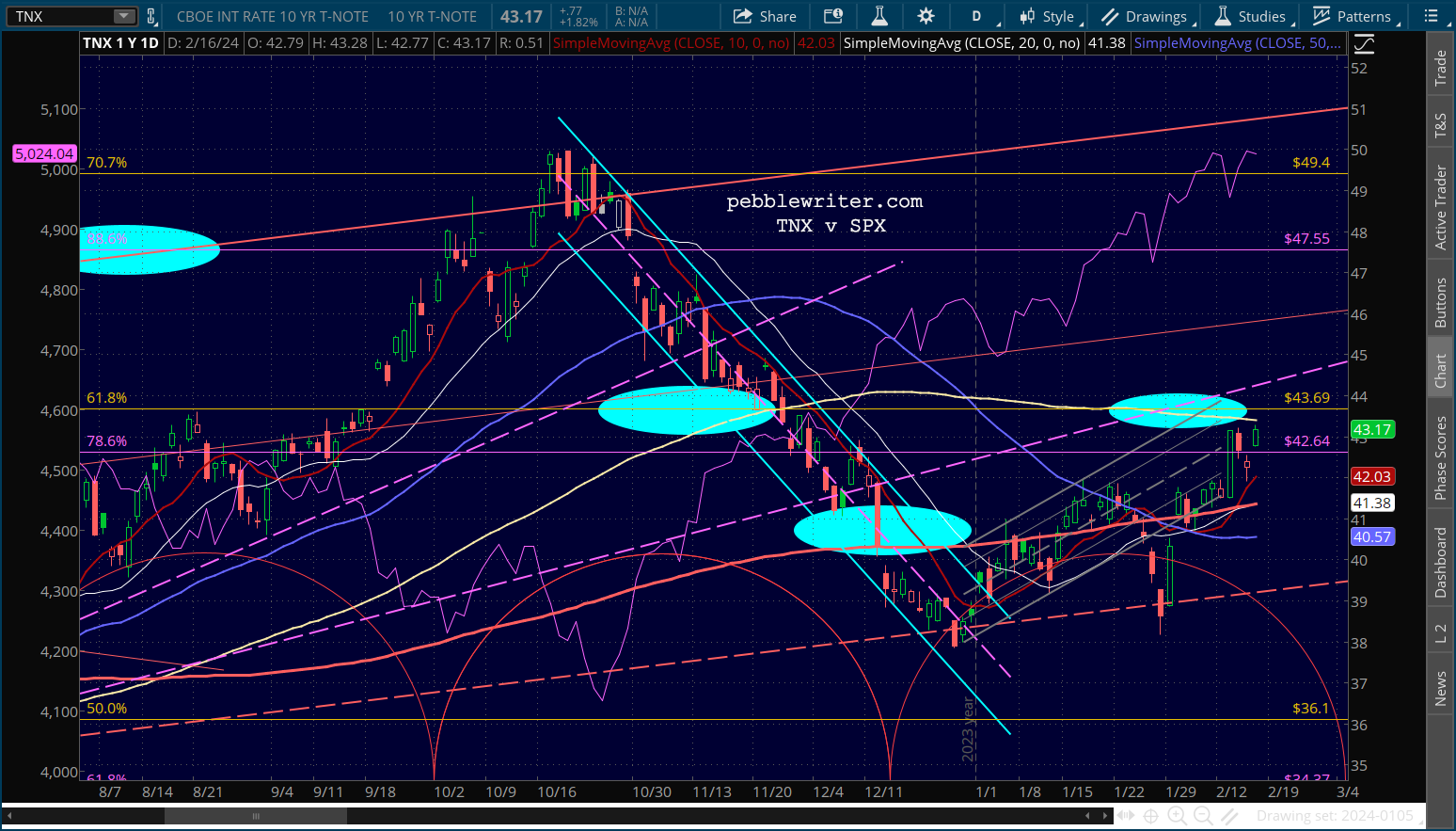

January PPI came in much hotter than expected while housing starts and permits fell far short of consensus, stoking persistent fears of stagflation. PPI came in at 0.3% MoM versus 0.1% expected. Excluding food and energy, core PPI rose 0.5% versus 0.1% expected. Stripping out trade services, the tally rose to 0.6%, its highest print since January 2023.

