Futures remained slightly lower following lower than expected initial claims (709K vs 740K consensus) and CPI – which came in at 1.2% annual and 0.0% for October. Note that it took a plug number outlier +1.2% pop in electricity to keep CPI from going negative.

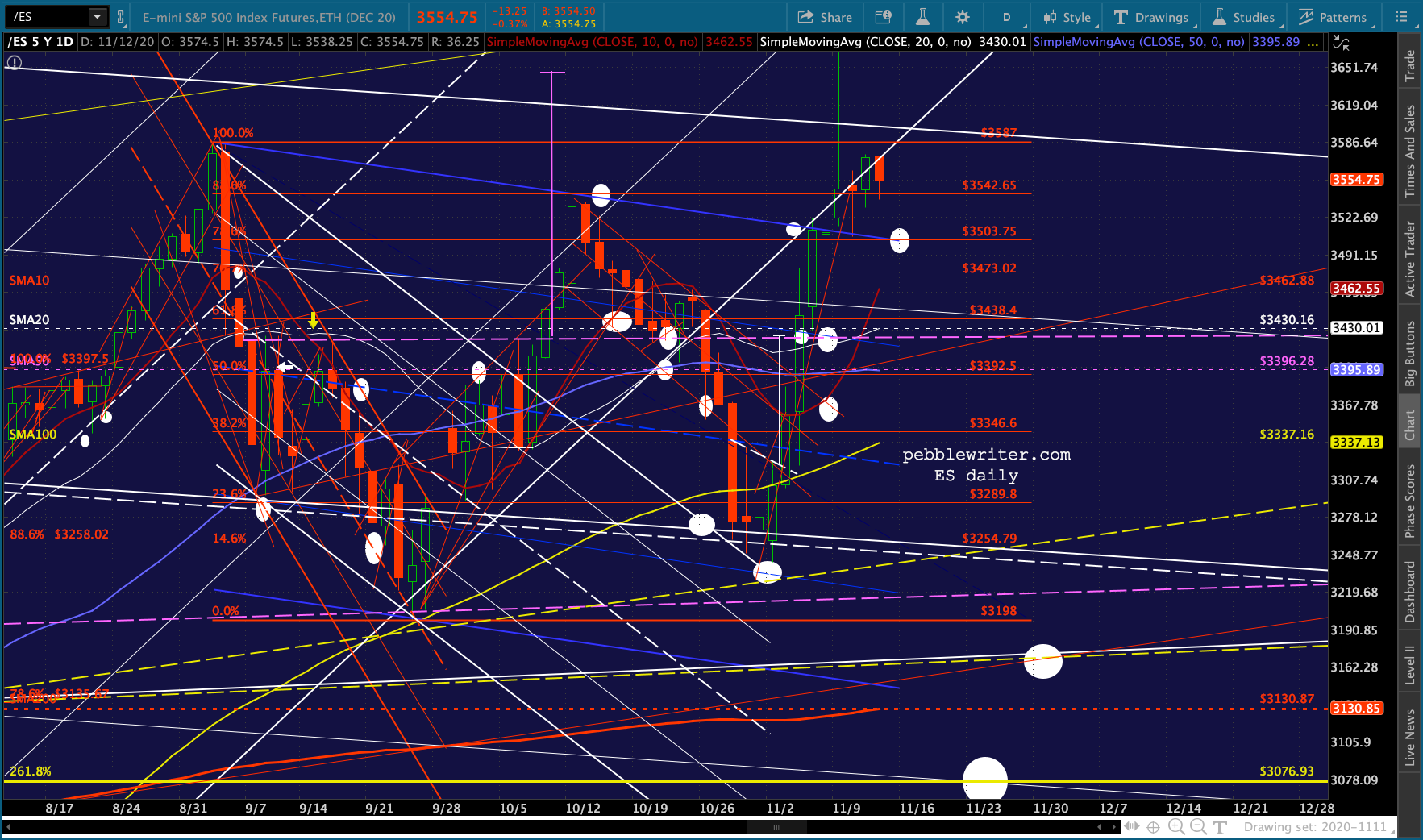

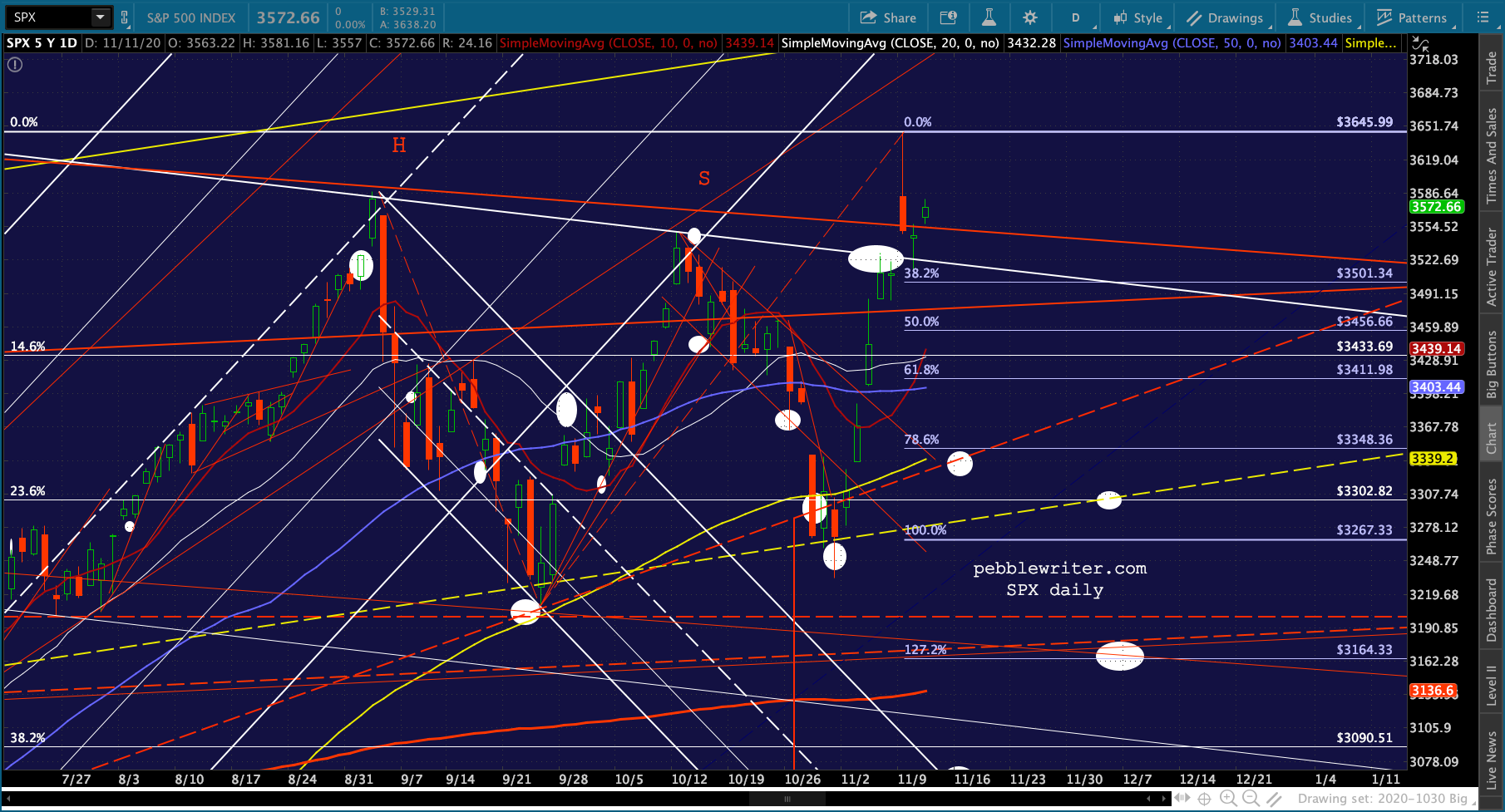

