Housing starts missed again this morning, underscoring the NAHB’s assessment that the housing industry is in a recession. Starts came in 100K below consensus and 9.5% below June’s report.

Futures, still laser focused on OPEX, didn’t budge.

The NAHB posted the 8th monthly decline in a row yesterday, reporting the lowest reading since May 2020. This presents a thorny issue for the Fed.

The NAHB posted the 8th monthly decline in a row yesterday, reporting the lowest reading since May 2020. This presents a thorny issue for the Fed.

Higher interest rates are bringing down prices as we anticipated over a hear ago [see: Time to Sell Your Home?] But, inflation doesn’t reflect housing prices, it reflects a goofy calculation known as owner’s equivalent rent – which is supposedly what you could rent your home for if you were so inclined.

Even this wackadoodle calculation shows that the latest spike is much higher and steeper than those which preceded the last two economic downturns/market crashes.

But, of course, it’s nowhere near the average 14% increases actually experienced nationwide. According to Freddie Mac, this has left 62% of Americans unsure about their ability to pay their rent over the coming year. Nearly 20% of those whose rent increased said they are now “extremely likely” to miss a payment. Then there’s foreclosures, which are up 143% from last year.

But, of course, it’s nowhere near the average 14% increases actually experienced nationwide. According to Freddie Mac, this has left 62% of Americans unsure about their ability to pay their rent over the coming year. Nearly 20% of those whose rent increased said they are now “extremely likely” to miss a payment. Then there’s foreclosures, which are up 143% from last year.

A cooling off of real estate prices would be desirable from the Fed’s standpoint as it might help mitigate high inflation. Yet, due to the COVID downturn, enough builders were more cautious that inventory remained below a 6-month supply until March 2022, when it began rising to June’s 9.3 month supply.

As the chart below shows, this is the same level seen in the lead up to the Great Financial Crisis…

Inventory topped out at 11.4 months in the midst of a 19% reset in prices. If the same percentage drop were to occur now, it would wipe out all gains since June 2021. Note that the median sales price has already dropped 12% so far.

Inventory topped out at 11.4 months in the midst of a 19% reset in prices. If the same percentage drop were to occur now, it would wipe out all gains since June 2021. Note that the median sales price has already dropped 12% so far.

Think about that for a moment. If you purchased a median-priced home in June 2021 ($374,700) and watched it rise to the median price of $457,000 in April 2022, that $82,000 in additional equity might encourage you to purchase a new car, take a vacation, or at least eat out more often. If that bump in your net worth were to vanish, so might your interest in spending.

Think about that for a moment. If you purchased a median-priced home in June 2021 ($374,700) and watched it rise to the median price of $457,000 in April 2022, that $82,000 in additional equity might encourage you to purchase a new car, take a vacation, or at least eat out more often. If that bump in your net worth were to vanish, so might your interest in spending.

When spending dries up, so do corporate sales and profits. As sales and profits drop, so does employment and stock prices. The resulting recession would thus be accompanied by a more severe market correction.

What builders need and want – lower interest rates – is not at all likely at this time, at least according to past and current Fed presidents. They have begrudgingly accepted the fact that sensationally low interest rates are what generated this disastrous inflation in the first place.

By raising rates just the right amount, the Fed hopes to tamp down inflation without causing a nasty recession. While technically not impossible, it’s never been done before. And, this Fed has proven itself fairly inept at reading the economic tea leaves.

