What the algos giveth, David Tepper (bearish) and Q3 GDP (+3.2% vs 2.9% est. and -0.6% last) taketh away. Futures are off sharply as we approach the open.

continued for members…

continued for members…

3.2% is a pretty nice GDP for an economy which is supposed to be in a recession. At the very least, it complicates the Fed’s job.

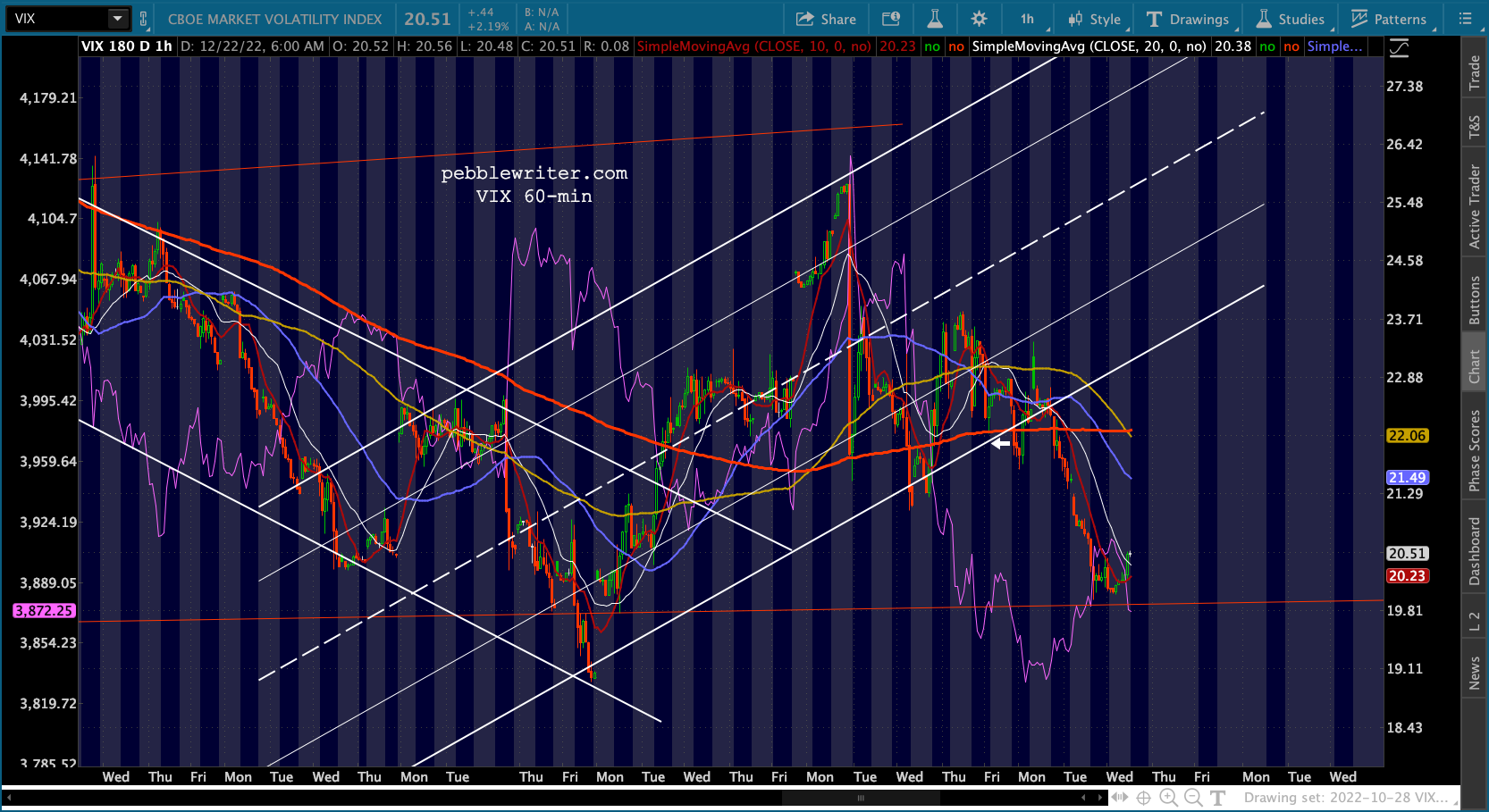

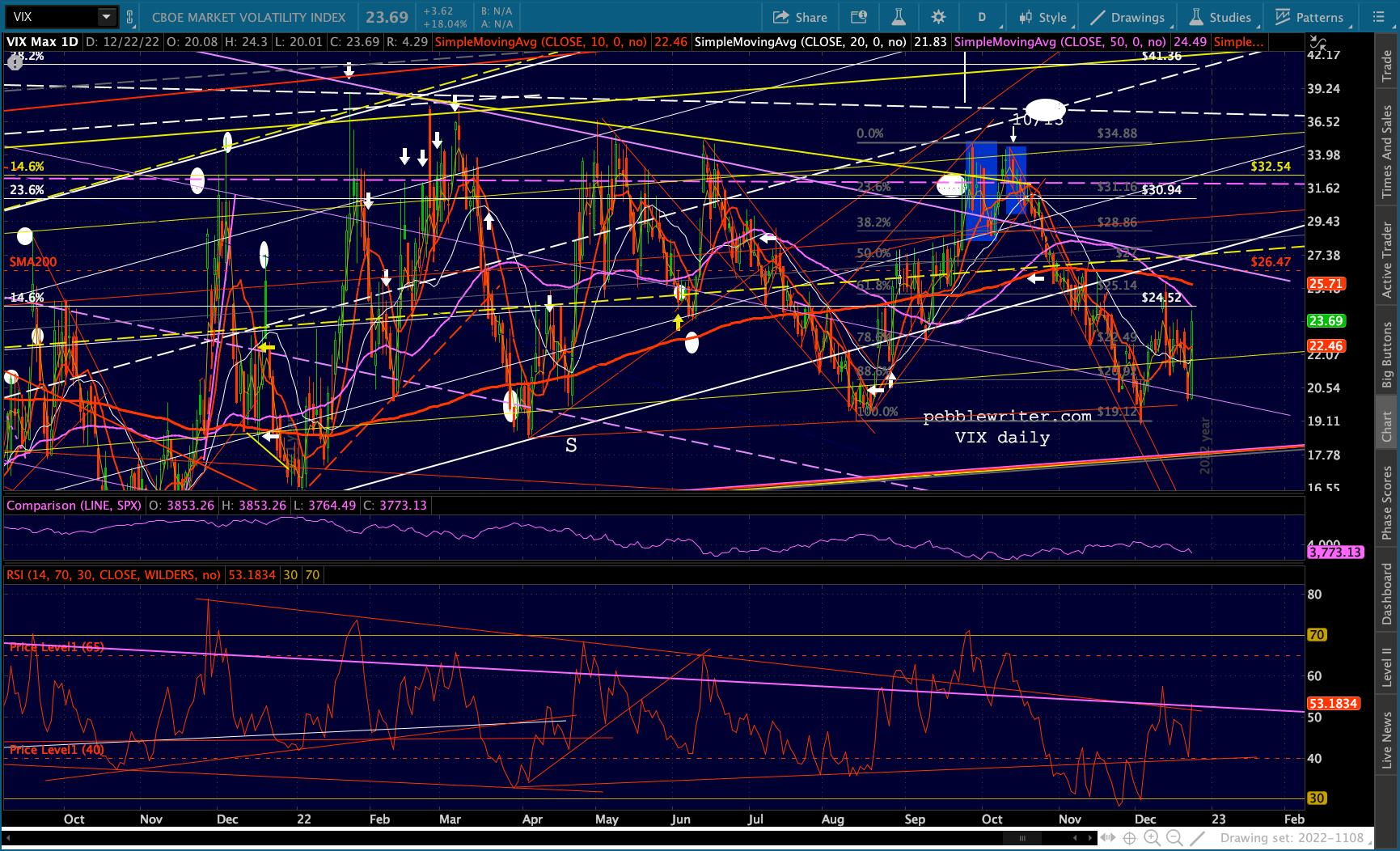

So far, VIX has declined to give up its bullish ways and is preventing a much bigger drop in equities.

