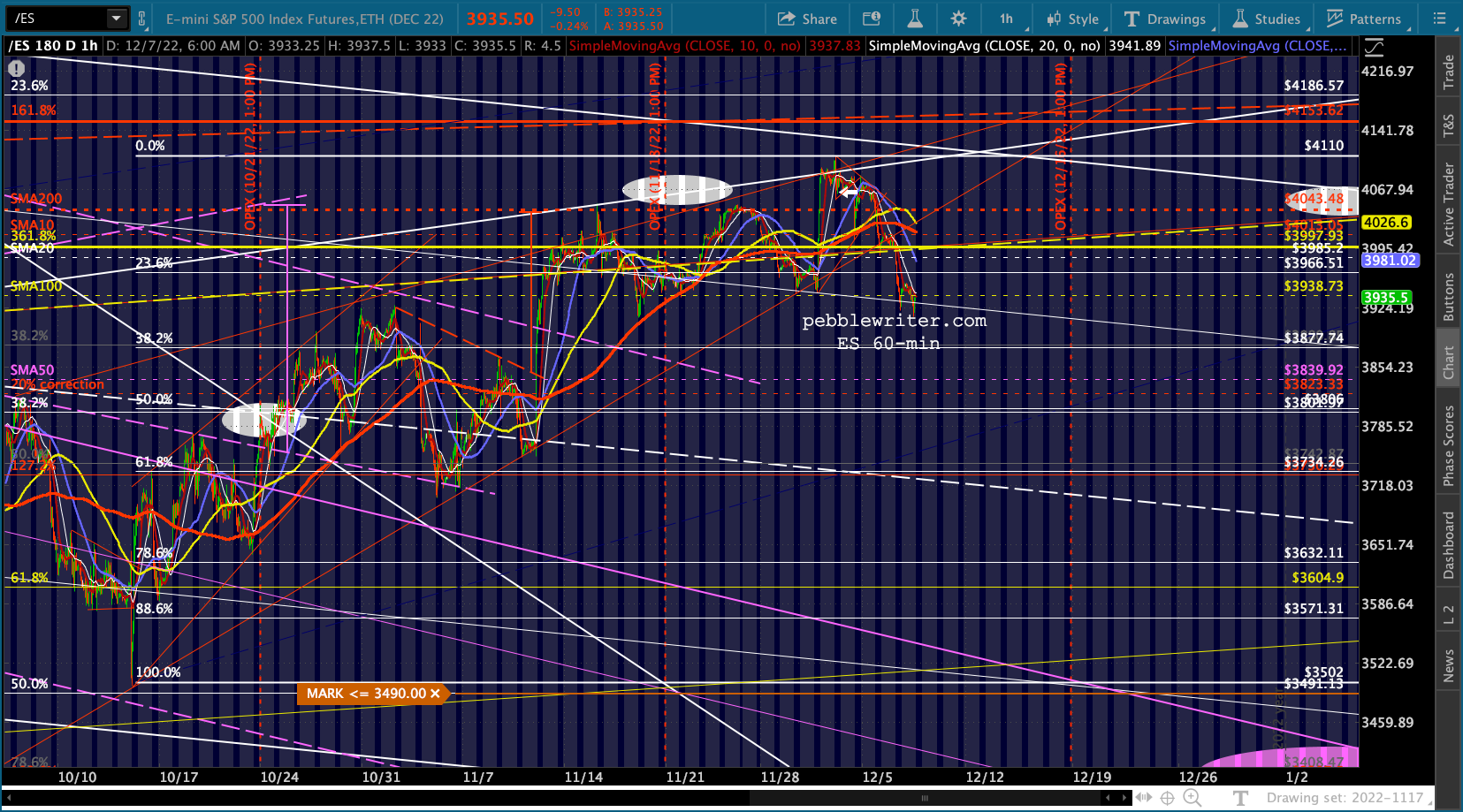

Futures have rebounded from the worst of their overnight losses, but are still on the wrong side of the tracks following yesterday’s breakdown of the rising wedge.

