Two quotes by Janet Yellen, only hours apart. The first clearly emphasizes the very real risk of rapidly rising inflation…

“It may be that interest rates will have to rise somewhat to make sure that our economy doesn’t overheat, even though the additional spending is relatively small relative to the size of the economy.”

…while the other clearly walks back the earlier assertion.

“I don’t think there’s going to be an inflationary problem. But if there is, the Fed will be counted on to address them.”

The reason for the second comment, of course, was the market’s reaction to the first – a tantrum, if you will.

Most of us remember when, in 2013, Bernanke spooked the markets with talk of a rollback in bond purchases. Yellen did the same thing a few years later as Fed chair. This one is slightly different, as it highlights the facts which, by now, should be clear to everyone: inflation is a very real danger to the economy and the markets.

Most of us remember when, in 2013, Bernanke spooked the markets with talk of a rollback in bond purchases. Yellen did the same thing a few years later as Fed chair. This one is slightly different, as it highlights the facts which, by now, should be clear to everyone: inflation is a very real danger to the economy and the markets.

Yellen’s retraction won’t change that.

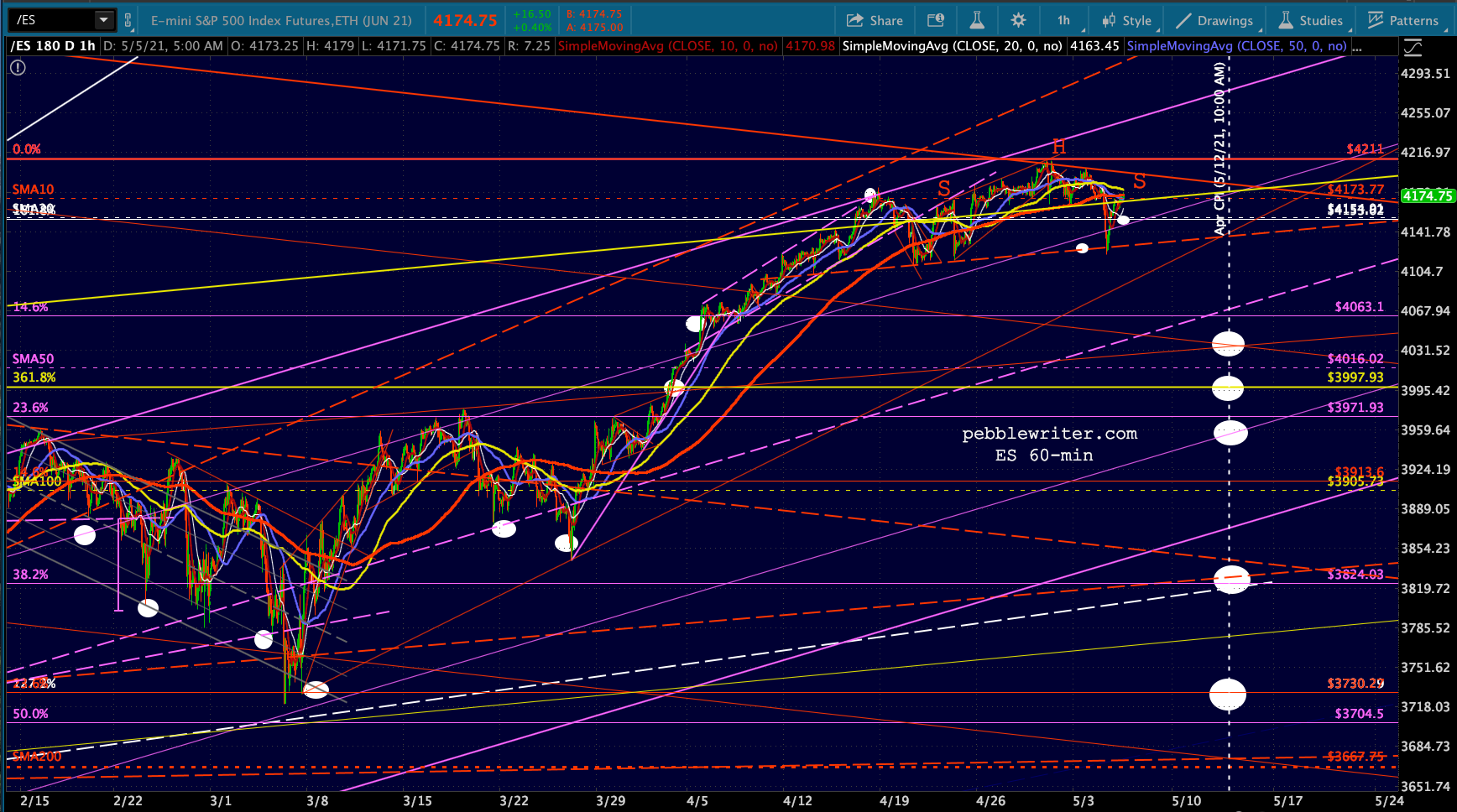

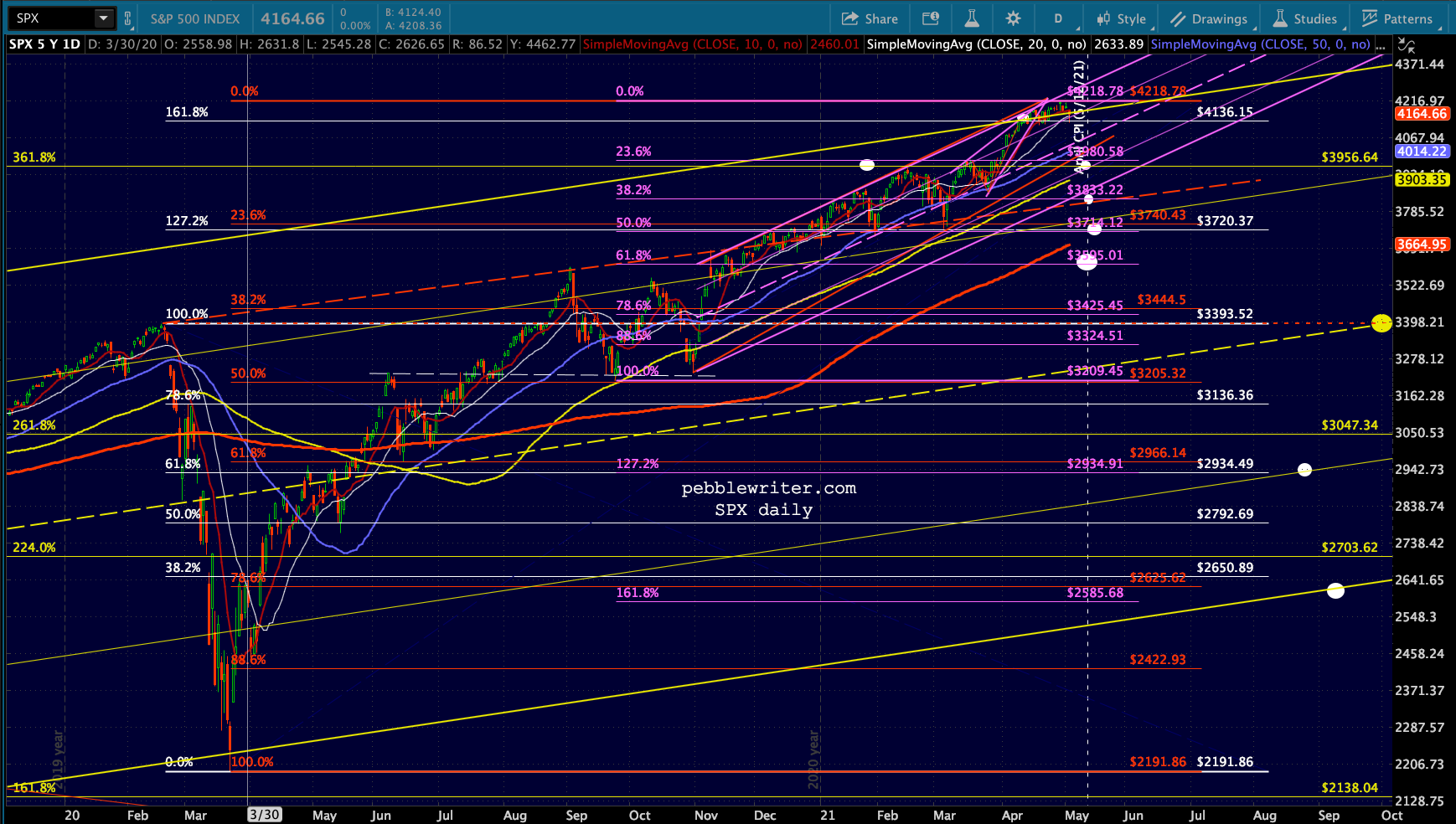

continued for members…Meanwhile, ES has reached a backtest of its SMA10 – the dividing line between a continuation of the uptrend and another leg down. We have a new H&S Pattern to watch, this one suggesting a 90-pt decline. There are so many near-term targets, but we should remember what the downside could be if the SMA200 should be tested and fail.

There are so many near-term targets, but we should remember what the downside could be if the SMA200 should be tested and fail.

The SPX version:

The SPX version:

