CPI soared to 6.24% YoY in October, well above the 5.9% expected and the highest since Nov 1990. The MoM print of 0.9% and the Core CPI print of 4.2% also came in hotter than expected and set multiyear records. Put simply, the Fed has lost control. As we’ve discussed, inflation continues to become more broad-based than the oil/gas-driven effect initially seen earlier this year.

As we’ve discussed, inflation continues to become more broad-based than the oil/gas-driven effect initially seen earlier this year.

The chart below shows the divergence from May-September and illustrates the importance of oil/gas prices to future inflation prints. If gas prices were to level off at today’s levels, the direct effect on CPI would cease in November. However, even if the base effect were to roll off, the other categories are now equally problematic.

The chart below shows the divergence from May-September and illustrates the importance of oil/gas prices to future inflation prints. If gas prices were to level off at today’s levels, the direct effect on CPI would cease in November. However, even if the base effect were to roll off, the other categories are now equally problematic.  Futures are off 20 points on the news, with several key factors indicating more to come.

Futures are off 20 points on the news, with several key factors indicating more to come.

Today marks the point at which the Fed officially stops cheering on the reflation trade.

continued for members…

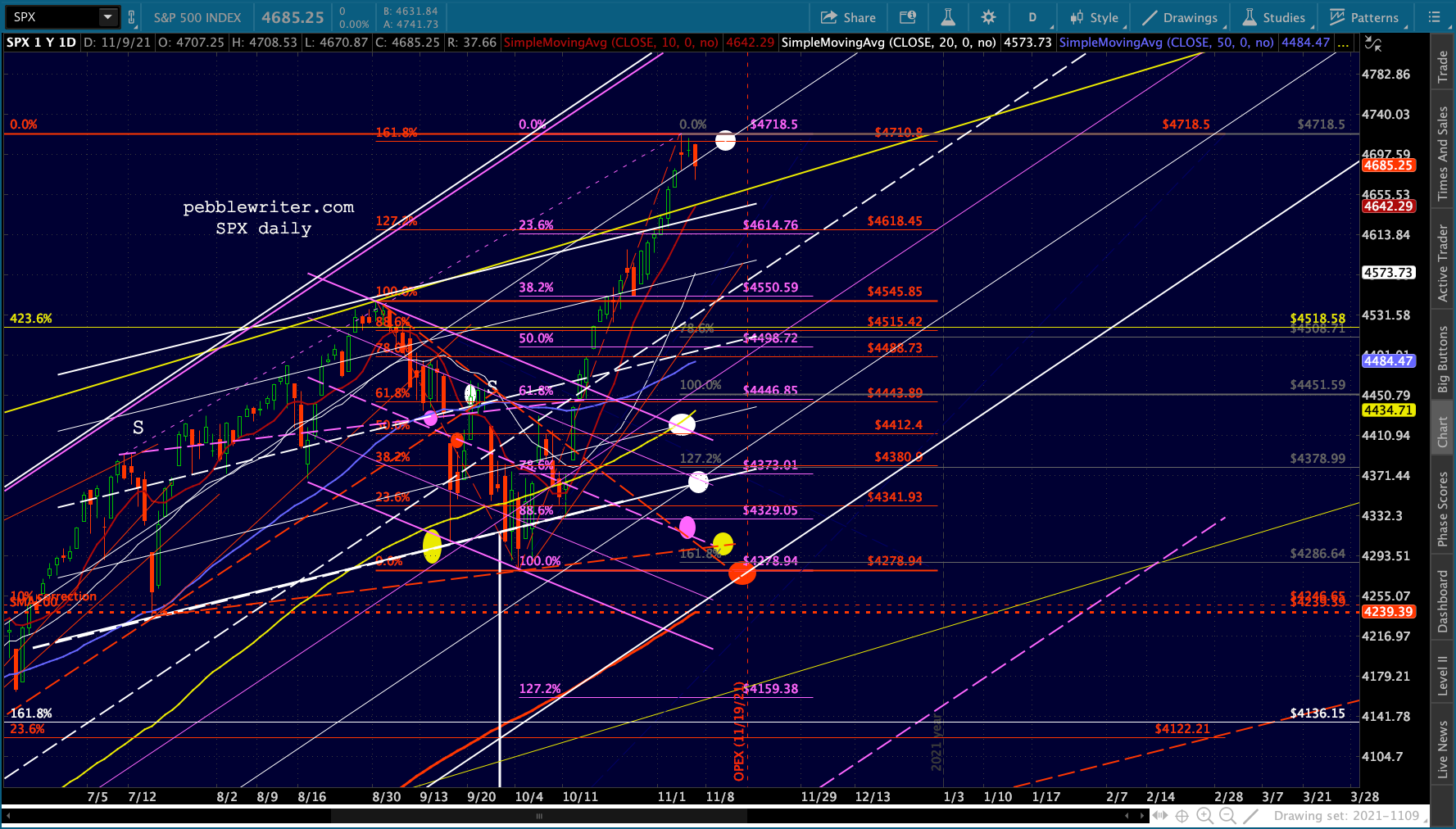

The equity picture: note that ES’ SMA200 is now only 1 point away from a 10% decline from the recent highs (the red oval.)

