There’s something in March’s durable orders report for both bulls and bears. The 3.2% topline number was wildly better than the 0.7% expected and -1.2% previous. But, it was driven primarily by large Boeing orders.

Non-defense capital goods excluding aircraft, a proxy for business spending plans, dropped 0.4%. And core shipping logged another 0.4% drop.

Non-defense capital goods excluding aircraft, a proxy for business spending plans, dropped 0.4%. And core shipping logged another 0.4% drop.

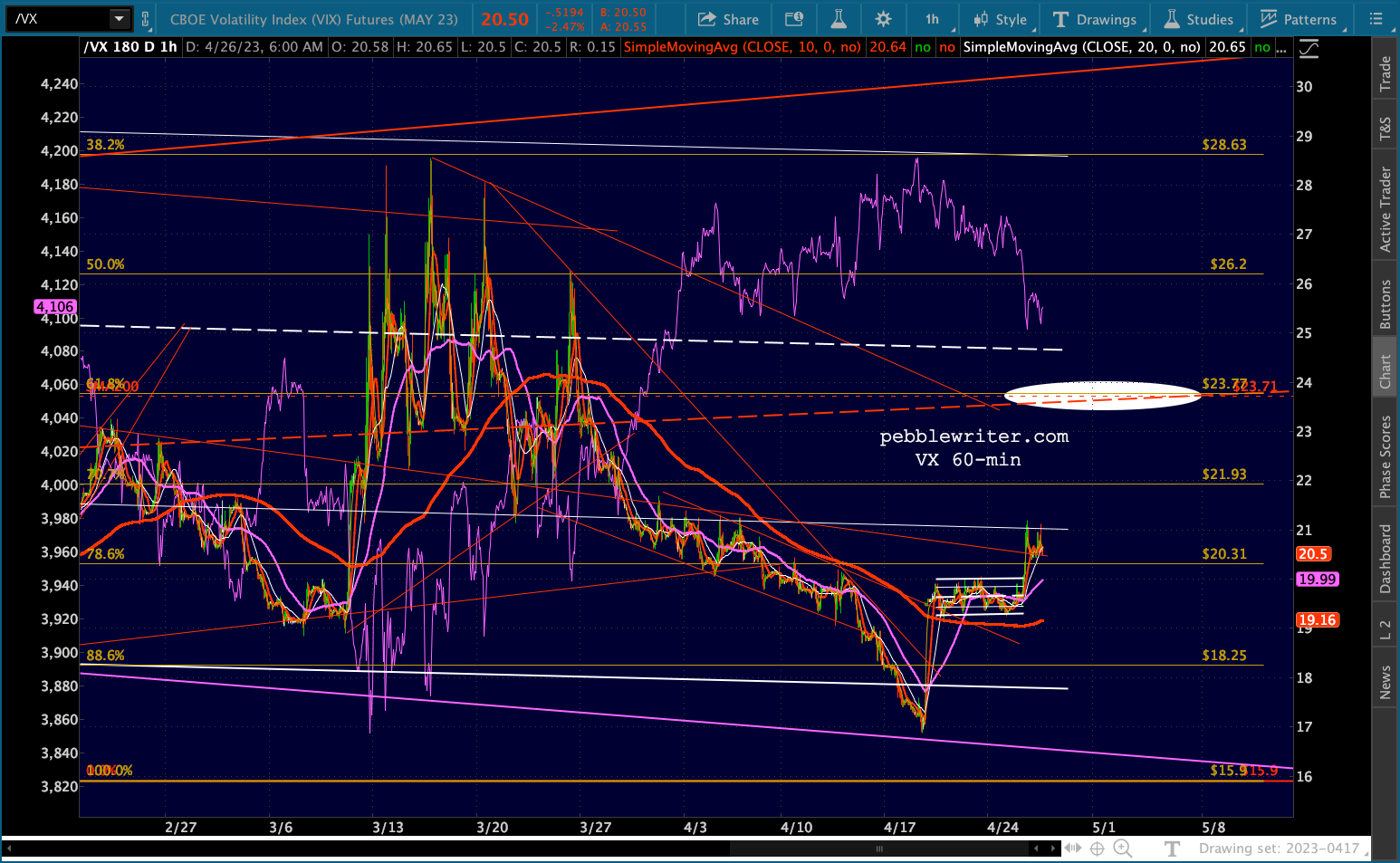

Stocks were little phased, as they’re still marching to VIX’s drumbeat. But, the 2Y is back below 4% as First Republic reminds us that the banking crisis has not gone away.

continued for members…

…which in turn revives warnings around the 2s10s breaking out.

…which in turn revives warnings around the 2s10s breaking out. The equity picture hasn’t changed.

