We’ve pretty much beat the inflation horse to death on these pages over the past six months. Bottom line, It’s too high and potentially out of control.

So far, however, the Fed’s been able to hoodwink investors and algos and commandeer the bond market. Aside from making things much more difficult for the little guy – who they claim to care about – there have been few negative repercussions.

But people are starting to talk. At first it was just fringe strategists like yours truly. Lately, it’s financial pundits, important bankers and hedge fund managers. Has the trance been broken? And, if so, will the market care? Today, we’ll finally find out how clever the Fed can be.

Two years ago, before any of us had ever heard of COVID-19, our charts already called for some pretty dramatic outcomes. We were pretty sure the 10Y, having reversed right on target at 3.25% in October 2018, was headed for at least 1.55%…

Two years ago, before any of us had ever heard of COVID-19, our charts already called for some pretty dramatic outcomes. We were pretty sure the 10Y, having reversed right on target at 3.25% in October 2018, was headed for at least 1.55%…

…a target that was adjusted to 0.15% — 1.33% on January 13 at which point Wuhan City had reported only 40 suspected cases and one death. On March 8, it reached 0.398% – well ahead of schedule thanks to COVID-19.

…a target that was adjusted to 0.15% — 1.33% on January 13 at which point Wuhan City had reported only 40 suspected cases and one death. On March 8, it reached 0.398% – well ahead of schedule thanks to COVID-19.  Its rebound has been impressive – aided by a sharp rebound in inflation due primarily to the even more impressive recovery in oil prices.

Its rebound has been impressive – aided by a sharp rebound in inflation due primarily to the even more impressive recovery in oil prices.

Ah, oil… We became convinced in March 2018 that oil was headed for a major breakdown, noting important cycles in its peaks and troughs. At the time, our model showed WTI (then at $62) dropping below $20 in early 2023.

On Jan 3, 2020 we got more specific, pinpointing $17.12 on April 23, 2023.

On Jan 3, 2020 we got more specific, pinpointing $17.12 on April 23, 2023.

Of course, it dropped much lower and much faster than that. And, it’s recovery has been higher and faster than anyone imagined (or the fundamentals would support.)

Of course, it dropped much lower and much faster than that. And, it’s recovery has been higher and faster than anyone imagined (or the fundamentals would support.) Interest rates and oil prices are irrefragably joined at the hip. Gasoline prices are especially highly correlated with inflation…

