We’re starting to see cracks in the equities and bond markets related to the debt ceiling. Interest rates are ratcheting higher. And, although OPEX-related maneuvers are working to prop up stocks, we had a momentary breakdown in SPX yesterday.

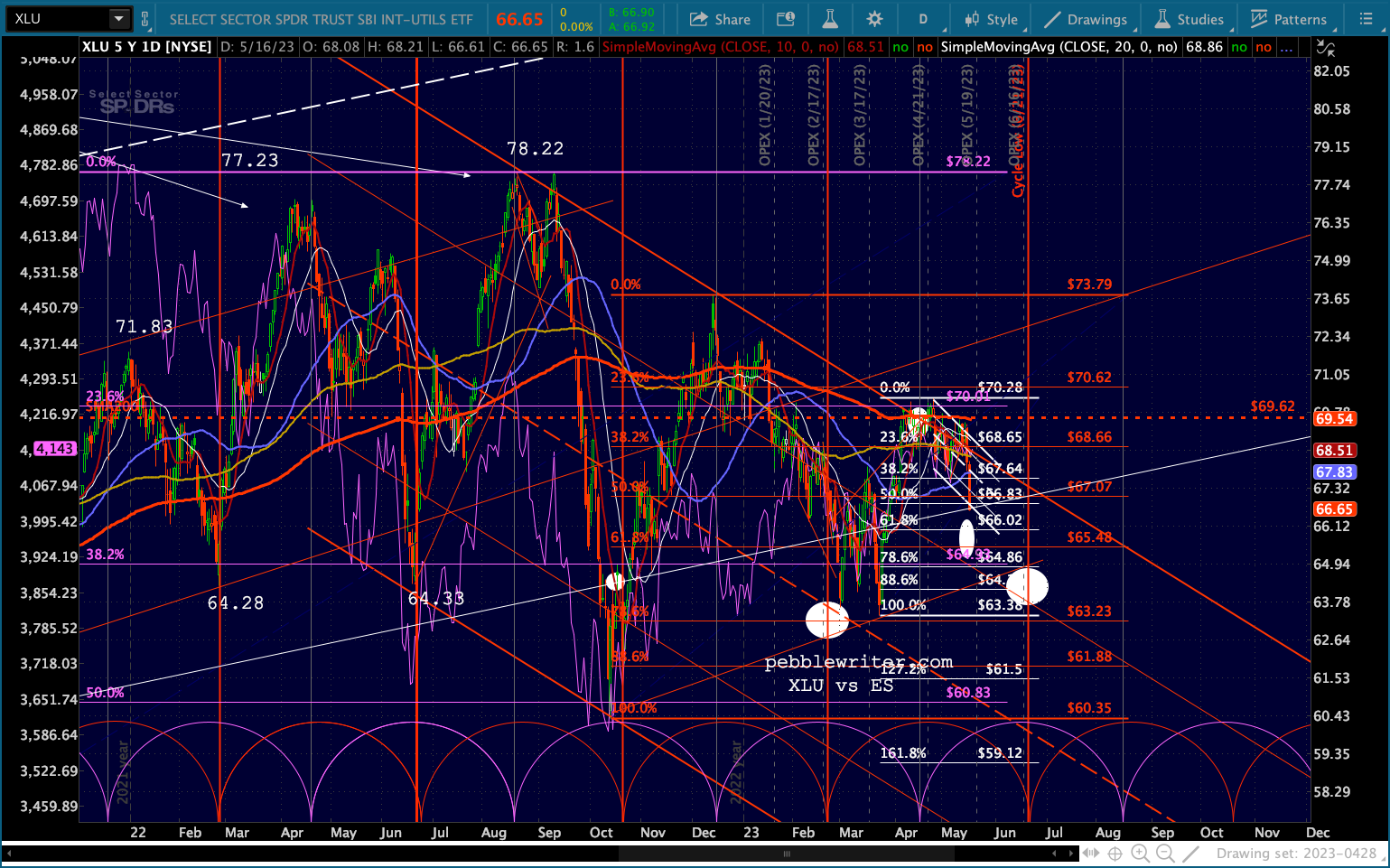

Utilities, a bond proxy for some, have taken a big hit this week as investors shift into shorter-term, less volatile treasuries.

Utilities, a bond proxy for some, have taken a big hit this week as investors shift into shorter-term, less volatile treasuries.

Which would you rather own, XLU with a beta of .56 and yield of 3.01% or a 6-mo Tsy paying 5.25%?

continued for members…

Remember, we’re looking for potentially much lower prices in XLU. In any case, our model calls for a cycle low around June 20.