Monthly gains in the index for final demand for services again outpaced that for goods at +0.6% versus -0.2%. Had energy prices not continued their decline (-1.7%) the print would have been even more alarming.

Futures had been slightly higher overnight, but fell into the red after the closely followed prints.  continued for members…

continued for members…

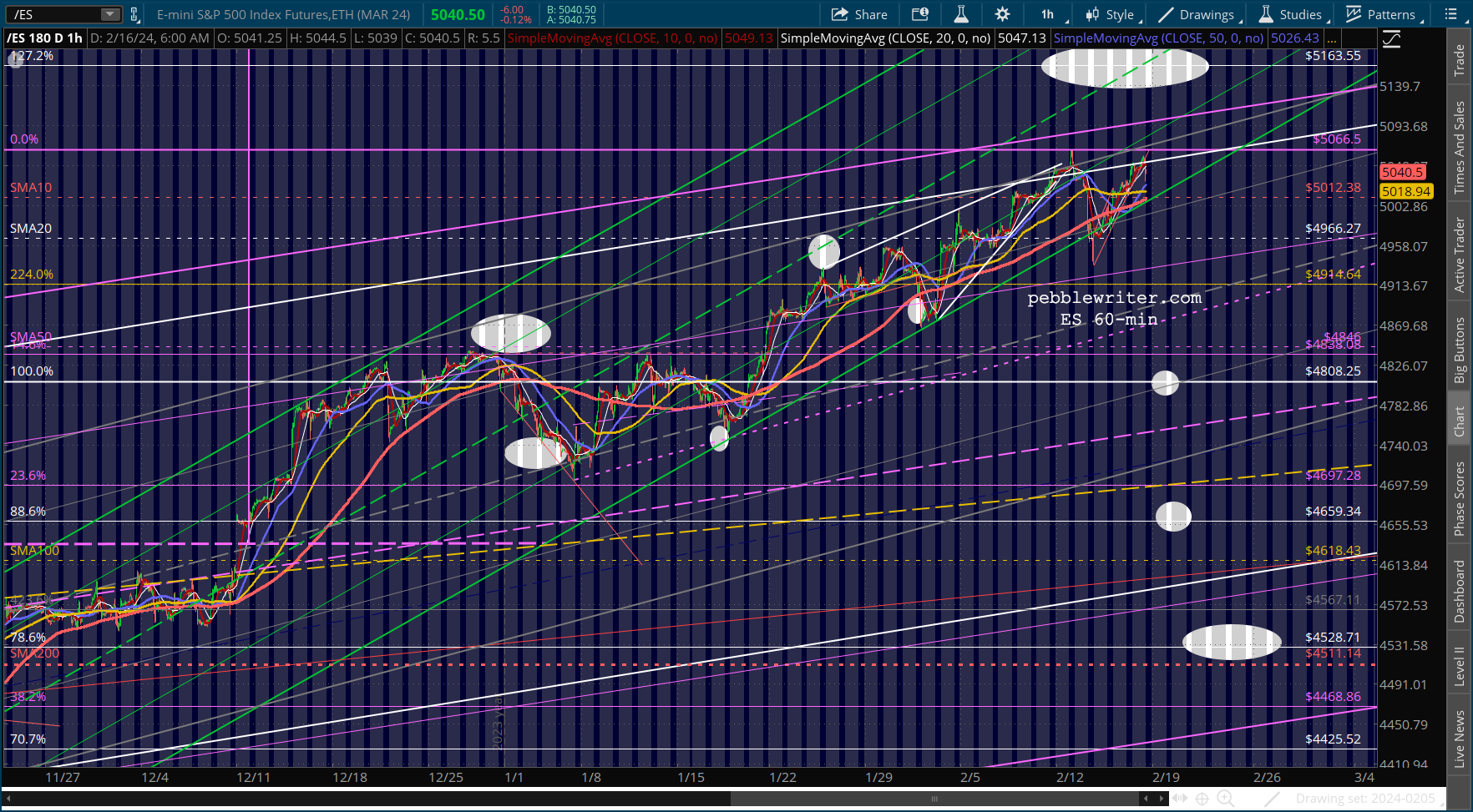

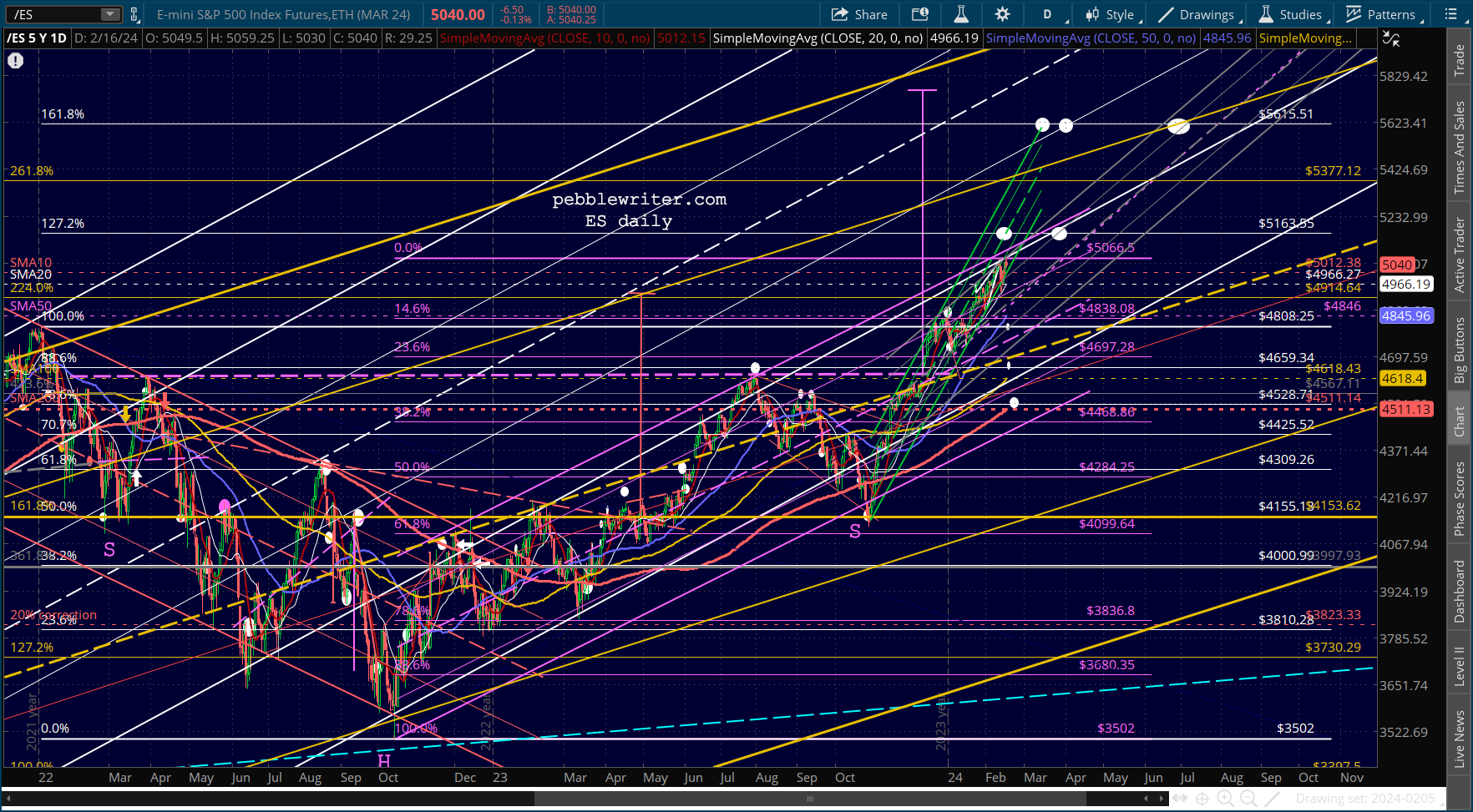

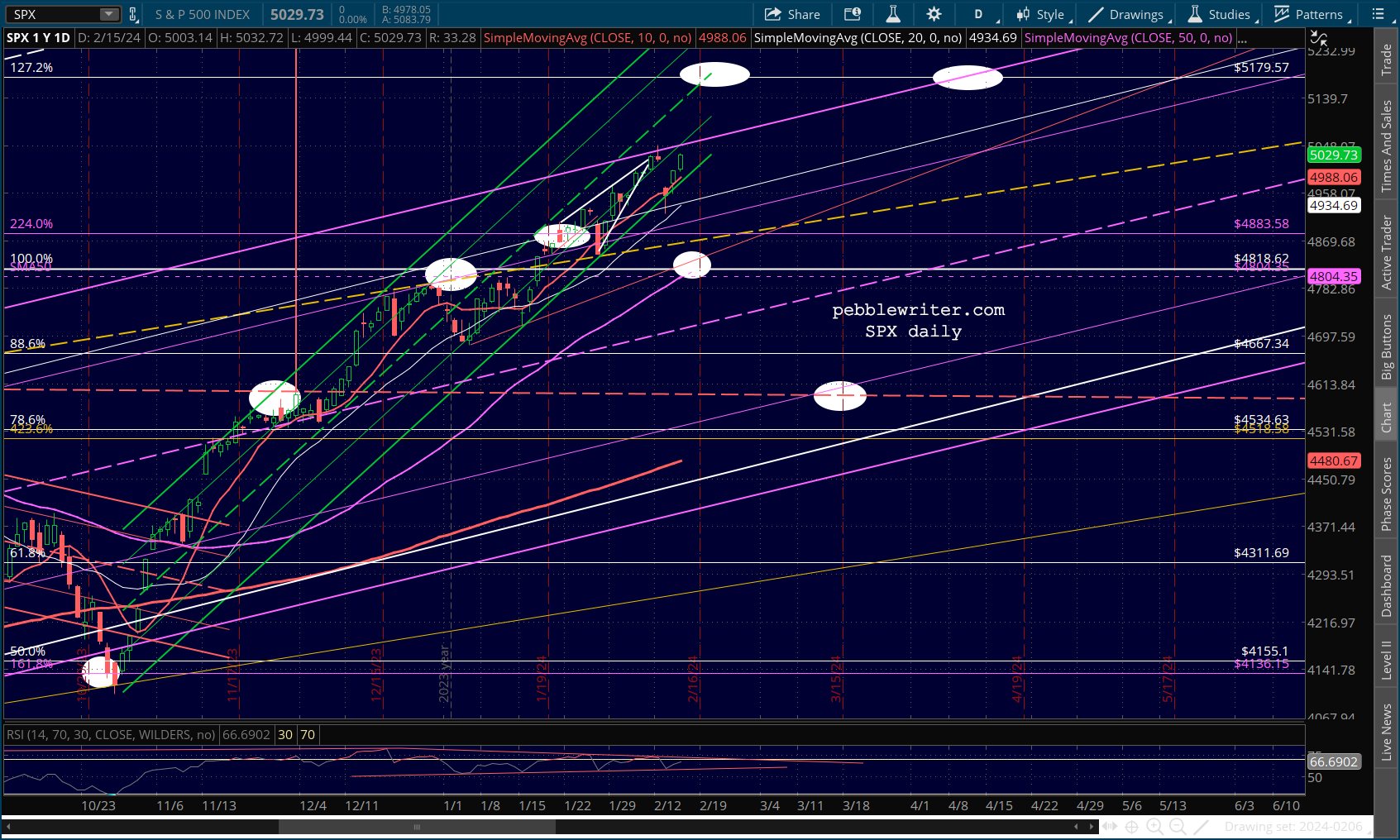

ES/SPX are safely back in the rising green channel, but are again running into the tops of the less steeply sloped purple and white channels – raising the question of timing more than anything. If the larger channel tops hold, ES/SPX will need to pull back for a couple of months. Otherwise, we would need to see a breakout here.

VIX has remained under pressure, initially being hammered to a 13 handle before being allowed to rise back to as high as 14.49. Note that all of the moving averages have essentially flatlined.