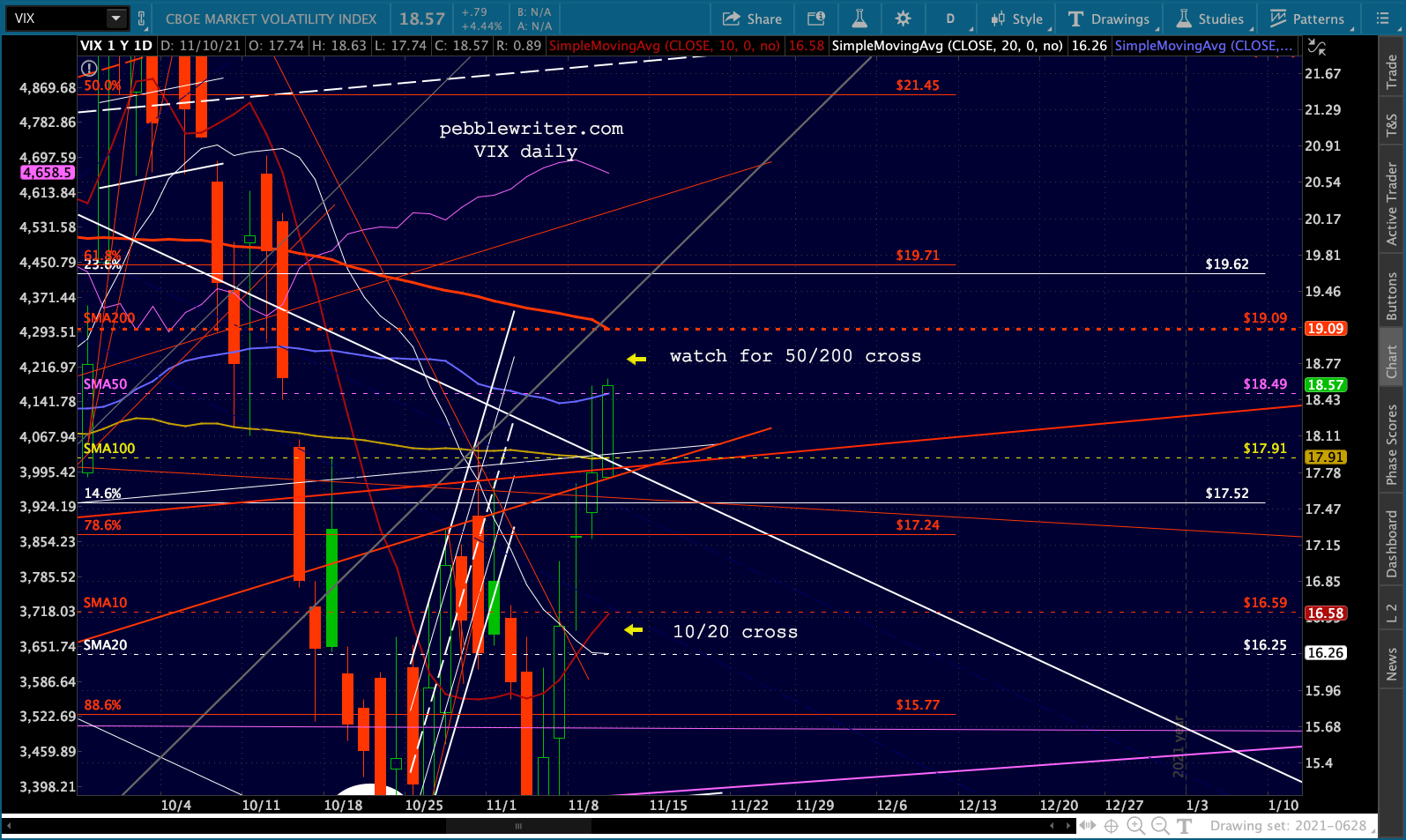

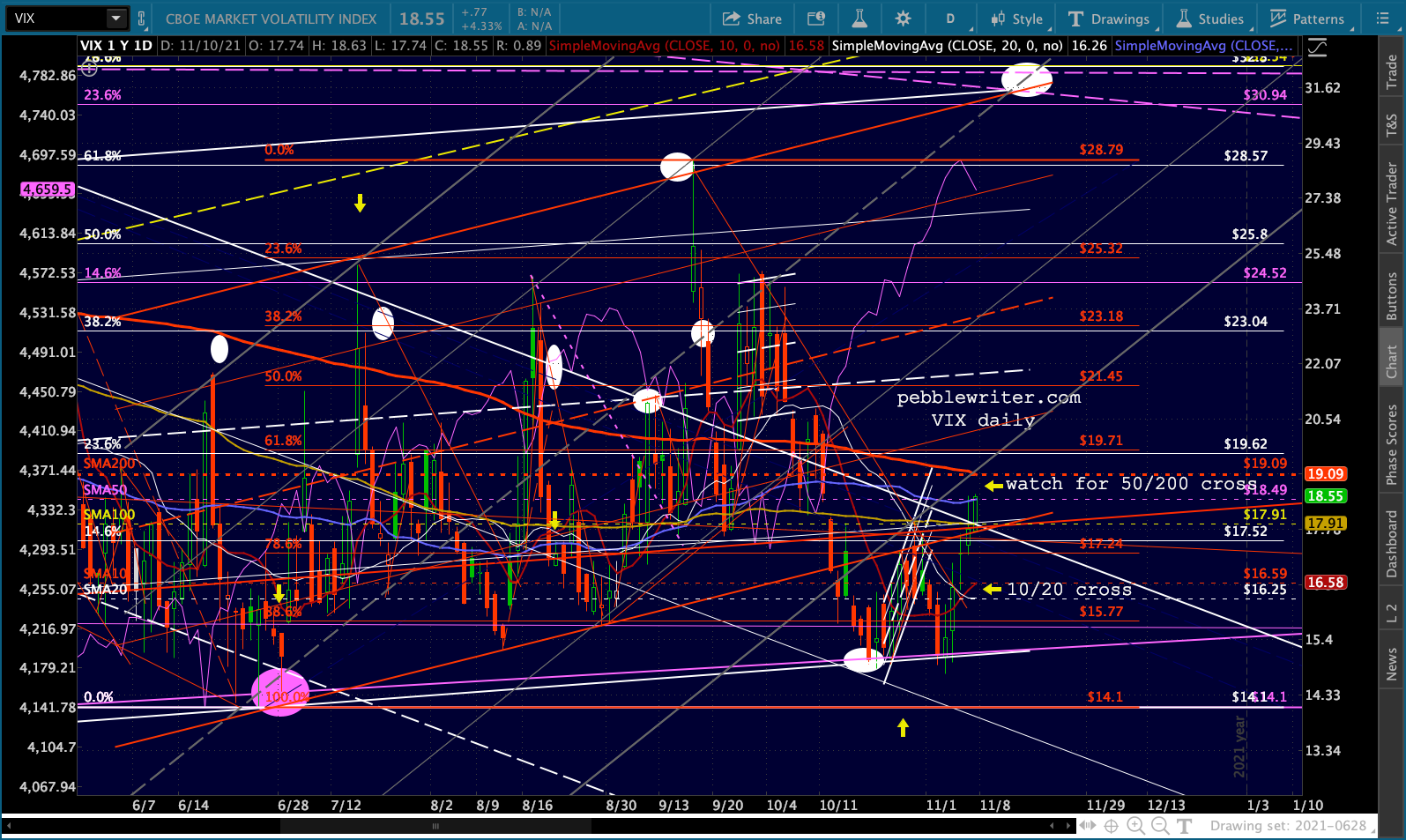

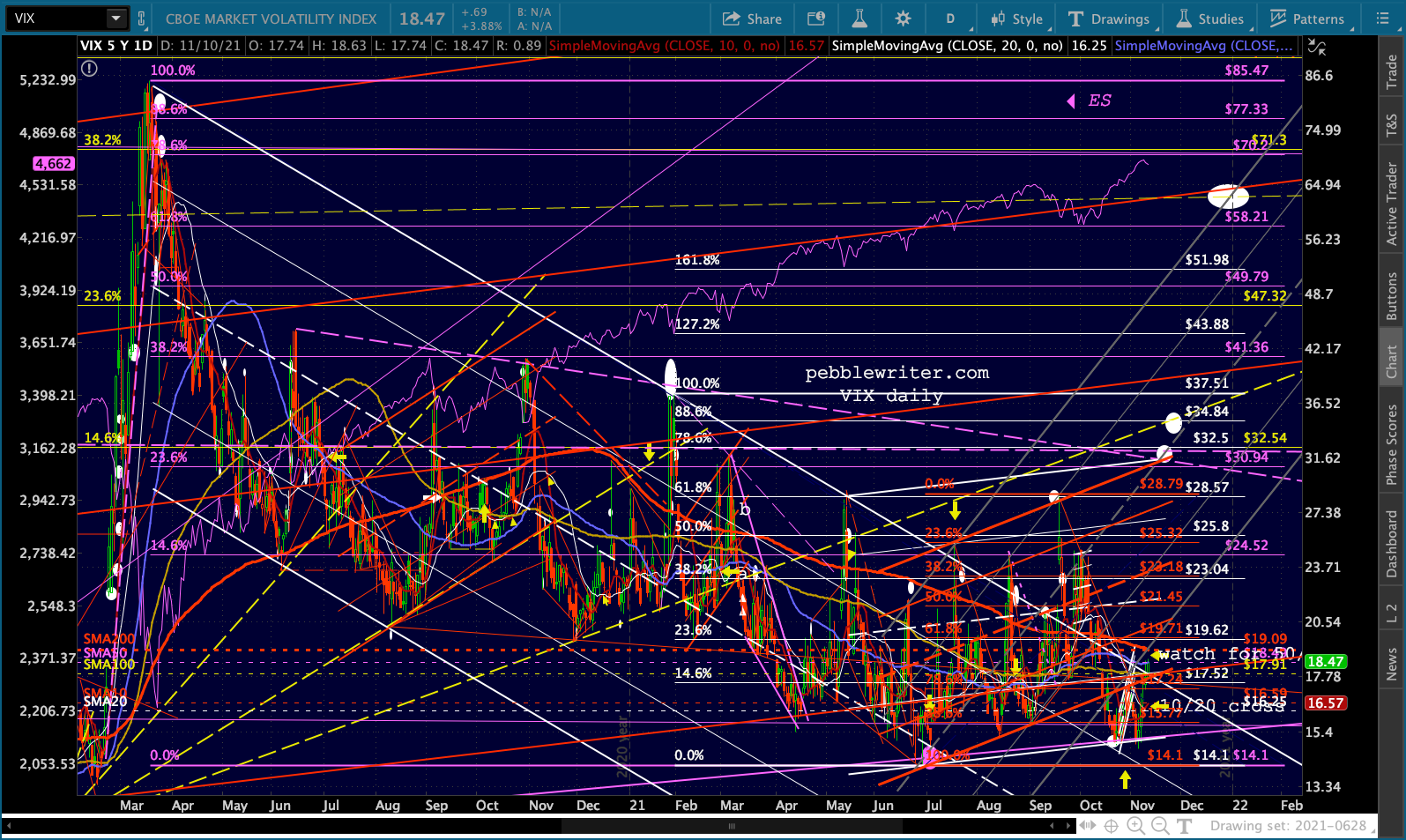

The biggest issue from a factor standpoint is VIX. Recall that we had a 10/20 cross earlier this week. VIX has now broken out of the falling white channel (again) and is closing in on a golden cross (SMA50 above the SMA200.) The bulls should try to hold the SMA50 at 18.49.

The biggest issue from a factor standpoint is VIX. Recall that we had a 10/20 cross earlier this week. VIX has now broken out of the falling white channel (again) and is closing in on a golden cross (SMA50 above the SMA200.) The bulls should try to hold the SMA50 at 18.49.