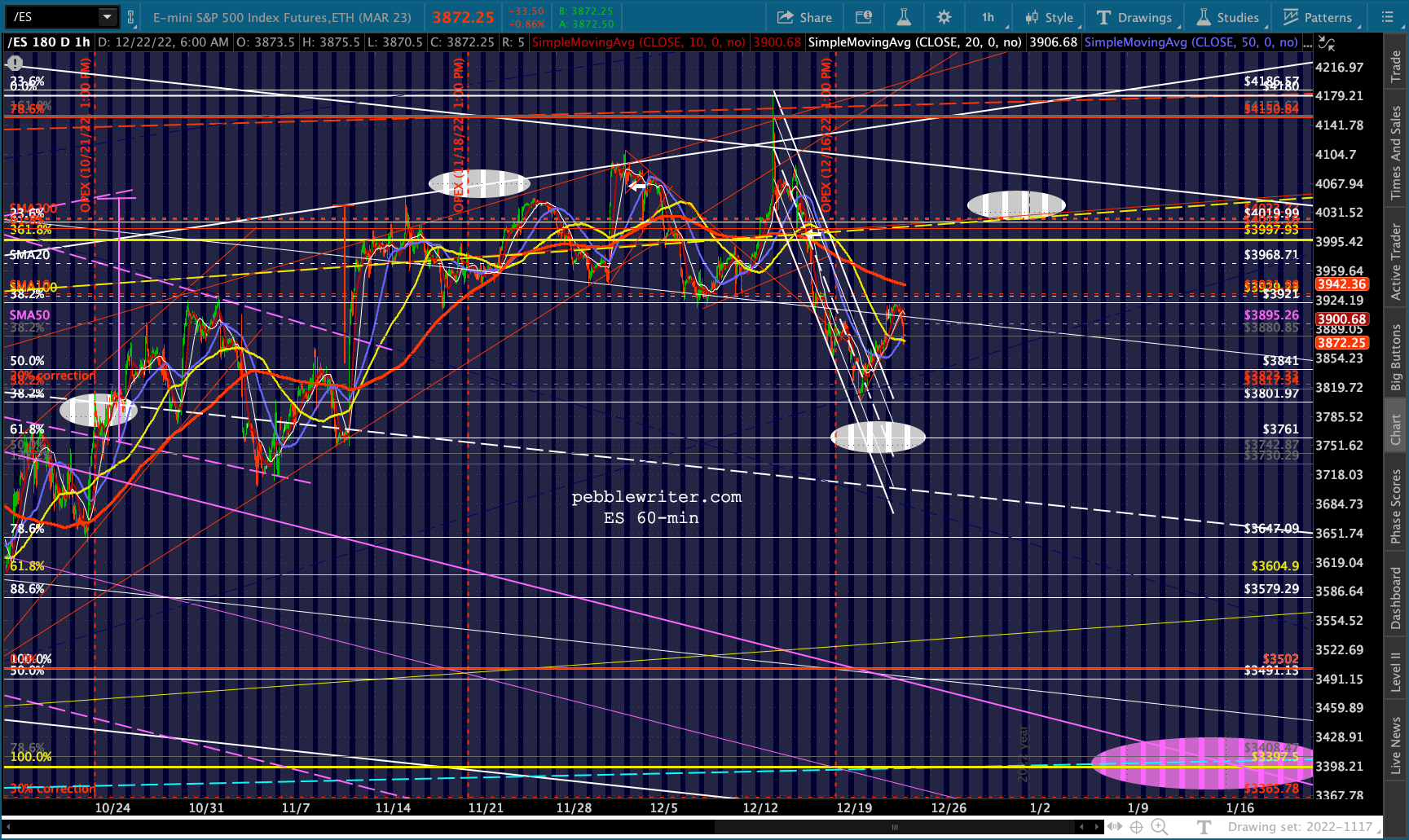

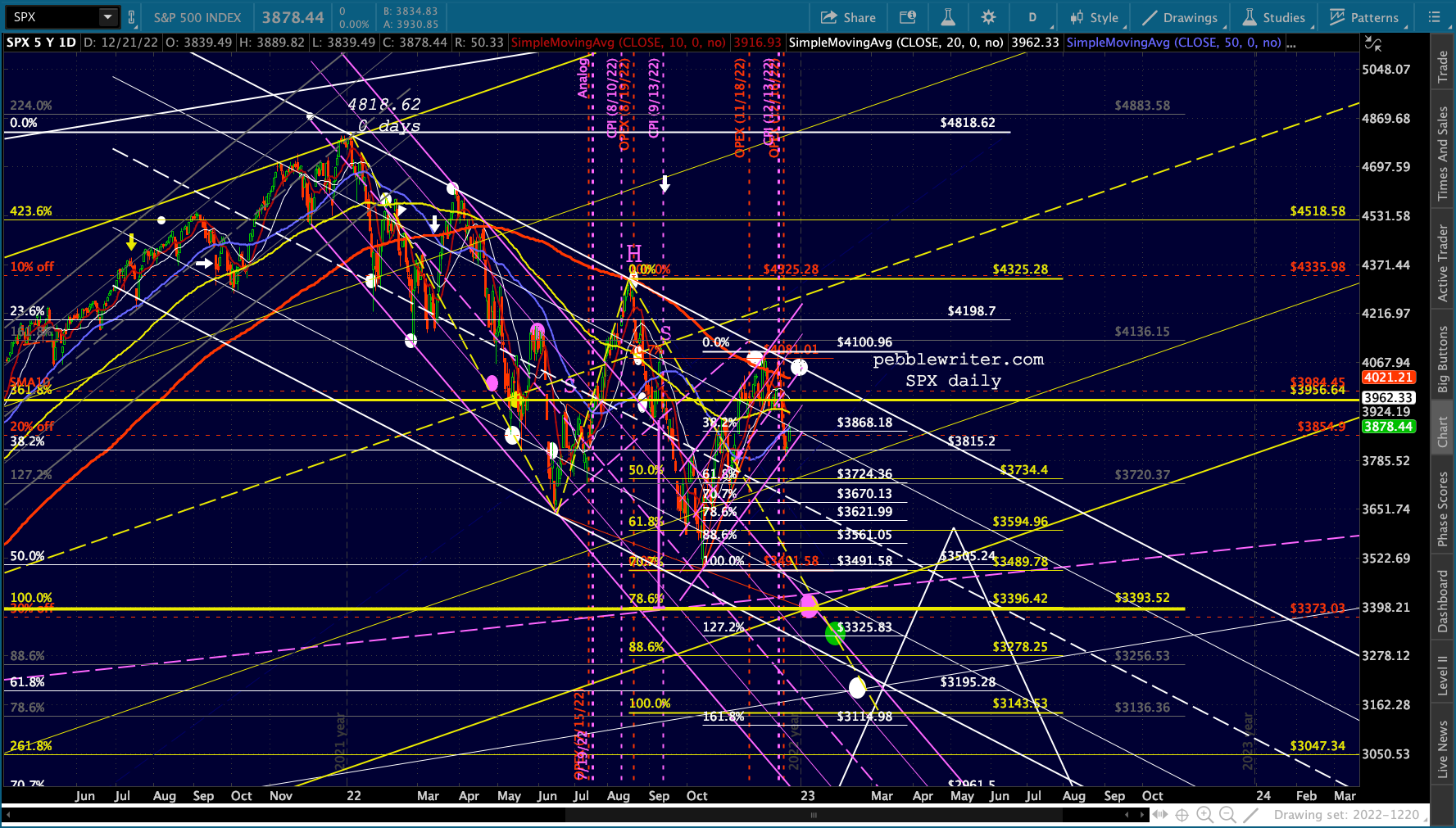

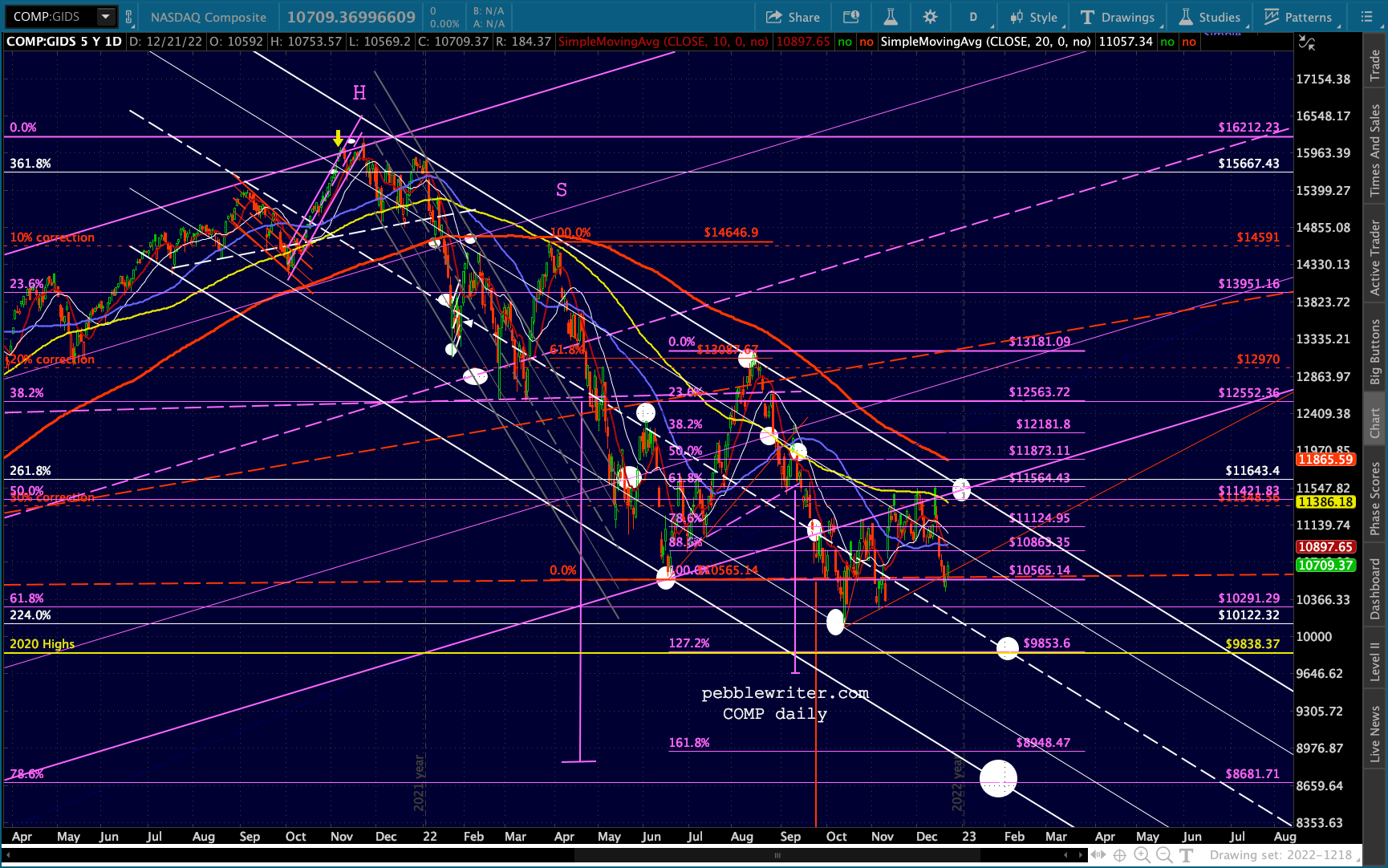

This is going to complicate a run up to the SMA200/channel top.

This is going to complicate a run up to the SMA200/channel top.