continued for members…

continued for members…

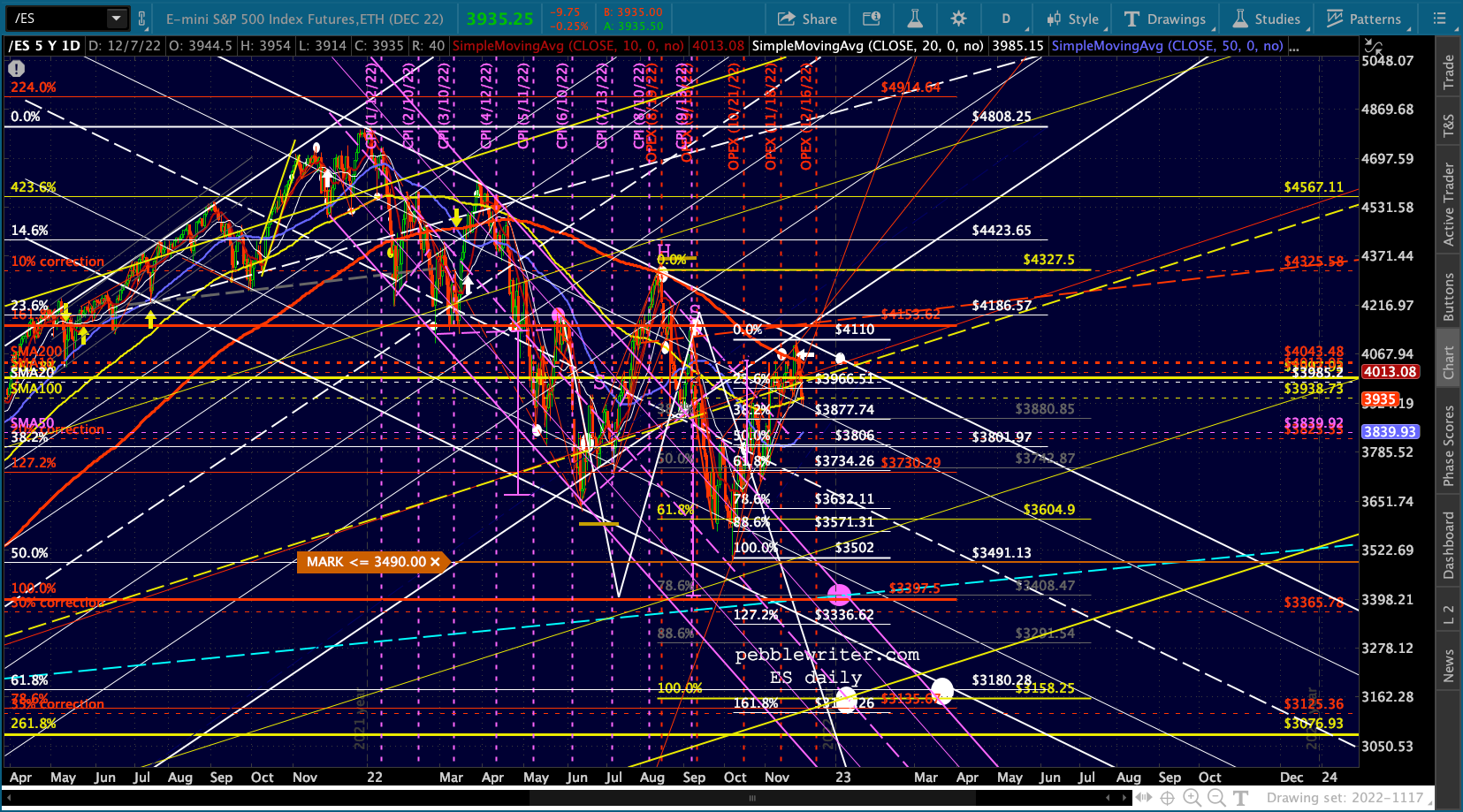

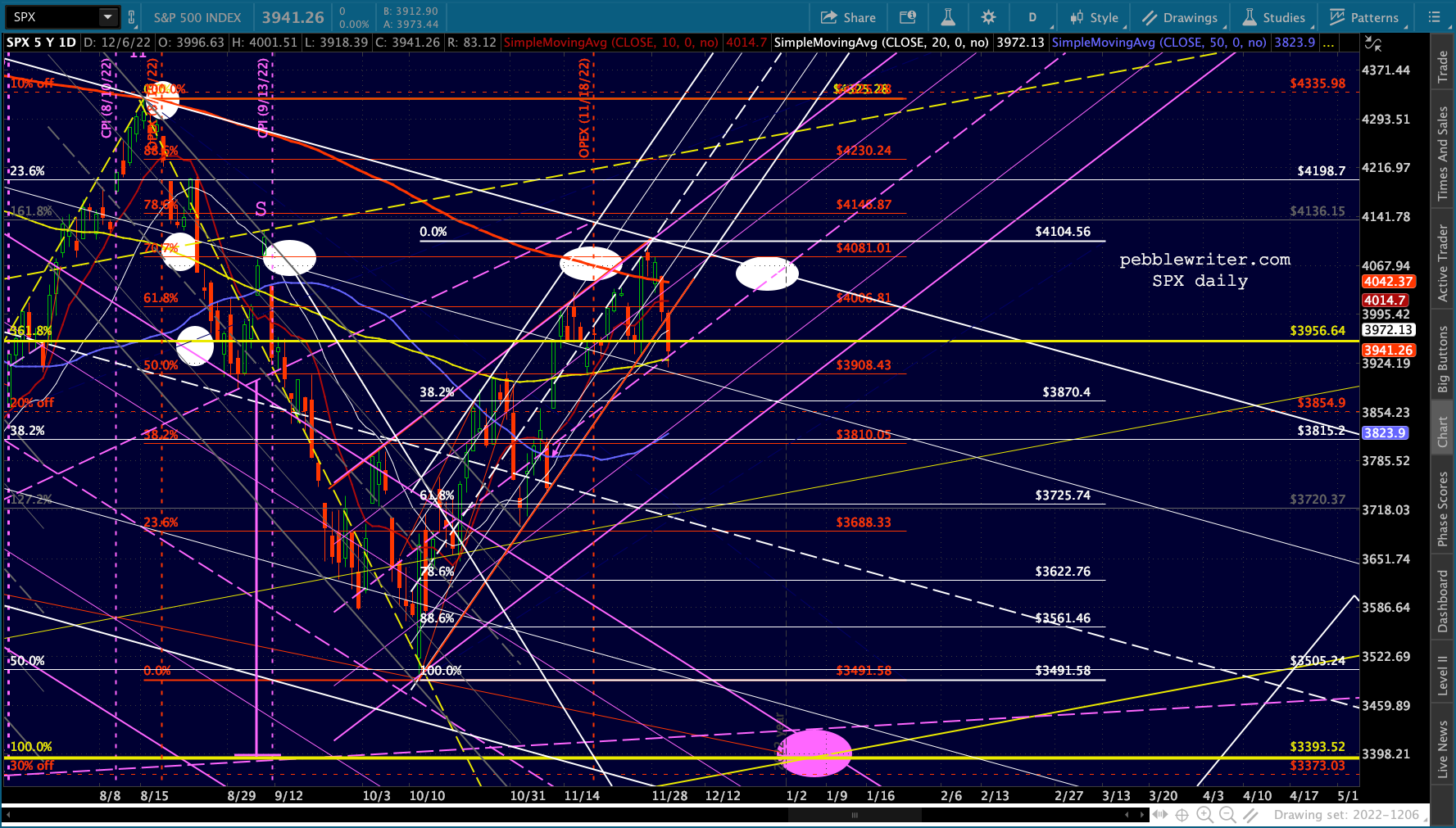

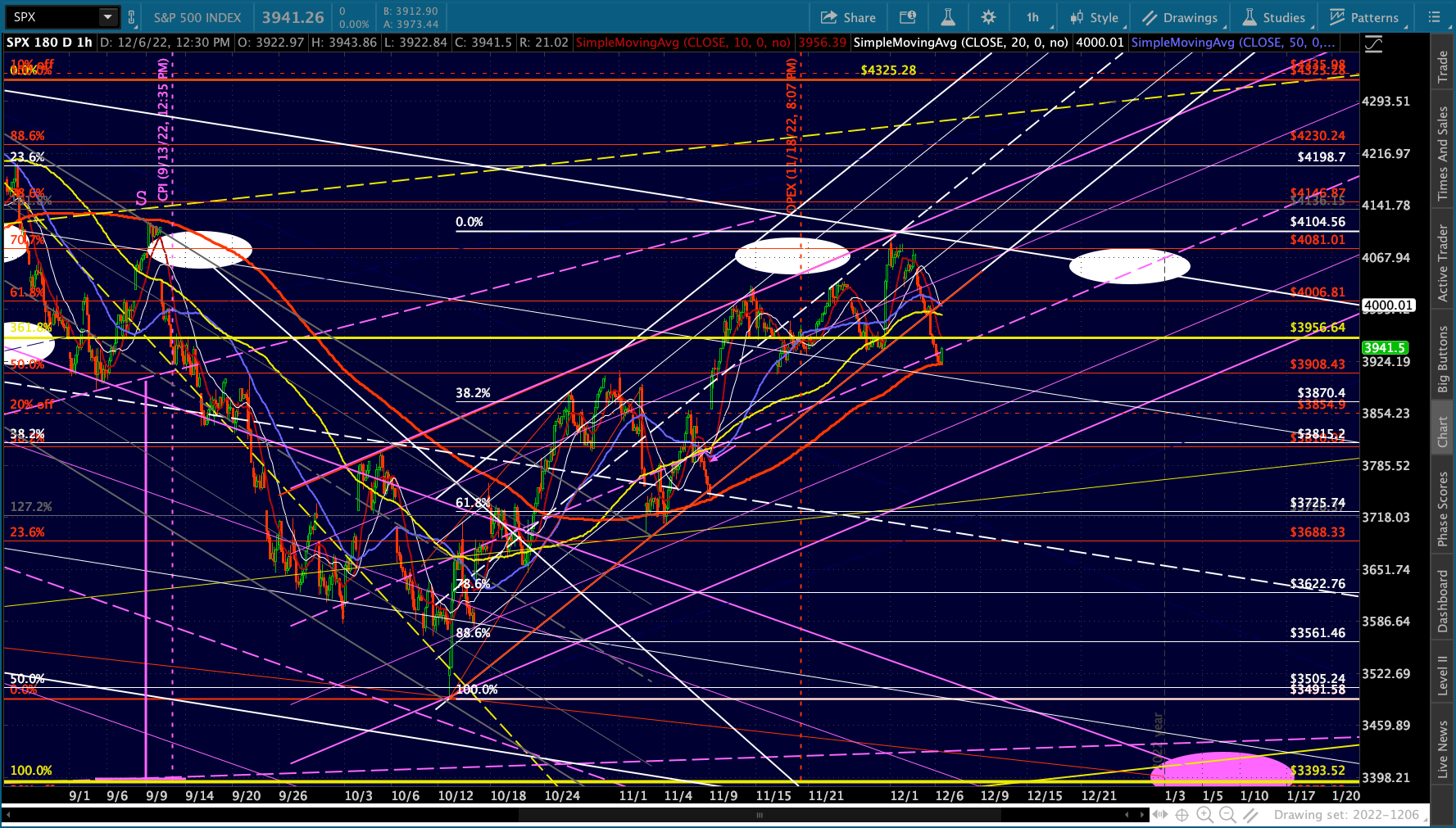

Note that the rising white channel is now out of the picture, leaving the purple one as a potential fallback position for the bulls.

Note that the rising white channel is now out of the picture, leaving the purple one as a potential fallback position for the bulls.

