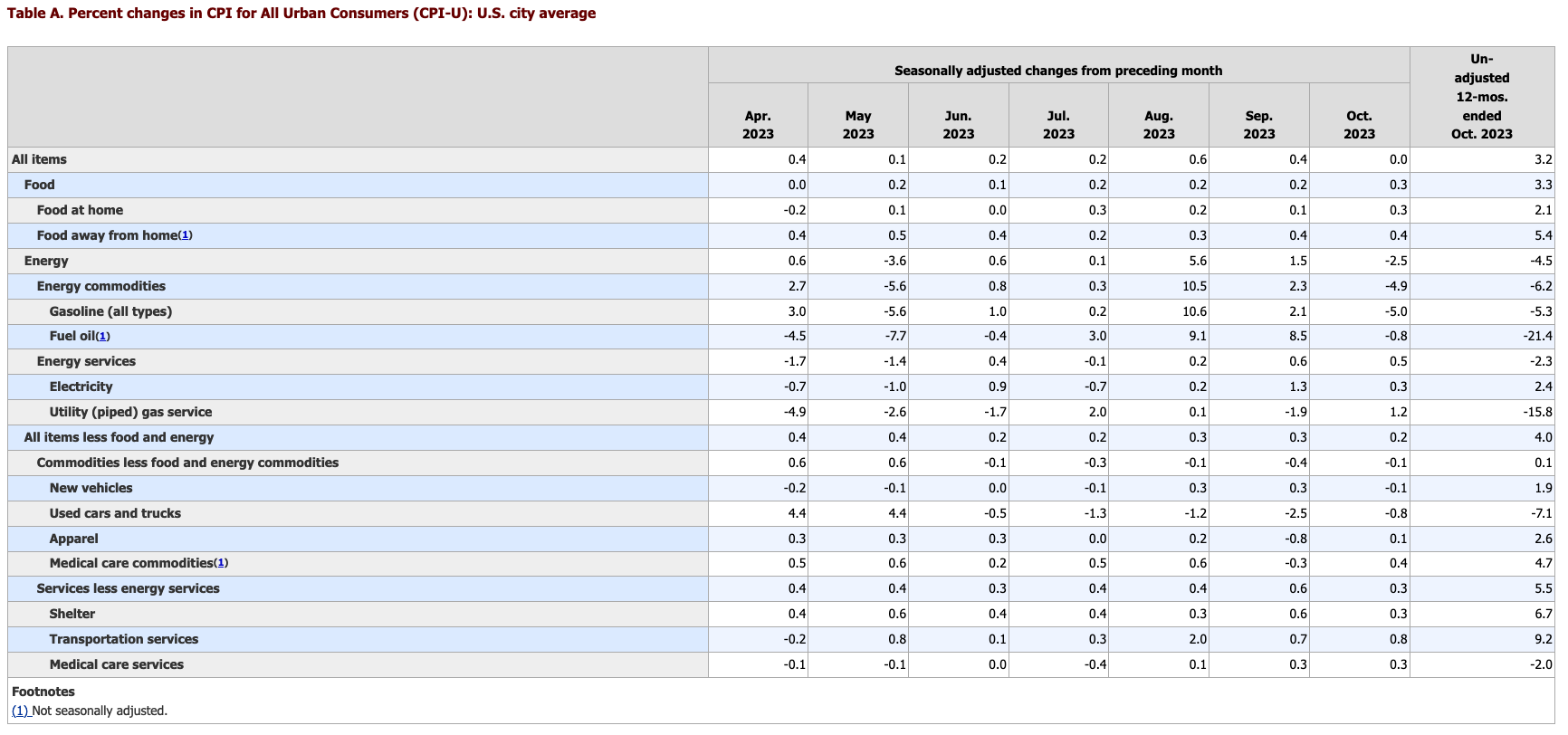

October CPI came in unchanged following a 0.4% increase in September. For the year, CPI dropped to 3.2% from 3.7% in September. Core came in at 4.0% YoY and 0.2% MoM.

Futures soared on the print.

