The last time we were this bearish on oil and gas was on October 3, 2018 [see: VIX Takes the Plunge.] Our reasoning at the time:

CL and RB [have] not only reached overhead resistance by our measure, but must deal with inflation that’s too high, bearish API data, another round of Trump tweeting, and a large build in EIA inventory. I think the time has finally come to revert to short…

WTI and RBOB both tumbled about 40% over the next three months.

At nearly 3%, inflation had been too high – sending the 10Y to 3.5%. Highly correlated, both had recently broken out of long-term downtrends: CPI above the black dotted line and the 10Y above the blue dotted line. Historically, this might have been perfectly acceptable. But, as we were shouting from the rooftops at the time [see: Why Rising Rates Are a Problem This Time] rising rates with a $1 trillion deficit and debt soaring past $20 trillion was completely unacceptable.

Historically, this might have been perfectly acceptable. But, as we were shouting from the rooftops at the time [see: Why Rising Rates Are a Problem This Time] rising rates with a $1 trillion deficit and debt soaring past $20 trillion was completely unacceptable.

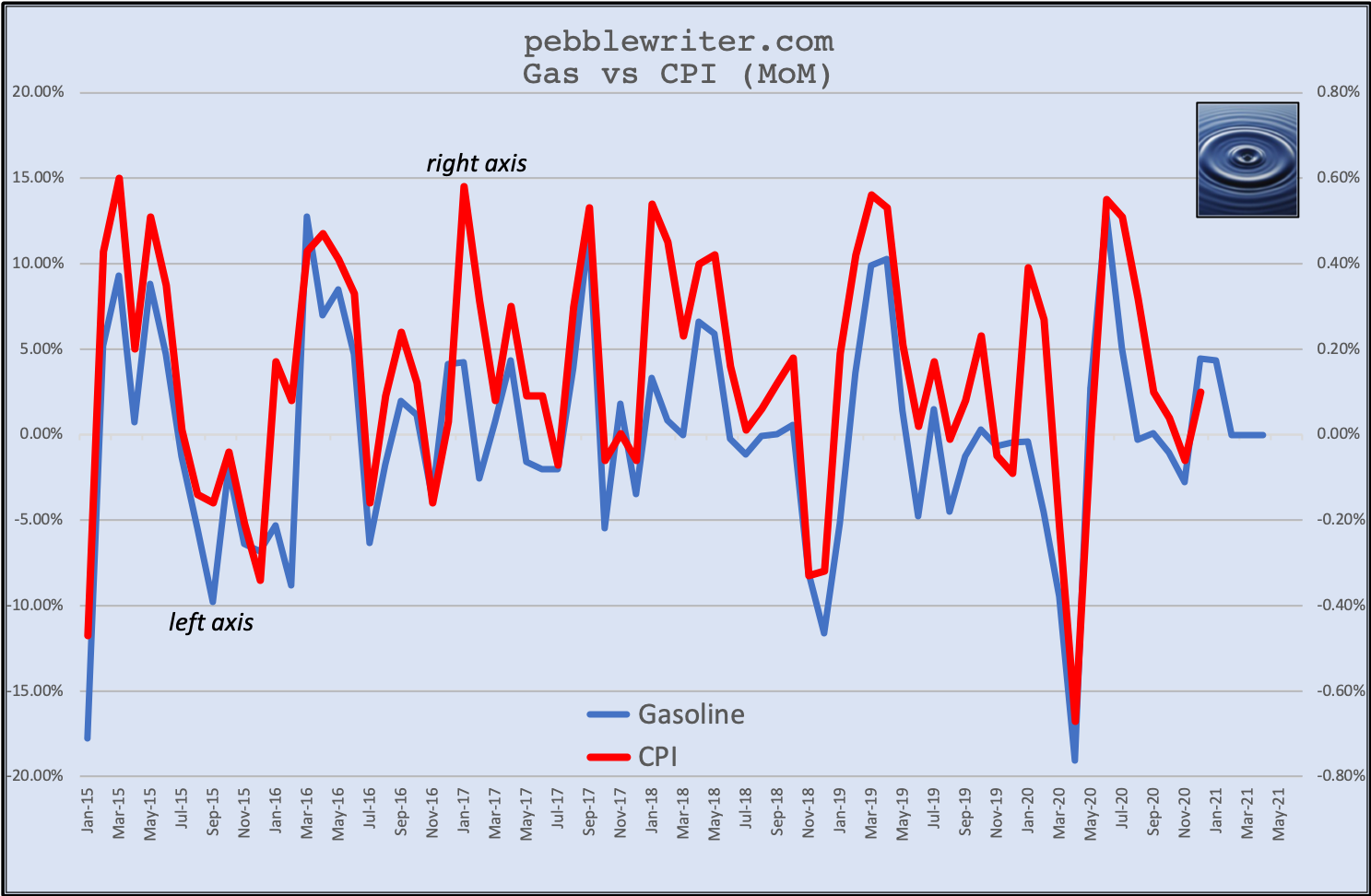

And, inflation was too high primarily because energy prices were too high. The correlation with the YoY rise in gasoline prices, in particular, has been quite strong over the years.

And, inflation was too high primarily because energy prices were too high. The correlation with the YoY rise in gasoline prices, in particular, has been quite strong over the years.

No doubt the Fed saw the writing on the wall – as did the White House. Trump had been tweeting about oil prices being too high for months. His tweets had taken on a decidedly desperate tone.

No doubt the Fed saw the writing on the wall – as did the White House. Trump had been tweeting about oil prices being too high for months. His tweets had taken on a decidedly desperate tone.

Yet Saudi Arabia politely ignored him, and oil prices continued higher – until Crown Prince Mohammed bin Salman slipped up in a very big way.

Yet Saudi Arabia politely ignored him, and oil prices continued higher – until Crown Prince Mohammed bin Salman slipped up in a very big way.