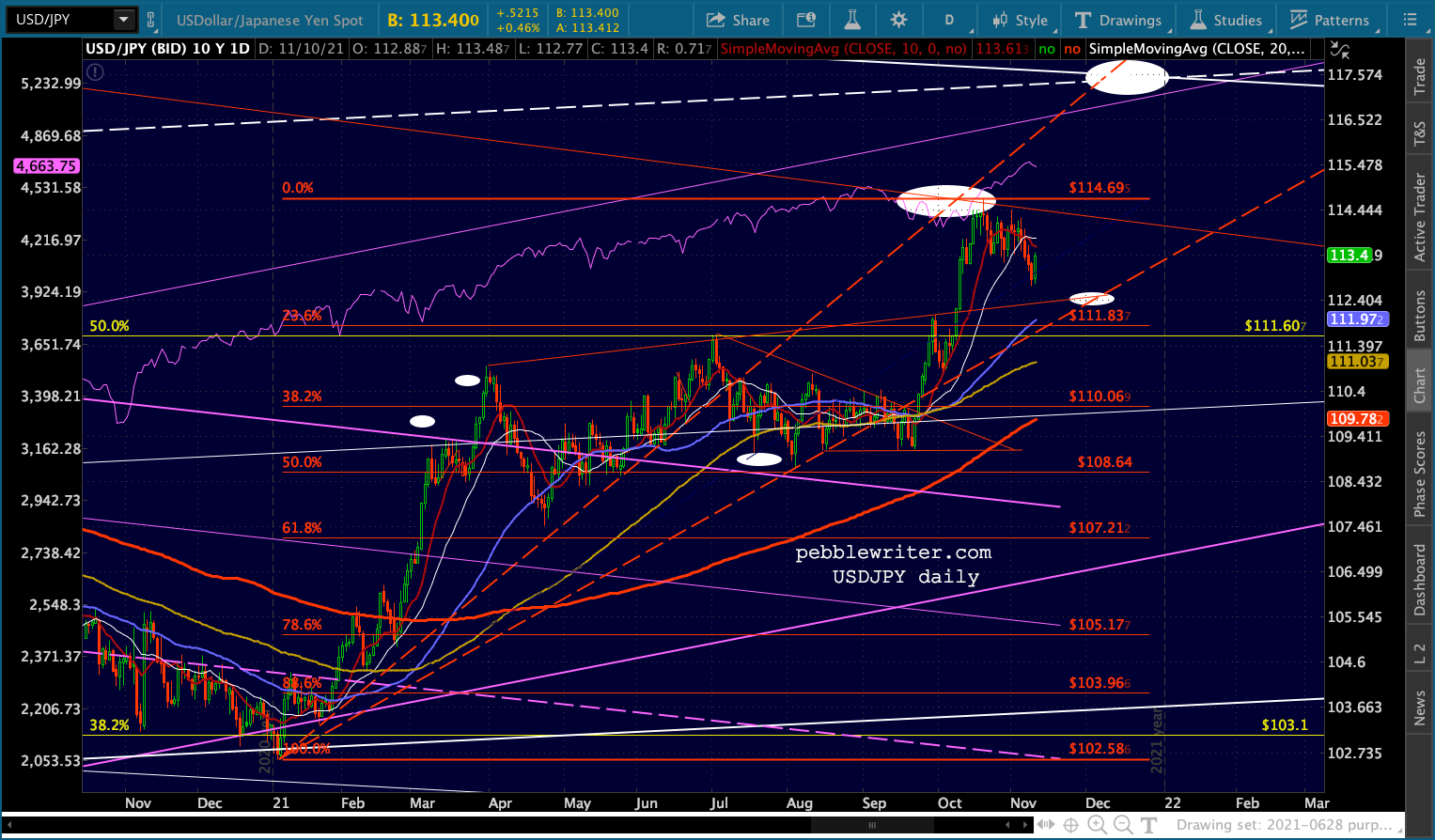

The expectations of an earlier hike in rates is sending USDJPY higher…

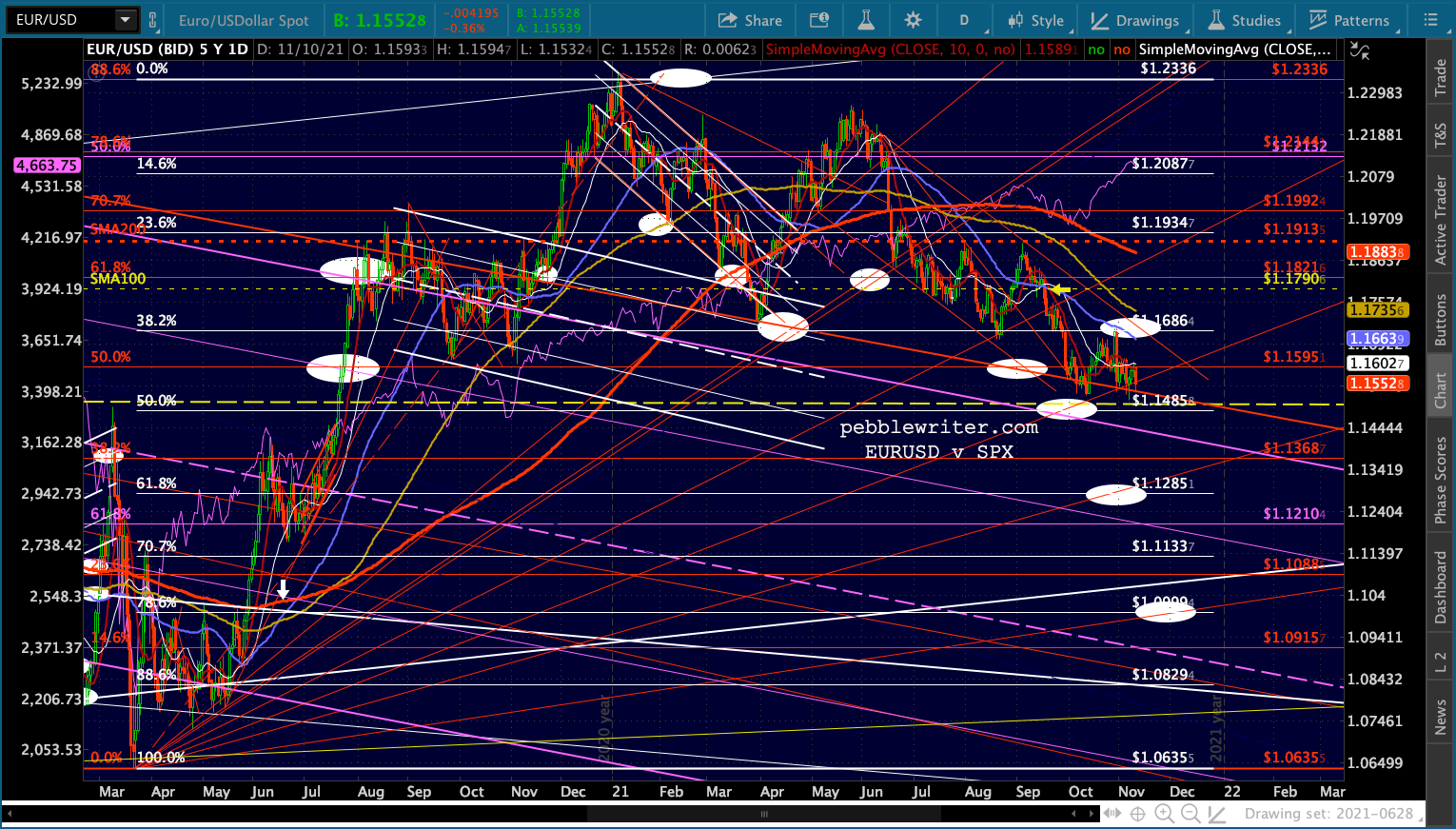

The expectations of an earlier hike in rates is sending USDJPY higher… …but the euro is keeping a lid on DXY.

…but the euro is keeping a lid on DXY.

