testify before Congress today. It will be interesting to see how they deflect re rising profitability amidst severe pain at the pump.

CL and RB are up moderately today, but oil company CEOs are due to testify before Congress today. It will be interesting to see how they deflect re rising profitability amidst severe pain at the pump.