It took about 5 minutes for virtually everyone to connect Khashoggi’s murder with MBS – who suddenly found himself without friends. Except for one who, coincidentally, needed a favor. As we wrote in Coincidences and Consequences at the time:

It took about 5 minutes for virtually everyone to connect Khashoggi’s murder with MBS – who suddenly found himself without friends. Except for one who, coincidentally, needed a favor. As we wrote in Coincidences and Consequences at the time:

It’s interesting how Khashoggi’s murder top-ticked oil and gas prices…and, so soon after Trump’s latest demand that OPEC lower oil prices. As Churchill famously said, “never let a good crisis go to waste.”

Some were aghast that we would insinuate such a thing. But, Bob Woodward’s excellent Rage recently shed some light on the topic… But, we digress. Oil and gas prices crashed 40%. Inflation and interest rates receded.

But, we digress. Oil and gas prices crashed 40%. Inflation and interest rates receded.  The story might have had a happy ending, but the Fed and White House had apparently forgotten about the strong correlation between oil/gas prices and the stock market. When RB plunged 42%, SPX gave up 20%.

The story might have had a happy ending, but the Fed and White House had apparently forgotten about the strong correlation between oil/gas prices and the stock market. When RB plunged 42%, SPX gave up 20%.

Not coincidentally, they both bottomed on Dec 24 (when Treasury Secretary Mnuchin convened the Plunge Protection Team – but that’s another story.) Trump probably texted to MBS…something to the effect of “jk!!! LOL!!!  ” because oil and gas prices rebounded sharply.

” because oil and gas prices rebounded sharply.

Wait, you’re probably wondering, what about interest rates? Bond yields drop for all kinds of reasons. Sometimes it’s because inflation is dropping. Other times, it’s because a stock market crash scares the crap out of equity investors who sell everything that isn’t nailed down and pile into bonds.

Wait, you’re probably wondering, what about interest rates? Bond yields drop for all kinds of reasons. Sometimes it’s because inflation is dropping. Other times, it’s because a stock market crash scares the crap out of equity investors who sell everything that isn’t nailed down and pile into bonds.