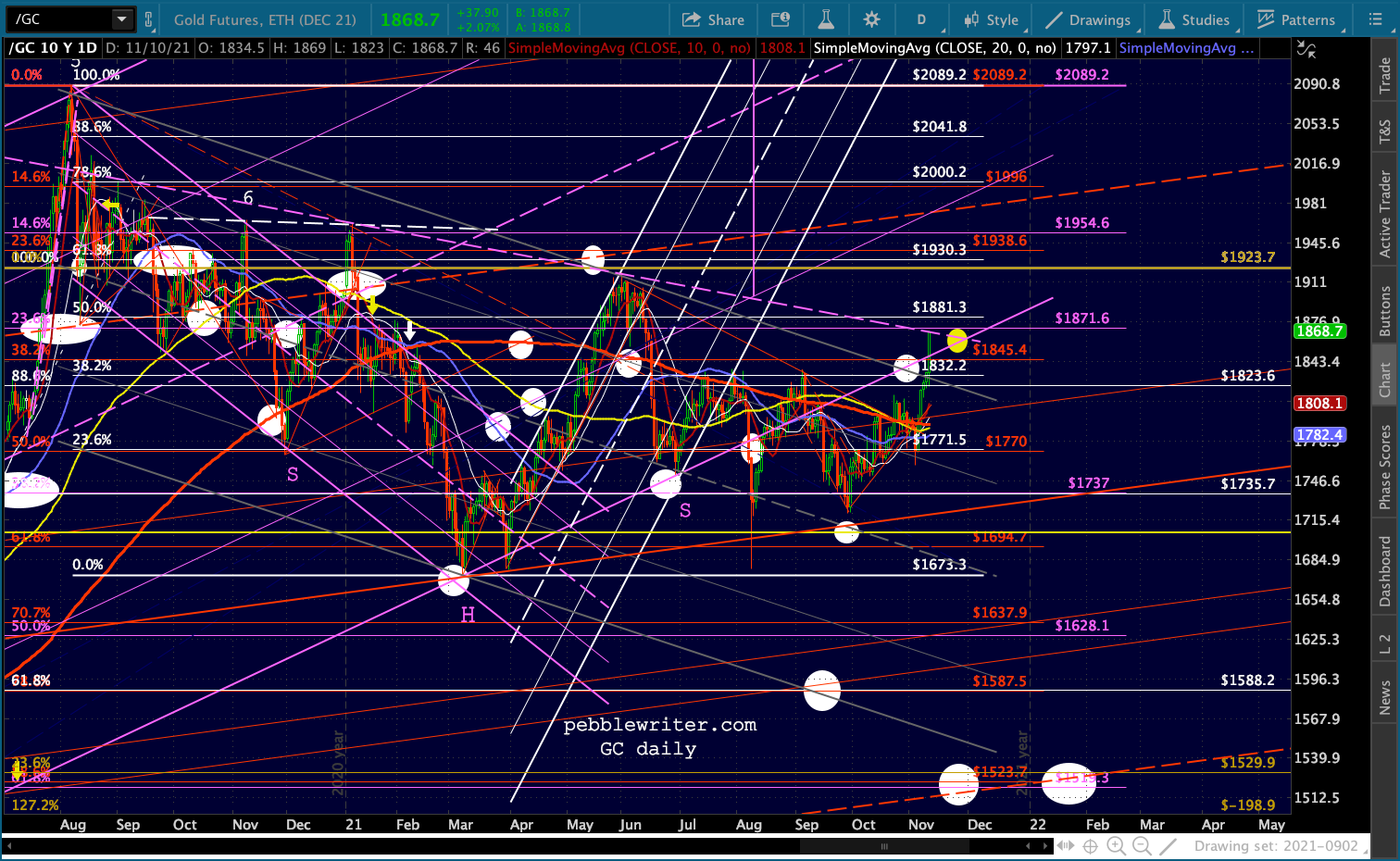

Gold is getting a big boost from the inflation data, and has now reached the purple neckline at 1870.6. I would revert to short with tight stops right here.

Gold is getting a big boost from the inflation data, and has now reached the purple neckline at 1870.6. I would revert to short with tight stops right here.

