It was a close shave, but ZN’s falling red channel has survived – at least so far. The runaway 10Y yield gave up all of its gains – and not a minute too soon for the bears.

continued for members…

continued for members…

This leaves (at least) a good backtest open for ZN… …and puts TNX back in play for a sizeable decline…

…and puts TNX back in play for a sizeable decline…  …which keeps DXY’s hopes for a rally intact. Again…for now.

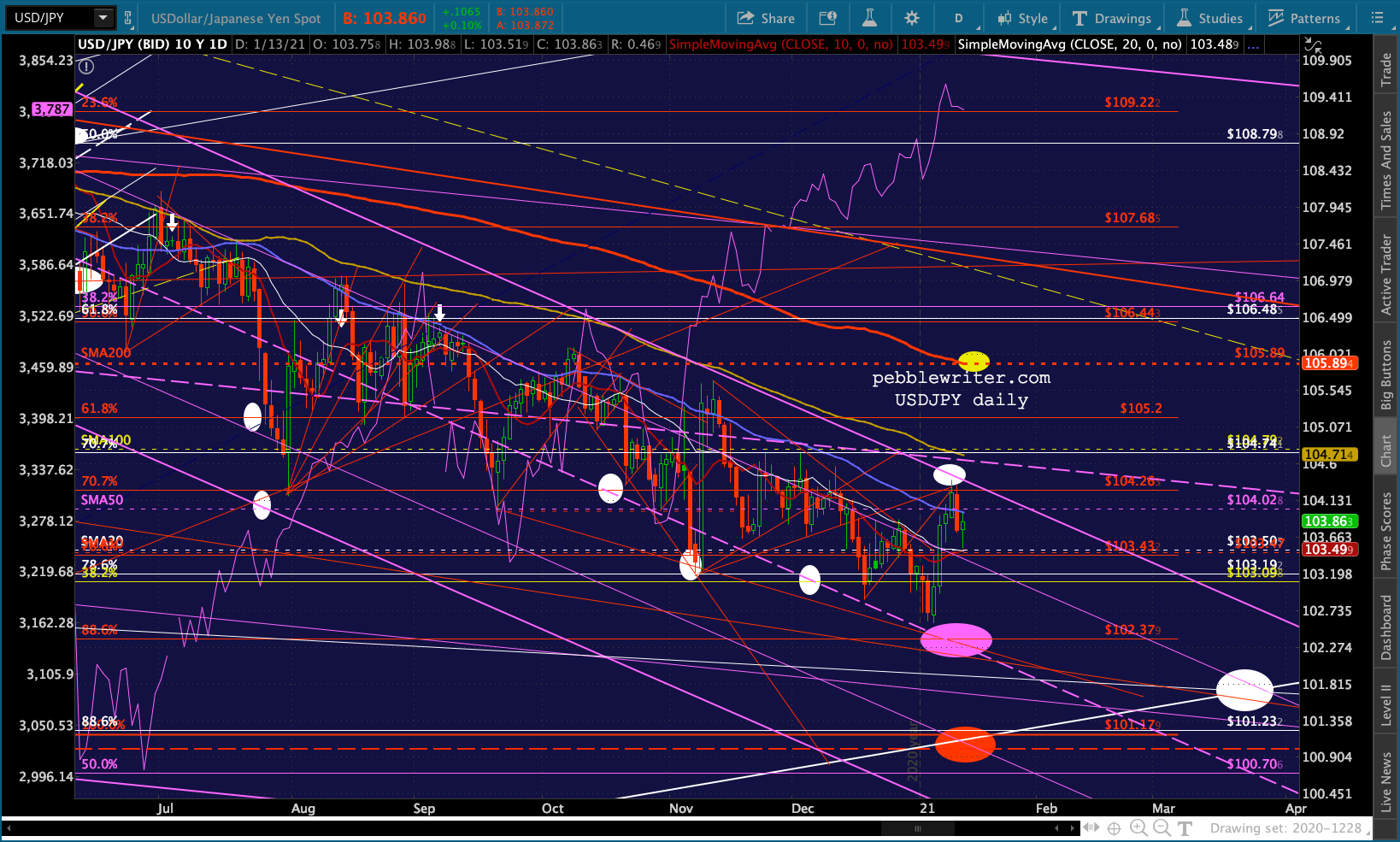

…which keeps DXY’s hopes for a rally intact. Again…for now. USDJPY cooperated by not breaking out.