continued for members…

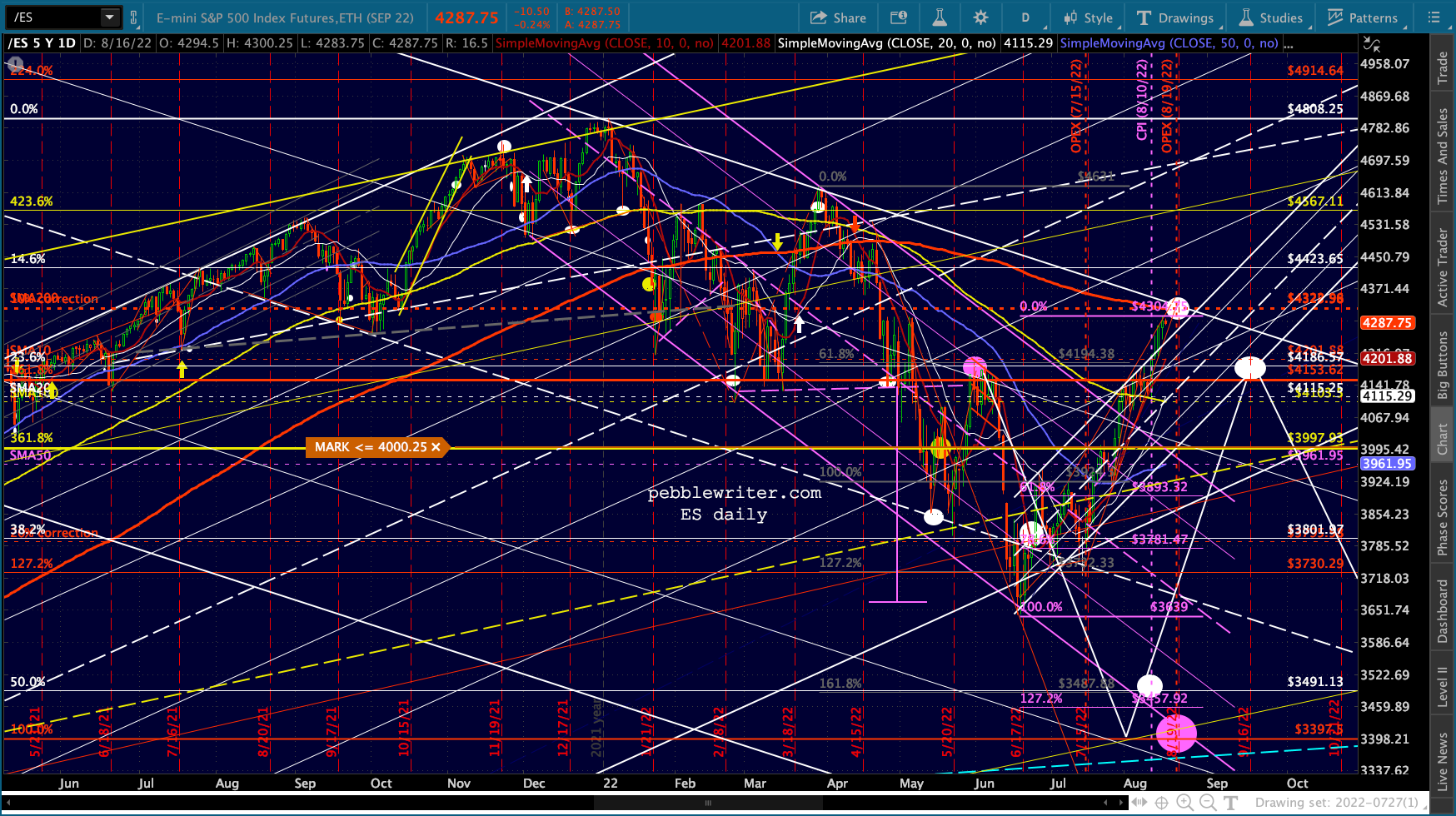

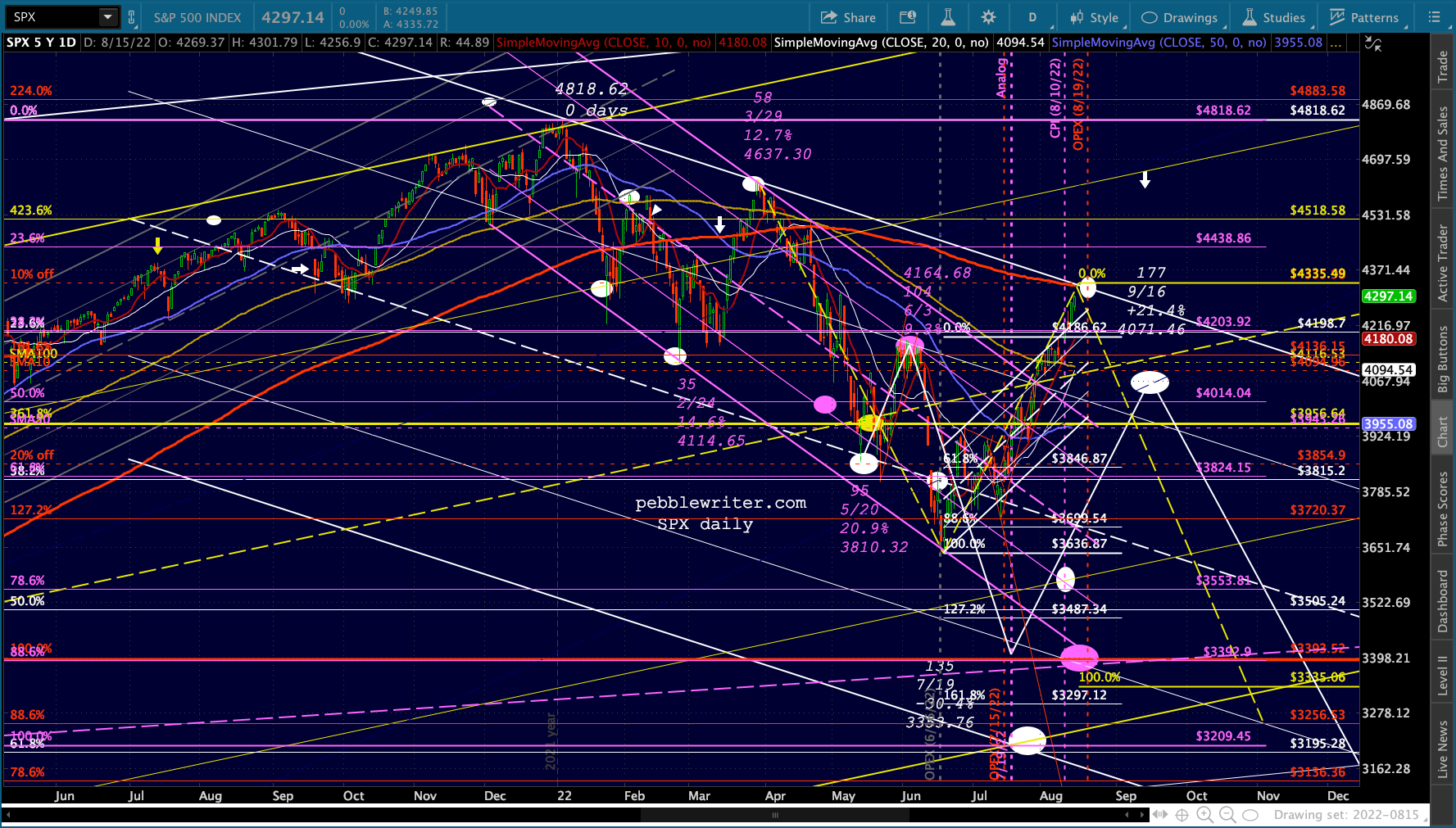

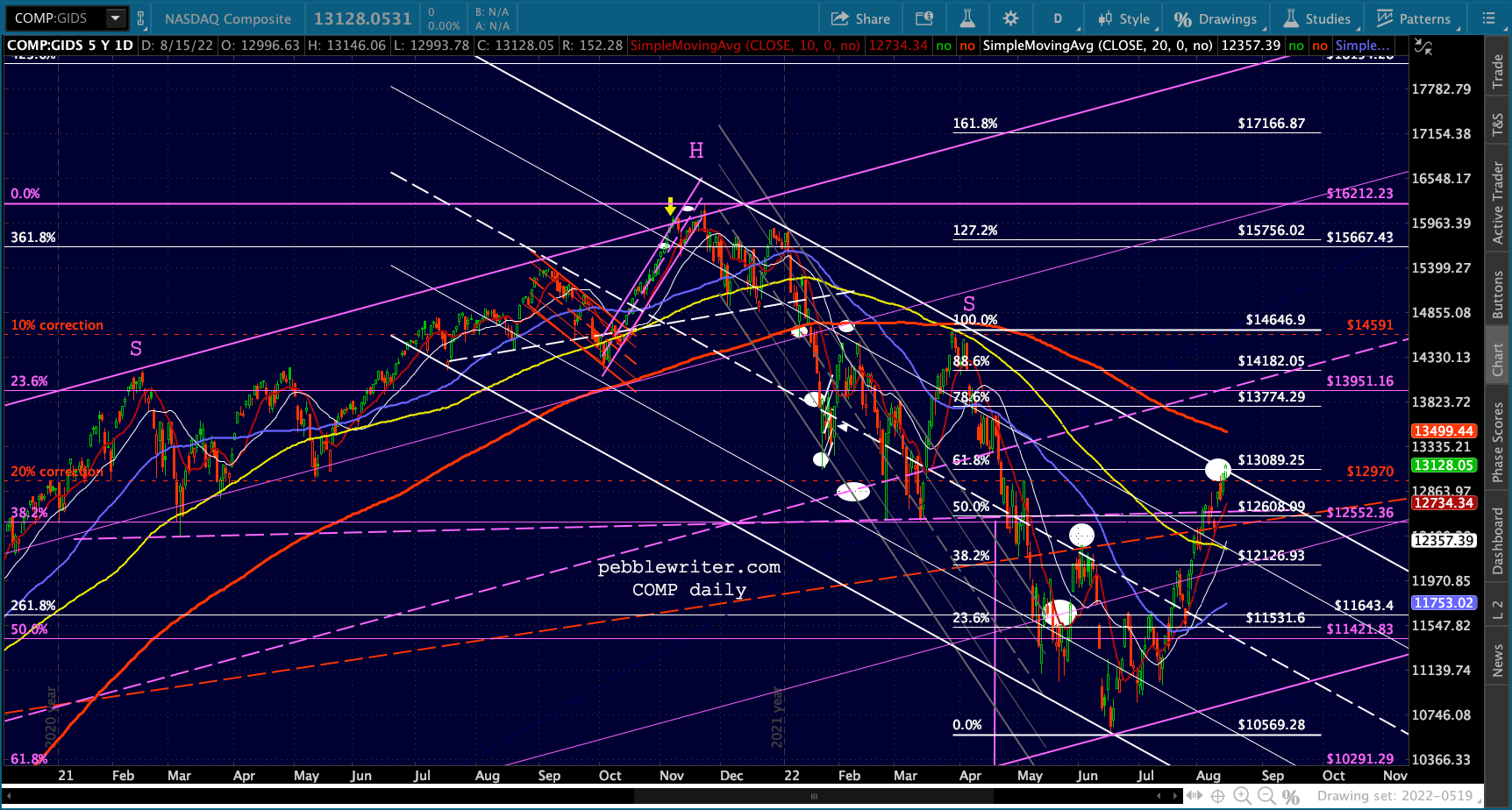

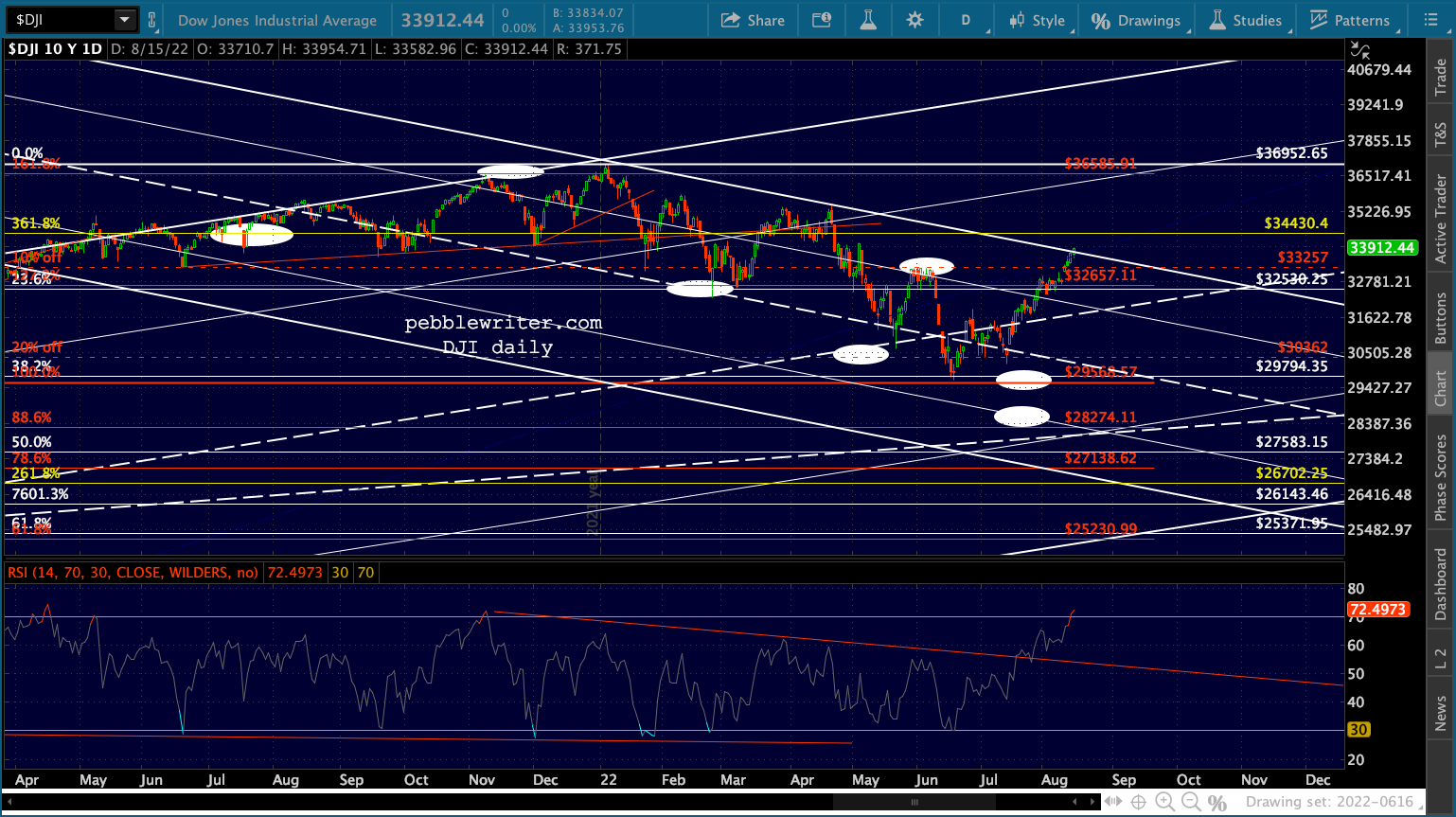

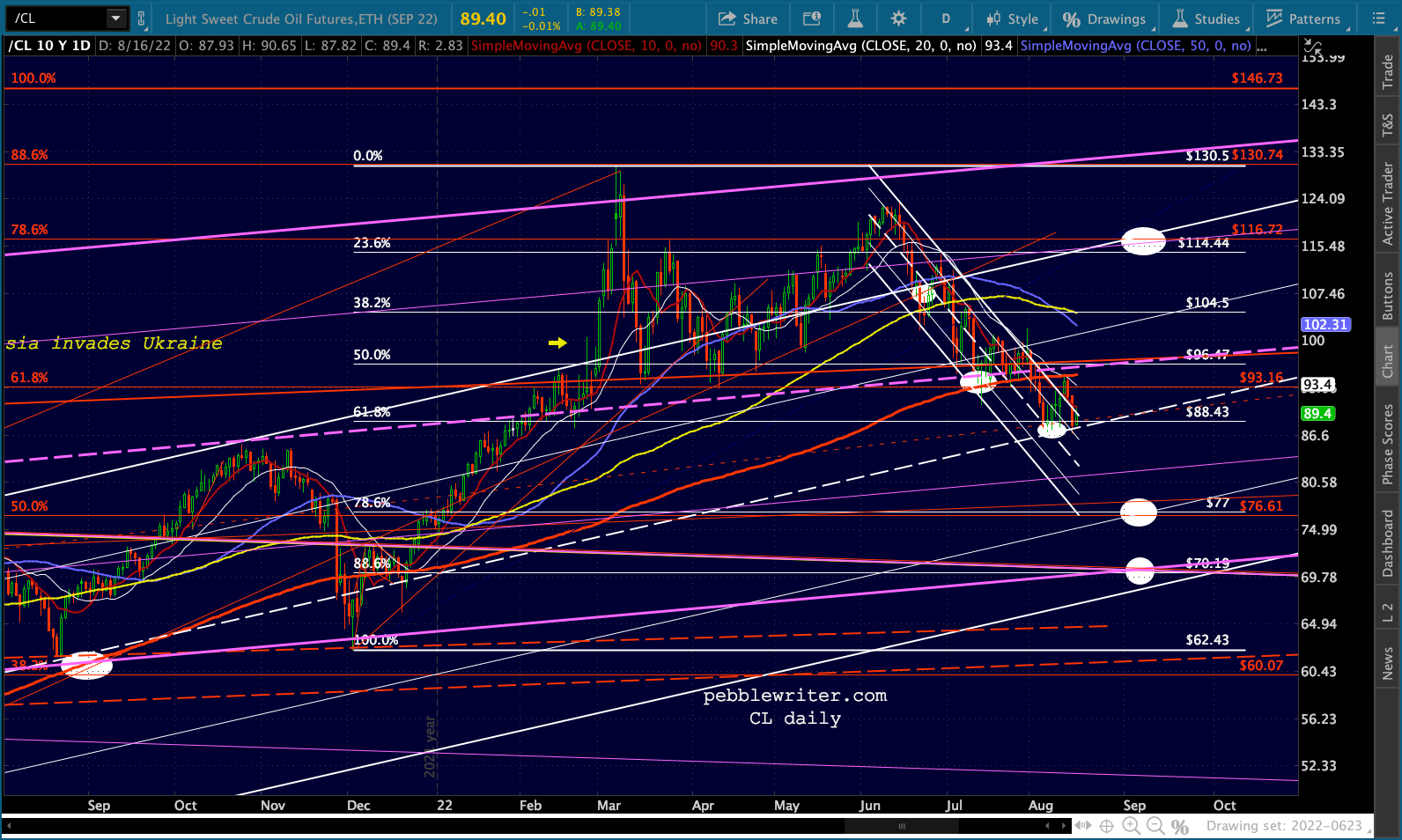

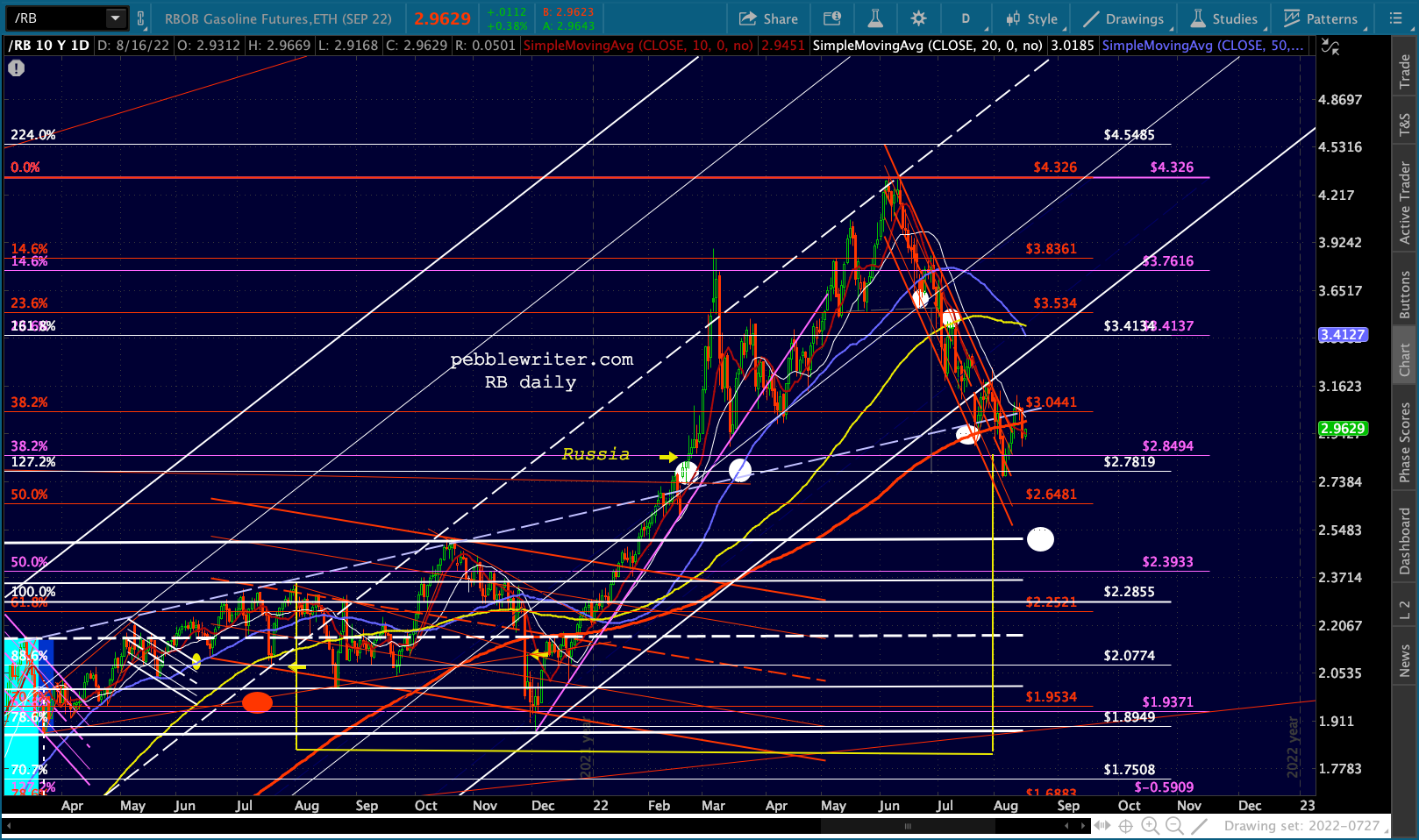

