January headline CPI reached 7.5%, a new 40-yr high, sending the 10Y up over 2% for the first time since August 2019 when CPI registered 1.75%. As has been the trend since November, oil/gas no longer leads the way.

Inflation has become widespread, higher than the Fed’s so-called 2% target in every category except, ironically, medical services. Energy was the only category showing a negative MoM change.

Inflation has become widespread, higher than the Fed’s so-called 2% target in every category except, ironically, medical services. Energy was the only category showing a negative MoM change.

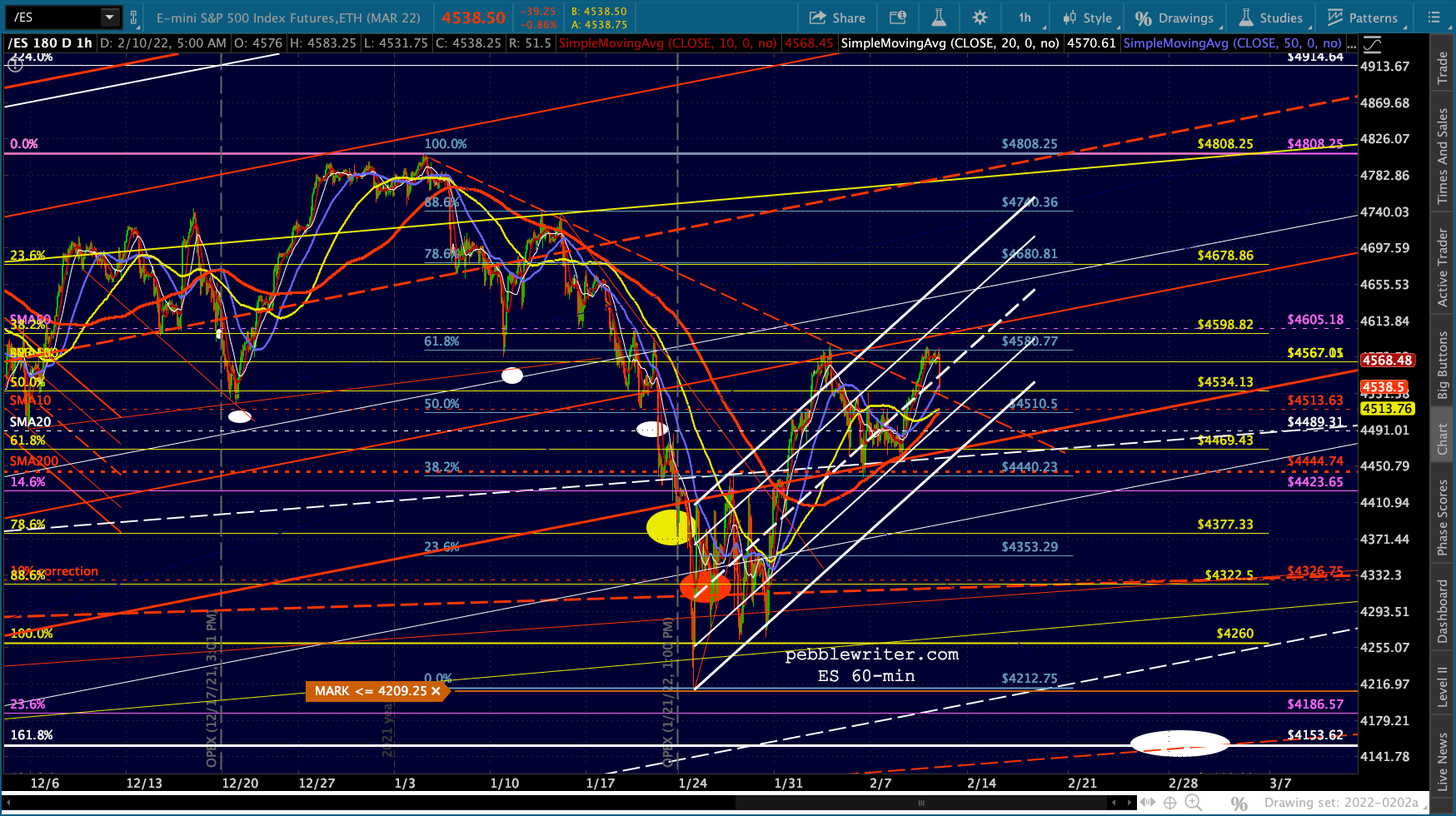

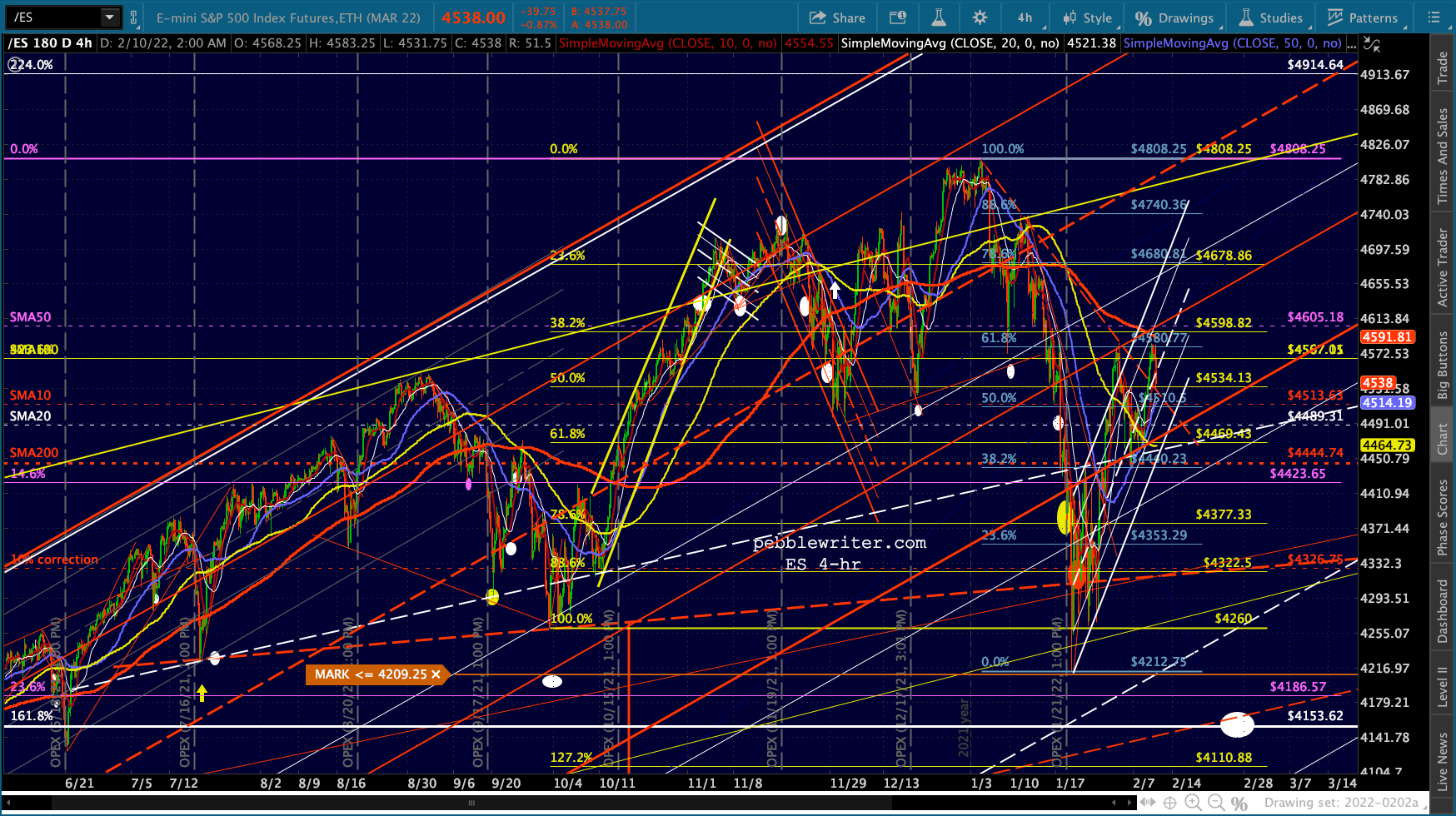