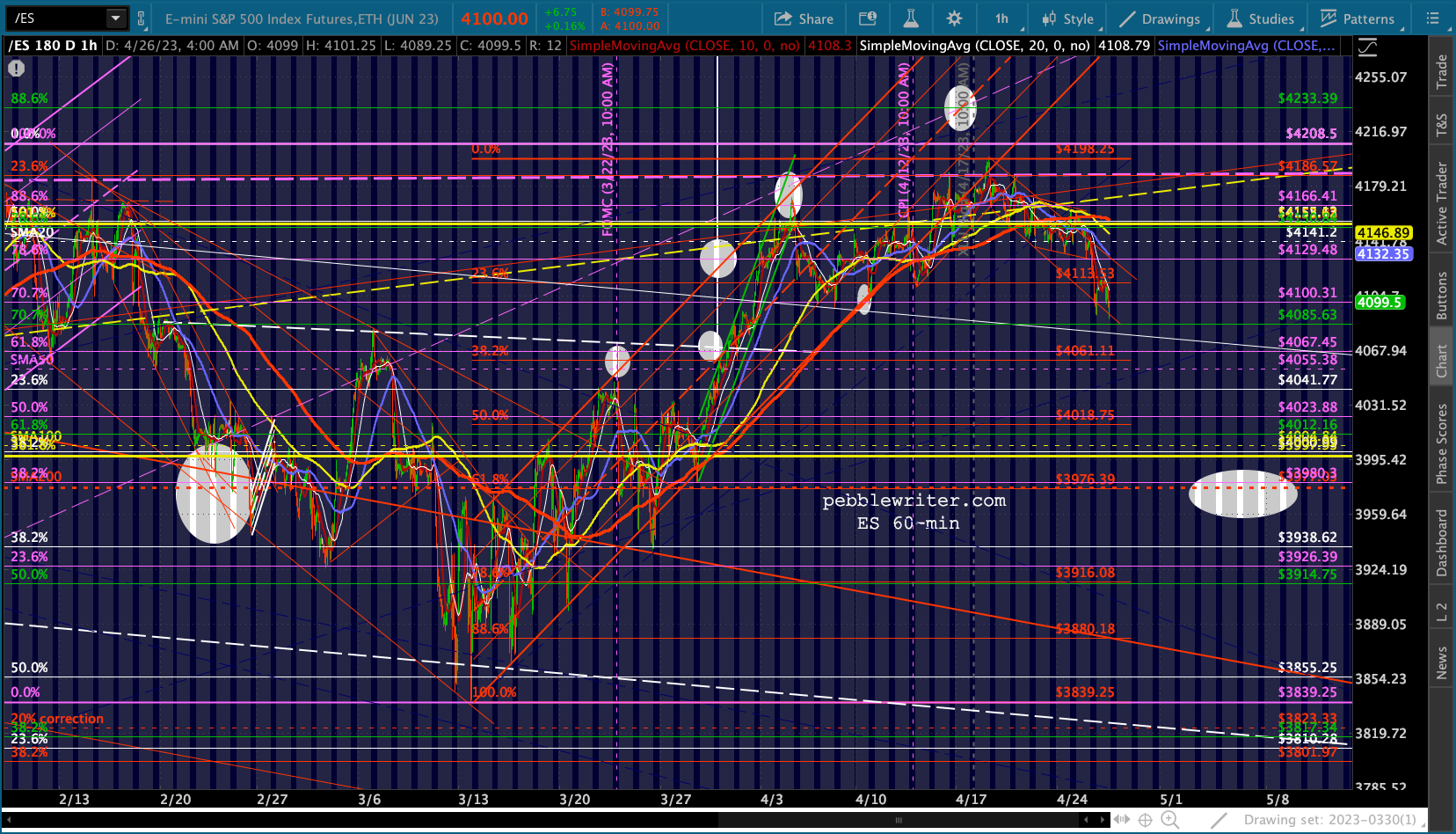

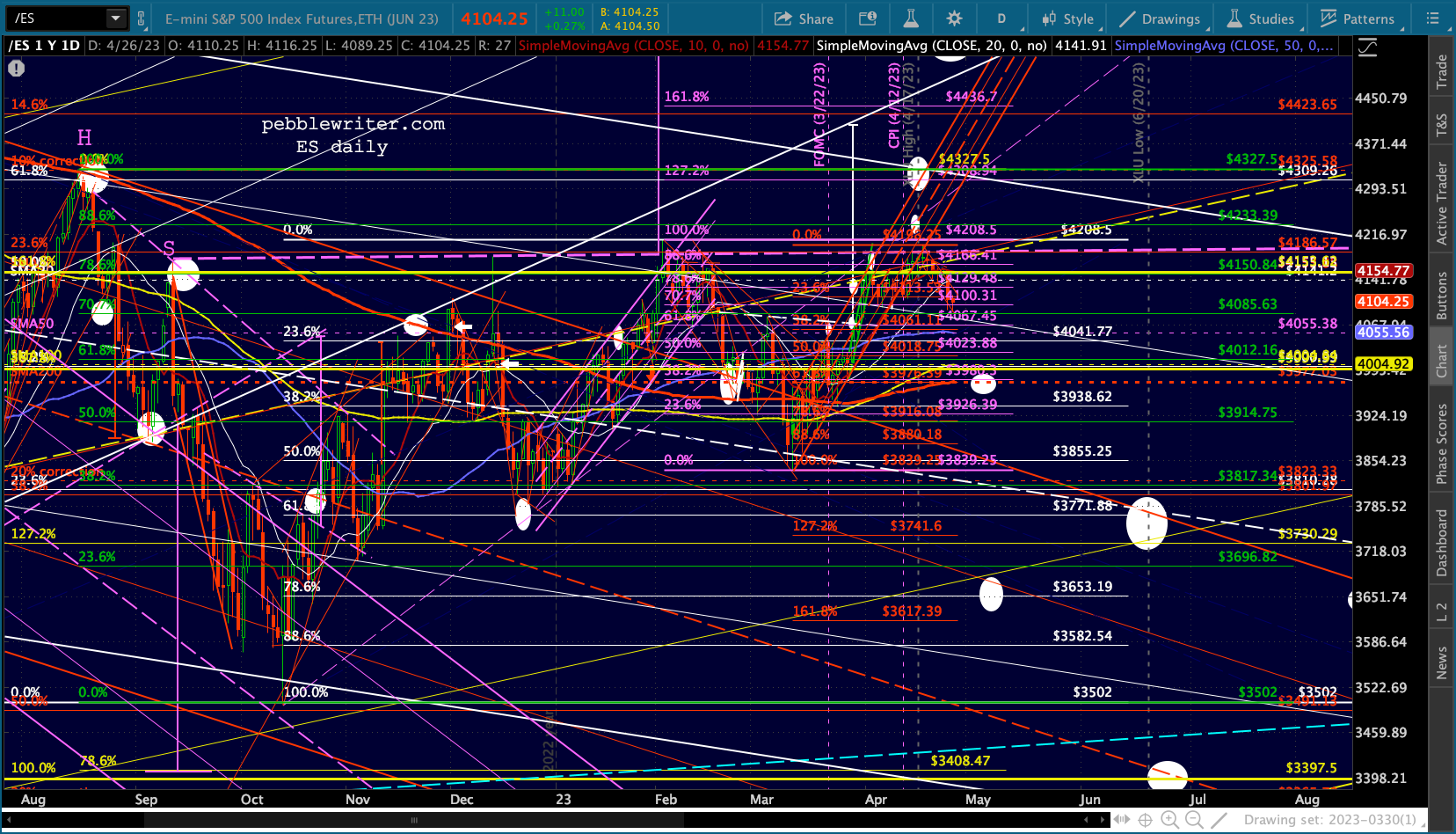

The equity picture hasn’t changed.

