August CPI came in at 0.6% MoM and 3.7% YoY, slightly higher than expectations. Core CPI was 0.3% MoM and 4.3% YoY, also higher than expectations. This is in line with our forecast, driven largely by higher costs for rent, transportation, and energy.

Futures are flat ahead of the open…

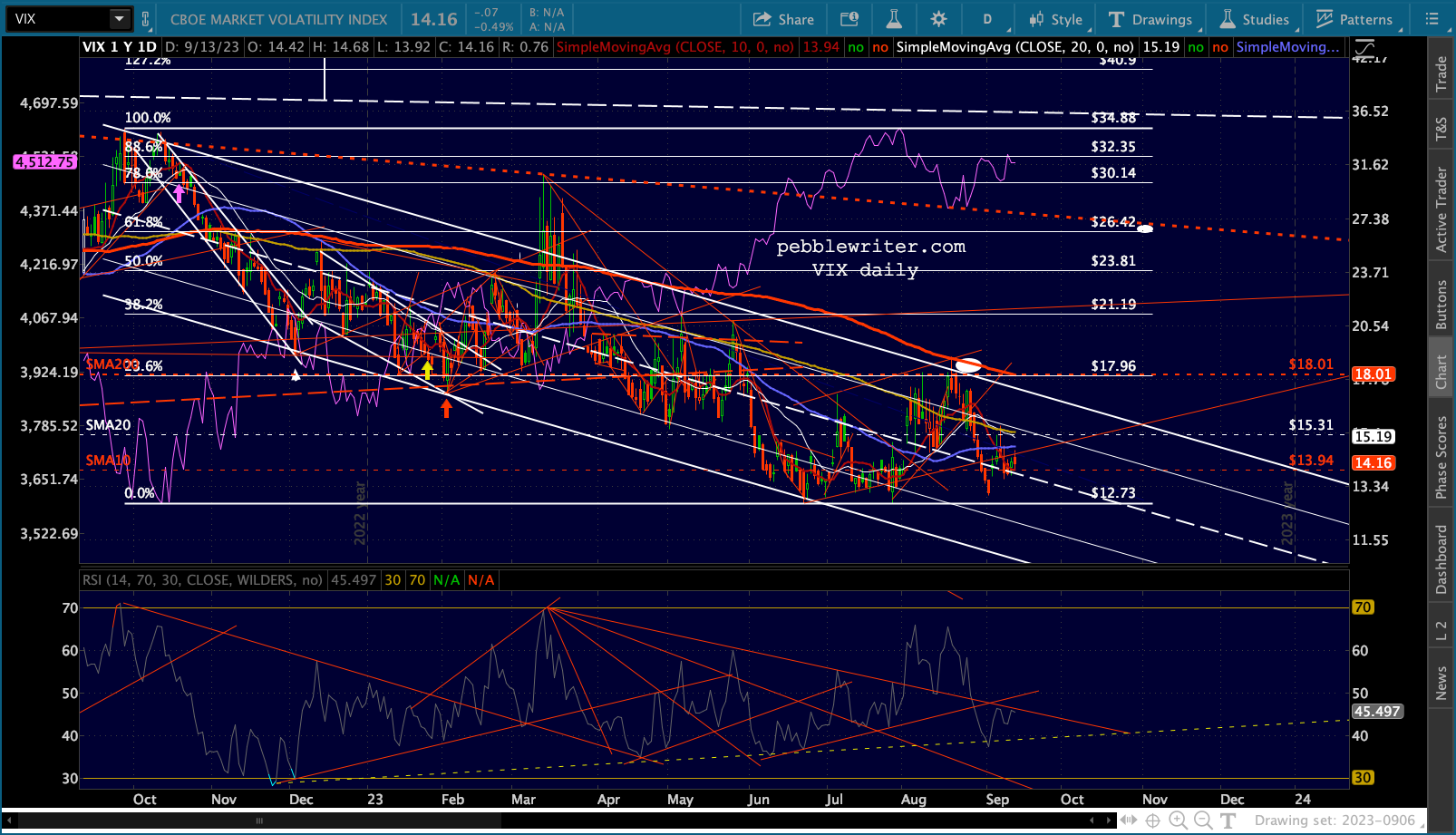

Futures are flat ahead of the open… …with VIX making lower lows on algo trading.

…with VIX making lower lows on algo trading.  Rising inflation, driven largely by YoY comps for energy prices, should make a Fed pause less likely.

Rising inflation, driven largely by YoY comps for energy prices, should make a Fed pause less likely.

