PCE increased 0.2% MoM and 2.6% YoY in December, in line with most estimates. Core PCE increased 2.9% YoY. This is the smallest gain since Mar 2021. Drilling down, goods rose 1.1% (durable goods 1.5%) in December while services rose 0.3%.

Real PCE rose 3.2% YoY, with the goods category growing 5% and durable goods rising 8.5%.

At 0.7% MoM, personal spending rose substantially more than the 0.4% estimates (and prior.) Spending rose 4.2% YoY, a slight decrease from November’s 4.4%.

December pending home sales far outpaced estimates at +8.3% versus 2.0% and -0.3% prior. The annual increase was much less frothy at 1.3%. The monthly beat was paced by 11.9% and 14.0% gains in the South and West respectively. Sales dropped 3.0% in the Northeast.

Futures are off slightly after rebounding from their overnight lows.

continued for members…

continued for members…

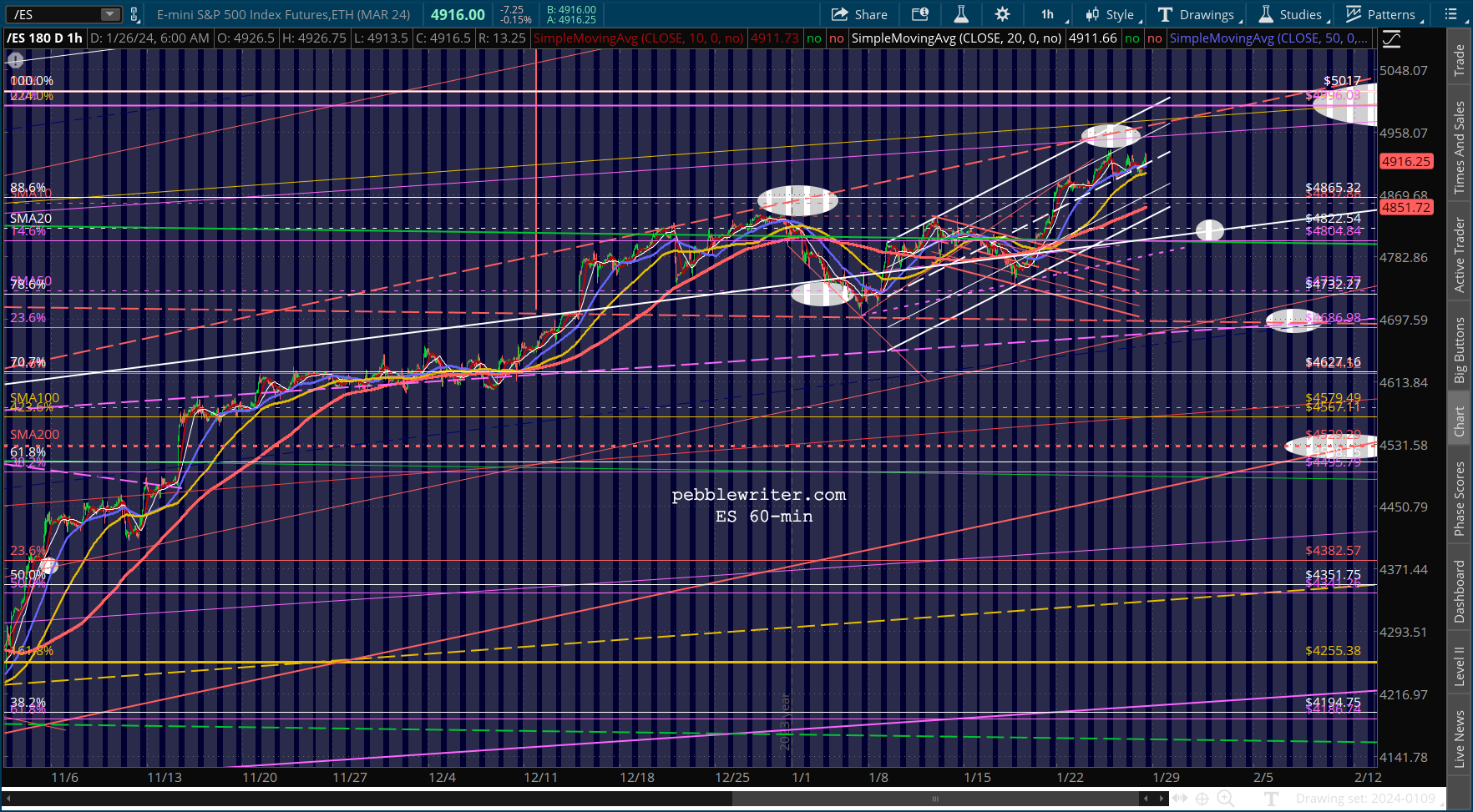

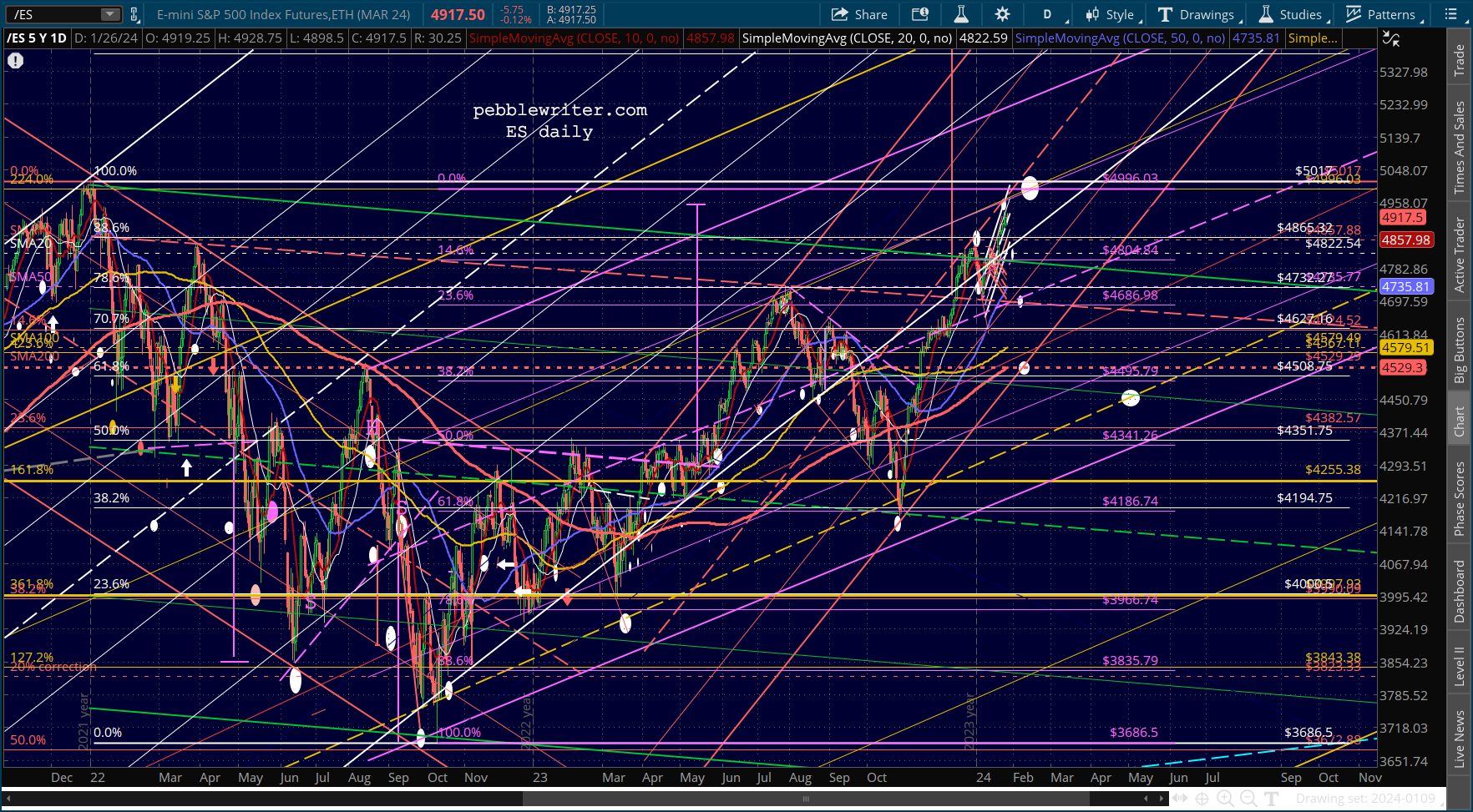

We continue to be susceptible to a 5% correction, though the signs of its likelihood remain quite muddled.