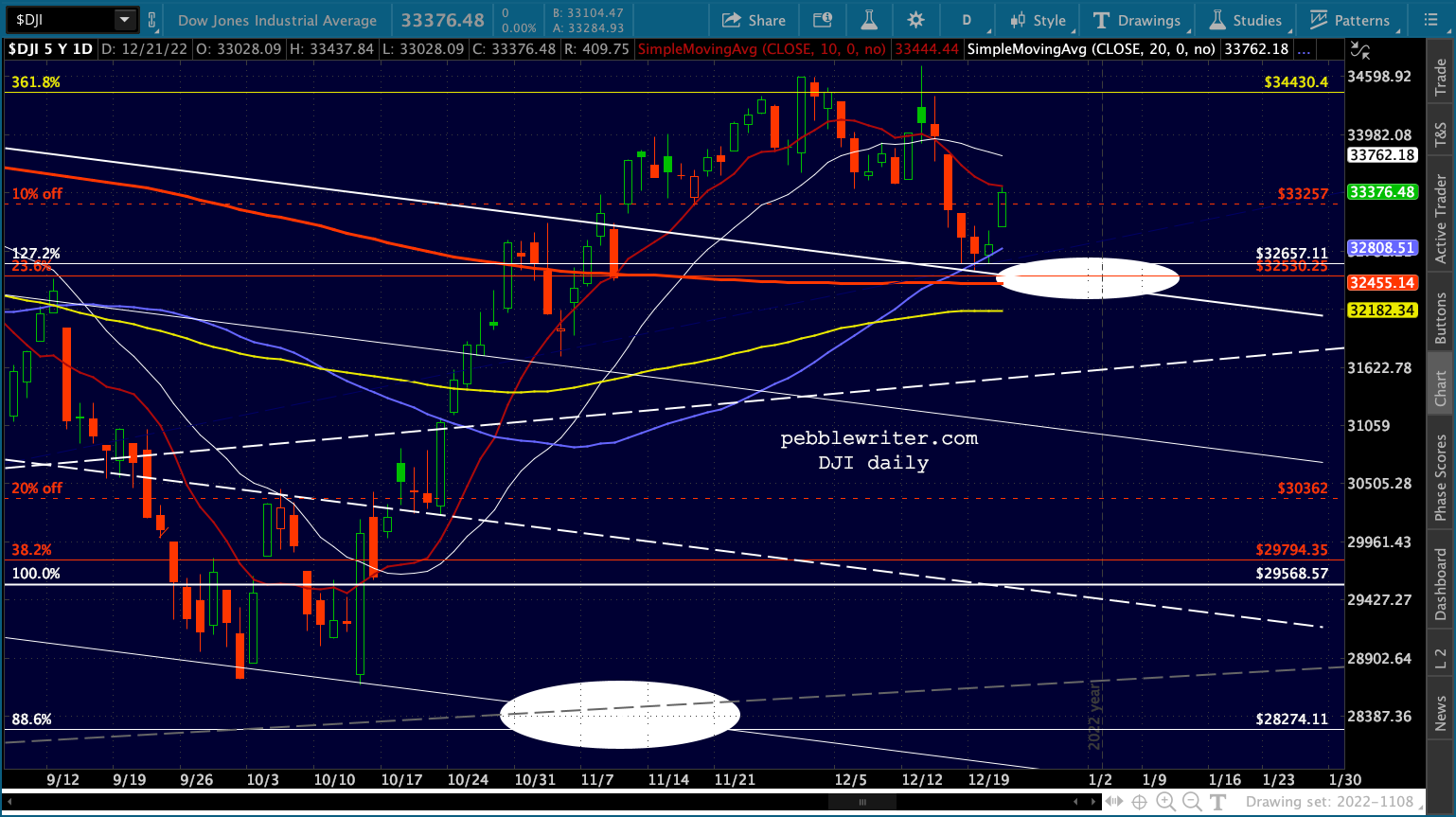

The Dow still needs a SMA200 tag…

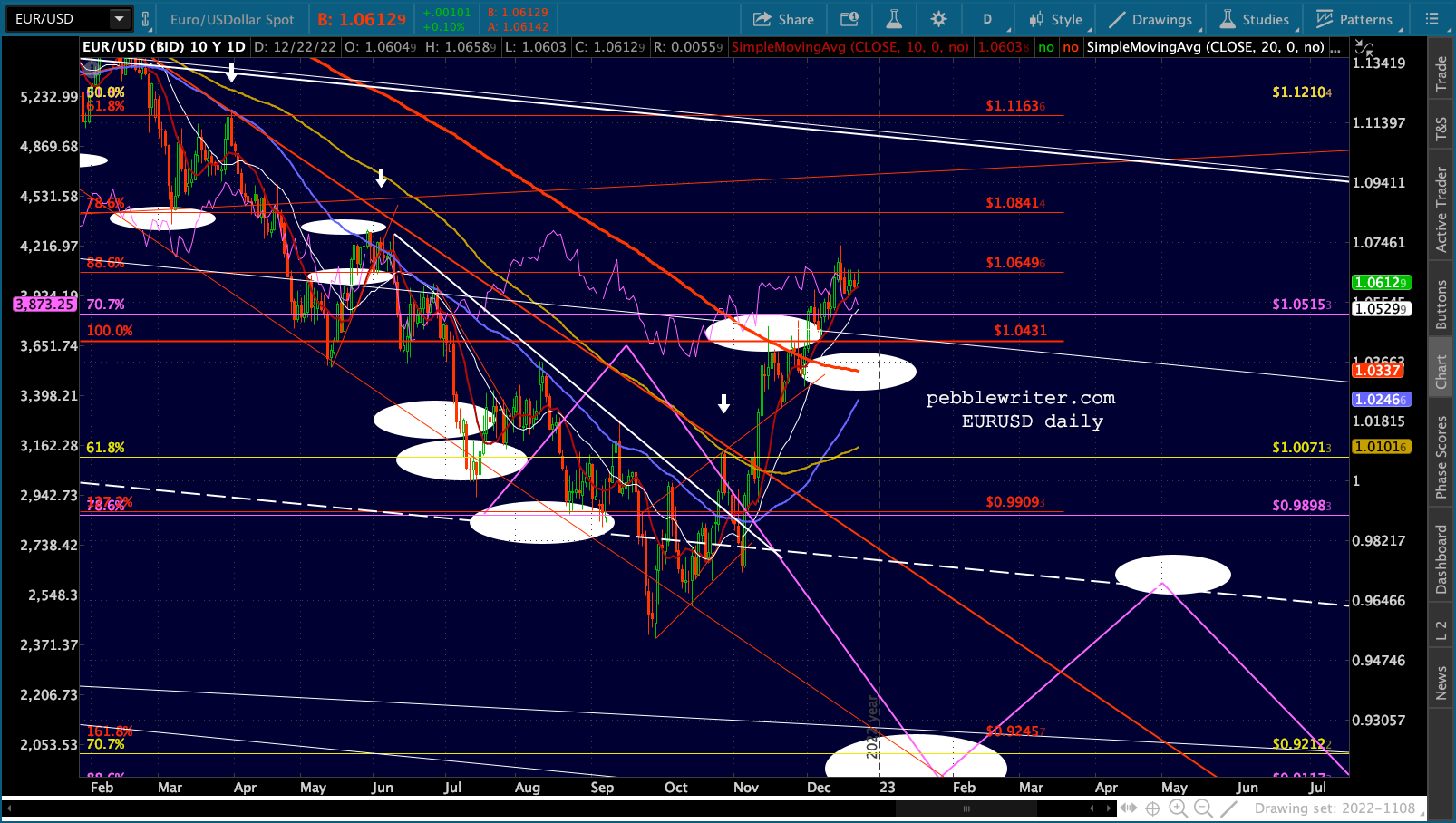

The Dow still needs a SMA200 tag…  Currencies have barely budged since yesterday’s realignment. In other words, still bullish in appearance – though the EURUSD “rally” is looking very, very tired.