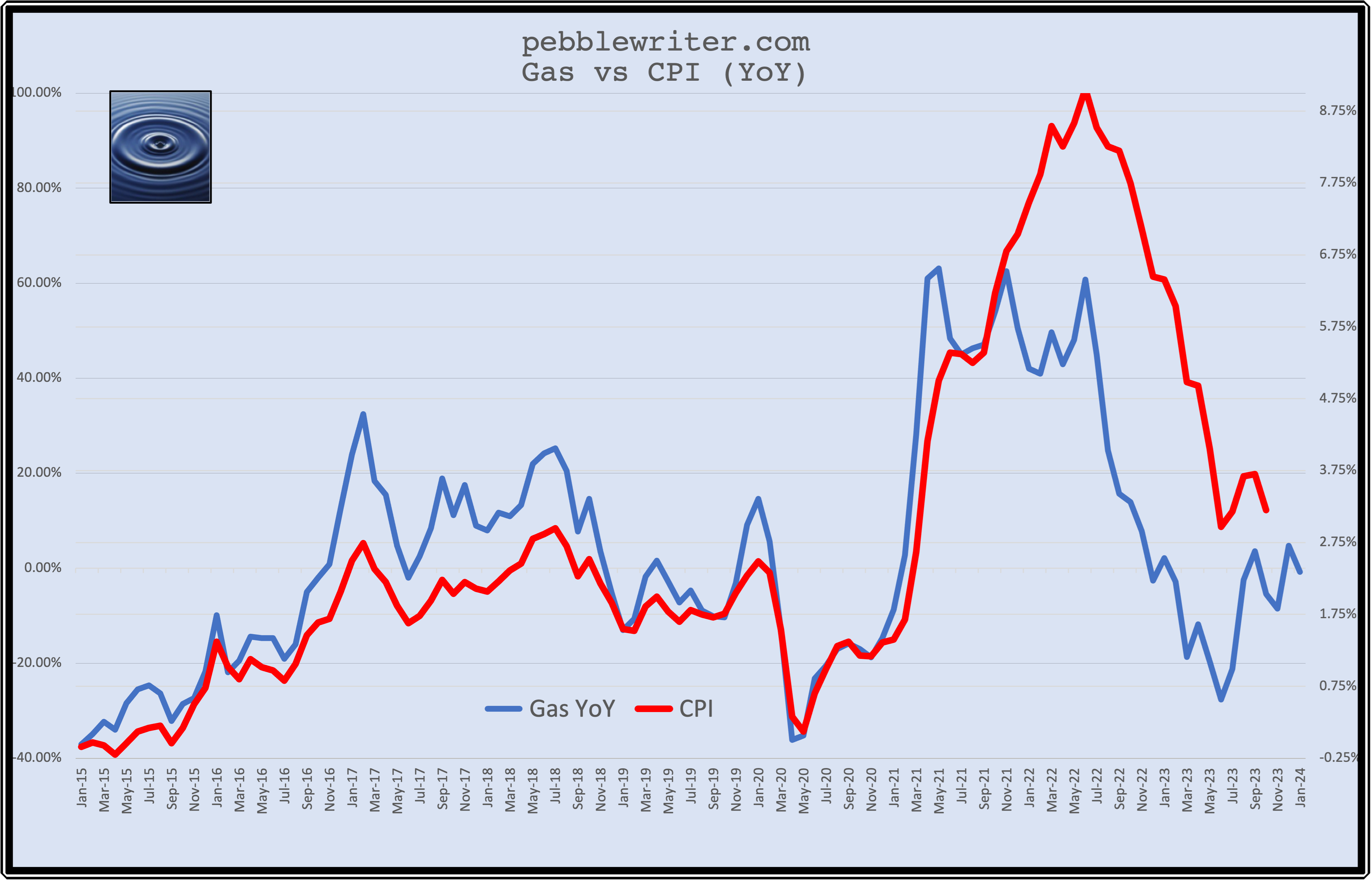

As we have anticipated for the past several months, it was a sharp drop in gas prices which produced the equity-friendly print. From CPI Continues Falling on July 12:

As we have anticipated for the past several months, it was a sharp drop in gas prices which produced the equity-friendly print. From CPI Continues Falling on July 12:

As we discussed last month, the benefit from YoY price declines in oil/gas has maxed out unless prices continue to fall. In other words, central bankers might need to drive oil/gas prices even lower.

