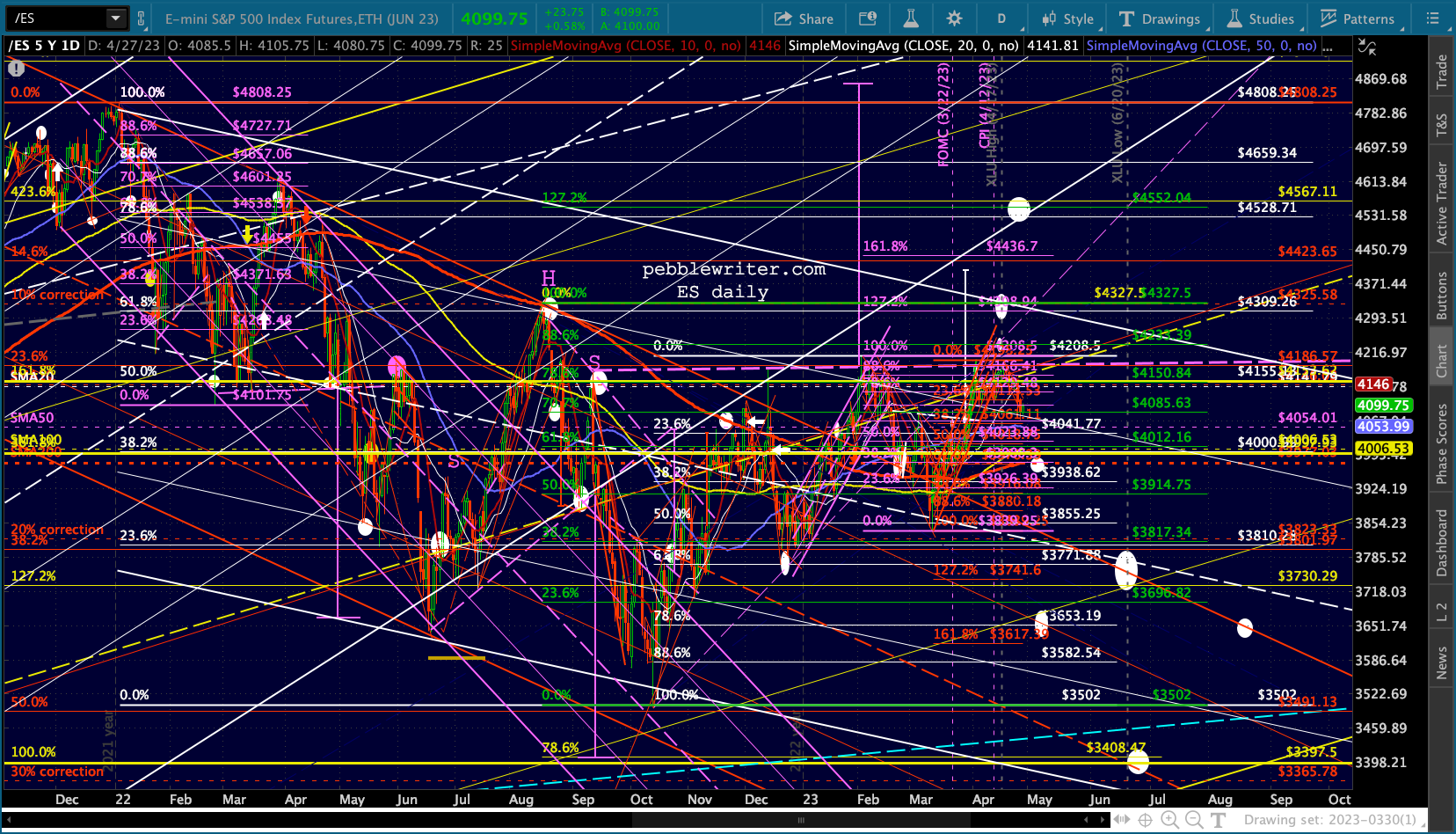

GDP increased at an annual rate of 1.1% versus expectations of over 2% and Q4’s 2.6%, fueling both recession fears and expectations that the Fed will soon halt rate hikes after next week’s 25 bps increase.

Futures dipped on the news but have since rebounded as the usual VIX smackdown convinced algos to look on the bright side.

For now, algos are ignoring the hotter Q1 PCE data embedded in the GDP print.