Futures are off over 40 points so far. If not for the ramp job of the last few days, ES would be back below its 200-DMA. It’s the markets version of raising prices so you can advertise a huge sale.

Futures are off over 40 points so far. If not for the ramp job of the last few days, ES would be back below its 200-DMA. It’s the markets version of raising prices so you can advertise a huge sale.

continued for members…

continued for members…

Instead, we had a bullish 10/20 cross yesterday and the SMA10 is now technical support.

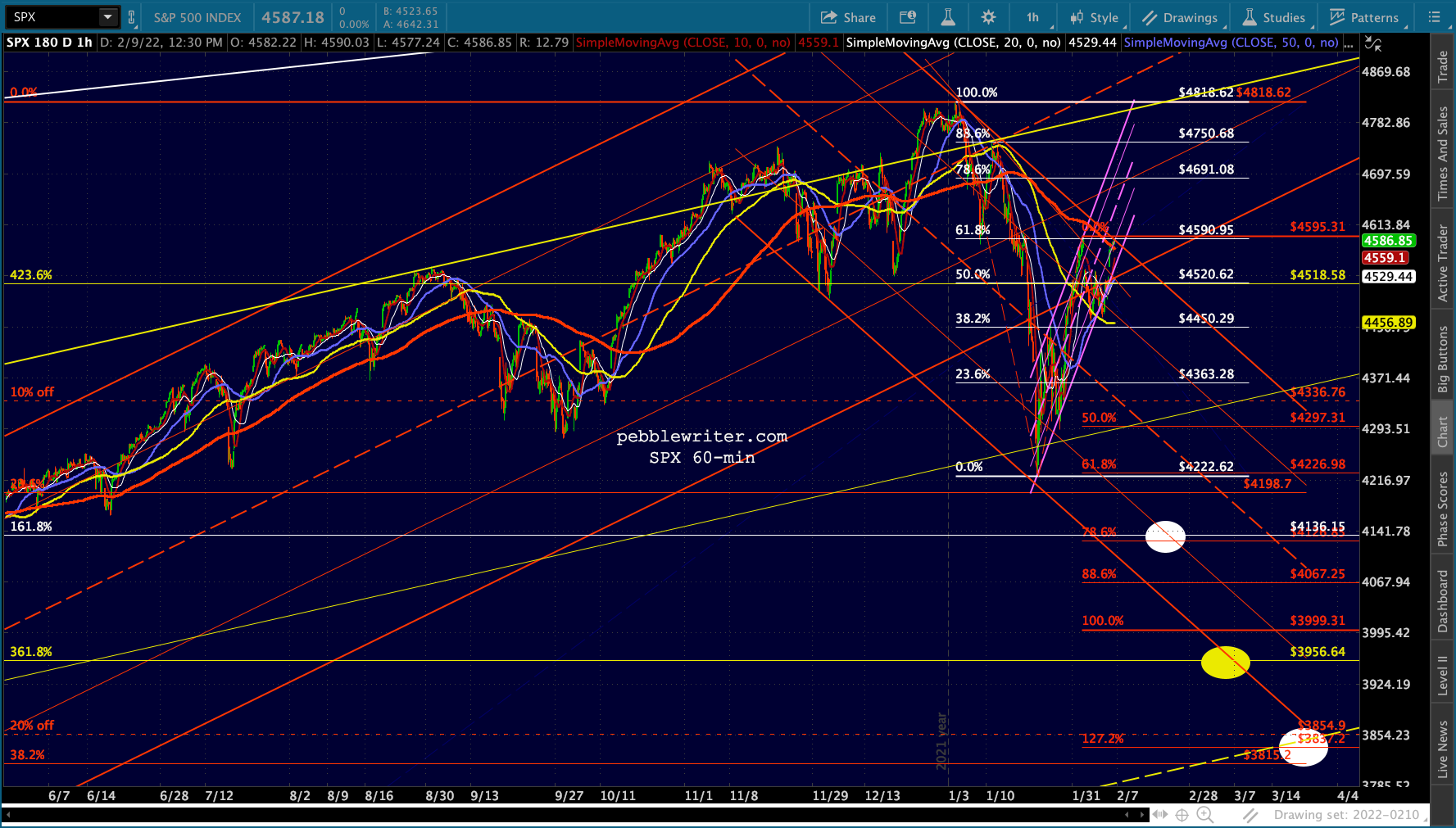

We’ll go ahead and adjust the SPX channel – still indicating lows in mid-March if we get another leg down.

We’ll go ahead and adjust the SPX channel – still indicating lows in mid-March if we get another leg down.