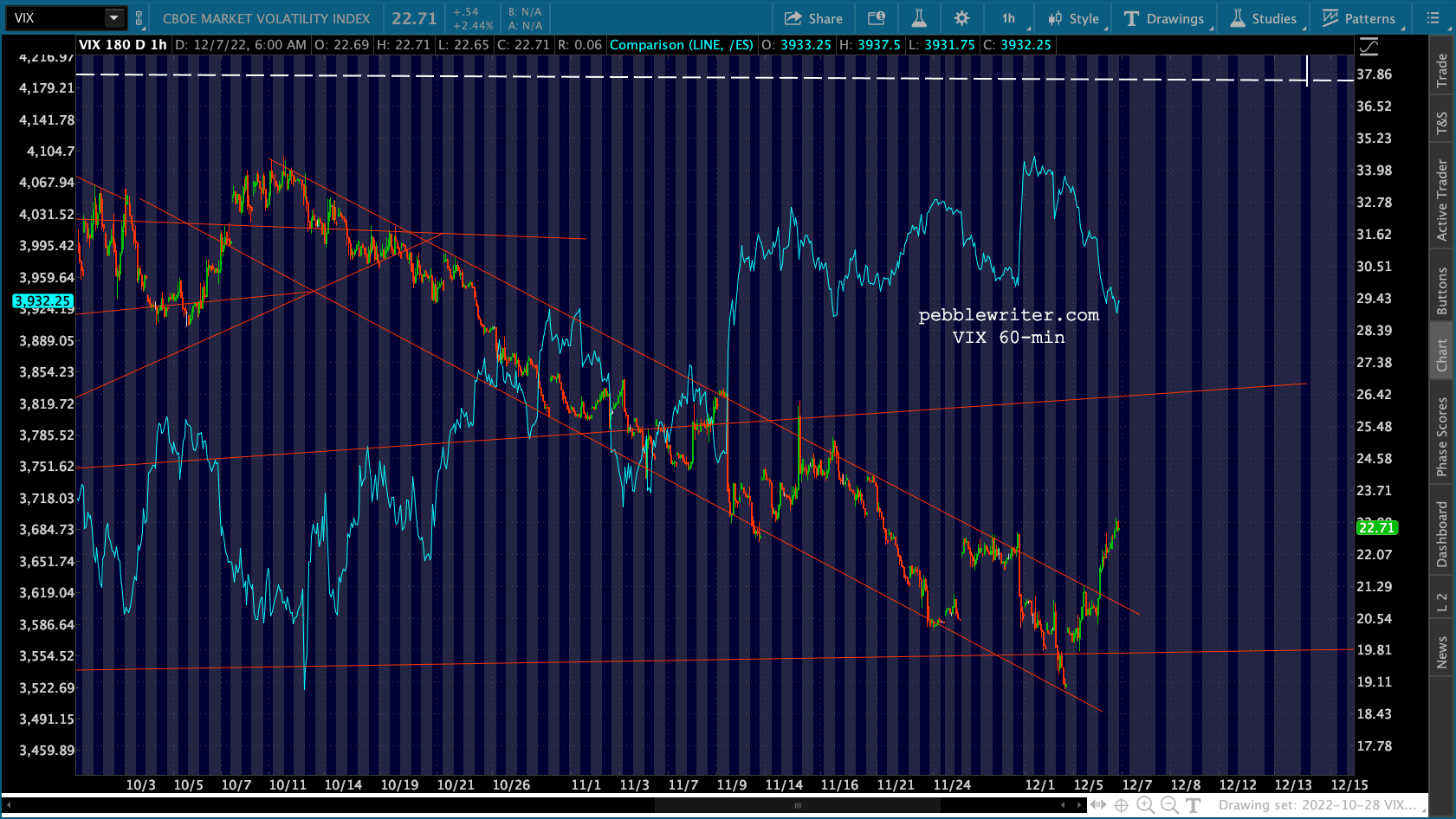

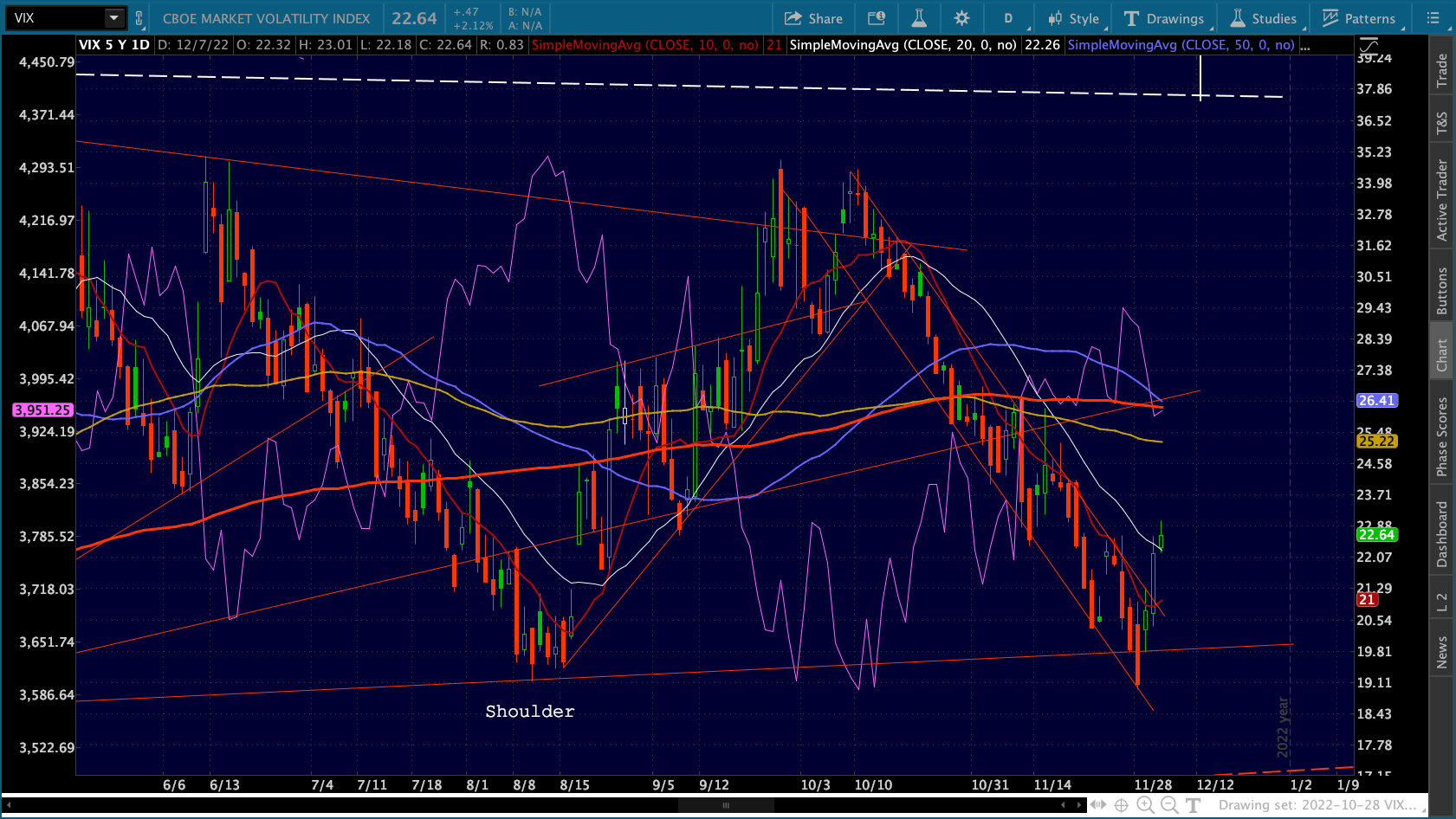

VIX has broken out of its falling red channel – a little more convincingly this time.

VIX has broken out of its falling red channel – a little more convincingly this time.  This puts it well above the red TL, an important sign for bears. At this point, the suggestion is that the breakdown was a “glitch” or, for the more cynical among you, a headfake designed to convince bears to ditch their puts before the downturn.

This puts it well above the red TL, an important sign for bears. At this point, the suggestion is that the