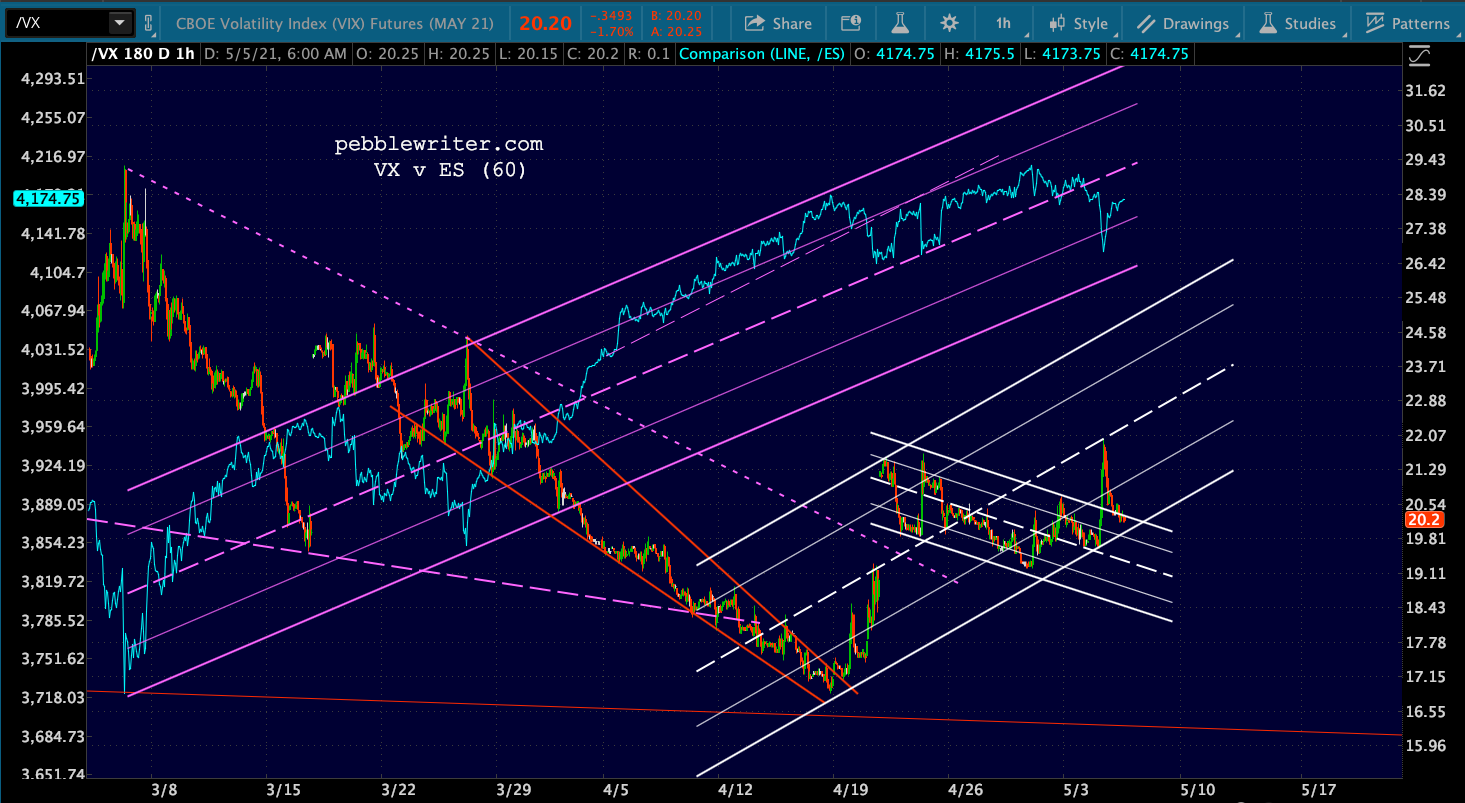

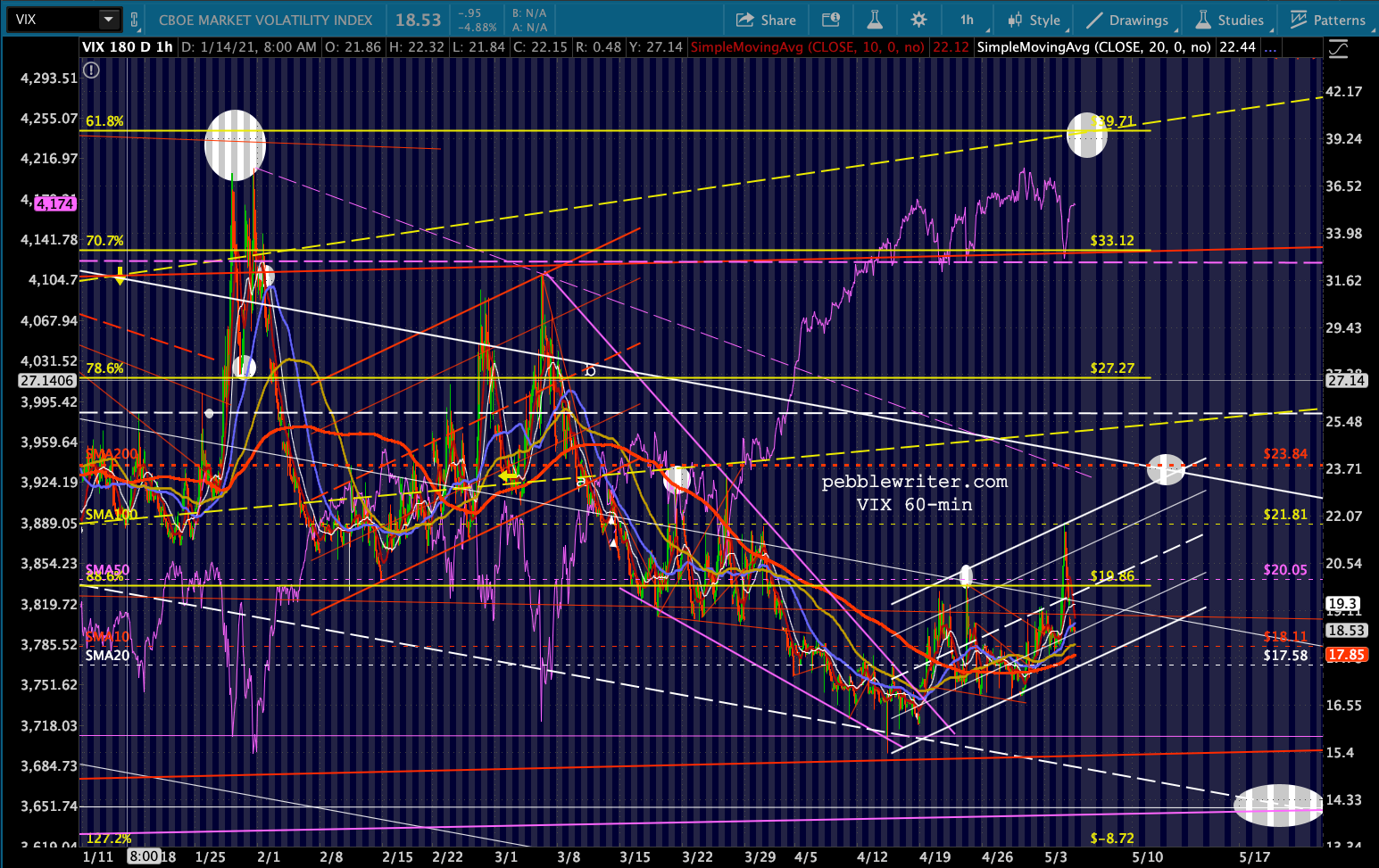

VIX continues to have potential up to its SMA200 at 23.84, while the futures have completed, broken out of, and backtested a flag pattern targeting 24.