continued for members…

continued for members…

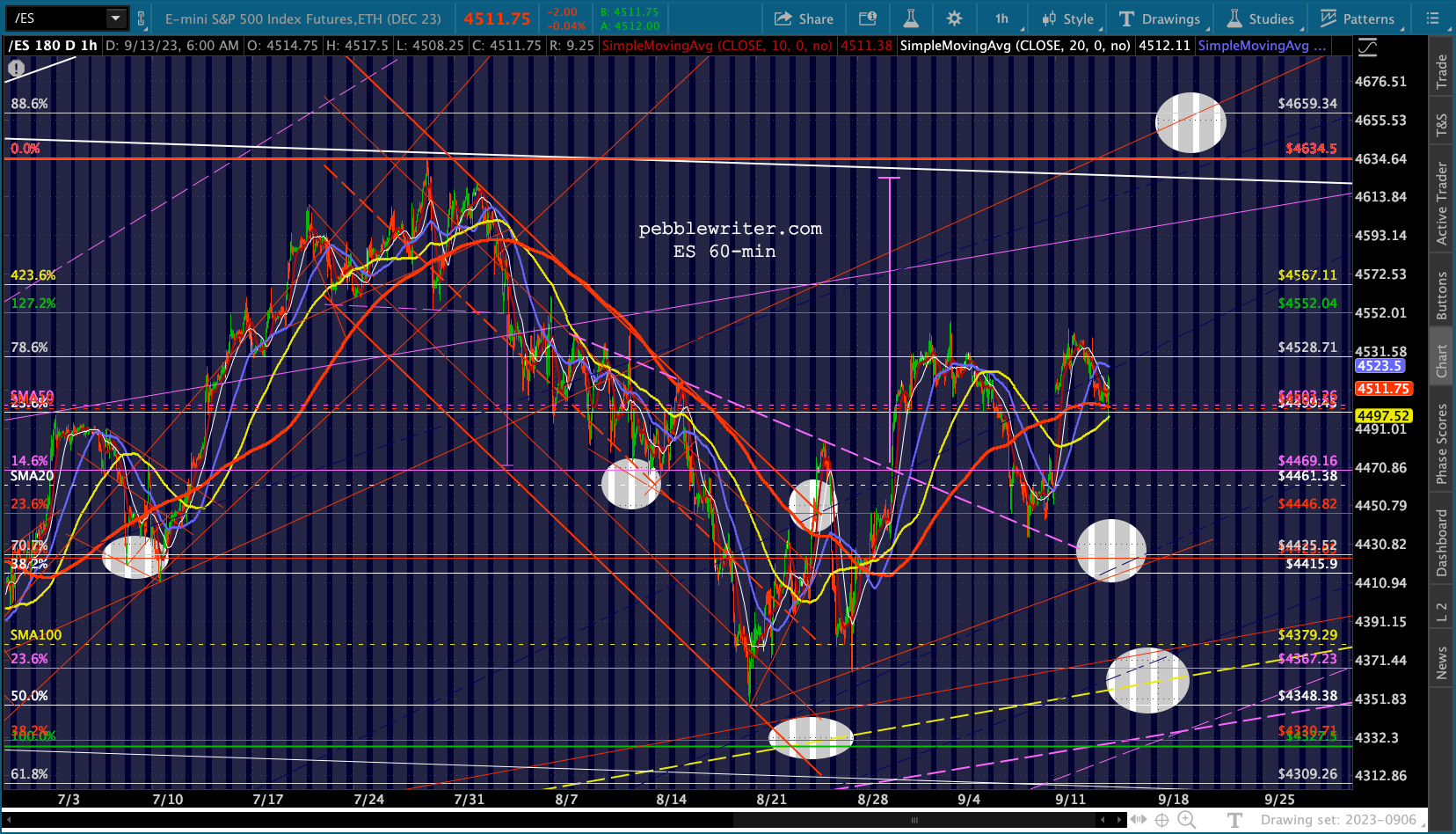

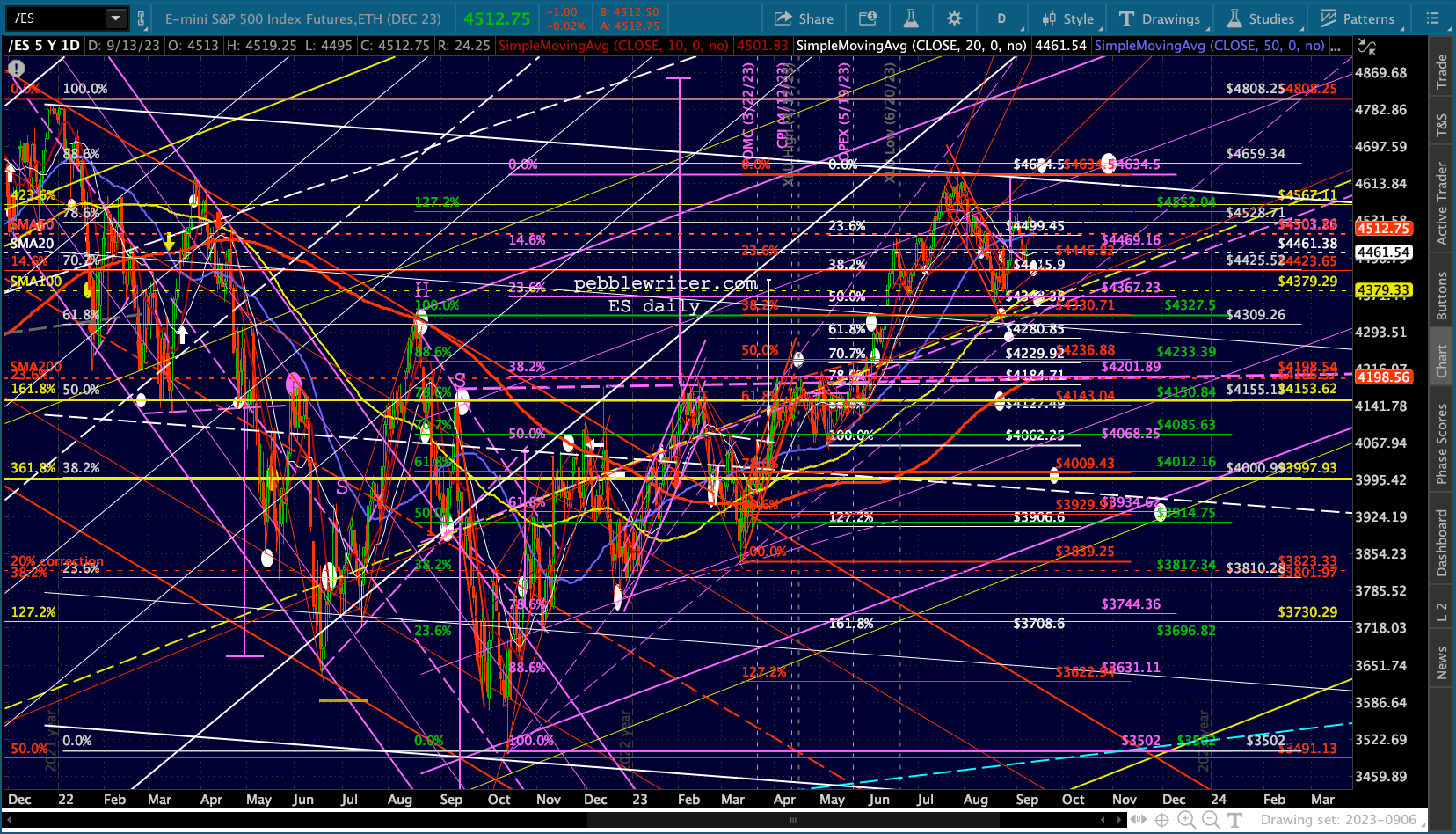

Note that ES is still holding above its SMA50…

