For months we’ve been warning about the coming inflation problem, wondering when the bond market would notice and/or care. The immediate problem in a nutshell:

One of the most highly correlated components of CPI with the headline rate is the price of energy, and gasoline in particular. If prices were to remain where they are now, the base effect will result in a 40% increase YoY in April. Historically, this has produced headline CPI in excess of 2.5%. The Fed points out this base effect bump will be transitory and should be ignored, but the recent rise in interest rates tells us that the bond market is not ignoring it. In fact, recent beats in economic data and sharp price increases across the commodity complex underscore the notion that the rise in inflation will not be transitory. The pop we could see in April would be only the beginning.

The Fed points out this base effect bump will be transitory and should be ignored, but the recent rise in interest rates tells us that the bond market is not ignoring it. In fact, recent beats in economic data and sharp price increases across the commodity complex underscore the notion that the rise in inflation will not be transitory. The pop we could see in April would be only the beginning.

As we approach $30 trillion in debt with more stimulus on the way, markets have to wonder what to make of CPI of 2.5-3.0% or higher. In our opinion, the US has no choice but to follow in the BoJ’s and ECB’s footsteps and repudiate higher rates until the end of time.

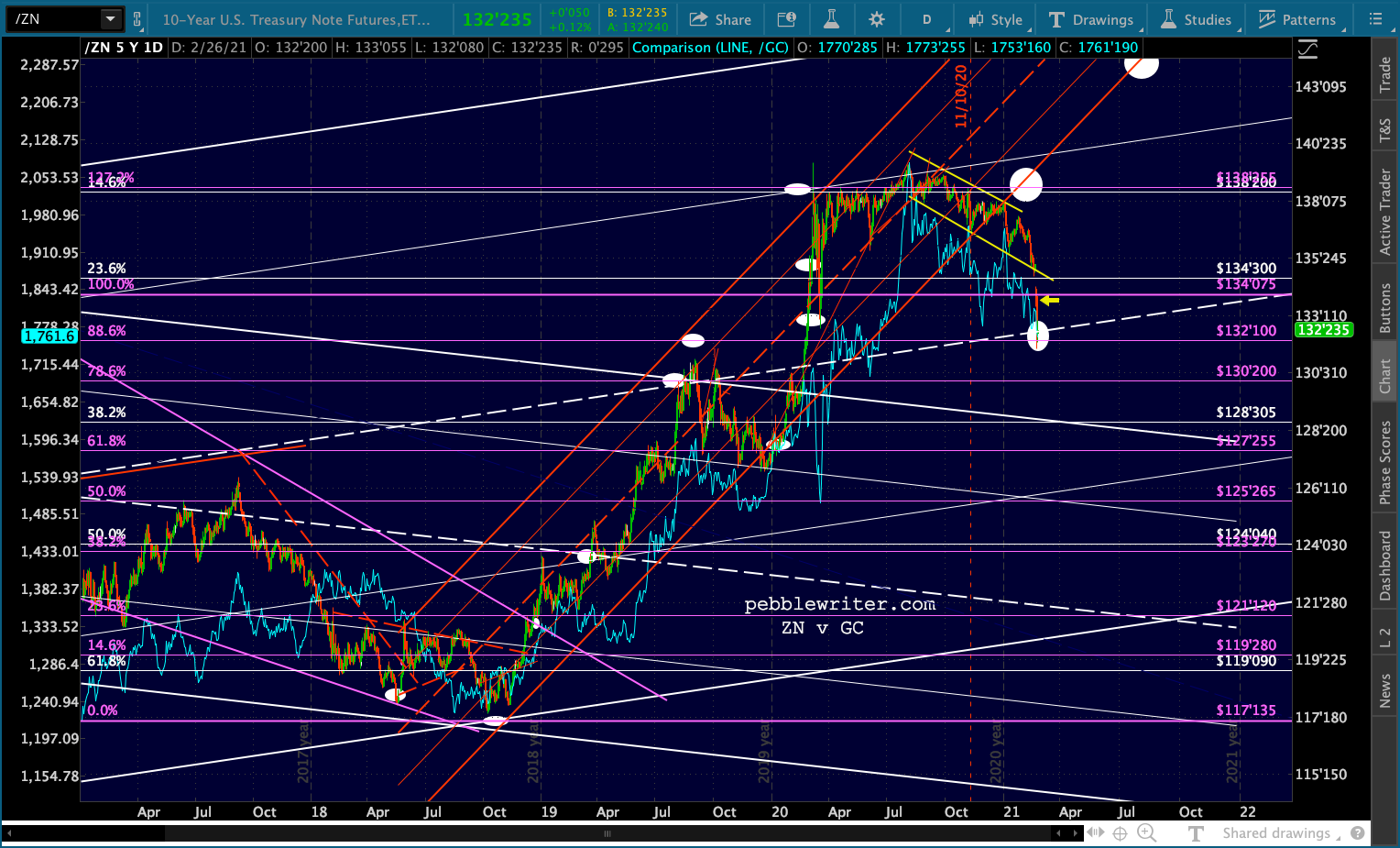

10Y note futures reached a level at which we have felt would represent critical support. A drop below this level, we reasoned, would sound loud alarm bells. As we wrote yesterday: “This is quite possibly the Fed’s last chance to avoid a real mess in the bond market.”