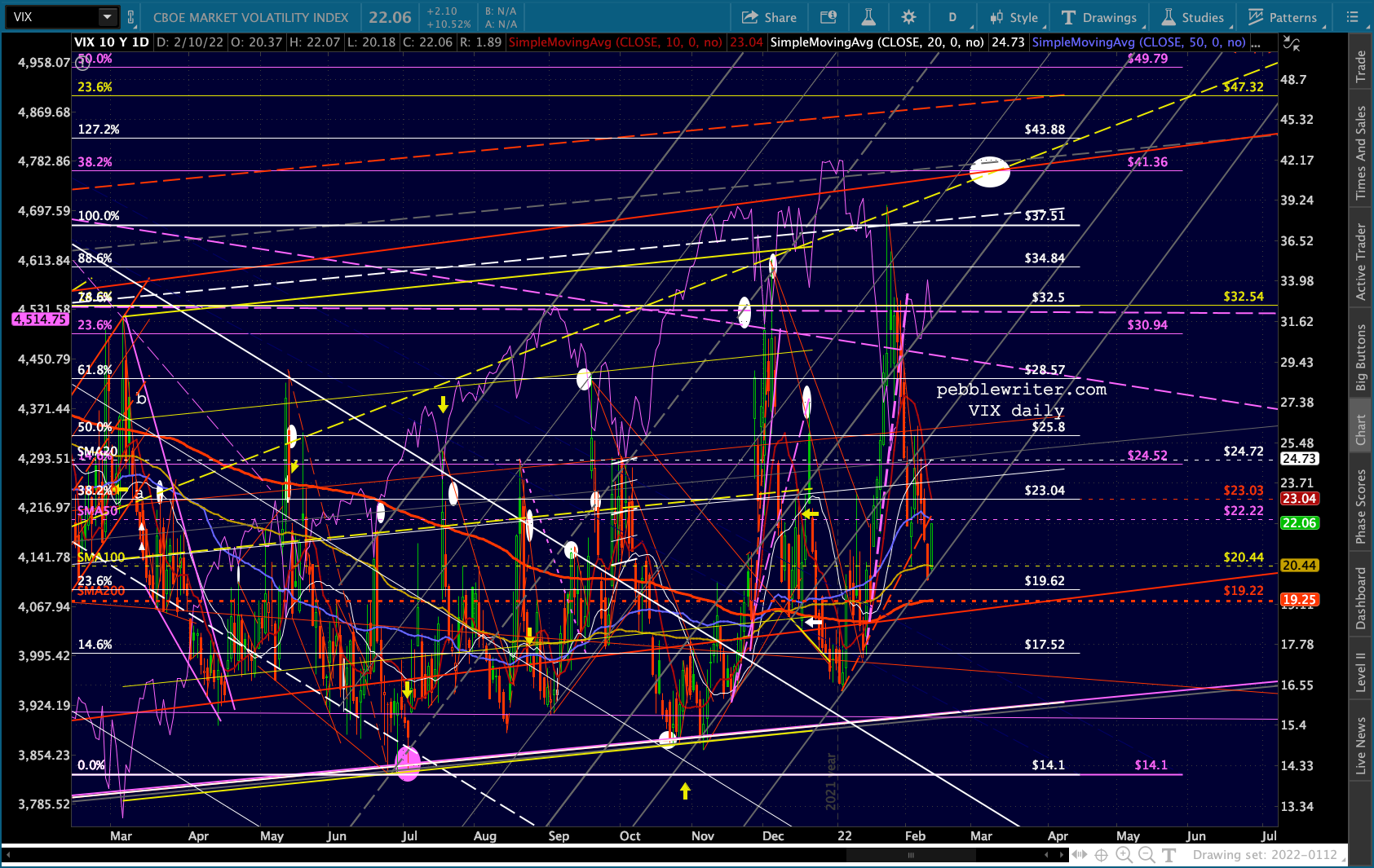

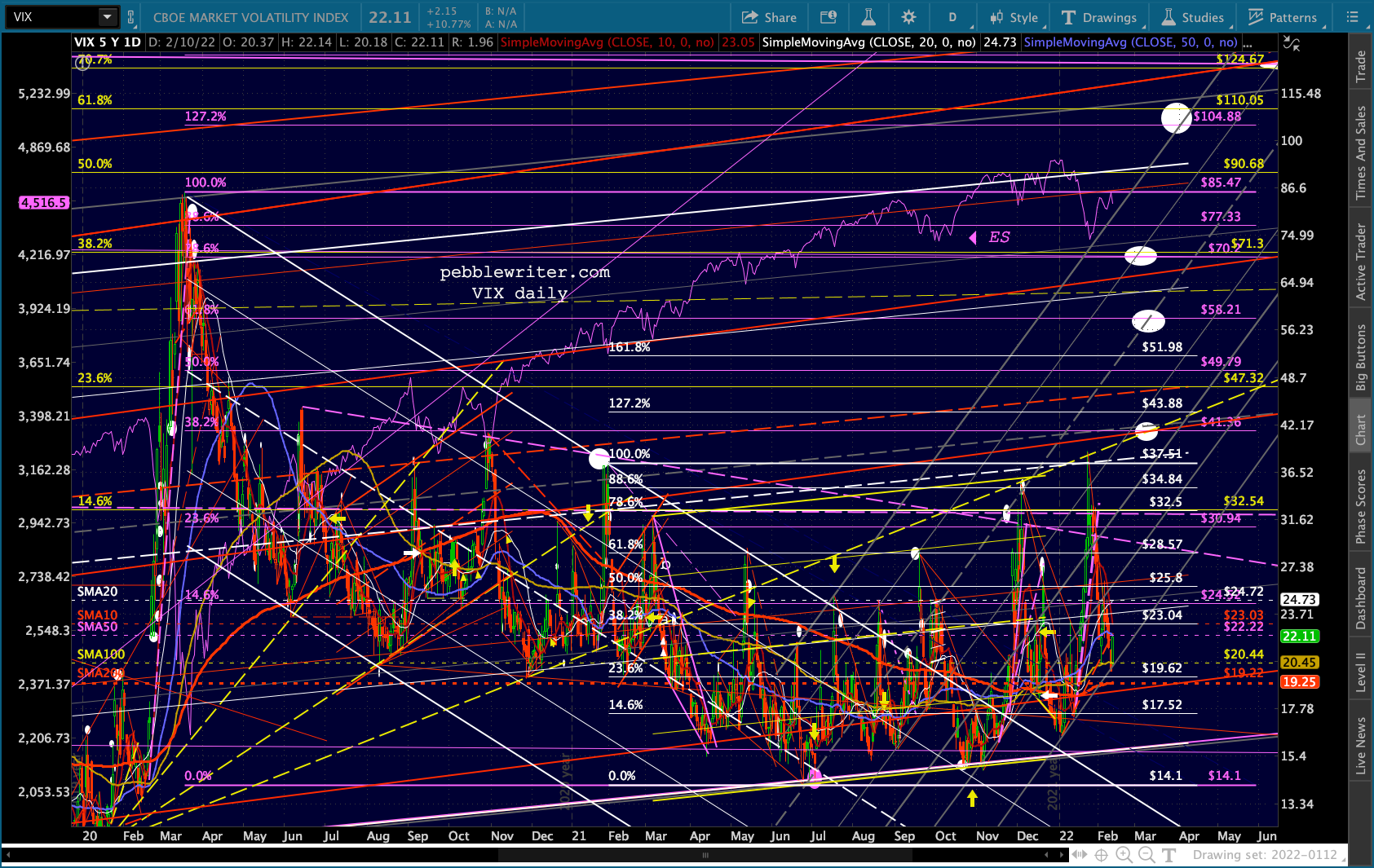

VIX, which also saw a bearish (bullish for stocks) 10/20 cross yesterday, must now force its way up through the SMA10, 20, and 50 in order to break out.

VIX, which also saw a bearish (bullish for stocks) 10/20 cross yesterday, must now force its way up through the SMA10, 20, and 50 in order to break out.