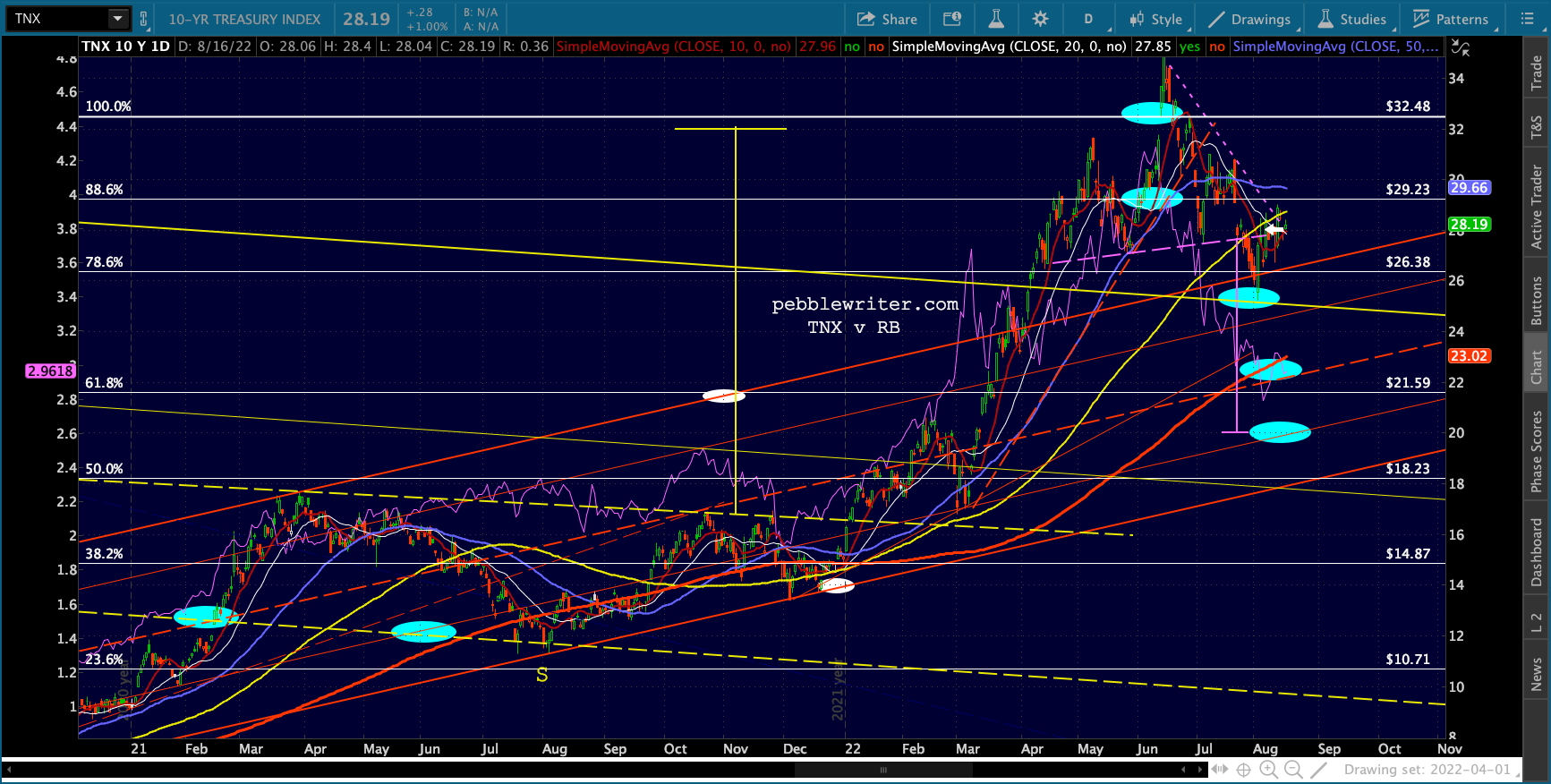

Today’s charts look very much the same as yesterday’s.

As tempting as it is to assume that the overhead resistance represented by channel tops and 200-day moving averages will stop this bounce, there is no way to know for sure. The past few weeks have reinforced the fact that markets can be and frequently are easily manipulated. With the Labor Day holiday weekend coming up, the odds of a “breakout” are further elevated.

As tempting as it is to assume that the overhead resistance represented by channel tops and 200-day moving averages will stop this bounce, there is no way to know for sure. The past few weeks have reinforced the fact that markets can be and frequently are easily manipulated. With the Labor Day holiday weekend coming up, the odds of a “breakout” are further elevated.

It will quite possibly come down to how bearish the Fed’s minutes and subsequent comments are. If they want to put a damper on things, they can announce a strong possibility of another 75 bps hike and/or the consideration of a 100 bps hike. If they want to ensure the rally continues, they need to simply say it’s time to pause and reflect, be data-dependent, etc.