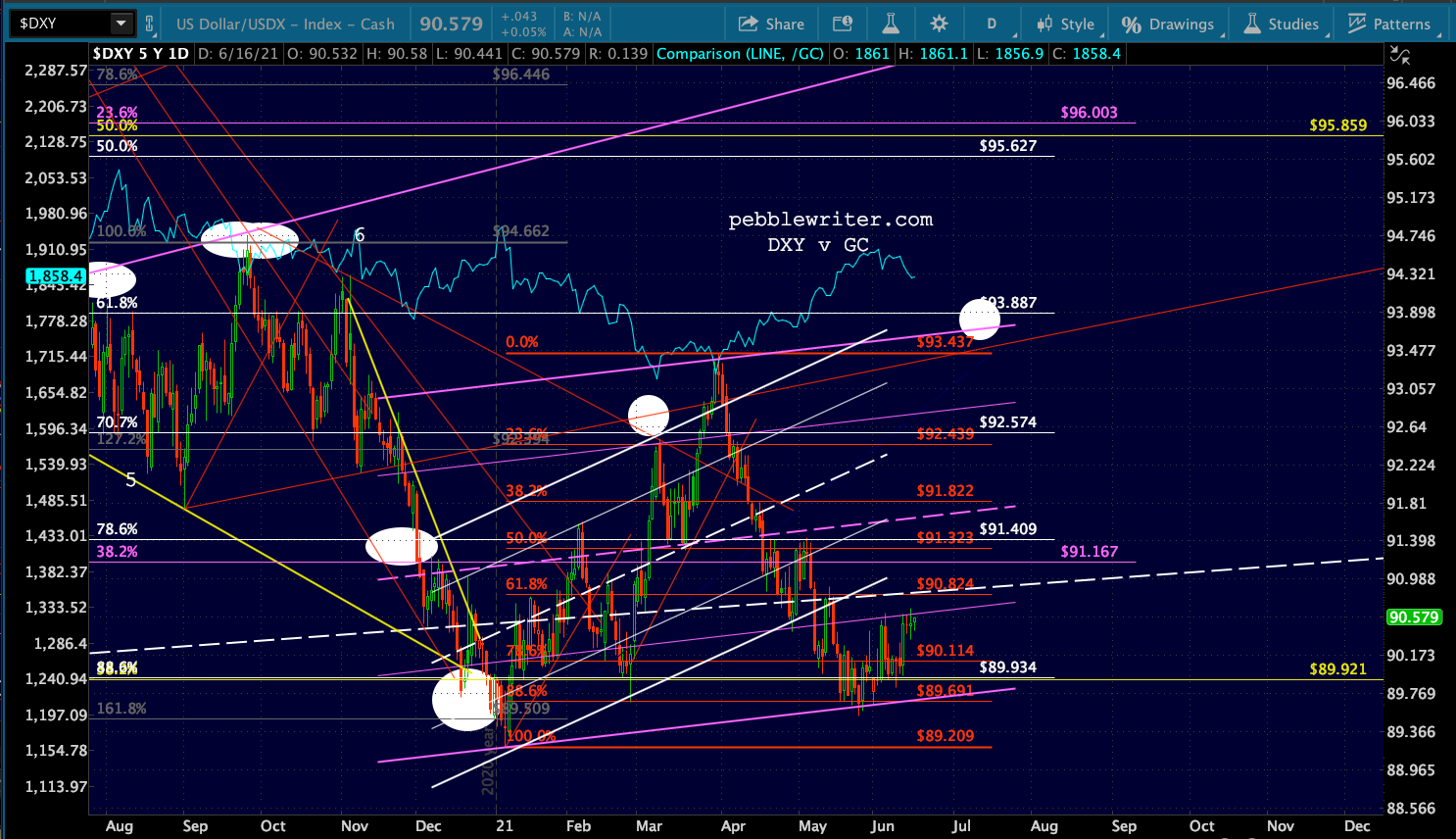

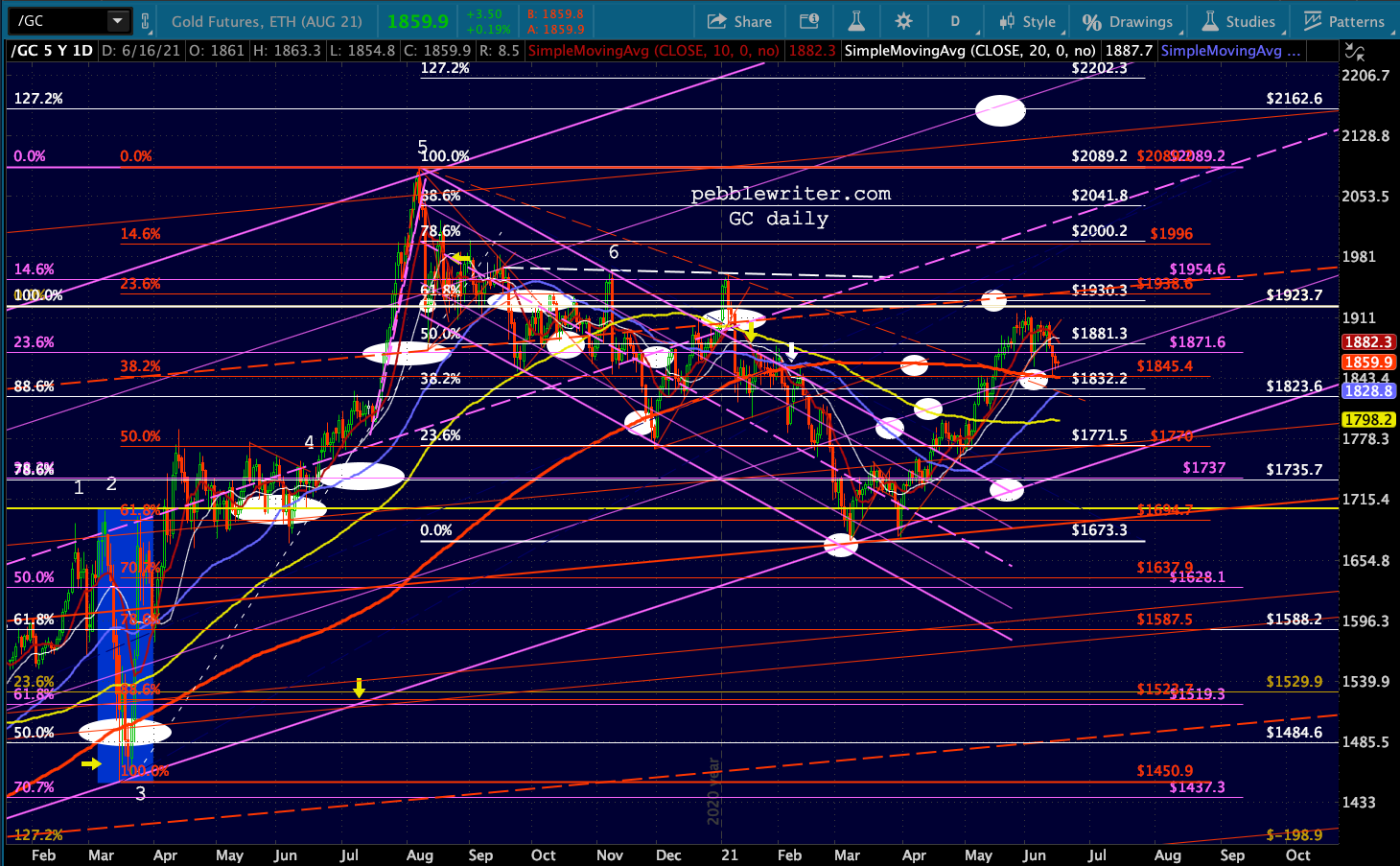

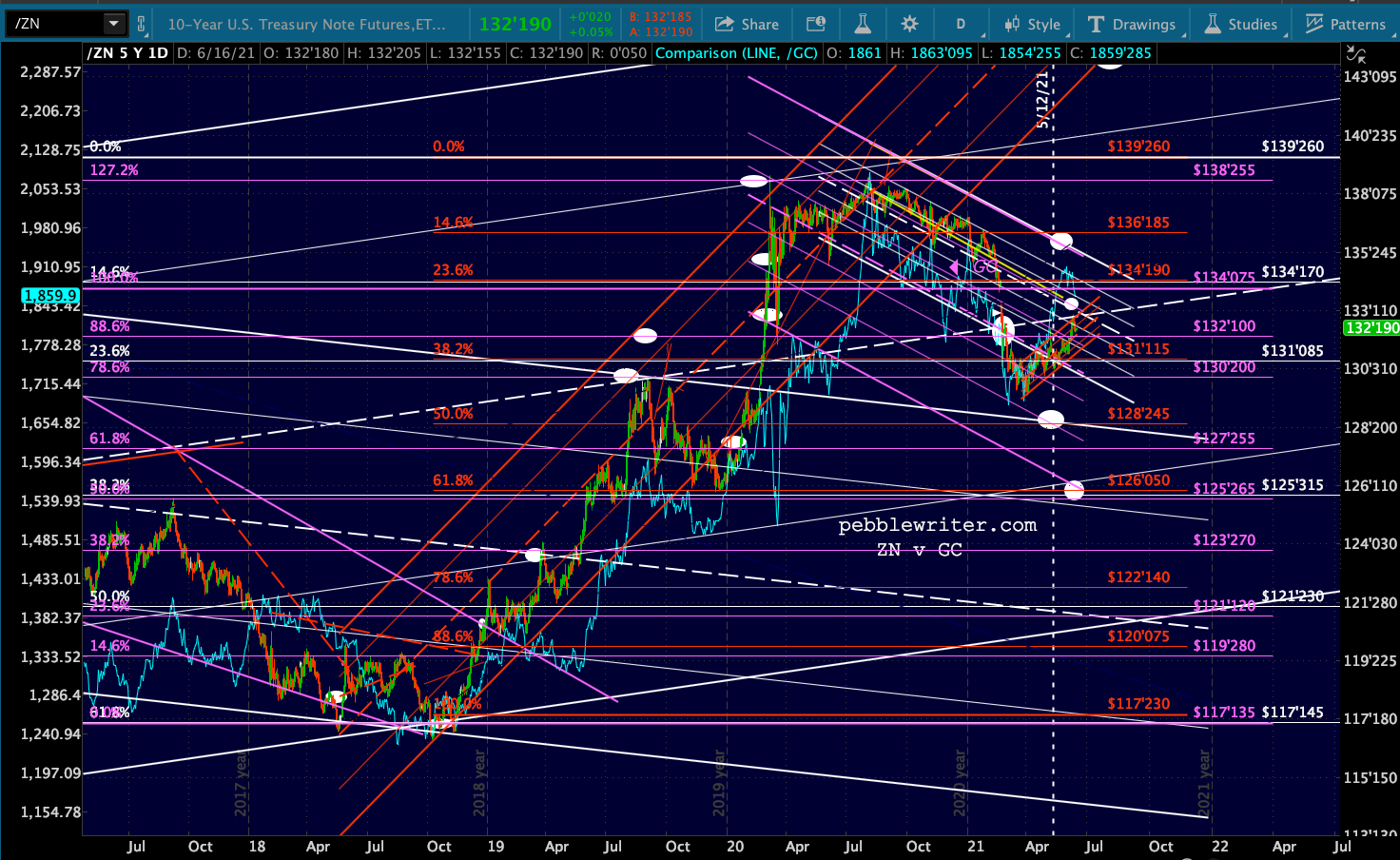

Interest rates and oil prices are irrefragably joined at the hip. Gasoline prices are especially highly correlated with inflation…  …which has traditionally been highly correlated with interest rates. But, that all changed in the last couple of months when, thanks to the Fed’s ability to control interest rates, the bond market stopped caring about inflation.

…which has traditionally been highly correlated with interest rates. But, that all changed in the last couple of months when, thanks to the Fed’s ability to control interest rates, the bond market stopped caring about inflation.

The stock market was elated as short rates flatlined while the 10Y marched higher…

The stock market was elated as short rates flatlined while the 10Y marched higher…

…leading to the first time in 20 years that a rapidly rising 2s10s didn’t lead to a market crash.

…leading to the first time in 20 years that a rapidly rising 2s10s didn’t lead to a market crash. The Fed has pulled off a pretty masterful reinflation of the everything bubble. Are they clever enough to avoid the inevitable pop?

The Fed has pulled off a pretty masterful reinflation of the everything bubble. Are they clever enough to avoid the inevitable pop?