From June’s No Surprise:

It’s important to note that oil/gas mustn’t rally any further. If gas were to level out at current levels, the strong positive correlation between YoY gas prices and CPI indicate that inflation would be on the rise from now through the end of the year.

And, Powell: Inflation Not Over:

… there is little chance of inflation not bouncing back up unless oil and gas prices collapse from current levels.

The breakout in July following OPEC’s production cut was followed by an incredible increase in geopolitical risks related to the Israel-Hamas war. Yet oil and gas prices are lower than they have been in almost two years.

It might not be a big enough drop to help Americans forget the 6.7% annual increase in shelter expenses. But, it’s certainly enough to break stocks out of their latest swoon.

Mission accomplished.

continued for members…

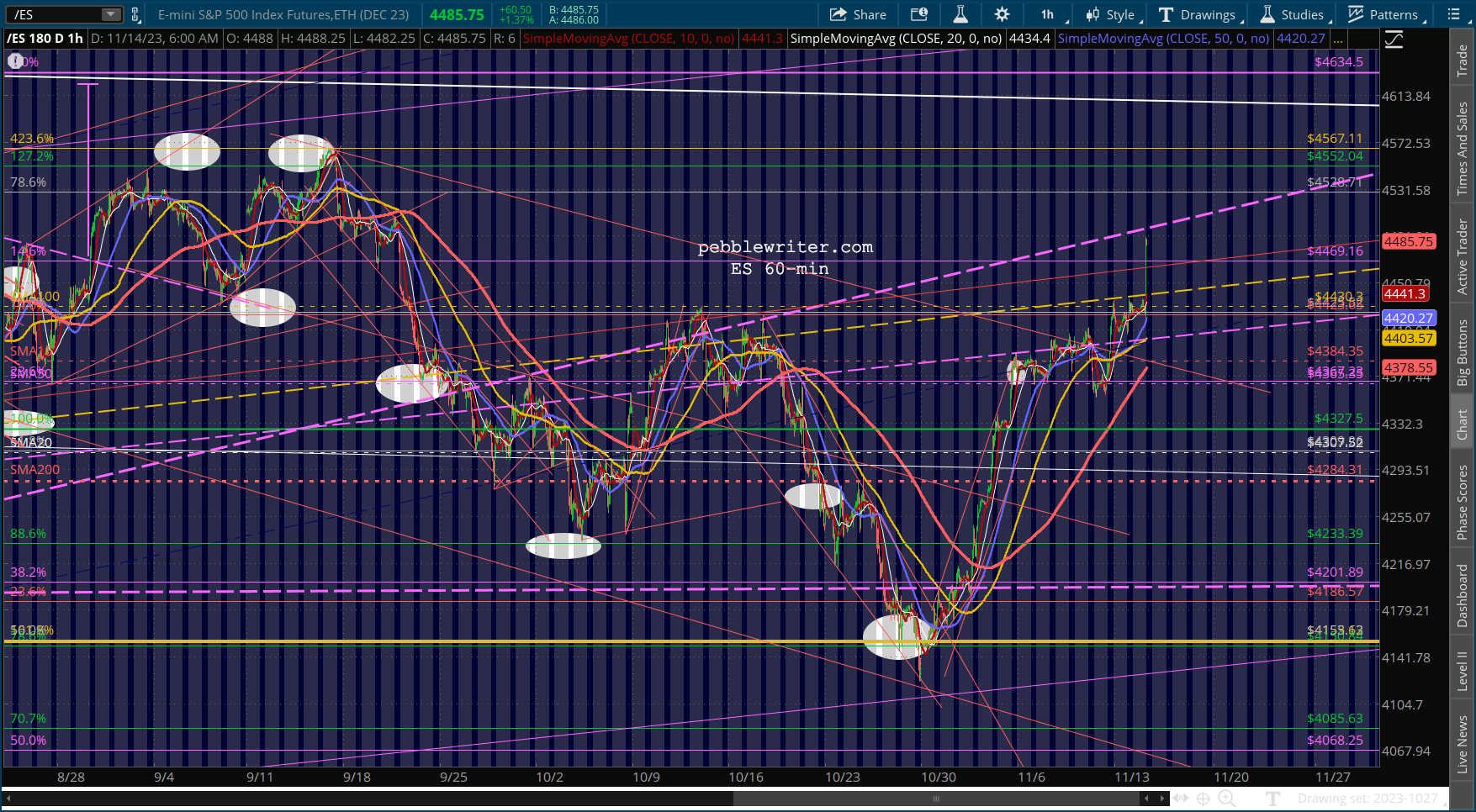

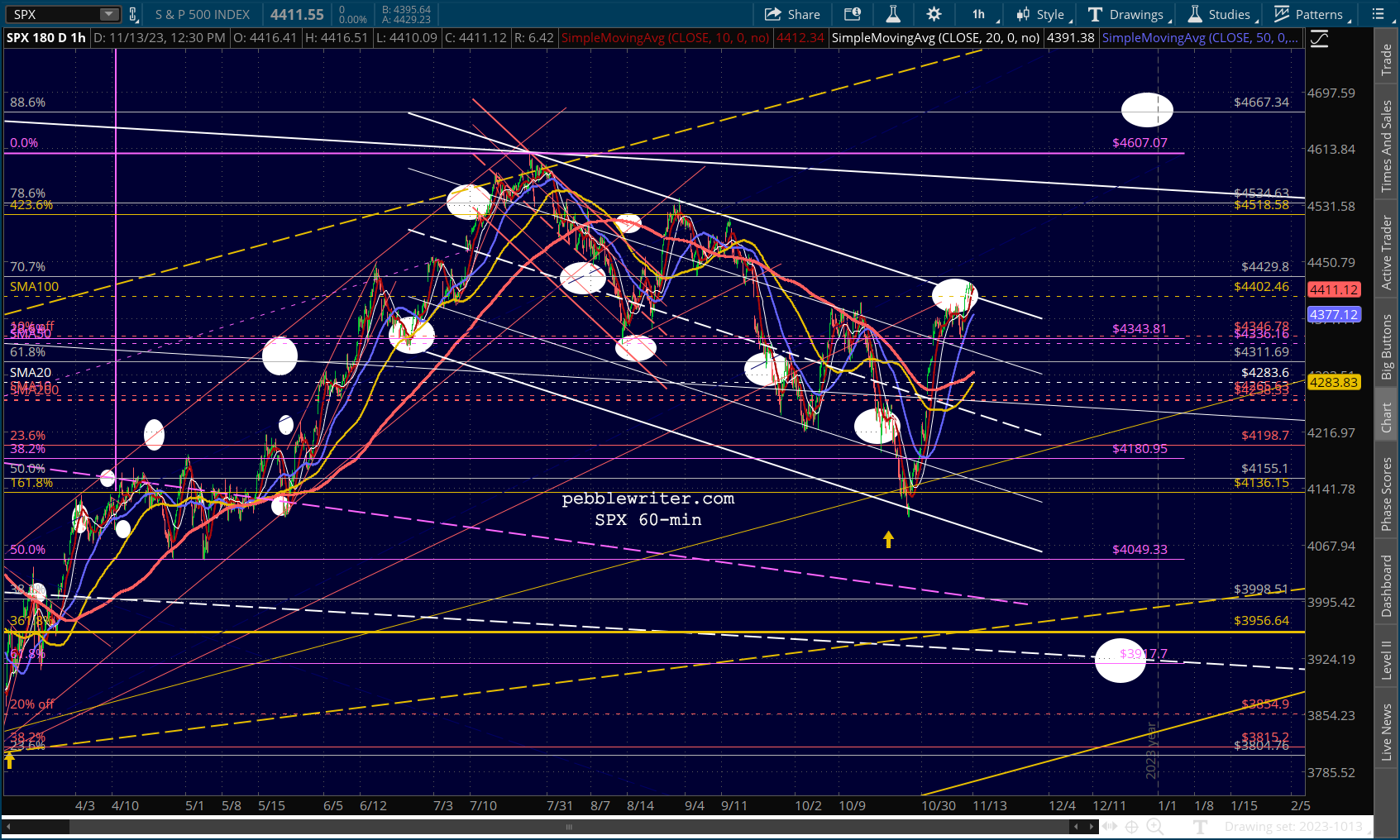

The flag pattern gave way for both ES and SPX as the expectations for additional rate hikes are now dead.