continued for members…

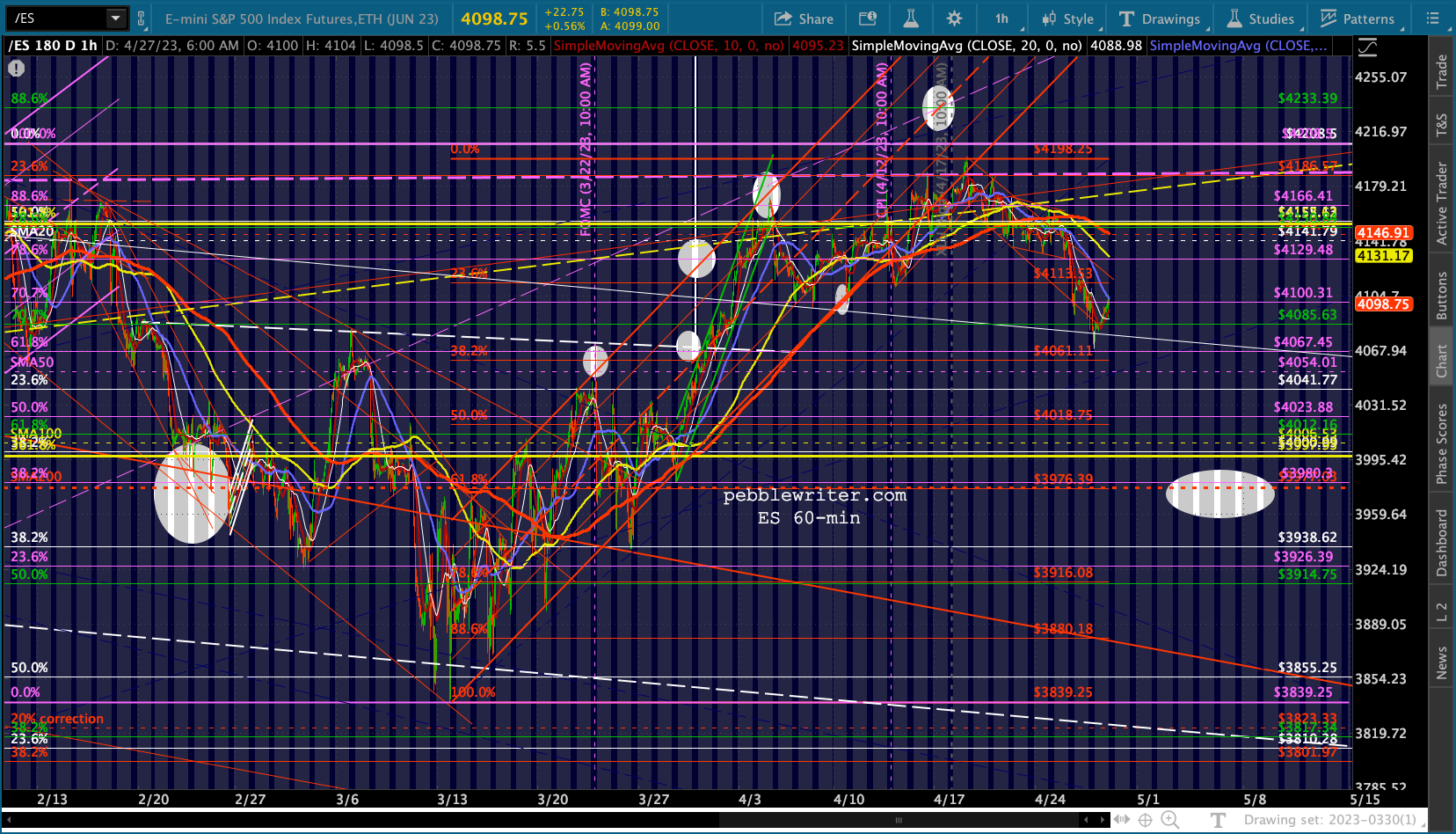

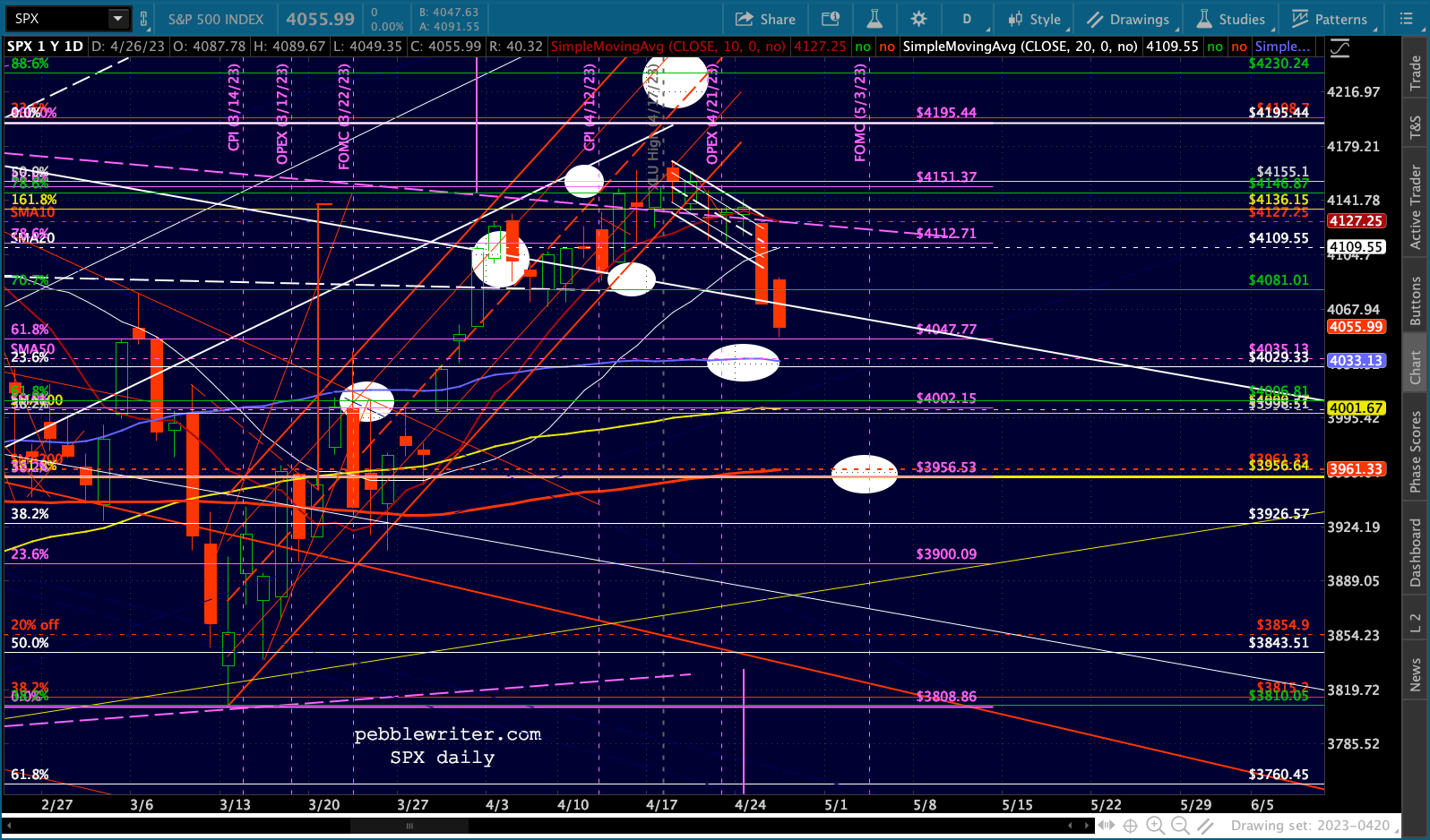

It remains to be seen whether or not we’re already in the pre-FOMC (next Wednesday) and pre-PCE print (Friday) ramp up.