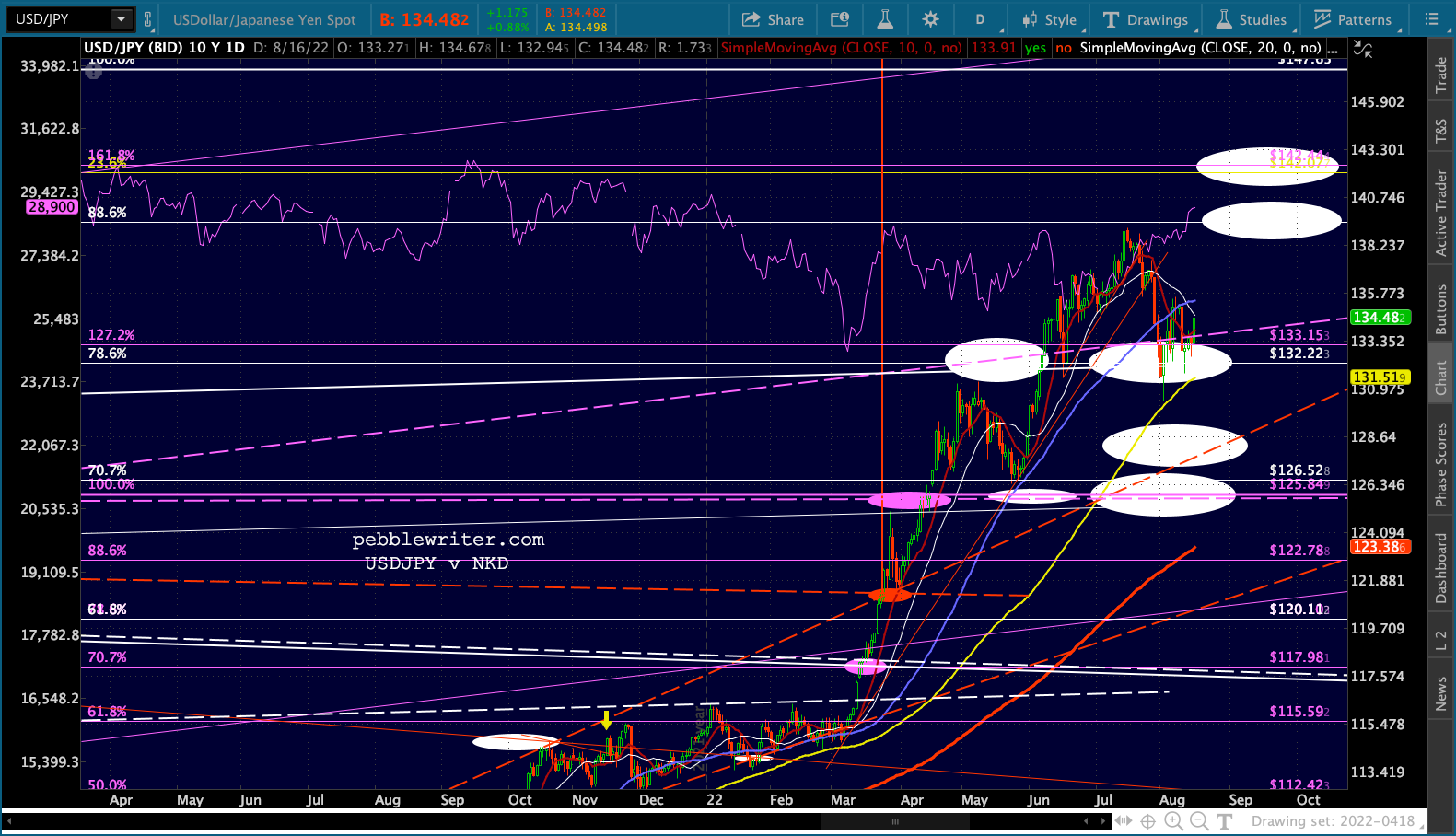

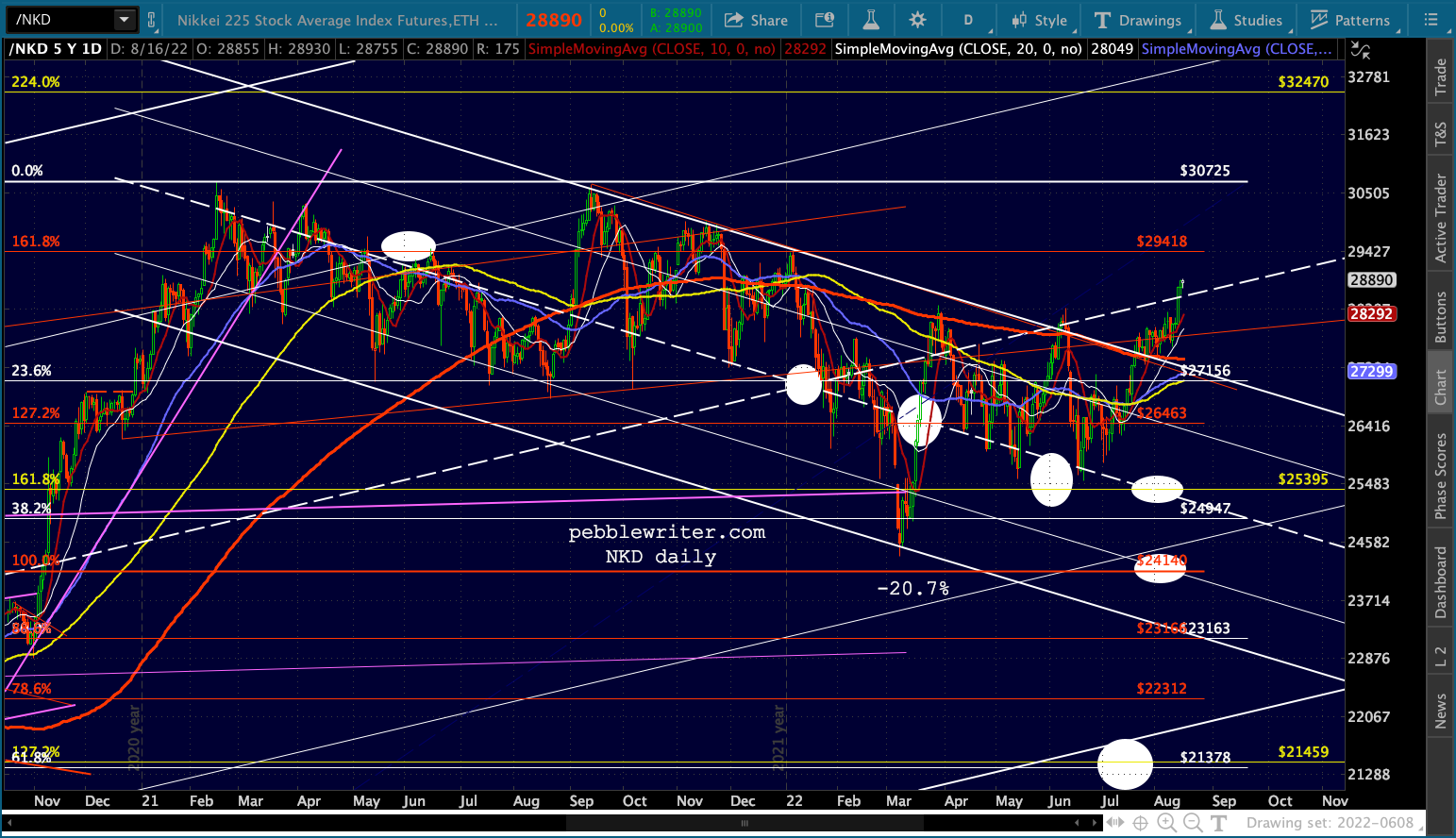

FWIW, the Dow appears to be breaking out already. And, it’s not just the Fed. We can see some action in USDJPY this morning, designed of course to ensure that NKD’s breakout continues.