Bottom line, don’t be fooled by the Fed’s ability to repeatedly bail out equities at the last minute.

Bottom line, don’t be fooled by the Fed’s ability to repeatedly bail out equities at the last minute.

The algos have learned well to respond to moves in VIX, currencies and oil/gas when they are so instructed. It’s no surprise that yesterday’s plunge was arrested at our previous SMA downside target.

The algos have learned well to respond to moves in VIX, currencies and oil/gas when they are so instructed. It’s no surprise that yesterday’s plunge was arrested at our previous SMA downside target.

The problem is bigger and more difficult to cope with than most – including, apparently, the Fed – can imagine.

The problem is bigger and more difficult to cope with than most – including, apparently, the Fed – can imagine.

continued for members…

There is still a possibility that SPX’s 3.618 at 3956.64 will be tagged. But, it’s looking more and more as though it’s just not worth the energy to boost it back up there. I’m focused more on the downside targets shown below.

VIX is again on the verge of a bullish (bearish for stocks) 10/20 cross. Another breakout of the falling white channel would be problematic for stocks.

VIX is again on the verge of a bullish (bearish for stocks) 10/20 cross. Another breakout of the falling white channel would be problematic for stocks.

Likewise, USDJPY could help a lot if it were to pop up through our 106.48 resistance.

Likewise, USDJPY could help a lot if it were to pop up through our 106.48 resistance. As suspected, yesterday’s breakout in EURUSD was a headfake. It should catch down to the rising SMA200 in the next week or so.

As suspected, yesterday’s breakout in EURUSD was a headfake. It should catch down to the rising SMA200 in the next week or so.  This should be constructive for DXY, even as rates moderate somewhat.

