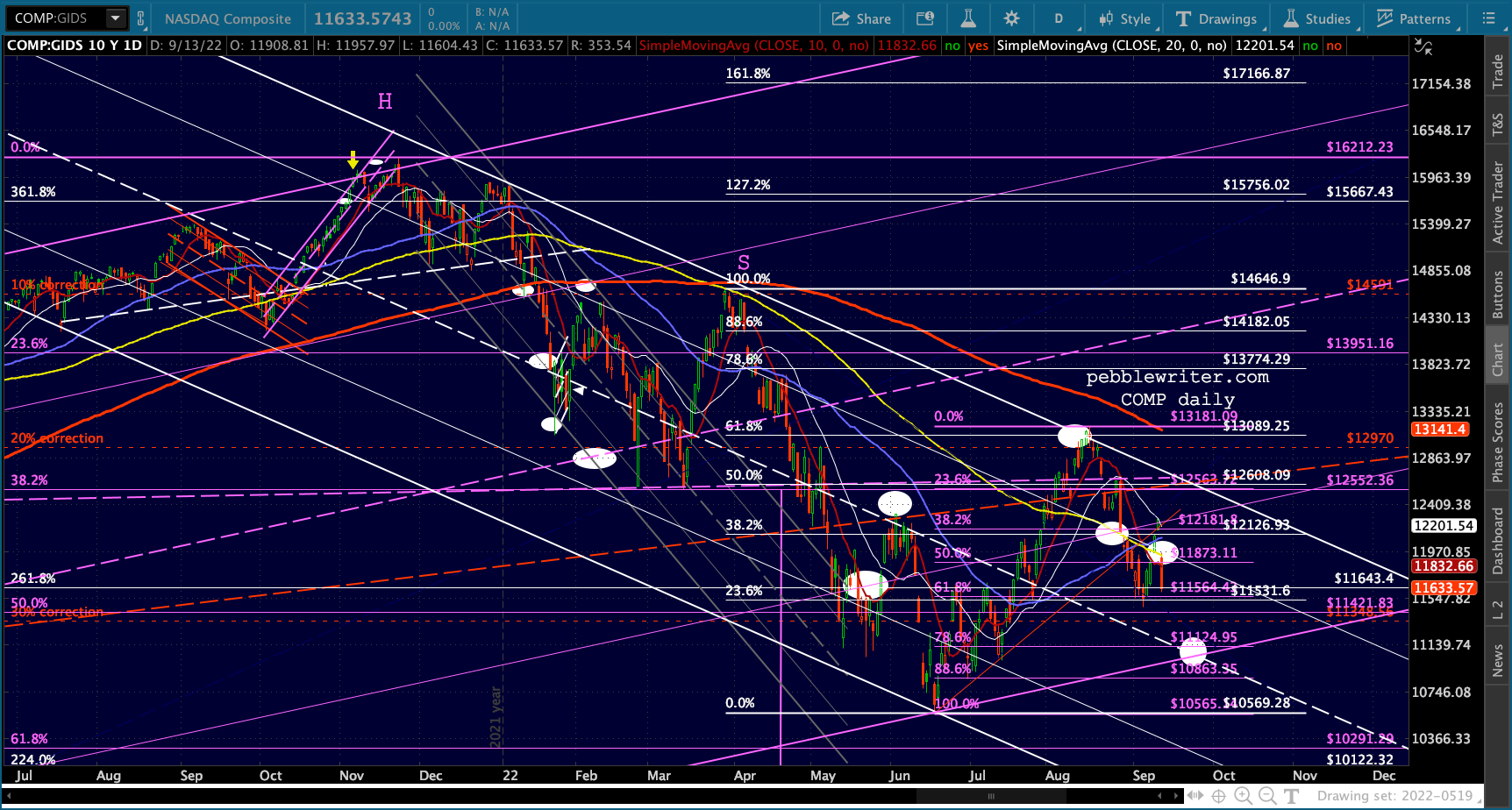

Apparently, investors aren’t quite as sanguine about inflation as it seemed. After slightly overshooting our upside target from February, SPX plunged 4.32% – about $1.5 trillion in market cap. Trillion-and-a-half here, trillion-and-a-half there, pretty soon you’re talking real money. It was the worst day in the markets since March 2020 and one of the worst on record.

Yet, the talking heads and financial press were all rainbows and unicorns leading up to the CPI print. The big question, of course, is “what happens next?”