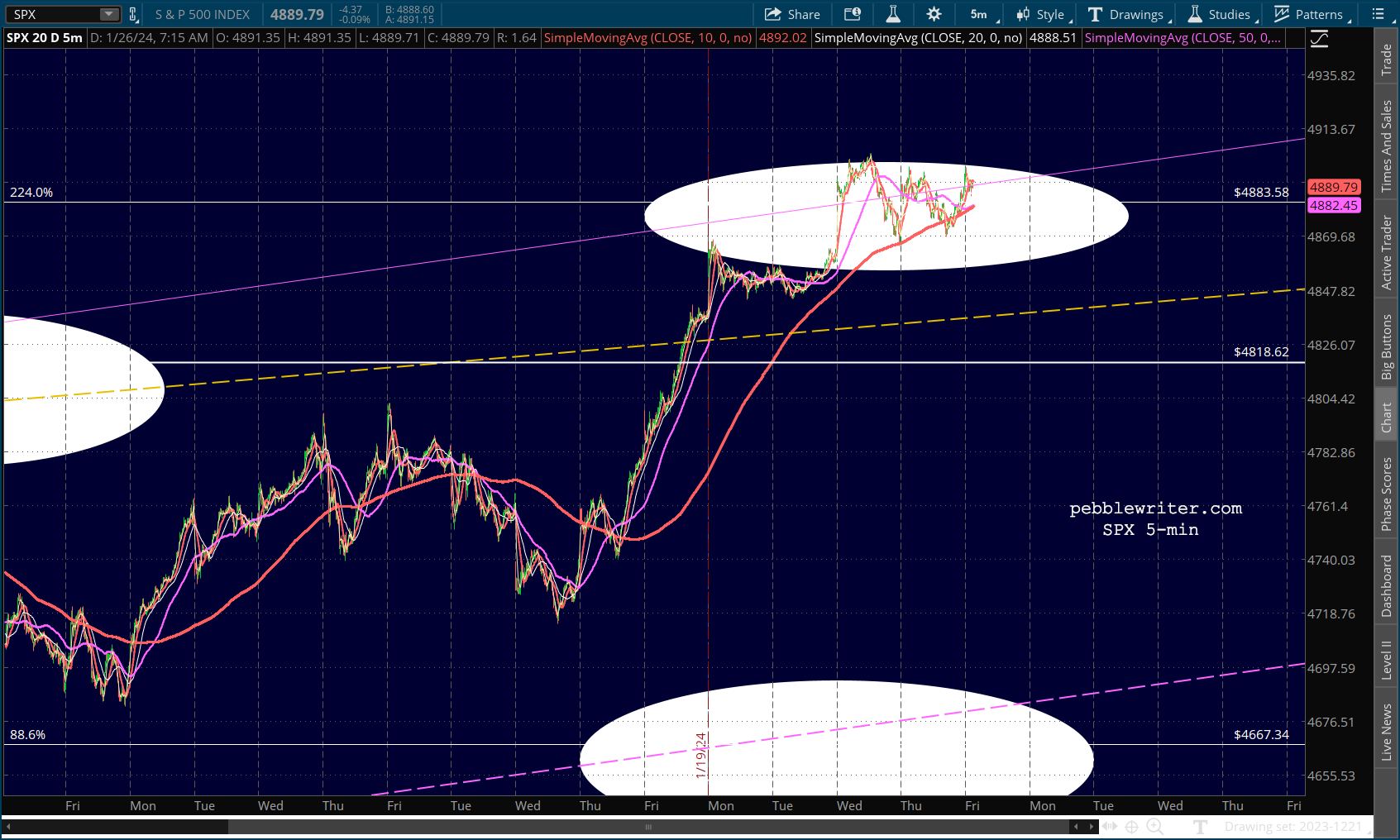

SPX continues to dance around its 2.24 Fib, leaving traders confused as to next moves. For a correction to get underway, it needs to break down below 4883. It has done so twice so far, but has rebounded both times.