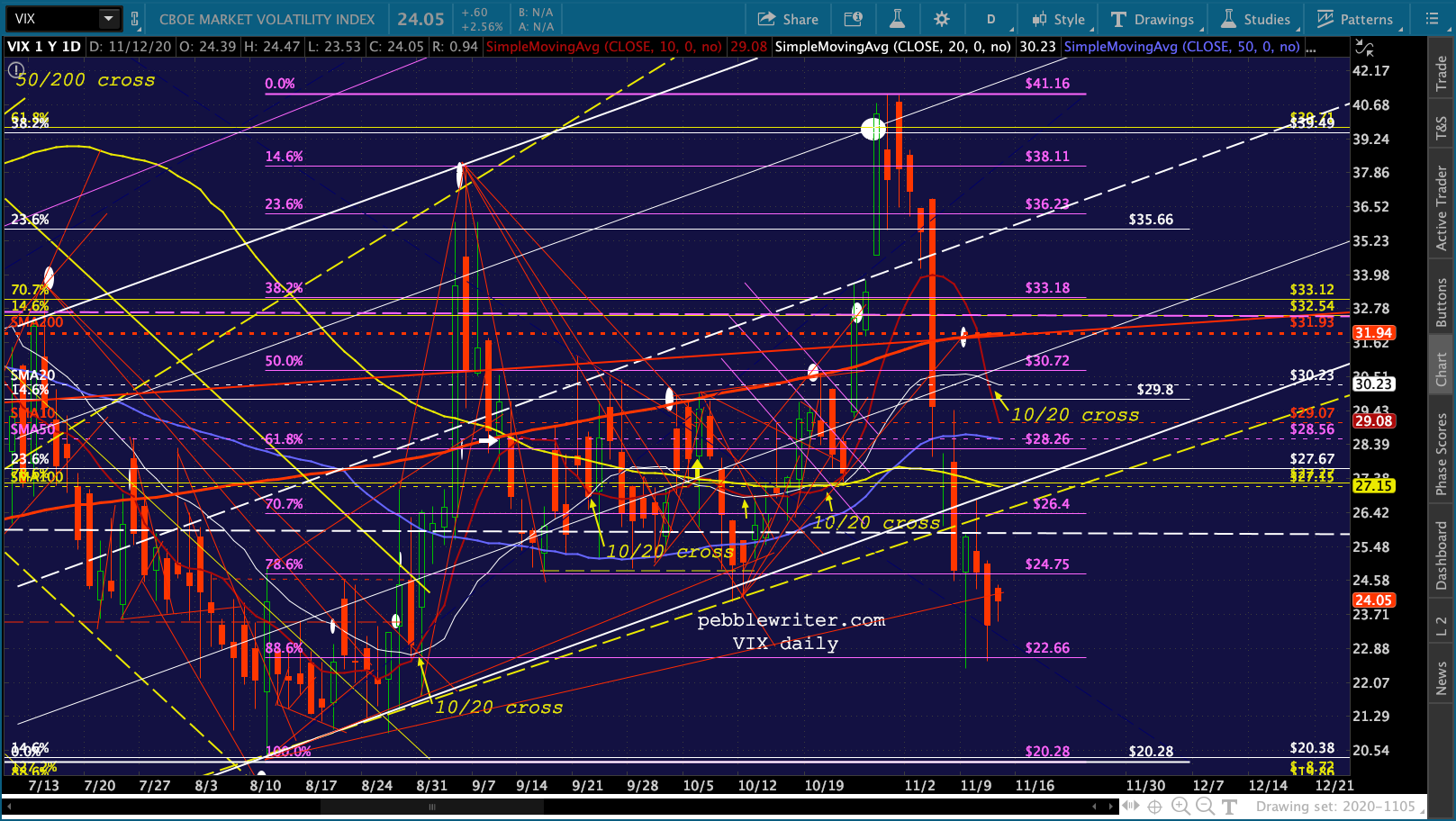

One would think if the economy were really all that healthy, especially with the flood of liquidity still being thrown at it, we’d see at least some inflation. But, hey, we got the 10/20 crosses we were expecting in ES, SPX and VIX. So, the rally is safe…right?