continued for members…

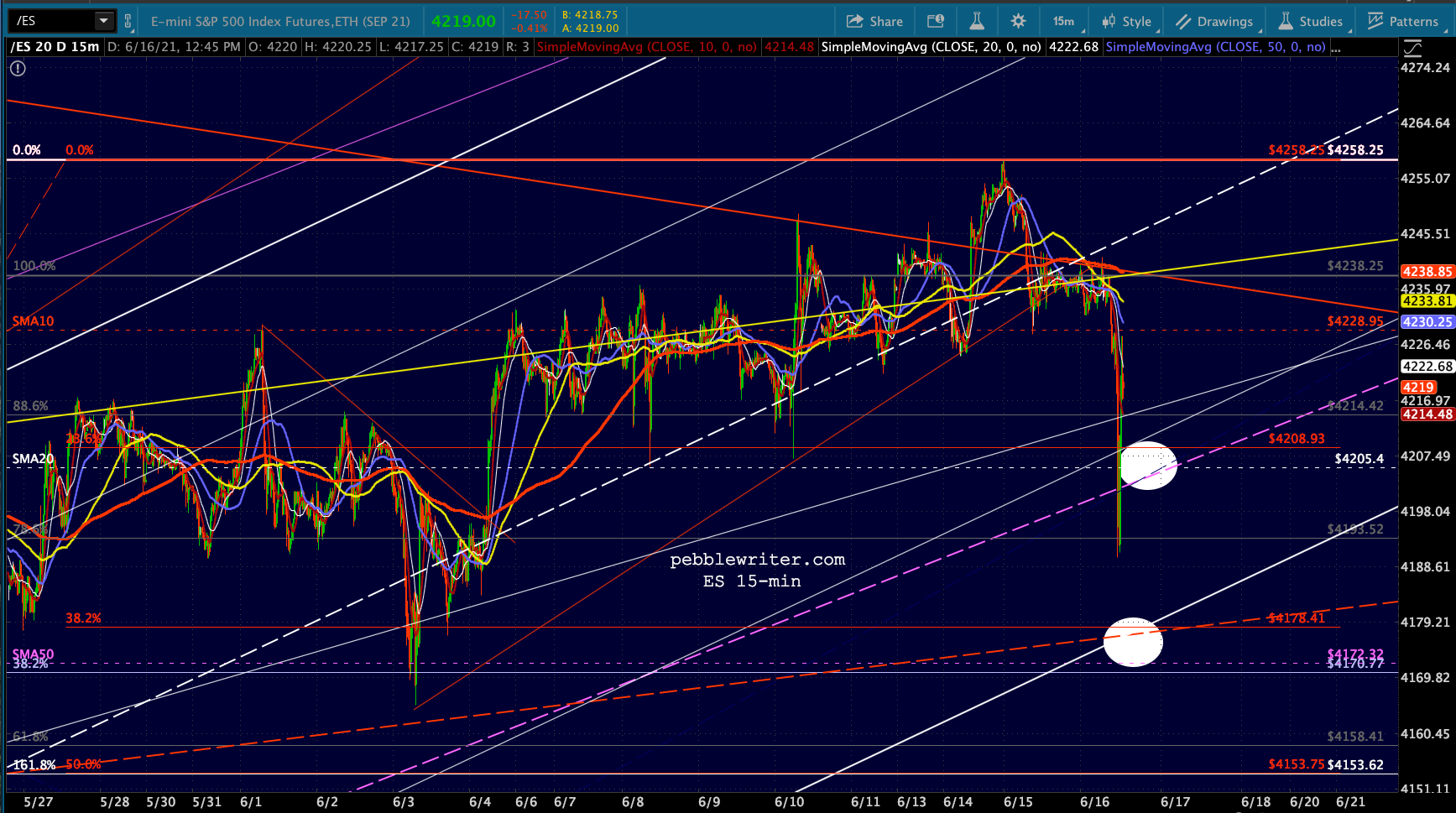

The question isn’t whether stocks will be propped out, it’s whether they can. The Fed would obviously like to quell the expectations, the criticism and, possibly the actual implications of higher inflation. Consensus is that they could do this by tapering. But, tapering would kill the equity rally.

So, the trick is to say/do just enough to slow inflation without saying/doing so much that the rally is killed. From our standpoint, the trick is to figure out what that pain threshold might be from the Fed’s perspective (measured in SPX points, of course.)