VIX continues to have potential up to its SMA200 at 23.84, while the futures have completed, broken out of, and backtested a flag pattern targeting 24.

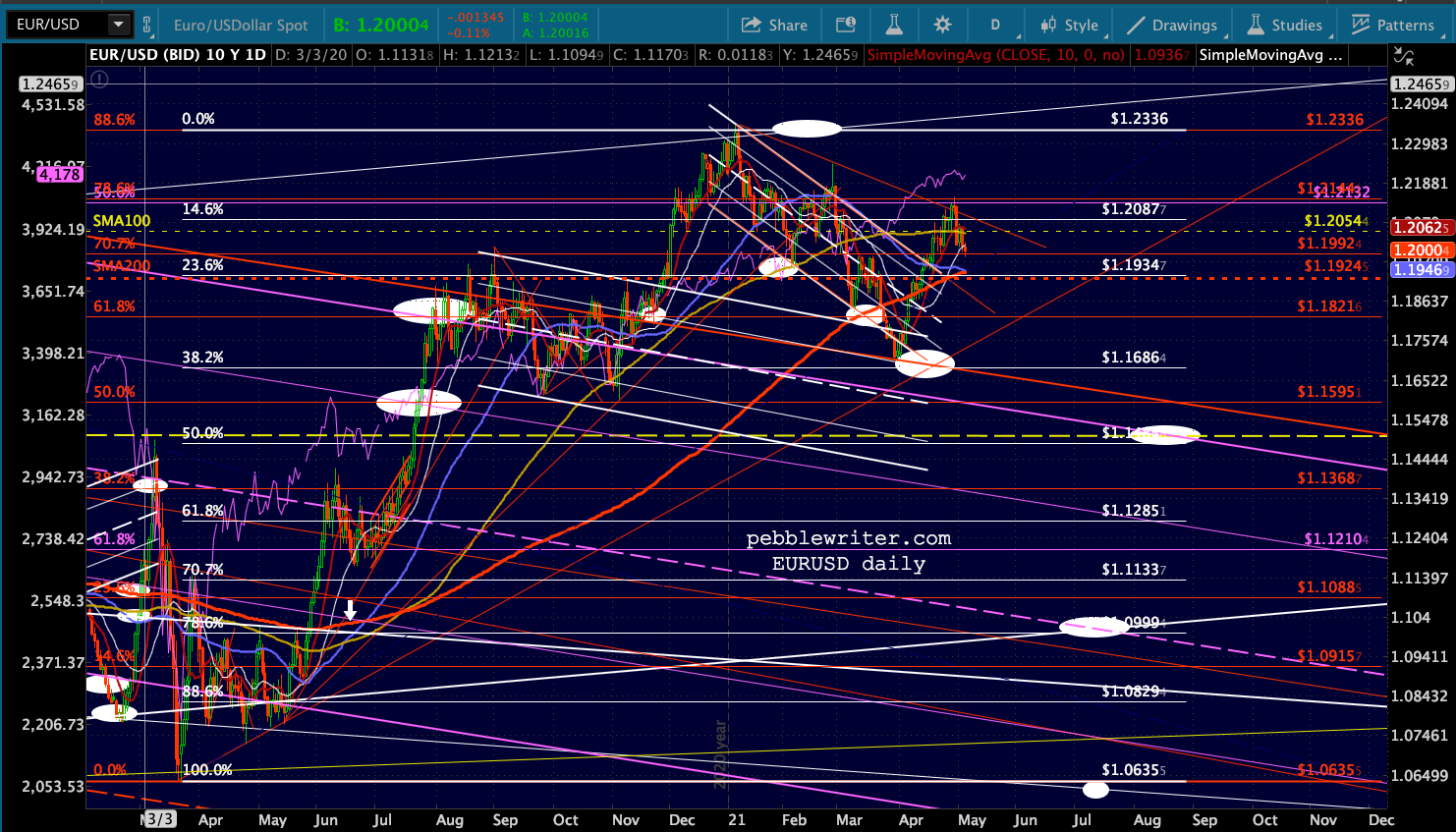

USDJPY is still on the bubble – threatening a breakout of the falling purple channel.