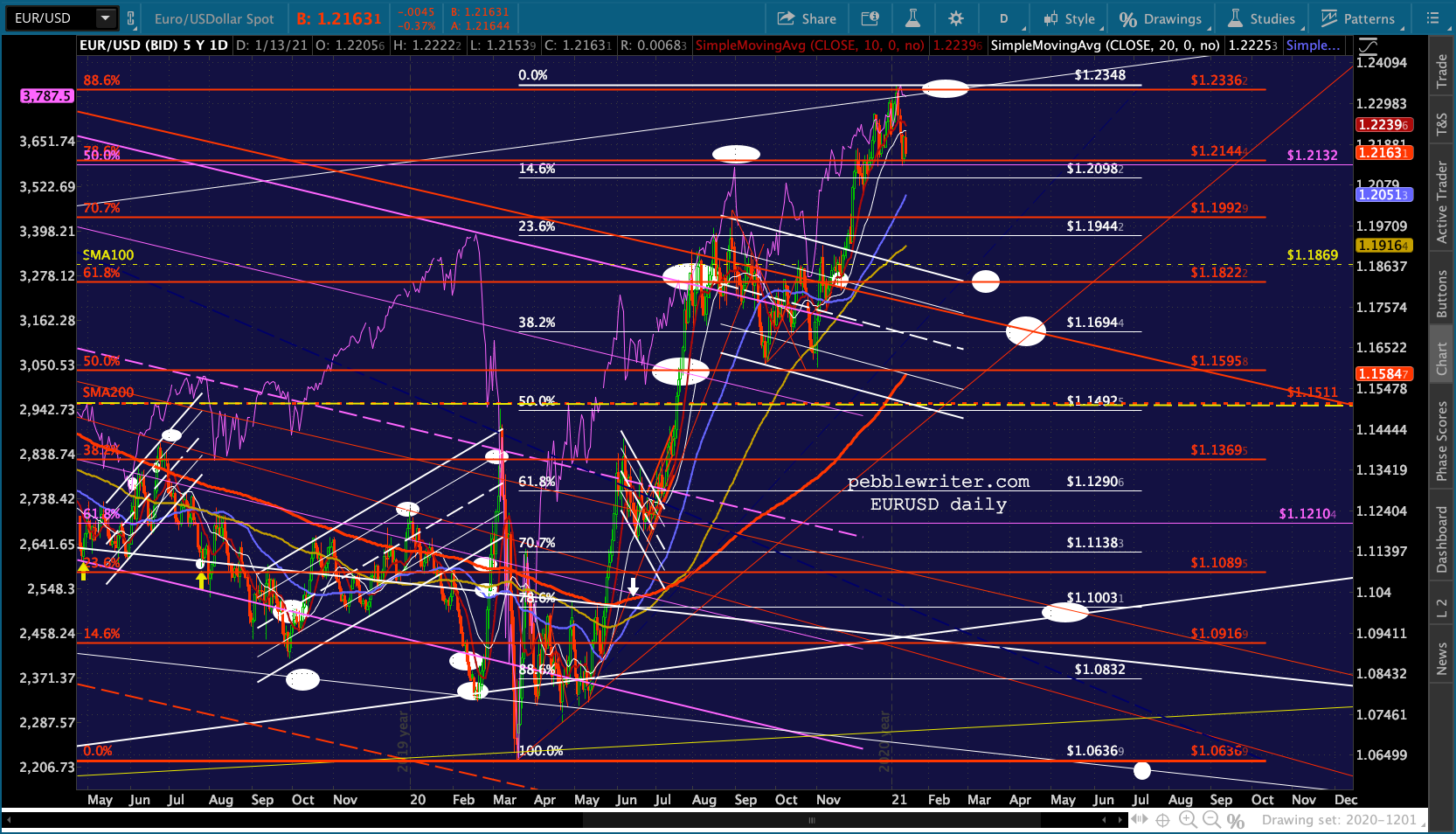

USDJPY cooperated by not breaking out.  And, EURUSD continues its decline.