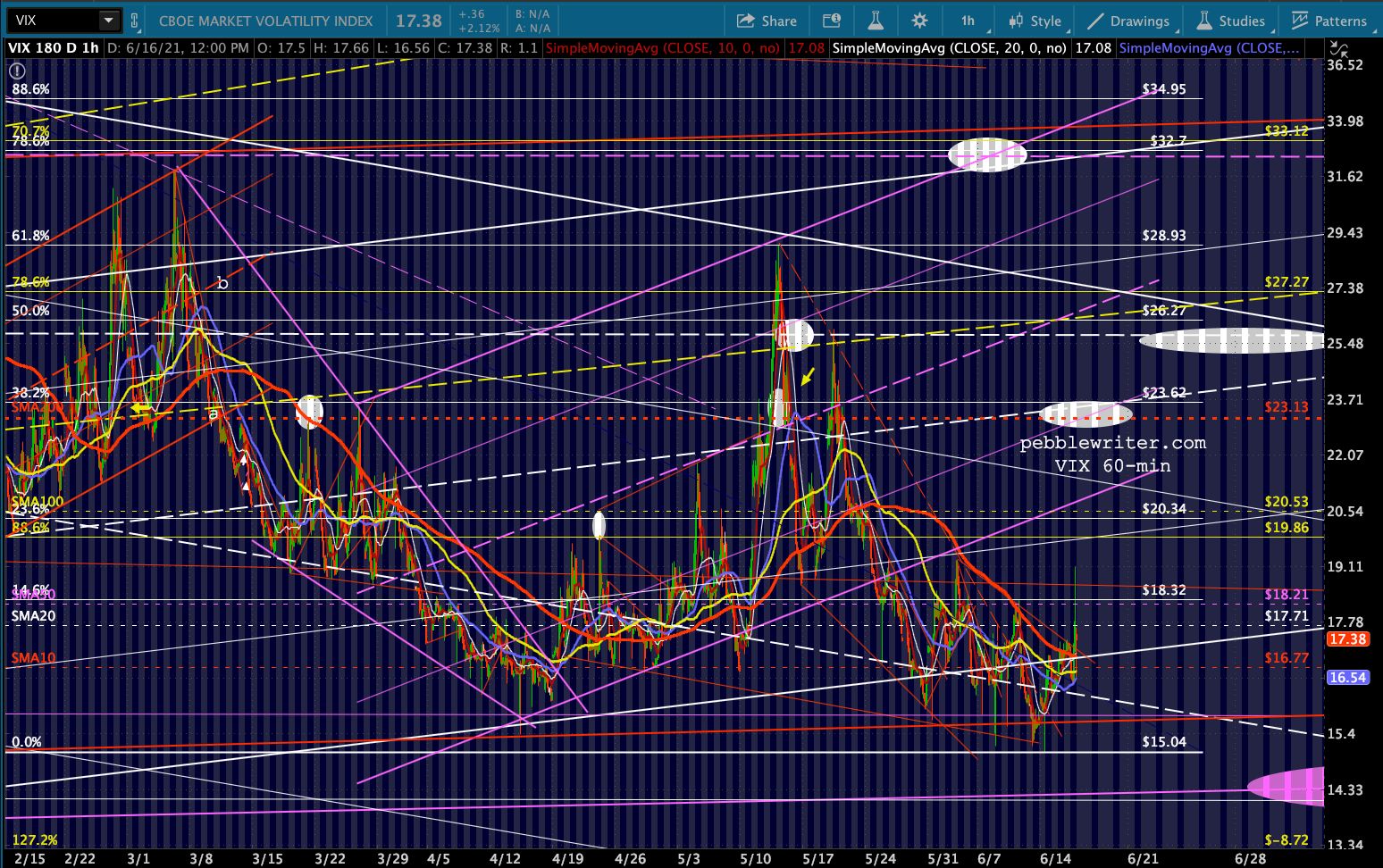

VIX remains in an excellent position to move lower and is currently using the nearby SMA10 to signal algos. If the market doesn’t like what Jay Powell says at 2:30, there is plenty of overhead resistance — all those moving averages (including the SMA200 which is conveniently near the top of the falling channel from Feb 2020) and that falling channel itself.

VIX remains in an excellent position to move lower and is currently using the nearby SMA10 to signal algos. If the market doesn’t like what Jay Powell says at 2:30, there is plenty of overhead resistance — all those moving averages (including the SMA200 which is conveniently near the top of the falling channel from Feb 2020) and that falling channel itself.

USDJPY also remains ready to rally to whatever extent it takes to protect stocks. It has already broken out of the falling purple channel. If it doesn’t like Powell’s comments, it has very good support at the white .618 at 105.78. But, all it has to do to help stop an equity correction is top 110.96 – with plenty of upside targets after that.

USDJPY also remains ready to rally to whatever extent it takes to protect stocks. It has already broken out of the falling purple channel. If it doesn’t like Powell’s comments, it has very good support at the white .618 at 105.78. But, all it has to do to help stop an equity correction is top 110.96 – with plenty of upside targets after that.