VIX has remained under pressure, initially being hammered to a 13 handle before being allowed to rise back to as high as 14.49. Note that all of the moving averages have essentially flatlined.

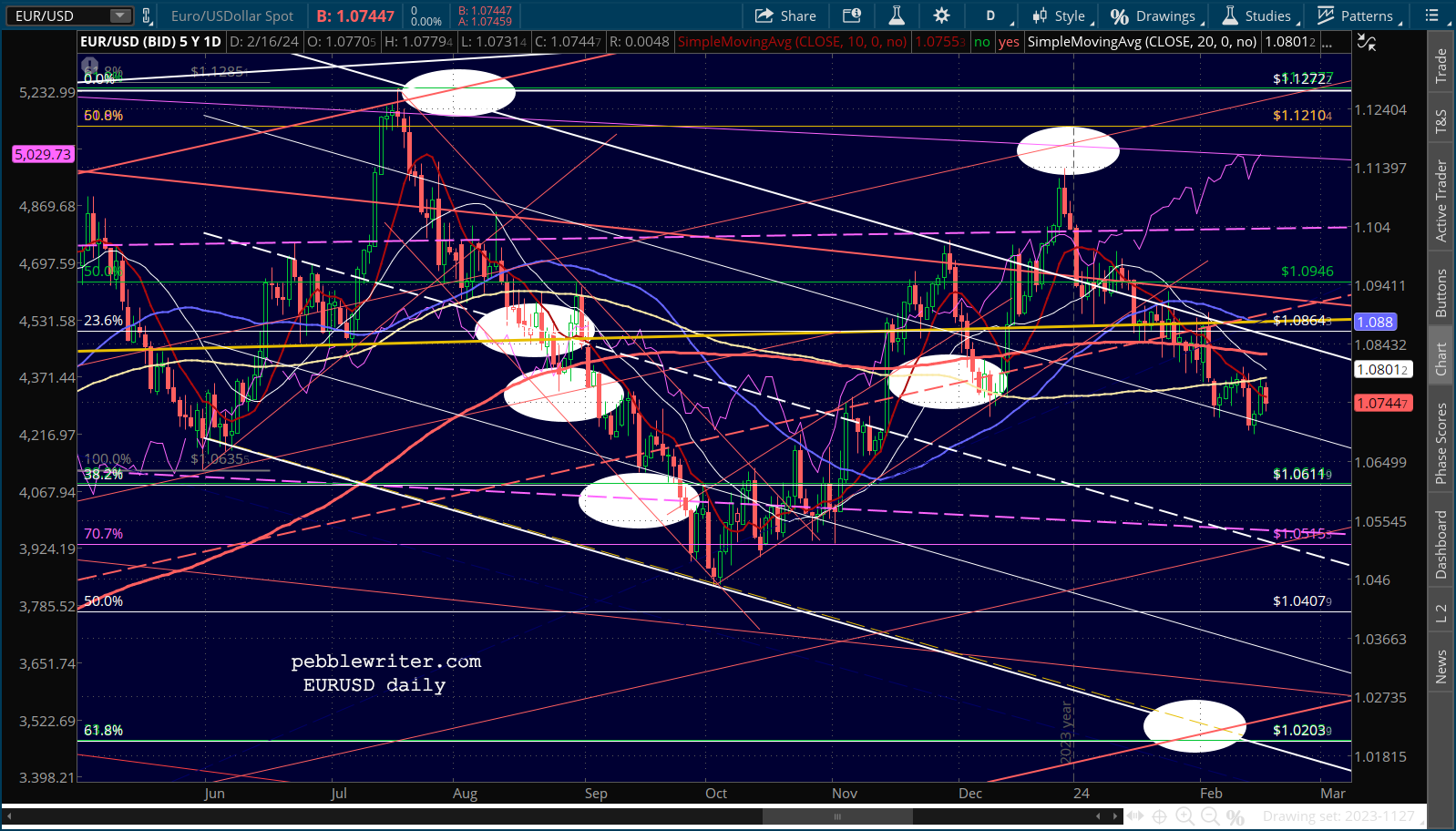

Currencies were little changed since yesterday, with EURUSD continuing to look vulnerable but not coming close to the kind of tumble seen earlier in the month.

