Almost a year ago we noted that the rapidly rising price of oil and gas would contribute to alarming CPI prints [see: Don’t Ignore Inflation.]

Punch line? Oil and gas will have to fall significantly by April or we’re looking at a 20%+ YoY increase in gas prices – which has historically produced 2.4-2.7% annual inflation and a 2%+ 10Y.

At the time, it was clear that the base effect would ultimately generate YoY deltas in gasoline that would exceed 40% and, if the correlation held, generate CPI over 3.5%. We were being too conservative. November’s delta should be around 62% and October CPI reached 6.22%.

Then…

…and now.

When inflation spilled over into stickier categories such as food, shelter and wages, CPI accelerated more than the rise in oil/gas prices alone would justify. As the chart above illustrates, CPI’s rate of change outpaced that of gasoline alone.

When inflation spilled over into stickier categories such as food, shelter and wages, CPI accelerated more than the rise in oil/gas prices alone would justify. As the chart above illustrates, CPI’s rate of change outpaced that of gasoline alone.

Investors finally began to notice. Maybe inflation wasn’t transitory after all. Rising interest rates suddenly became a concern rather than a bullish confirmation of the reflation trade.

In our last update on oil and gas [see: Nov 19 Update] we reiterated the fact that oil and gas deltas would need to be held in check if inflation and interest rates were to stabilize.

Regardless of where this correction peters out, November should mark a turning point in CPI, with December and future months declining back towards an “acceptable” level. The trick is to keep interest rates from breaking out, which means the Fed must put the brakes on inflation right here and now.

Friday’s plunge was a good start. CL came within 0.8% of our downside target, shedding nearly 14% on the day and over 21% from its October highs.

It’s too early to say whether the omicron variant will feature the sort of transmission and mortality rates that could send the global economy into another tailspin. But, one thing is clear: non-OPEC+ countries are breathing a sigh of relief at the correction in energy prices – even if it means more downside for equities.

It’s too early to say whether the omicron variant will feature the sort of transmission and mortality rates that could send the global economy into another tailspin. But, one thing is clear: non-OPEC+ countries are breathing a sigh of relief at the correction in energy prices – even if it means more downside for equities.

