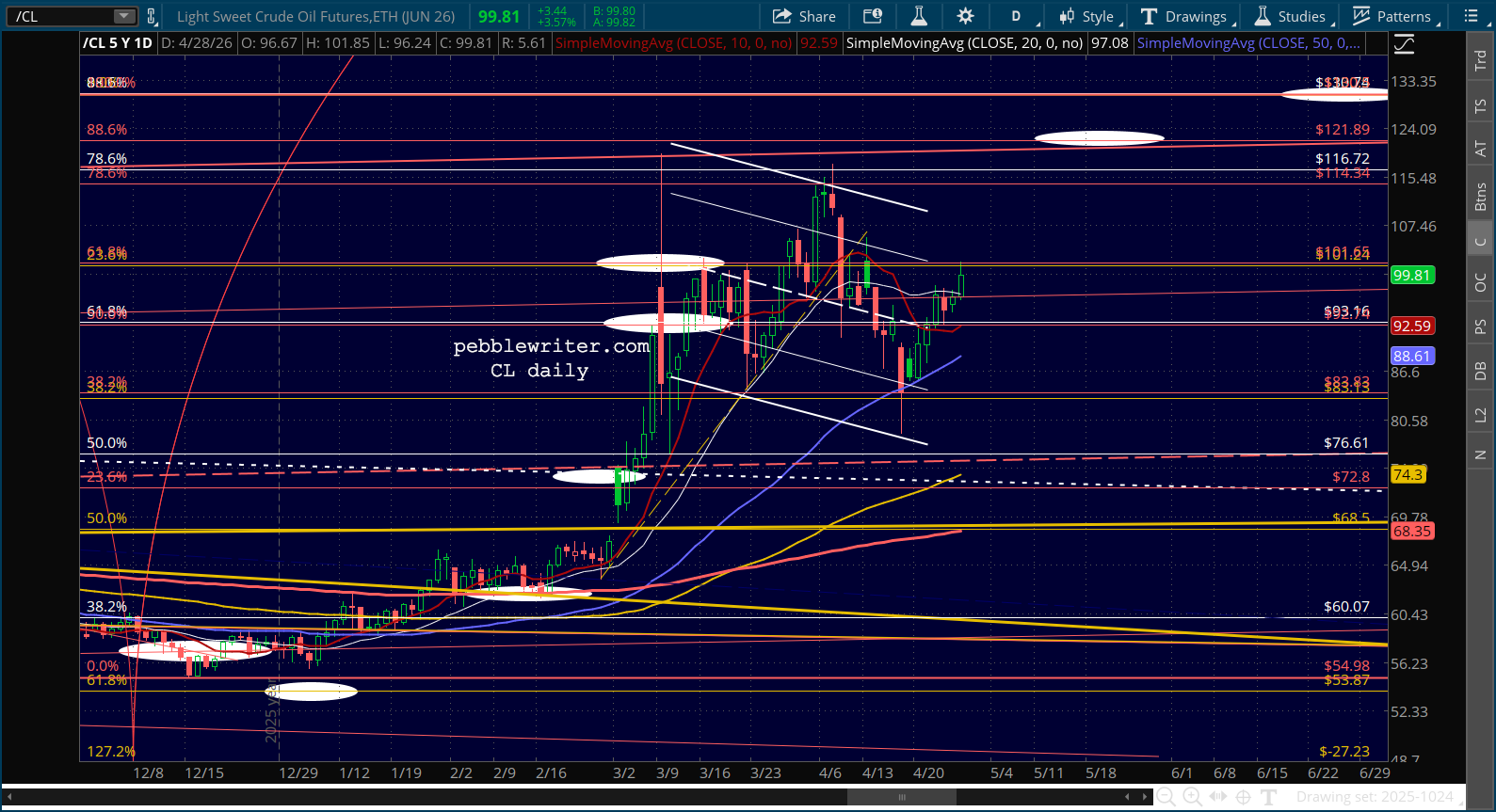

Futures are moderately lower as WTI futures bump up against 100/bbl again. Although WTI and Brent are the two most quotes price points, it’s important to recognize that they are futures and represent prices a couple of months out when it is presumed that the Iran War will be over and normal oil operations have resumed. Note the “JUN 26” in the description in the chart below.

This is in stark contrast to the real prices that countries which are running out of oil right now are experiencing. EA reports that physical oil prices right now are substantially higher.

The physical market paints a starkly different picture. Dated Brent has surged well above $140/bbl. Dubai, the key Asian benchmark, spiked to $260/bbl before contract changes reduced the number of deliverable cargoes. West African and North Sea cargo prices are trading at substantial premiums to benchmarks. And once freight costs are factored in, crude is landing in Asia at approximately $170/bbl.