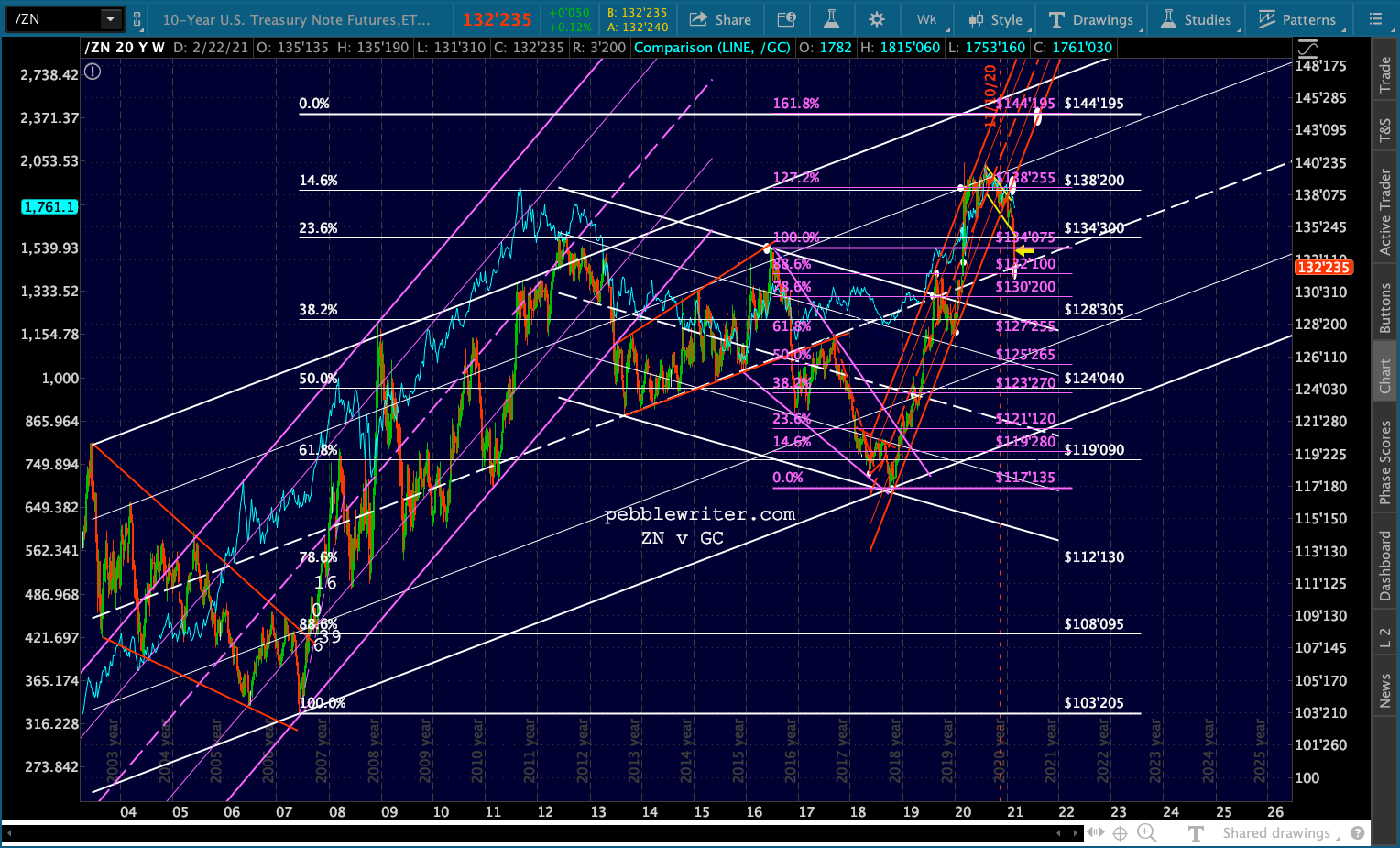

This should be constructive for DXY, even as rates moderate somewhat.  Speaking of rates, remember the weekly chart illustrates the risk of the Fed not catching this particular knife. A drop through the white midline would open ZN up to a 3-8% loss.

Speaking of rates, remember the weekly chart illustrates the risk of the Fed not catching this particular knife. A drop through the white midline would open ZN up to a 3-8% loss.

Examined from the standpoint of TNX, we can see backtests of the 2012 and 2016 lows, but also a backtest of the white flag pattern that guided rates sideways between 2013-2020. It remains my view that the Fed has no interest in letting rates “normalize.”

Examined from the standpoint of TNX, we can see backtests of the 2012 and 2016 lows, but also a backtest of the white flag pattern that guided rates sideways between 2013-2020. It remains my view that the Fed has no interest in letting rates “normalize.”

The relationship beween TNX and CL has never been more clear.

The relationship beween TNX and CL has never been more clear.  As we wrap up February, the monthly YoY gains in oil and gas will begin to matter. While CL and RB have risen further than I expected, it should be all downhill from here.

As we wrap up February, the monthly YoY gains in oil and gas will begin to matter. While CL and RB have risen further than I expected, it should be all downhill from here.