Not surprisingly, VIX broke down big time, though its RSI is still clinging to potential support – leaving the door open to a backtest of SPX’s flag pattern top.

Not surprisingly, VIX broke down big time, though its RSI is still clinging to potential support – leaving the door open to a backtest of SPX’s flag pattern top.

EURUSD spiked up to our SMA200 target…

EURUSD spiked up to our SMA200 target…

…while USDJPY continued its meltup.

…while USDJPY continued its meltup.

CL backtested its SMA200 and RB bounced up through its SMA20 after besting its SMA10 yesterday.

CL backtested its SMA200 and RB bounced up through its SMA20 after besting its SMA10 yesterday.

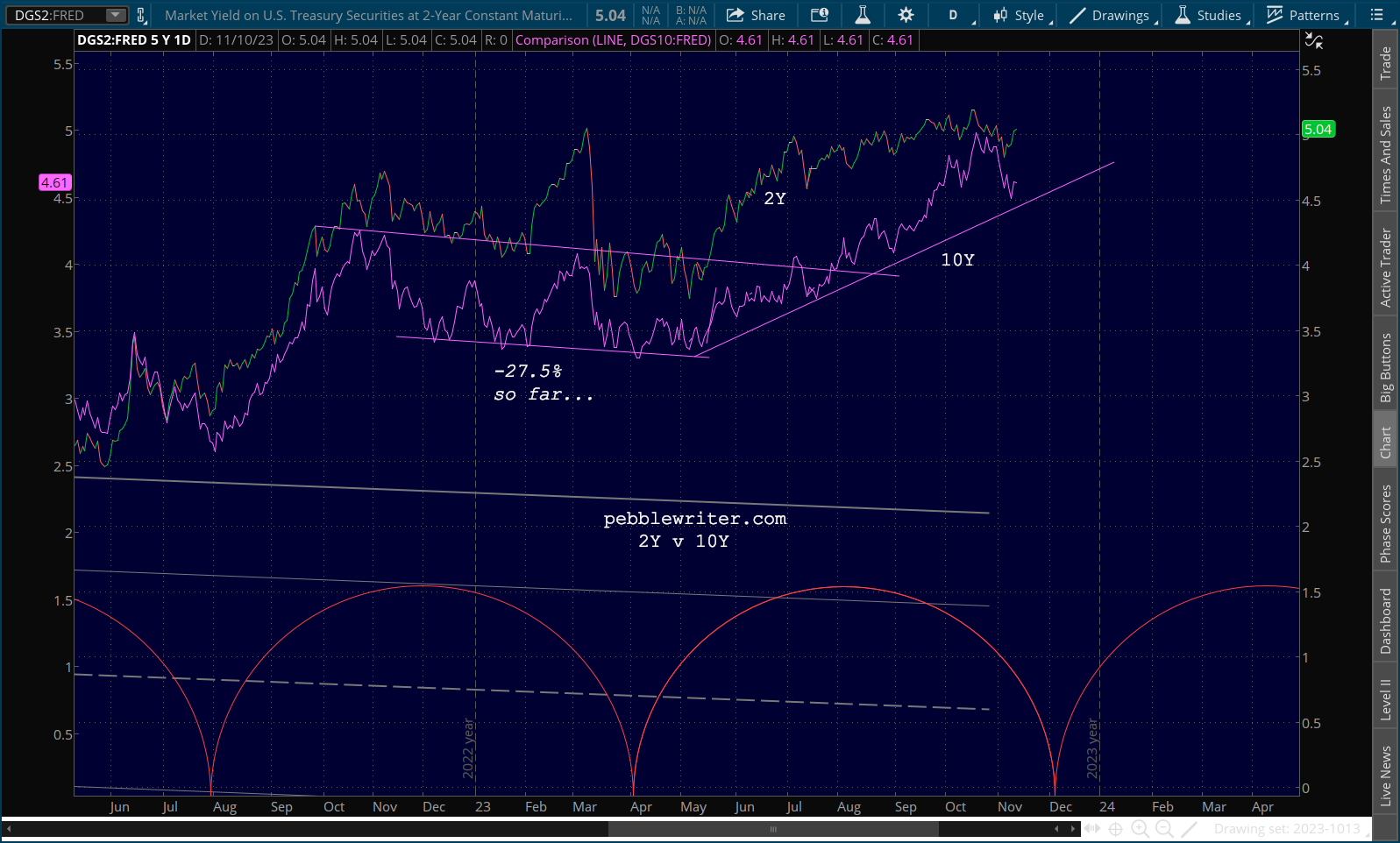

Needless to say, the 10Y plunged on the print...

Needless to say, the 10Y plunged on the print... …leaving its ascent hanging by a thread…

…leaving its ascent hanging by a thread…

Ditto for the 2s10s.

Ditto for the 2s10s.

The CPI picture was a mess in October, with strong advances in shelter offset by a sharp drop in gas prices.