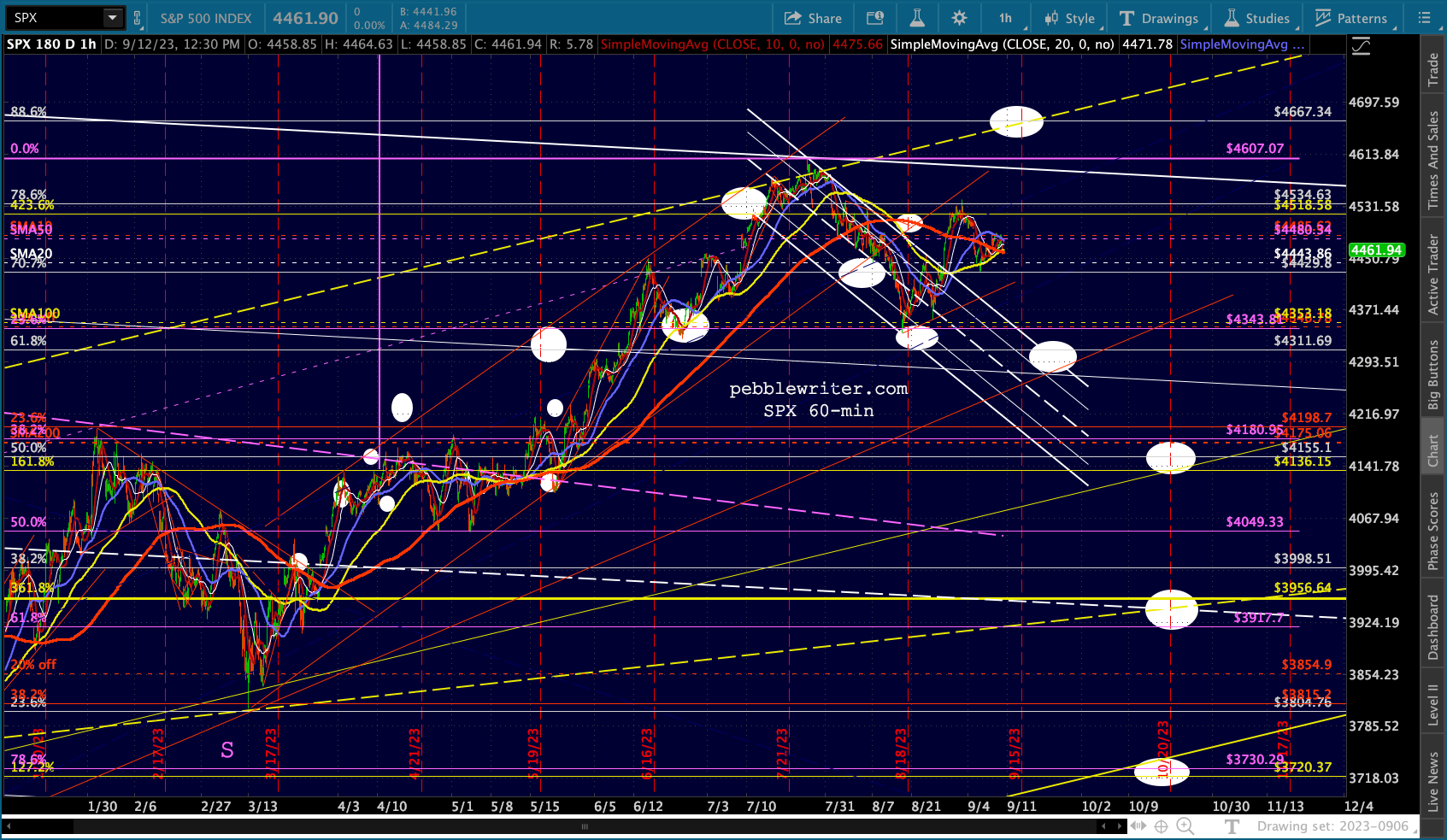

…while SPX is below its.

…while SPX is below its. VIX should continue to drive equity prices, but as yet it hasn’t really broken down or out.