continued for members…

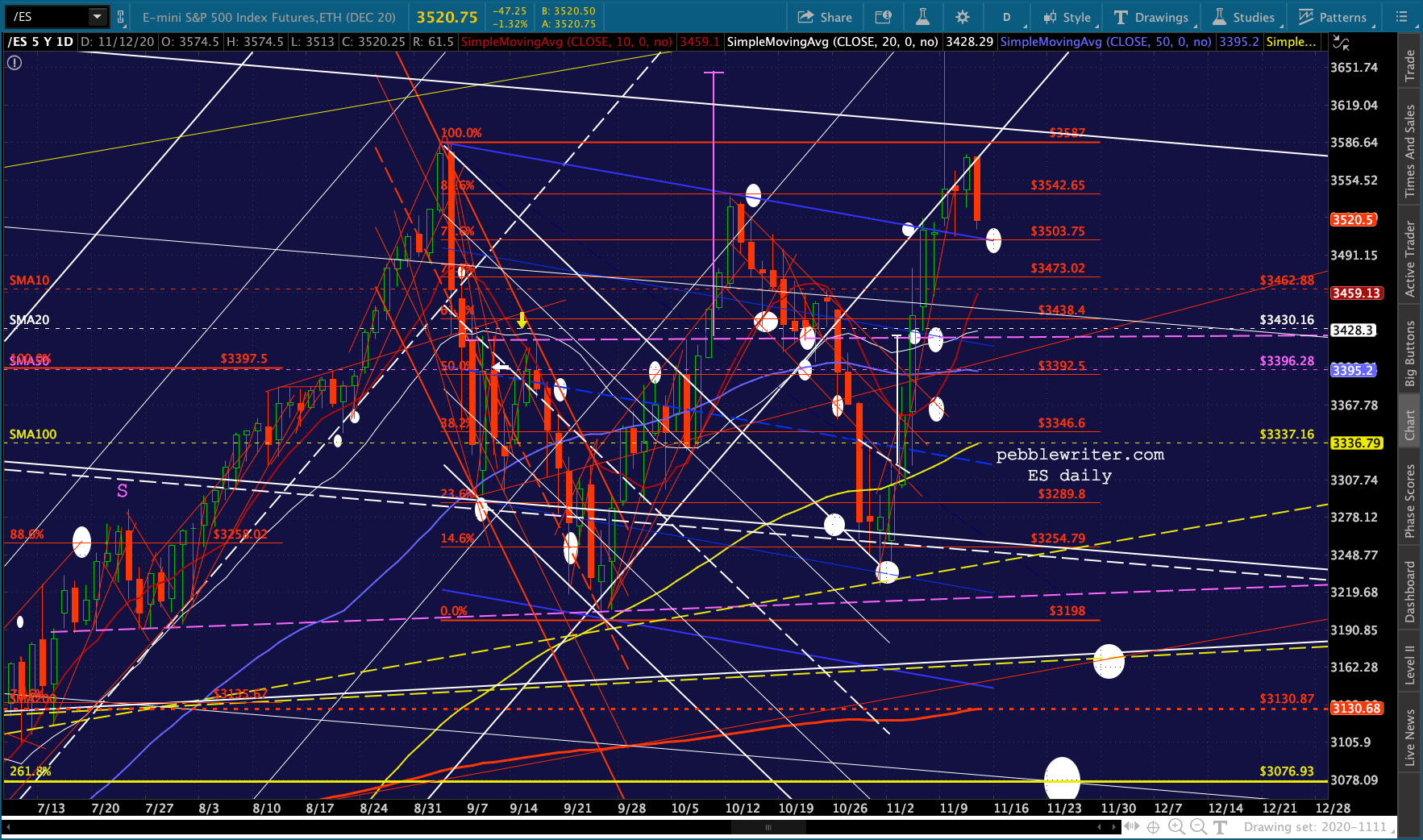

ES’ 10/20 cross is up to 22 points right off the bat…

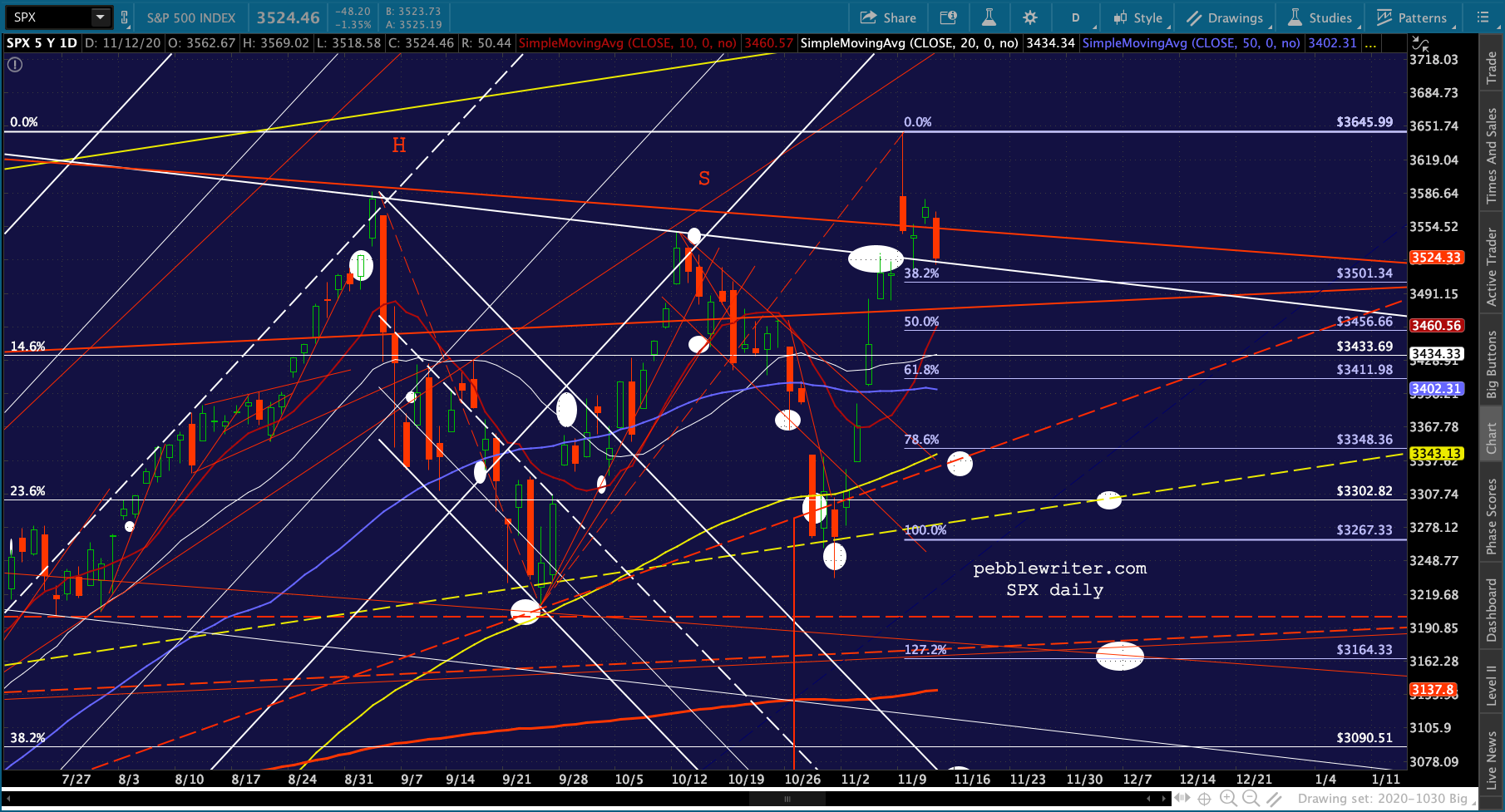

…while SPX’s is a little more modest. Since many of the bearish patterns have been busted, we have to turn to the SMA200 for a solid downside target if either SPX or ES can manage more than a backtest of their broken flag patterns.

…while SPX’s is a little more modest. Since many of the bearish patterns have been busted, we have to turn to the SMA200 for a solid downside target if either SPX or ES can manage more than a backtest of their broken flag patterns. The big 10/20 cross, of course, was in VIX.

