CPI increased 0.3% MoM and 1.4% YoY in January – buoyed by a 7.4% increase in the price of gasoline which almost single-handedly accounted for the 3.5% monthly increase in energy prices.  Without food and energy to bolster it, core CPI was unchanged in January and showed a 1.4% increase YoY.

Without food and energy to bolster it, core CPI was unchanged in January and showed a 1.4% increase YoY.

The Fed has its work cut out for it. Energy prices are still down YoY, but that is about to change dramatically when the March-April price plunge is factored in. As we’ve discussed many times, the data points to a surge in CPI to well over 2% unless gas prices correct substantially in the coming months.

The Fed has its work cut out for it. Energy prices are still down YoY, but that is about to change dramatically when the March-April price plunge is factored in. As we’ve discussed many times, the data points to a surge in CPI to well over 2% unless gas prices correct substantially in the coming months.  Futures spurted slightly higher, not on the CPI data…

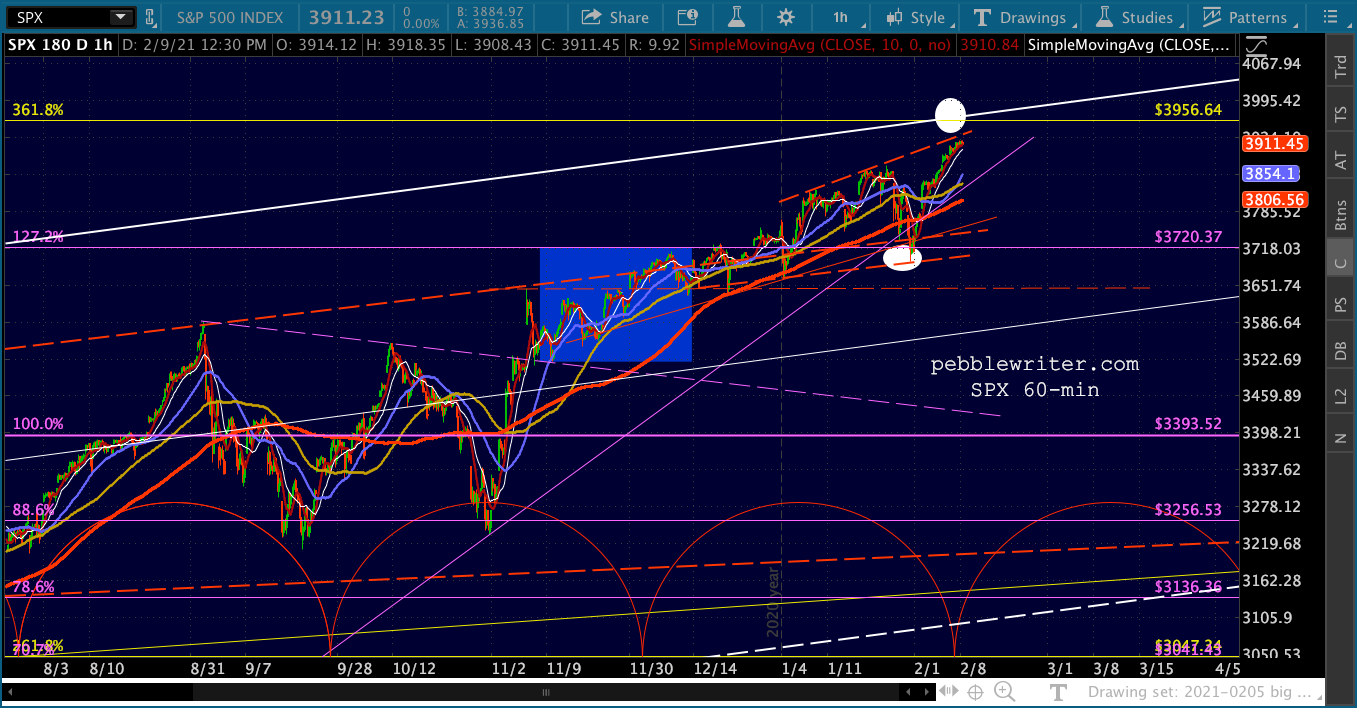

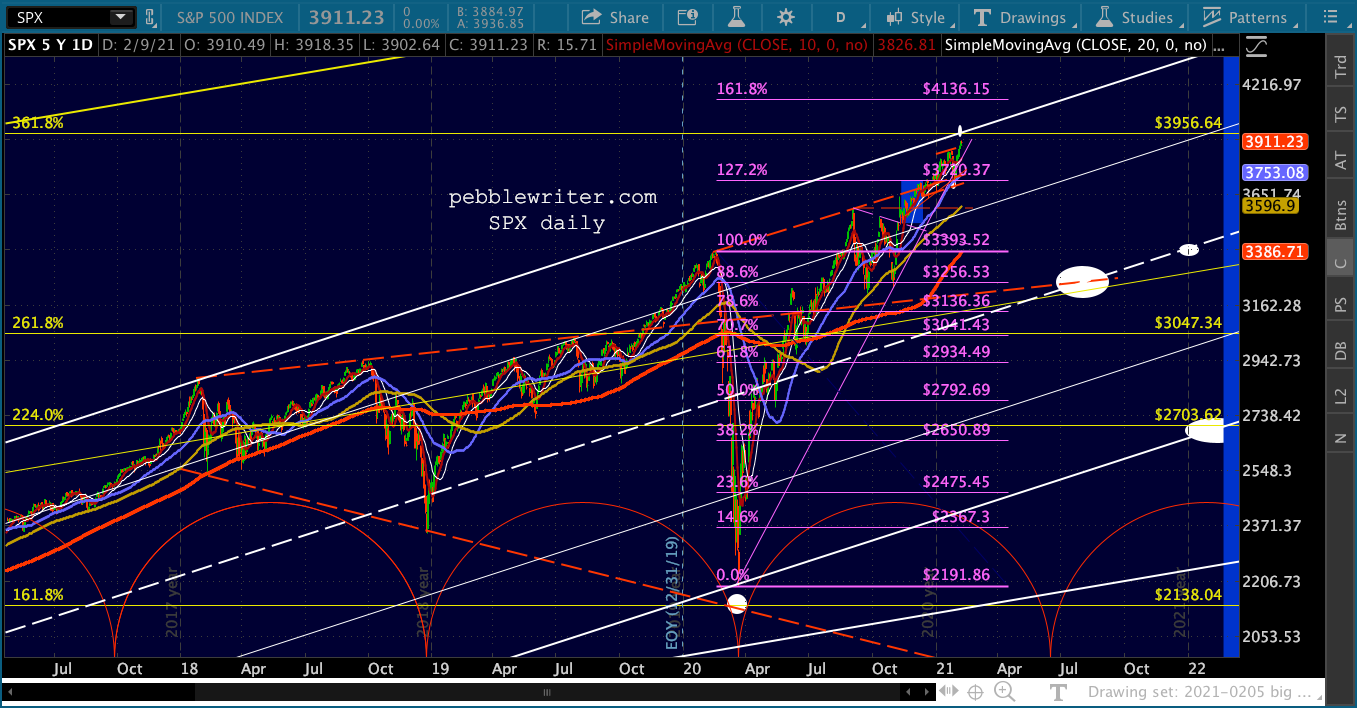

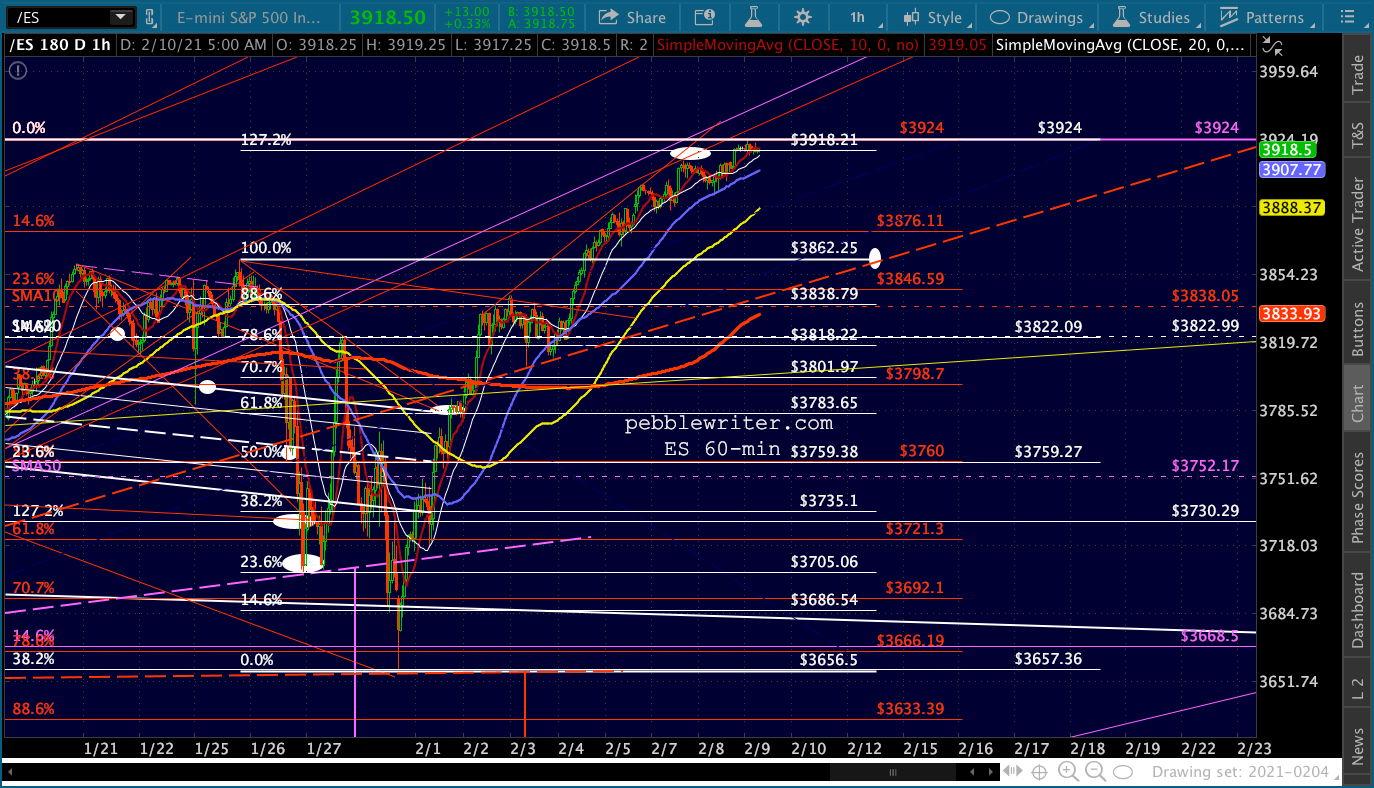

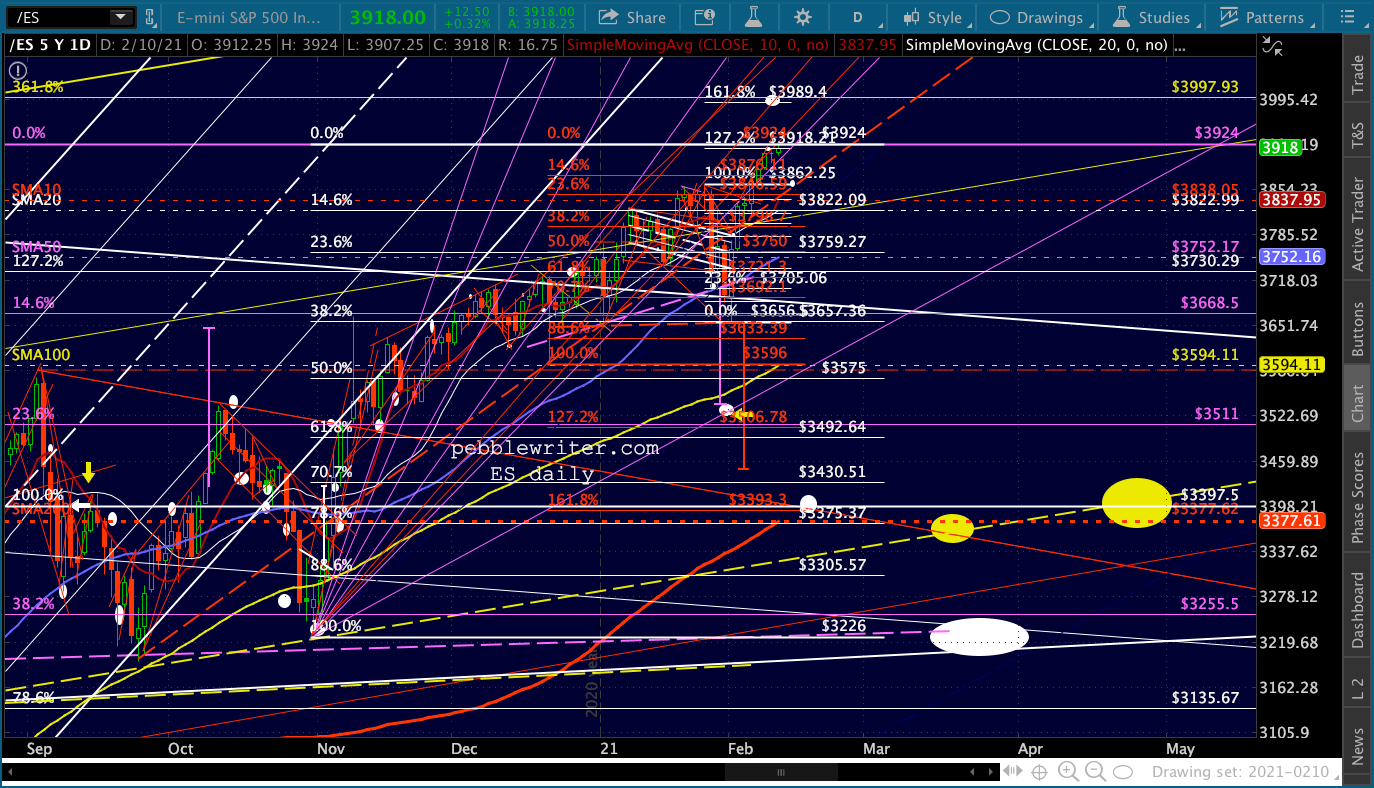

Futures spurted slightly higher, not on the CPI data… …but in response to the signals VIX continues to send the algos. Every dip below the white channel bottom has resulted in a new high for ES.

…but in response to the signals VIX continues to send the algos. Every dip below the white channel bottom has resulted in a new high for ES. continued for members…ES has reached the smaller