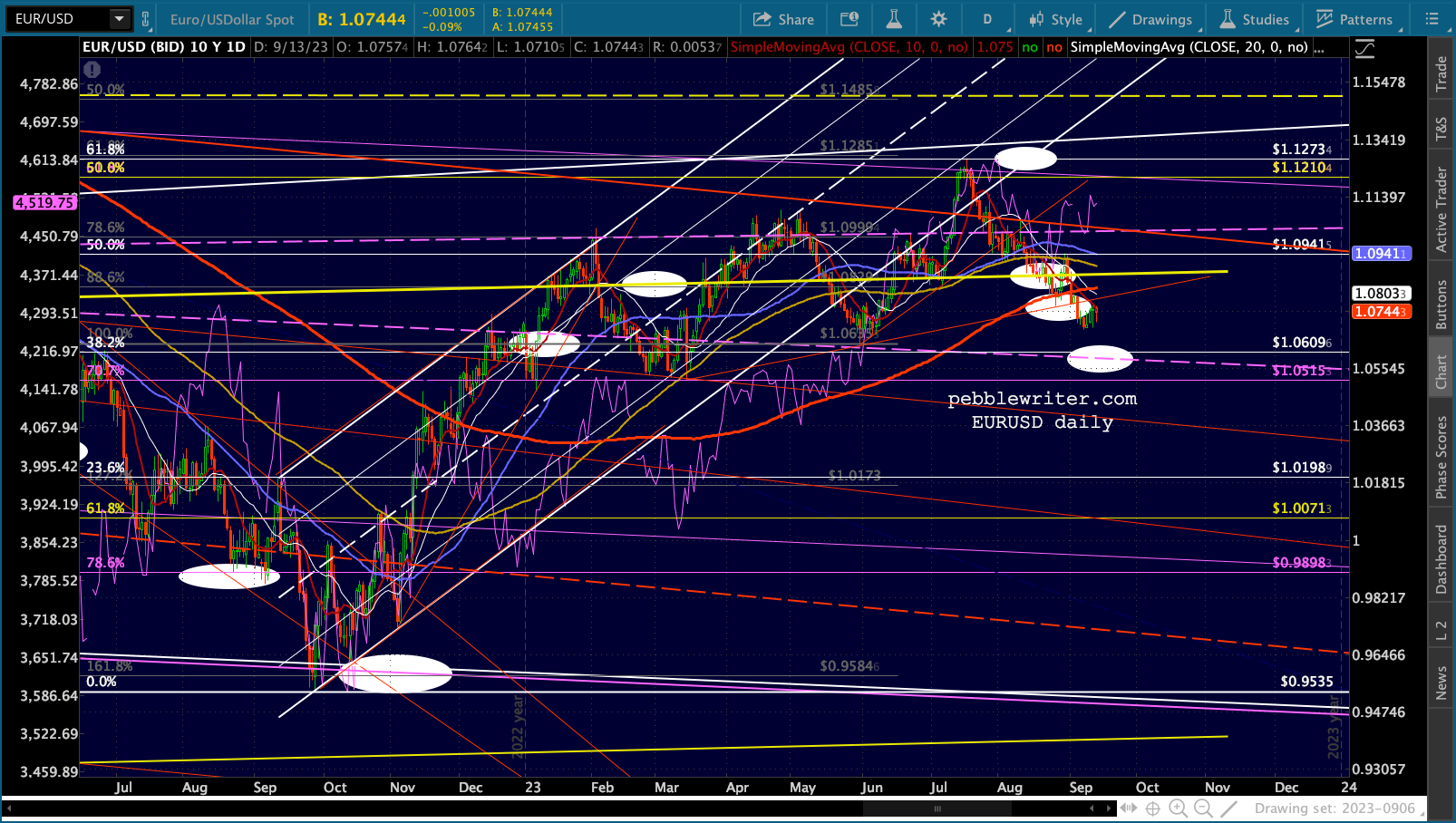

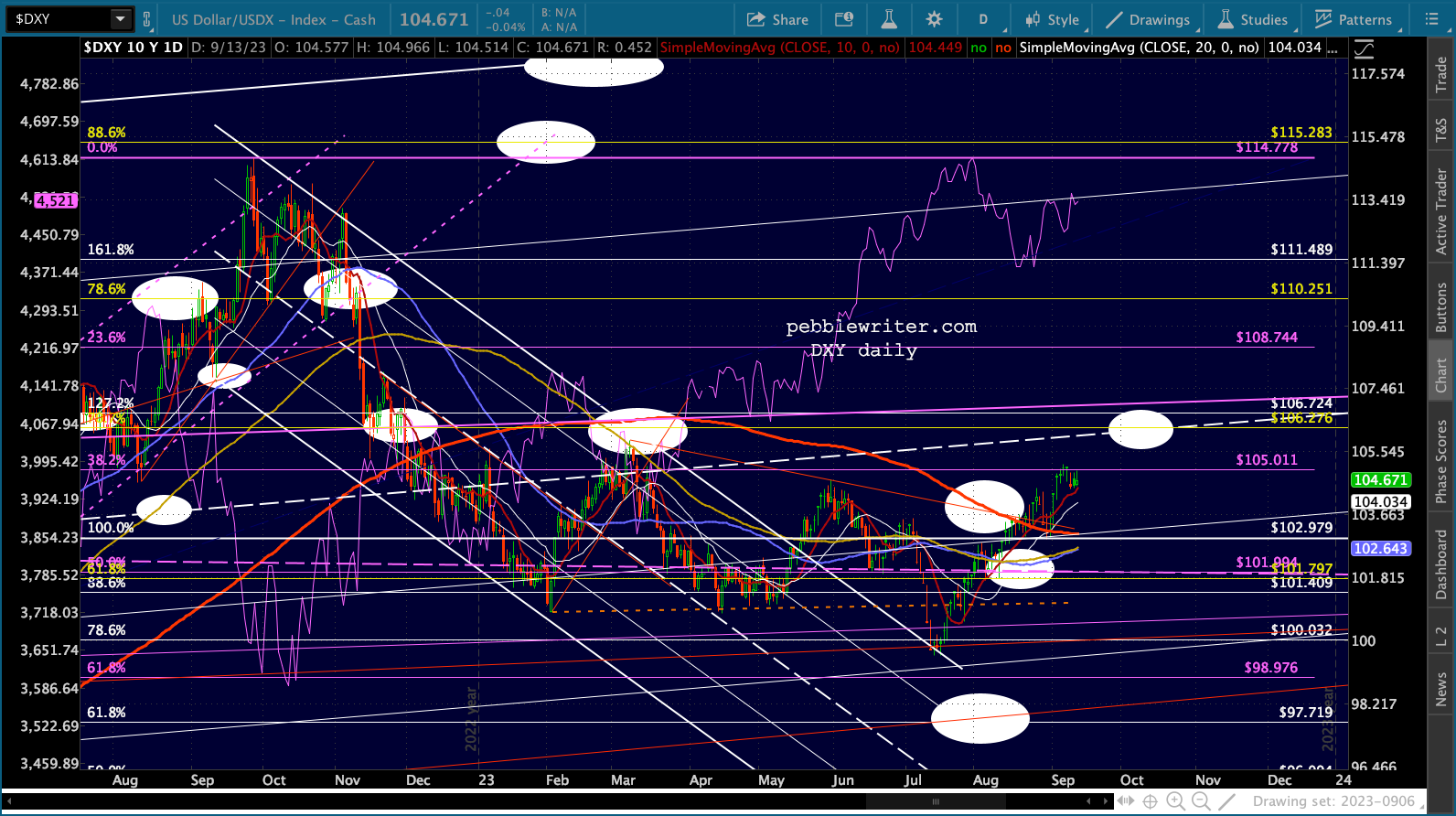

VIX should continue to drive equity prices, but as yet it hasn’t really broken down or out. Currencies are being supported in the wake of CPI, with EURUSD slightly higher and backtesting its SMA10 while DXY backtests its.

Currencies are being supported in the wake of CPI, with EURUSD slightly higher and backtesting its SMA10 while DXY backtests its.