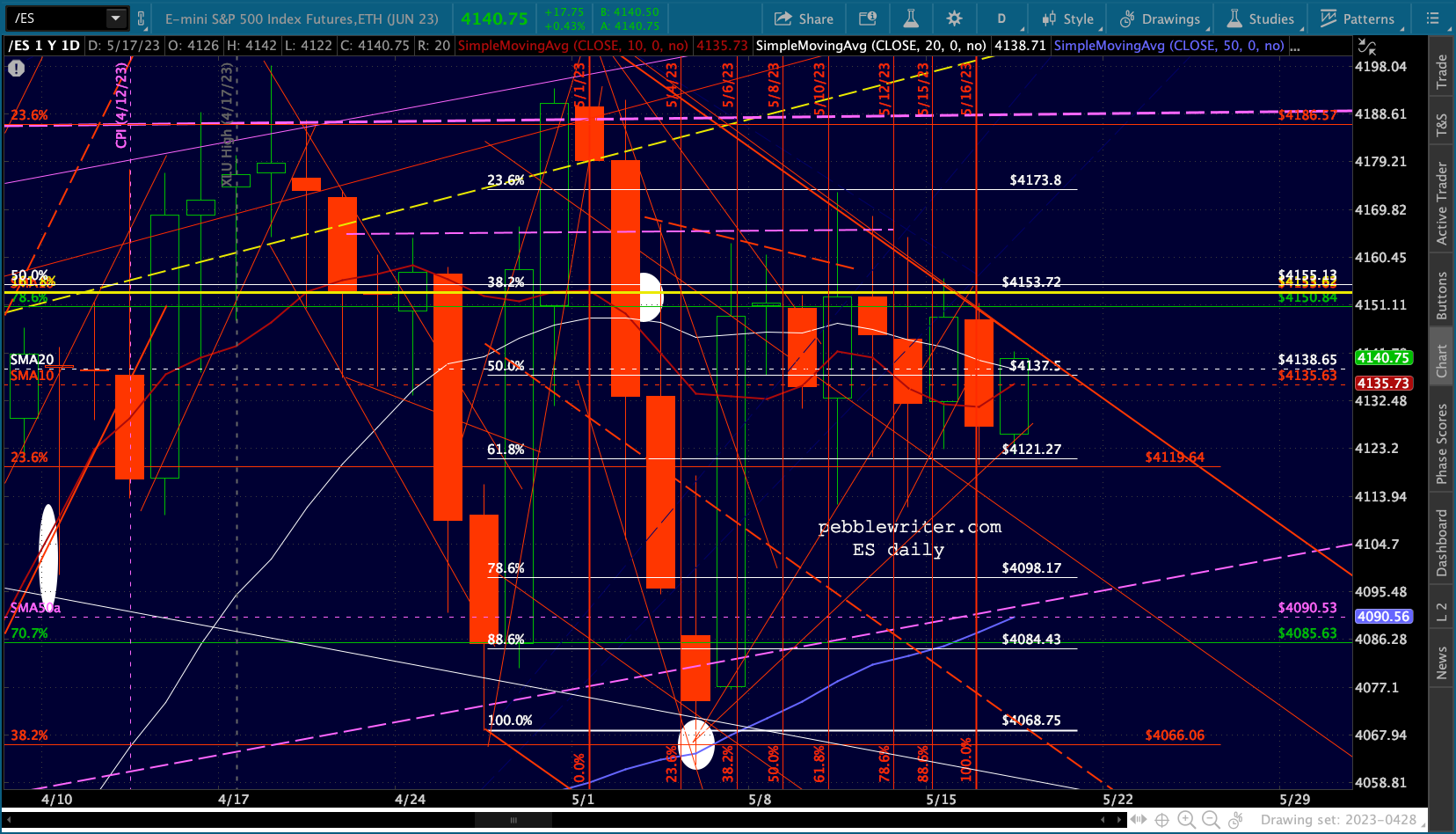

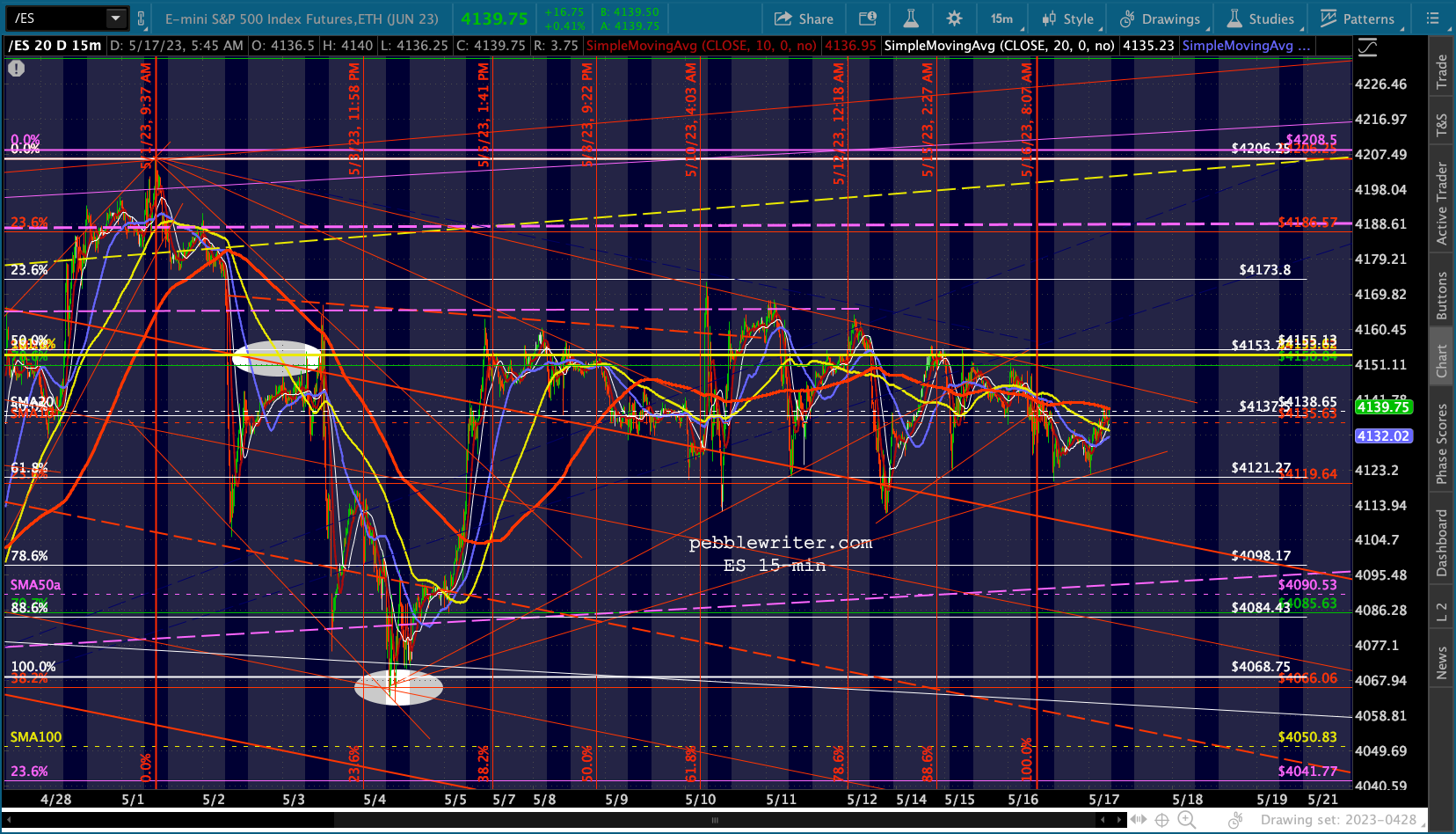

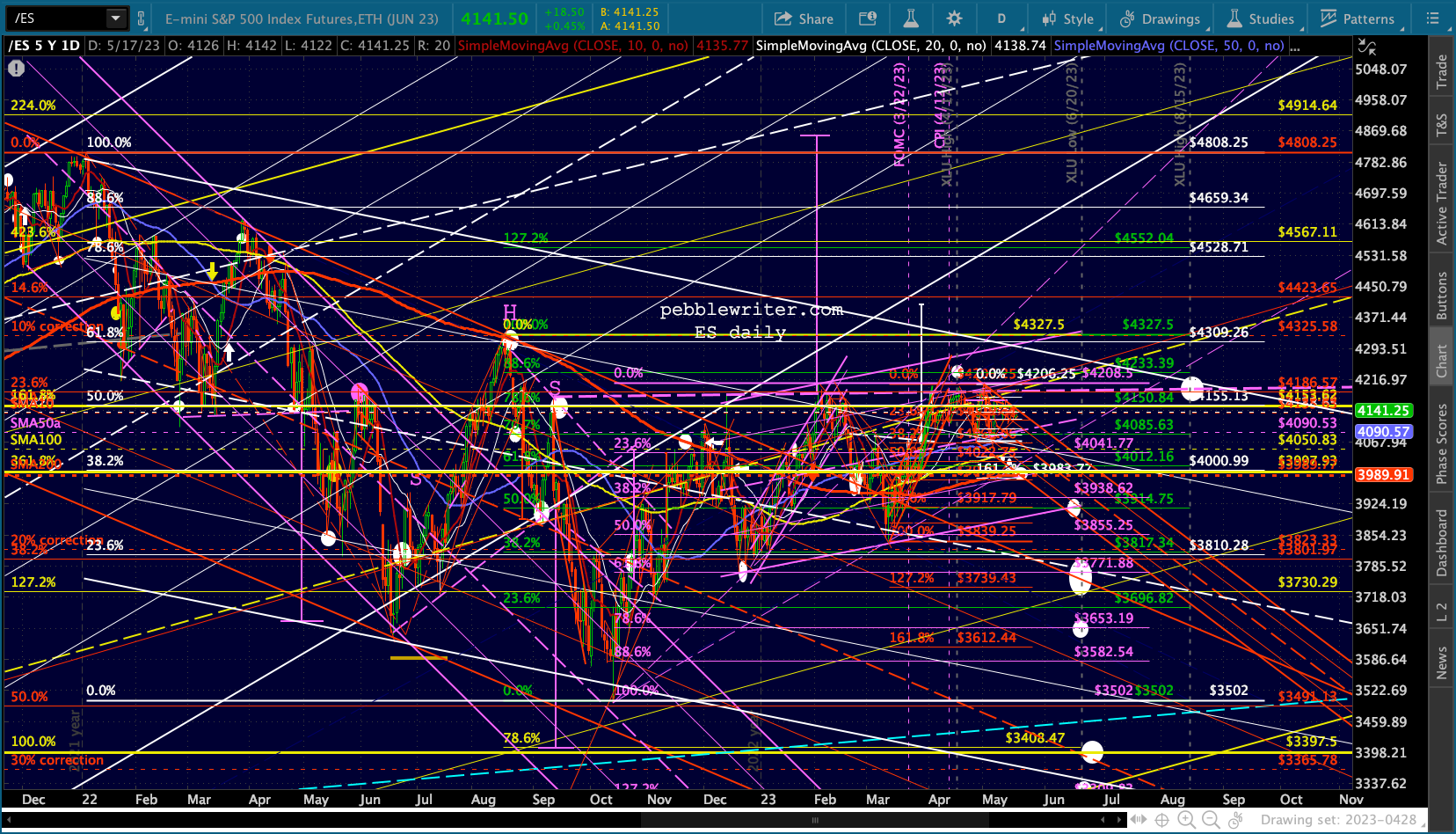

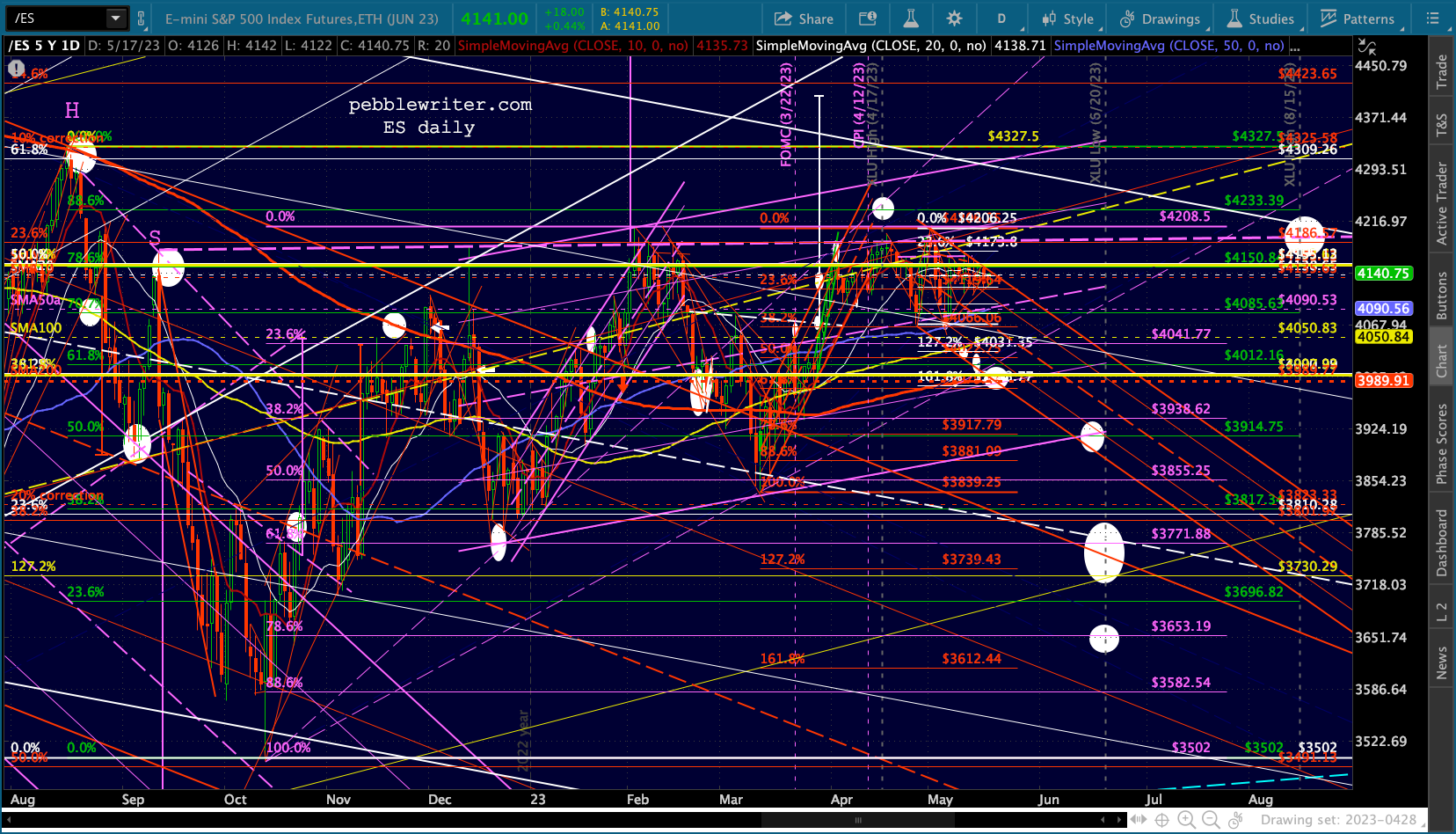

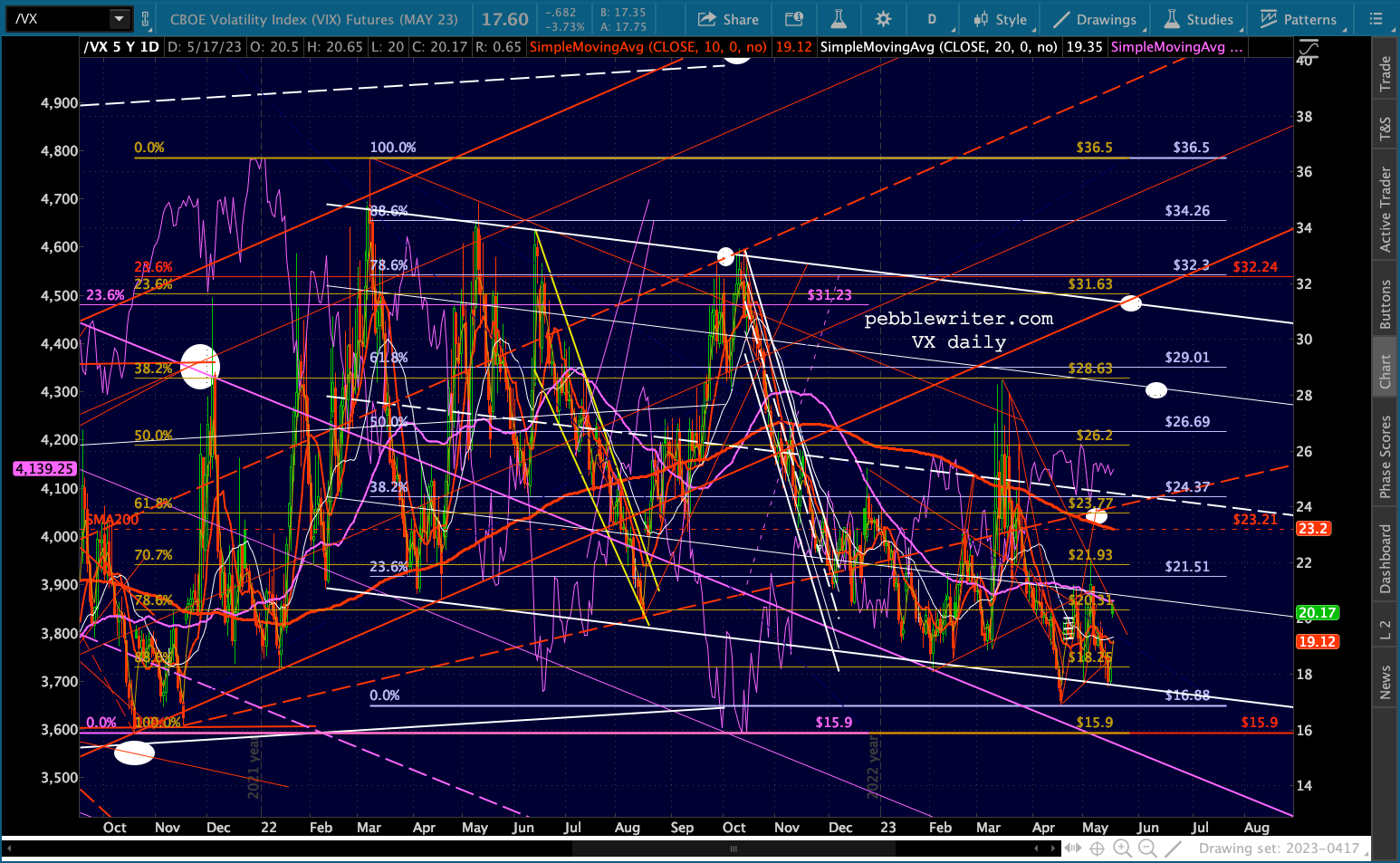

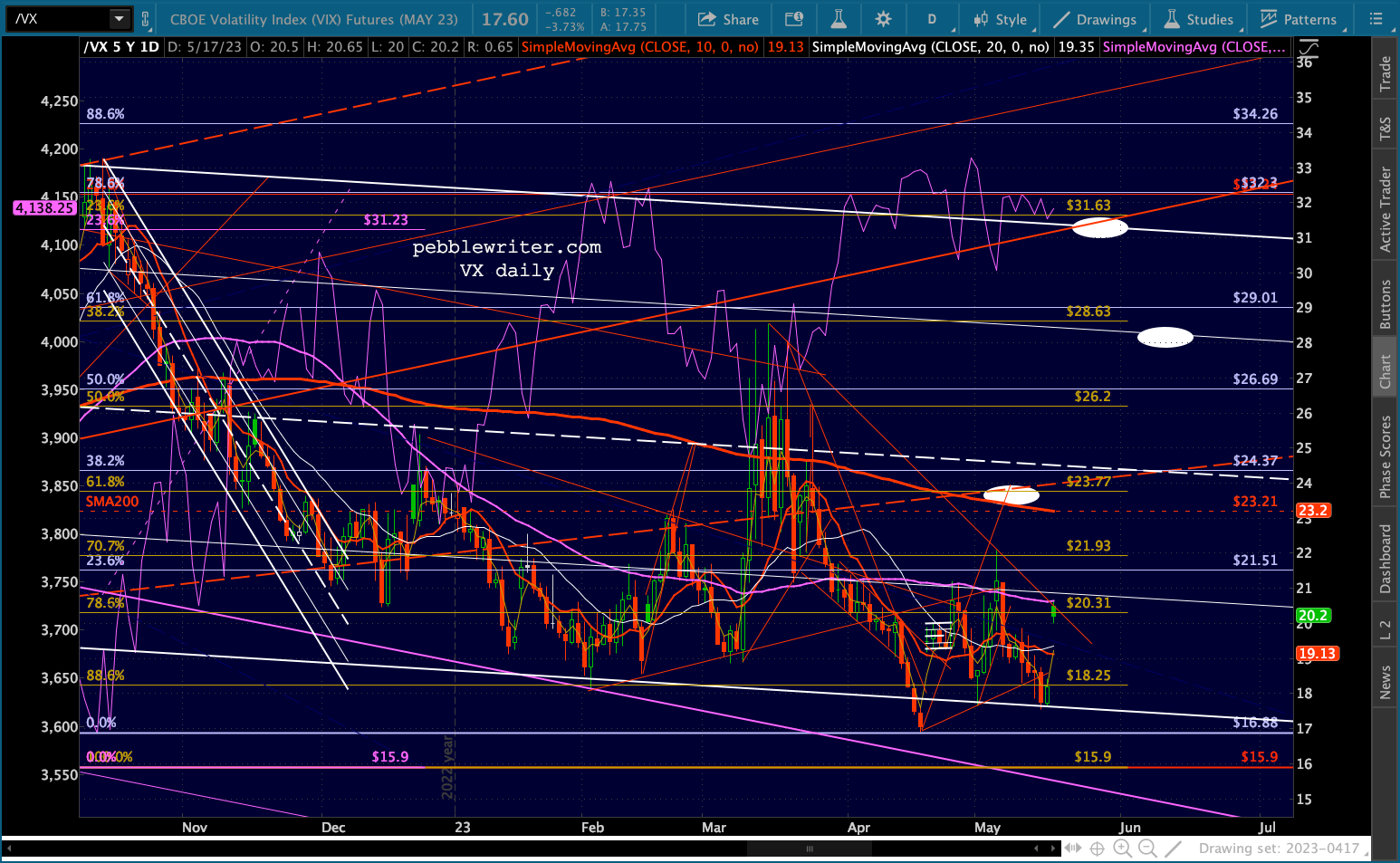