The CPI picture was a mess in October, with strong advances in shelter offset by a sharp drop in gas prices. This has been our premise for many months and the basis for our expectations of a big drop in RB.

This has been our premise for many months and the basis for our expectations of a big drop in RB.

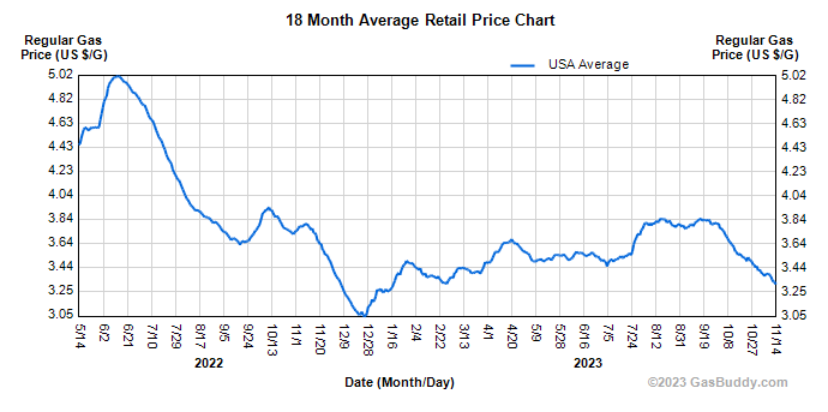

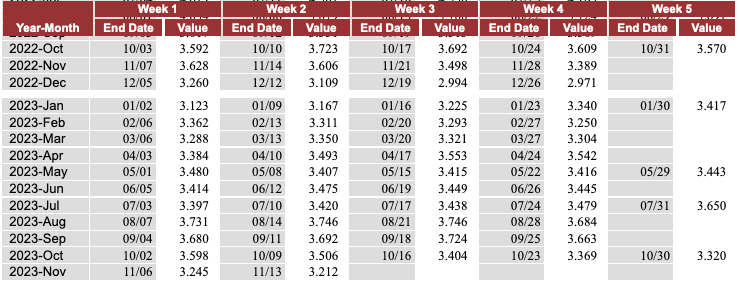

Note that gas prices have continued to drop in November, with an average so far of 3.2285 the first two weeks.

Note that gas prices have continued to drop in November, with an average so far of 3.2285 the first two weeks.  If prices were to remain at these levels, we’d be looking at another brief bump.

If prices were to remain at these levels, we’d be looking at another brief bump. The Fed obviously doesn’t need another big drop in oil/gas, as current prices would produce a -8.5% YoY drop in November.

The Fed obviously doesn’t need another big drop in oil/gas, as current prices would produce a -8.5% YoY drop in November.