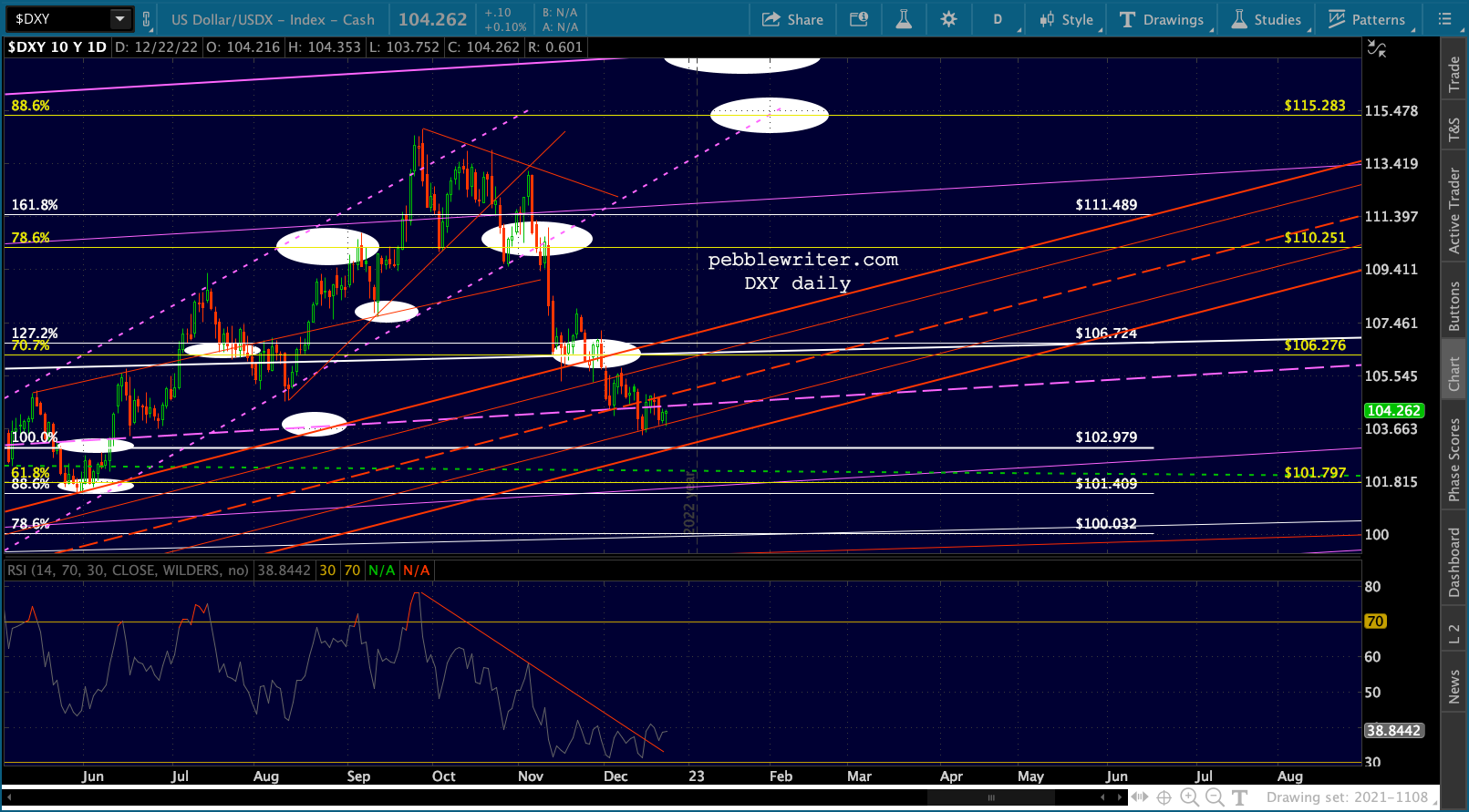

Currencies have barely budged since yesterday’s realignment. In other words, still bullish in appearance – though the EURUSD “rally” is looking very, very tired.