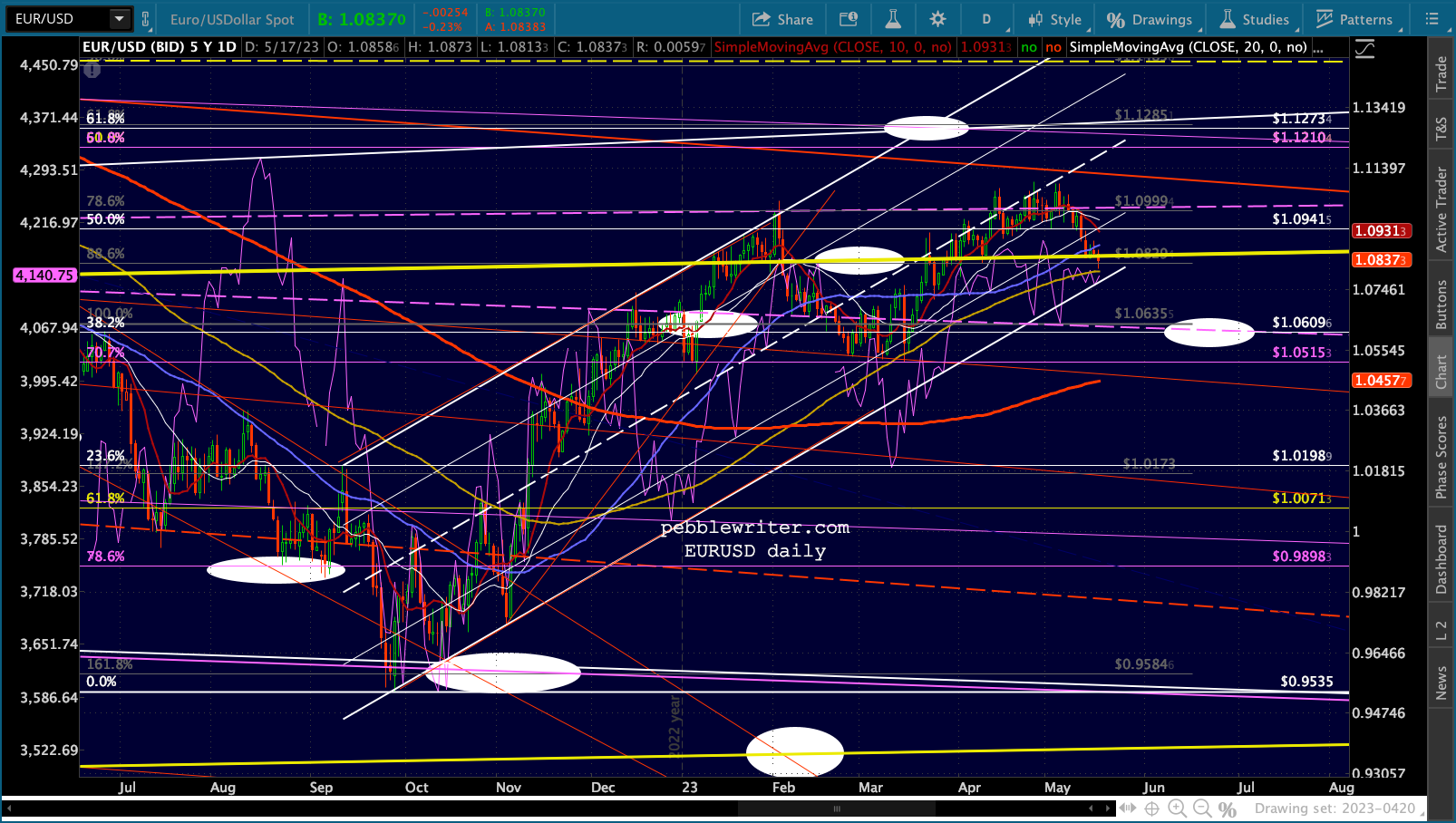

The rest of today’s charts:

The rest of today’s charts:

Note that the SMA10 remains below the SMA20, but it’s not by much. Futures have pushed back above both overnight. Another longer triangle has formed that enables ES to continue sideways as long as VIX and currencies cooperate. Note that I have adjusted the falling red channel to match the May 1 highs.

Another longer triangle has formed that enables ES to continue sideways as long as VIX and currencies cooperate. Note that I have adjusted the falling red channel to match the May 1 highs.

Note that VX stalled at a fan line from Mar 15 and its SMA50 – for now.

Note that VX stalled at a fan line from Mar 15 and its SMA50 – for now.