Yet, the talking heads and financial press were all rainbows and unicorns leading up to the CPI print. The big question, of course, is “what happens next?”

continued for members…

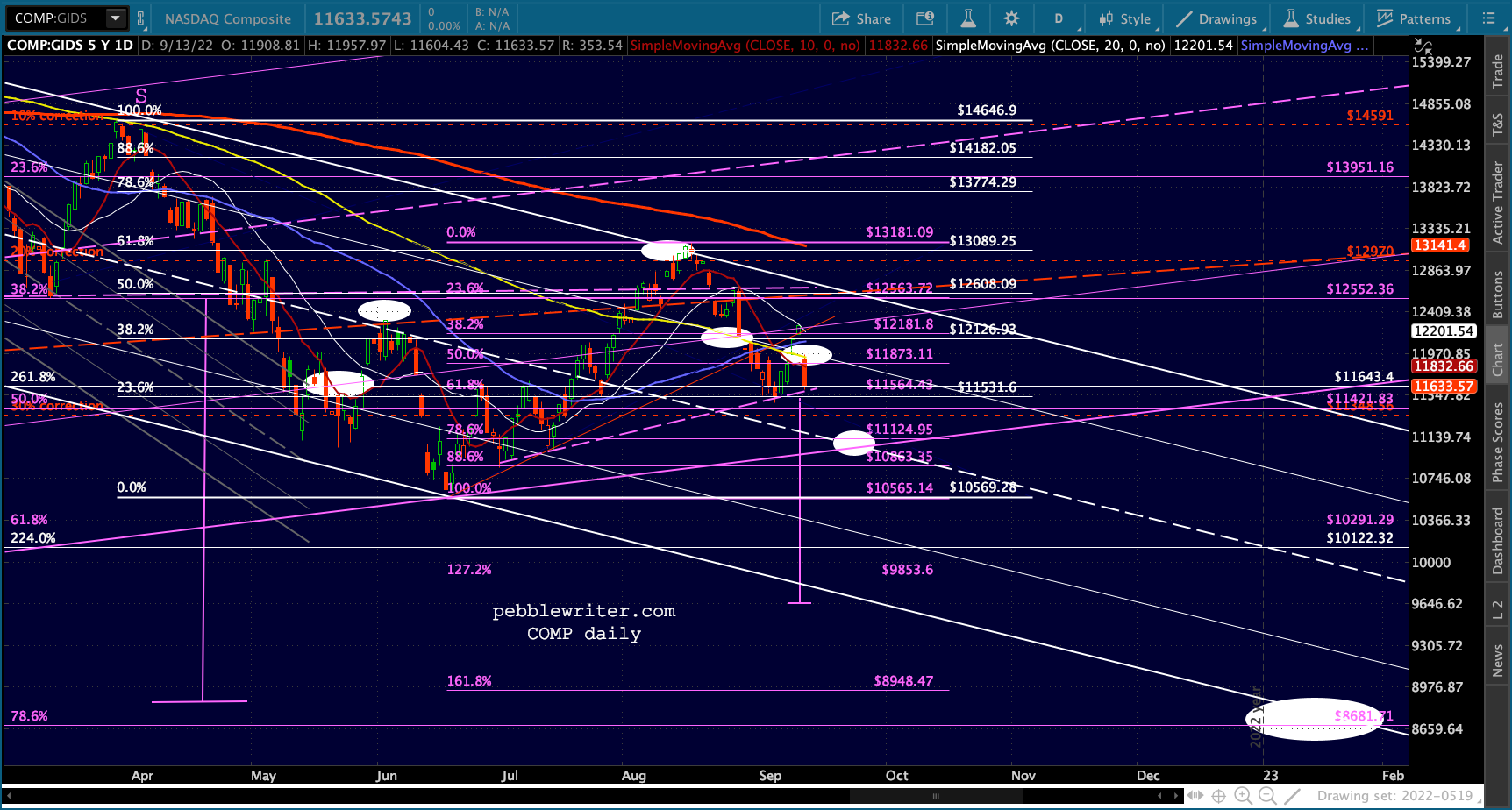