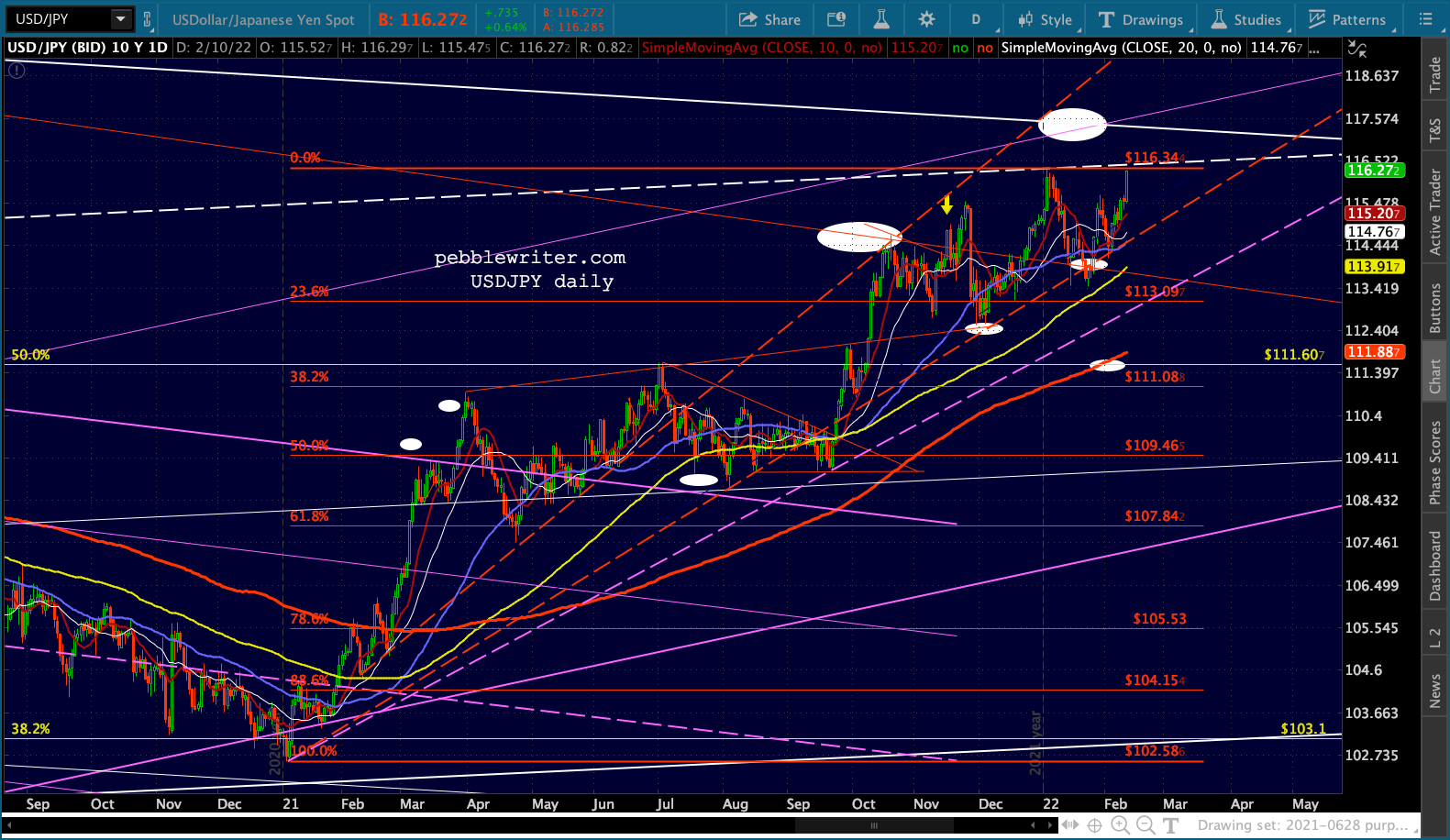

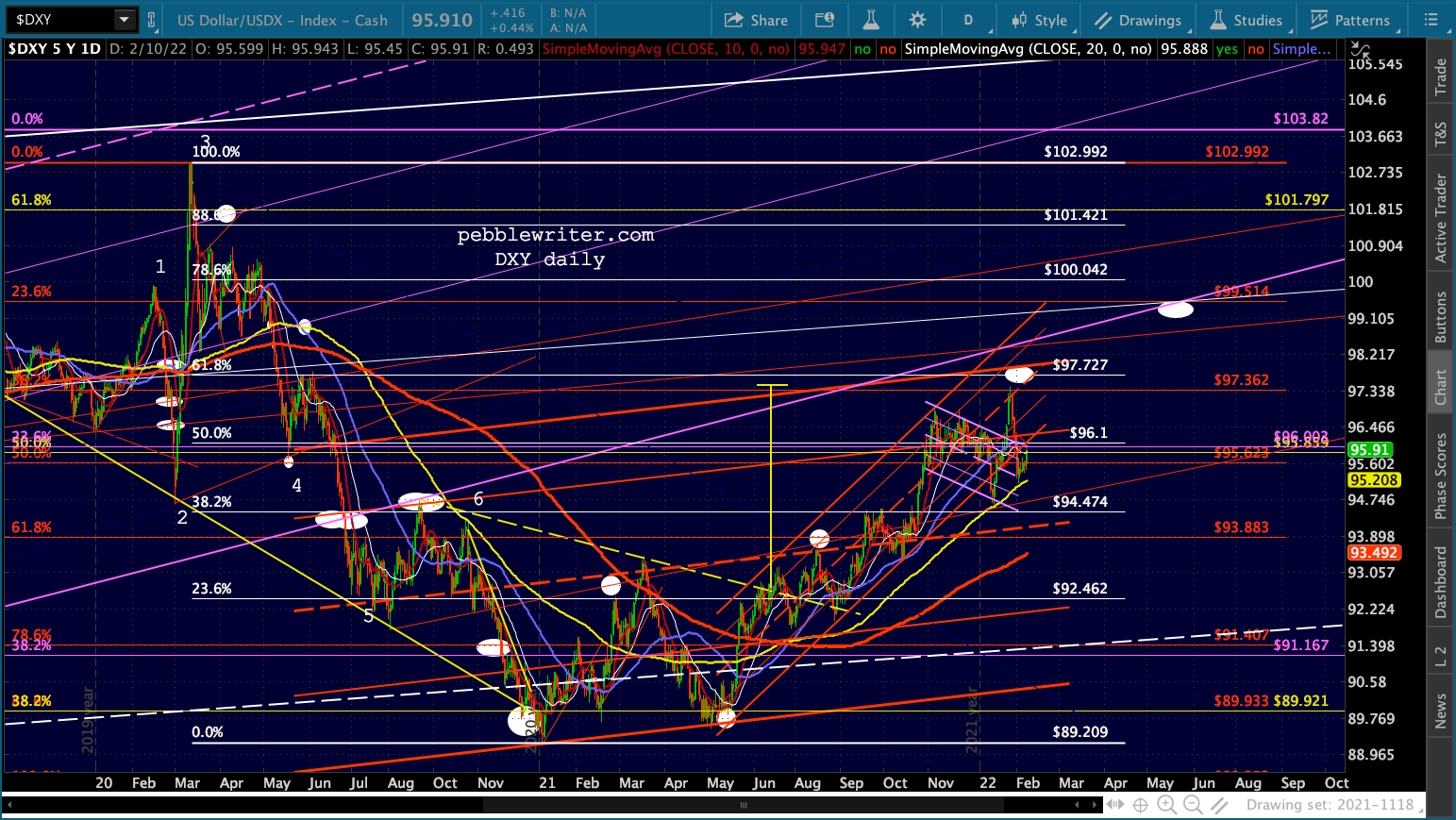

DXY is getting a small boost, mostly courtesy of the yen.

DXY is getting a small boost, mostly courtesy of the yen.