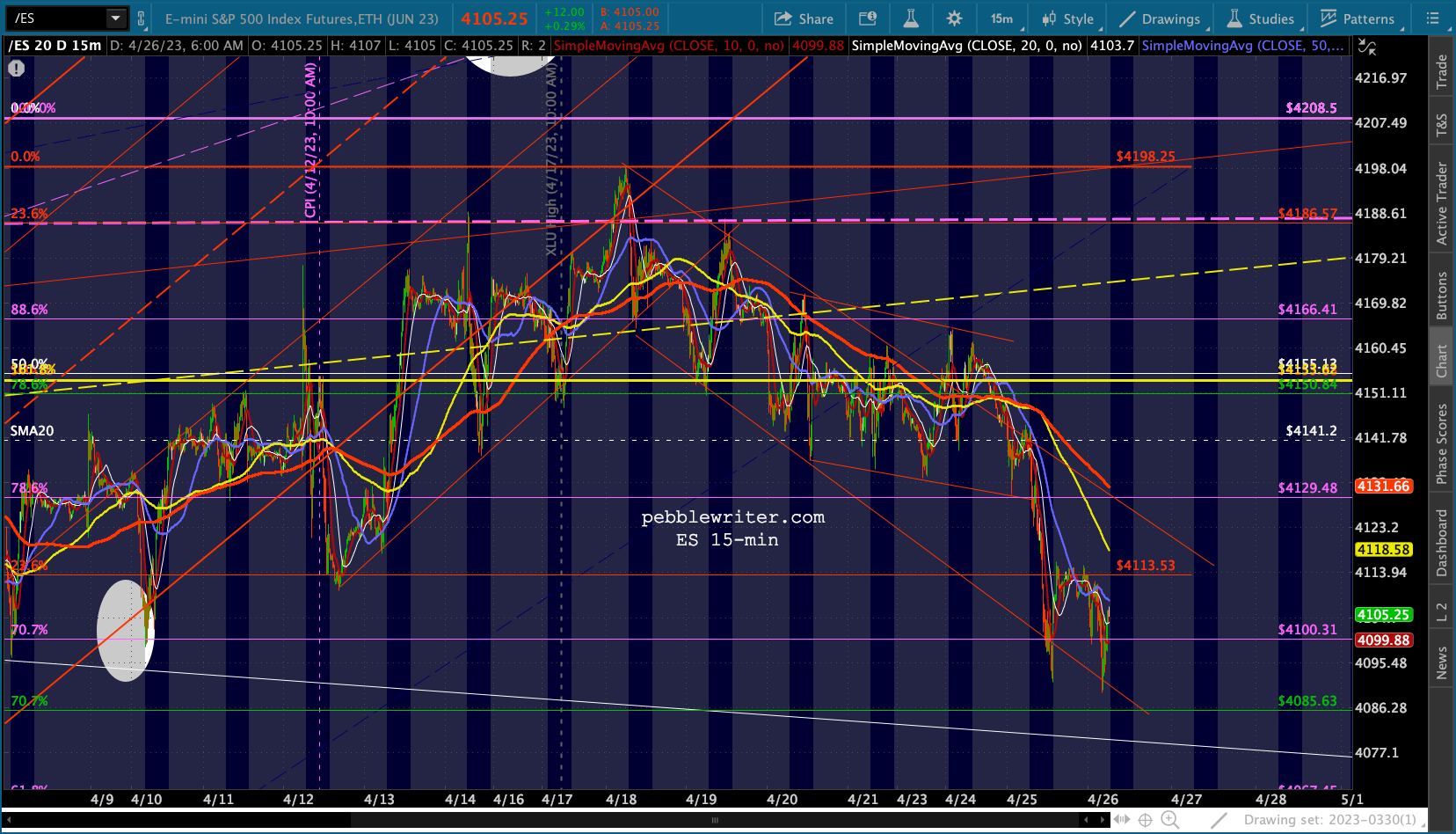

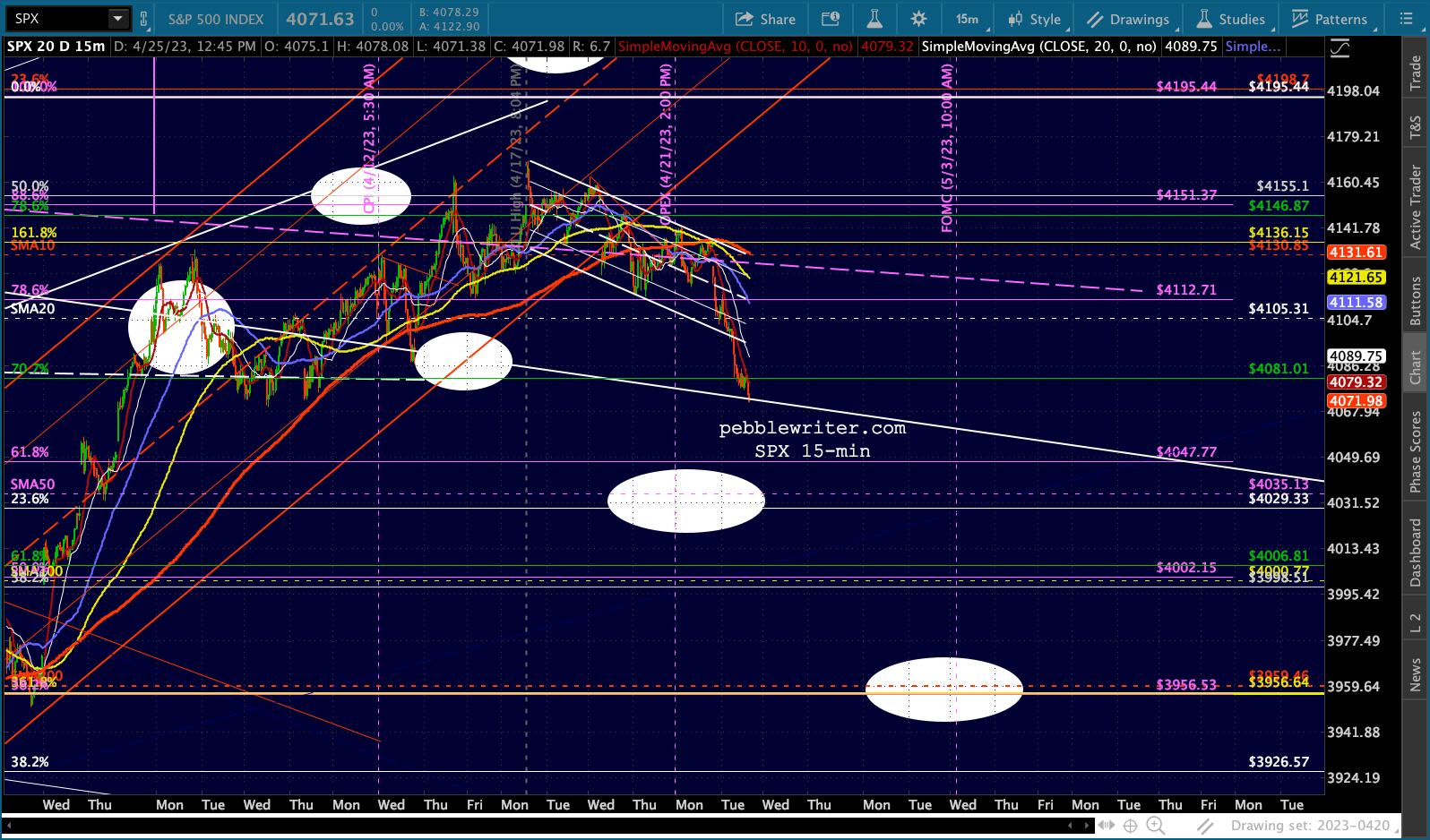

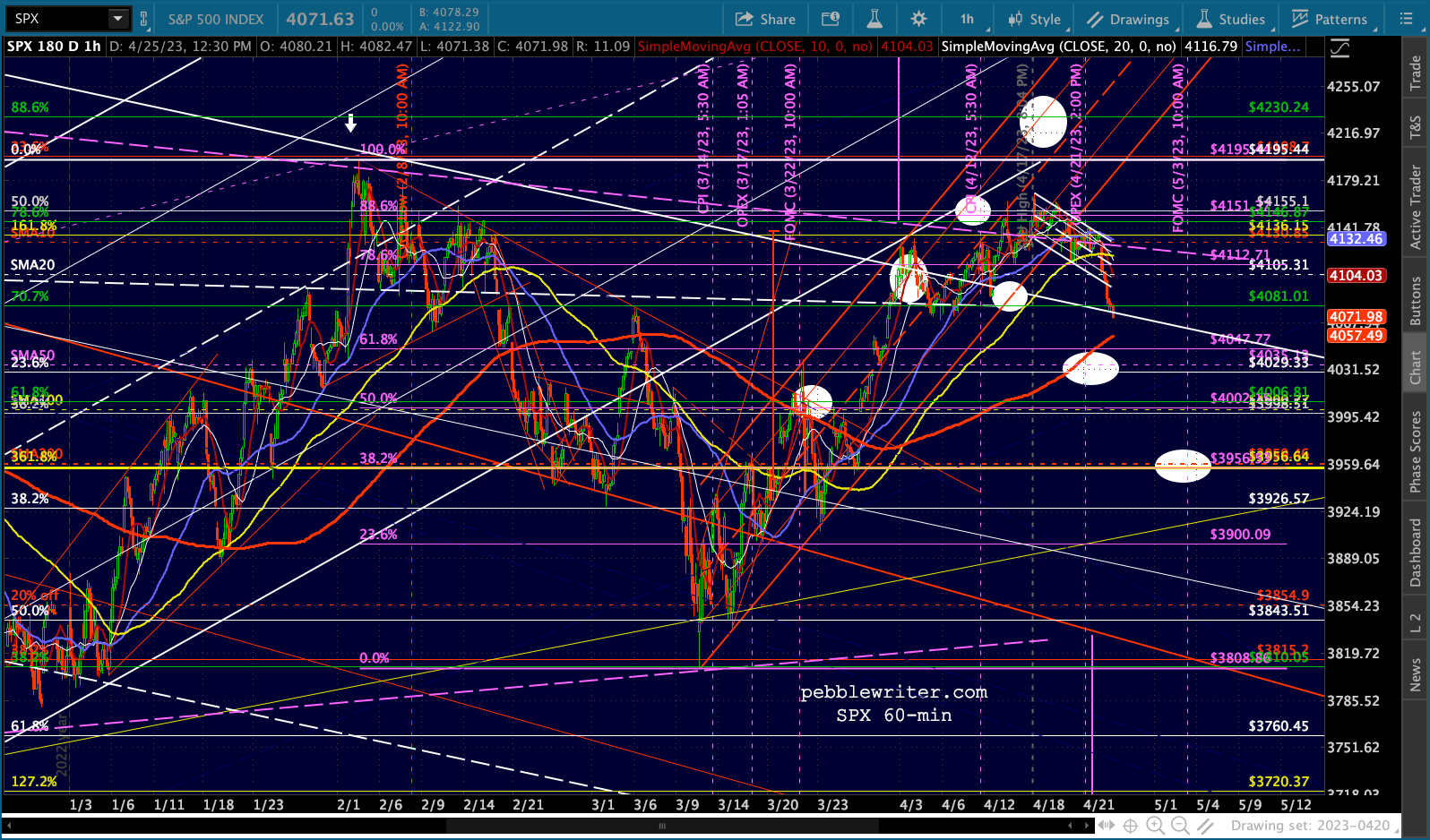

ES’ and SPX’s SMA10s have rolled over and are within a day or two of crossing below the SMA20s.