scale 1.272 and surpassed it – while it and SPX still have bigger fish to fry with their 3.618 Fibs just above.

continued for members…ES has reached the smaller scale 1.272 and surpassed it – while it and SPX still have bigger fish to fry with their 3.618 Fibs just above.

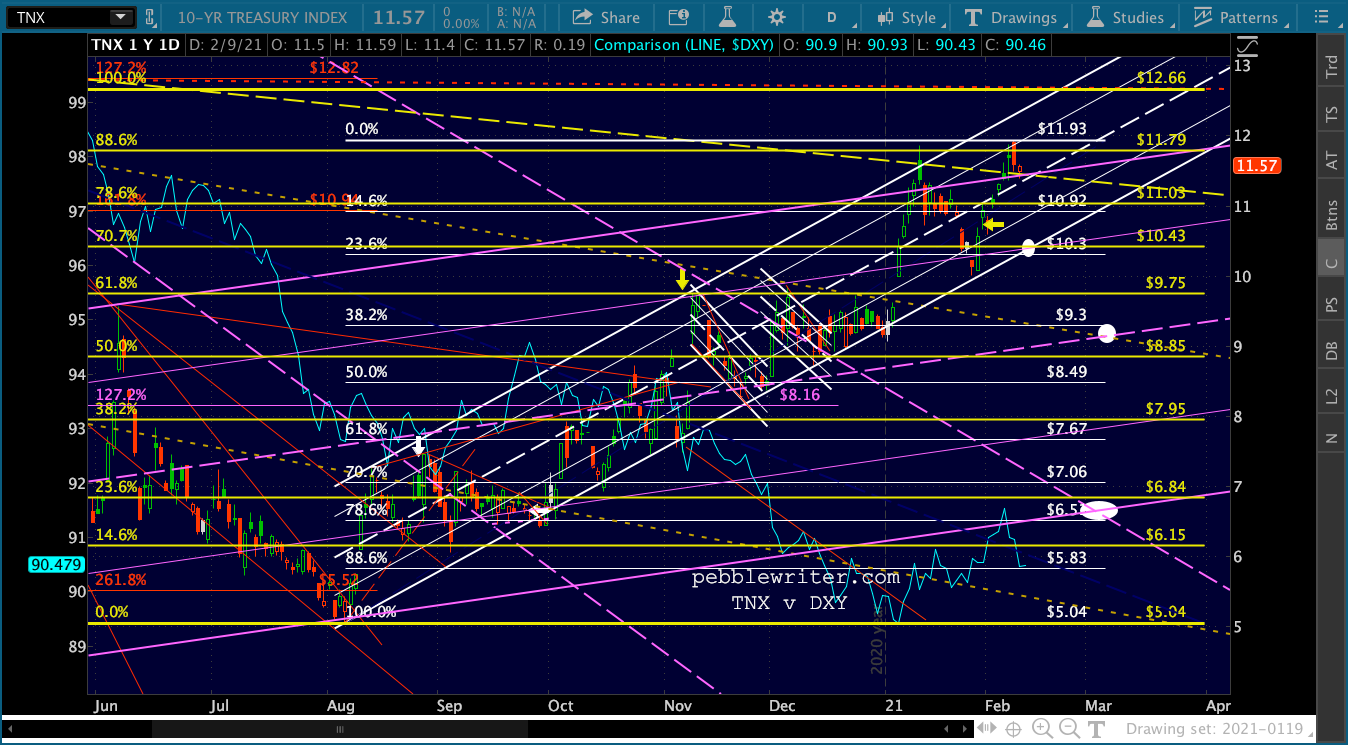

The lackluster inflation numbers will likely continue taking wind from the sails of the 10Y and the US dollar…

The lackluster inflation numbers will likely continue taking wind from the sails of the 10Y and the US dollar…