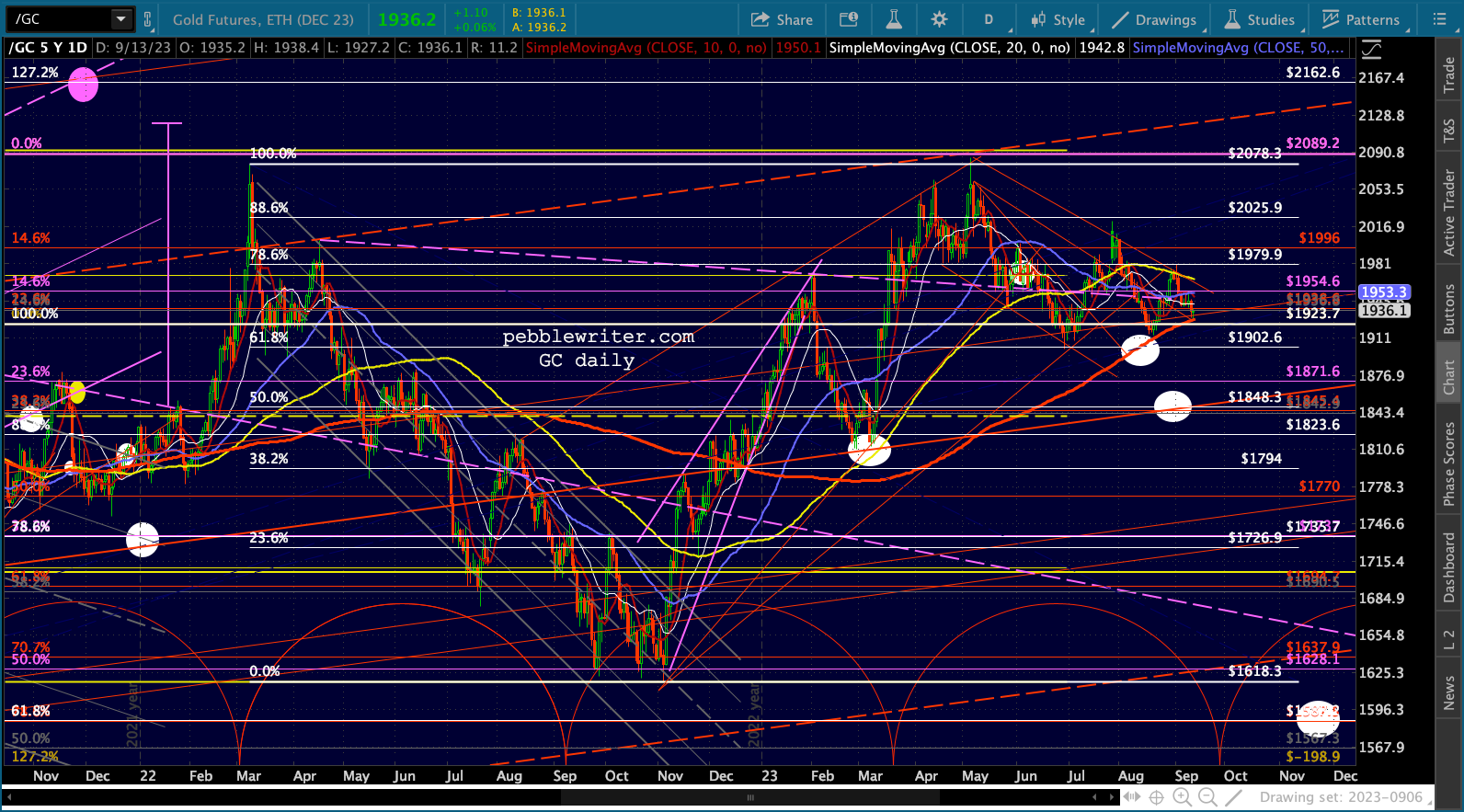

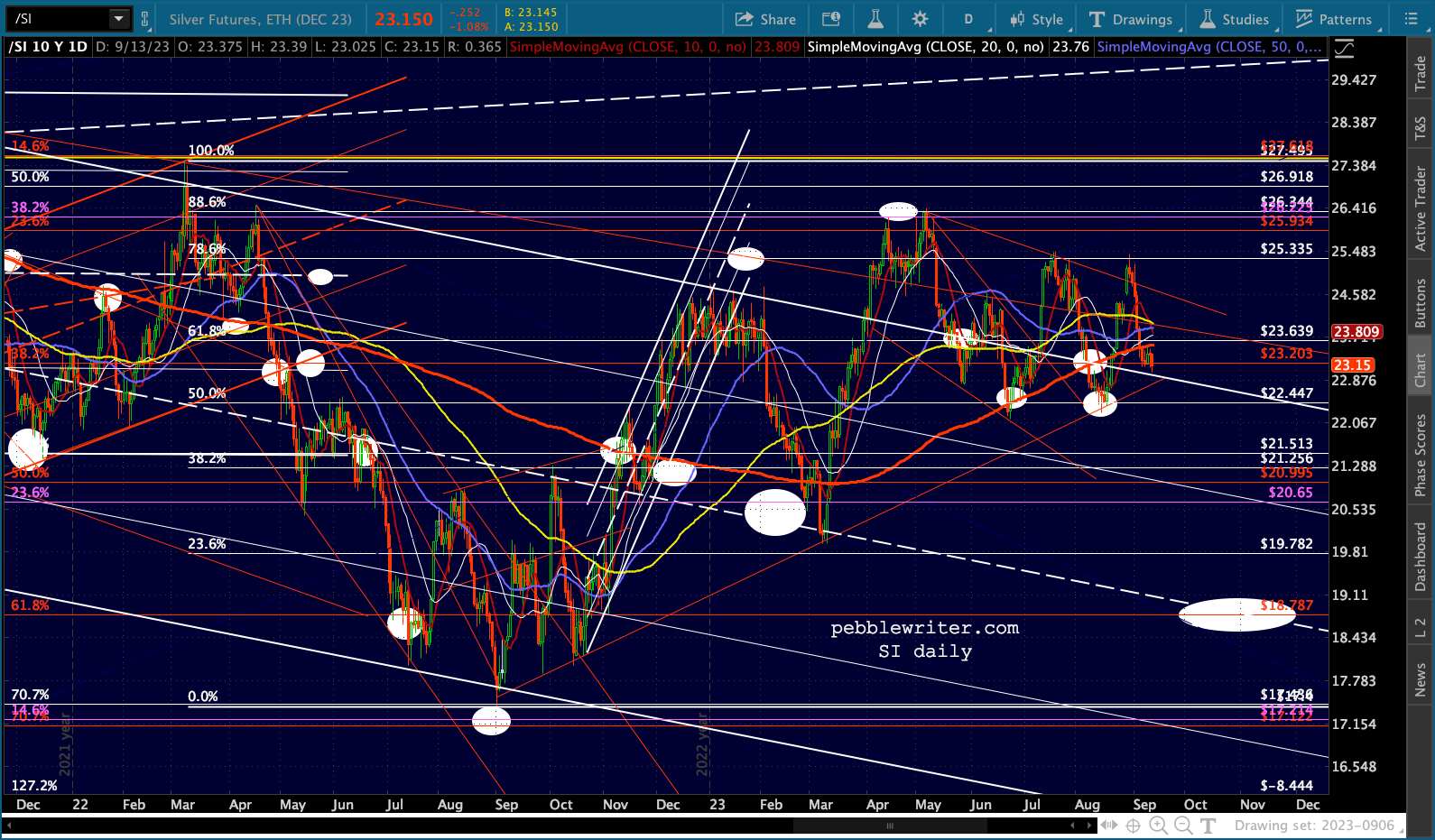

GC and SI continue to falter. GC has backtested its SMA200 again and SI is still below its SMA200 and nearing the red TL of support.

GC and SI continue to falter. GC has backtested its SMA200 again and SI is still below its SMA200 and nearing the red TL of support.