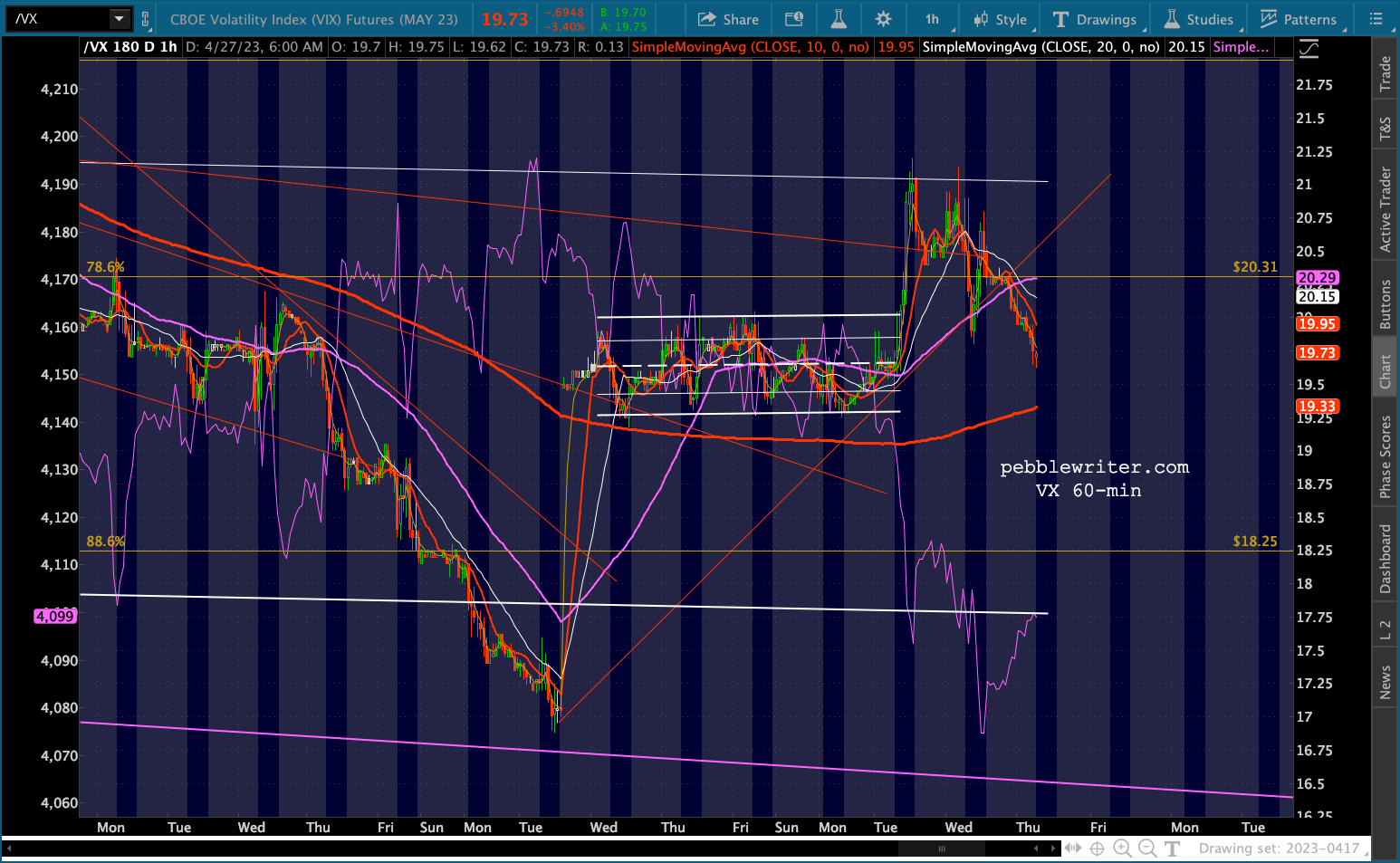

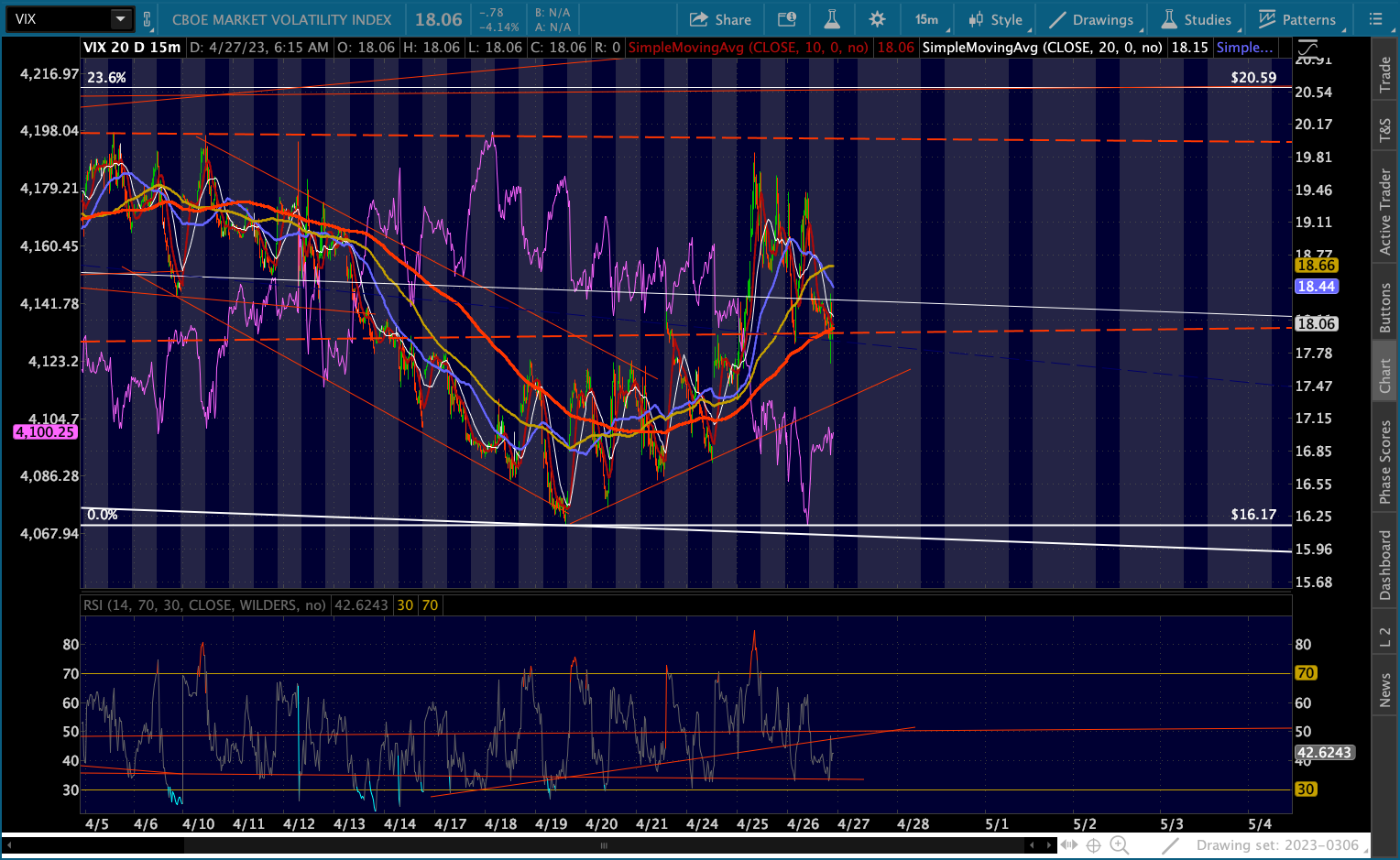

VIX could drop even lower without breaking down.

VIX could drop even lower without breaking down. Probably the most important chart to watch today…