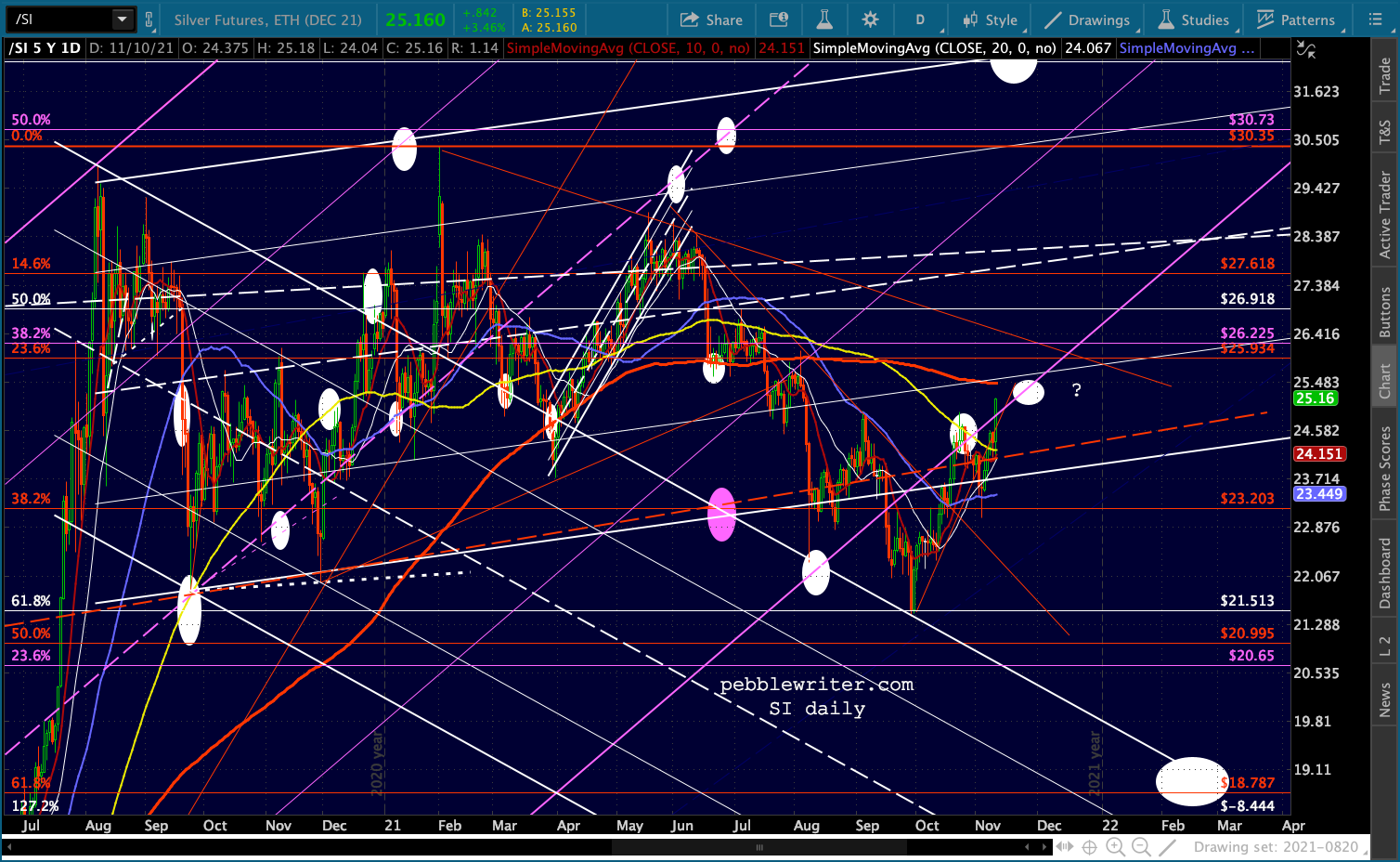

SI probably has a little further to go, with its SMA200 in sight.

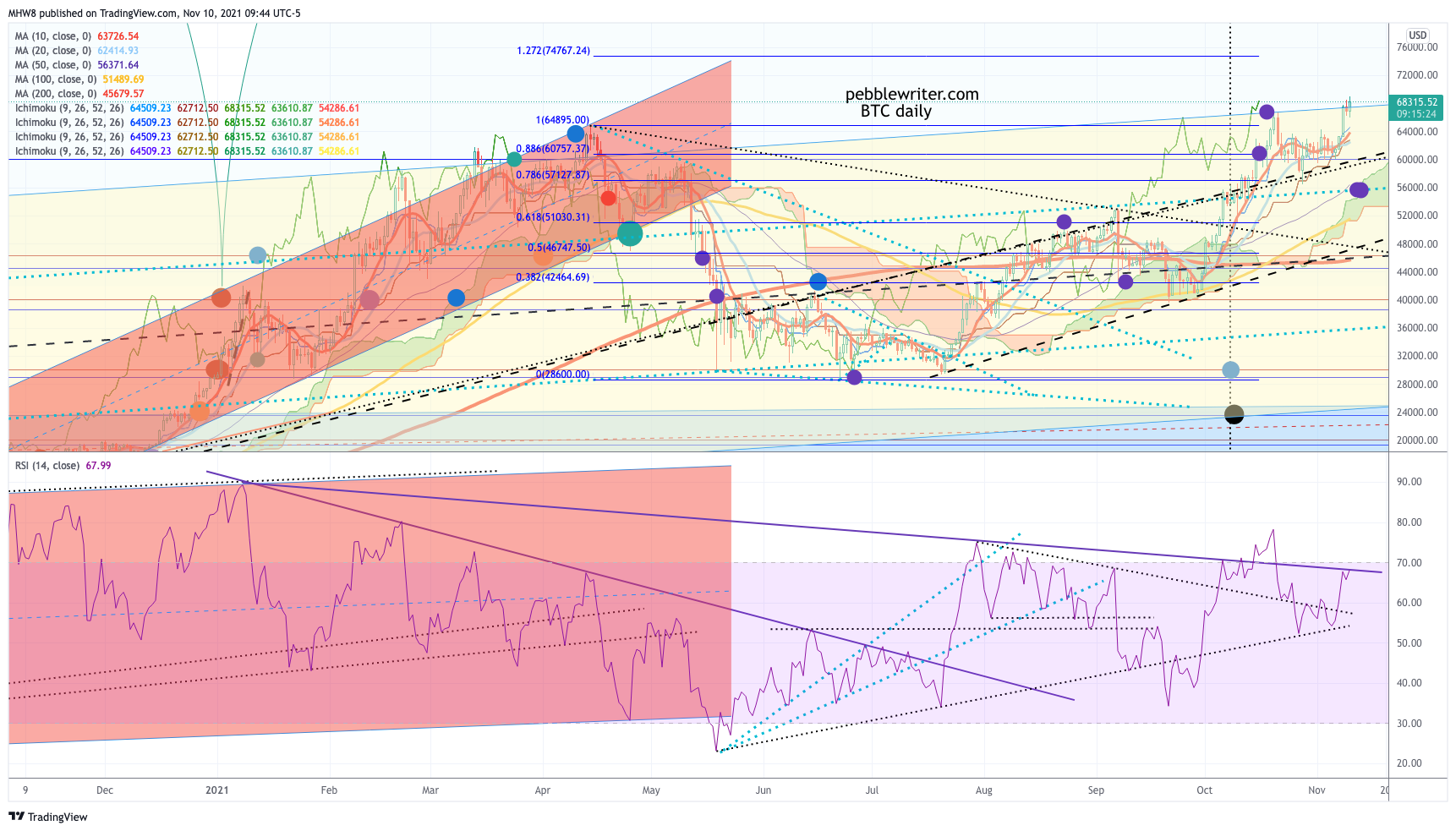

SI probably has a little further to go, with its SMA200 in sight. BTC is getting a leg up, though I still expect it to back off from these levels.