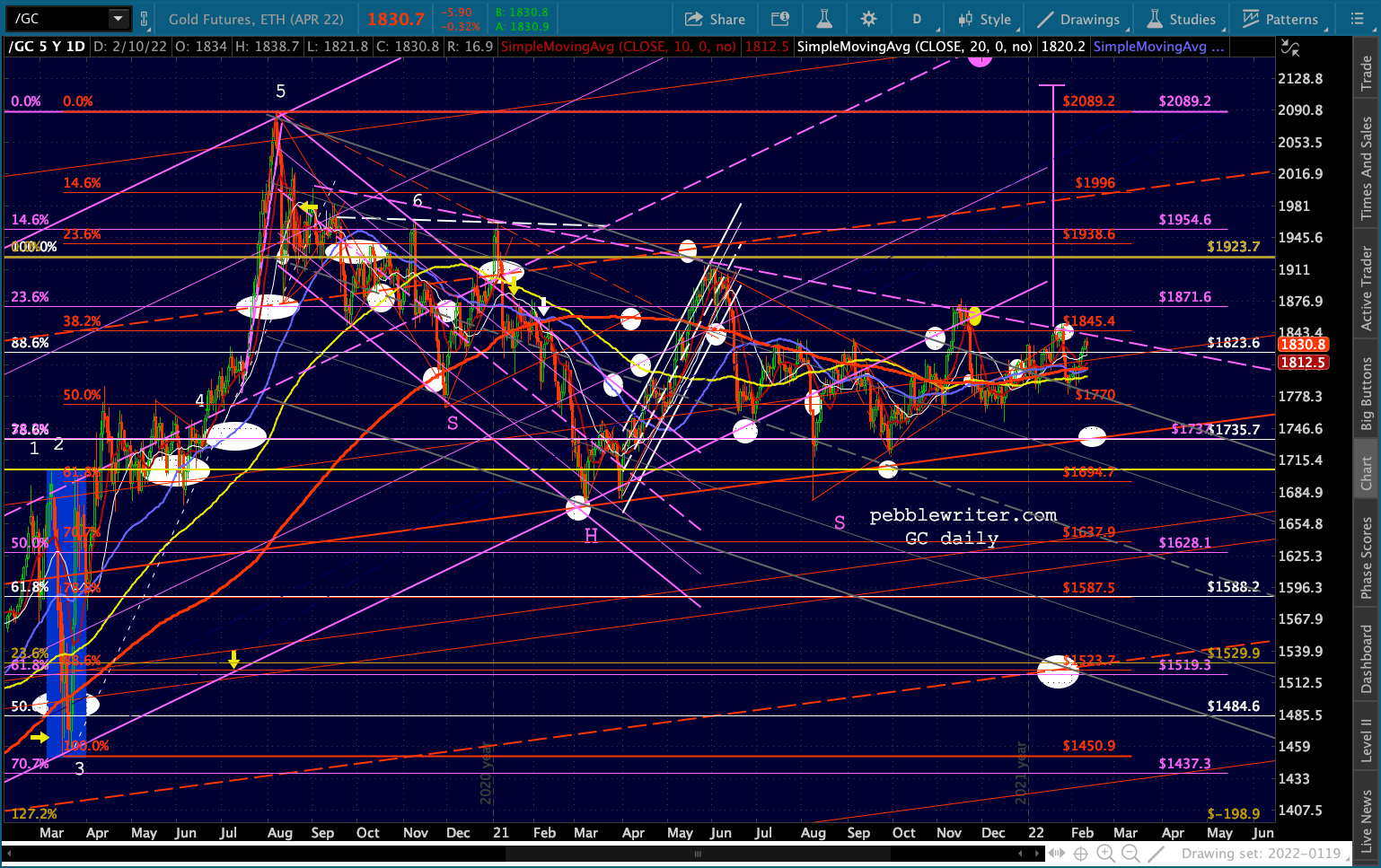

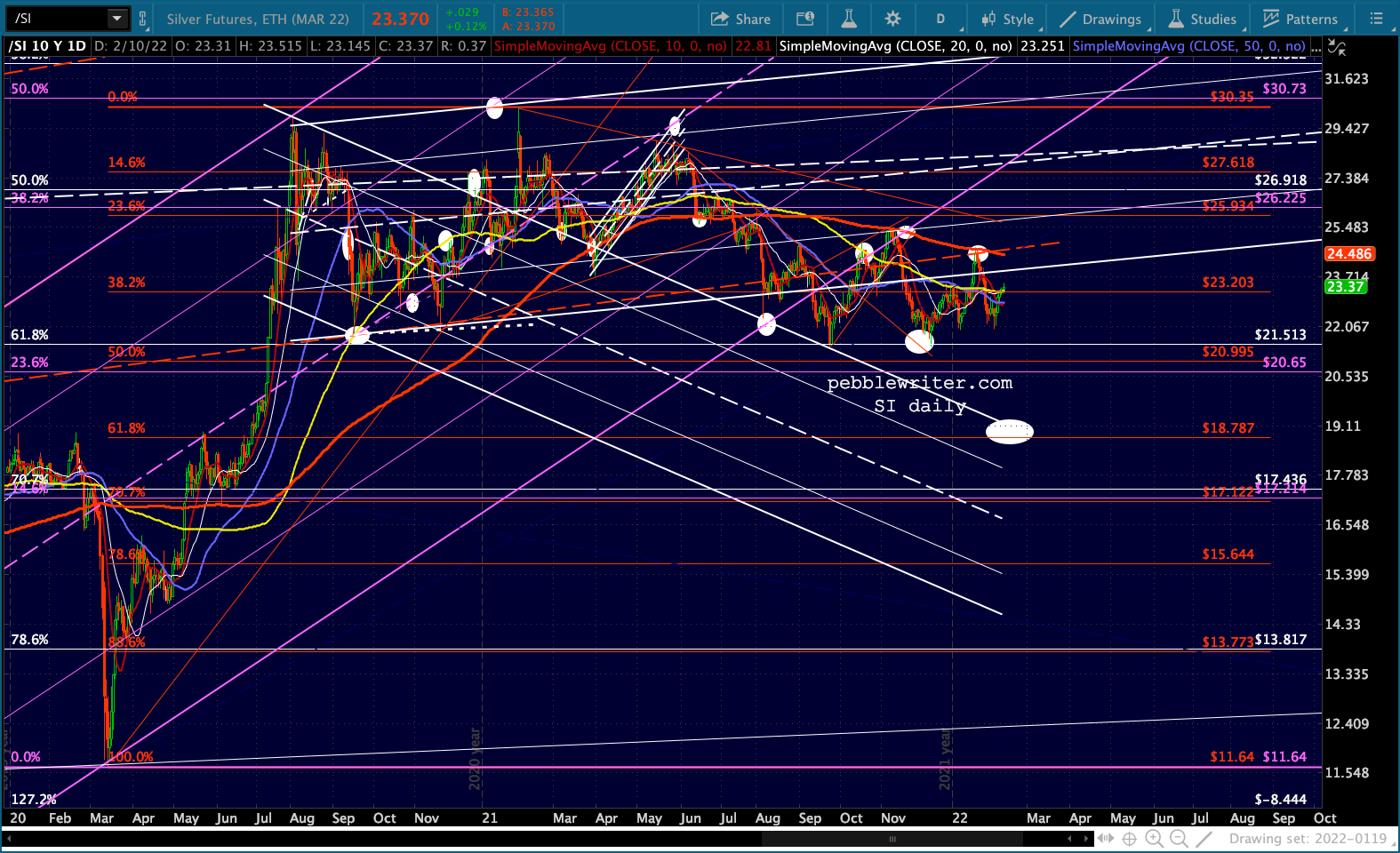

GC and SI have shown little reaction.

GC and SI have shown little reaction.