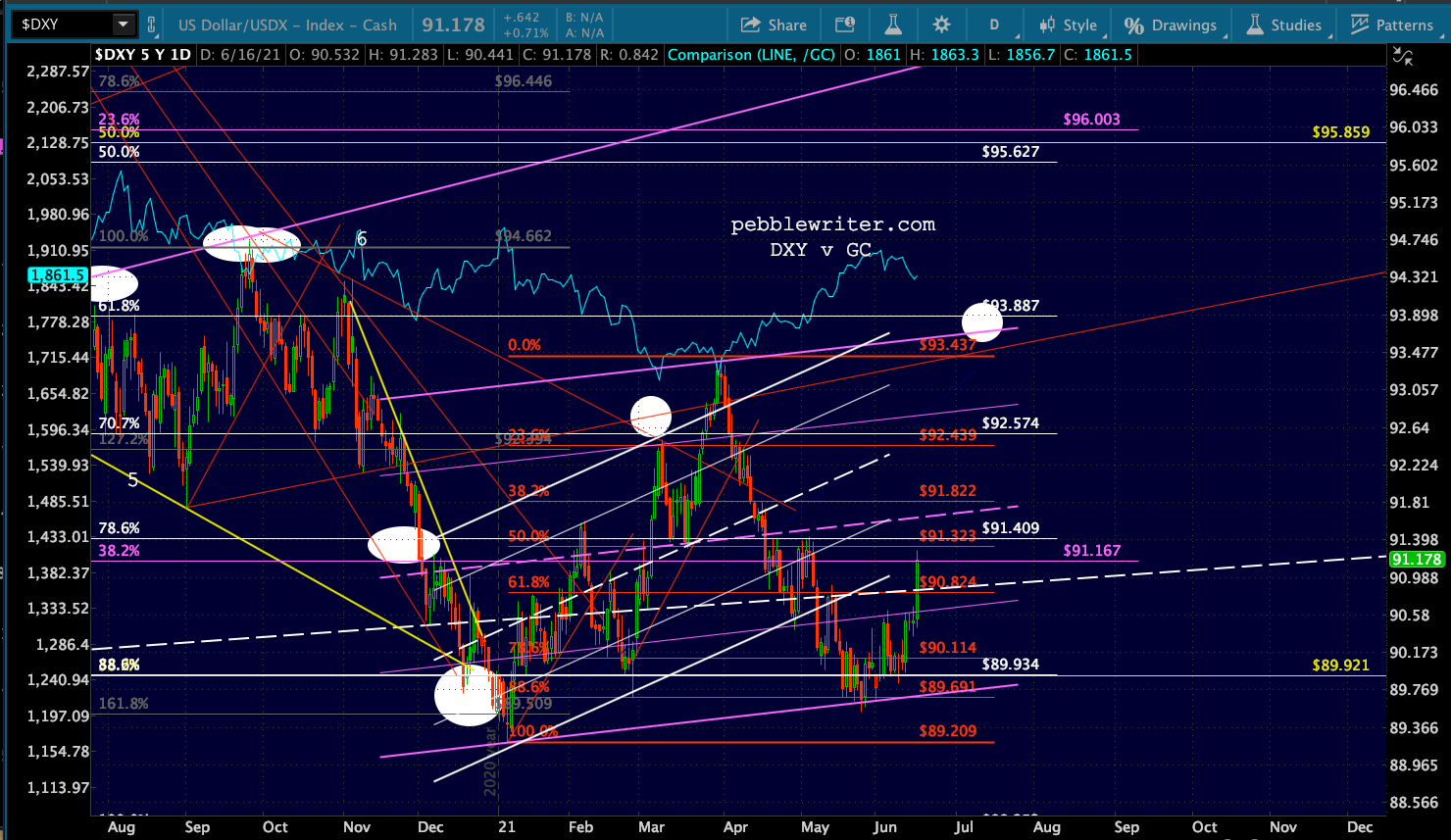

The EURUSD can largely offset the move by backtesting either the SMA200 of the rising red TL. But, it doesn’t matter all that much as DXY would have to rally quite a bit to alarm equity investors. It might, but it’s not all that likely if the Fed hints at even lower interest rates unless they also hint at tapering.

The EURUSD can largely offset the move by backtesting either the SMA200 of the rising red TL. But, it doesn’t matter all that much as DXY would have to rally quite a bit to alarm equity investors. It might, but it’s not all that likely if the Fed hints at even lower interest rates unless they also hint at tapering.