BTC is getting a leg up, though I still expect it to back off from these levels.

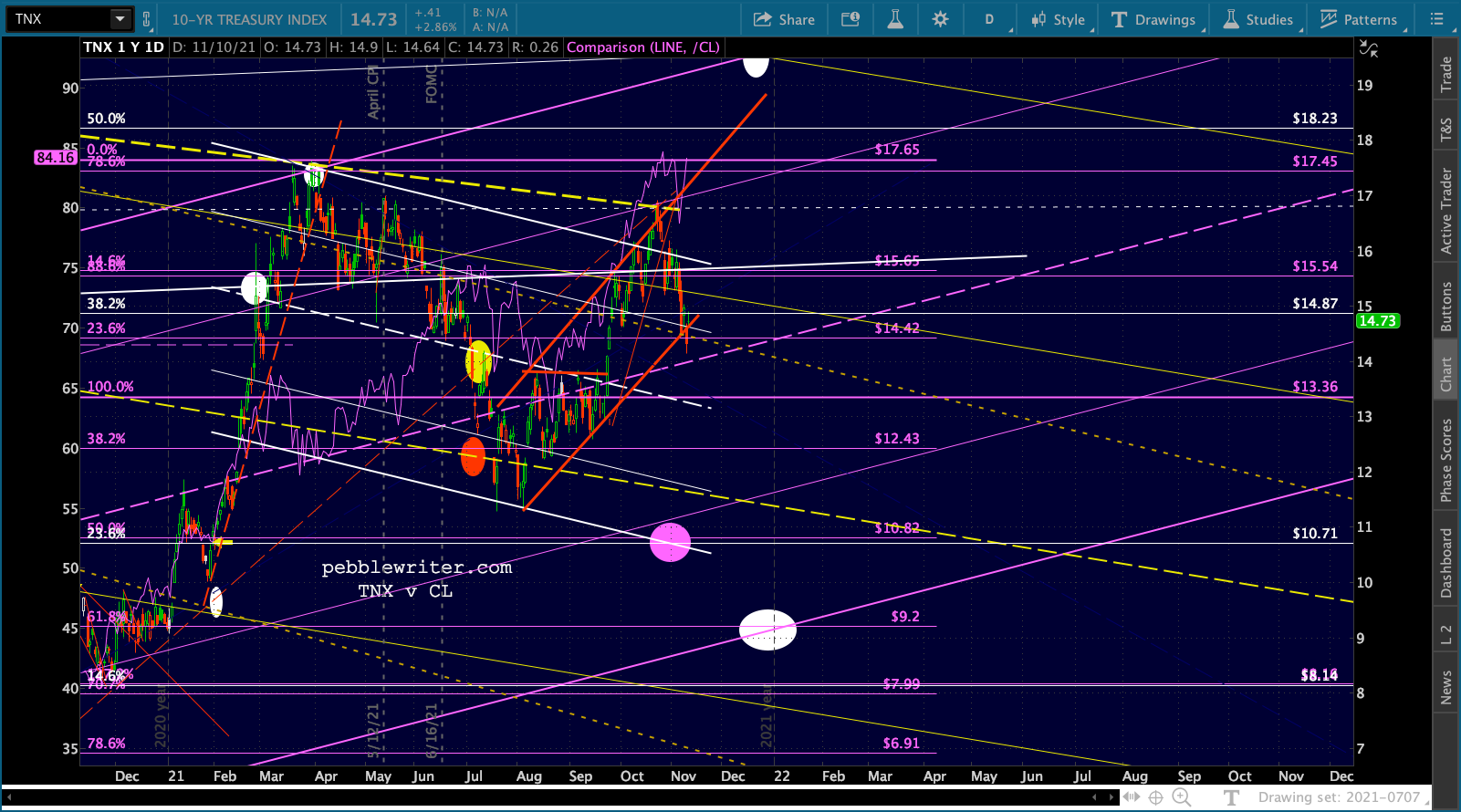

Last, TNX has rebounded back above the red channel bottom. An equity selloff would change that.

Last, TNX has rebounded back above the red channel bottom. An equity selloff would change that.

The reality is that the market could shrug off all the inflation news, including the likelihood of more aggressive tapering and rate hikes. But, at this point, the Fed needs a selloff in energy, a breakout in DXY, and a decline in interest rates that doesn’t rely on QE. It’s unlikely that these could all happen without a commensurate decline in equities.

The reality is that the market could shrug off all the inflation news, including the likelihood of more aggressive tapering and rate hikes. But, at this point, the Fed needs a selloff in energy, a breakout in DXY, and a decline in interest rates that doesn’t rely on QE. It’s unlikely that these could all happen without a commensurate decline in equities.

Stay tuned…