ES’ and SPX’s SMA10s have rolled over and are within a day or two of crossing below the SMA20s.

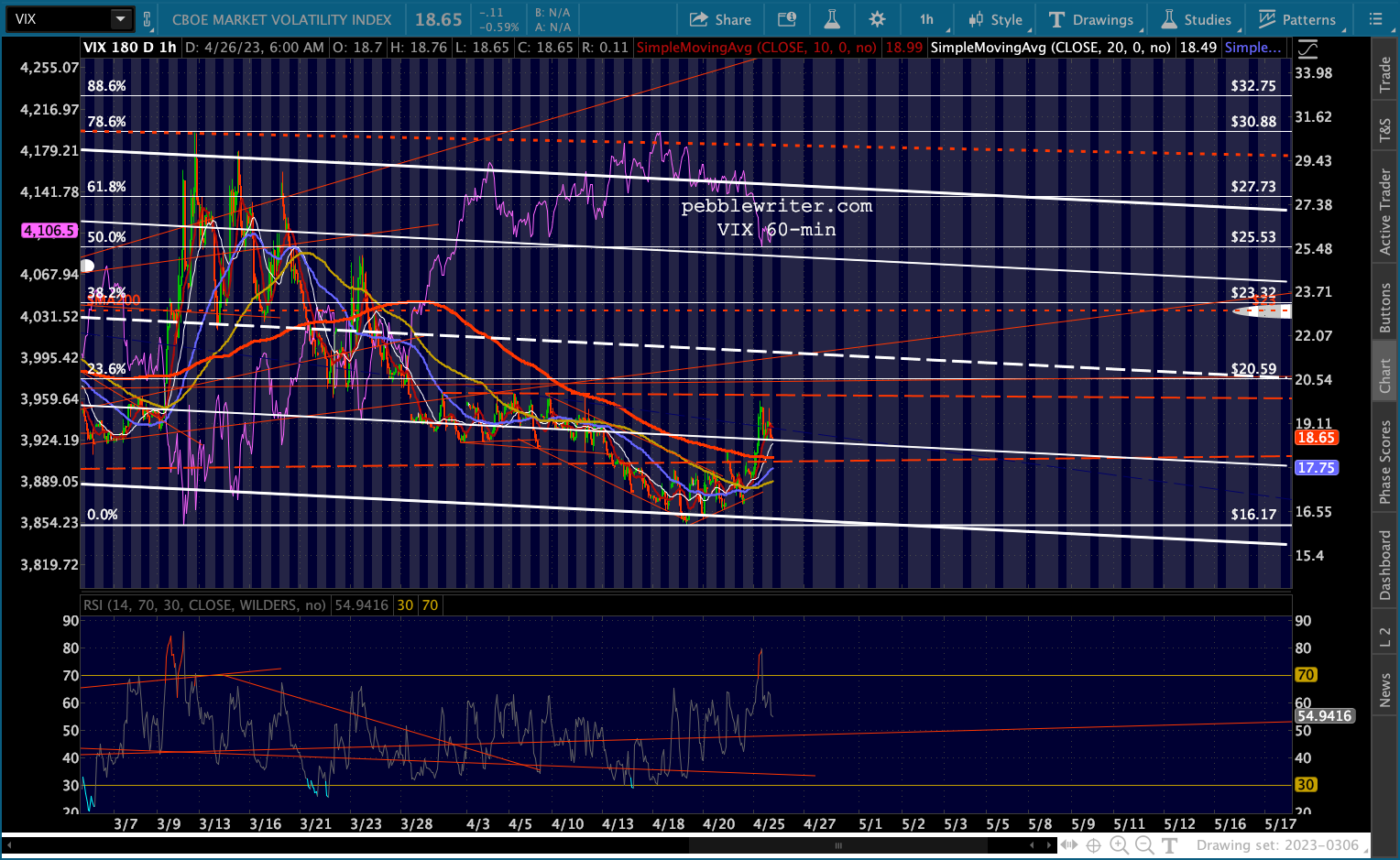

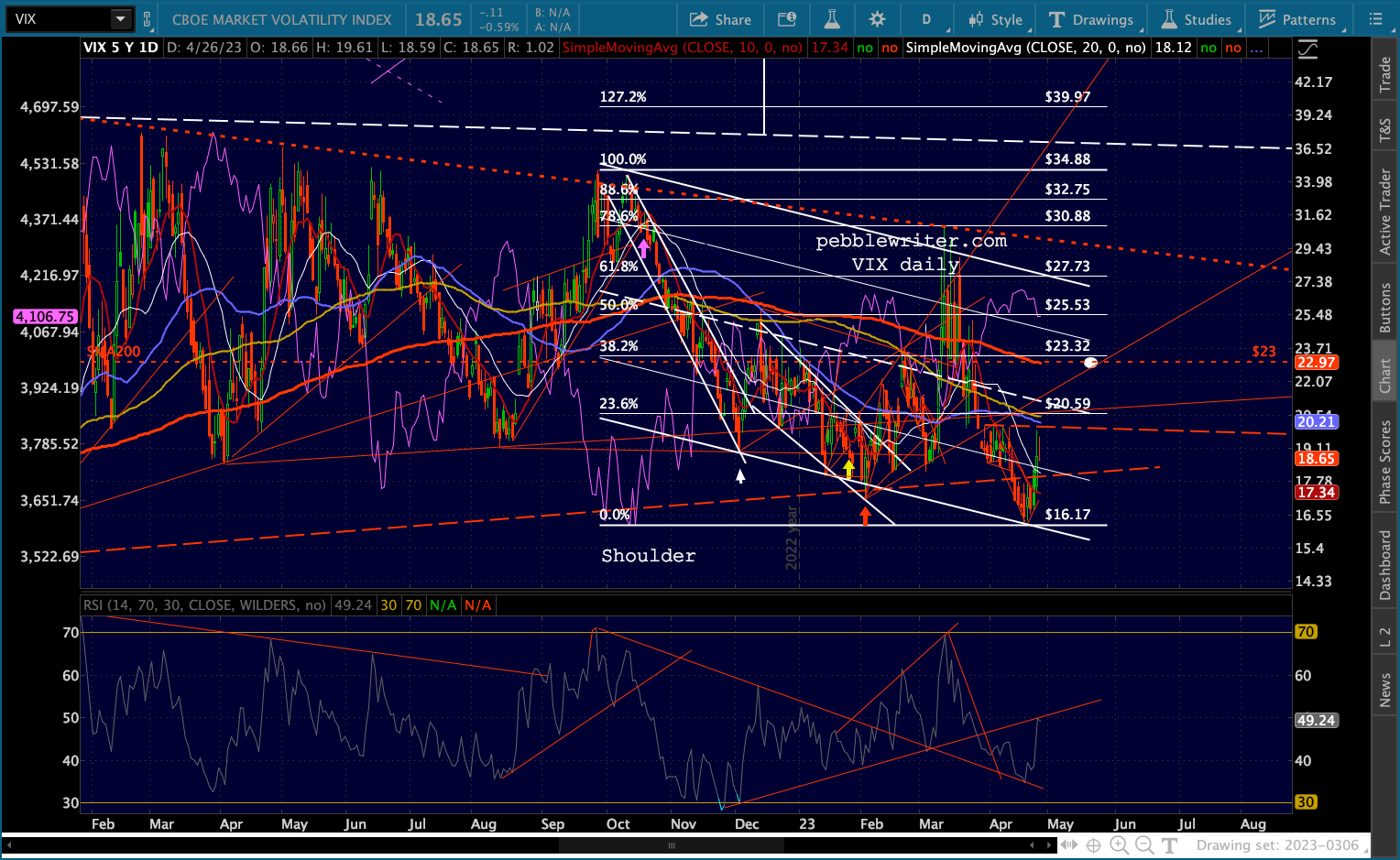

Note that VIX’s RSI has reached the important overhead resistance trendline – previously support. If it punches through, the current equity selloff will gain momentum.