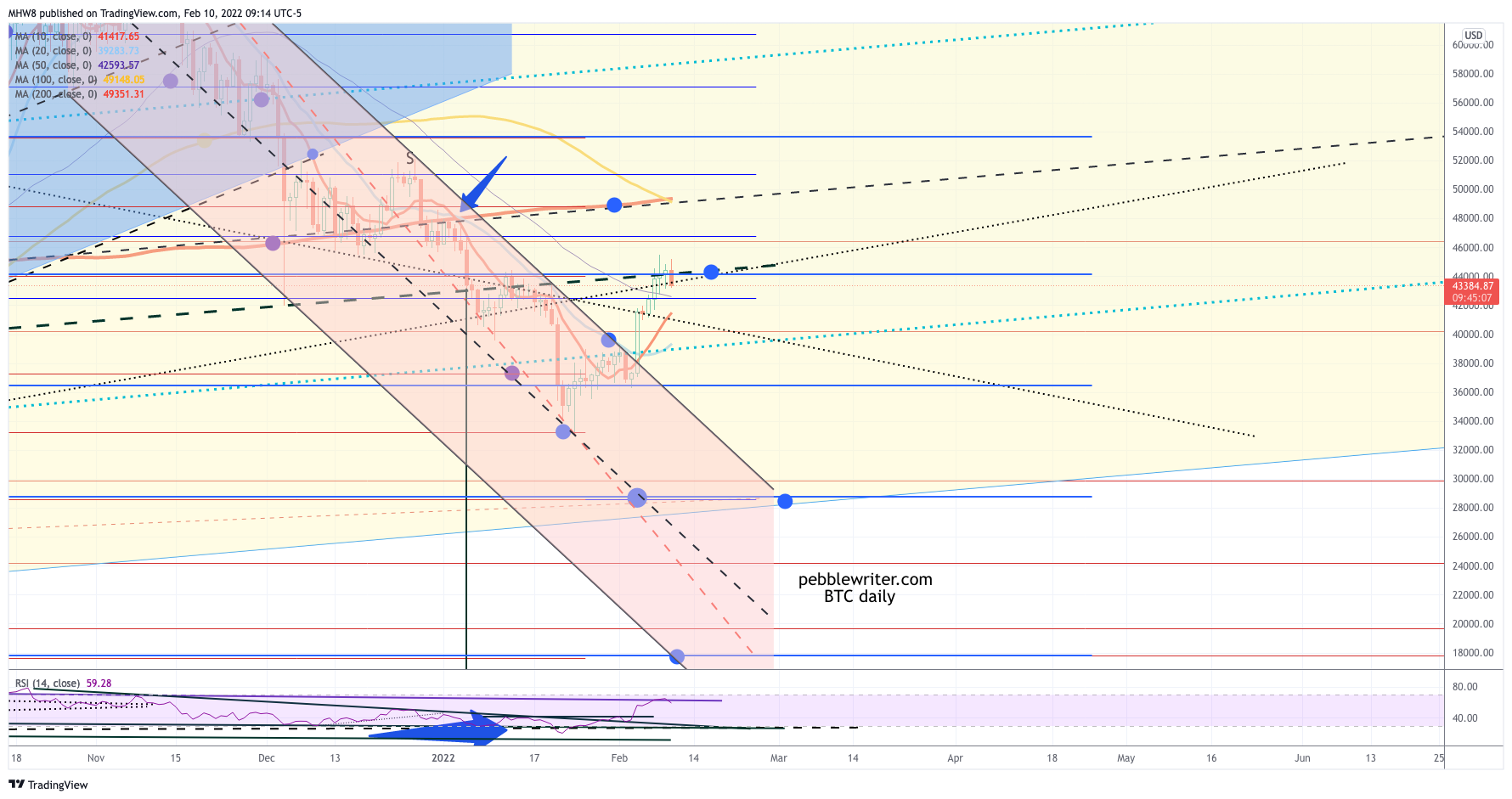

But BTC, having backtested its neckline, is selling off.