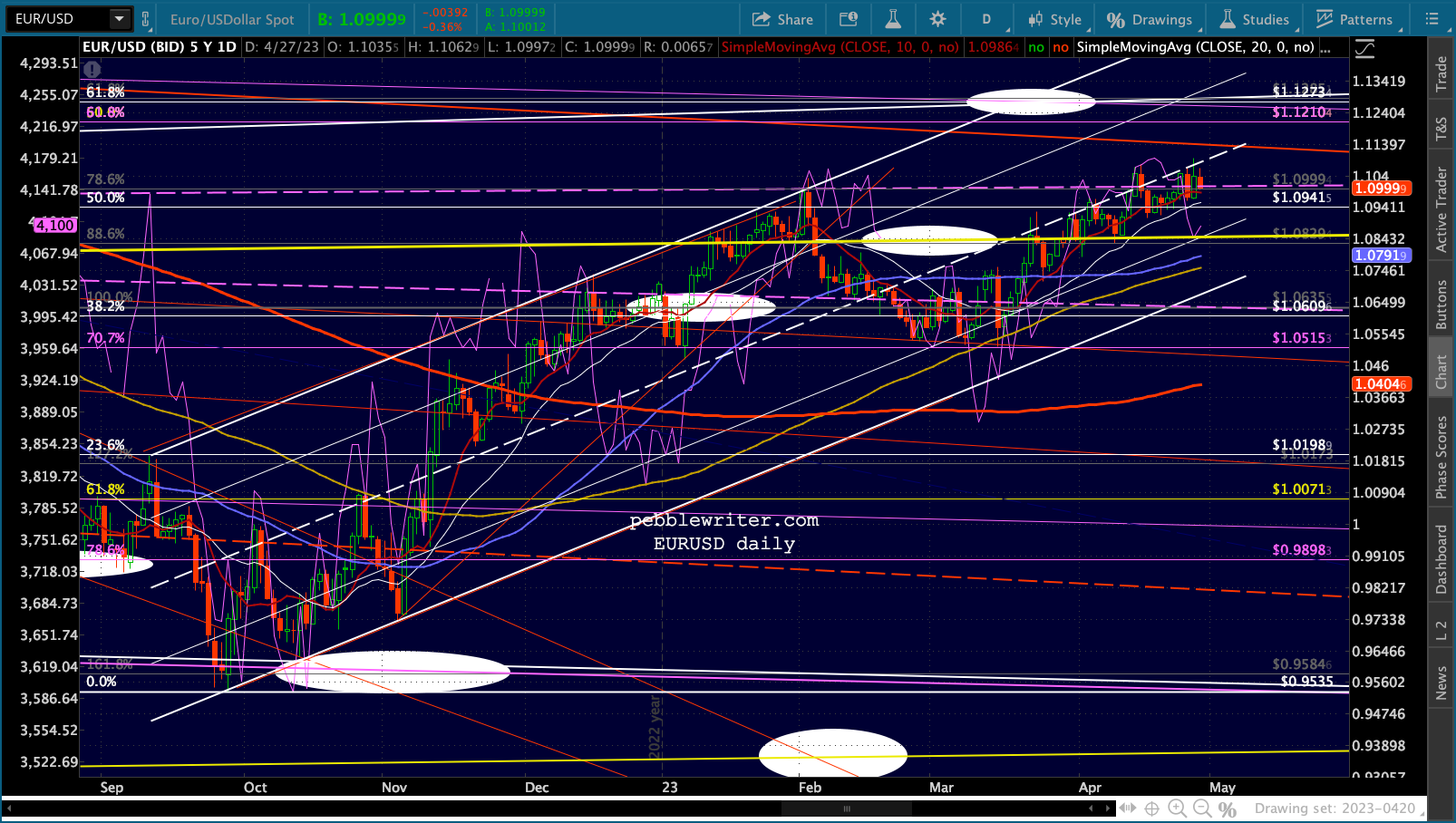

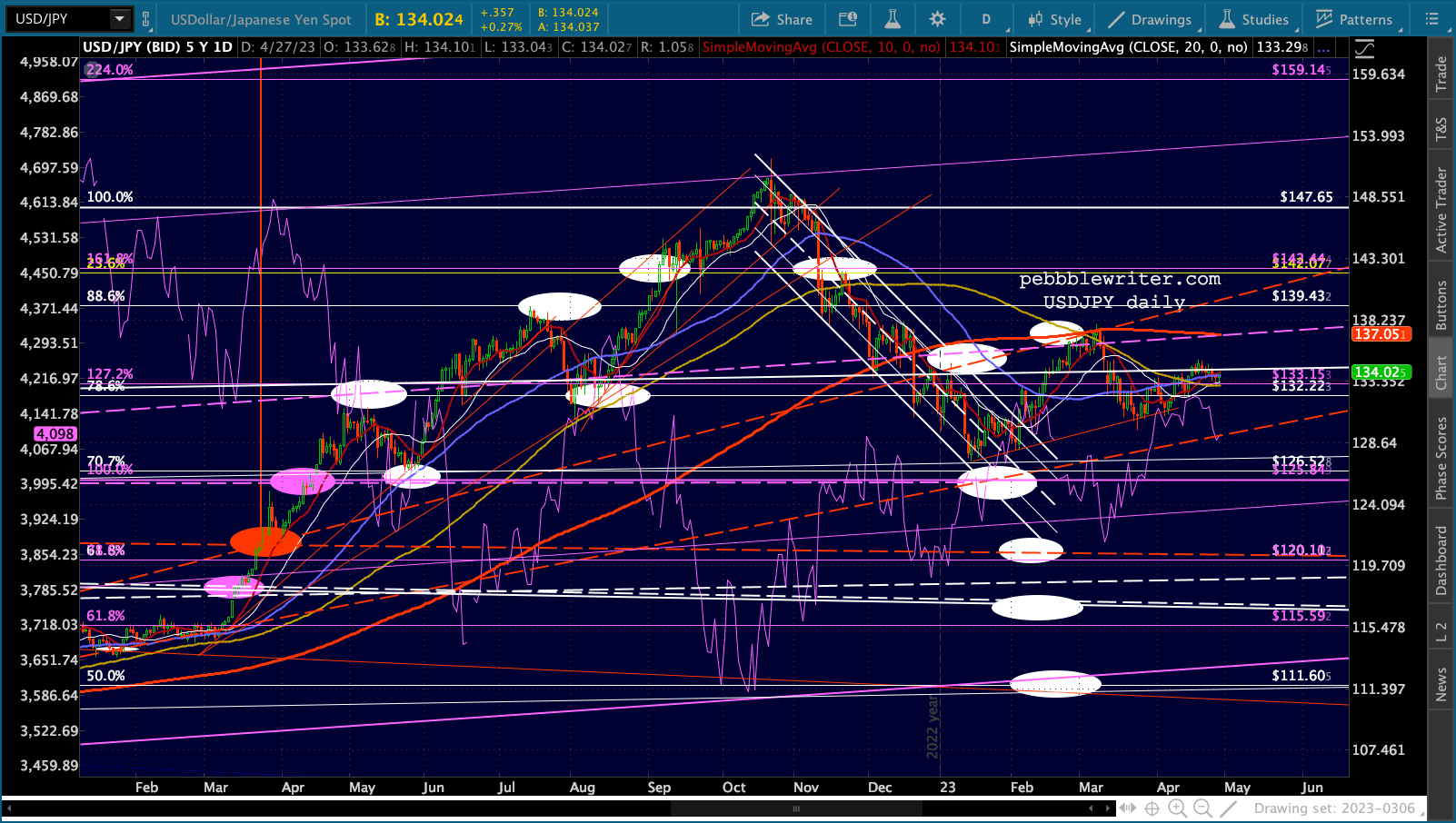

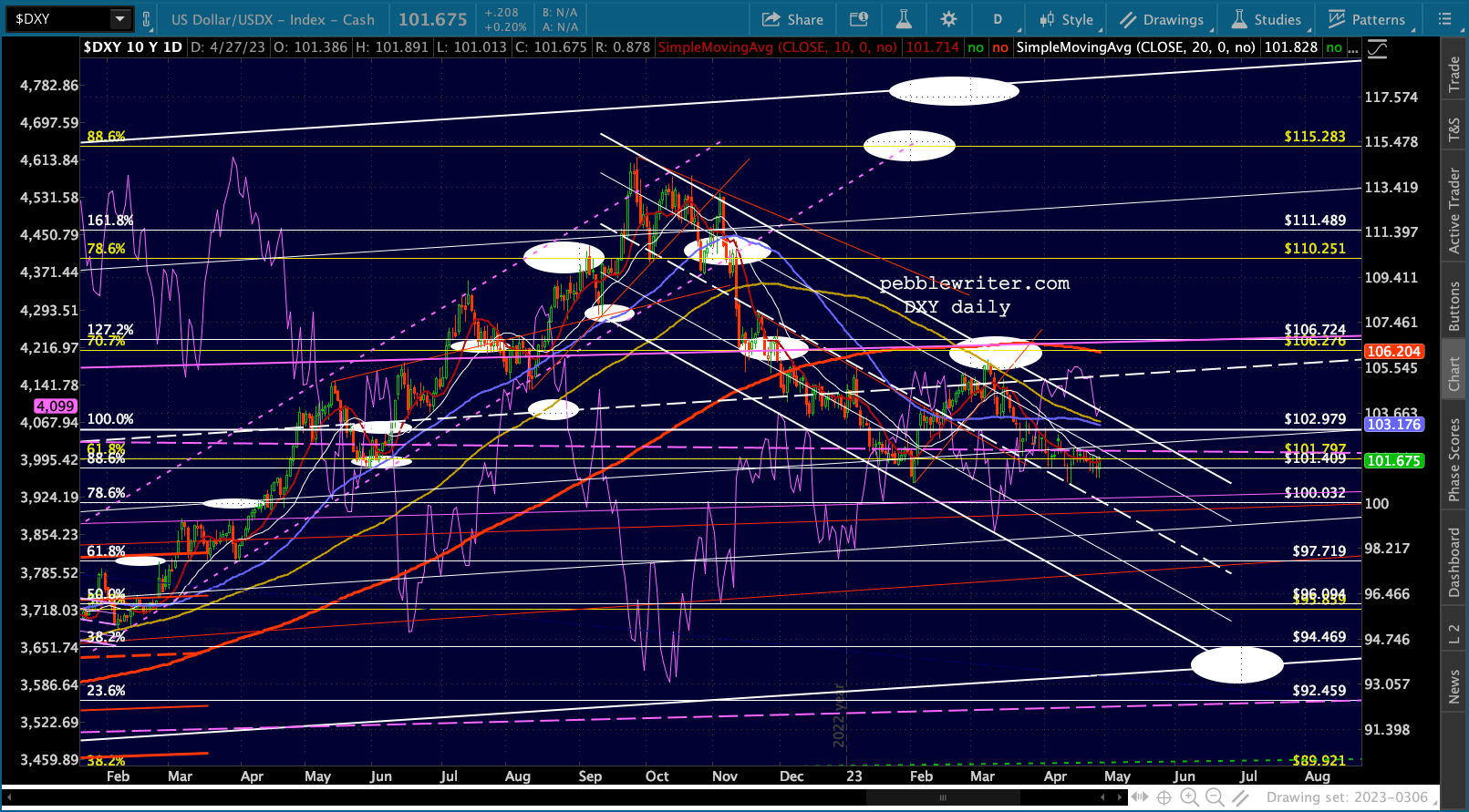

Probably the most important chart to watch today… Needless to say, the weak GDP print hasn’t helped the DXY. In strengthening the argument for a Fed pause/pivot, it also boosts the odds of euro-based rates outpacing USD ones. Of course, that argument depends on an acceptable March PCE print on Friday.

Needless to say, the weak GDP print hasn’t helped the DXY. In strengthening the argument for a Fed pause/pivot, it also boosts the odds of euro-based rates outpacing USD ones. Of course, that argument depends on an acceptable March PCE print on Friday.