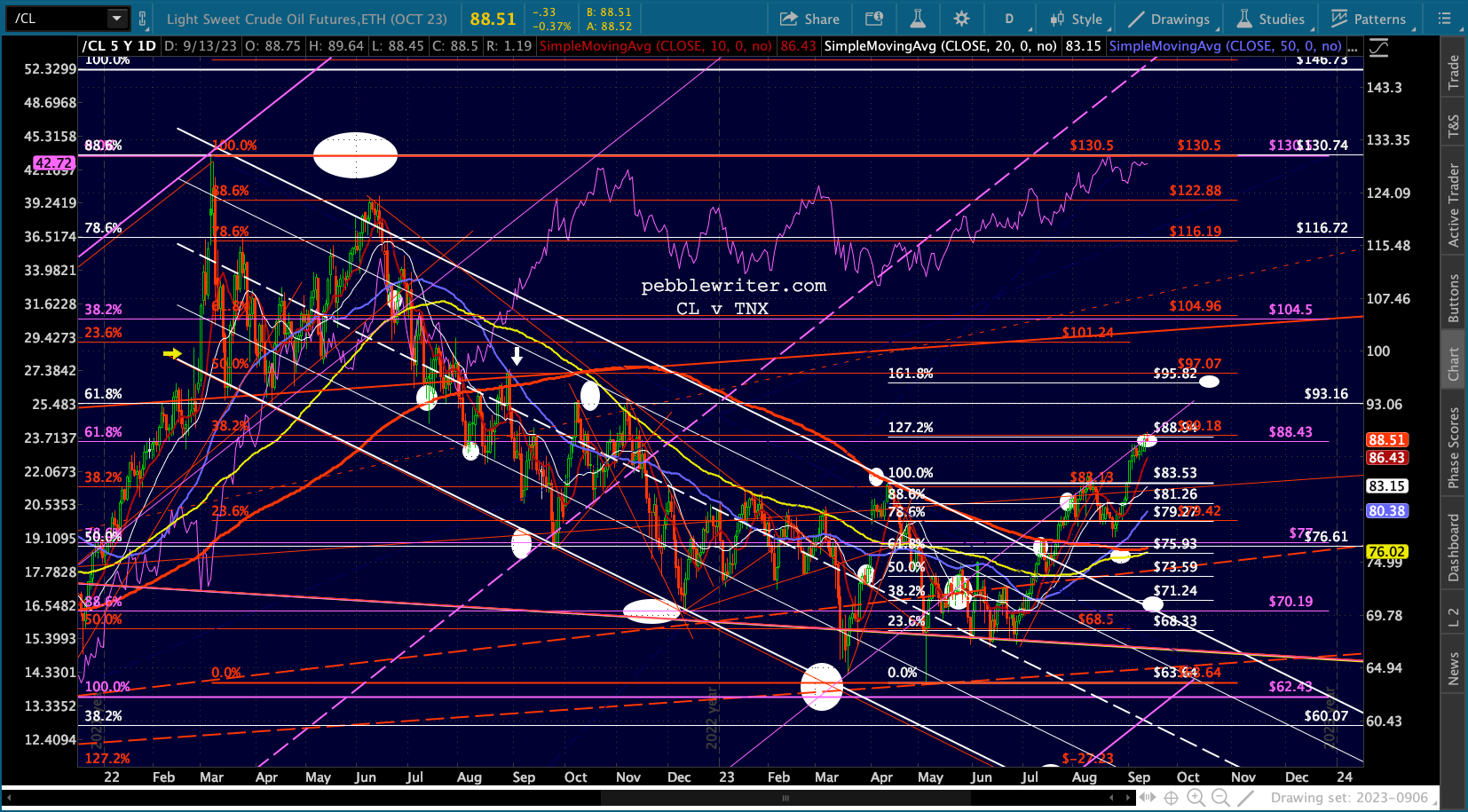

CL has reached out 88.94 target and has some important decisions to make.

CL has reached out 88.94 target and has some important decisions to make.