breakdown was a “glitch” or, for the more cynical among you, a headfake designed to convince bears to ditch their puts before the downturn. It’s a bonus for bears that VIX has also pushed above its SMA20. If it can hold for a few more sessions, we’d even have a shot at a 10/20 cross.

It’s a bonus for bears that VIX has also pushed above its SMA20. If it can hold for a few more sessions, we’d even have a shot at a 10/20 cross.

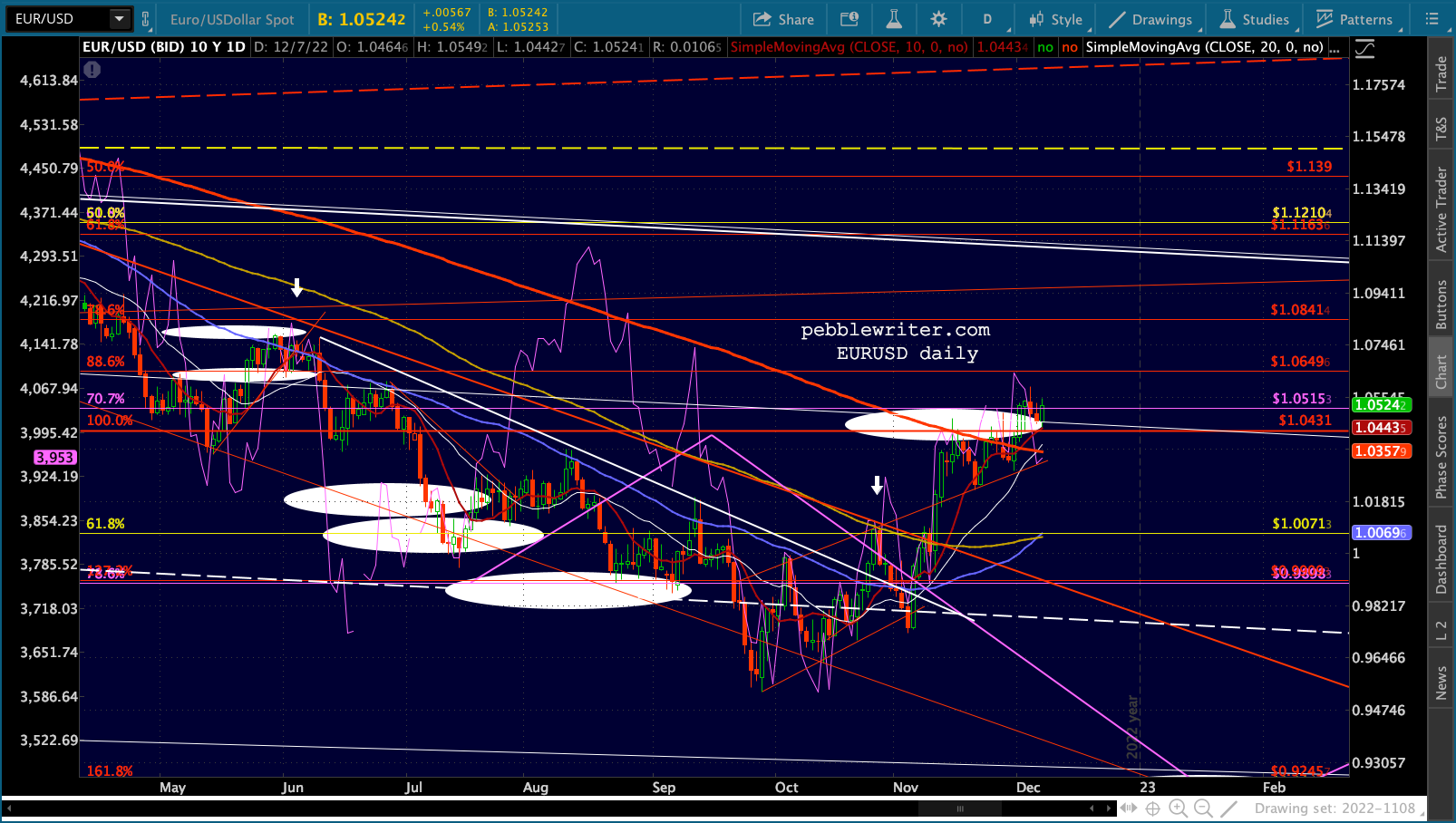

Currencies are fairly quiet this morning, with EURUSD getting a small bump but failing to notch new highs for the second session in a row.