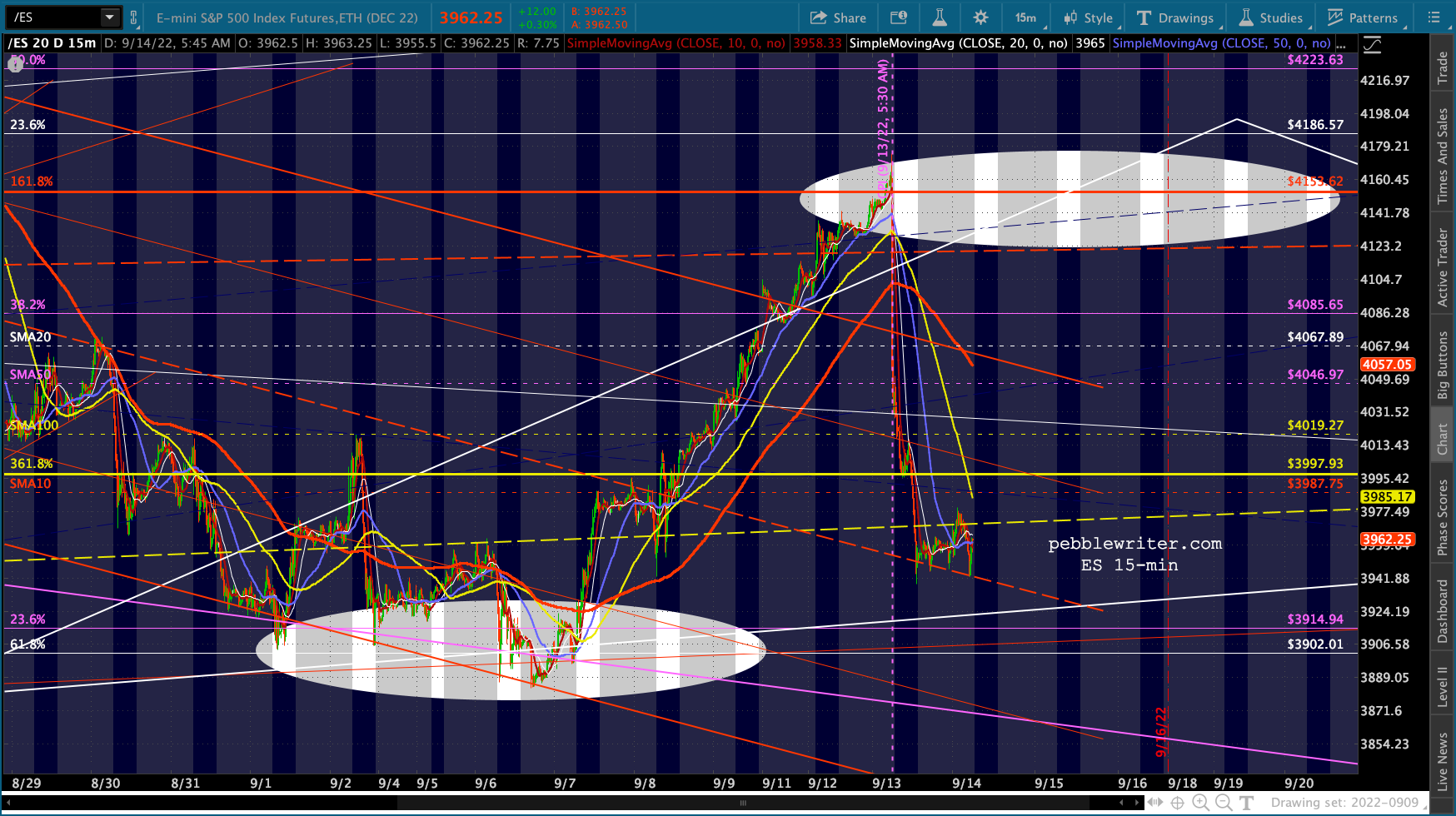

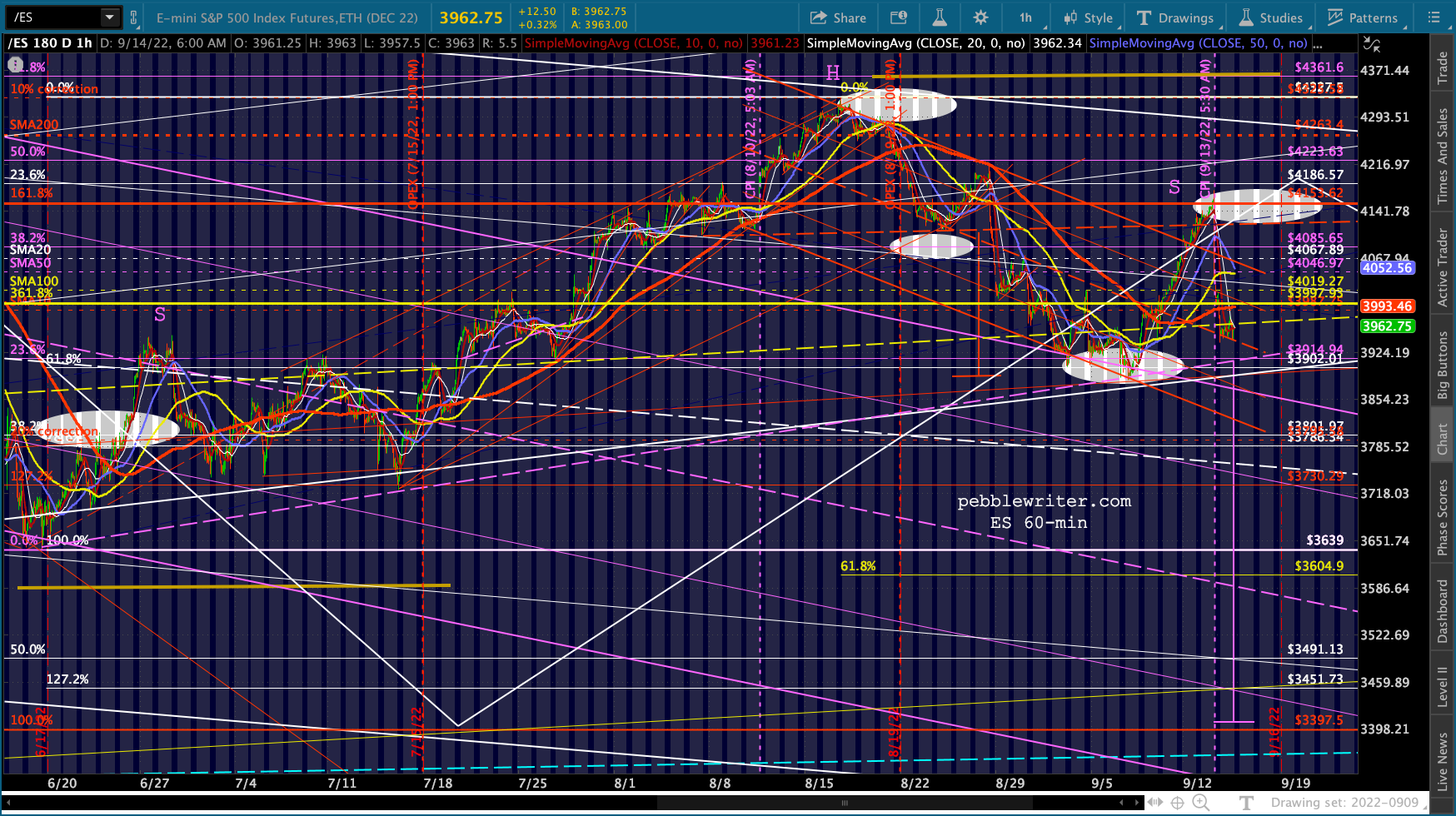

As we discussed yesterday, just about everything stopped just short of a more serious breakdown.

