Annual CPI remained at 5.4%, the highest in 30 years. And, that alarming number masks plenty of data which the BLS methodology simply ignores. Shelter, for instance, registered a 2.8% YoY increase per BLS’ survey-based calculation. Yet observed apartment rents increased at 9.2% in just the first six months of 2021. And, housing prices have been rising at the fastest rate in over 30 years.

Aside from the games played by the government, some non-transitory trends remain concerning: energy, vehicles and commodities all remain quite elevated. Combined with swiftly rising wages, it will be difficult to put this genie back in the bottle.

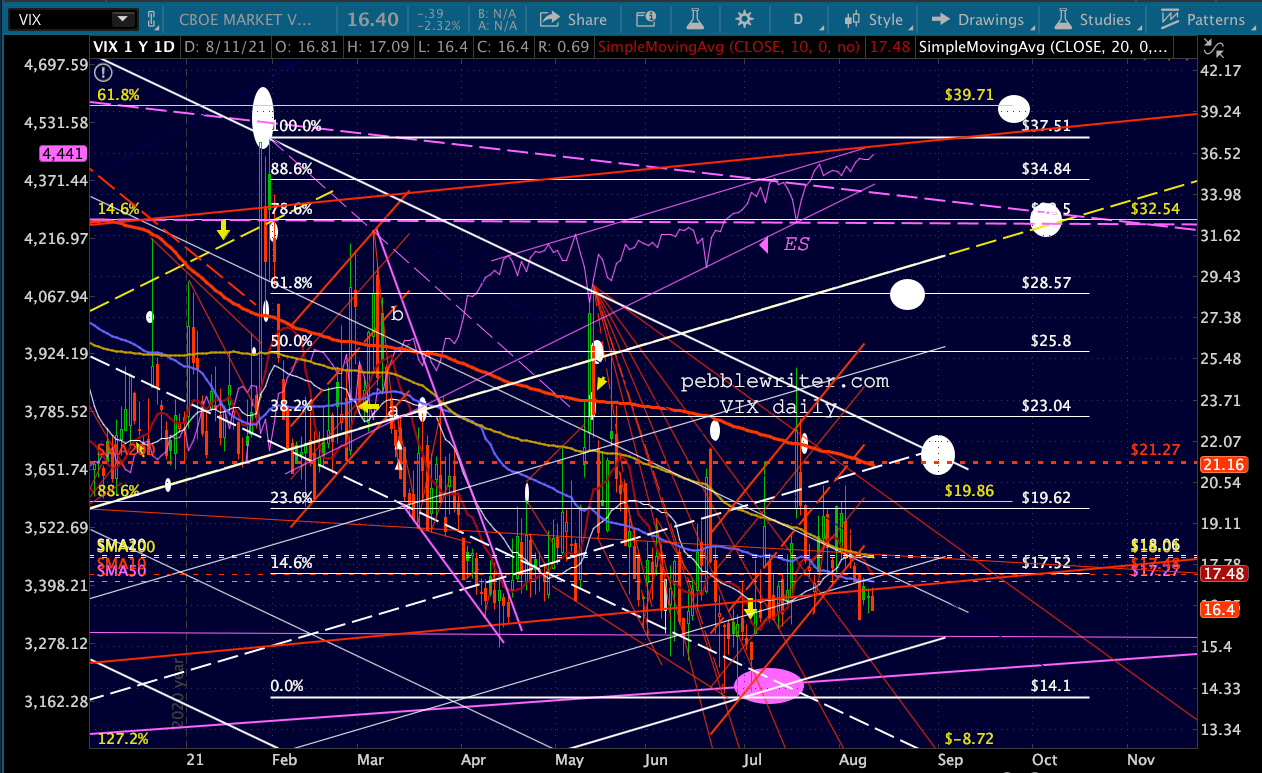

The algos are more concerned, however, with another overnight smackdown in VIX which sent S&P futures to new highs – for now. Pay attention to where that leaves some important Fib retracement levels.

The algos are more concerned, however, with another overnight smackdown in VIX which sent S&P futures to new highs – for now. Pay attention to where that leaves some important Fib retracement levels.

continued for members…

continued for members…

Note that our 10% correction base case is bolstered by the presence of a .618 Fib retracement in line with a TL connecting the two most significant recent dips.

It would appear the administration has finally had enough of high inflation, as the White House publicly called on OPEC to increase production.

It would appear the administration has finally had enough of high inflation, as the White House publicly called on OPEC to increase production.