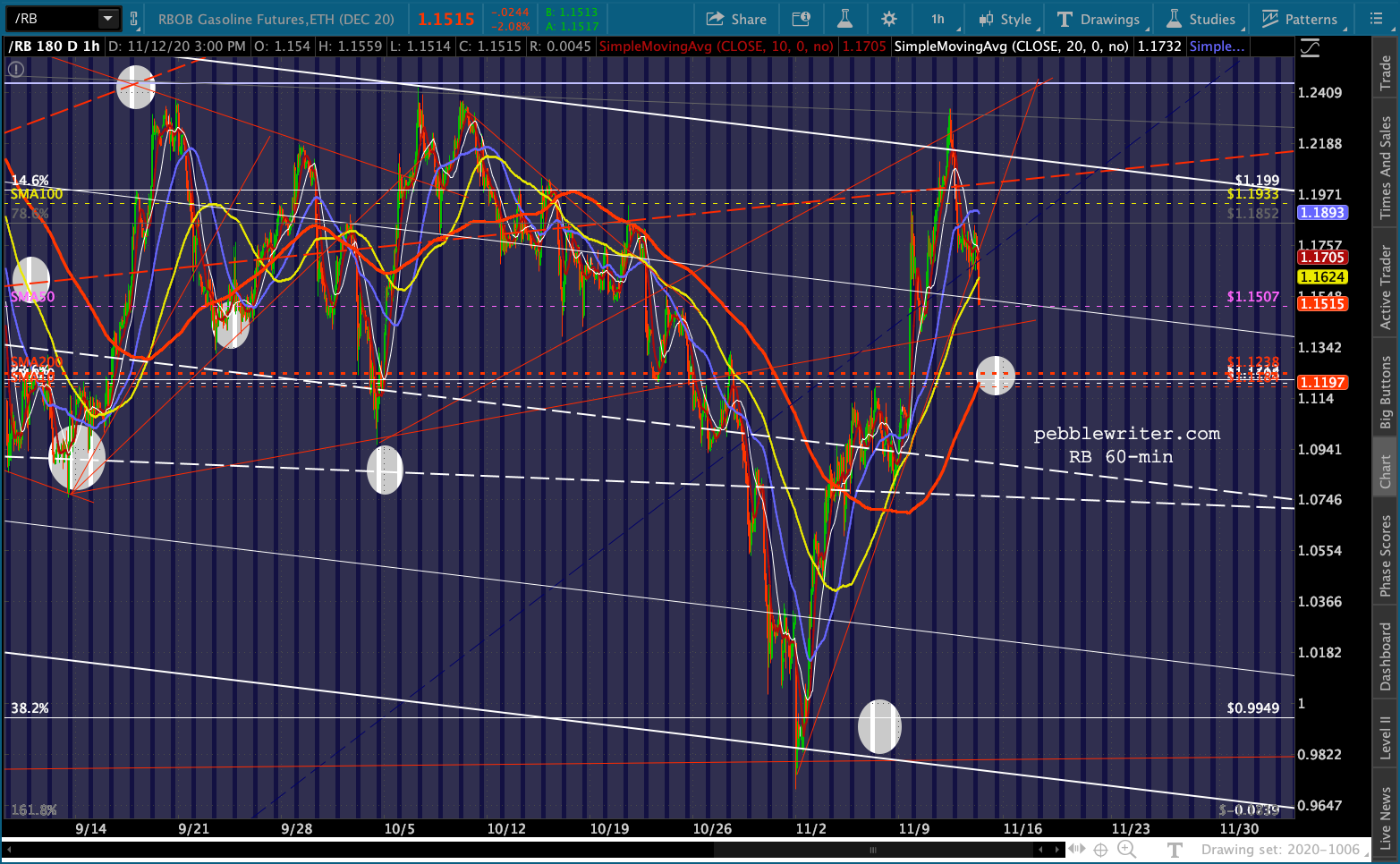

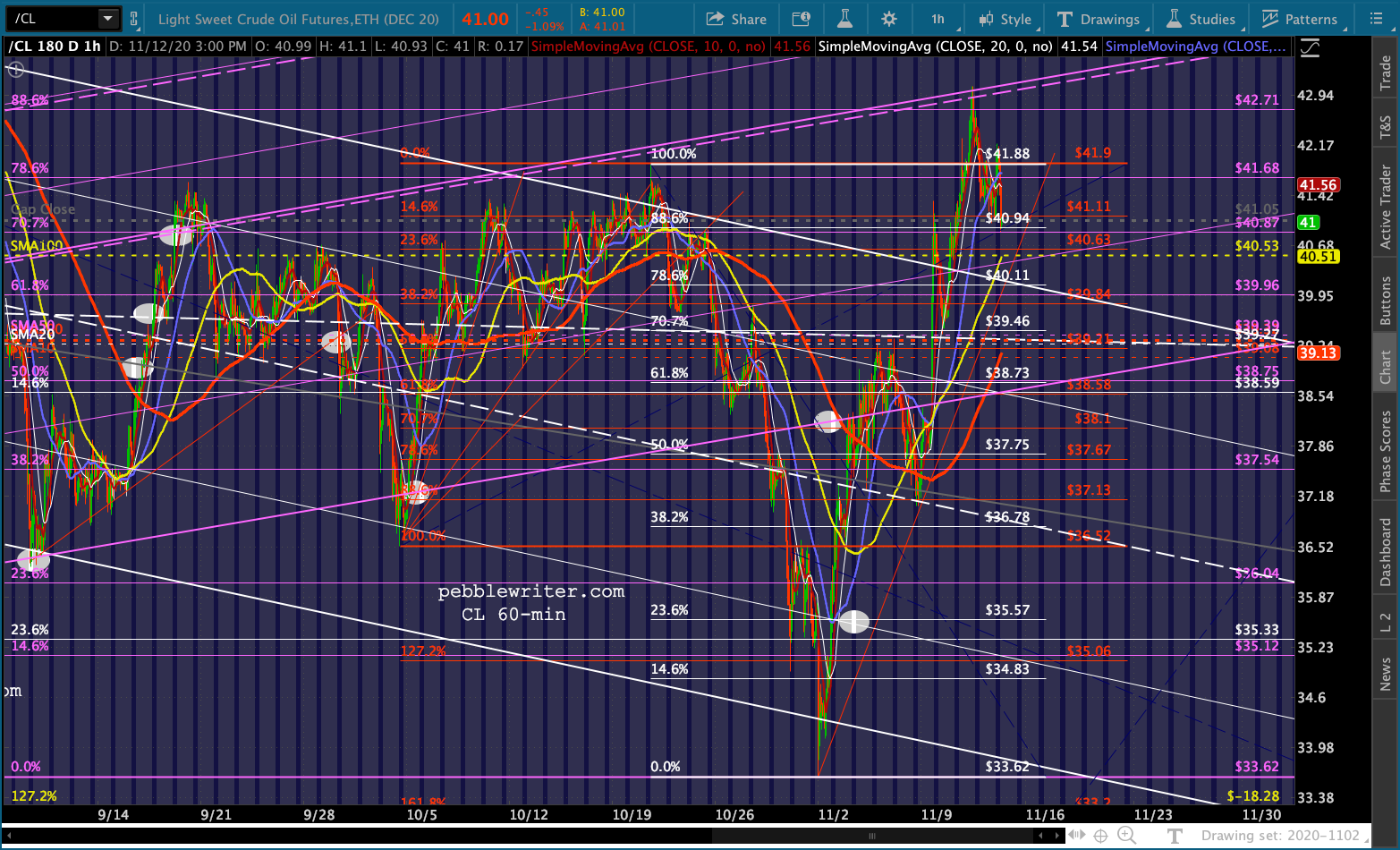

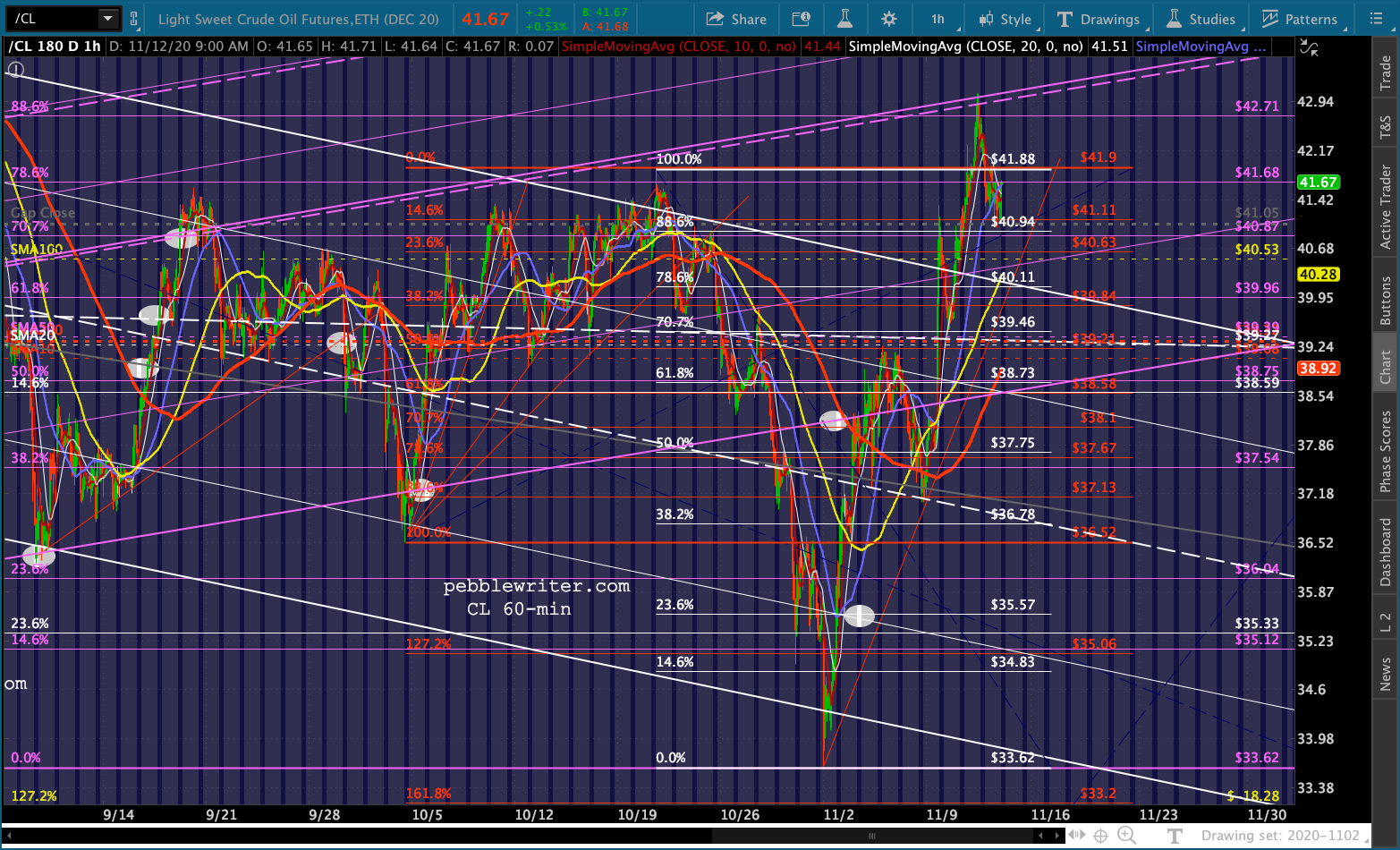

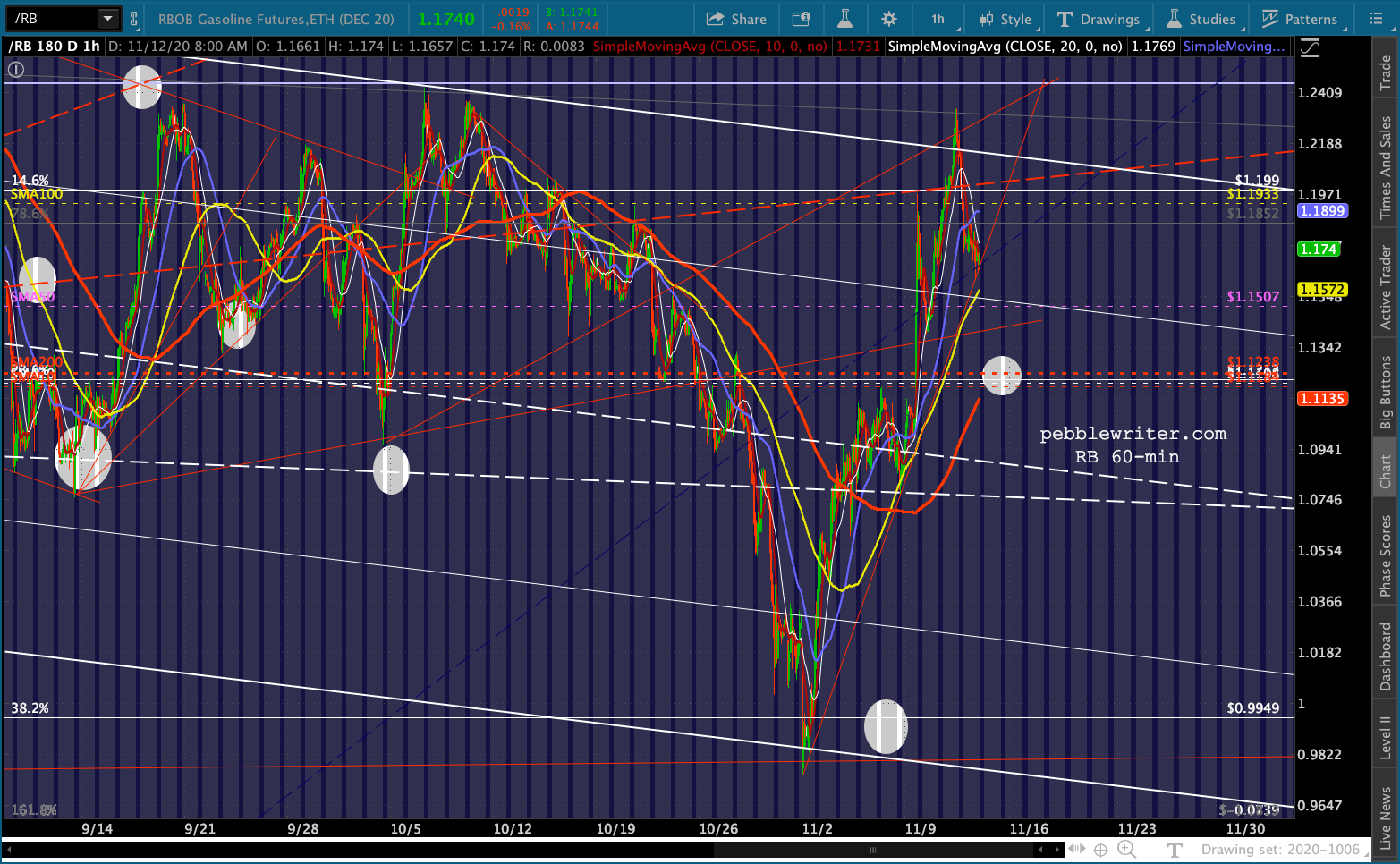

The big 10/20 cross, of course, was in VIX.  RB and CL are still on the cusp of a bullish cross – but are very very extended, especially given the COVID trends around the world. Remember, the holiday-delayed EIA inventory data is due out this morning.

RB and CL are still on the cusp of a bullish cross – but are very very extended, especially given the COVID trends around the world. Remember, the holiday-delayed EIA inventory data is due out this morning.