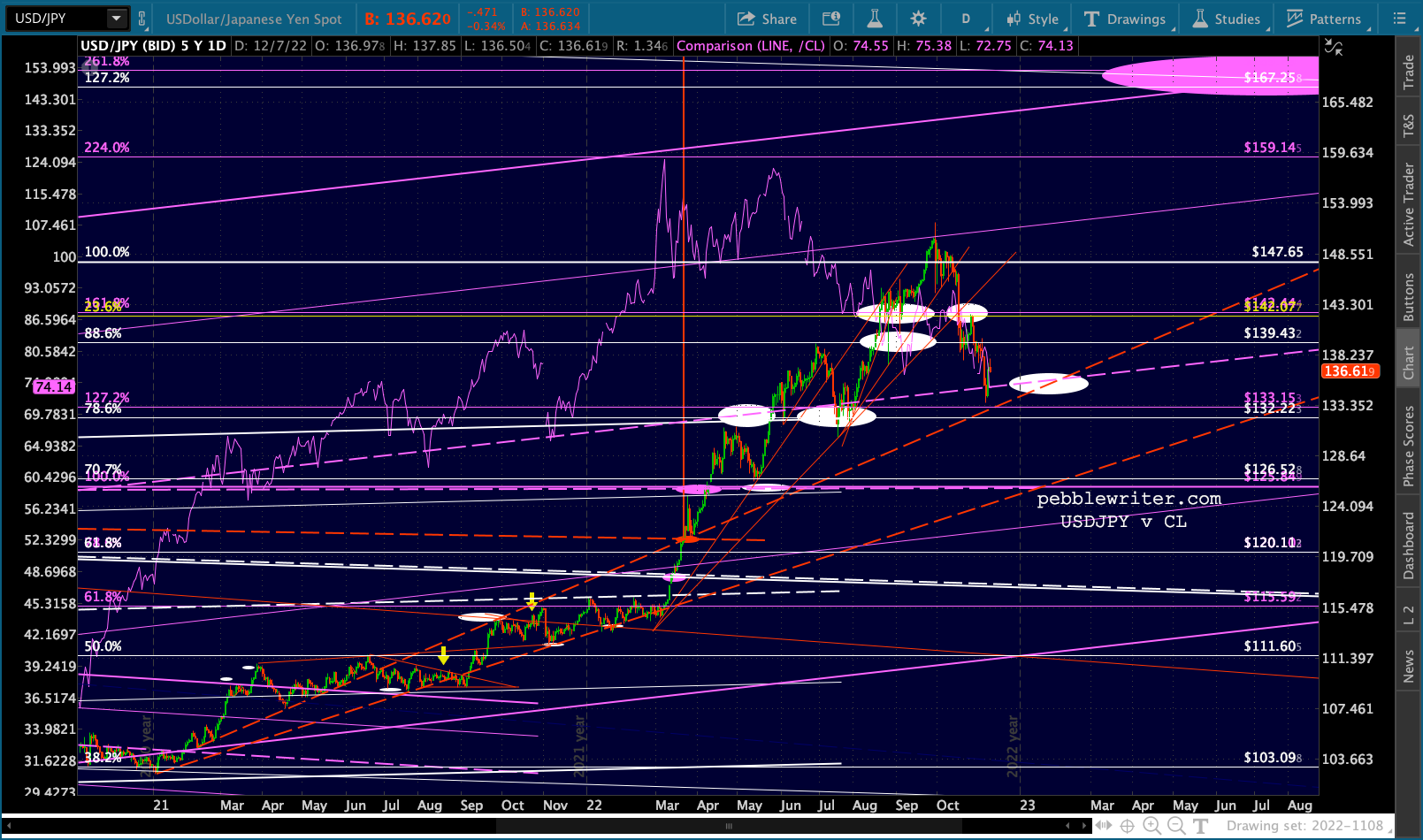

Currencies are fairly quiet this morning, with EURUSD getting a small bump but failing to notch new highs for the second session in a row.  USDJPY is off slightly, still holding the purple midline.

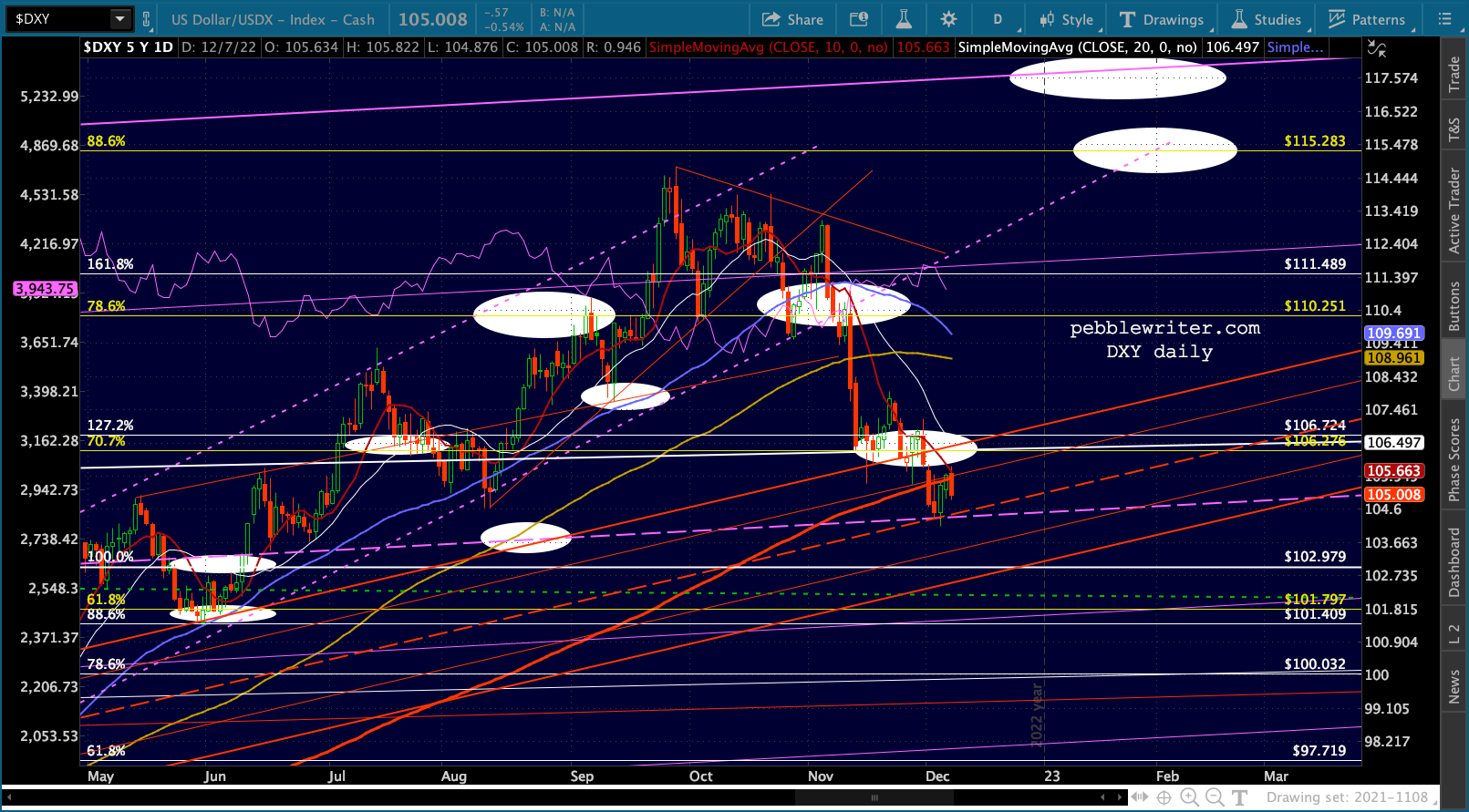

USDJPY is off slightly, still holding the purple midline. And, DXY is having a little trouble punching through the SMA200 and SMA10. I continue to expect it to rally nicely.