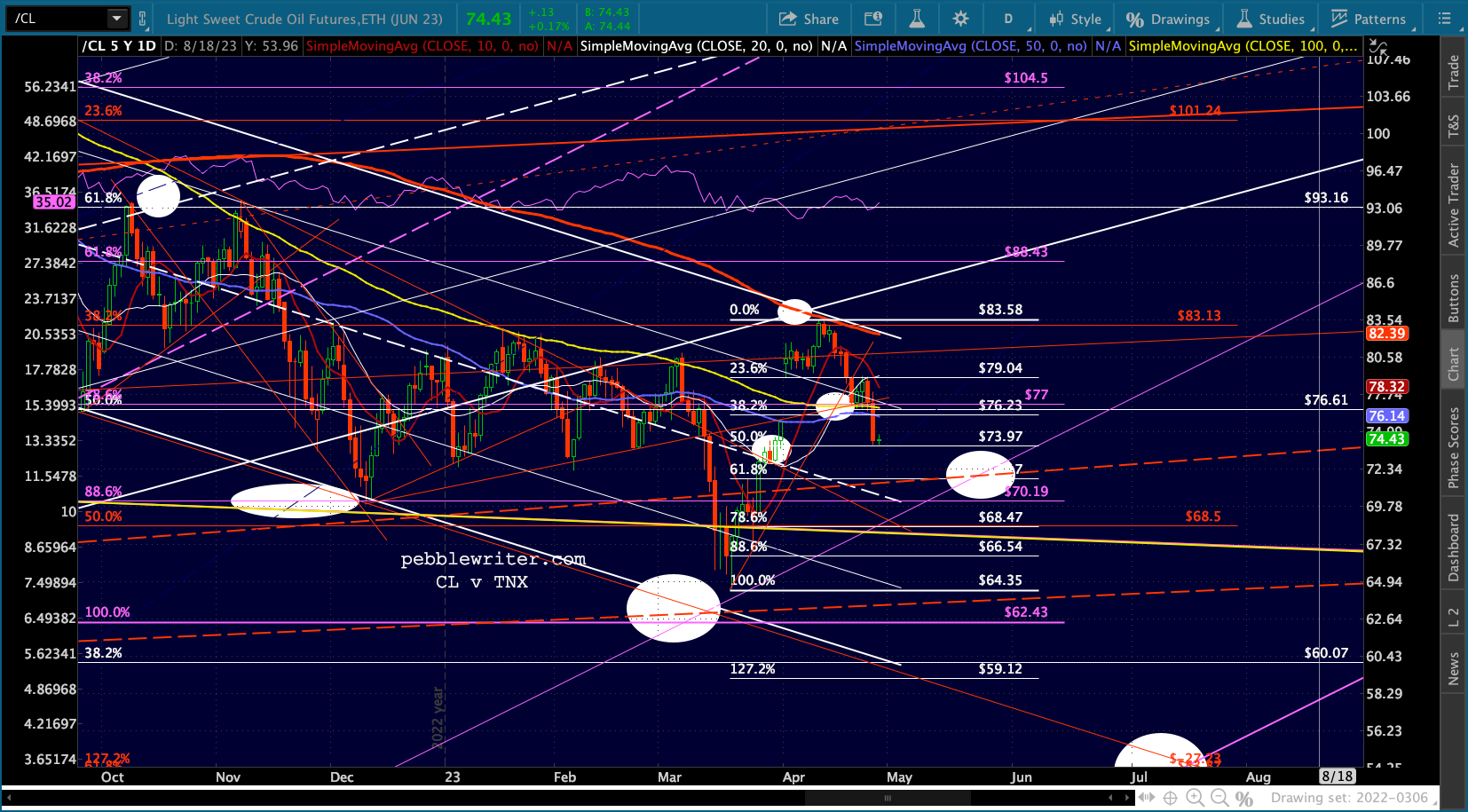

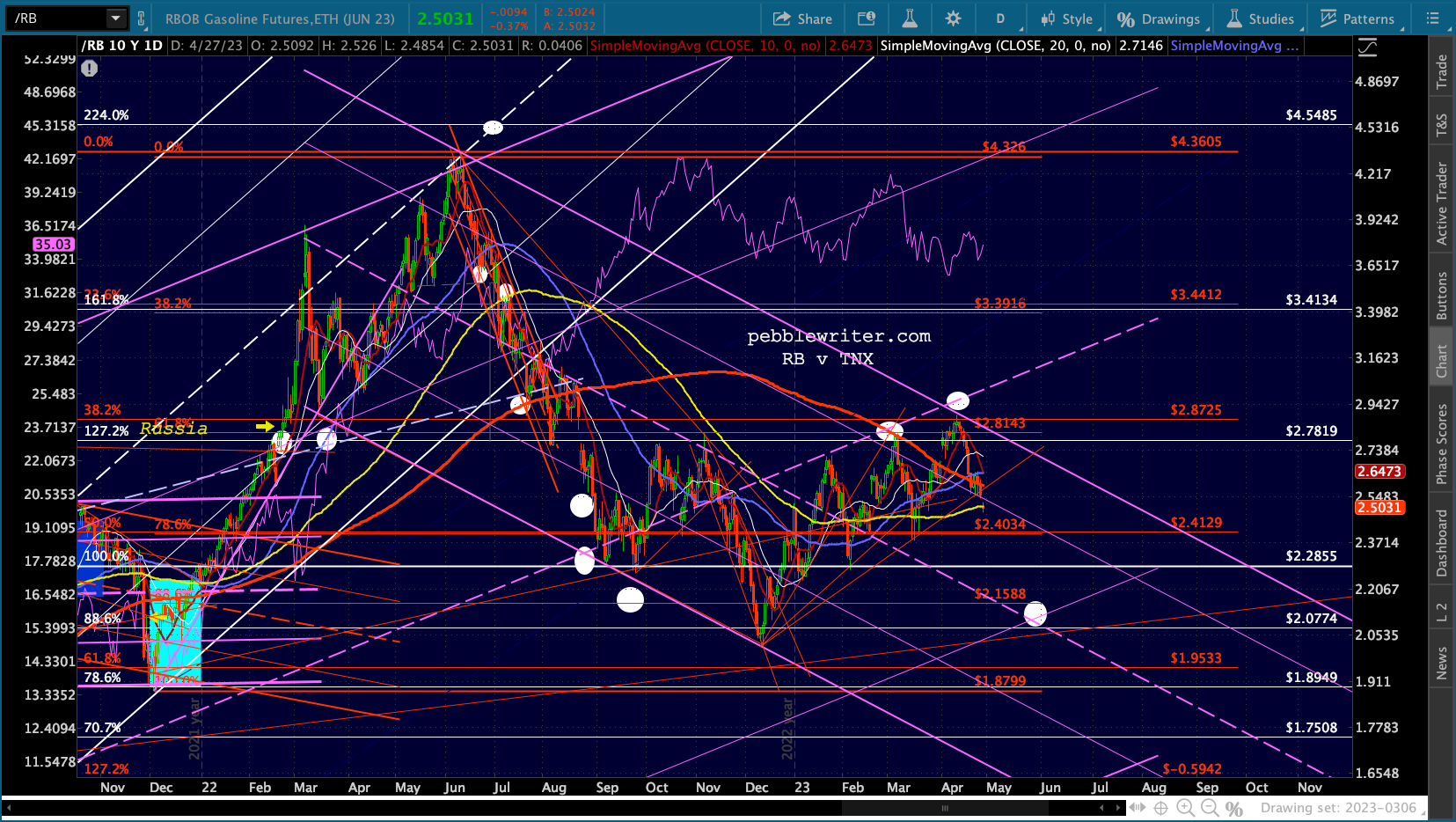

CL is holding yesterday’s lows, but RB has finally broken down and is clinging to its SMA100.

CL is holding yesterday’s lows, but RB has finally broken