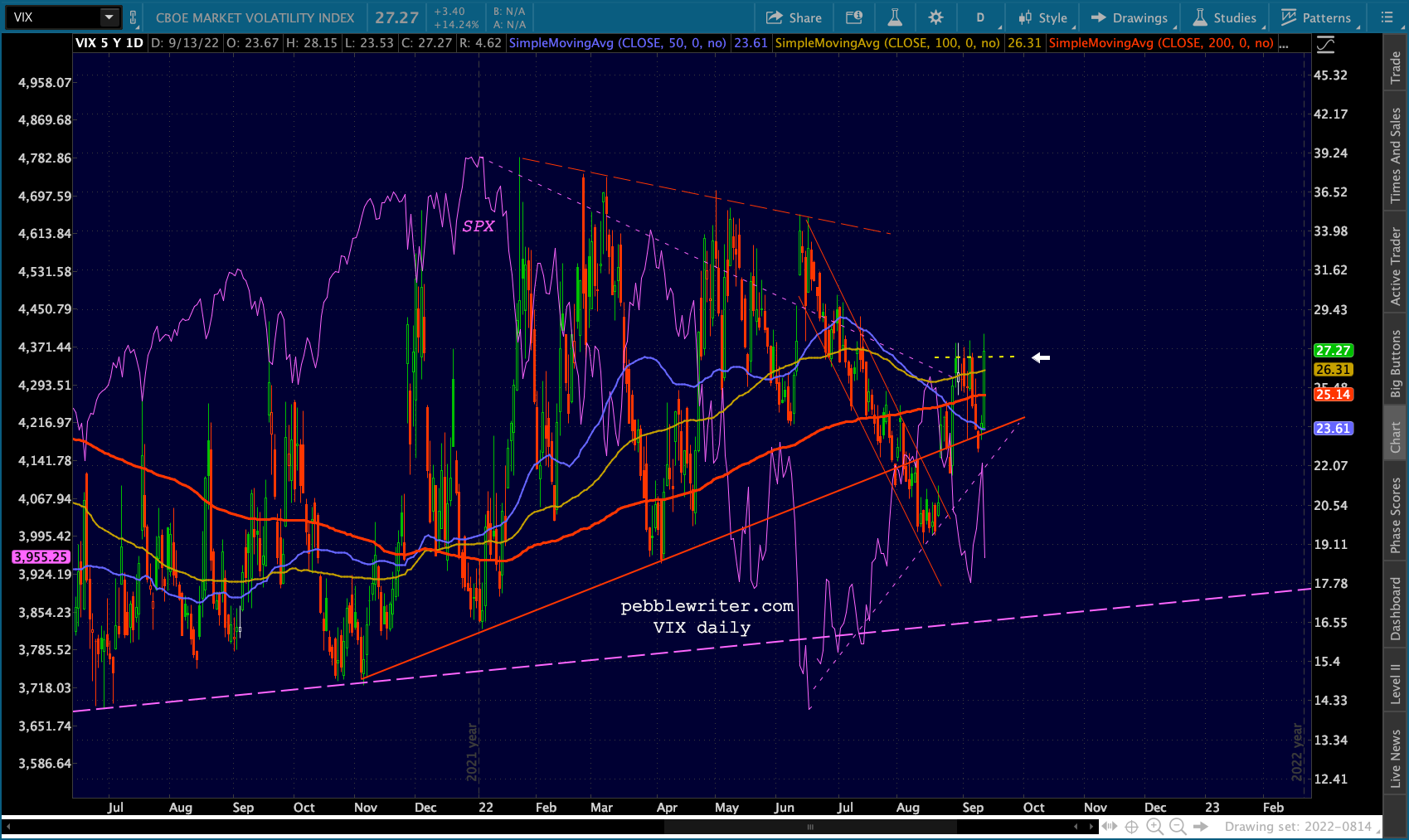

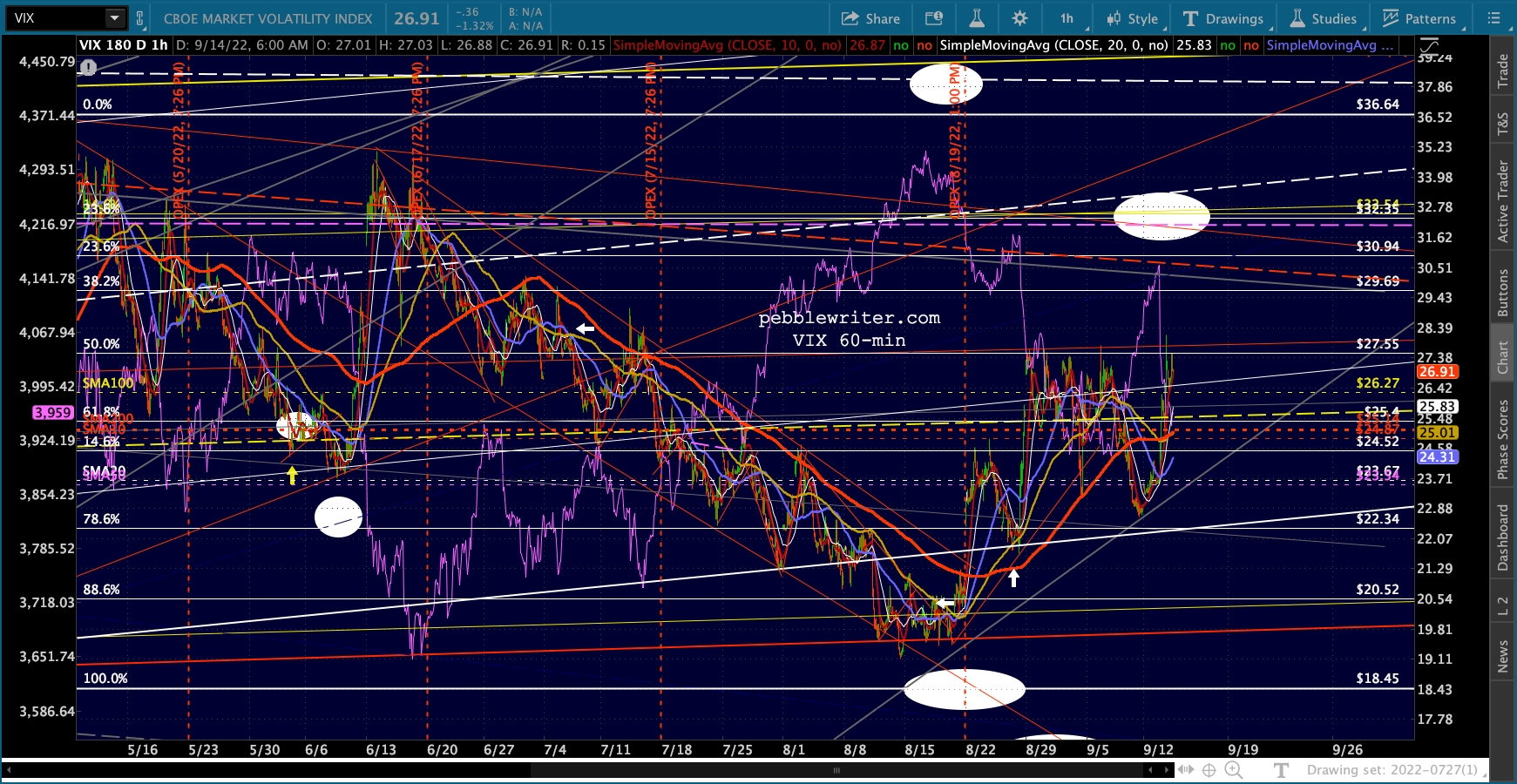

With OPEX coming up Friday, it would surprise no one if stocks muddled through the next couple of sessions to limit the bloodshed.

With OPEX coming up Friday, it would surprise no one if stocks muddled through the next couple of sessions to limit the bloodshed.

This morning, that’s what appears to be happening. With all those H&S Patterns, it will at least be pretty easy to see if/when things are breaking down.

