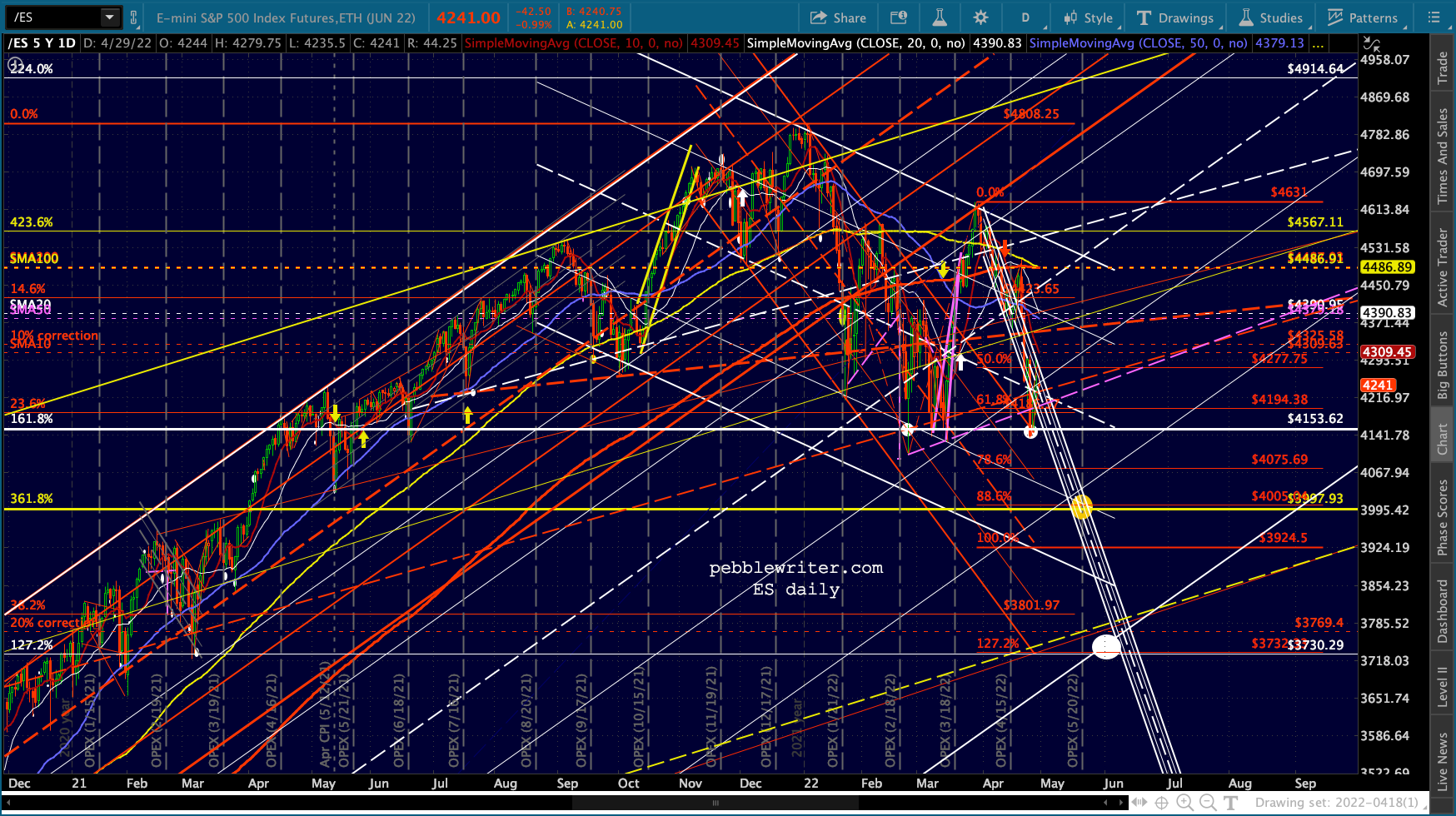

Futures came roaring back into the falling white channel yesterday, revealing what many know but few say out loud: the market is broken. When expectations of a 1% quarterly rise in GDP yield, instead, a 1.4% decline, stocks should decline. Plain and simple.

The old “bad news is good news” argument doesn’t work any more because the Fed no longer has the ability (at least this coming meeting) to ease in response to a slowing economy. Perhaps they would have if they hadn’t squandered the opportunity to taper months ago, but that’s water under the bridge.

Instead, we get this massive disconnect which is, at the end of the day, a means of ramping stocks in advance of the bad news we all know is coming via the Fed’s meeting next week: a 50+ bps rate hike. Beyond monetary policy, which is now a headwind instead of a tailwind, we see more and more indications of tough times ahead. As Bill Blain (a treasure) sums it up:

The world is not what we think it should be. It is what it is…and that is getting less pretty.

continued for members…Despite the huge bounce, nothing has really changed since yesterday morning on the equity front.