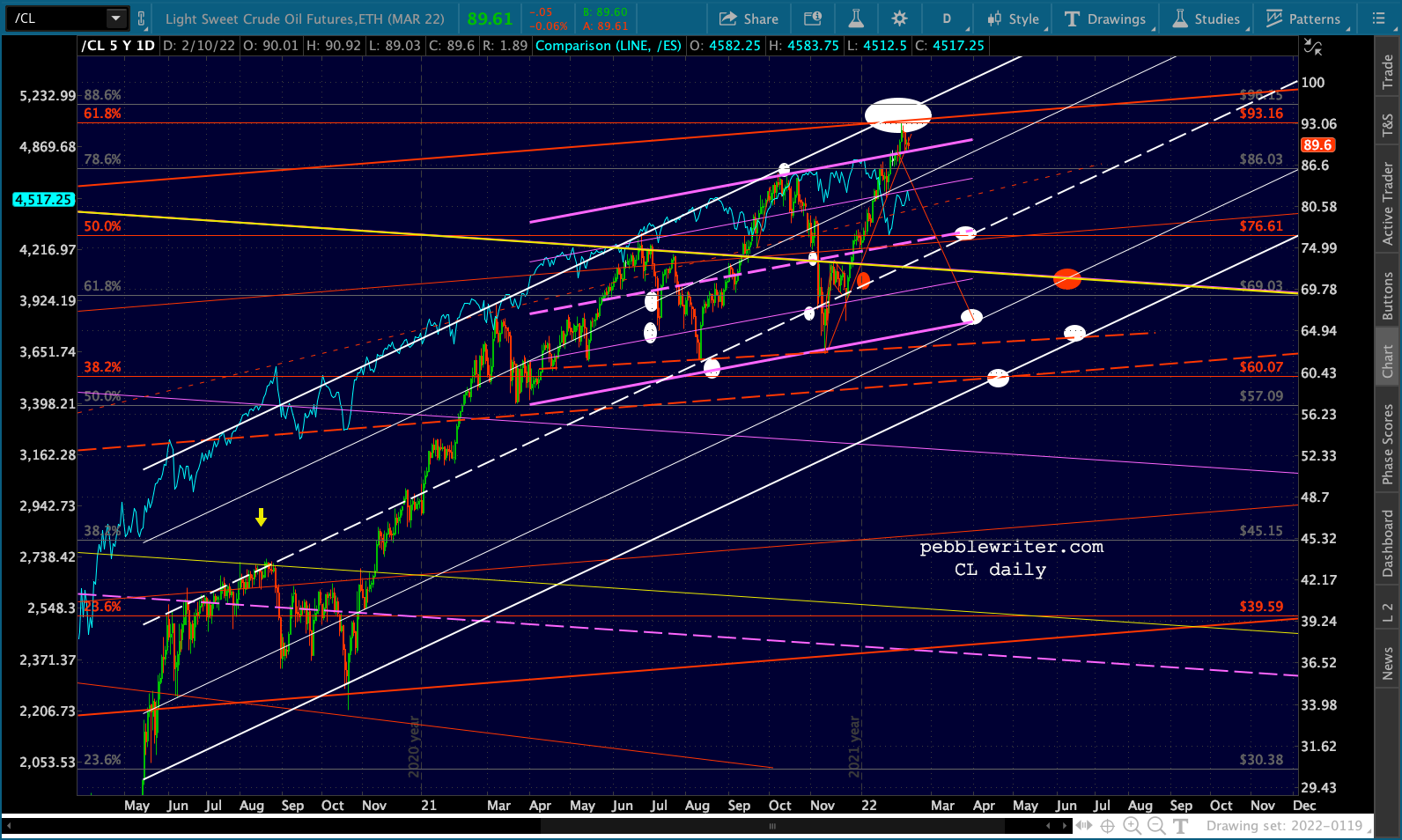

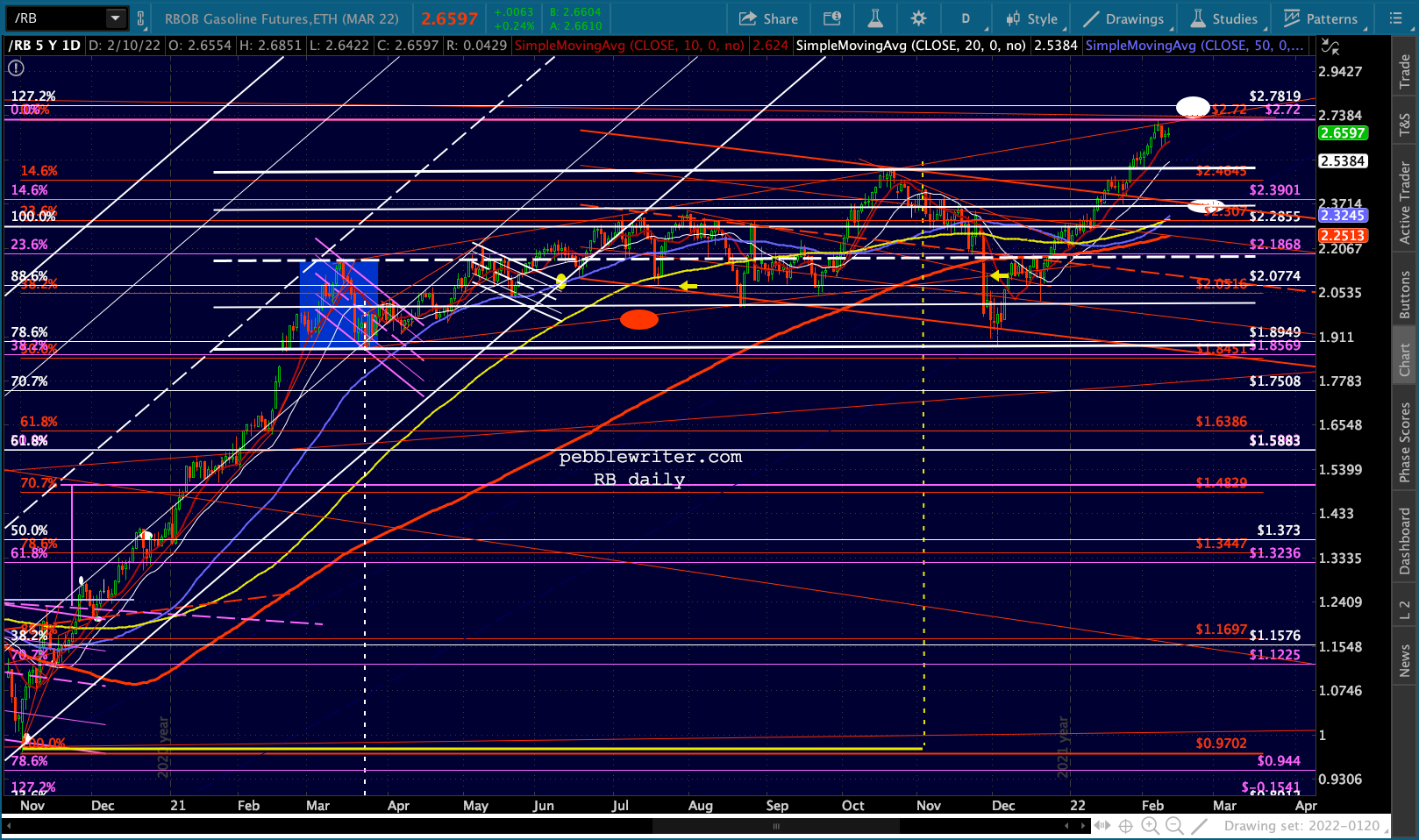

But BTC, having backtested its neckline, is selling off.  CL and RB are bouncing slightly, with RB potentially still eyeing the 2.7819 target.

CL and RB are bouncing slightly, with RB potentially still eyeing the 2.7819 target.