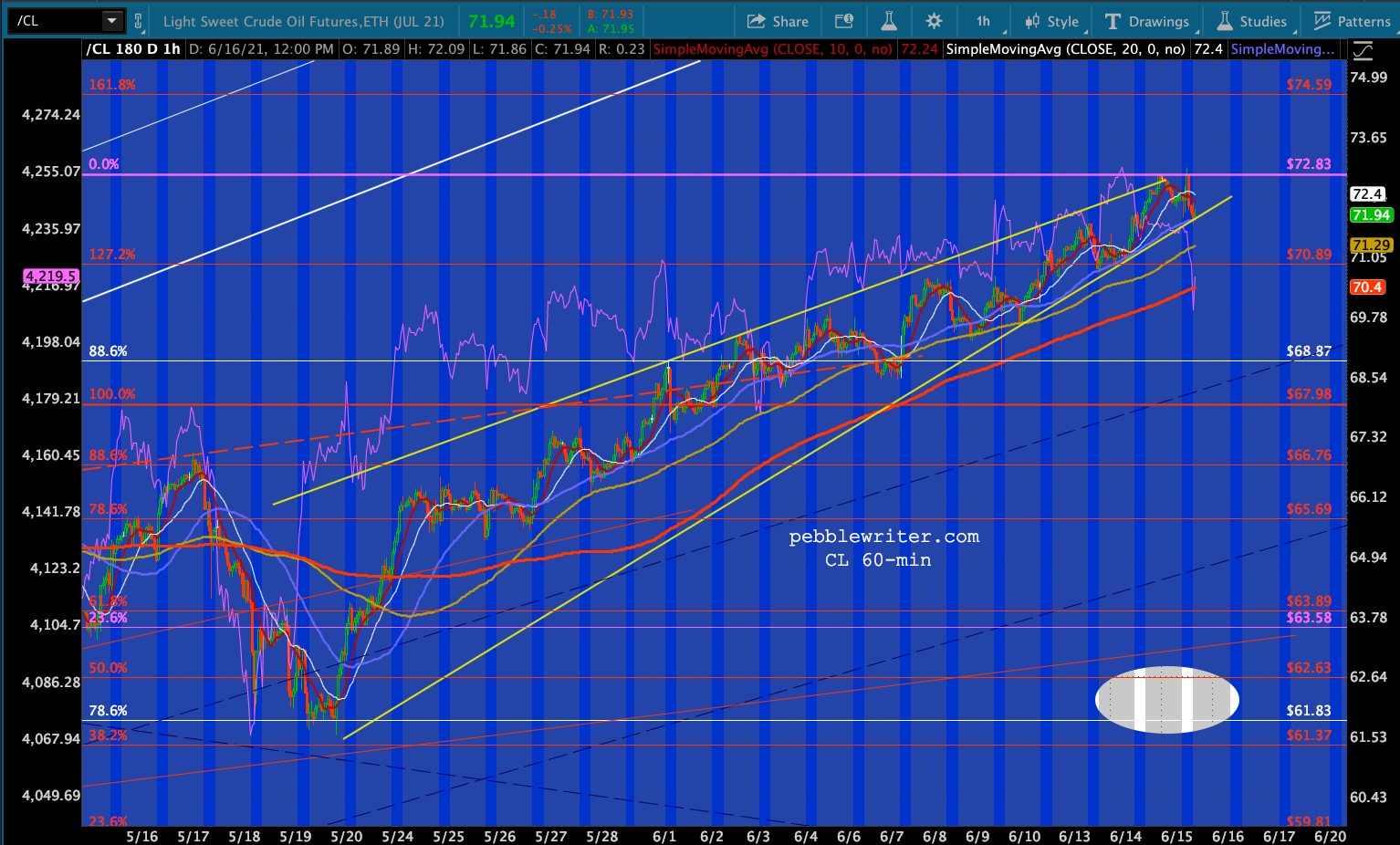

I have suggested quite strenuously in the past that the obvious solution is to knock oil/gas prices back down. They are both way overbought, running serious negative divergence, and are way out of whack with fundamentals. Energy use is nowhere close to what it was prepandemic, yet prices are near their Oct 2018 (May 2018 for RB) highs.

But, despite having done this very successfully in the past, central bankers have so far passed on this technique – perhaps due to the effect it would have on stocks, but who knows what kind of deals they might have struck with the Saudis and/or oil majors?

The bottom line is that while the oil/gas base effect will ebb somewhat over the coming months, it will still leave inflation too high for prices to remain at these levels. Having taken control of the bond market, central banks must decide how much criticism they’re willing to take and how much inflation pain they’re willing to dish out to consumers who are still hurting. The one’s who are hurting, by the way, are in for even more pain with the impending termination of supplemental unemployment and eviction moratoriums.

Unless we see significant deflation in certain sectors which needs offsetting by high oil/gas prices, oil/gas prices must come down.

The bond market is where they action should be, but it remains to be seen whether it has completely lost touch with reality.

The bond market is where they action should be, but it remains to be seen whether it has completely lost touch with reality.

I’ll post more after the press conference.

I’ll post more after the press conference.

UPDATE: 3:45 PM

Pretty much going as expected…