Jerome Powell gave a good news/bad news speech to the Economic Club of New York. He noted that employment is still 10 million below February 2020 levels and that a broader range of unemployment would put the current rate at 10%, adding, “We are still very far from a strong labor market whose benefits are broadly shared.”

As the algos were spinning up their sell orders, he delivered the good news upon which the market relies: “Achieving and sustaining maximum employment will require more than supportive monetary policy.” He added that it could take “many years” to overcome the effects of long-term unemployment and scoffed at the idea of problematic inflation.

As the algos were spinning up their sell orders, he delivered the good news upon which the market relies: “Achieving and sustaining maximum employment will require more than supportive monetary policy.” He added that it could take “many years” to overcome the effects of long-term unemployment and scoffed at the idea of problematic inflation.

From my vantage point, he’s right and he’s wrong. The strong earnings and cheerleading from pandemic lockdown beneficiaries have drowned out the wails from the pandemic’s have-nots: those who find that even a $1,400 stimulus check won’t pay the rent, the millions of small businesses and self-employed who couldn’t qualify for PPP loans, the millions for whom unemployment benefits are unobtainable or inadequate.

But, make no mistake about inflation. Yesterday’s CPI data reiterates our long-held conviction that, although official core inflation is mild, actual inflation is much higher. Even the understated official CPI will soon soar to levels not seen since before the pandemic (when 10Y yields topped 2%) unless the manufactured rebound in oil and gas prices unwinds posthaste.