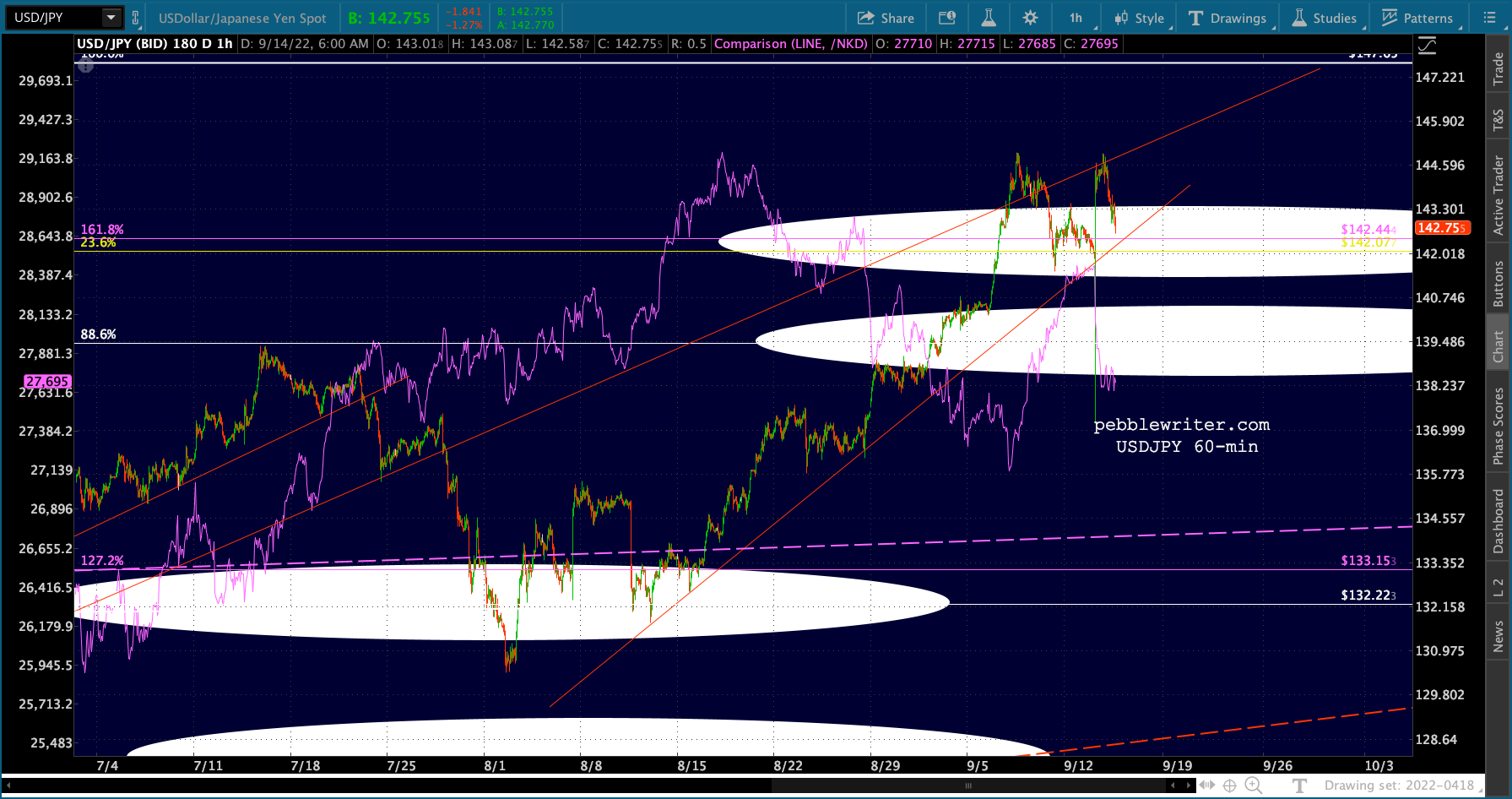

The currencies are voting for a bounce here, especially USDJPY with its comical recovery after the CPI print – the BoJ’s typical nothing-to-see-here-move-along fashion.

The currencies are voting for a bounce here, especially USDJPY with its comical recovery after the CPI print – the BoJ’s typical nothing-to-see-here-move-along fashion.

