Official core PCE came in at 3.5% YoY (0.2% MoM) which was high enough to knock fuutres off their overnight highs but not enough to drive VIX above its 10-day moving average.

We pay a lot of attention to VIX as it’s perhaps the most important daily driver of algo behaviour. After poking up above its SMA10 in October for all of nine sessions, it has now spent an entire month ducking below it – stymieing any equity pullbacks…until now.

continued for members…

continued for members…

The current equity picture remains unchanged. Prices continue to climb toward our year-end target, though they declined to remain broken out above the white channel line discussed yesterday.

It can be best seen in the SPX chart.

It can be best seen in the SPX chart.

Needless to say, this is a very, very big deal. Failure to break through means no more upside at best…and potentially a substantial downturn.

Needless to say, this is a very, very big deal. Failure to break through means no more upside at best…and potentially a substantial downturn. Equities are also running into some resistance from EURUSD, which is taking at least a pause here.

Equities are also running into some resistance from EURUSD, which is taking at least a pause here. And USDJPY is hanging by a thread to its fan line from March, with its SMA200 still making plenty of sense down at 142.03.

And USDJPY is hanging by a thread to its fan line from March, with its SMA200 still making plenty of sense down at 142.03. DXY’s chart is interesting, as the influence from the euro and yen have been enough to keep it above a TL off its Jun 2021 lows. Although it fell through its SMA200 recently, it’s making an aggressive backtest today. A push back above the SMA200 would be a big negative for stocks.

DXY’s chart is interesting, as the influence from the euro and yen have been enough to keep it above a TL off its Jun 2021 lows. Although it fell through its SMA200 recently, it’s making an aggressive backtest today. A push back above the SMA200 would be a big negative for stocks.

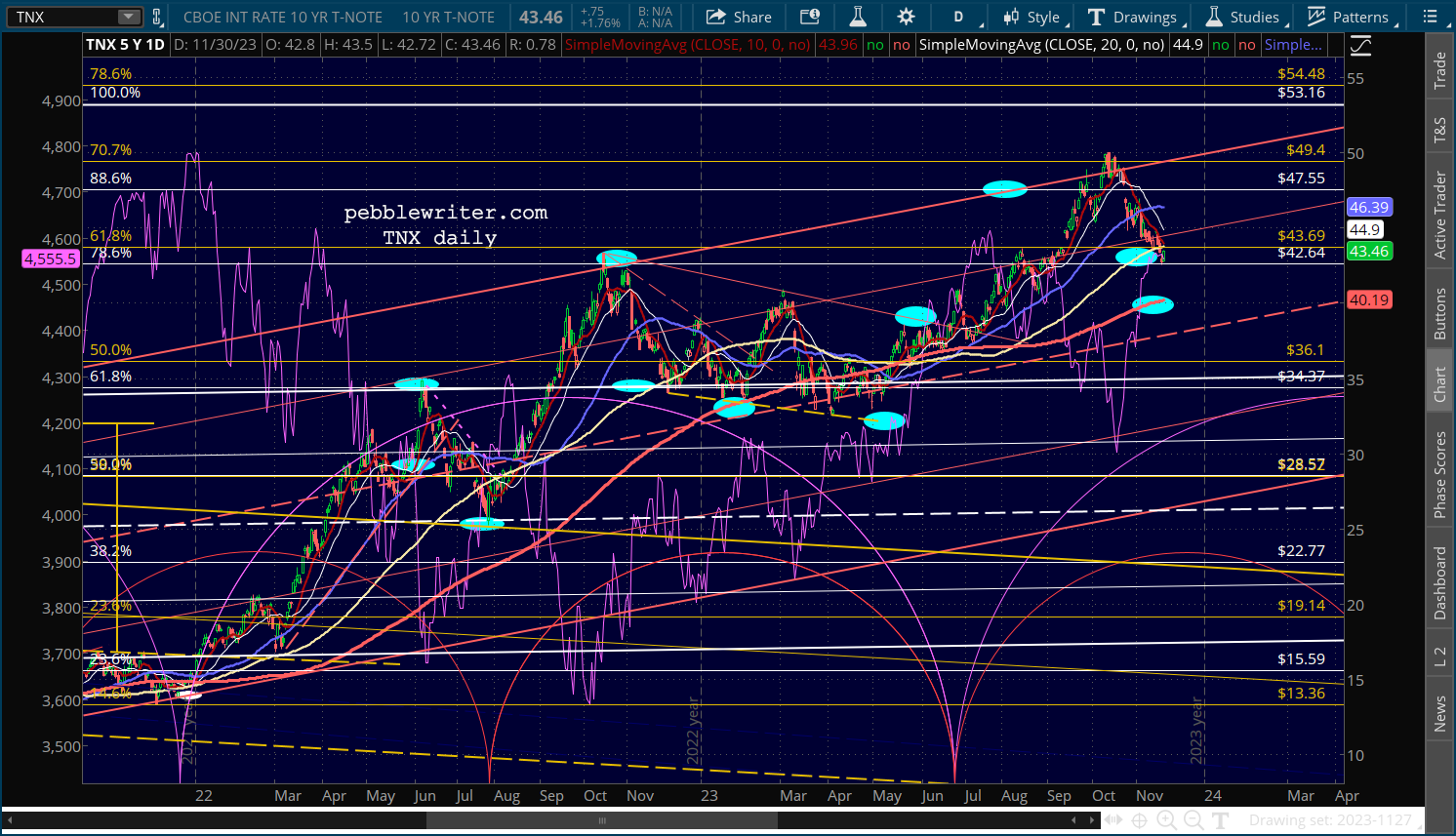

Meanwhile, OPEC+ agreed on a 1MM bpd production cut, sending CL back above its SMA200 and dinging the low inflation argument. Don’t be surprised if this sends the 10Y back above 4.4%.

Meanwhile, OPEC+ agreed on a 1MM bpd production cut, sending CL back above its SMA200 and dinging the low inflation argument. Don’t be surprised if this sends the 10Y back above 4.4%.

It would potentially prevent a breakdown of the 10Y – or at least cause a backtest.

It would potentially prevent a breakdown of the 10Y – or at least cause a backtest.

Stay tuned…

Stay tuned…

UPDATE: EOD

FWIW, the Dow came within 37 points of its .886 retracement from the Jan 2022 highs.