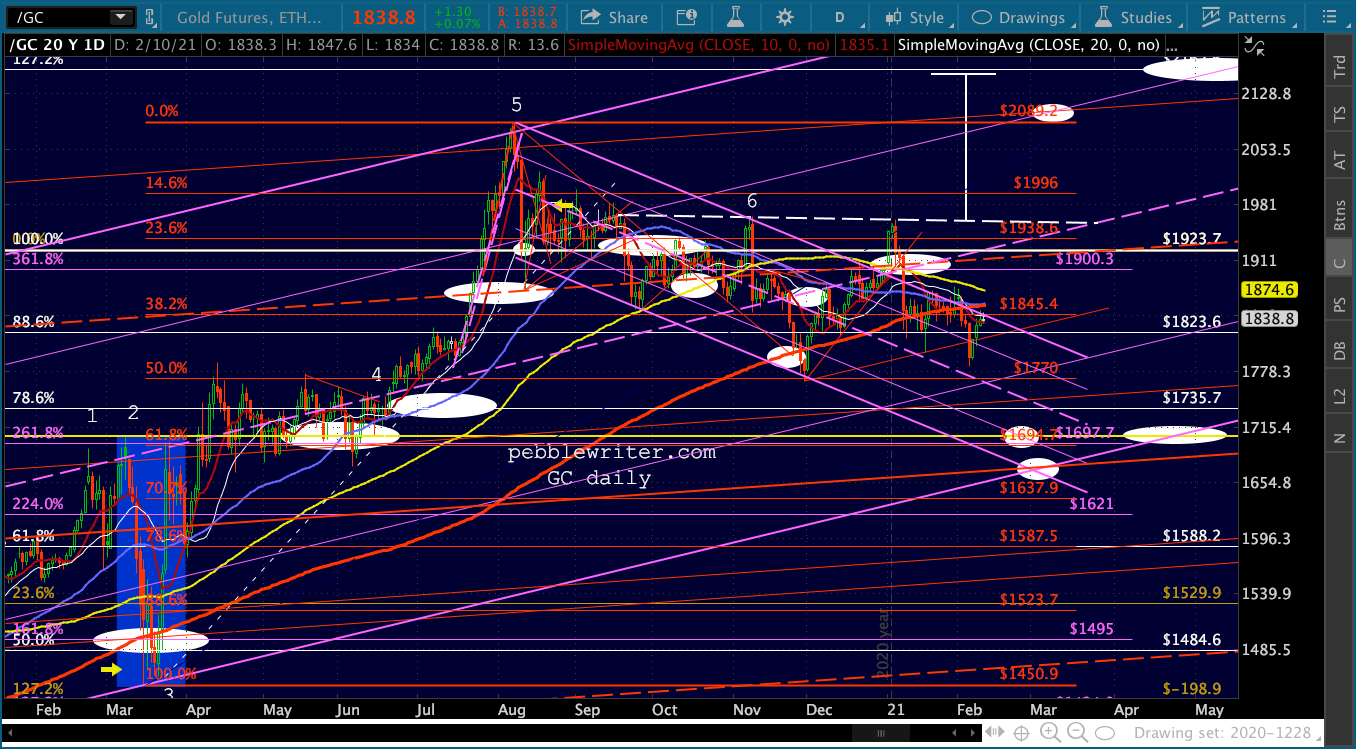

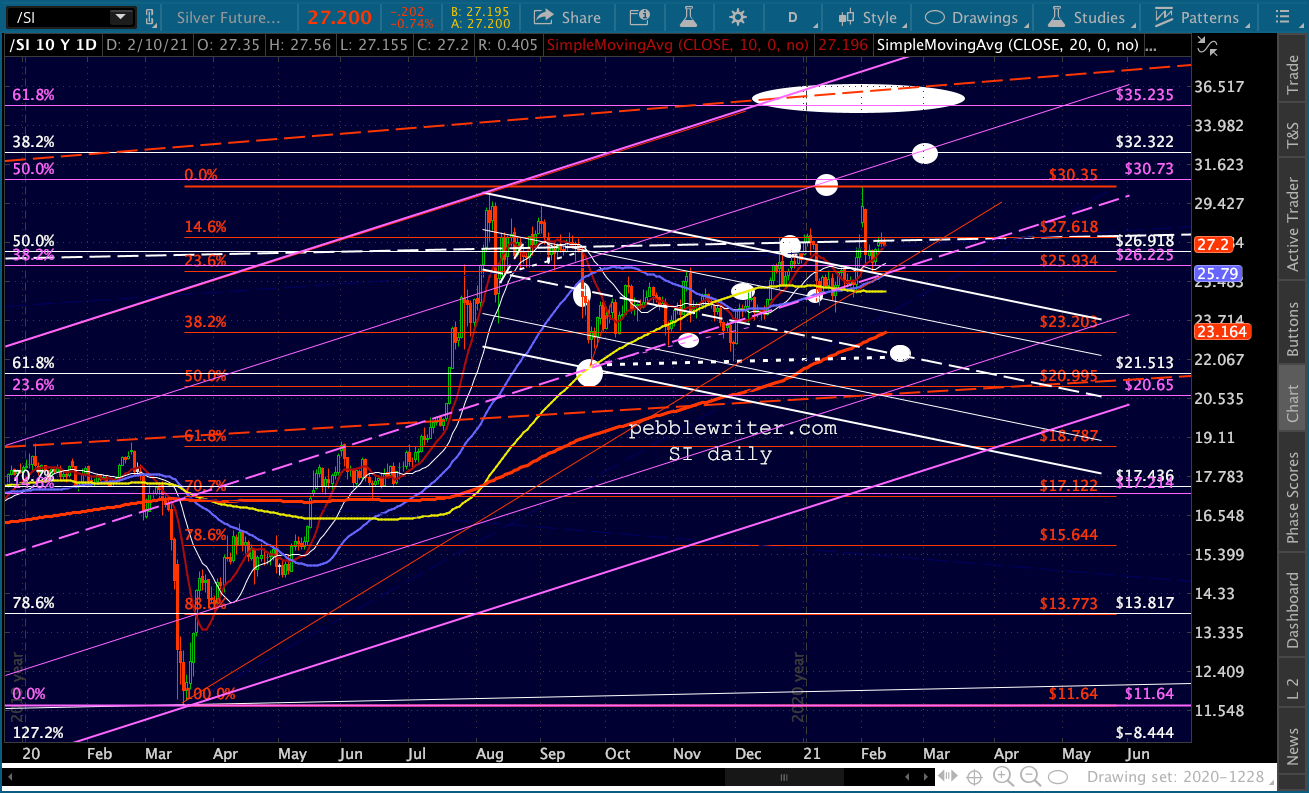

…not to mention GC and SI.

…not to mention GC and SI.

The EURUSD has reached its SMA50 and the top of a little falling wedge that should result in a SMA200 tag in March…

The EURUSD has reached its SMA50 and the top of a little falling wedge that should result in a SMA200 tag in March… …while the USDJPY very nearly tagged our backtest target. At this point, it has a decision to make: continue higher in the rising white channel (bullish for stocks and the DXY) or break down (bearish for stocks and DXY.) If it breaks down, I would look for a backtest of the .886 it almost reached, potentially in April as a backtest also of the broken purple channel. An alternative would be the bottom of the much larger rising white channel.