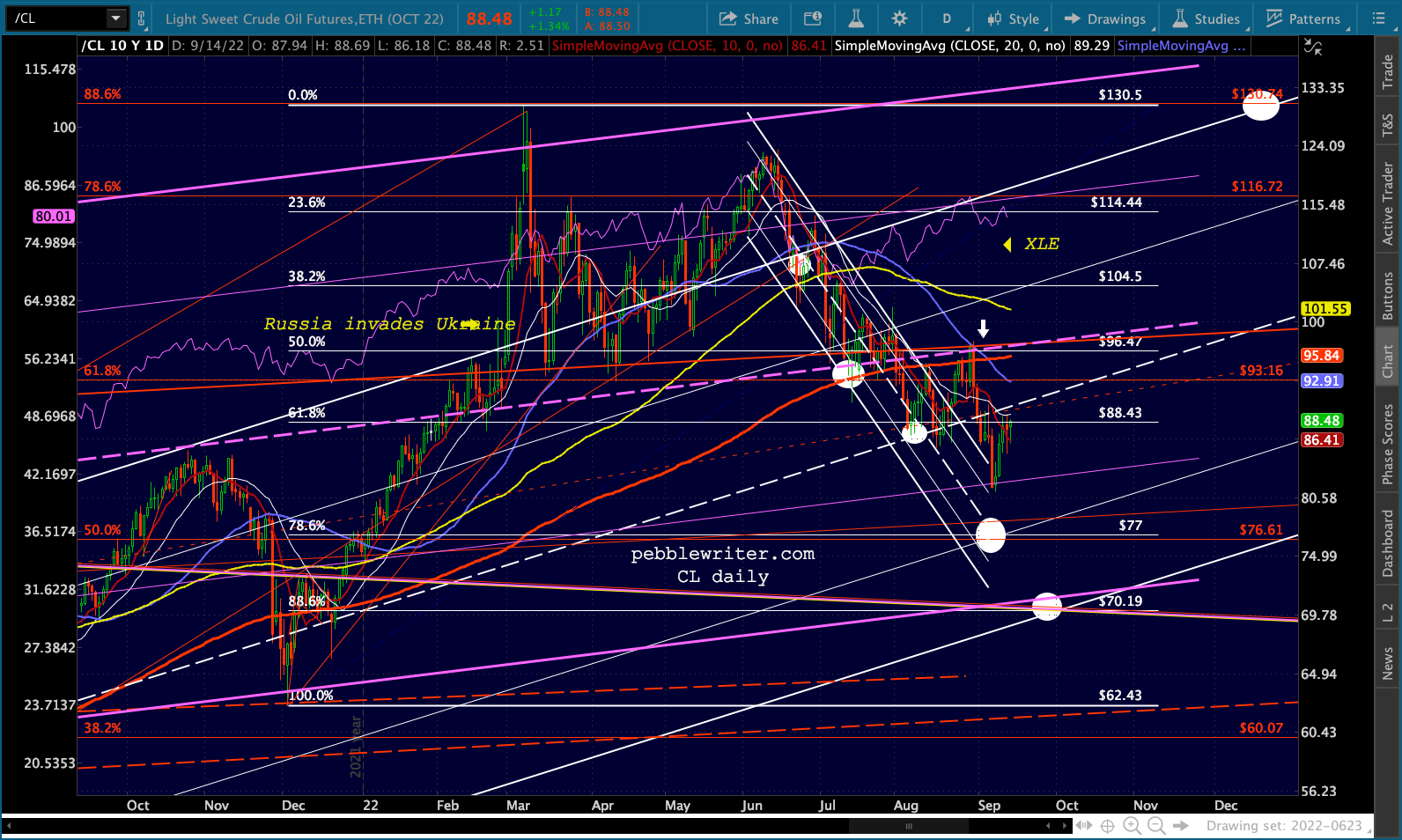

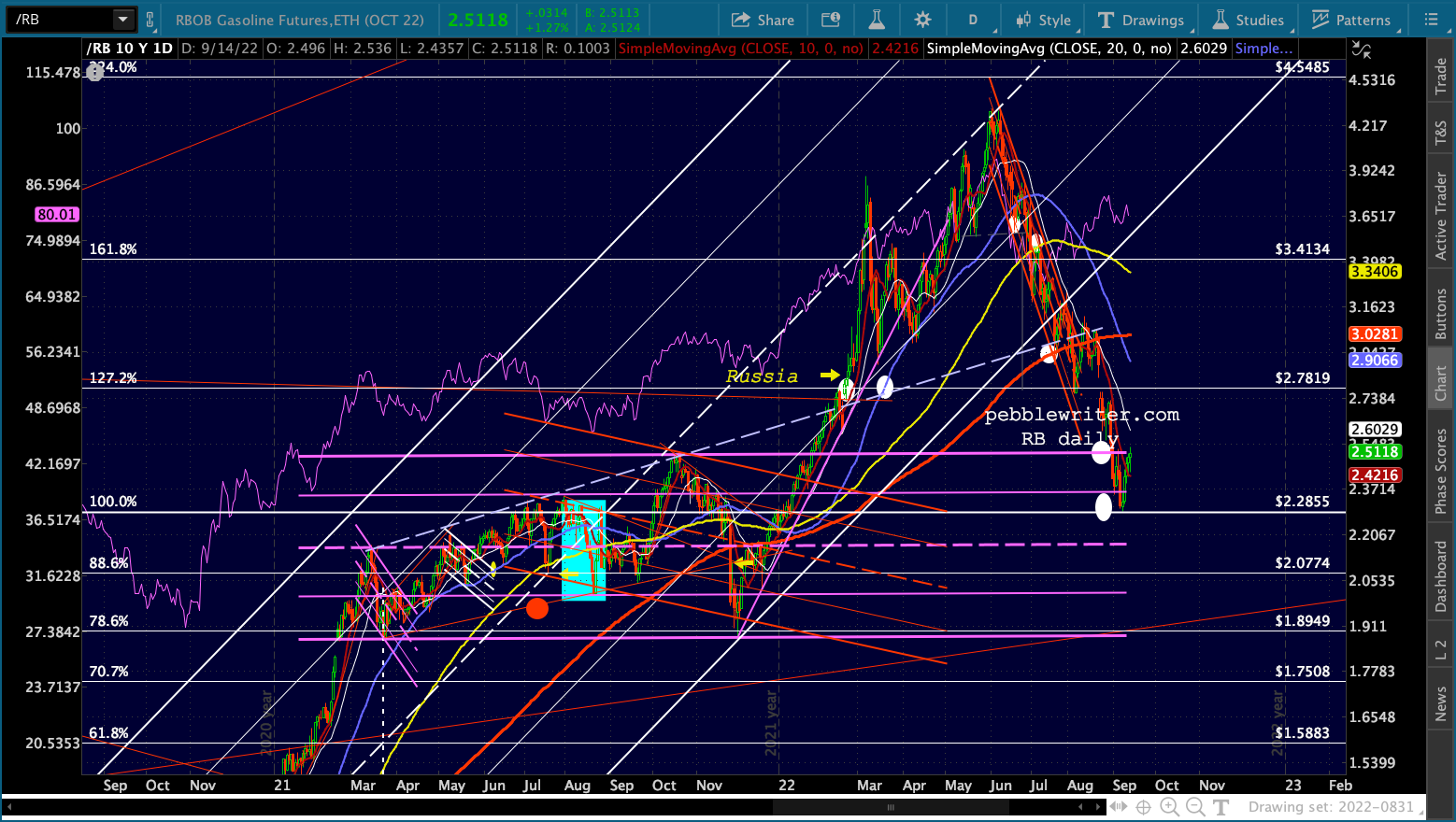

Oil and gas remain wild cards, with RB’s bounce in particular being an obvious double edged sword. Too much, and the inflation problem looks worse.