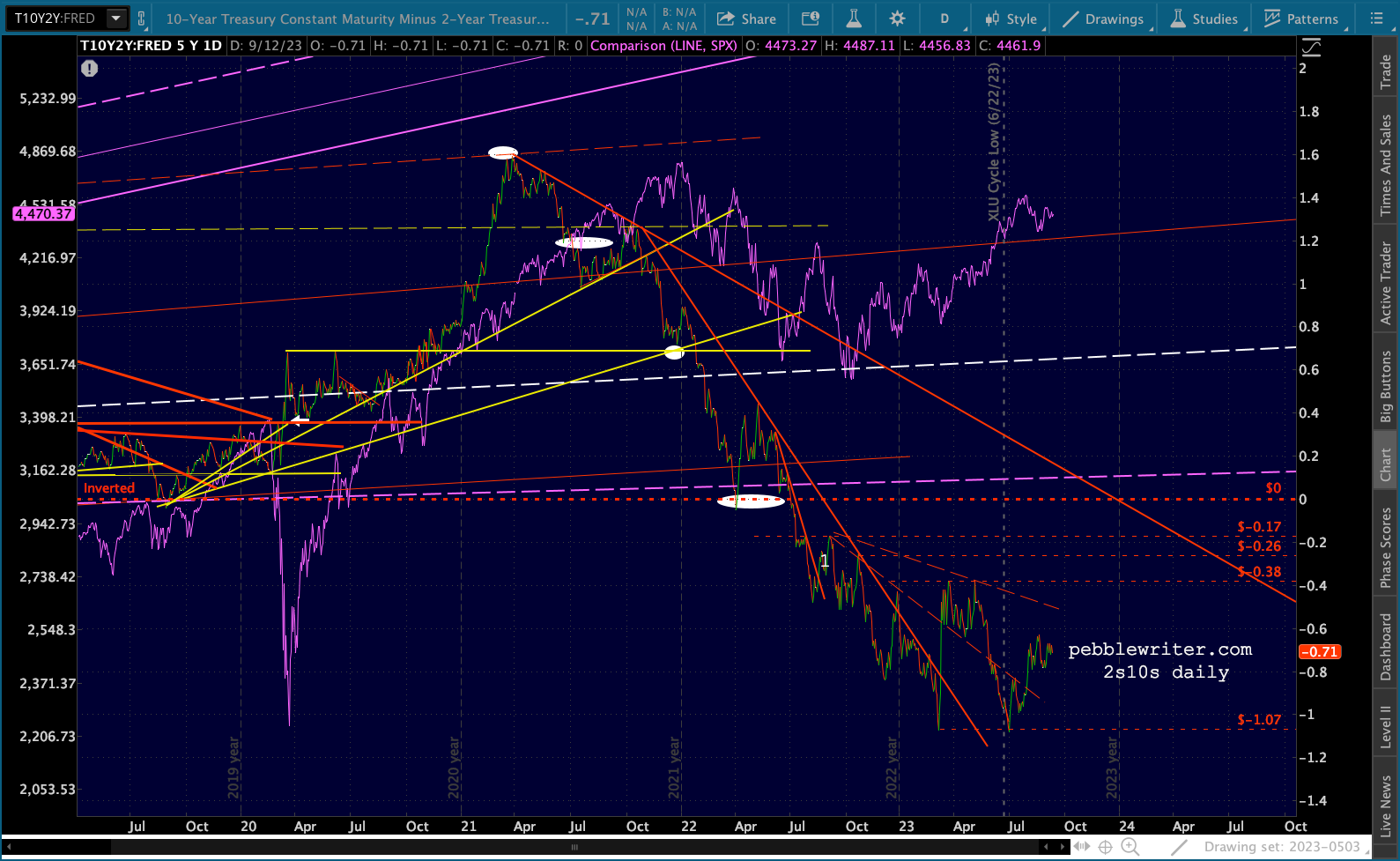

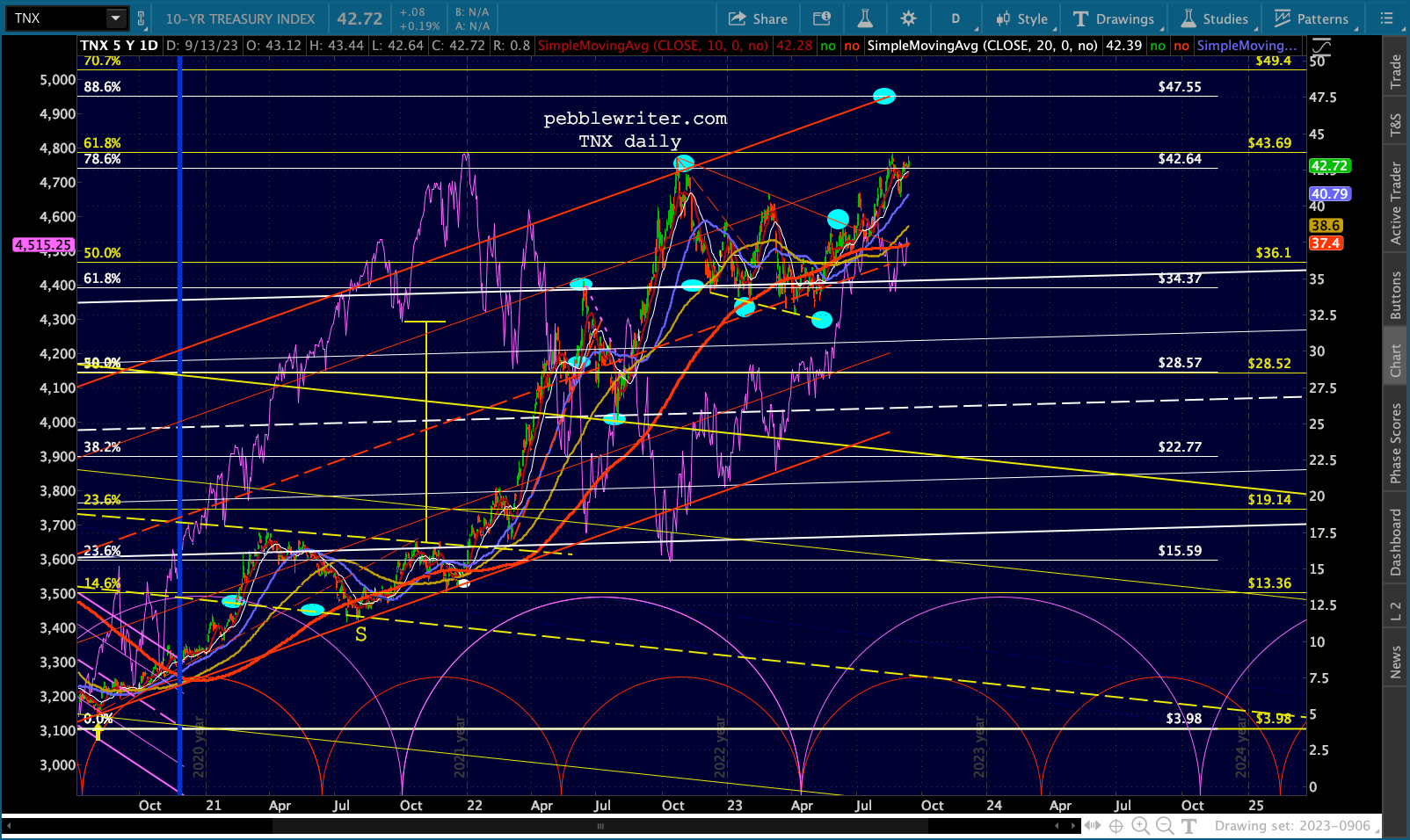

Both the 2Y and 10Y are nearing new highs, though the 2s10s remains in a state of flux.

Both the 2Y and 10Y are nearing new highs, though the 2s10s remains in a state of flux.