This should put a serious dent in the reflation trade narrative upon which equities have been so reliant.

This should put a serious dent in the reflation trade narrative upon which equities have been so reliant.

UPDATE: 11:00 AM

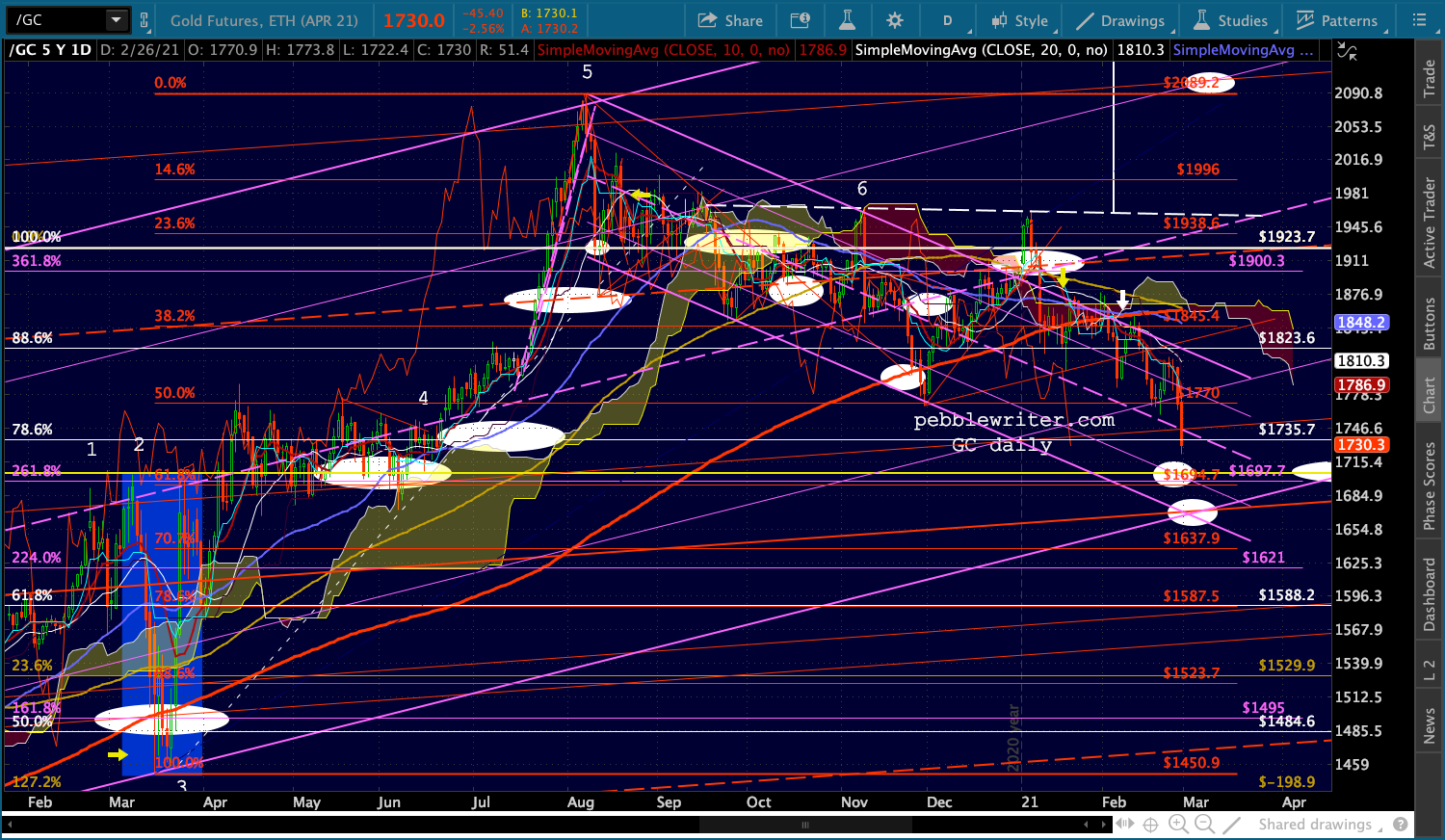

Not surprisingly, ZN’s demise has enabled another downward leg in GC – which should reach 1705 or 1670 target in the very near future.