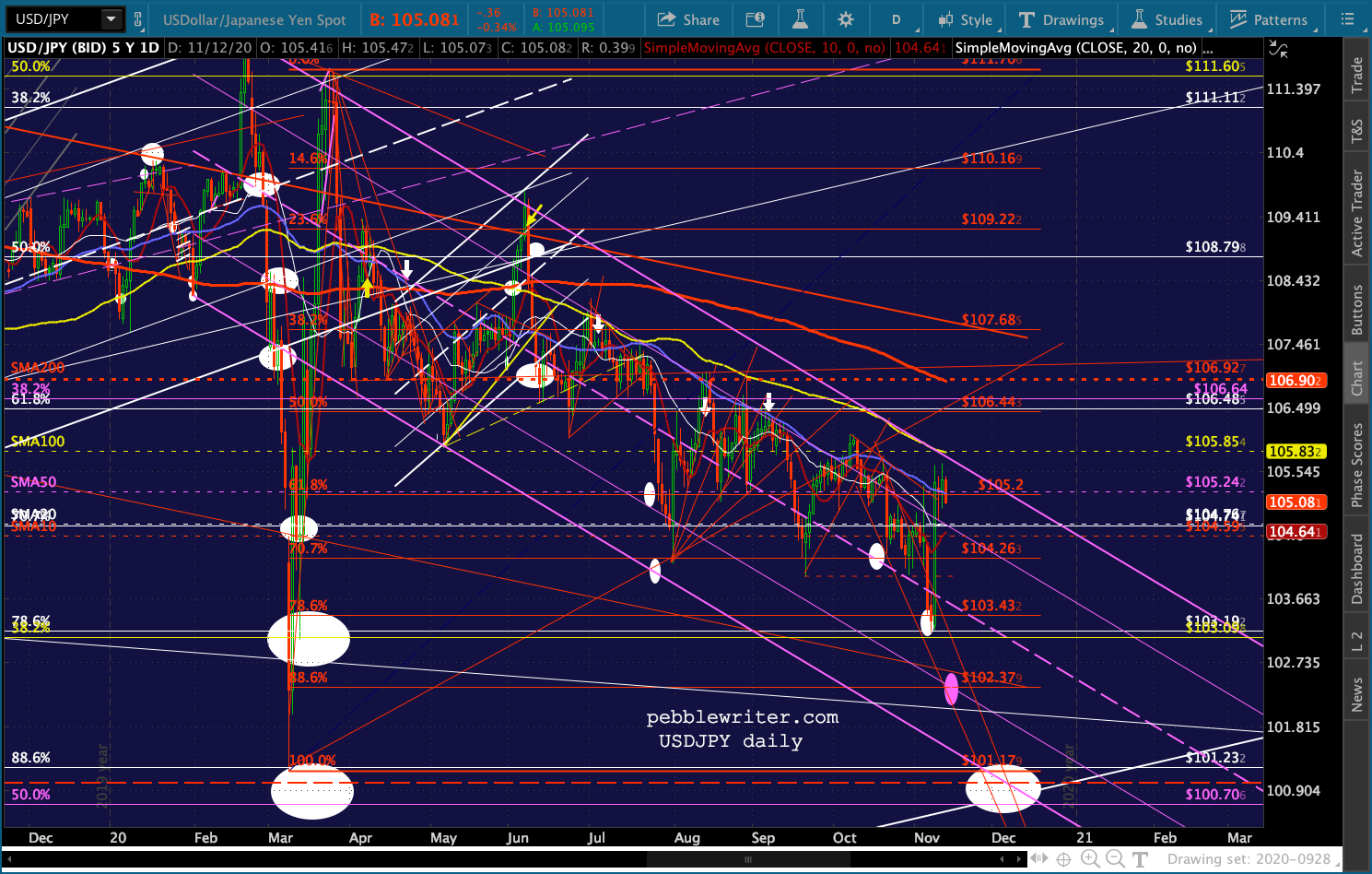

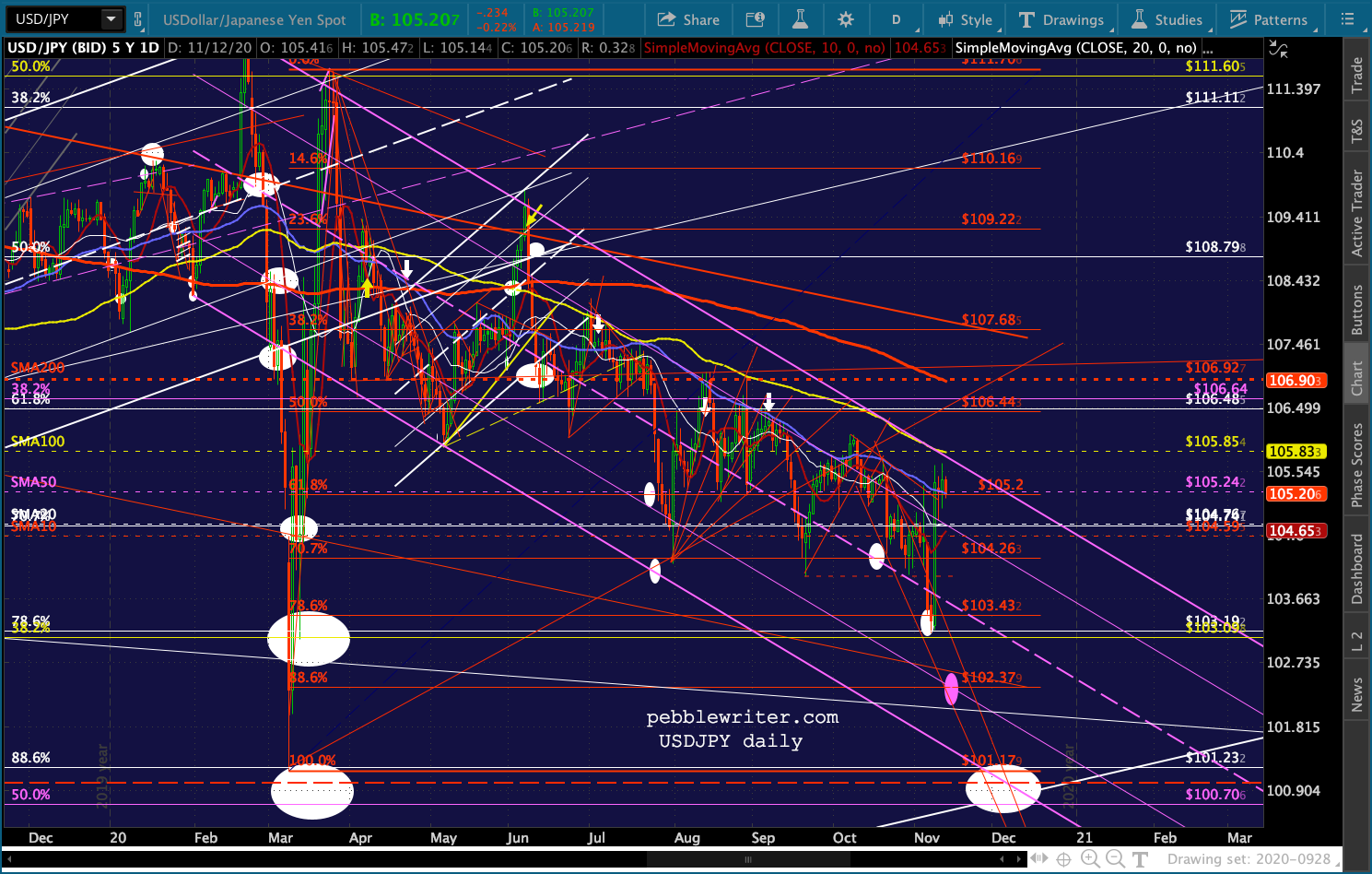

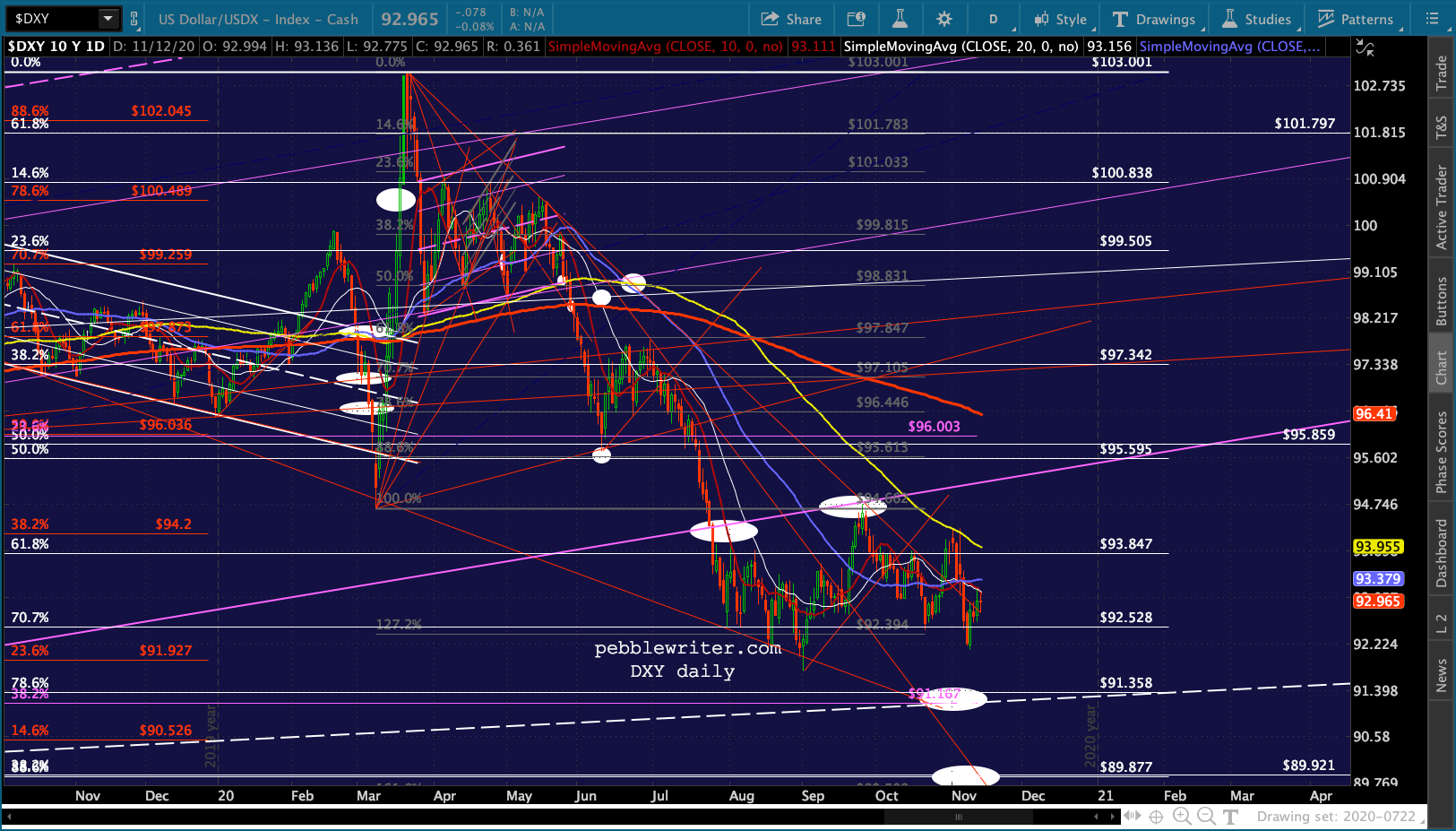

The best shot at triggering a significant decline in stocks remains in the hands of USDJPY…