And, it’s not just the Fed. We can see some action in USDJPY this morning, designed of course to ensure that NKD’s breakout continues.

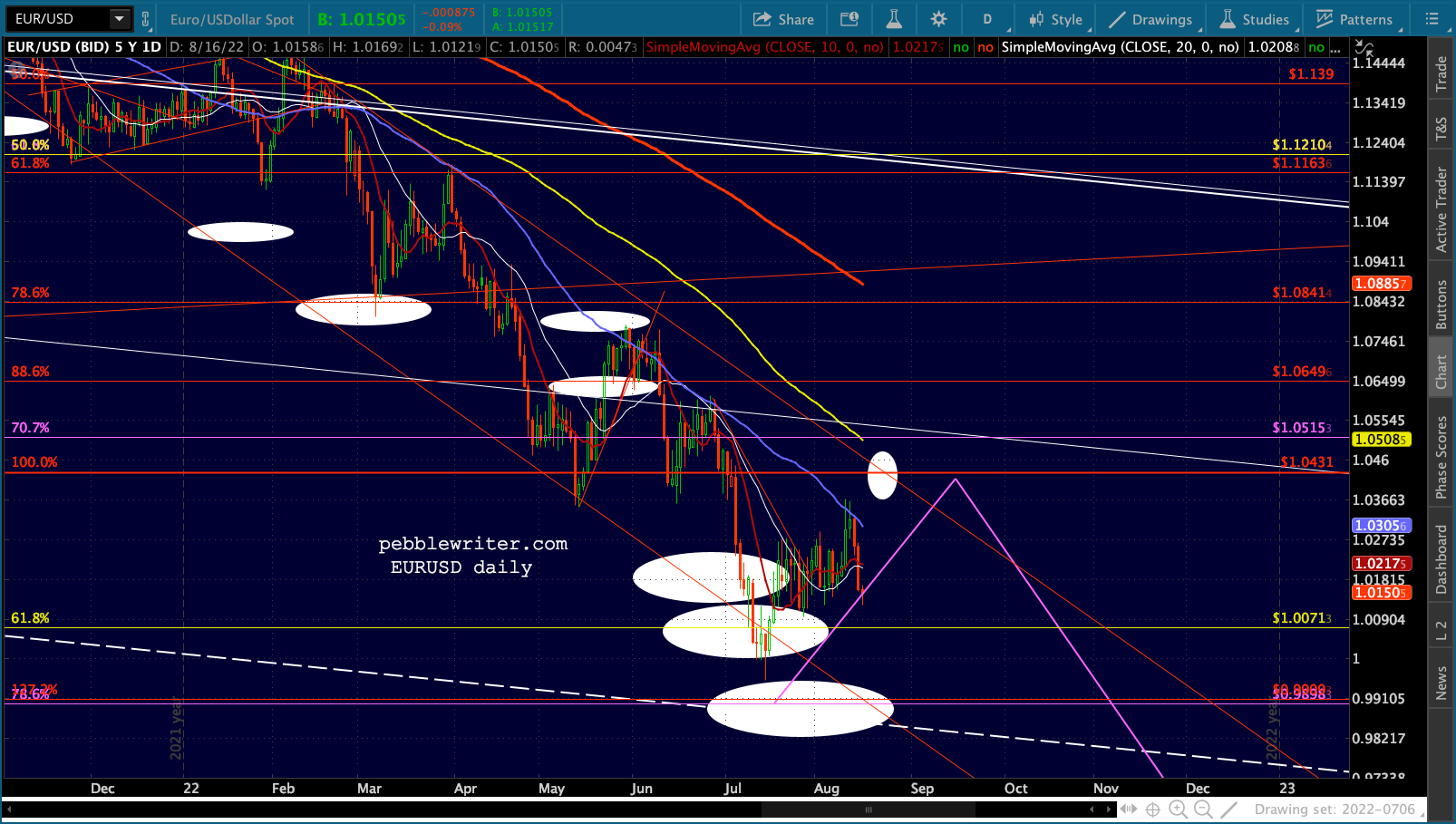

Odds are the USDJPY’s rise will run counter to the EURUSD’s drop.

Odds are the USDJPY’s rise will run counter to the EURUSD’s drop.

Stay tuned…

Stay tuned…