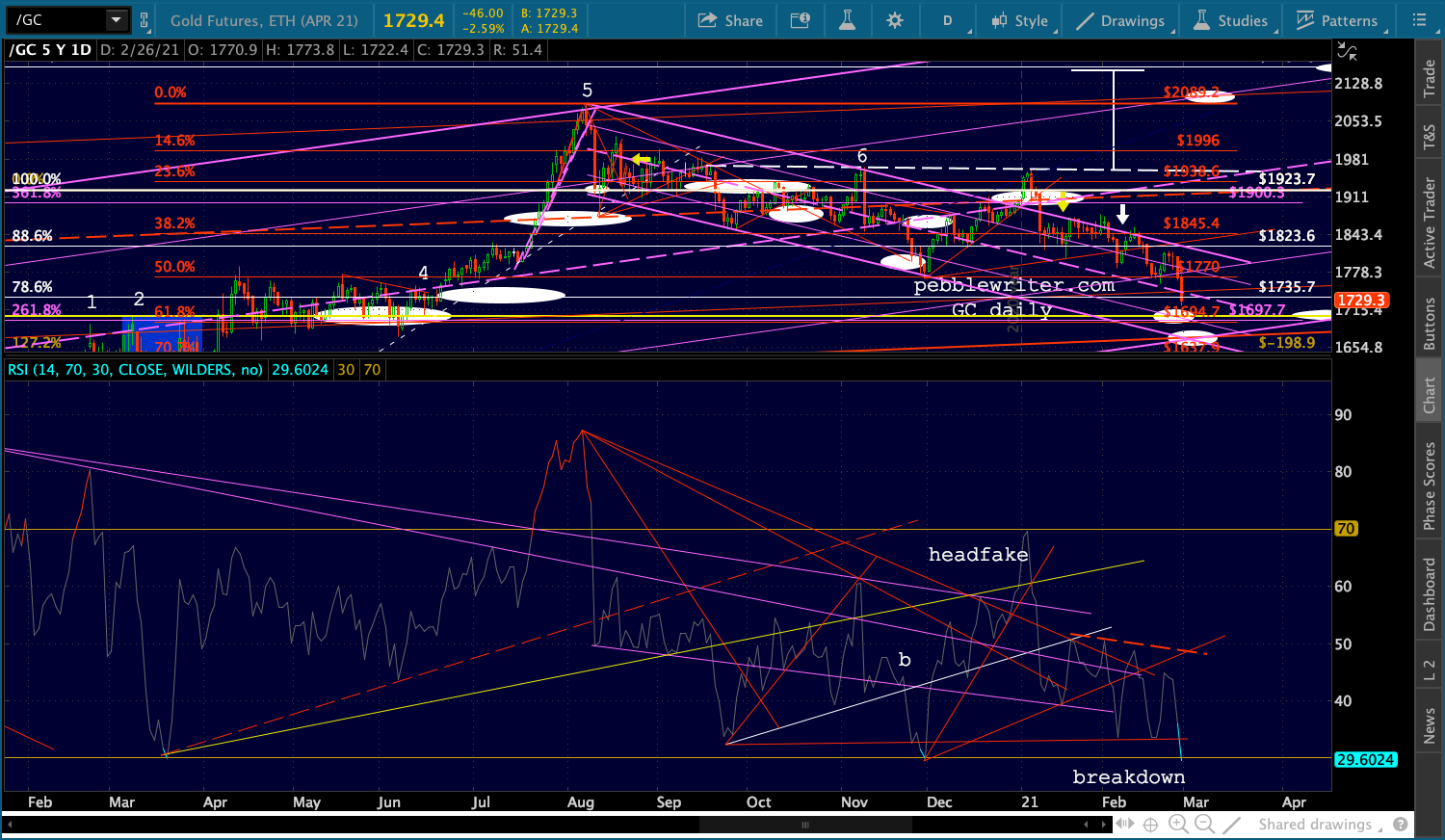

Big test here for GC’s RSI…

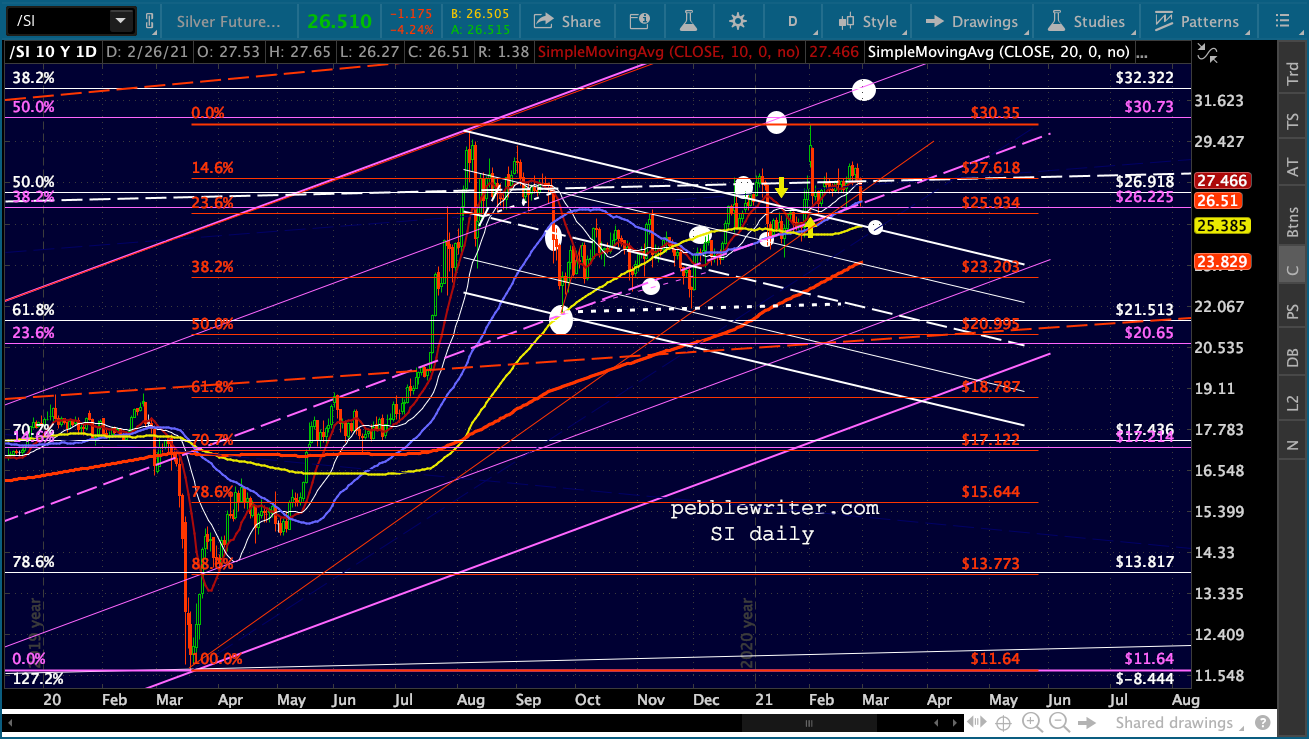

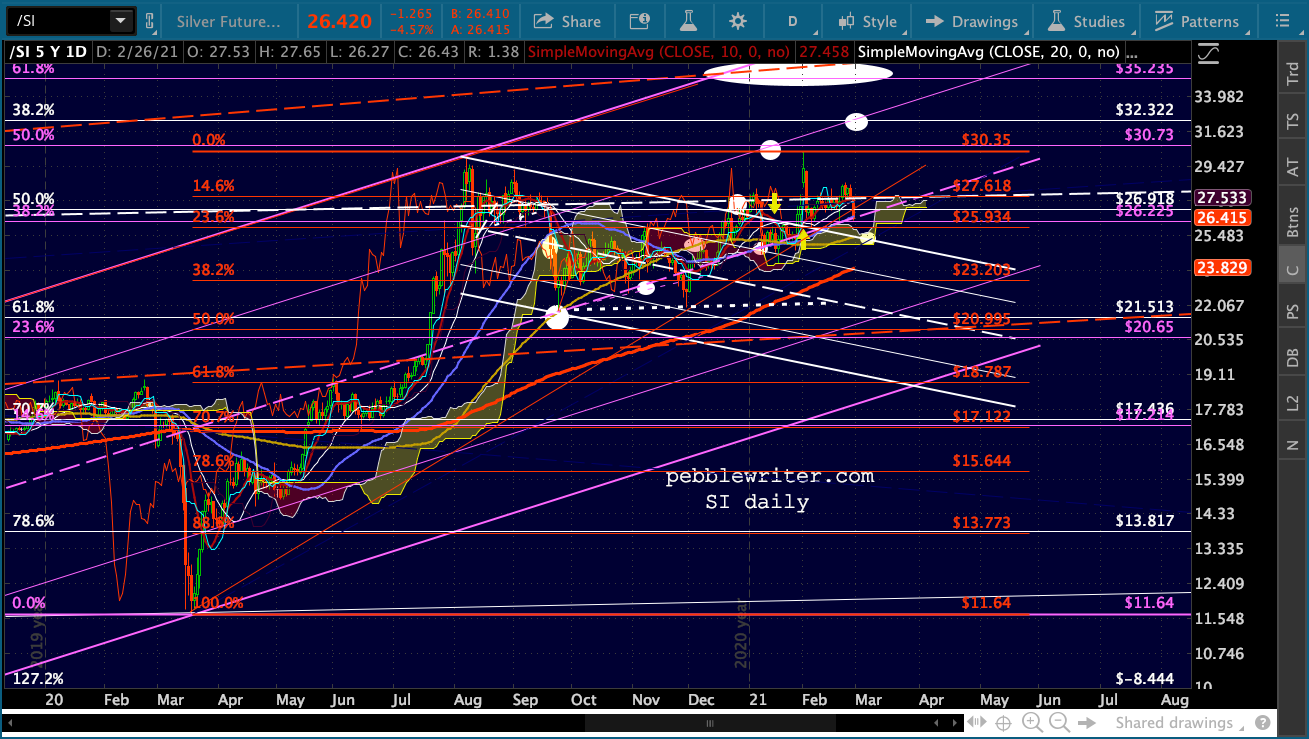

Big test here for GC’s RSI… While SI is suffering more on a percentage basis, it is backtesting. So, it’s situation is somewhat less dire. Still looking for a backtest of its SMA100 and cloud. Should that fail, its SMA200.

While SI is suffering more on a percentage basis, it is backtesting. So, it’s situation is somewhat less dire. Still looking for a backtest of its SMA100 and cloud. Should that fail, its SMA200.

Like GC, its RSI chart suggests this is important support.