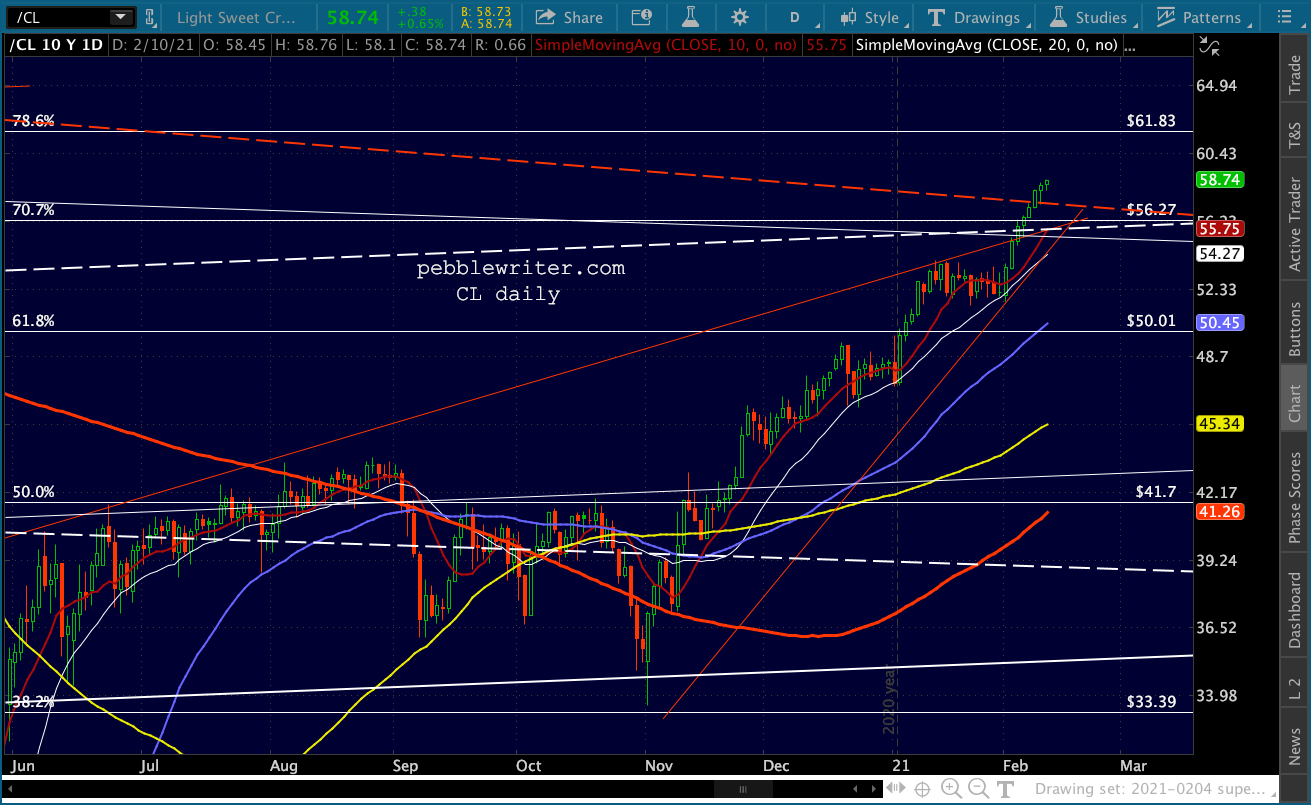

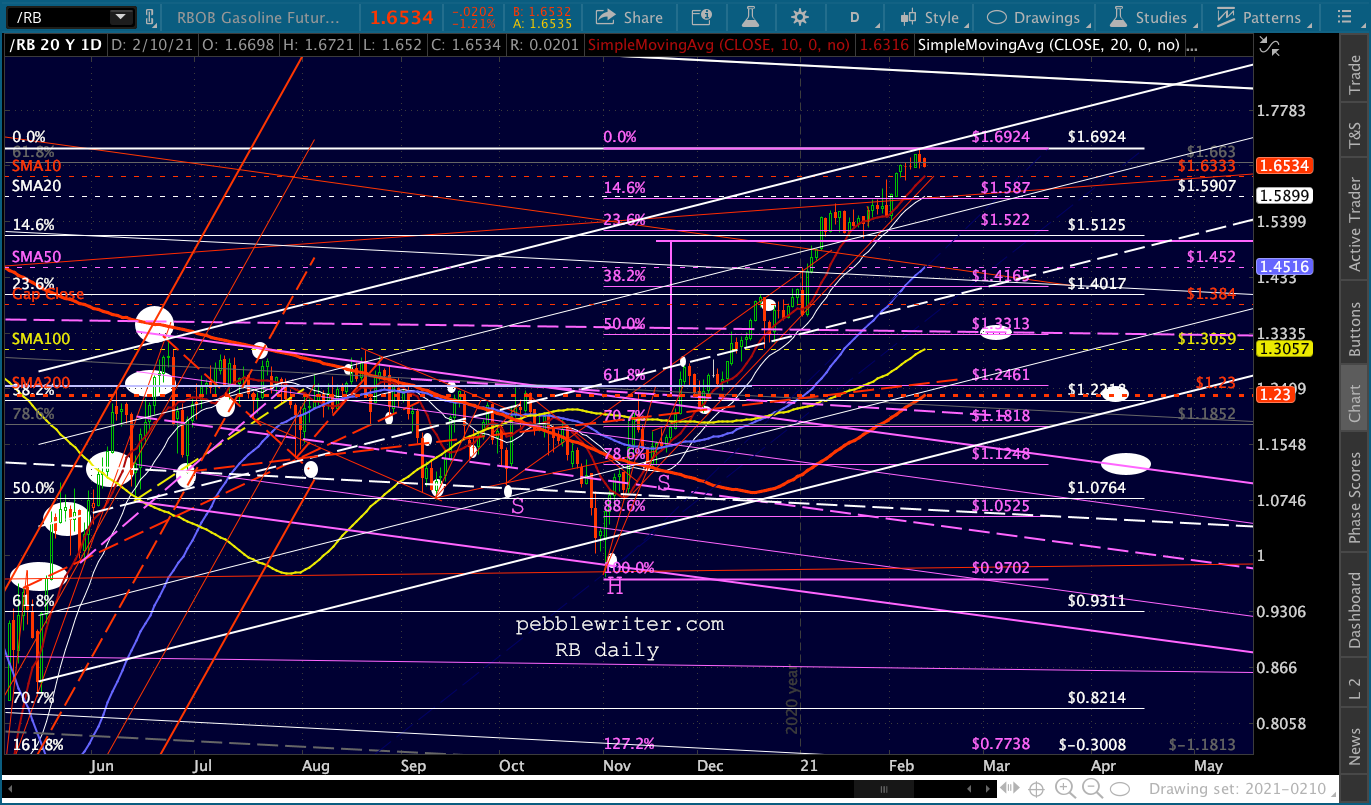

…while the USDJPY very nearly tagged our backtest target. At this point, it has a decision to make: continue higher in the rising white channel (bullish for stocks and the DXY) or break down (bearish for stocks and DXY.) If it breaks down, I would look for a backtest of the .886 it almost reached, potentially in April as a backtest also of the broken purple channel. An alternative would be the bottom of the much larger rising white channel. Oil is edging higher…