While the PPT’s volatility crush gathered momentum, the Fed announced that the recent round of rate hikes was kaput and began cutting. Stocks were thrilled.

The occasional mini-crashes in the stock market helped drive rates even lower, until the 10Y finally bottomed out at 1.43% on Sep 3, 2019 – down sharply from its 3.25% October 2018 highs.

Oil and gas, which had nudged stocks back to their September 2018 highs, could take a breather. Their ascent had been way out of line with the fundamentals, and the charts strongly suggested a reversal. As we wrote on April 22, 2019 [see: Oil Fails to Rally Stocks]:

Oil and gas, which had nudged stocks back to their September 2018 highs, could take a breather. Their ascent had been way out of line with the fundamentals, and the charts strongly suggested a reversal. As we wrote on April 22, 2019 [see: Oil Fails to Rally Stocks]:

One of the more effective factors in prompting algos to buy stocks is the price of oil. Yet, as we’ve been discussing, higher oil prices are a double-edged sword as they can drive inflation to levels which prompt uncomfortably high interest rates. The oil and gas picture shows RB and CL have both run out of room. It’s time to short again.

CL, which closed at 75.04 that day, fell 15% over the next six weeks. It bounced around in in the 60-70 range until January 2020, when it finally broke down. RB, which closed at 2.13 on Apr 22, fell 32% before stabilizing somewhat. It finally broke down in March 2020.

The culprit this time, of course, was the coronavirus pandemic. As we noted on February 20 [see: Buckle Up] the stage was set for the algos to keep pushing stocks higher. But, as we had discussed on January 6 [see: Middle East Tensions Escalate] the repeated failure to break out in response to numerous opportunities was itself a strong sell signal.

CL has tagged its white .886 and, having broken out above the red TL, will threaten the April highs if it breaks 64.77. If it can’t break the April highs, it will be very susceptible to a downturn. Remember, if the rising white channel breaks down, we could be looking at a major crash. Meanwhile, RB failed to break out past either its SMA200 or the red TL from the April highs. For those not already short, this is the place.

It certainly was.

continued for members…

We’re only two weeks into January, but at this stage a large gap is shaping up between current gasoline prices and the April 2020 prices. If current gas prices persist, the MoM delta wouldn’t be a problem…