Oil and gas remain wild cards, with RB’s bounce in particular being an obvious double edged sword. Too much, and the inflation problem looks worse.

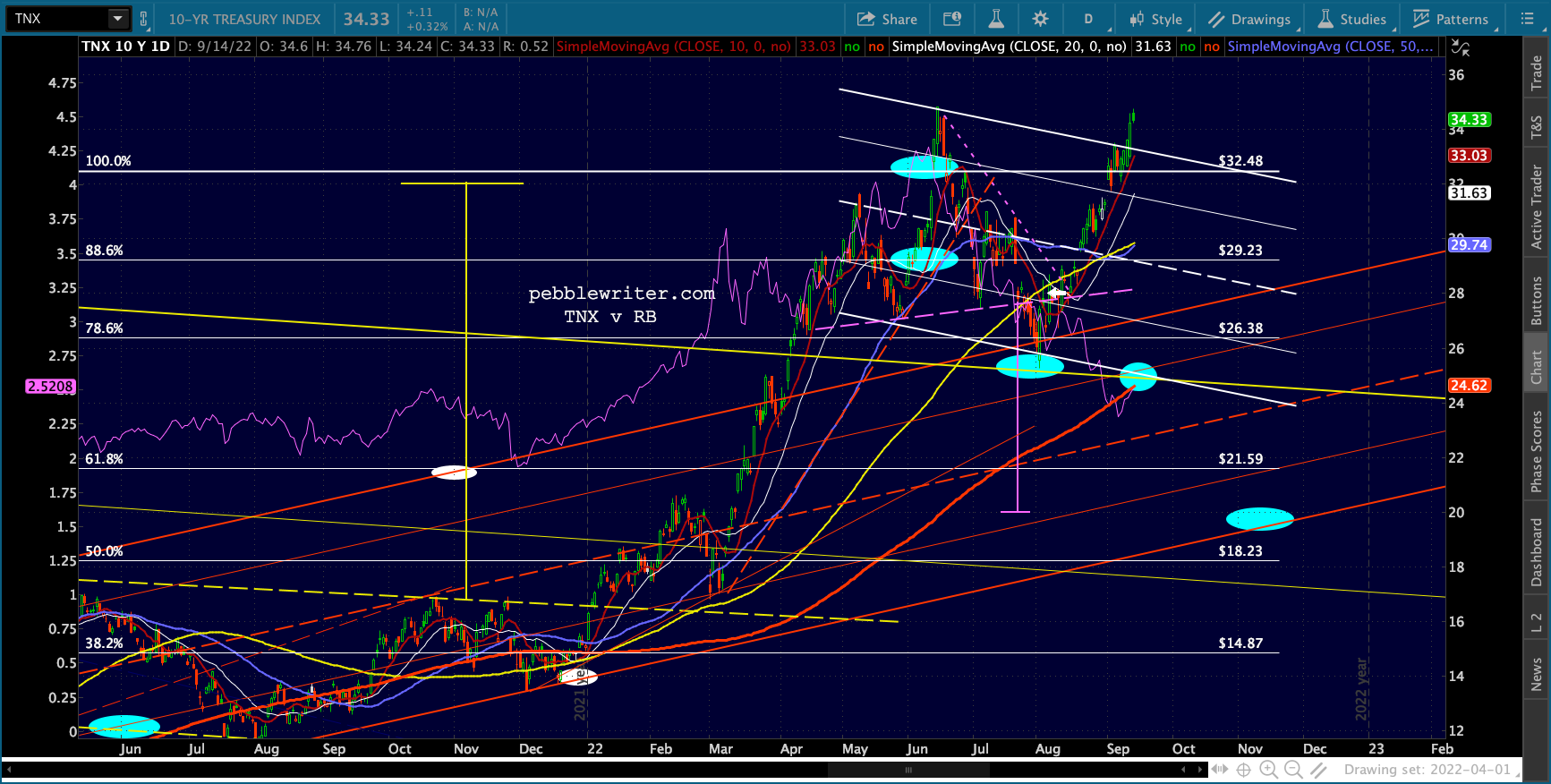

The 10Y came very close to topping the Jun highs – which would have officially doomed the H&S Pattern which completed in July (already on life support.)

The 10Y came very close to topping the Jun highs – which would have officially doomed the H&S Pattern which completed in July (already on life support.) This is something TPTB can’t abide. So, don’t be surprised if the EIA inventory report due out at 10:30 ET sends oil and gas prices lower again.

This is something TPTB can’t abide. So, don’t be surprised if the EIA inventory report due out at 10:30 ET sends oil and gas prices lower again.

Stay tuned.