February headline CPI came in at 0.4% versus 0.3% expected (and January.) Core CPI registered a 0.4% rise versus .03% forecast and 0.4% prior. YoY, headline was up 3.15%, up from 3.09% in January and a slight beat of the 3.1% expected, while core rose 3.8%, down from 3.9% in January.

Shelter and gas price increases were responsible for 60% of the rise in February.

This is in keeping with our Gas v CPI model which shows a slight uptick in MoM pricing in the midst of a YoY decline.

This is in keeping with our Gas v CPI model which shows a slight uptick in MoM pricing in the midst of a YoY decline.

The short-volatility algos were busy this morning, with VIX diving more than 5% in minutes to back below the 200-DMA.

The short-volatility algos were busy this morning, with VIX diving more than 5% in minutes to back below the 200-DMA.

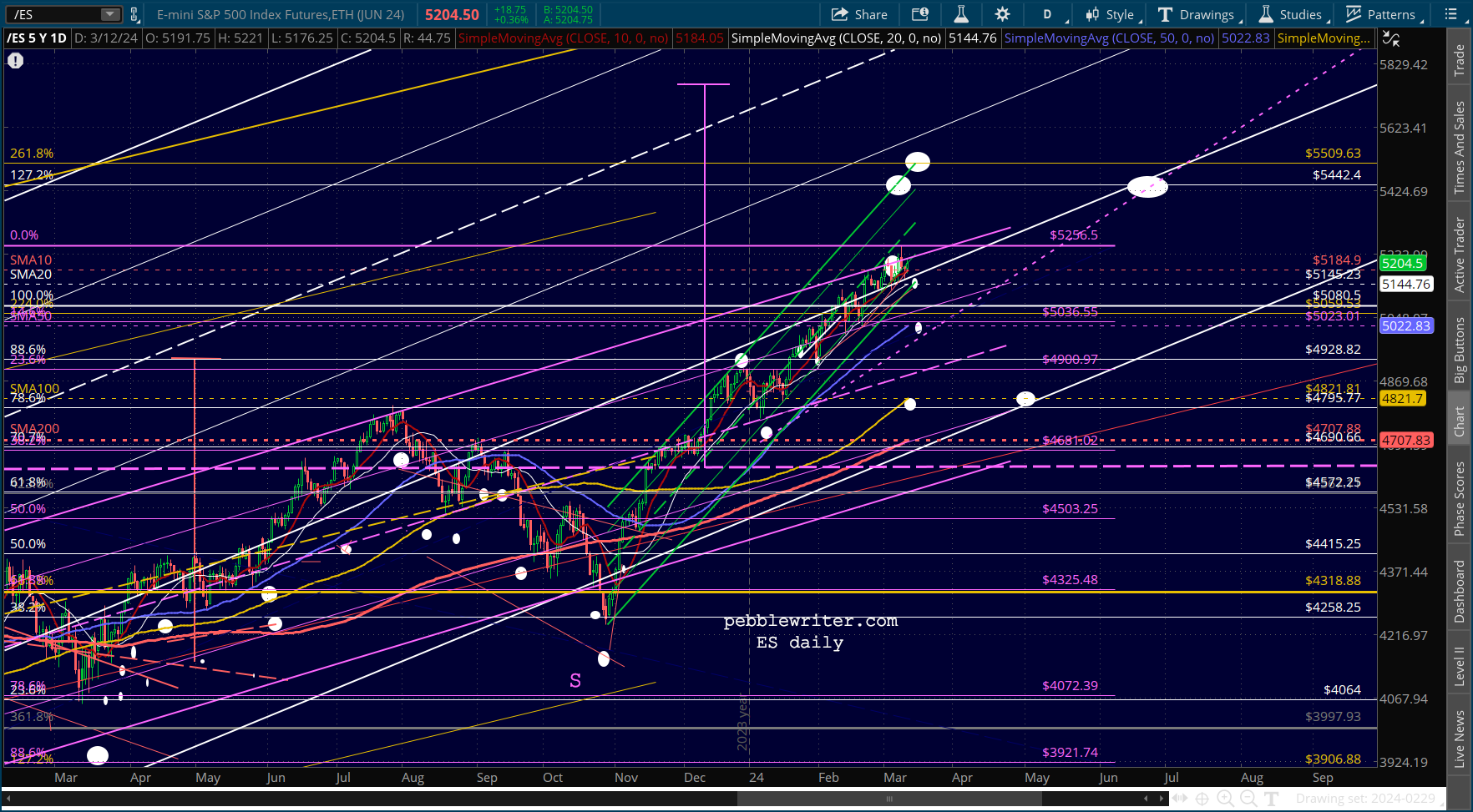

Futures, which might have been expected to tumble on the expectation of further delays to FOMC rate cuts, rallied instead.

Futures, which might have been expected to tumble on the expectation of further delays to FOMC rate cuts, rallied instead.  continued for members…

continued for members…

If the pre-market ramp holds, the green channel would remain intact and the RSI would continue to consolidate. More of the same…

If the pre-market ramp holds, the green channel would remain intact and the RSI would continue to consolidate. More of the same…

VIX’s nosedive (and pending 10/20 cross) will continue to be important to that equation…

VIX’s nosedive (and pending 10/20 cross) will continue to be important to that equation… …as will EURUSD’s refusal to slip lower…

…as will EURUSD’s refusal to slip lower… …and USDJPY’s ability to bounce at its SMA200.

…and USDJPY’s ability to bounce at its SMA200.

GC and SI were a little softer after the CPI print. GC is backtesting the 1.272 Fib, with the IH&S neckline down at 2086 the more important support.

GC and SI were a little softer after the CPI print. GC is backtesting the 1.272 Fib, with the IH&S neckline down at 2086 the more important support.

CL and RB continue to hold up well…

CL and RB continue to hold up well…

…contributing to support for the 10Y. Note that there’s an important 10Y auction at 1pm ET today.

…contributing to support for the 10Y. Note that there’s an important 10Y auction at 1pm ET today.

GLTA

GLTA