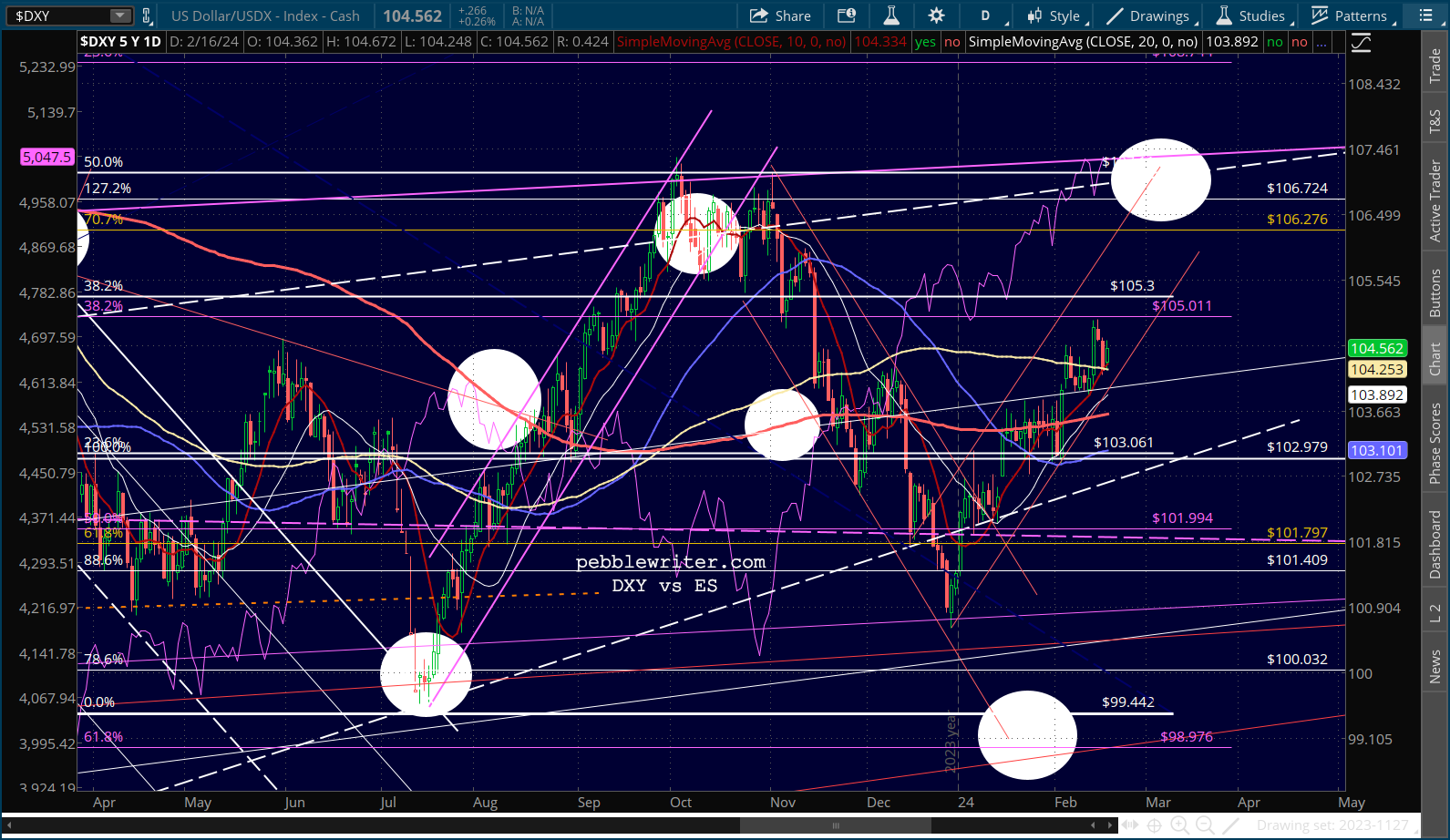

As a result, DXY’s rise remains muted.