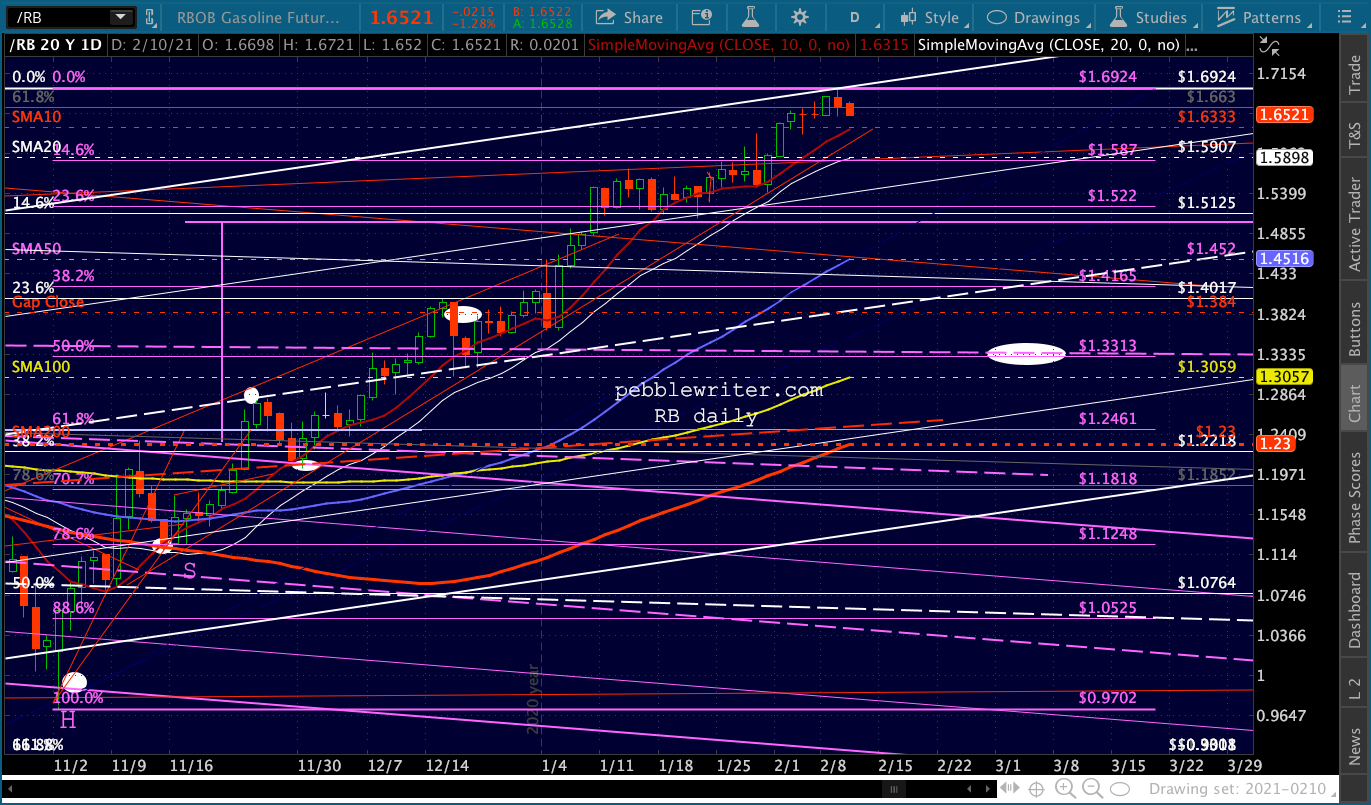

Oil is edging higher… …while RB is working on putting in a lower low.

…while RB is working on putting in a lower low.

To the extent that fundamentals are able to make a difference today, these CPI data certainly don’t support the reflation trade.

To the extent that fundamentals are able to make a difference today, these CPI data certainly don’t support the reflation trade.

GLTA.