USDJPY is still on the bubble – threatening a breakout of the falling purple channel.

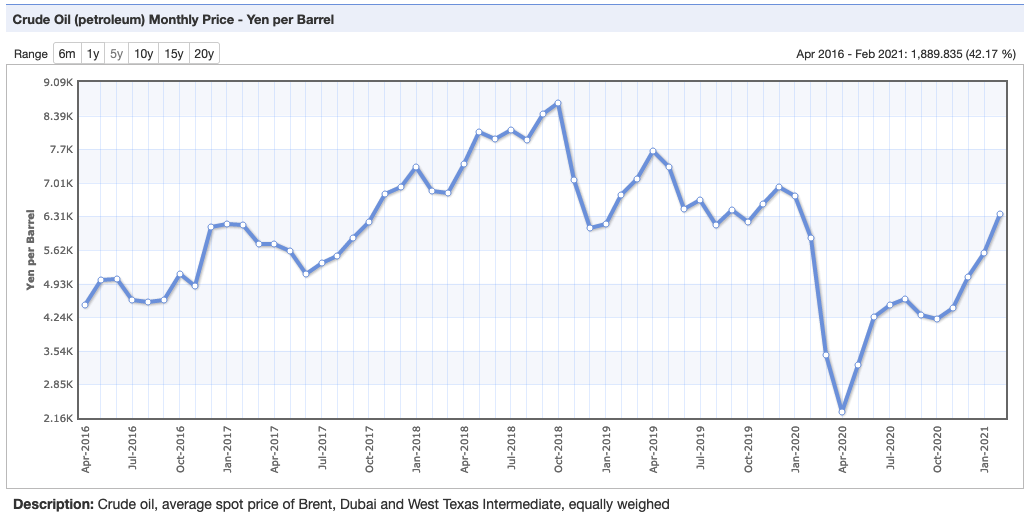

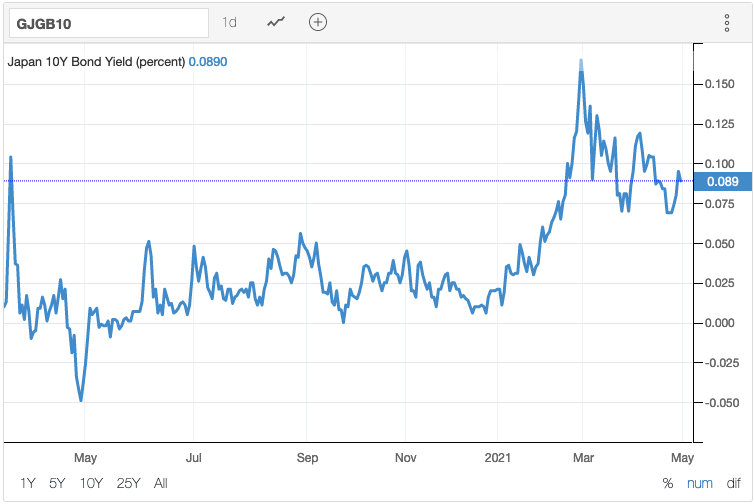

A breakout (devaluing the yen) would mean even more expensive oil and gas for Japan…

A breakout (devaluing the yen) would mean even more expensive oil and gas for Japan… … which has seen interest rates under upward pressure ever since oil in yen bottomed out in Apr 2020.

… which has seen interest rates under upward pressure ever since oil in yen bottomed out in Apr 2020.