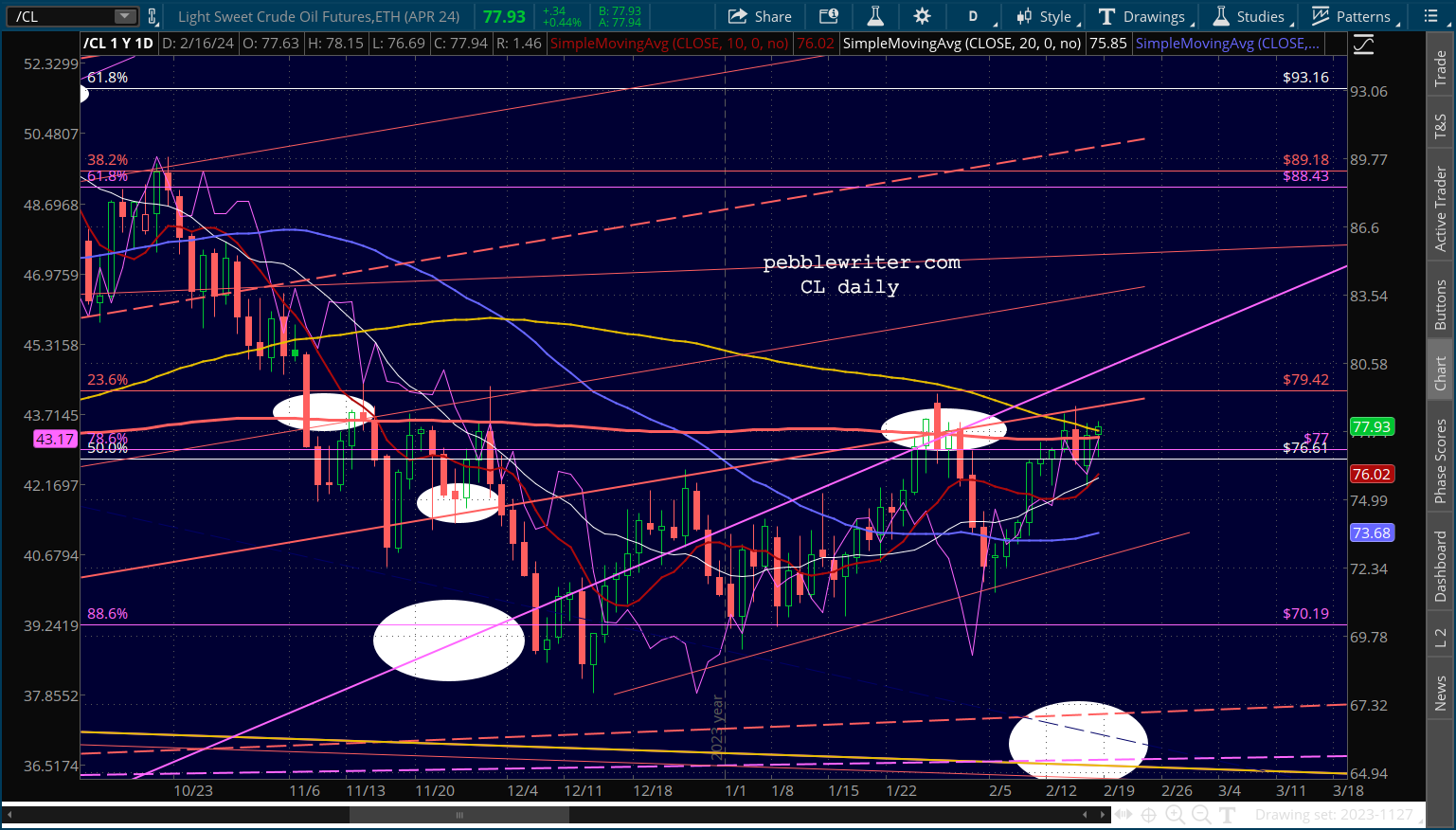

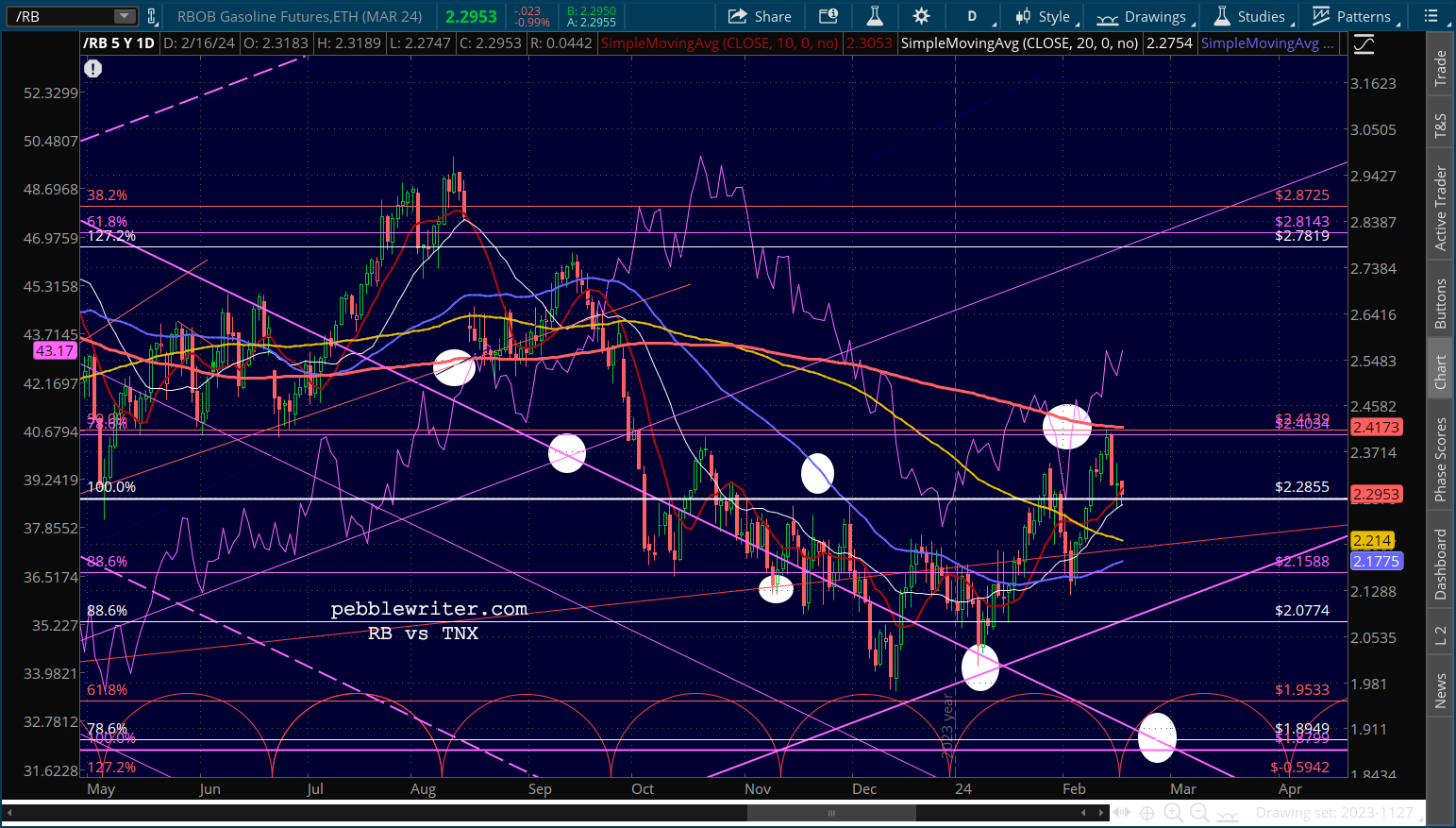

As a result, DXY’s rise remains muted. CL and RB are split, with CL still threatening a breakout above its SMA200.

CL and RB are split, with CL still threatening a breakout above its SMA200.

But, the PPI print is offering plenty of upside pressure as it is. Tuesday’s near miss of the SMA200 could easily be remedied today.

But, the PPI print is offering plenty of upside pressure as it is. Tuesday’s near miss of the SMA200 could easily be remedied today.