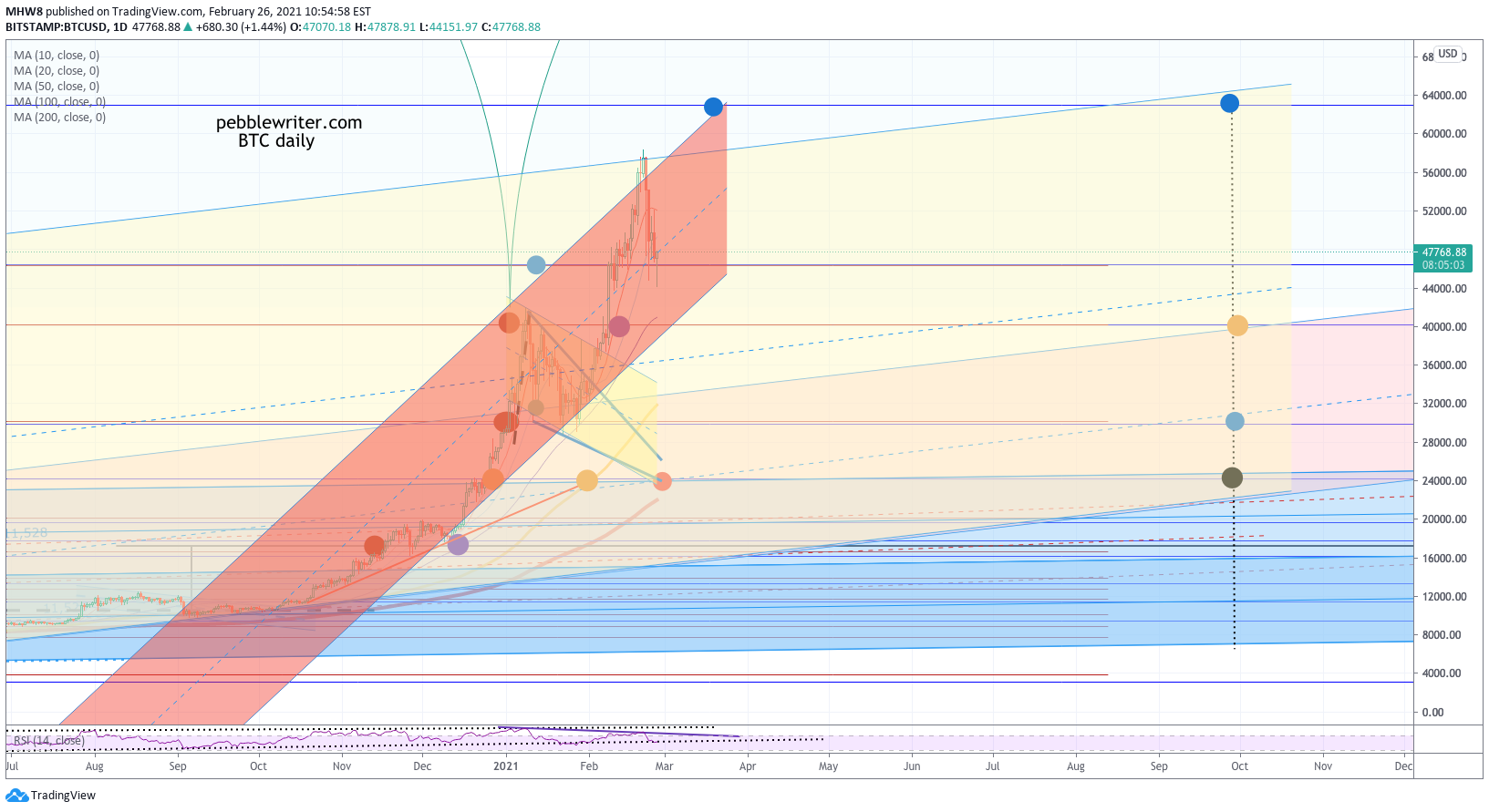

Like GC, its RSI chart suggests this is important support. BTC is flashing a similar situation, with RSI support a key consideration in keeping it from also dropping through its 2.24 Fib at 40,180.. Where’s Elon when you need him?

BTC is flashing a similar situation, with RSI support a key consideration in keeping it from also dropping through its 2.24 Fib at 40,180.. Where’s Elon when you need him?

UPDATE: 12:46 PM

No surprise, but SPX has regained its rising channel – which will probably expand to include the Oct 30 lows… …unless ES reverses here at its red channel .786 line…

…unless ES reverses here at its red channel .786 line…  …and VIX can rise back above its SMA200.

…and VIX can rise back above its SMA200.  USDJPY has broken above our next upside target, which opens up 106.92 and 107.20.

USDJPY has broken above our next upside target, which opens up 106.92 and 107.20. It’s been a long week with little sleep thanks to the new shoulder. I’m going to knock off early today and hope to have some extra energy for charting this weekend. Wishing everybody a safe and enjoyable weekend!

It’s been a long week with little sleep thanks to the new shoulder. I’m going to knock off early today and hope to have some extra energy for charting this weekend. Wishing everybody a safe and enjoyable weekend!