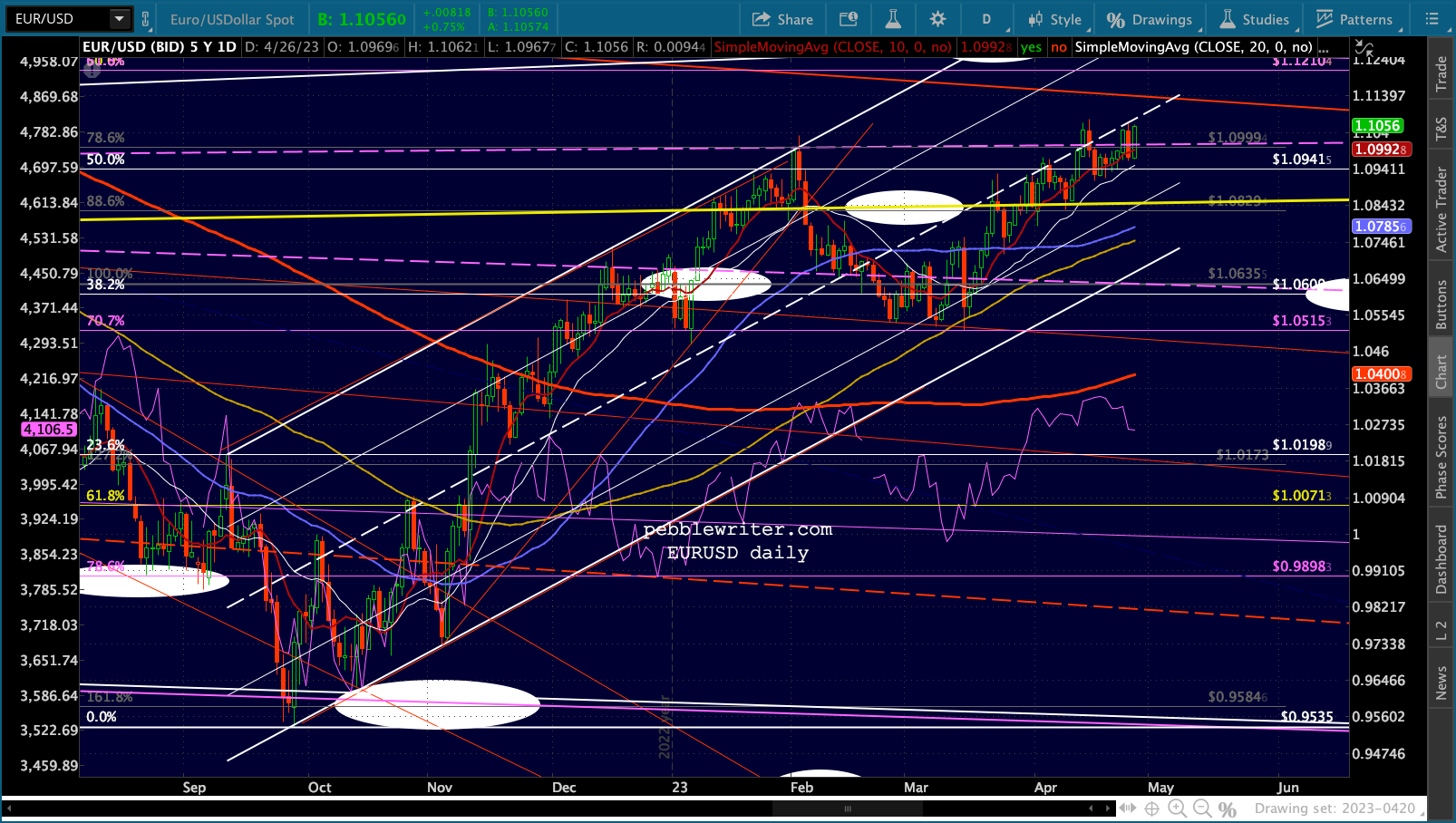

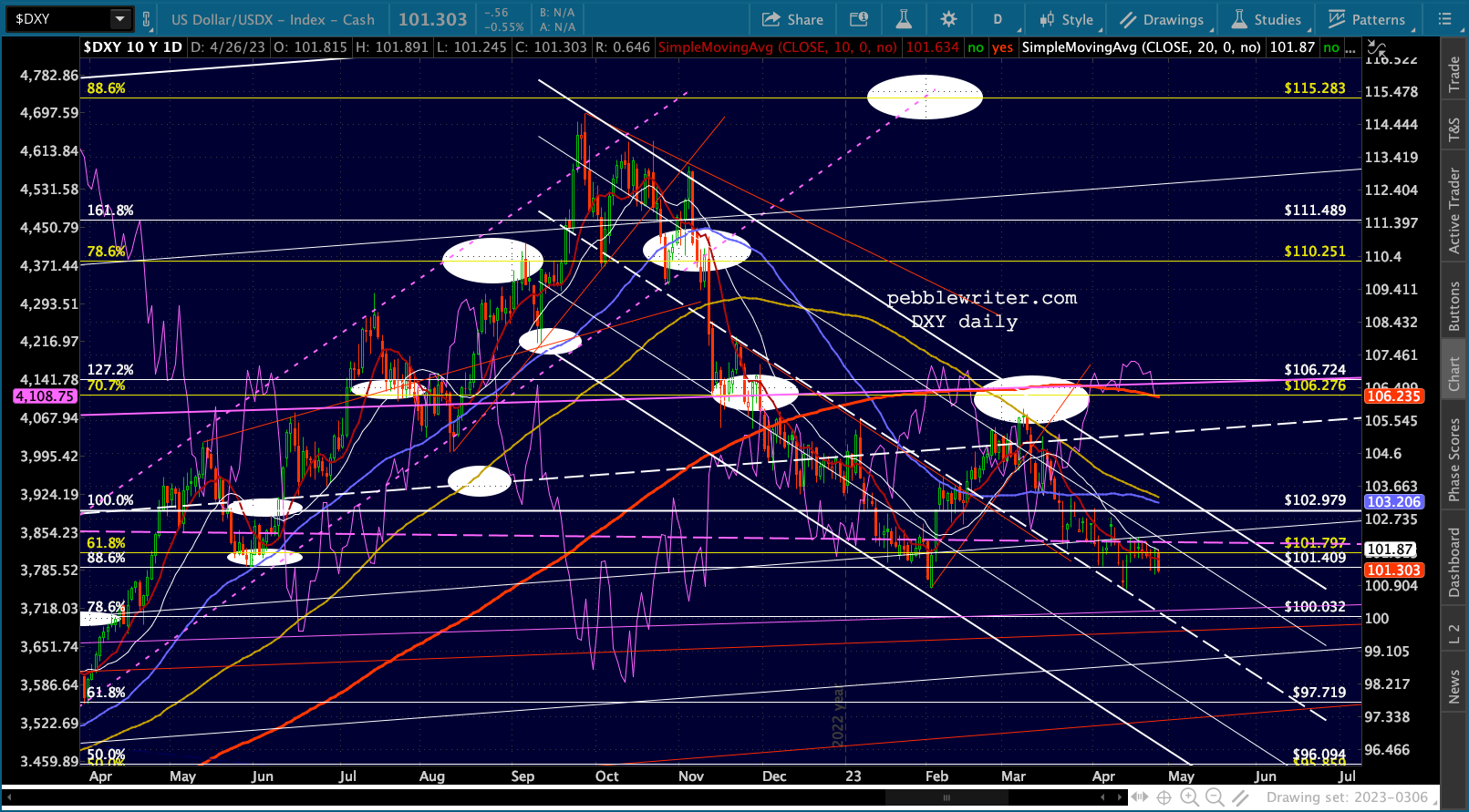

Note that VIX’s RSI has reached the important overhead resistance trendline – previously support. If it punches through, the current equity selloff will gain momentum. Currencies are working to prop up stocks this morning, with the euro pushing to higher highs and the DXY taking it on the chin.

Currencies are working to prop up stocks this morning, with the euro pushing to higher highs and the DXY taking it on the chin.