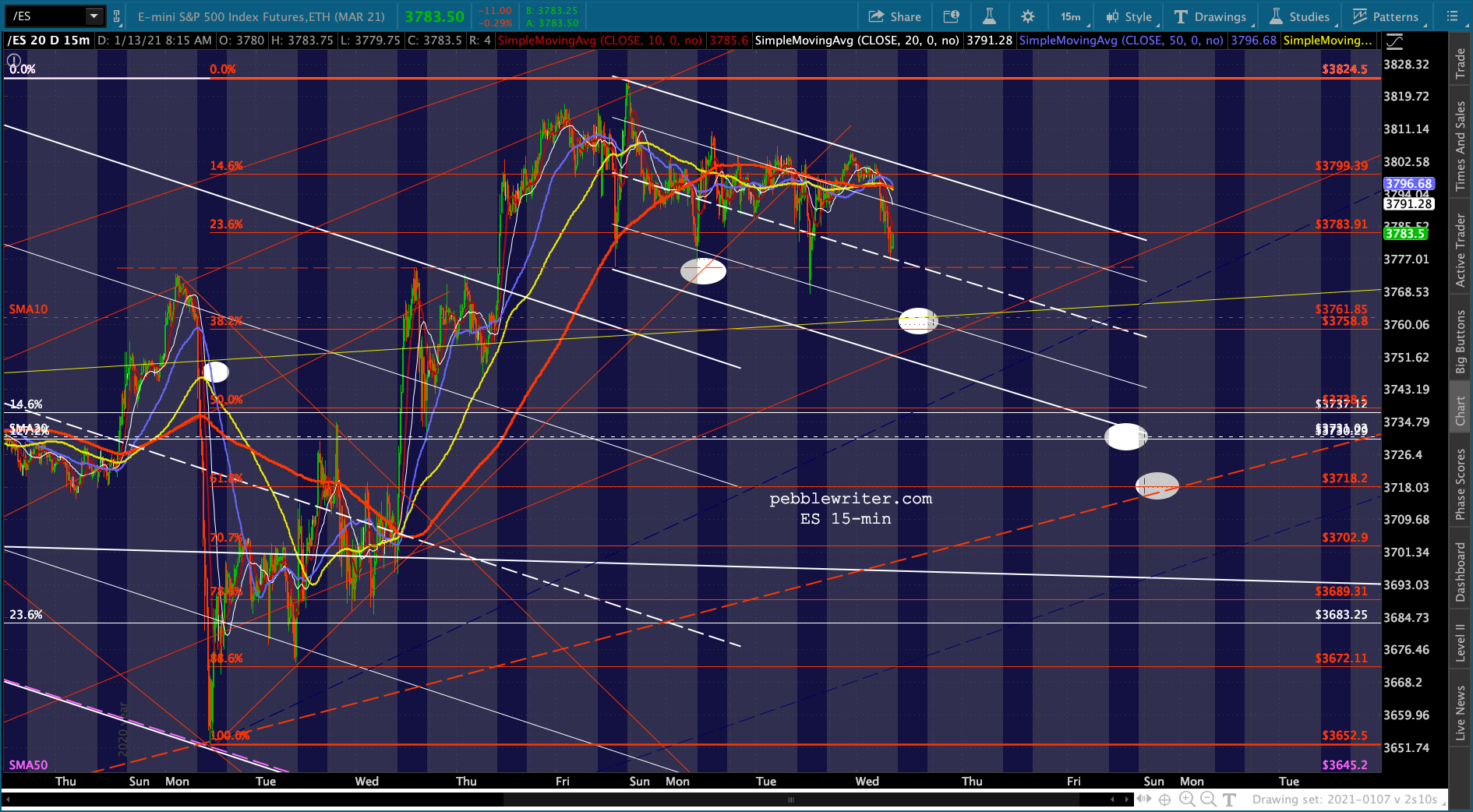

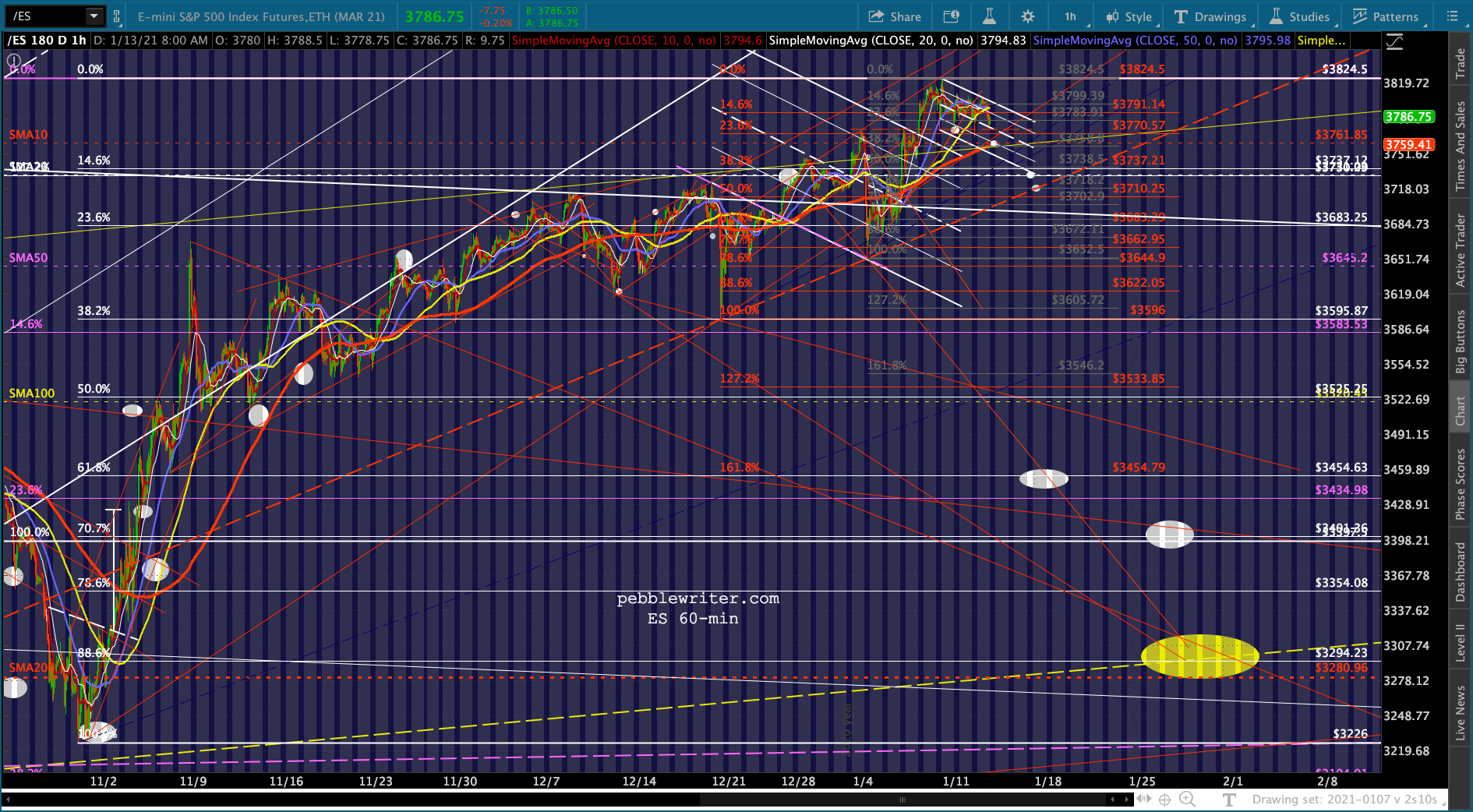

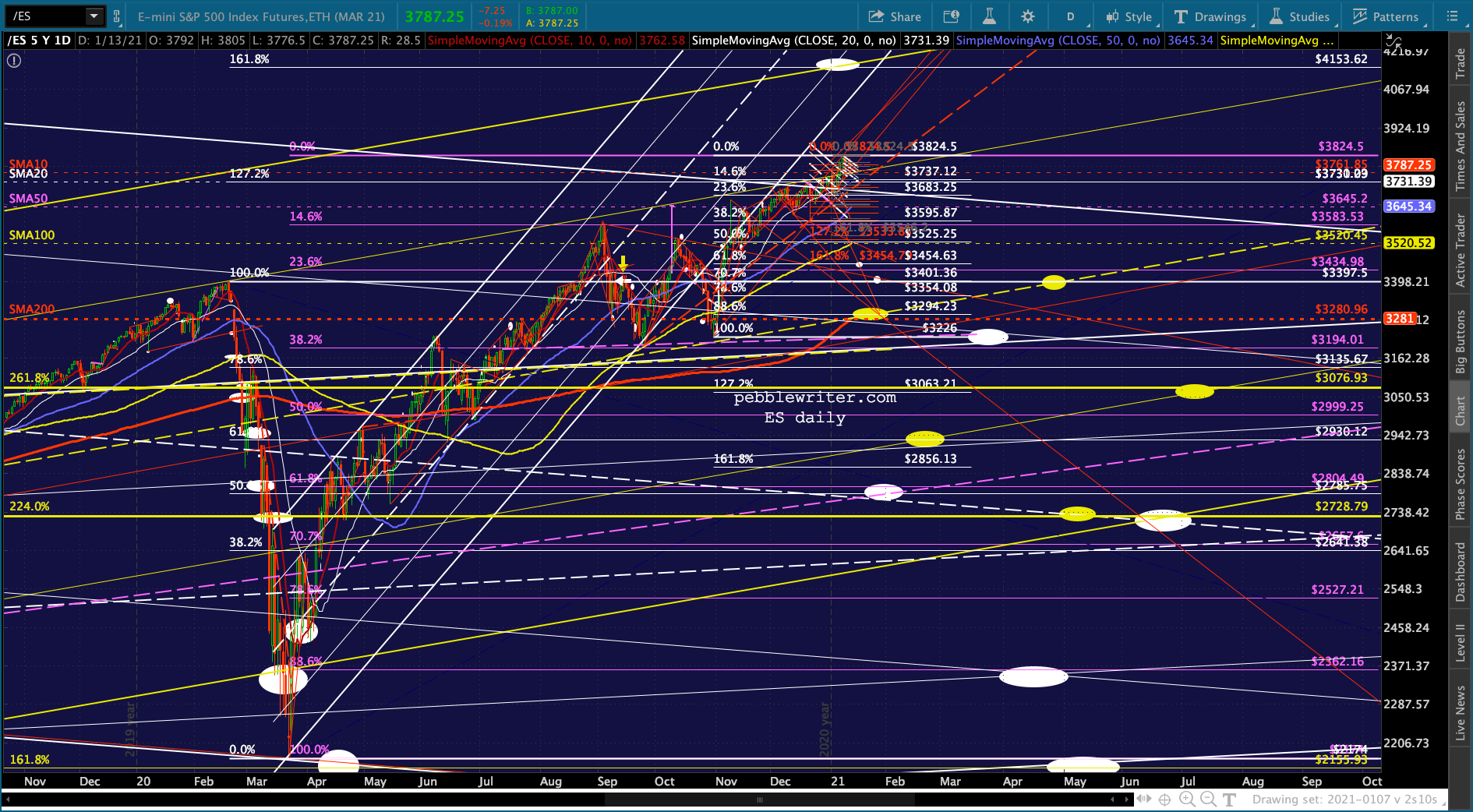

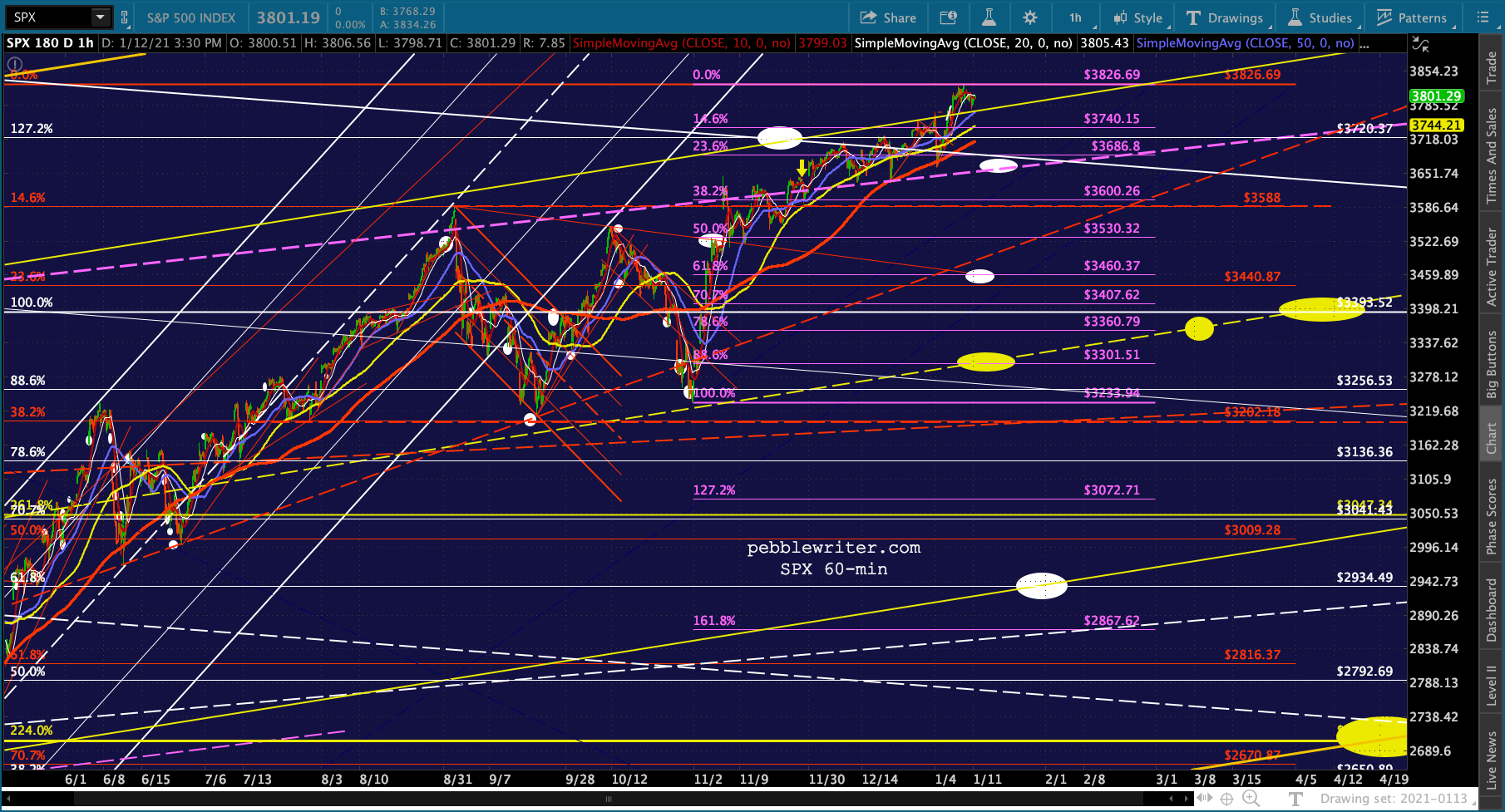

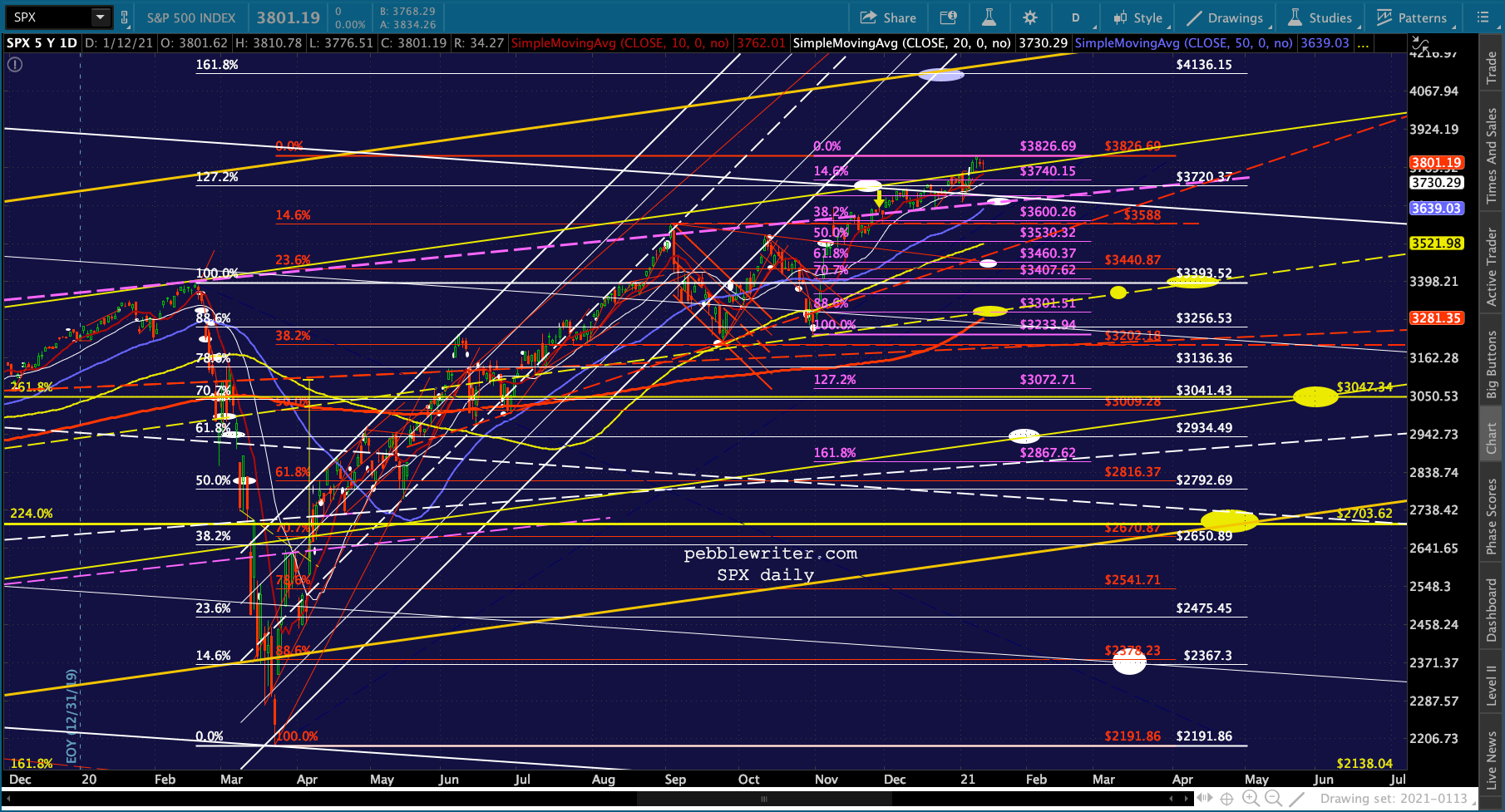

And, EURUSD continues its decline.  If all continues as it seems to, ES has established a parallel falling white channel which should reach its 1.272 backtest at 3730 either Friday or Monday. But, there’s a very good case for it not holding – with 3718 looking really good in the same time frame.

If all continues as it seems to, ES has established a parallel falling white channel which should reach its 1.272 backtest at 3730 either Friday or Monday. But, there’s a very good case for it not holding – with 3718 looking really good in the same time frame. If the dashed red TL breaks down, I continue to like ES 3294/SPX 3301 around, ahem, inauguration day.

If the dashed red TL breaks down, I continue to like ES 3294/SPX 3301 around, ahem, inauguration day.

As we’ve discussed over the past several months, the rally in oil and gas prices continues to be extremely important to the inflation picture.

As we’ve discussed over the past several months, the rally in oil and gas prices continues to be extremely important to the inflation picture.

December CPI came in at 0.4% MoM and 1.4% YoY versus 1.17% and -0.06% for November. The rapid rise was a primarily a function of rising gas prices (+8.4% MoM) and food prices (0.4% MoM, 3.9% YoY.) Core came in at 0.1% MoM and remained at 1.6% YoY for the third consecutive month.