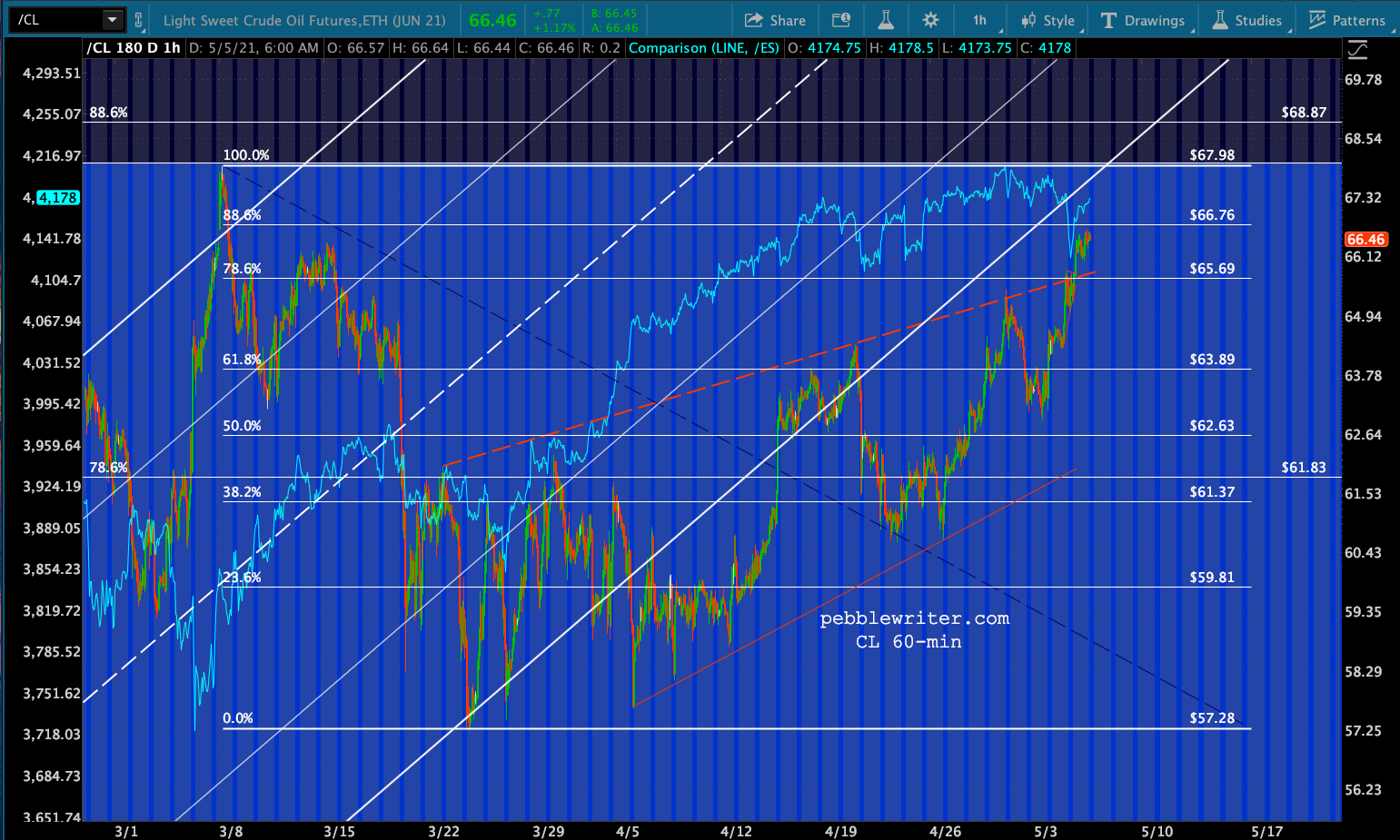

Speaking of rising oil and gas prices, CL sent a bullish signal by breaking above the red TL (though not quite reaching the .886 at 66.76)…