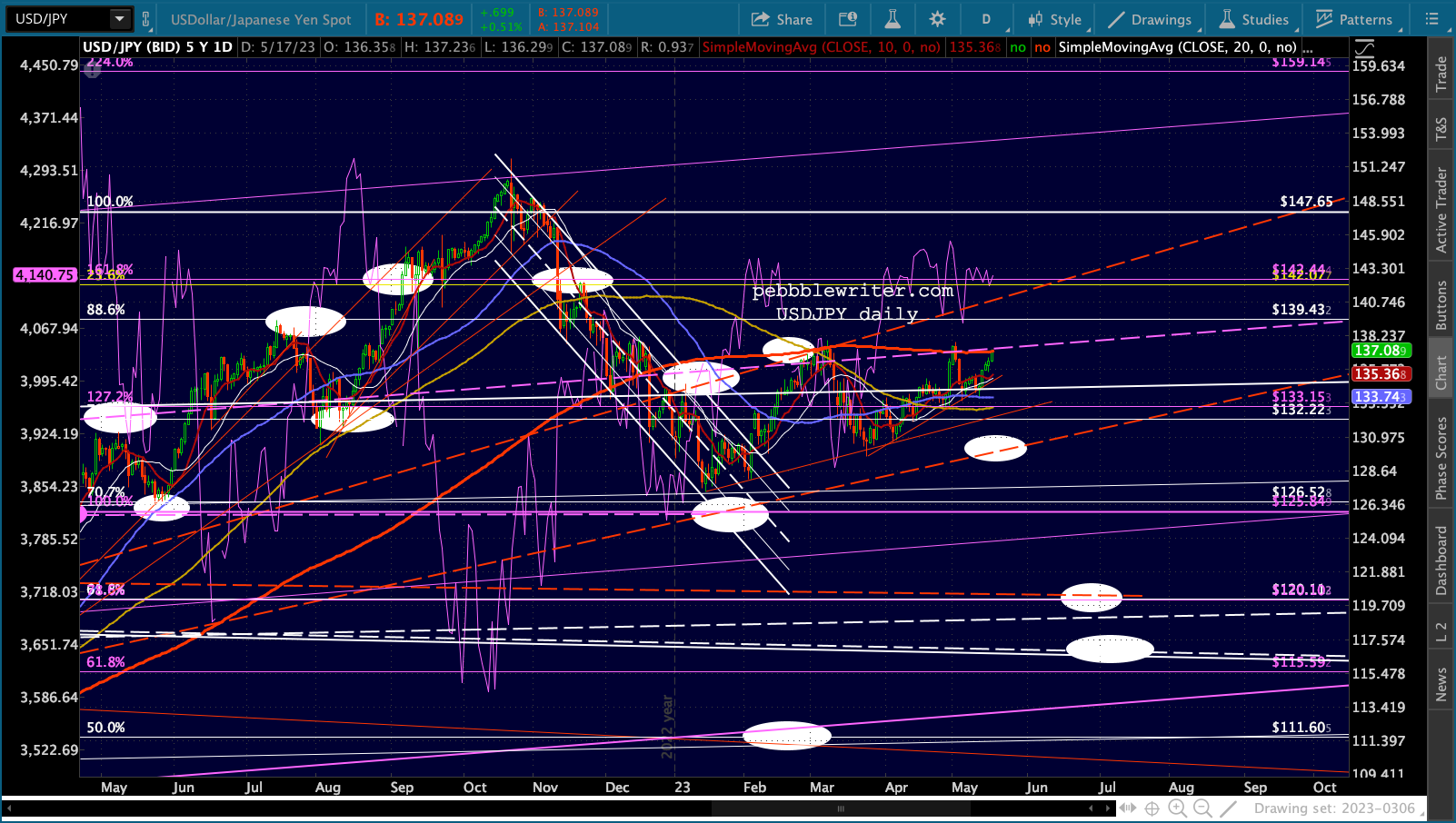

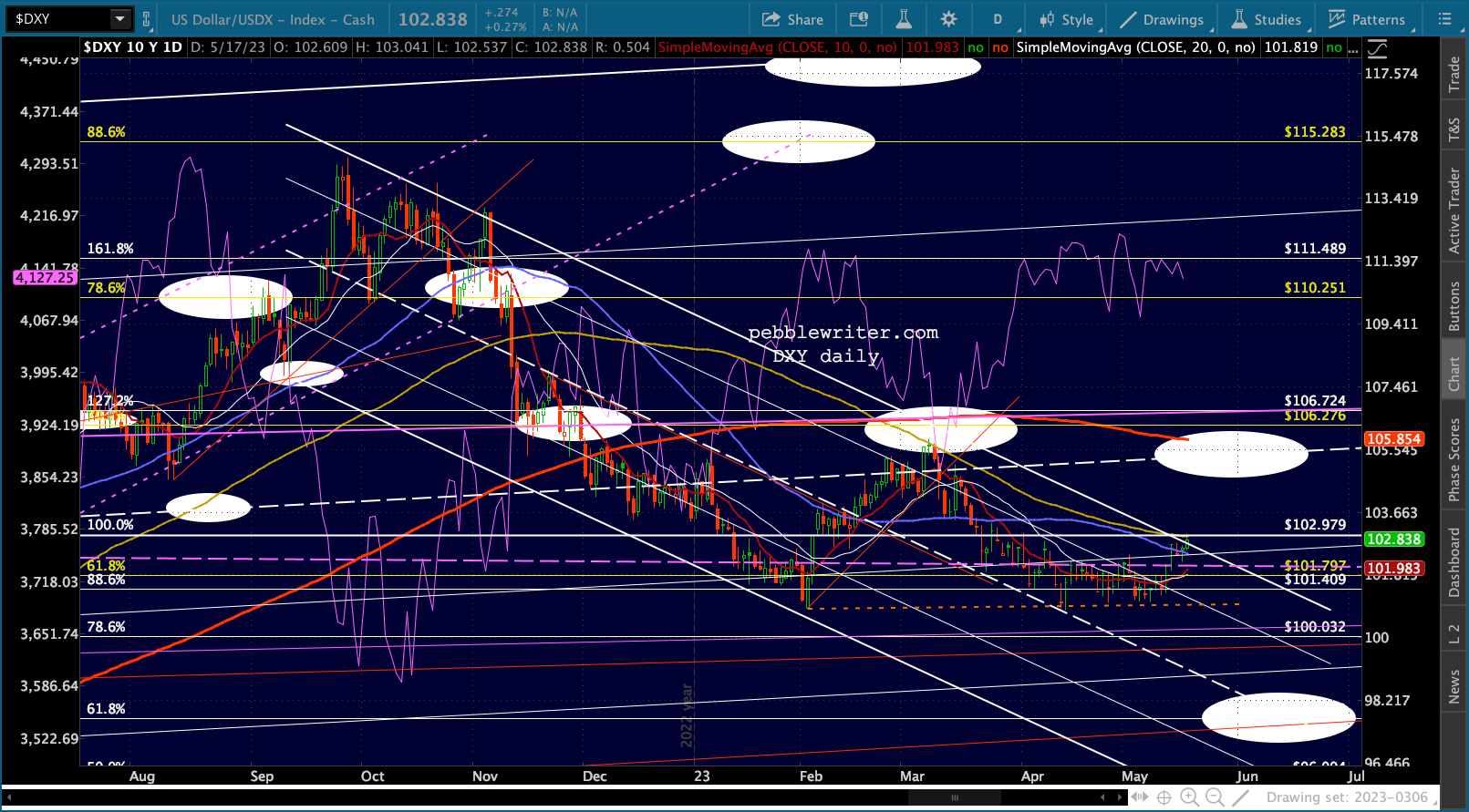

Currencies favor the DXY today, meaning we’re seeing a potential breakout – generally bearish for stocks…

Currencies favor the DXY today, meaning we’re seeing a potential breakout – generally bearish for stocks…

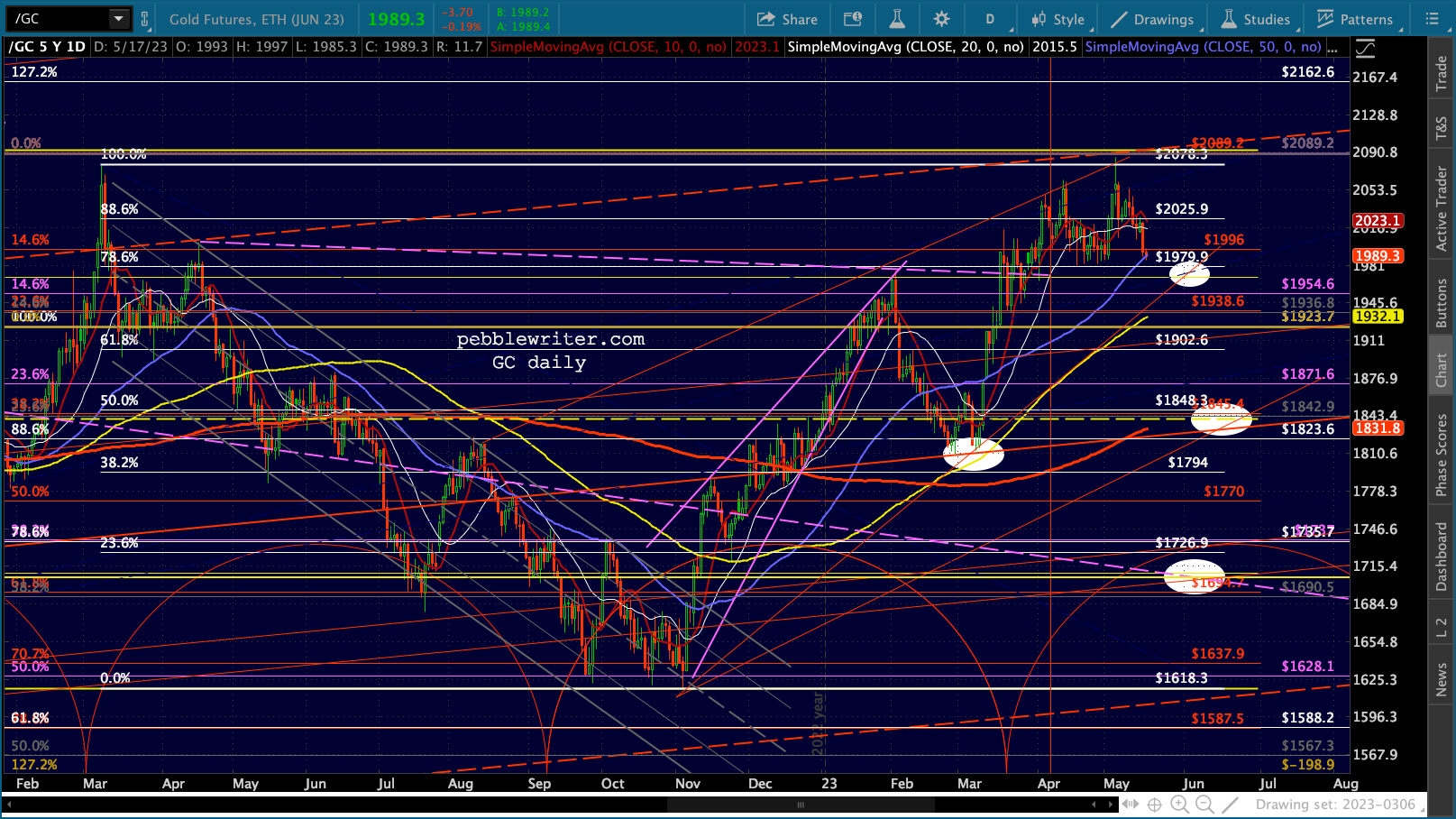

…and definitely bearish for GC, SI and BTC.

…and definitely bearish for GC, SI and BTC.