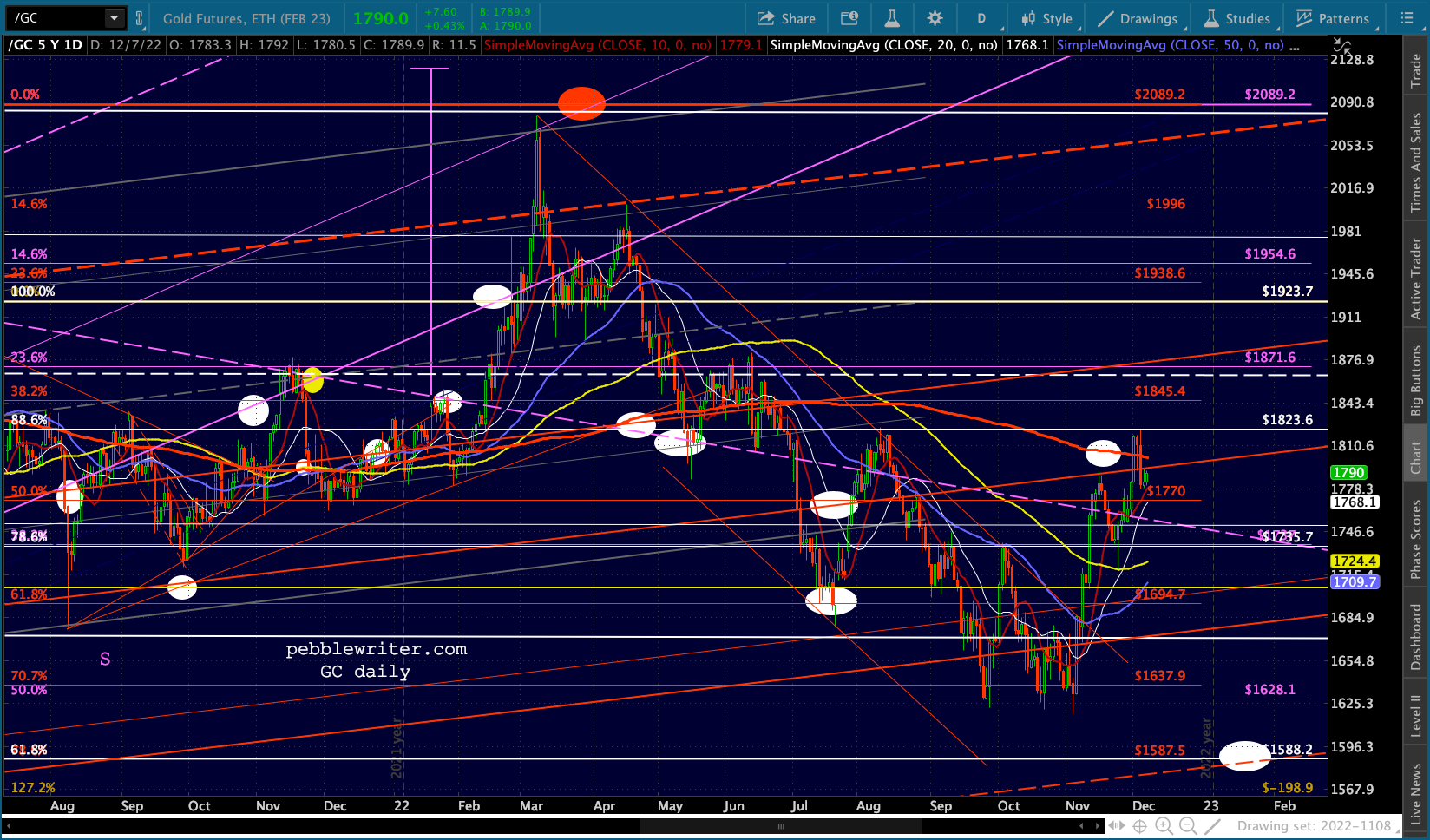

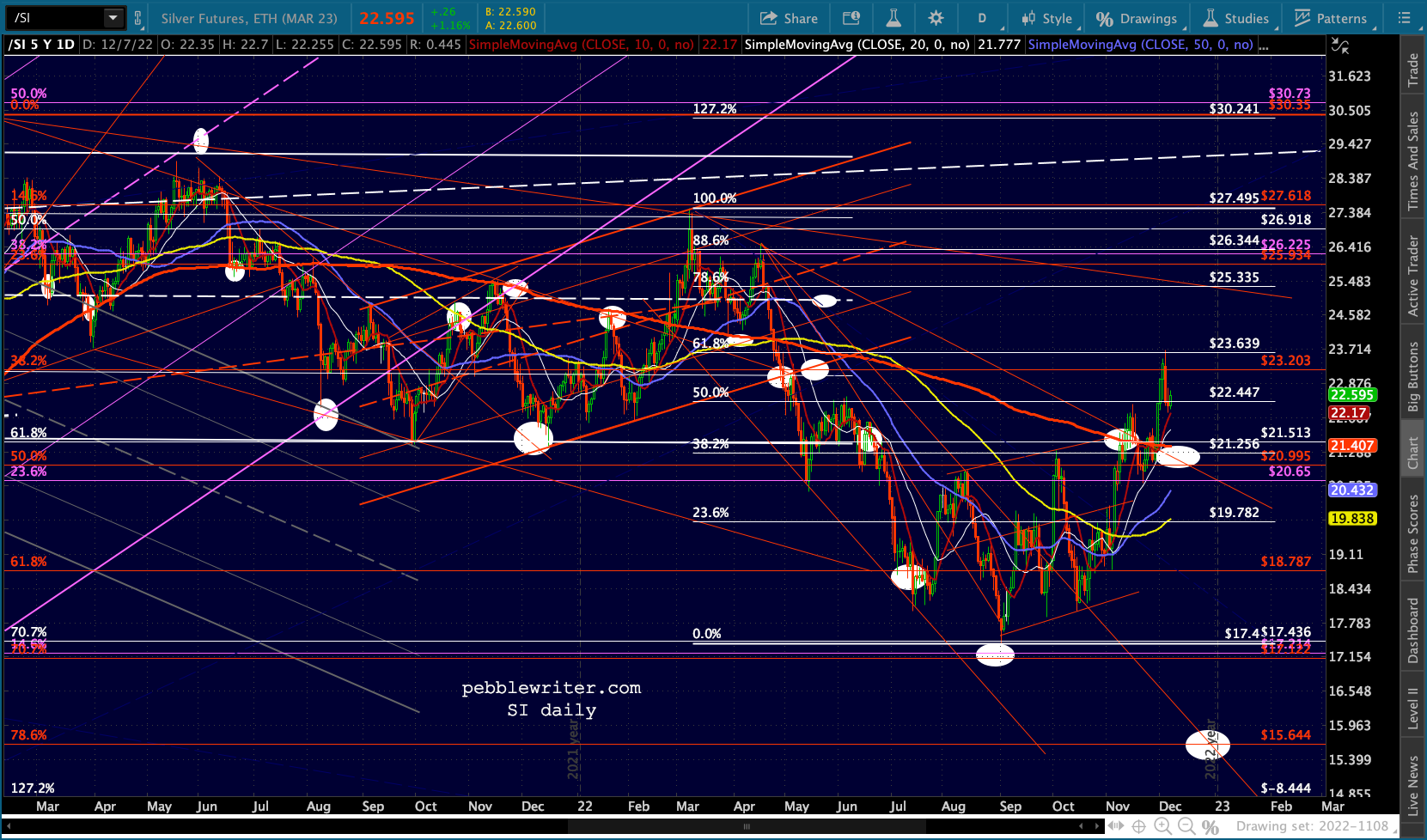

And, DXY is having a little trouble punching through the SMA200 and SMA10. I continue to expect it to rally nicely. This has left the door open for GC and SI to bounce off their SMA10s. No new highs, but it keeps the possibility alive.