Biden’s national security adviser Jake Sullivan criticized the world’s major oil producers, including Saudi Arabia, for what he said were insufficient crude production levels in the aftermath of the global COVID-19 pandemic.

“At a critical moment in the global recovery, this is simply not enough,” he said in a statement.

Oil and gas are modestly lower.

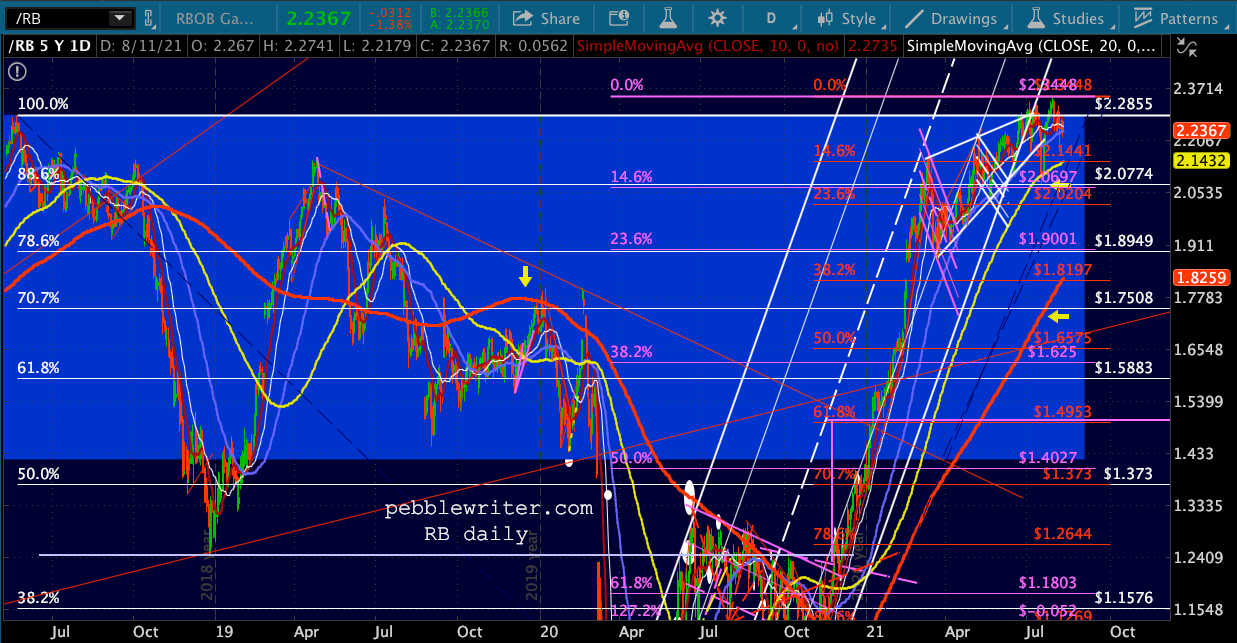

As we’re previously pointed out, CL is at the upper bound of a falling channel from 2008 and RB is at the upper range of the last seven years of price swings. Both are pushing the Oct 2018 highs – the last time a president called on OPEC to increase production due to inflation being too high. For those not already short, this is another reminder…

As we’re previously pointed out, CL is at the upper bound of a falling channel from 2008 and RB is at the upper range of the last seven years of price swings. Both are pushing the Oct 2018 highs – the last time a president called on OPEC to increase production due to inflation being too high. For those not already short, this is another reminder…

We watch USDJPY very closely as its movements offer great insight into the thinking of central banks. Currently, it’s bouncing. But, I continue to expect another leg down – presumably to backtest the falling purple channel again as the SMA200 emerges from it in Sep-Oct.

We watch USDJPY very closely as its movements offer great insight into the thinking of central banks. Currently, it’s bouncing. But, I continue to expect another leg down – presumably to backtest the falling purple channel again as the SMA200 emerges from it in Sep-Oct.

This weakening of the dollar versus the yen should somewhat offset the continuing strengthening versus the euro. EURUSD continues to near our downside targets.

This weakening of the dollar versus the yen should somewhat offset the continuing strengthening versus the euro. EURUSD continues to near our downside targets. We’ll want to watch DXY closely as it approaches the white flag pattern top at 93.89. A breakout to the 97.37 target would almost certainly coincide with an equity correction.