down and is clinging to its SMA100.

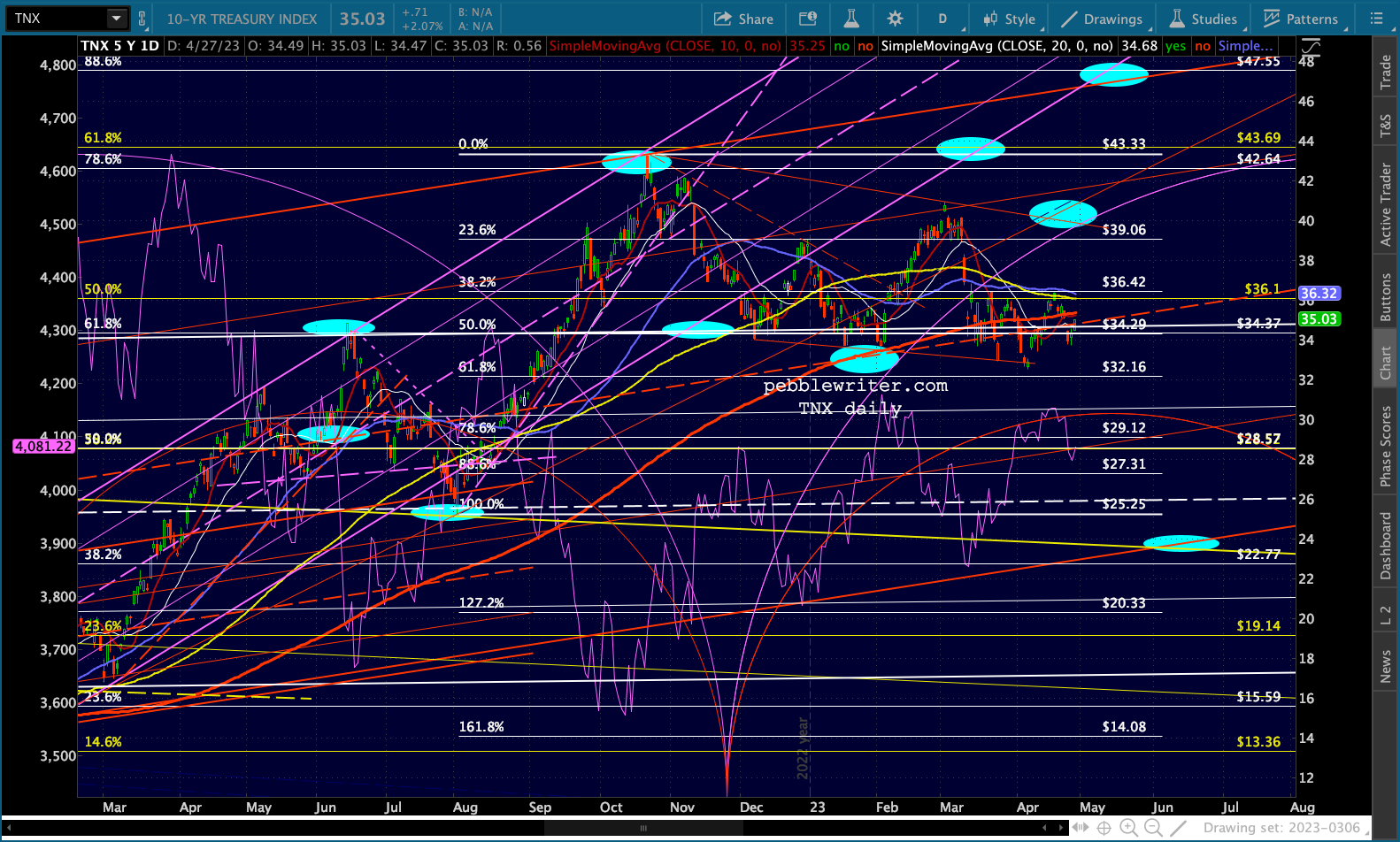

The equity bounce sees the 2Y back above 4% and the 2s10s back below -50 bps.

The equity bounce sees the 2Y back above 4% and the 2s10s back below -50 bps.