Will physical prices be back below $100 in the near future? Not according to some experts. Paul Sankey of Sankey Research says that the situation is guaranteed to get worse as pre-war oil shipments via tankers from the Persian Gulf have only now reached their destinations. With the Strait of Hormuz closed off for the past six weeks, the lack of new supplies can no longer be ignored.

We can be sure that the next two months is going to be an ongoing, absolute disaster even if you open the straits tomorrow because it’s just locked in by virtue of tankers, and the tankers are all in the wrong places. Over the coming months, this is going to unfortunately deteriorate badly. We’re locked into that.

JPMorgan estimates that OECD inventories will be depleted sometime between May 9-30, “at which point price increases become exponential rather than linear.”

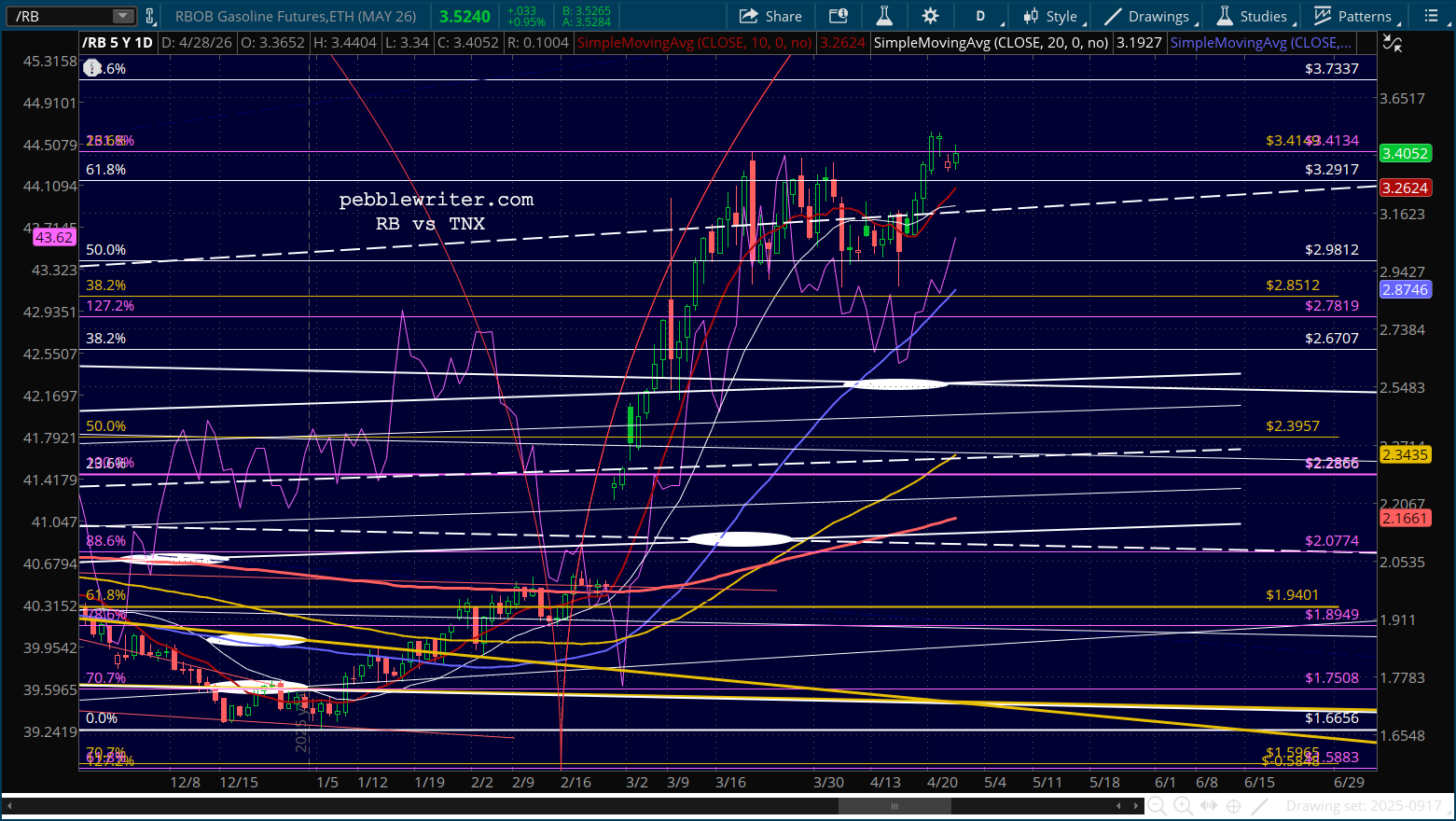

RB is bumping up against its recent highs again.