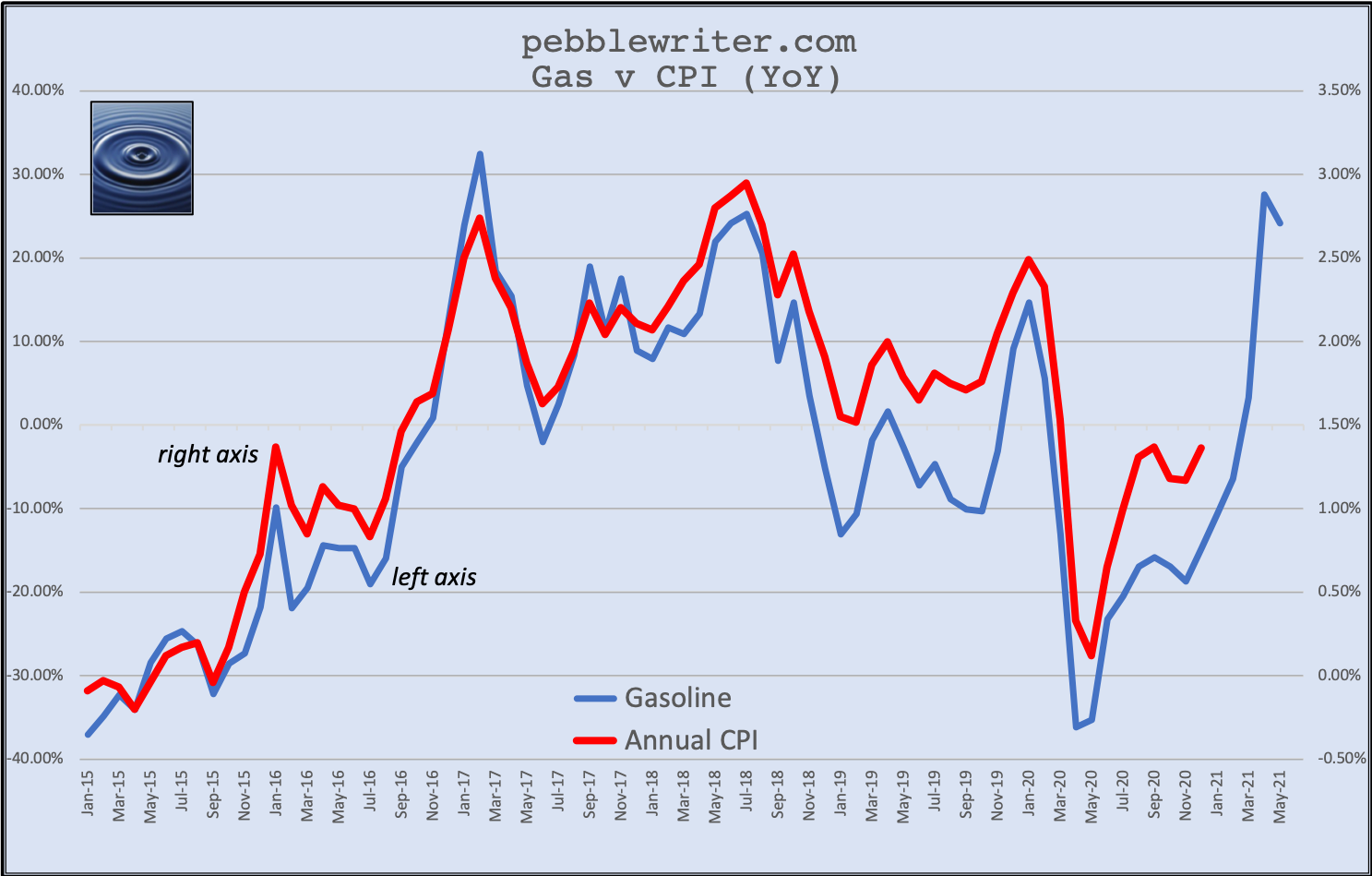

…but the YoY chart would look like the one below. It doesn’t take much imagination to guess what that would do to CPI. And guess what that would do to interest rates?

And guess what that would do to interest rates?

The trick is to figure out:

The trick is to figure out:

(1) how high can inflation and interest rates go before the Fed wigs out?

(2) what would that mean in terms of RB/CL?

In terms of inflation and interest rates, we might have already reached the limit. The 2s10s has already broken out a couple of times, which has historically been tough on stocks.

The difference between now and those previous bear markets is that the rapid steeping which is happening is primarily the result of the 10Y ramping higher while the 2Y is staying pretty flat.

The difference between now and those previous bear markets is that the rapid steeping which is happening is primarily the result of the 10Y ramping higher while the 2Y is staying pretty flat. But, the charts indicate that the 10Y might need a significant pause here. It’s the top of two channels, the midline of another, and an .886 retracement of the drop from the Mar 18 highs.

But, the charts indicate that the 10Y might need a significant pause here. It’s the top of two channels, the midline of another, and an .886 retracement of the drop from the Mar 18 highs.

Higher would probably continue to benefit stocks. I think the Fed has been pleased to get stocks back to their Feb 2020 highs. But, it’s hard to believe they see stocks as being undervalued. It’s more likely they recognize that a new bubble has been formed – thus amping up the risks of another market crash. The Fed will no doubt continue crowing about the need to get inflation back to 2%. And, I will continue to believe that argument is a canard – justification for the easy money policy that keeps stocks afloat.

The Fed will no doubt continue crowing about the need to get inflation back to 2%. And, I will continue to believe that argument is a canard – justification for the easy money policy that keeps stocks afloat.

continuing…