continued for members…

First, a quick roundup of the markets…

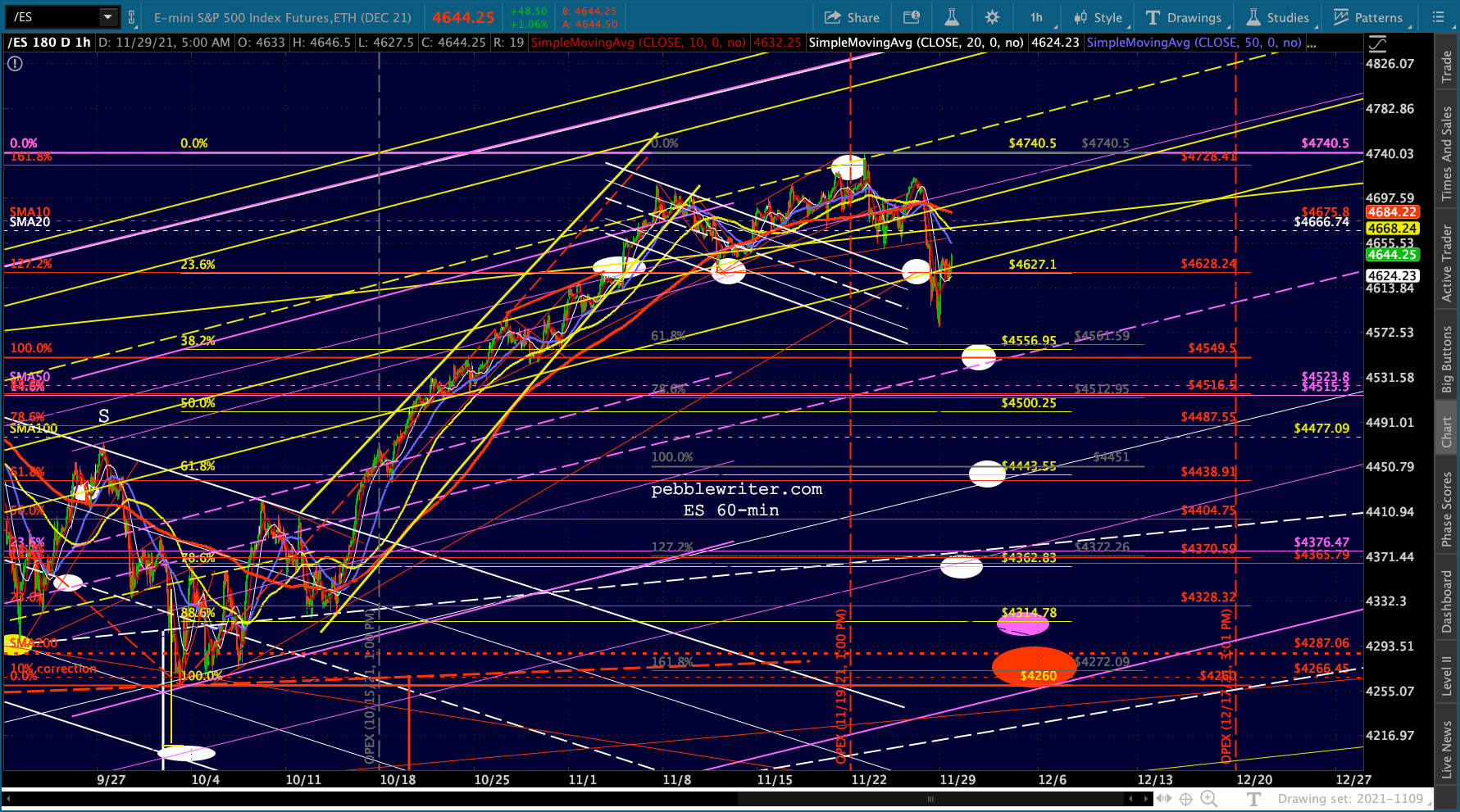

ES completed a small H&S pattern that targets 4563 – about where the SMA50 will be in a few days. Last night’s rally looks like a pop and drop to me.

The USDJPY is getting a slight bounce off its SMA50…

The USDJPY is getting a slight bounce off its SMA50… …but the DXY is still picking up momentum from the euro.

…but the DXY is still picking up momentum from the euro.

Last, BTC officially tagged our cloud bottom target yesterday.

Last, BTC officially tagged our cloud bottom target yesterday. Okay, back to oil and gas…

Okay, back to oil and gas…

As we pointed out last week, the 10Y is under significant pressure. October inflation came in at 6.22%, so the Fed had no choice but to announce a taper and eventual increase in interest rates.

They have no interest, however, in raising rates. With $30 trillion (and growing) in debt, higher rates are a recipe for disaster. Japan and the ECB learned this, which is why their rates are at or below zero. Ours will surely follow suit if only the Fed can engineer it. The solution is keeping oil and gas prices under control.

As in October 2018, the Fed knows that a good crisis should never be wasted. The omicron variant might or might not be crisis-worthy, but it will do until something else comes along.

The last time RB traded at Friday’s lows was in late April, when gas prices were around 2.77. If prices were to fall to 2.77 in December, the YoY delta in gas prices would be 37% versus November’s estimated 62%. All else being equal, this would bring CPI down to the 3-4% range. But, everything else isn’t equal. Unless omicron results in a serious slowdown, those other, stickier categories are going to be with us for a while.

November inflation should be above 6.2%, probably closer to 6.5%. The type of decline we’ve seen so far in gasoline would reduce December CPI to closer to 4.5 – 5.5%. This would be preferable to a sudden plunge to, say 3%, which would probably raise fears over economic stagnation. What then, is the optimal solution?

A slow, steady decrease in inflation which would get inflation back down to 2% by the time the taper is completed and, thus, eliminate the calls for interest rate hikes.

Easier said than done, right? Not necessarily. In a sense, inflation is a math problem. It focuses on month-to-month and year-to-year increases in prices. So, if gasoline prices were to flatline at current prices, we would see the YoY delta close in on zero a year from now.

The chart below assumes the price of 2.77 per gallon going forward. As it turns out, we needn’t wait a full year for the YoY delta to reach zero. Gas prices averaged 2.77 in April 2020. So, with this example, we could get to a YoY delta of 0% by April 2022 when the taper schedule still calls for $45 billion in purchases.

I find this model appealing as it would permit a .75% monthly drop in CPI, targeting 2% for April – May. This would require that the current spread between Gas and CPI remains constant. If, instead, inflation were to continue rising until the middle of 2022 as Powell recently stated then the math is all off.

My model indicates that a delta of 5-10% is most compatible with 2% CPI. If the delta reached zero in Apr 22 and turned negative thereafter, then inflation would likely drop below 2%. One way to avoid such an outcome would be for gas prices to begin a .10 rise each month beginning in April. The outcome would look something like this.

There’s always a lag in between futures prices and retail prices. So, I’m not suggesting that retail prices will necessarily drop to 2.77 overnight. But, if RB stabilizes in the current range, then they should gradually drop to that vicinity.

There’s always a lag in between futures prices and retail prices. So, I’m not suggesting that retail prices will necessarily drop to 2.77 overnight. But, if RB stabilizes in the current range, then they should gradually drop to that vicinity.

An aside – note that RB’s lows have been followed by significant highs almost exactly one year later. The white pattern ran from Mar 23, 2020 to Mar 12, 2021 – missing the one year anniversary by only 6 sessions. The yellow pattern ran from Nov 2, 2020 to Oct 21, 2021, 8 sessions away from exactly one year. The RB charts currently indicate a potential drop to 1.56-1.75, which would put retail prices closer to 2.25-2.40 – about where they were in Jan-Feb 2021. Obviously, this is a more bearish scenario that would likely mean the omicron situation gets much worse in the near term.

The RB charts currently indicate a potential drop to 1.56-1.75, which would put retail prices closer to 2.25-2.40 – about where they were in Jan-Feb 2021. Obviously, this is a more bearish scenario that would likely mean the omicron situation gets much worse in the near term.

I’ll stick with the CL target prices for now with a note to self to reevaluate downside targets once DXY reaches 97.73.