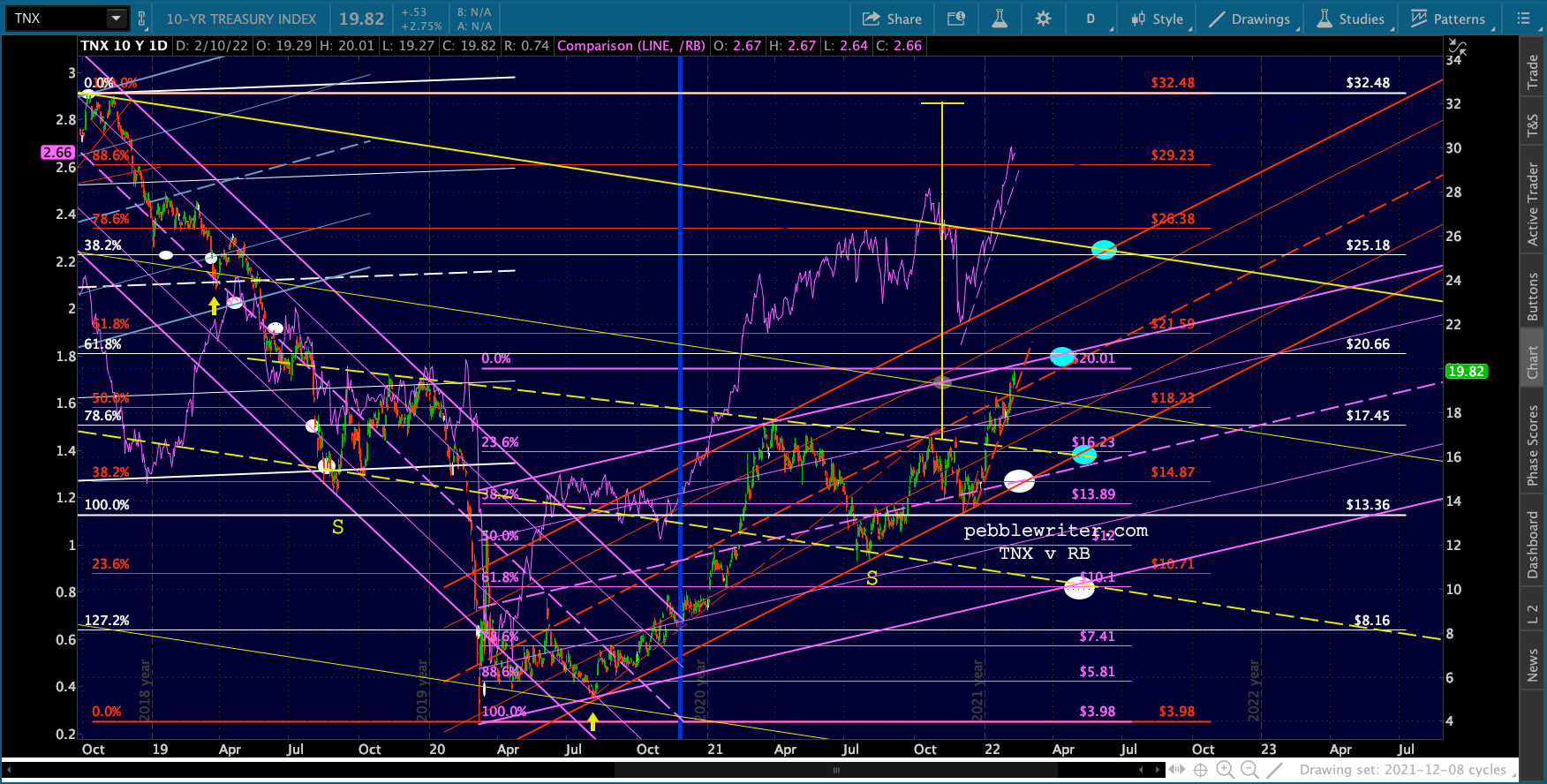

In other words, TNX has had no reason not to top 2%.

In other words, TNX has had no reason not to top 2%. I will still be out all day today, but will post later tonight if I get the chance.

I will still be out all day today, but will post later tonight if I get the chance.

GLTA.