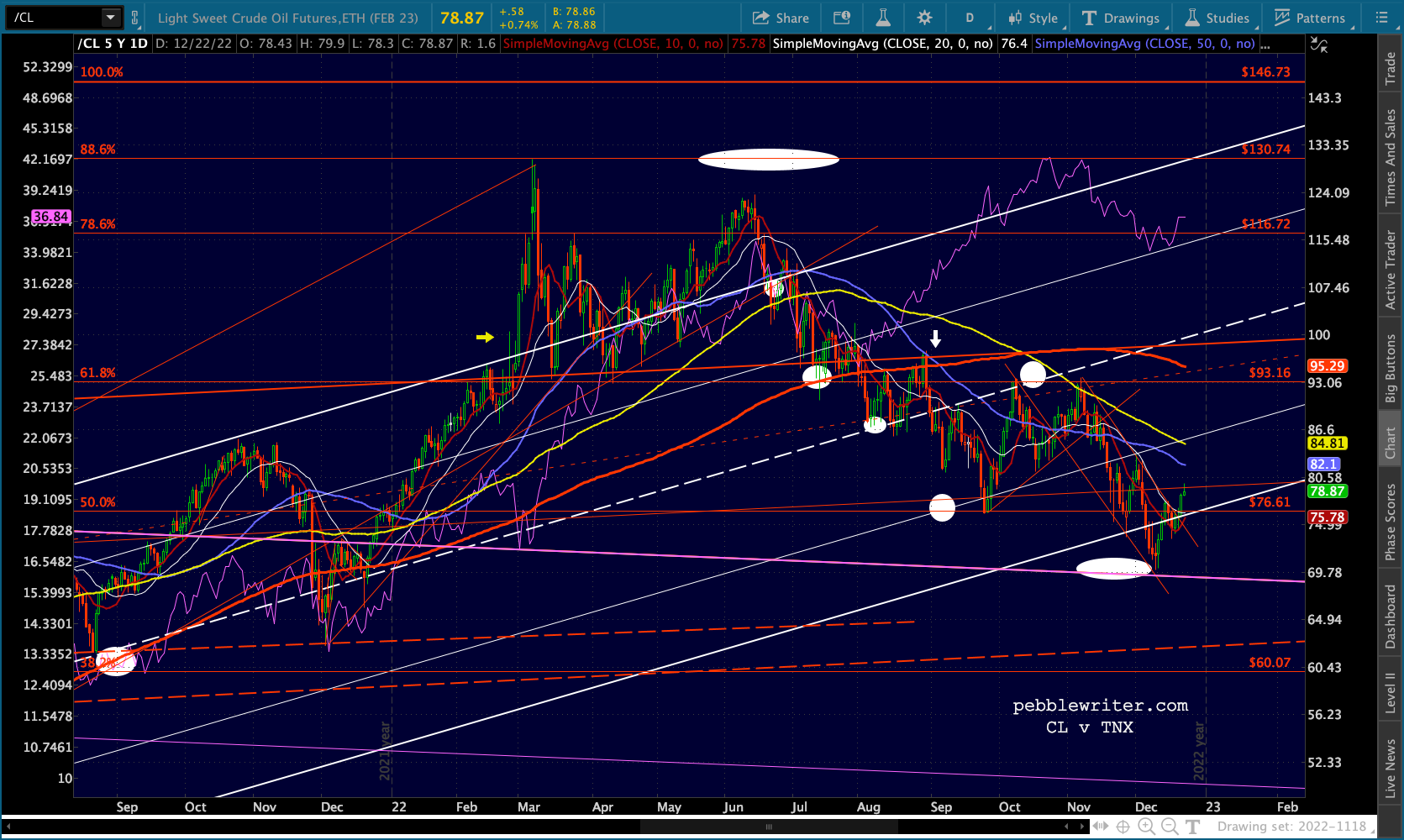

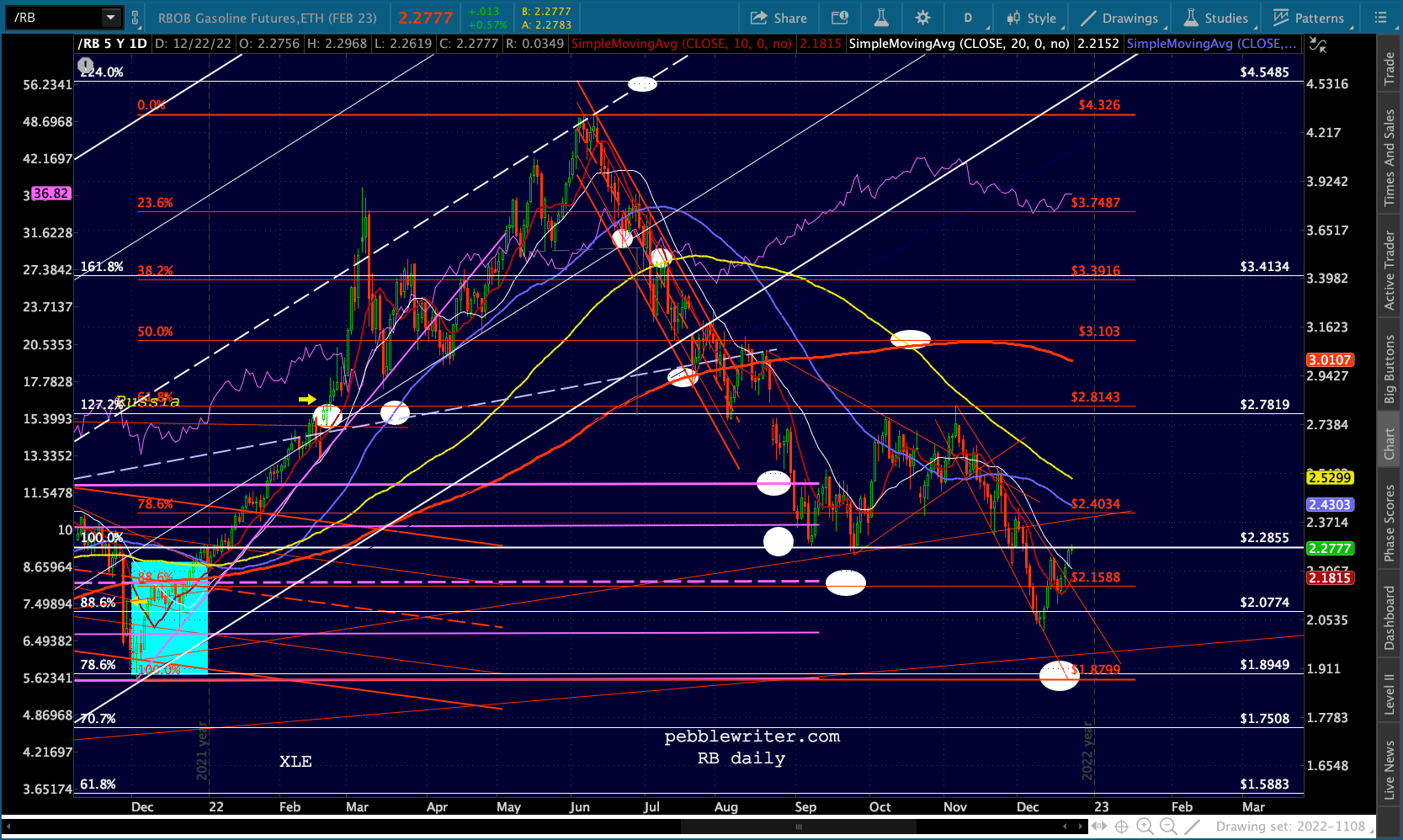

CL and RB are nudging slightly higher. But, it’s hard to imagine the bounce lasting very long given the COVID news trickling out of China (and HERE.)

CL and RB are nudging slightly higher. But, it’s hard to imagine the bounce lasting very long given the COVID news trickling out of China (and HERE.)

The Dow’s need to tag its SMA200 (32,451.84) is both the bears’ opportunity and their challenge. Once it’s reached, will there be a huge effort to hold it? Perhaps. Assuming there’s at least a bounce, will it drag SPX/ES/COMP/SPY out of their bearish channels? Perhaps. I expect the Dow’s tag to be more important than ES reaching the .618 at 3761.

The Dow’s need to tag its SMA200 (32,451.84) is both the bears’ opportunity and their challenge. Once it’s reached, will there be a huge effort to hold it? Perhaps. Assuming there’s at least a bounce, will it drag SPX/ES/COMP/SPY out of their bearish channels? Perhaps. I expect the Dow’s tag to be more important than ES reaching the .618 at 3761.

I also fully expect there to be a difficult choice to be made – and over a holiday weekend, at that. In my experience, this suggests that traders take a break once the target is reached. To play additional downside or a substantial bounce is more of a gamble than a strategy.

Remember, DJIA saw a golden cross the other day, so the bulls might really be hoping/planning to cling to that positive momentum. And, even though it’s getting a nice bounce today, VIX hasn’t reached its own SMA200 at 25.71 or even its SMA50 at 24.49.

I mentioned the other day that I will be off tomorrow as well as Monday (also a market holiday.) Sometime over the next few days, however, I hope to post a review of 2022 and a look ahead at 2023.

I mentioned the other day that I will be off tomorrow as well as Monday (also a market holiday.) Sometime over the next few days, however, I hope to post a review of 2022 and a look ahead at 2023.

It has been a pleasure researching/writing for everyone this past year. I wish you all a very happy holiday!