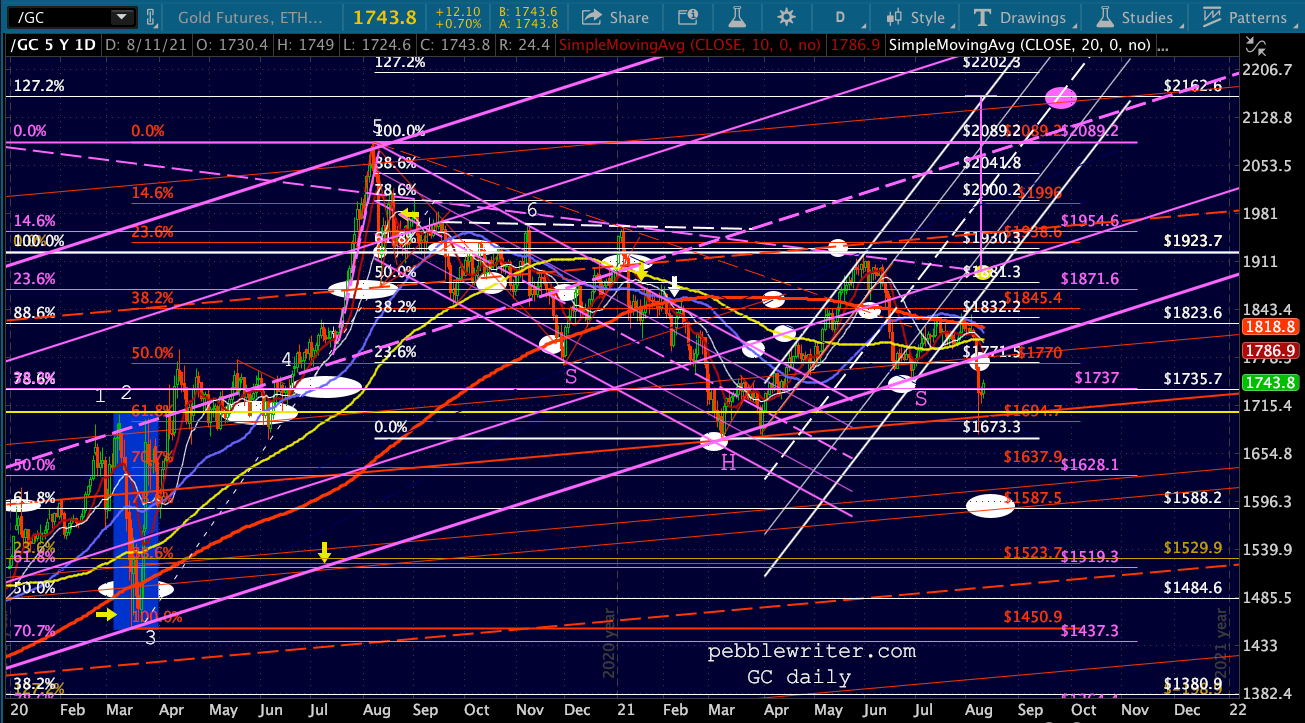

We’ll want to watch DXY closely as it approaches the white flag pattern top at 93.89. A breakout to the 97.37 target would almost certainly coincide with an equity correction. Gold and silver are still trying to make up their minds, with SI still at important support and GC essentially floundering.

Gold and silver are still trying to make up their minds, with SI still at important support and GC essentially floundering.

My gut tells me that with oil and gas probably on the way down, the inflation data going forward will not be constructive for precious metals. But, it’s hard to see an unwind hitting very hard and fast.

My gut tells me that with oil and gas probably on the way down, the inflation data going forward will not be constructive for precious metals. But, it’s hard to see an unwind hitting very hard and fast.

The factor which has made the entire reflation exercise possible, of course, is the Fed’s massive bond buying program which has pinned interest rates at historic lows despite the spike in inflation it has caused.

Complicating the interest rate picture, ZN has dipped back inside the falling purple channel top. If it persists, the risk of a drop in the 10Y to 80 bps will obviously go away.

Complicating the interest rate picture, ZN has dipped back inside the falling purple channel top. If it persists, the risk of a drop in the 10Y to 80 bps will obviously go away. As I’ve previously mentioned, I will be out of the office tomorrow, Aug 12. I hope to get a chance to post later this evening if anything startling occurs. Stay frosty.

As I’ve previously mentioned, I will be out of the office tomorrow, Aug 12. I hope to get a chance to post later this evening if anything startling occurs. Stay frosty.