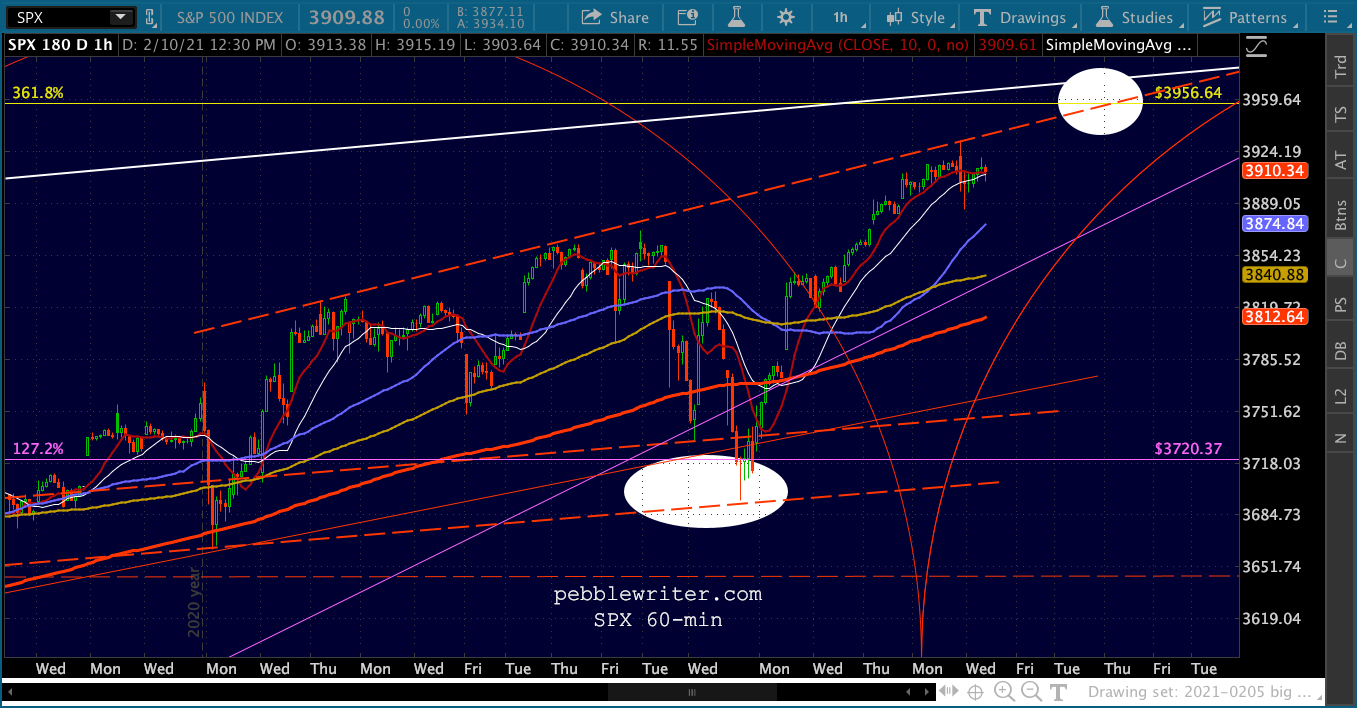

The morning after, futures have regained most of their losses and are again knocking on the door of the 1.272 Fibonacci extension…