This has left the door open for GC and SI to bounce off their SMA10s. No new highs, but it keeps the possibility alive.

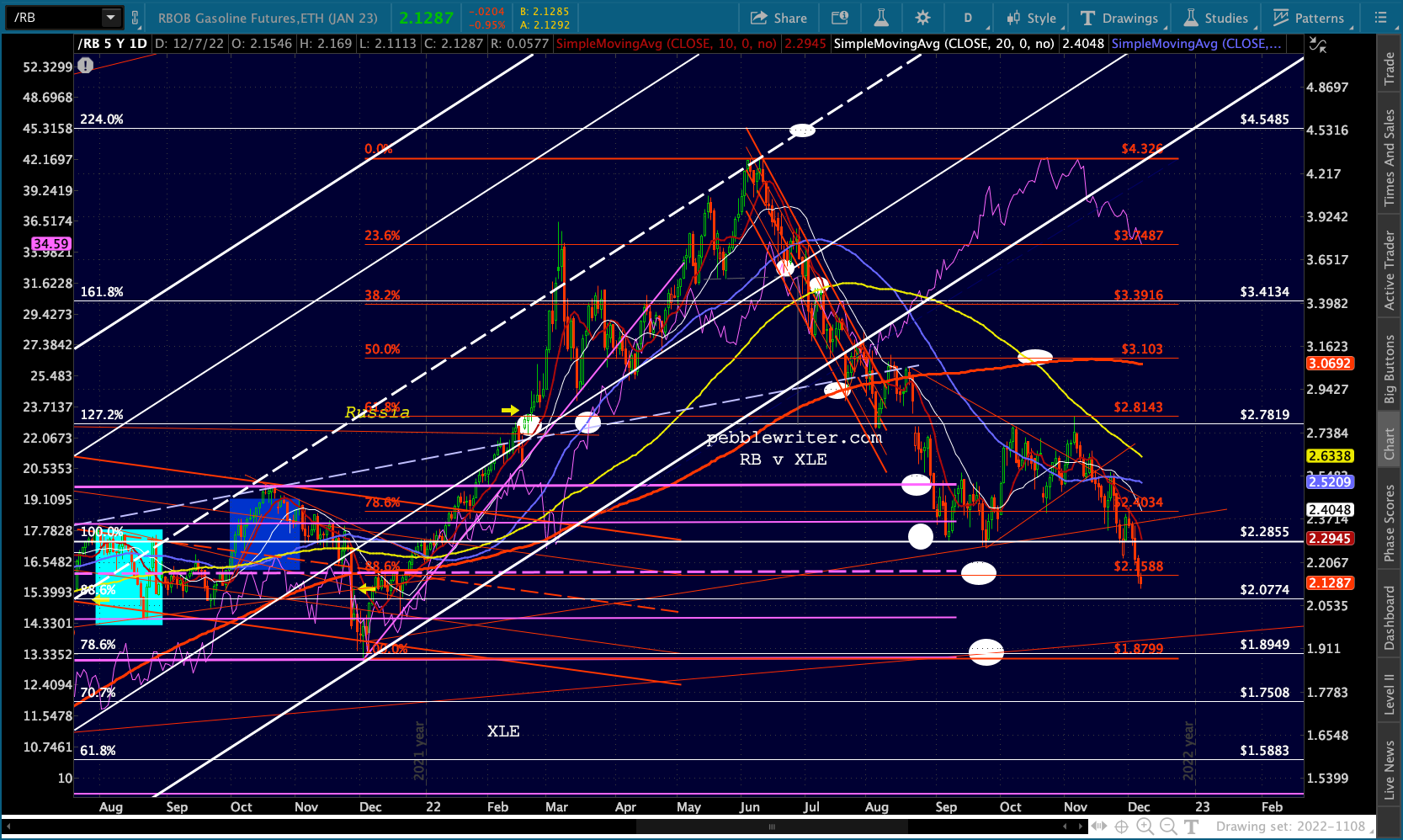

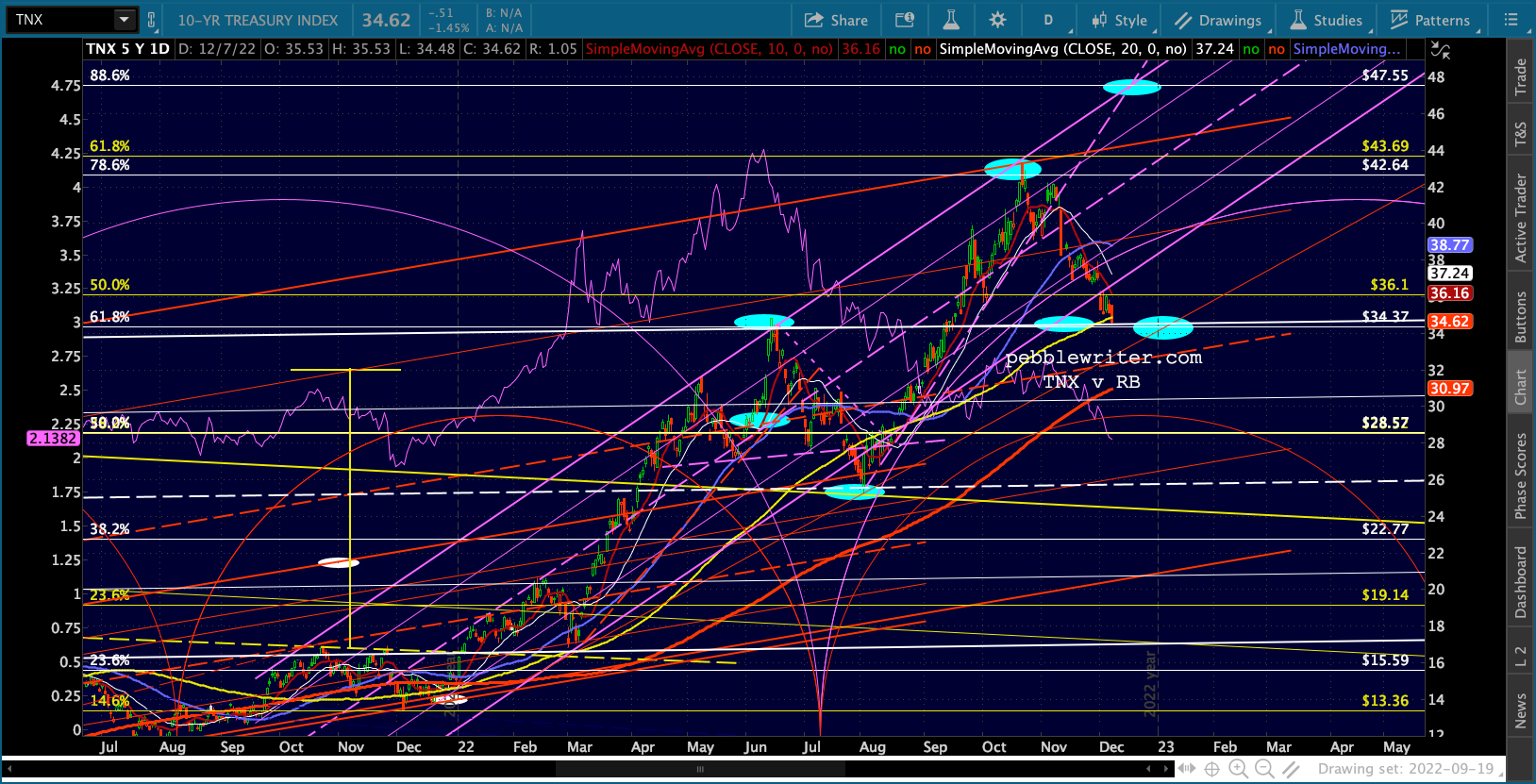

RB, which officially reached our 2.1588 target yesterday, is notching a new low. Still looking for 1.8949 or lower.

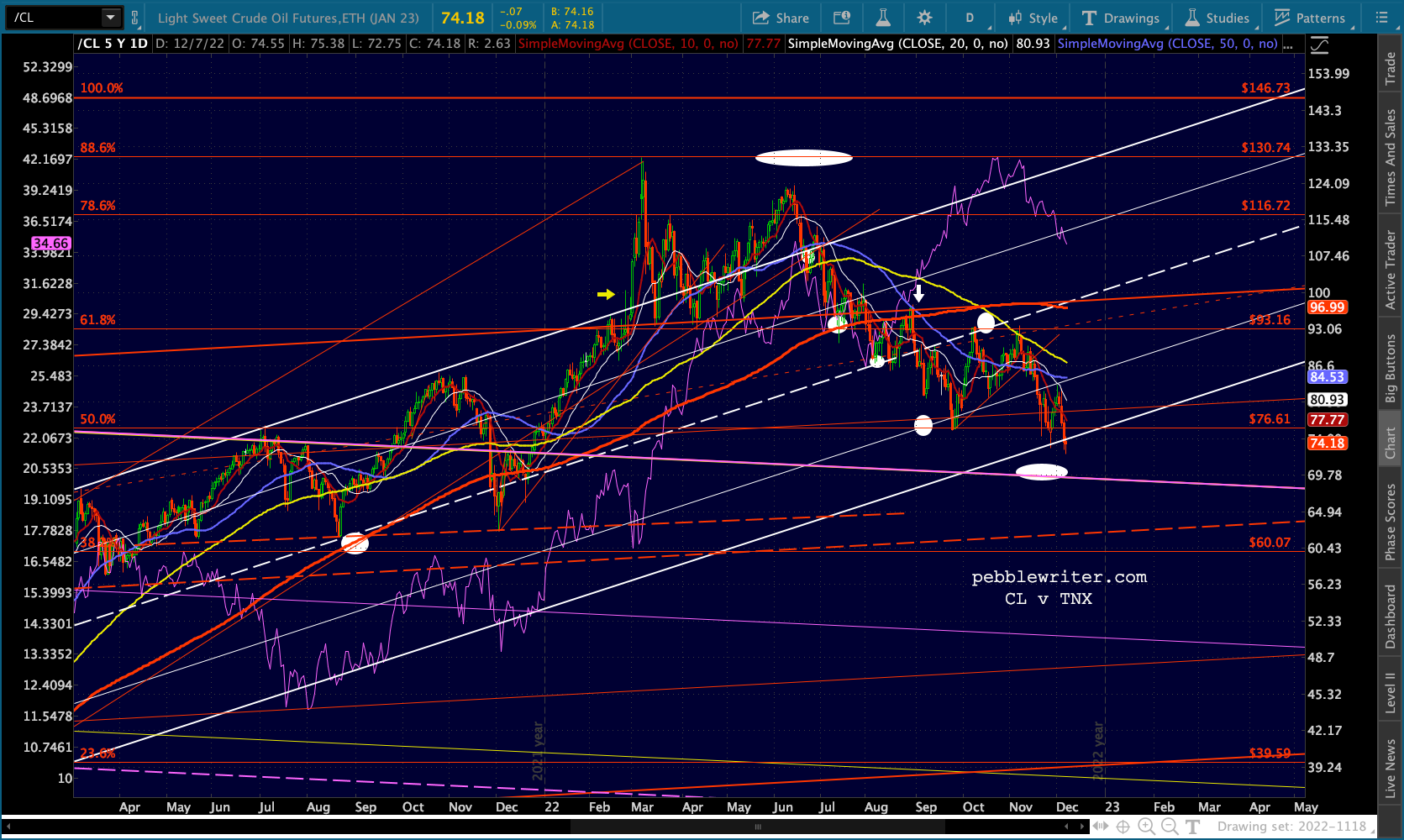

RB, which officially reached our 2.1588 target yesterday, is notching a new low. Still looking for 1.8949 or lower. And, CL is still bumping along the bottom of the rising white channel. As we discussed last week, this one is tricky as w push down to the backtest target at 69.50ish is still a good possibility.

And, CL is still bumping along the bottom of the rising white channel. As we discussed last week, this one is tricky as w push down to the backtest target at 69.50ish is still a good possibility.  