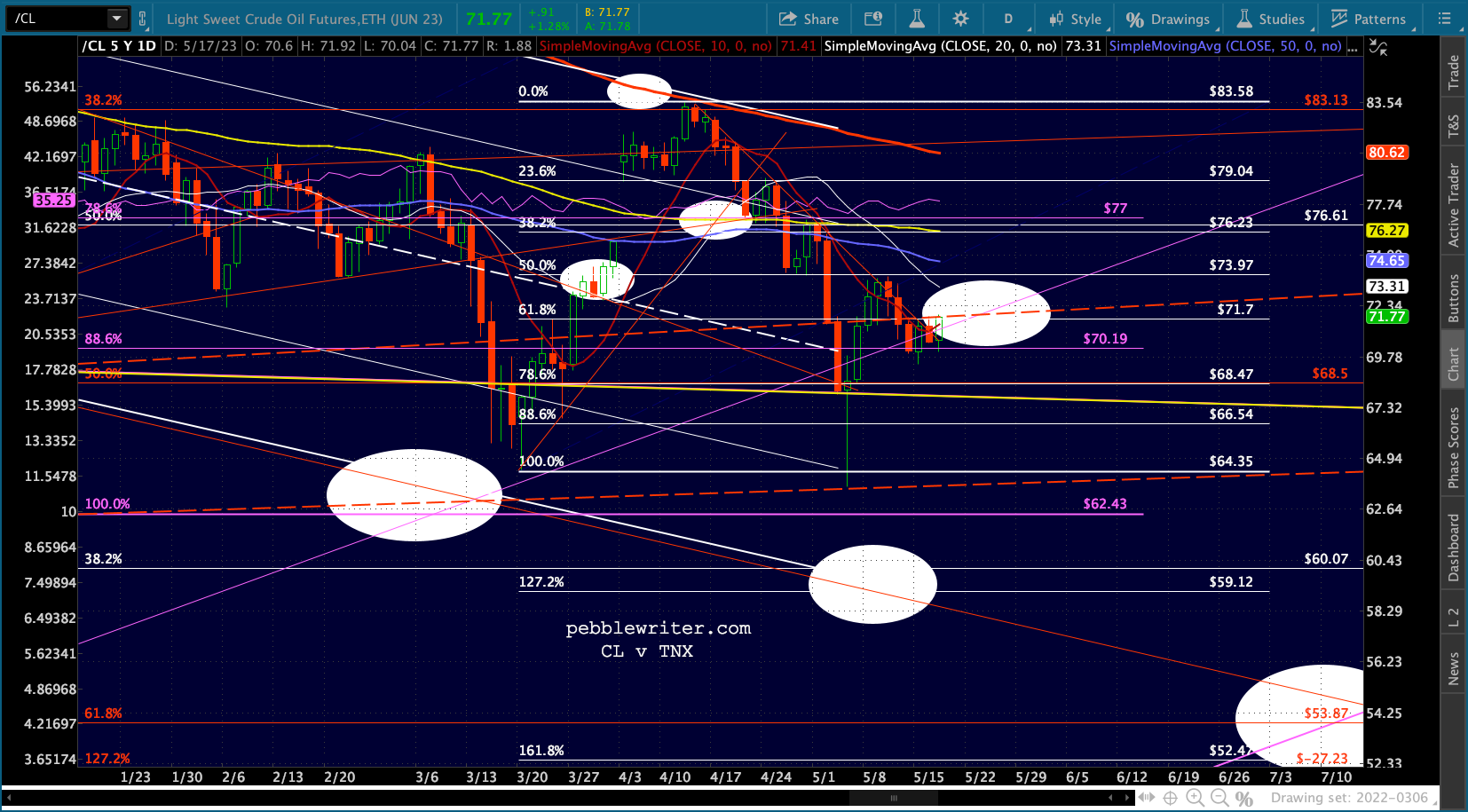

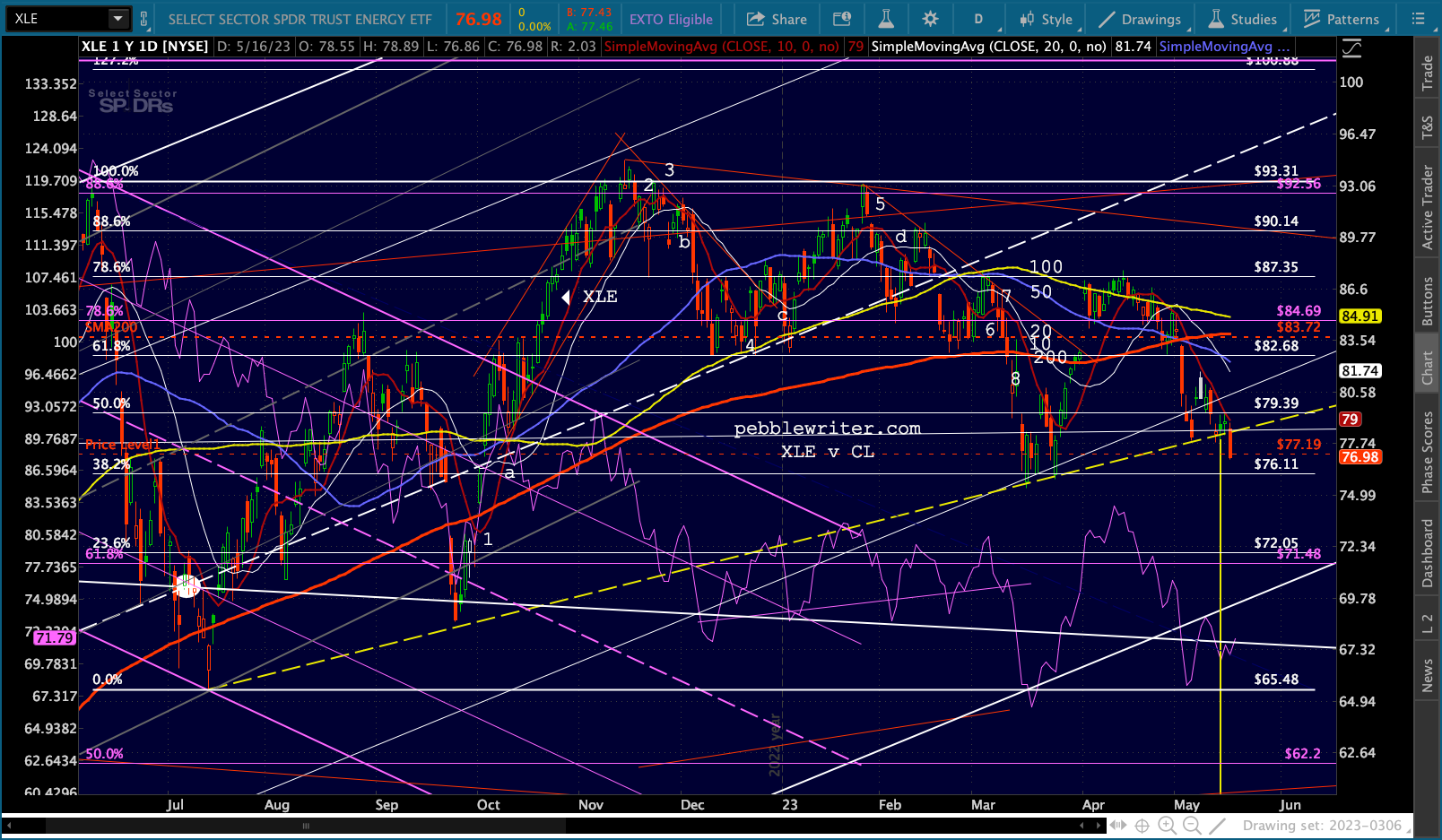

CL and RB are getting a nice 1%+ bounce today…

CL and RB are getting a nice 1%+ bounce today…

…but, XLE definitely broke down yesterday. And, even its small bounce hasn’t been enough to undo the breakdown.