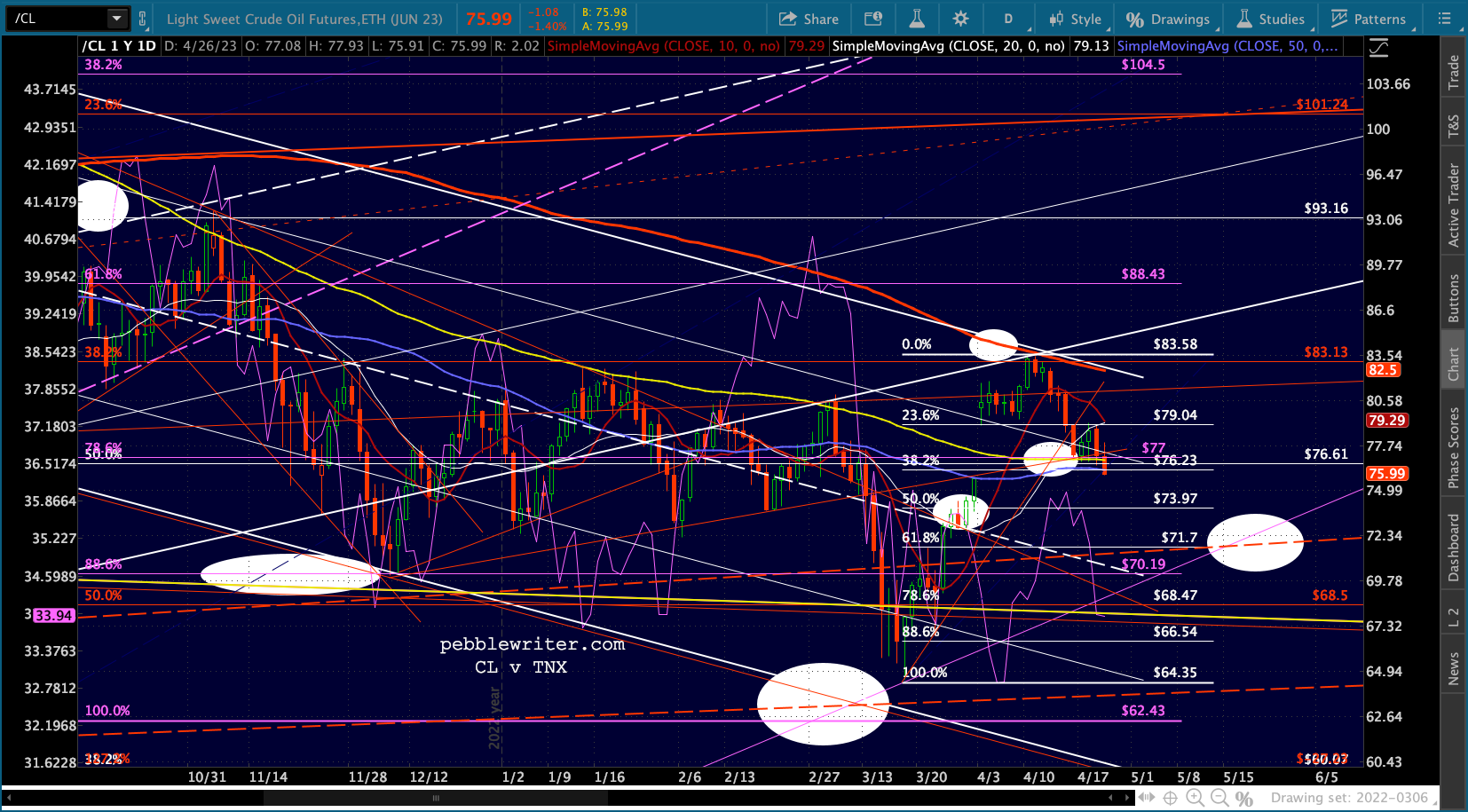

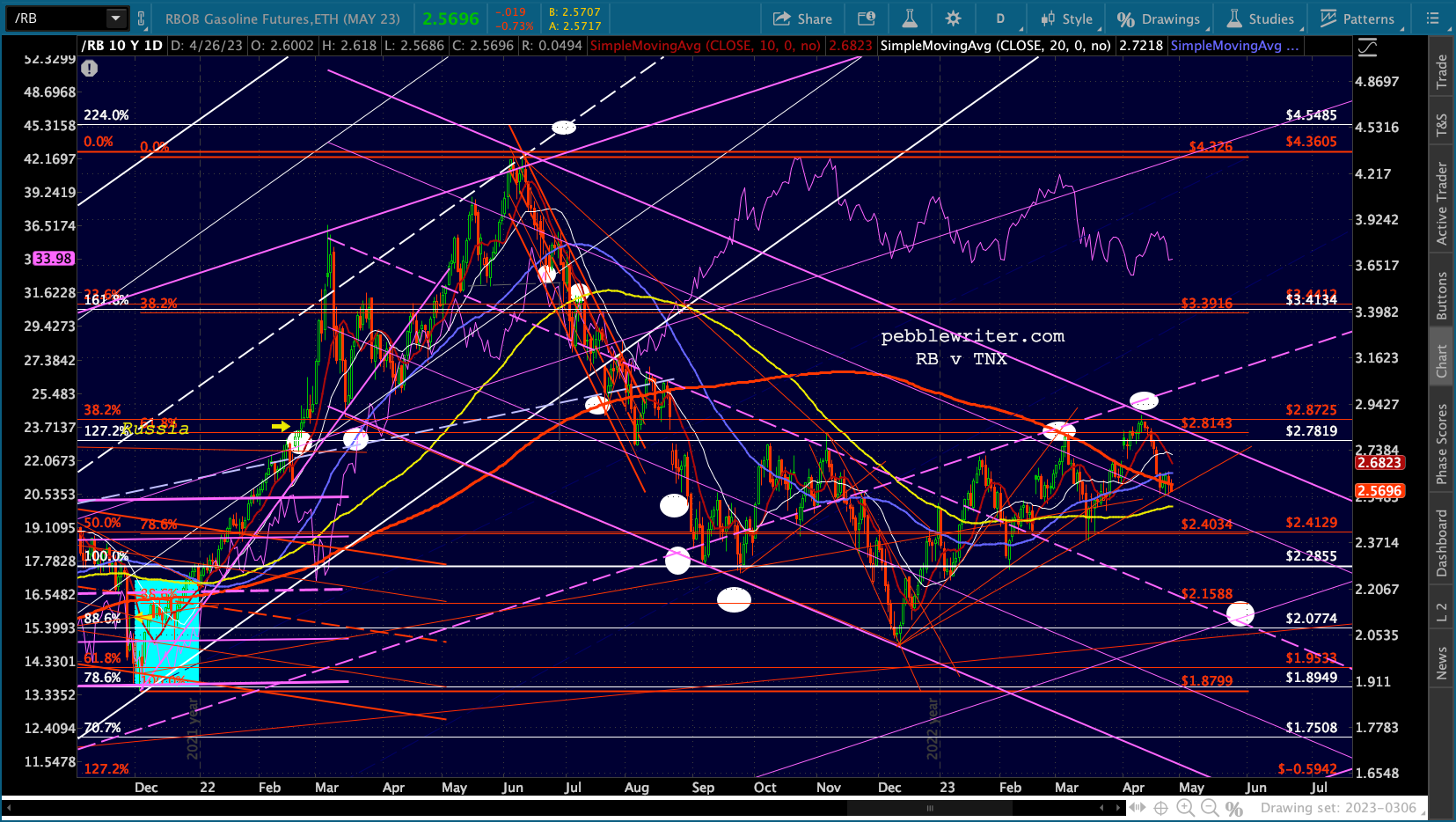

But, CL’s breakdown and the recent OPEX+ maneuver’s failure are now pretty obvious. CL has nearly closed the gap from Mar 31 and a SMA10/20 cross is in the works. RB has already seen a 10/20 cross, but still hasn’t broken down.

But, CL’s breakdown and the recent OPEX+ maneuver’s failure are now pretty obvious. CL has nearly closed the gap from Mar 31 and a SMA10/20 cross is in the works. RB has already seen a 10/20 cross, but still hasn’t broken down.

Stay tuned…

Stay tuned…