The Fed can talk about core inflation all they like, but real people pay real money for food and gas and the increases will bite – particularly in April and May, unless gas prices drop about 40%.

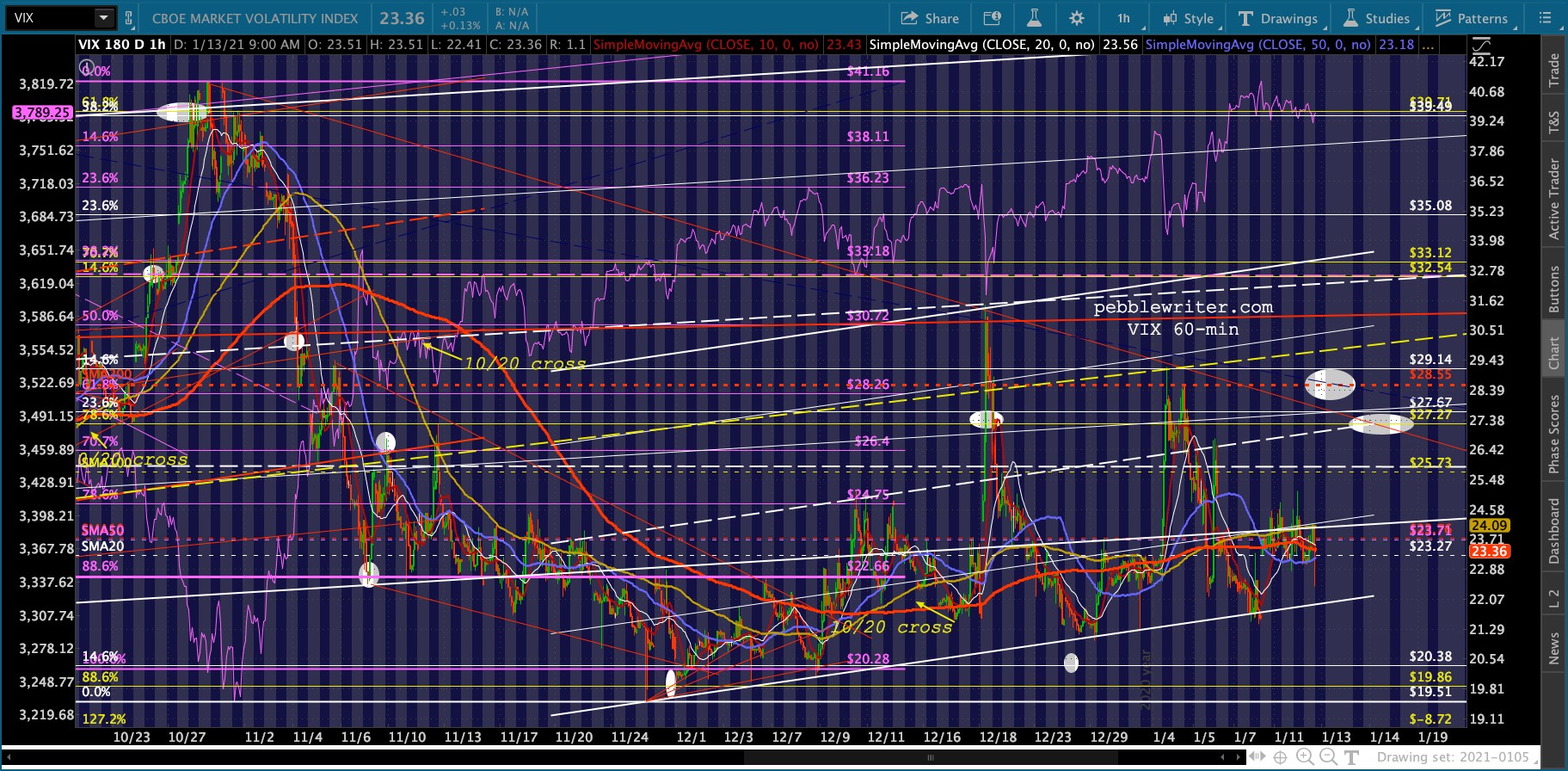

Just like yesterday, look for VIX to attempt to moderate any declines.

Just like yesterday, look for VIX to attempt to moderate any declines.