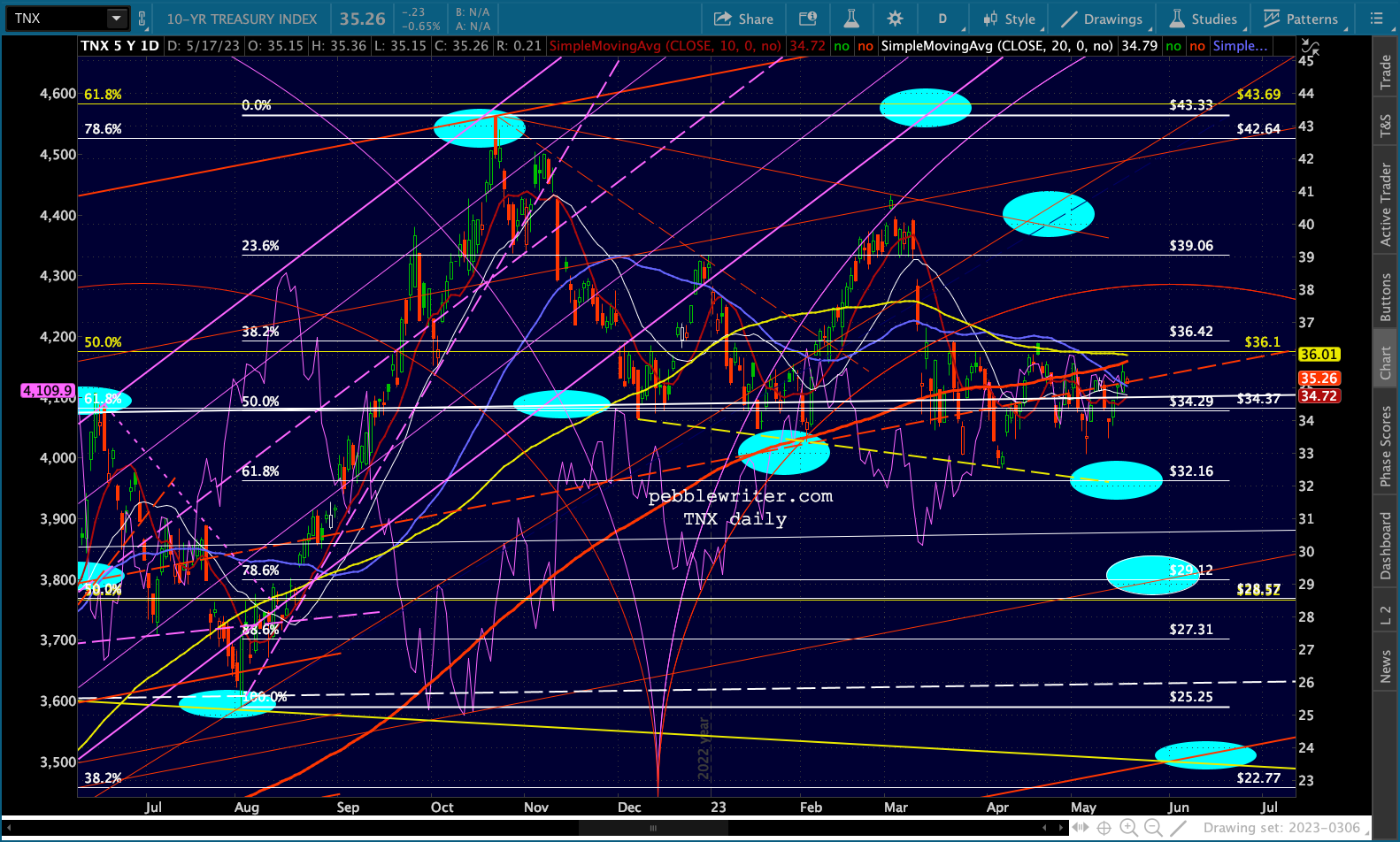

…but, XLE definitely broke down yesterday. And, even its small bounce hasn’t been enough to undo the breakdown. As mentioned above, rates are moving slightly higher. TNX, which backtested its SMA200 yesterday, is holding those levels.

As mentioned above, rates are moving slightly higher. TNX, which backtested its SMA200 yesterday, is holding those levels.

More action is seen on the very short end, with 6-mo bills nearly back to their March highs. Note that yields topped at 5.32% on Mar 7, the day after SPX peaked at 4078. By Mar 14, with SPX dropping as low as 3808 (-6.6%), the bills had fallen to 4.51% – a rapid flight to safety.

More action is seen on the very short end, with 6-mo bills nearly back to their March highs. Note that yields topped at 5.32% on Mar 7, the day after SPX peaked at 4078. By Mar 14, with SPX dropping as low as 3808 (-6.6%), the bills had fallen to 4.51% – a rapid flight to safety. The 2-yr fell from 5.09% to 3.72% during that same period – a stunning drop of 1.37%. The equivalent today would be from 4.13% to 2.76%. I’m certainly not suggesting that will happen unless we get a very strong selloff in stocks.

The 2-yr fell from 5.09% to 3.72% during that same period – a stunning drop of 1.37%. The equivalent today would be from 4.13% to 2.76%. I’m certainly not suggesting that will happen unless we get a very strong selloff in stocks.

A 6.6% drop from recent highs would put SPX around 3879, a little more than a .786 retrace of the gains from Mar 13. By contrast, the 10Y fell by 70 bps between its 4.07% Mar 1 high and Mar 14. In fact, it kept falling, shedding 82 bps by the time it bottomed on Apr 5 at 3.25%.

By contrast, the 10Y fell by 70 bps between its 4.07% Mar 1 high and Mar 14. In fact, it kept falling, shedding 82 bps by the time it bottomed on Apr 5 at 3.25%.

The recent increase in yields has pushed 2s10s away from the danger of crossing above recent highs: -58bps versus -38 bps. But, if we applied the Mar changes to current yields, we’d be looking at a positive 8.9 bps for the 2s10s – certainly in keeping with past equity corrections.

The recent increase in yields has pushed 2s10s away from the danger of crossing above recent highs: -58bps versus -38 bps. But, if we applied the Mar changes to current yields, we’d be looking at a positive 8.9 bps for the 2s10s – certainly in keeping with past equity corrections.

Again, not suggesting that this scenario is any more likely than the rest – just that it would be in keeping with the last time yields reached these levels.

Again, not suggesting that this scenario is any more likely than the rest – just that it would be in keeping with the last time yields reached these levels.

To see a 6%+ decline in equities, we’d need the debt ceiling concerns turn into a debt ceiling crisis. We could also experience a sharp drop if Apr PCE comes out much hotter than expected or GDP does something alarming.

In sum, this is a fairly dangerous point in the markets. Although we might get through this Friday’s OPEX relatively unscathed, it could get pretty volatile going forward.

In sum, this is a fairly dangerous point in the markets. Although we might get through this Friday’s OPEX relatively unscathed, it could get pretty volatile going forward.

GLTA.

UPDATE: 1:36 PM

Stocks are supposedly all hot and bothered about the prospect of the debt ceiling crisis being solved.  But, actually, it’s the usual VIX tricks at work in service of Friday’s OPEX. Note that both VIX and VIX futures were egging on the algos and could easily continue their bullish ways – especially with all the jawboning from politicians, none of whom wants to be blamed for a market correction.

But, actually, it’s the usual VIX tricks at work in service of Friday’s OPEX. Note that both VIX and VIX futures were egging on the algos and could easily continue their bullish ways – especially with all the jawboning from politicians, none of whom wants to be blamed for a market correction.

Treasury yields closed off their intraday highs and 2s10s closed at -58 bps. But, it’s too early to say the crisis is over. If it isn’t solved by Friday’s OPEX, Monday could be nasty.

Treasury yields closed off their intraday highs and 2s10s closed at -58 bps. But, it’s too early to say the crisis is over. If it isn’t solved by Friday’s OPEX, Monday could be nasty.