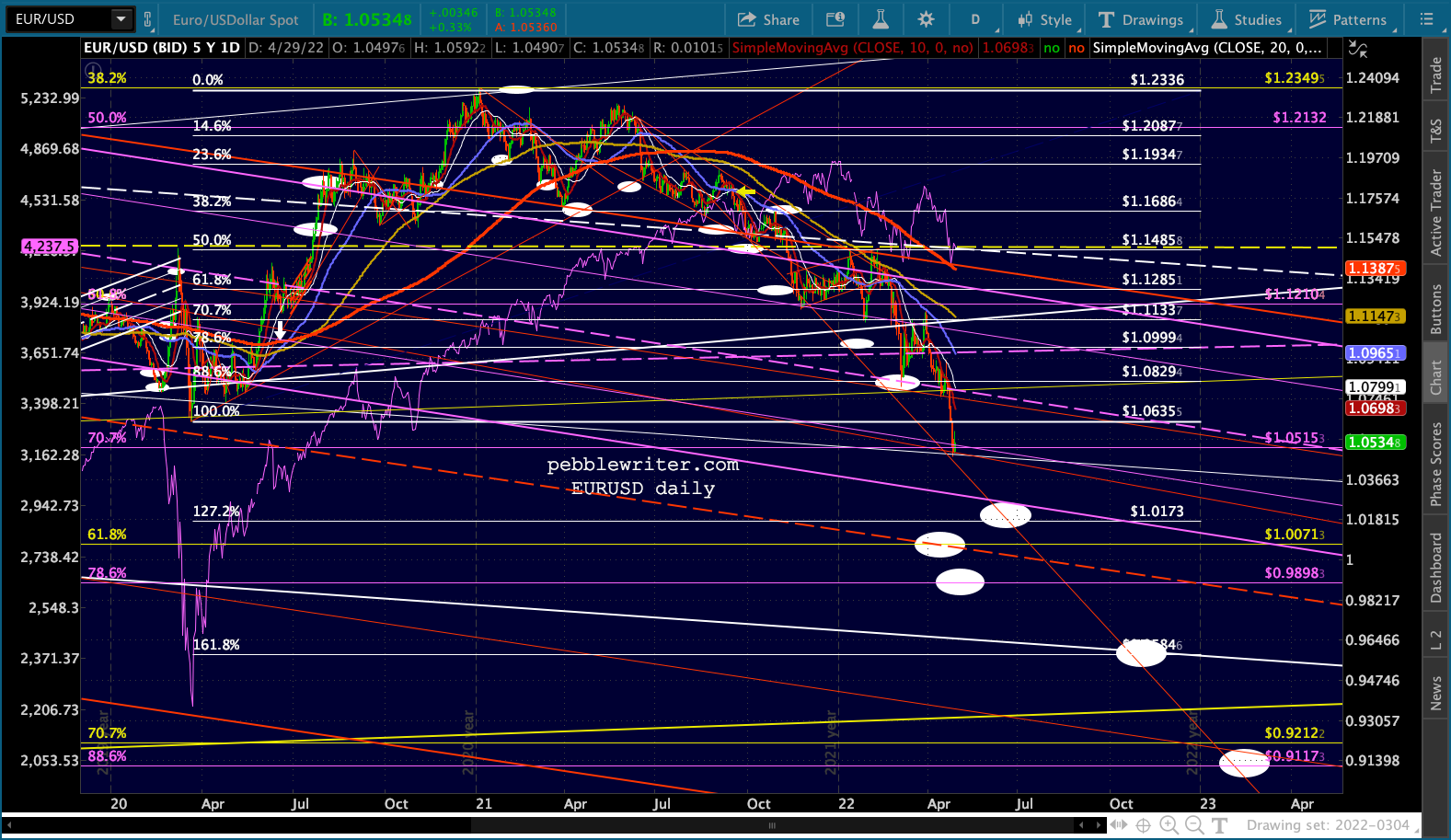

The only change on the currency front is that DXY is backtesting its old highs as EURUSD takes a breather.

The only change on the currency front is that DXY is backtesting its old highs as EURUSD takes a breather.

Oil is bouncing slightly on speculation that China’s shutdown might be turning a corner, but RB is unchanged.

Oil is bouncing slightly on speculation that China’s shutdown might be turning a corner, but RB is unchanged.

TNX is following CL’s lead, regaining the ground it has given up since reaching 29.23. While a backtest of the channel top would be normal, it’s not necessary. As long as it remains above 29.23, the 32.48 former top and IH&S target should be the 10Y’s next stop.

TNX is following CL’s lead, regaining the ground it has given up since reaching 29.23. While a backtest of the channel top would be normal, it’s not necessary. As long as it remains above 29.23, the 32.48 former top and IH&S target should be the 10Y’s next stop. GLTA

GLTA