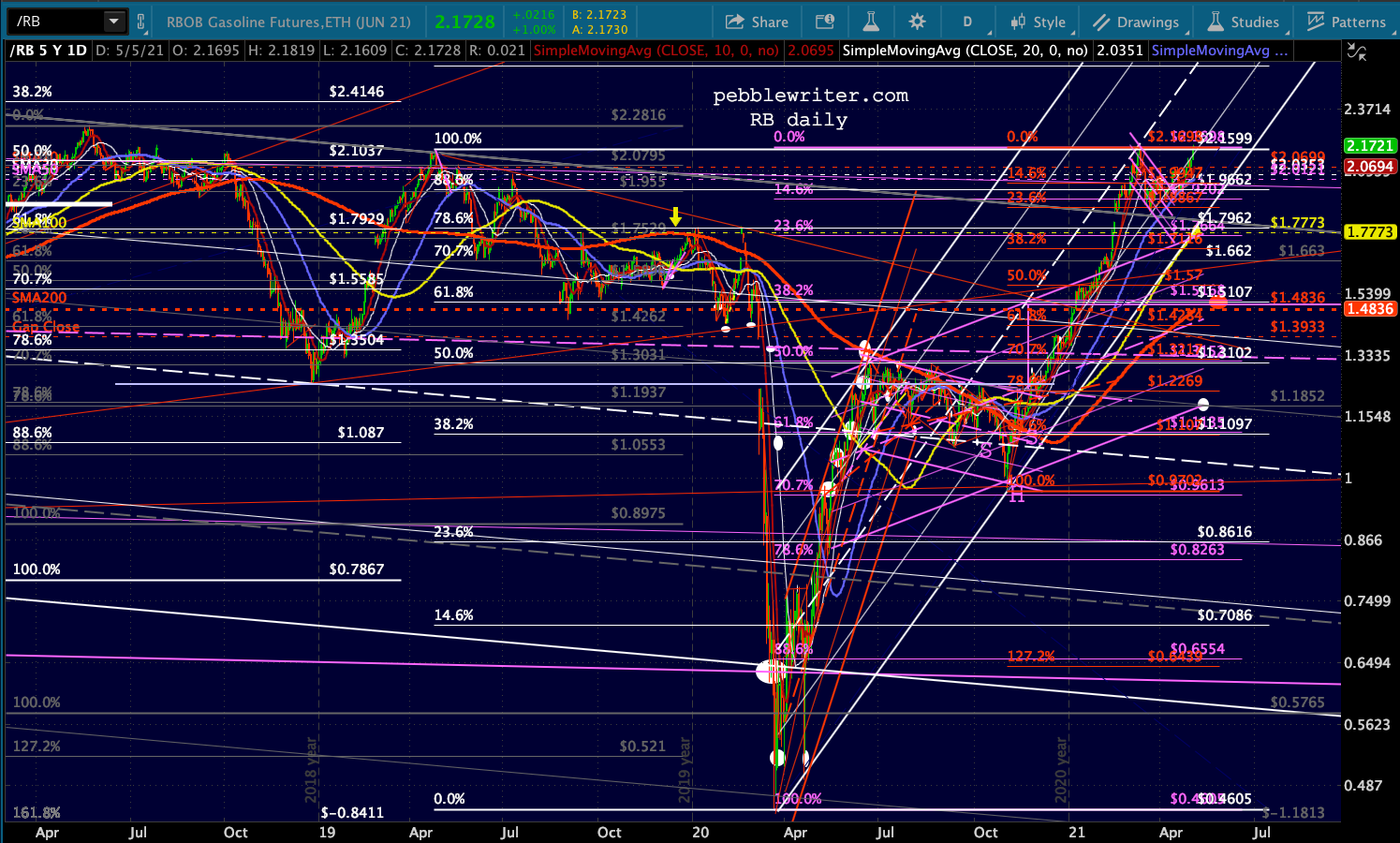

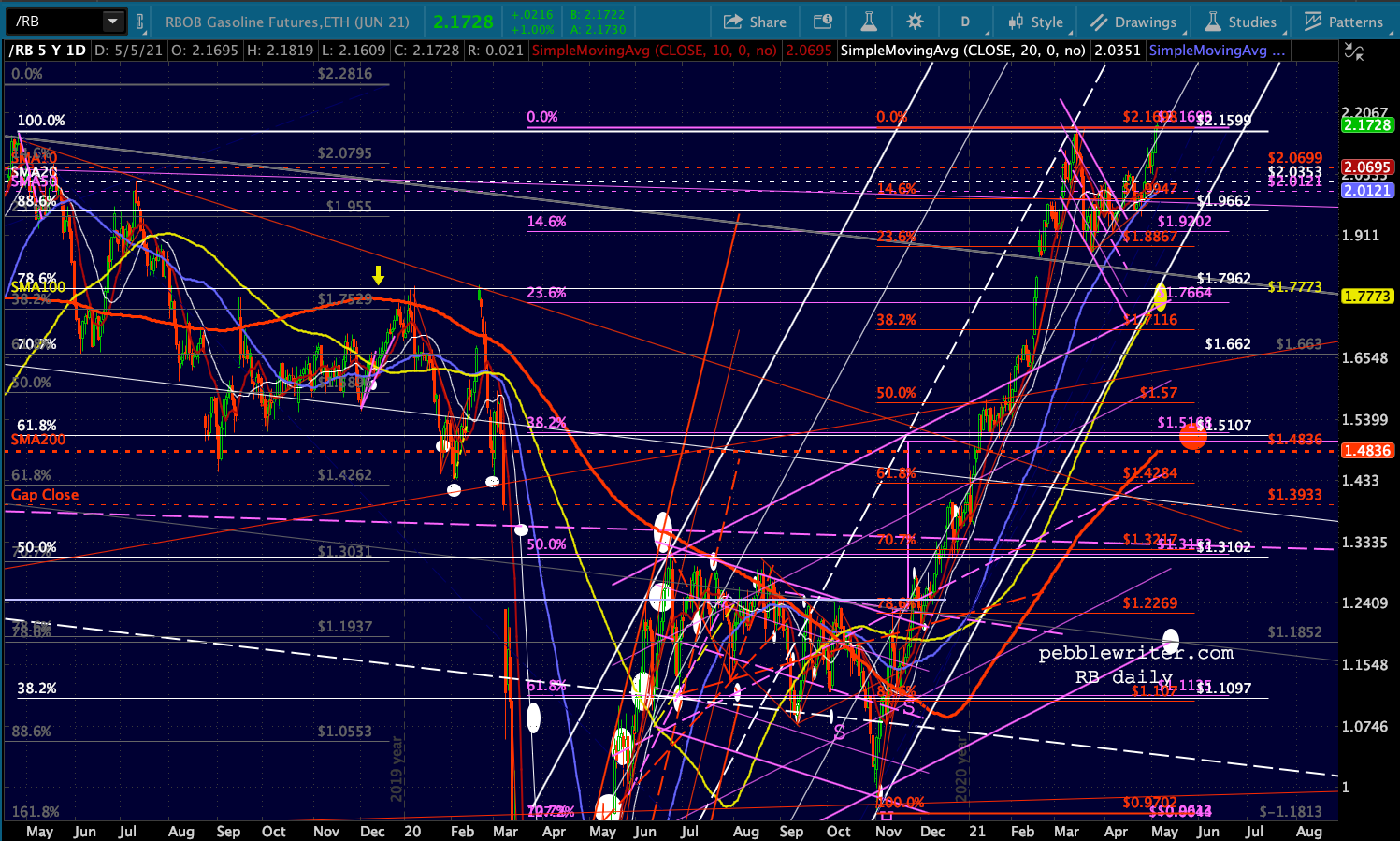

Speaking of rising oil and gas prices, CL sent a bullish signal by breaking above the red TL (though not quite reaching the .886 at 66.76)… …and RB topped its 4/25/19 highs again. Recall that it did this back on 3/15/21, promptly shedding 13.8% before climbing back to these levels.