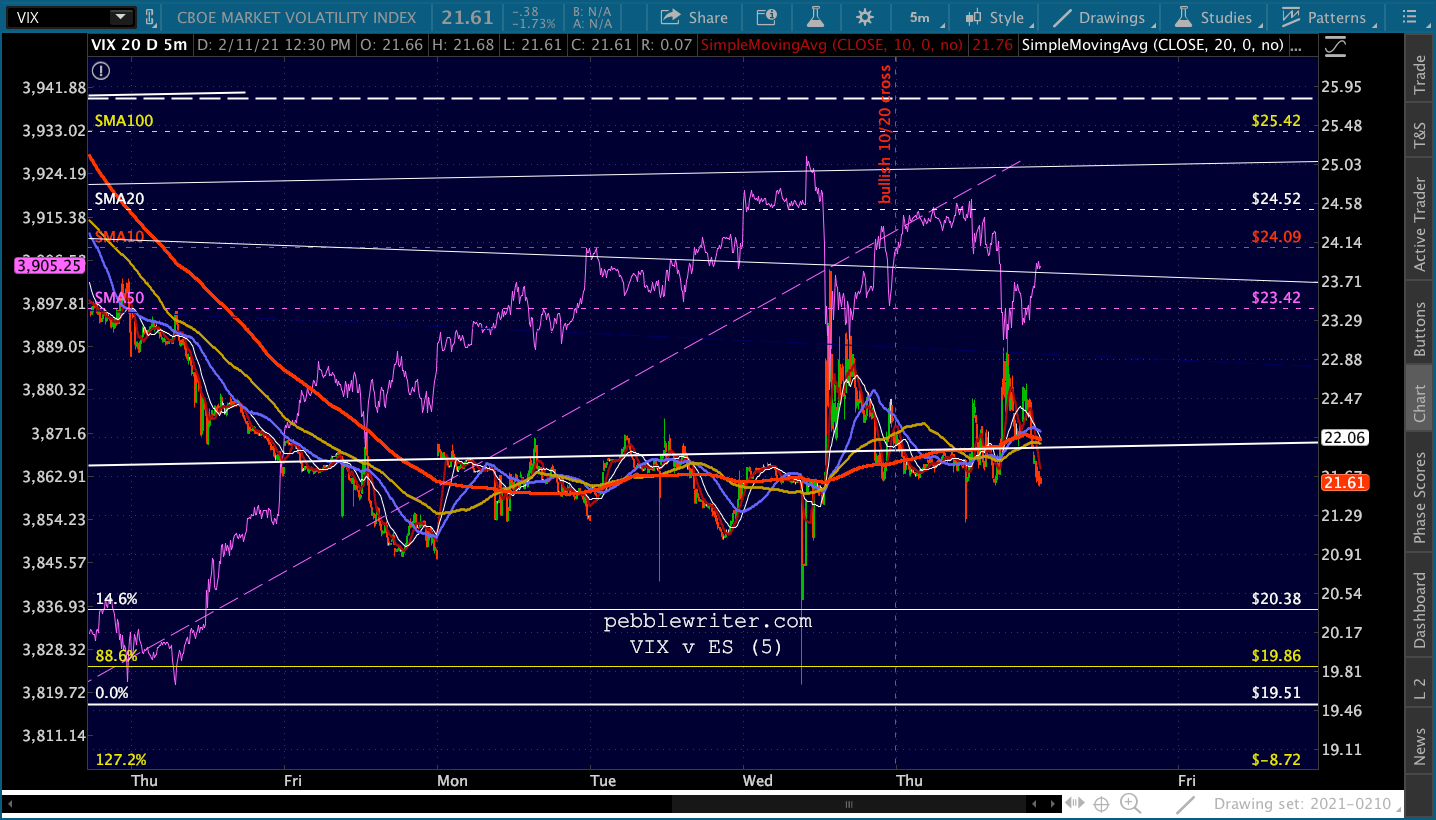

The morning after, futures have regained most of their losses and are again knocking on the door of the 1.272 Fibonacci extension… …thanks primarily to yet another VIX “breakdown” from its rising channel which, as we discussed yesterday, has produced another bearish (bullish for stocks) 10/20 SMA cross.

…thanks primarily to yet another VIX “breakdown” from its rising channel which, as we discussed yesterday, has produced another bearish (bullish for stocks) 10/20 SMA cross. Will it be enough to offset the cold water with which Powell just drenched the reinflation trade?

Will it be enough to offset the cold water with which Powell just drenched the reinflation trade?

continued for members…

The bigger picture shows ES and SPX still eyeing their 3.618 Fib extensions:

With USDJPY having officially tagged its SMA100 and ready to help ramp them higher…

With USDJPY having officially tagged its SMA100 and ready to help ramp them higher… …but DXY breaking down, especially after Powell’s comments.

…but DXY breaking down, especially after Powell’s comments.  Yields certainly won’t benefit from Powell’s downbeat inflation assessment.

Yields certainly won’t benefit from Powell’s downbeat inflation assessment.

Despite making a rare lower low, RBOB is bouncing again today. I don’t expect it to last.

Despite making a rare lower low, RBOB is bouncing again today. I don’t expect it to last.

Ditto for CL.

Ditto for CL. Elsewhere in the currency world, GC is still finding a breakout quite impossible. Powell’s comments won’t help.

Elsewhere in the currency world, GC is still finding a breakout quite impossible. Powell’s comments won’t help. Although it has already broken out, SI is having a hard time not breaking down again.

Although it has already broken out, SI is having a hard time not breaking down again. EURUSD is still backtesting its SMA50 and could easily expand its falling wedge to a falling channel by merely remaining at these levels a little longer.

EURUSD is still backtesting its SMA50 and could easily expand its falling wedge to a falling channel by merely remaining at these levels a little longer.

On the whole, I am bearish because of the coming downturn in oil and especially gas and what I expect will be another decline in yields and rise in DXY.

On the whole, I am bearish because of the coming downturn in oil and especially gas and what I expect will be another decline in yields and rise in DXY.

But, I am also respectful of the very real potential for stocks to break out and tag their 3.618 extensions should TPTB decide to crash VIX below support and ramp the USDJPY higher. Traders would do well to let ES’ 1.272 extension at 3918.21 and VIX 22 be their guides.

If ES pulls back from here, it has potential down to the previous high of 3862.25. Below that, I’m still mindful that the SMA200 is approaching the Feb 2020 highs at 3397.50. Other levels of interest are the red .886 at 3633 and the white .618 at 3494.

UPDATE: 3:30 PM

Not much to report – just stocks giving up slightly more ground as VIX is employed to keep it from getting out of hand.

Note that Michigan sentiment will be released at 10am tomorrow. I will be taking off around 10:30 to drive my daughter back to college, so my initial post tomorrow morning will be the only one for the day.

Note that Michigan sentiment will be released at 10am tomorrow. I will be taking off around 10:30 to drive my daughter back to college, so my initial post tomorrow morning will be the only one for the day.

GLTA.