The best shot at triggering a significant decline in stocks remains in the hands of USDJPY…

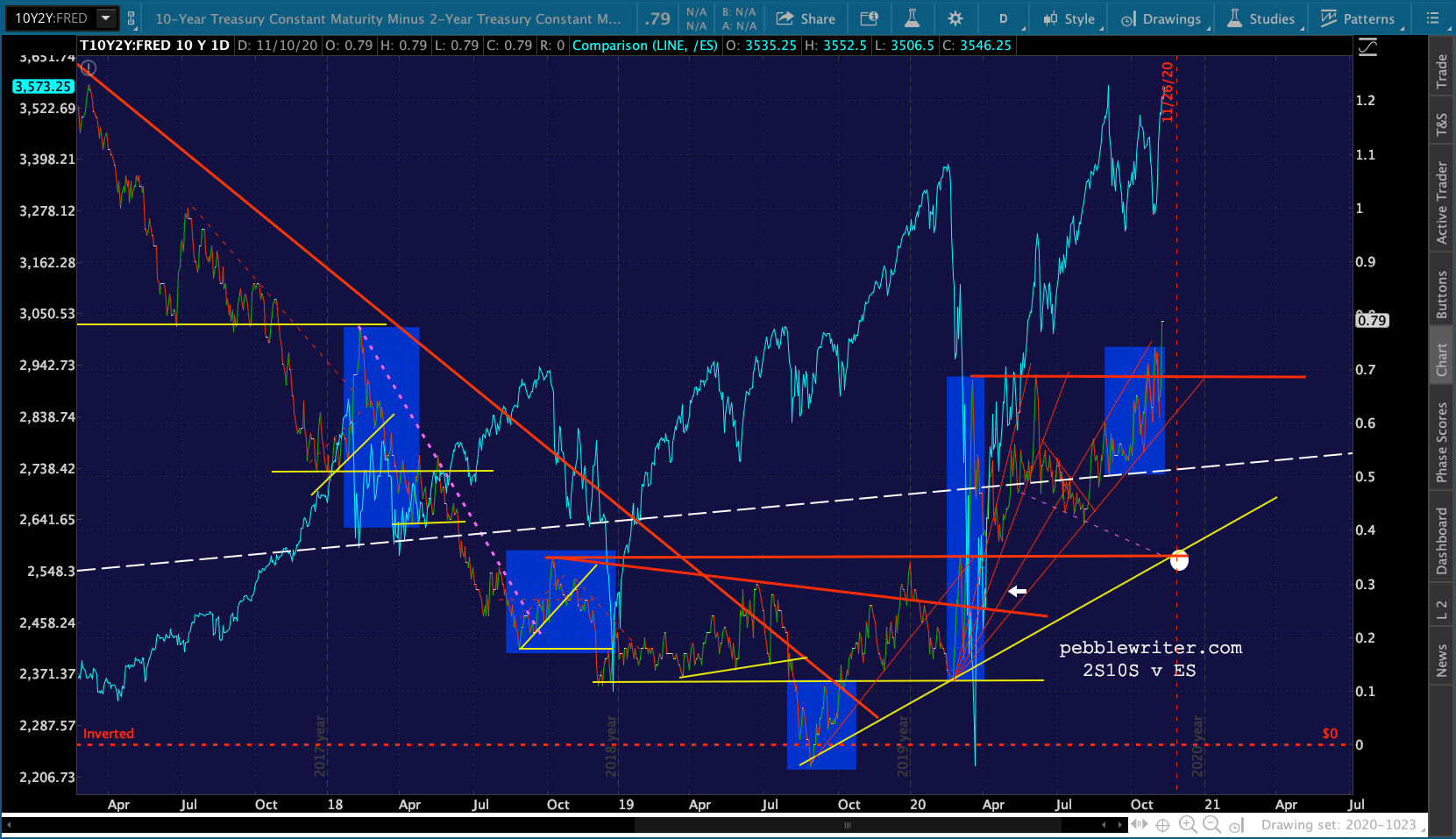

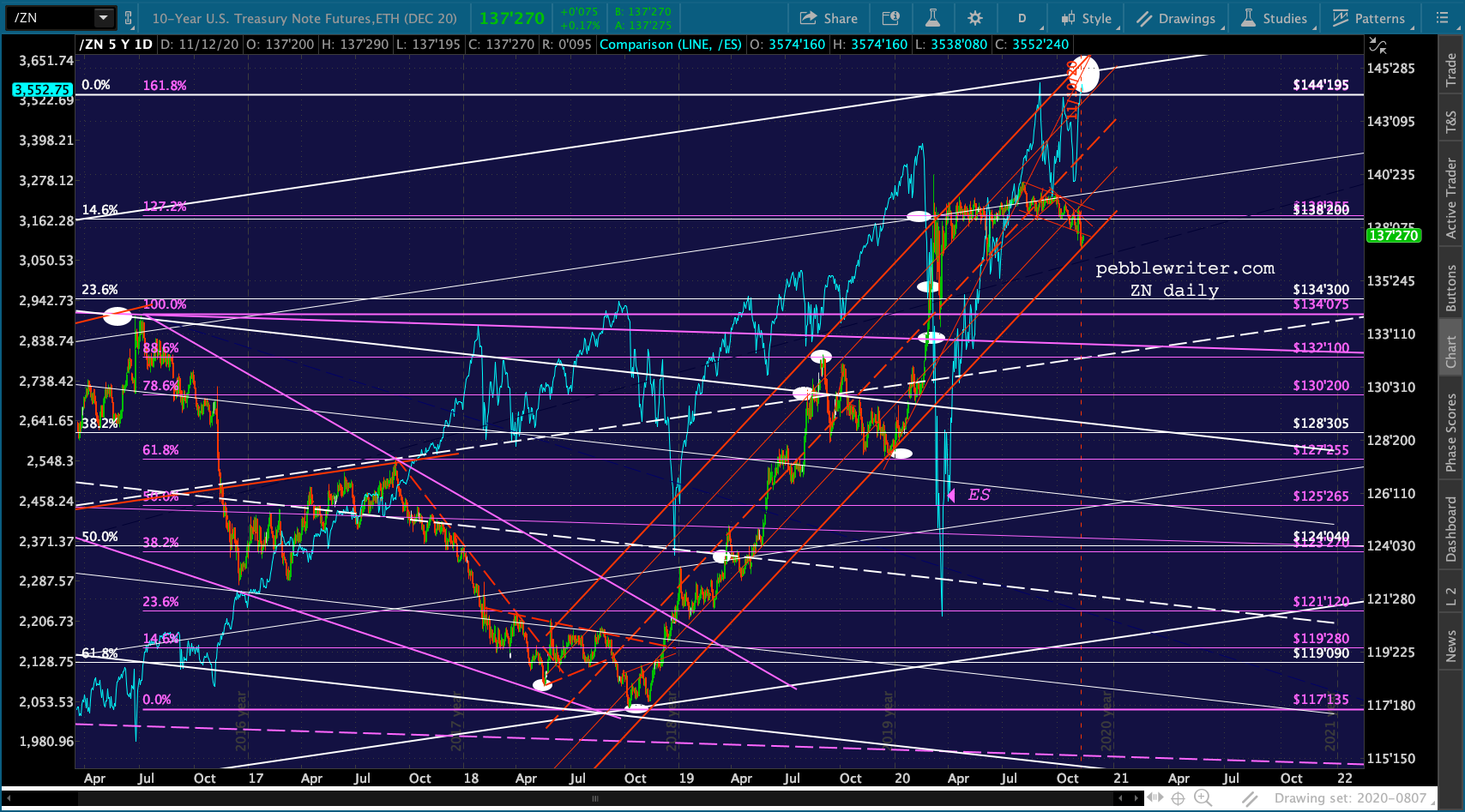

…the yield curve…

…the yield curve… …and the 10Y.

…and the 10Y.