…and RB topped its 4/25/19 highs again. Recall that it did this back on 3/15/21, promptly shedding 13.8% before climbing back to these levels.

The EIA reported weekly prices on Monday at 2.79 – the highest since October 2018. Remember, we get EIA inventory data at 10:30 this morning.

The EIA reported weekly prices on Monday at 2.79 – the highest since October 2018. Remember, we get EIA inventory data at 10:30 this morning.

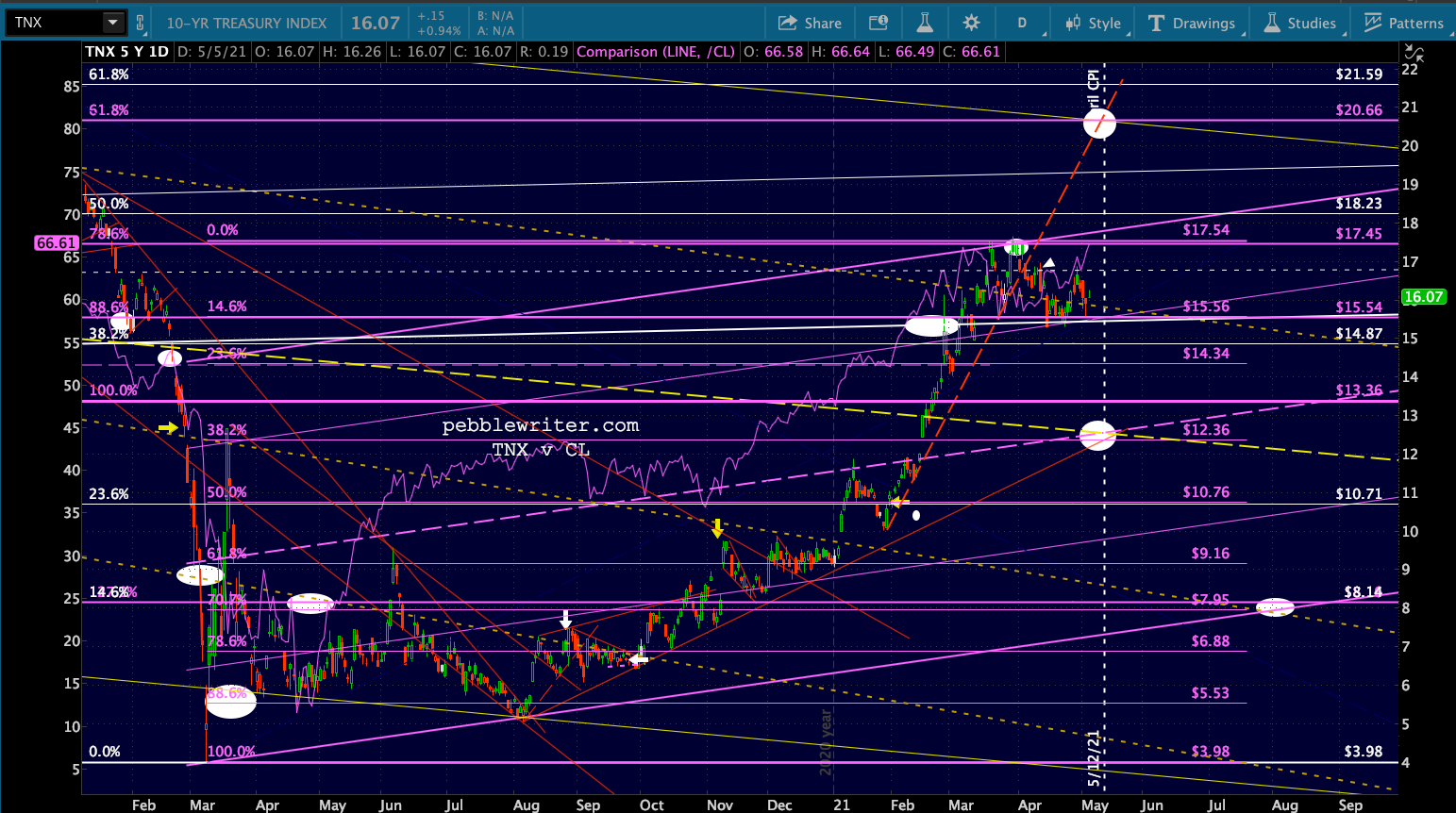

Bonds continue to live in a bubble, seemingly unconcerned with, well, anything. Though the May 12 CPI report for April will apparently matter quite a bit.