The weakness in energy has helped TNX come very close to our 34.37 target. I originally placed it after year end because that’s when the SMA200 should intersect. A drop through 34.37 to tag the SMA200 sooner than that would fit with a December selloff.

The weakness in energy has helped TNX come very close to our 34.37 target. I originally placed it after year end because that’s when the SMA200 should intersect. A drop through 34.37 to tag the SMA200 sooner than that would fit with a December selloff. In other words, timing remains a question mark.

In other words, timing remains a question mark.

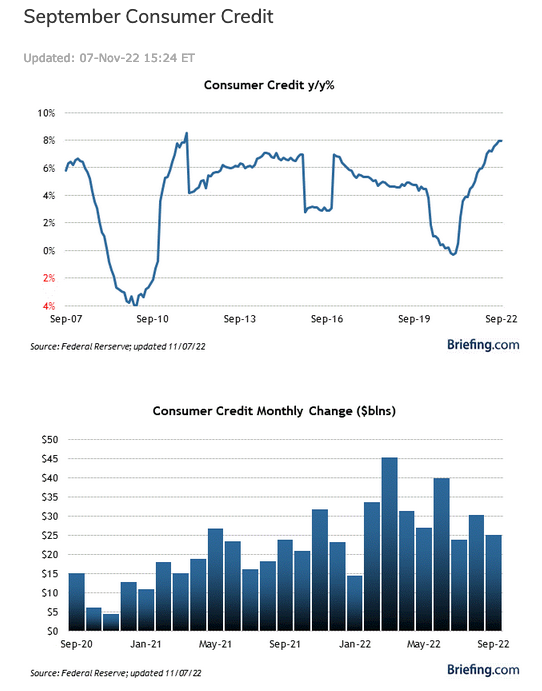

Consumer credit isn’t usually a market mover, but this afternoon’s print might ruffle some feathers. Higher levels of debt have gradually morphed from an indication of consumer strength to one of consumer debt burden in a rising interest rate environment.