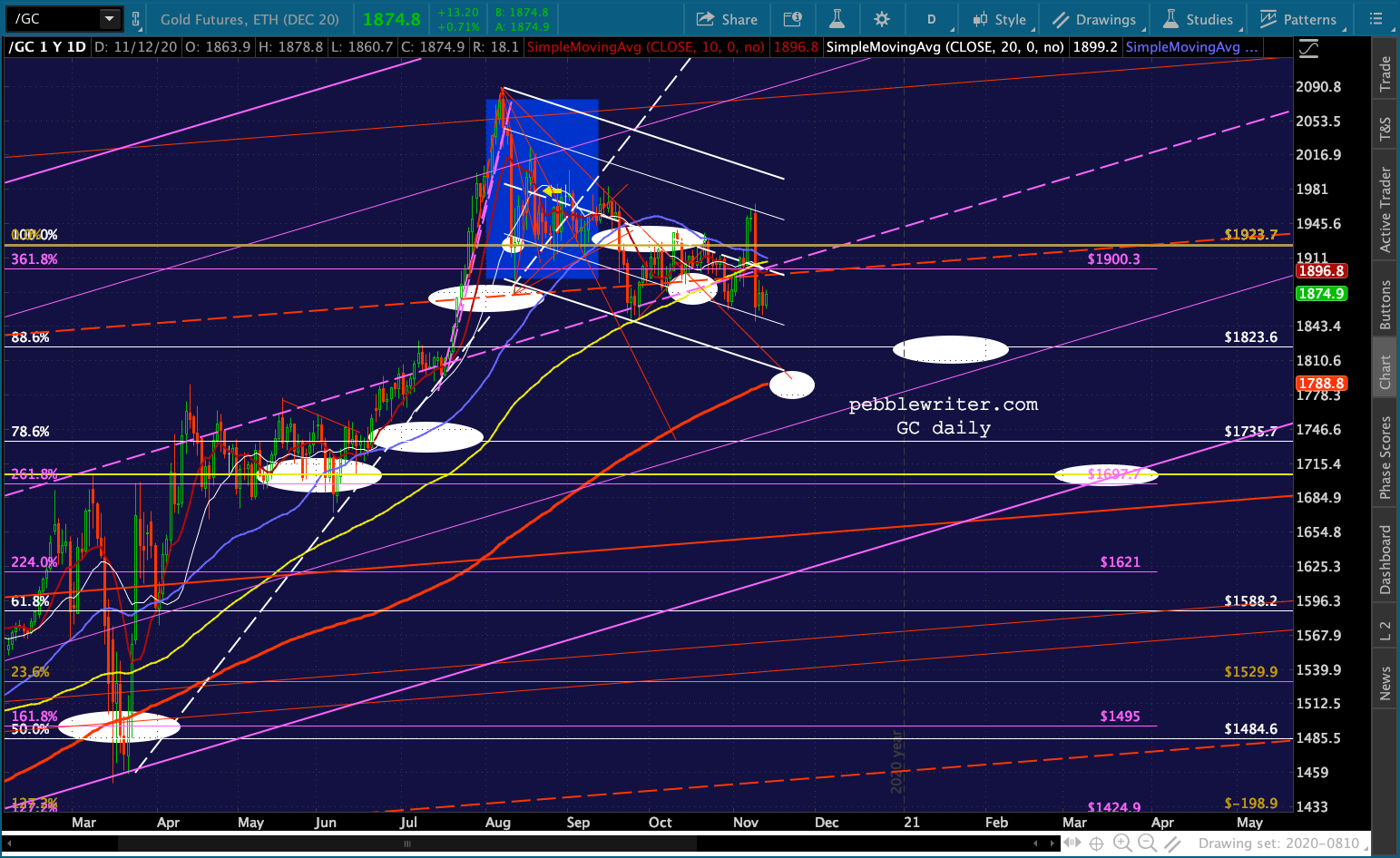

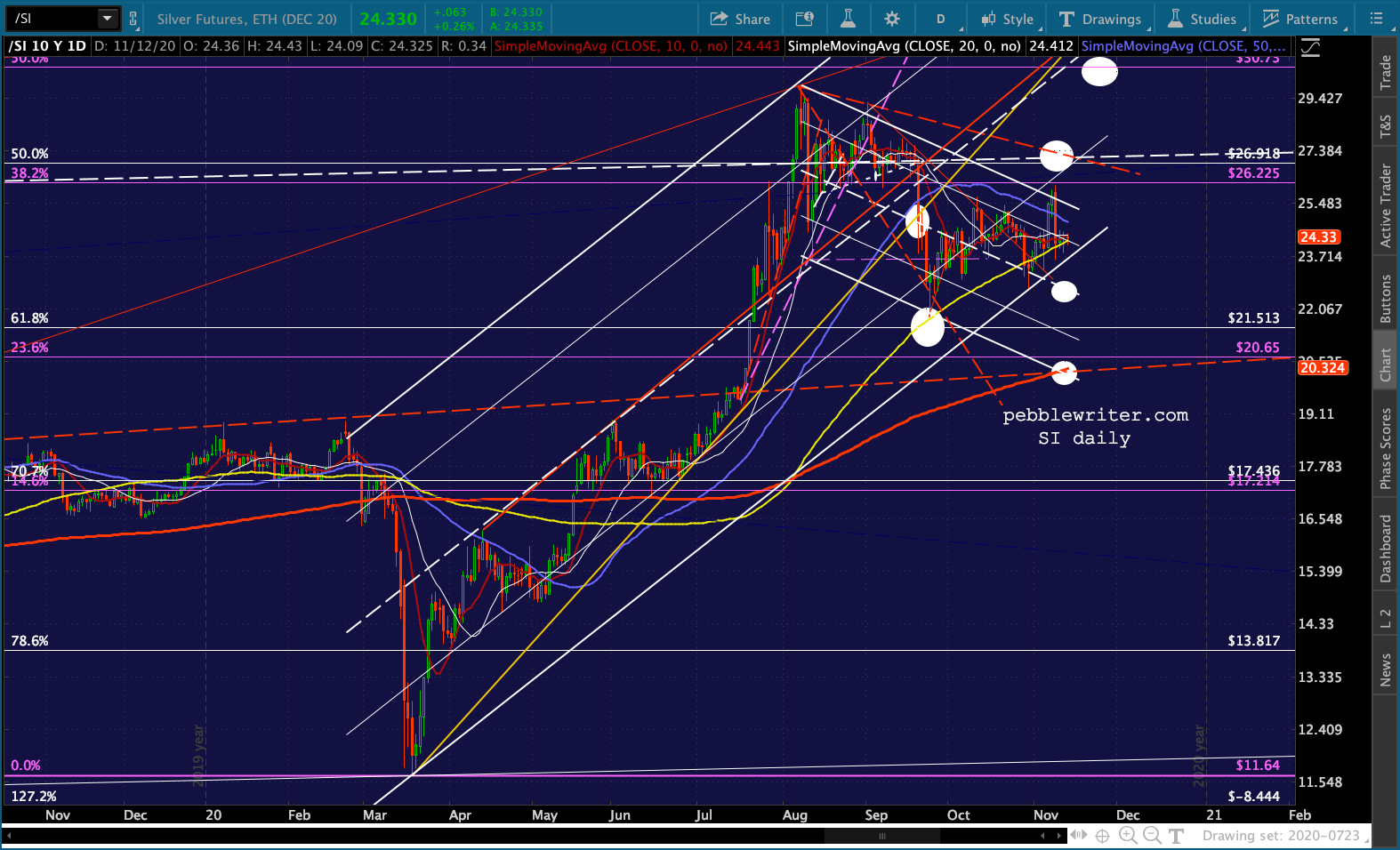

Persistent low inflation won’t do much to support higher interest rates, which means we should see USD weakness. It also increases the risk of the SMA200 scenarios for GC and SI.

Persistent low inflation won’t do much to support higher interest rates, which means we should see USD weakness. It also increases the risk of the SMA200 scenarios for GC and SI.

more later…

more later…

UPDATE: 3:34 PM

Backtests are making nice progress.