SPX continues to dance around its 2.24 Fib, leaving traders confused as to next moves. For a correction to get underway, it needs to break down below 4883. It has done so twice so far, but has rebounded both times.

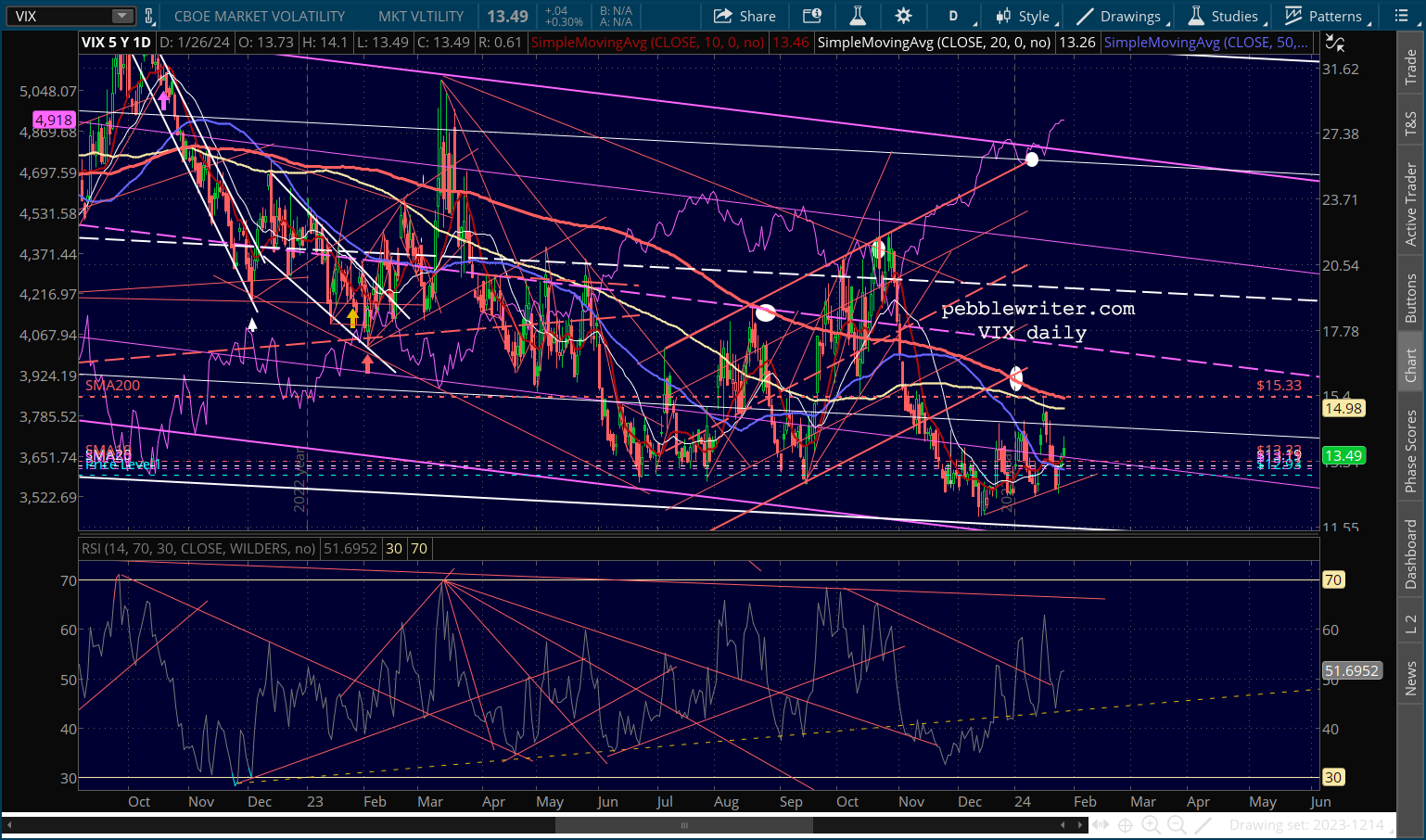

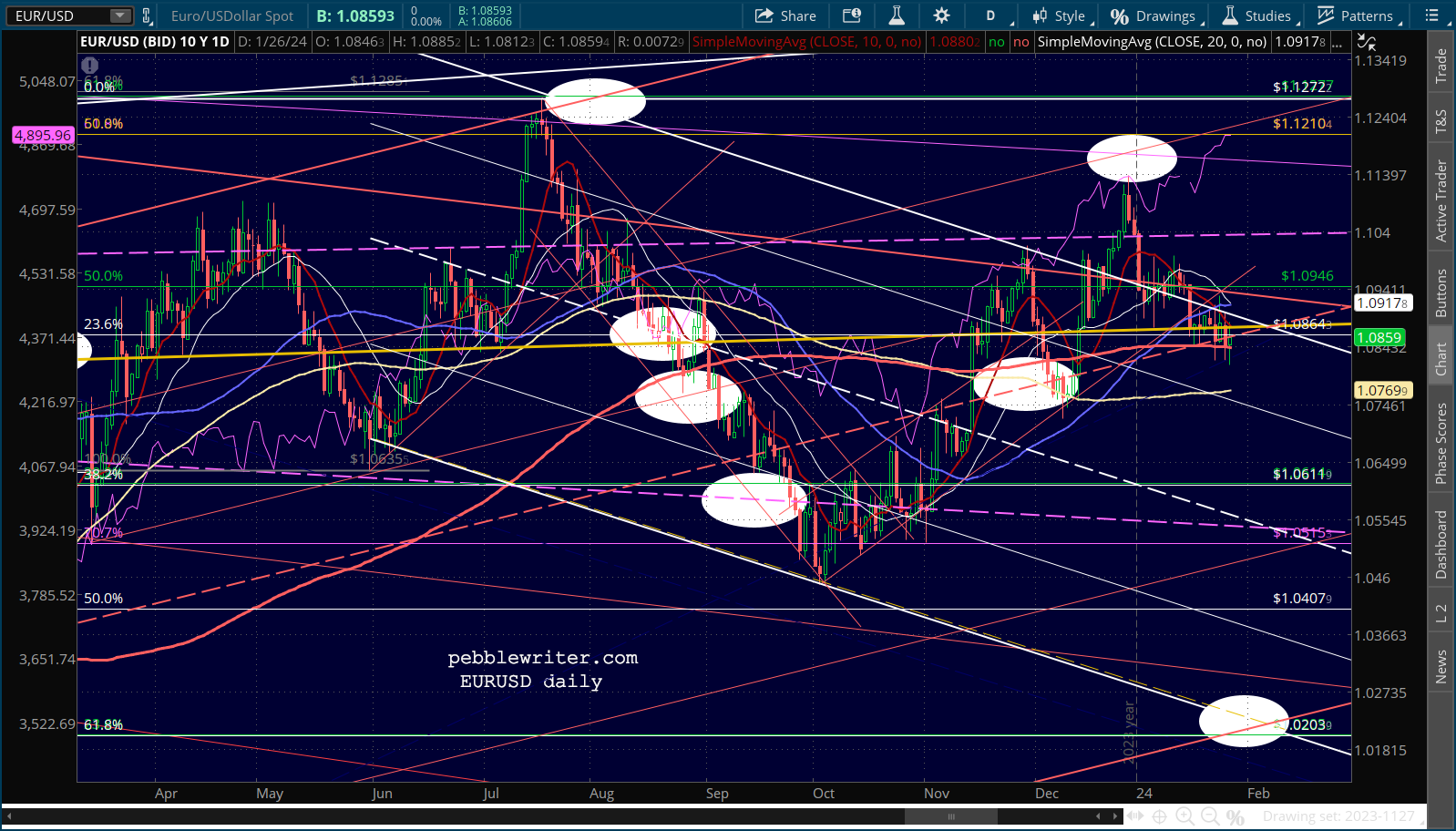

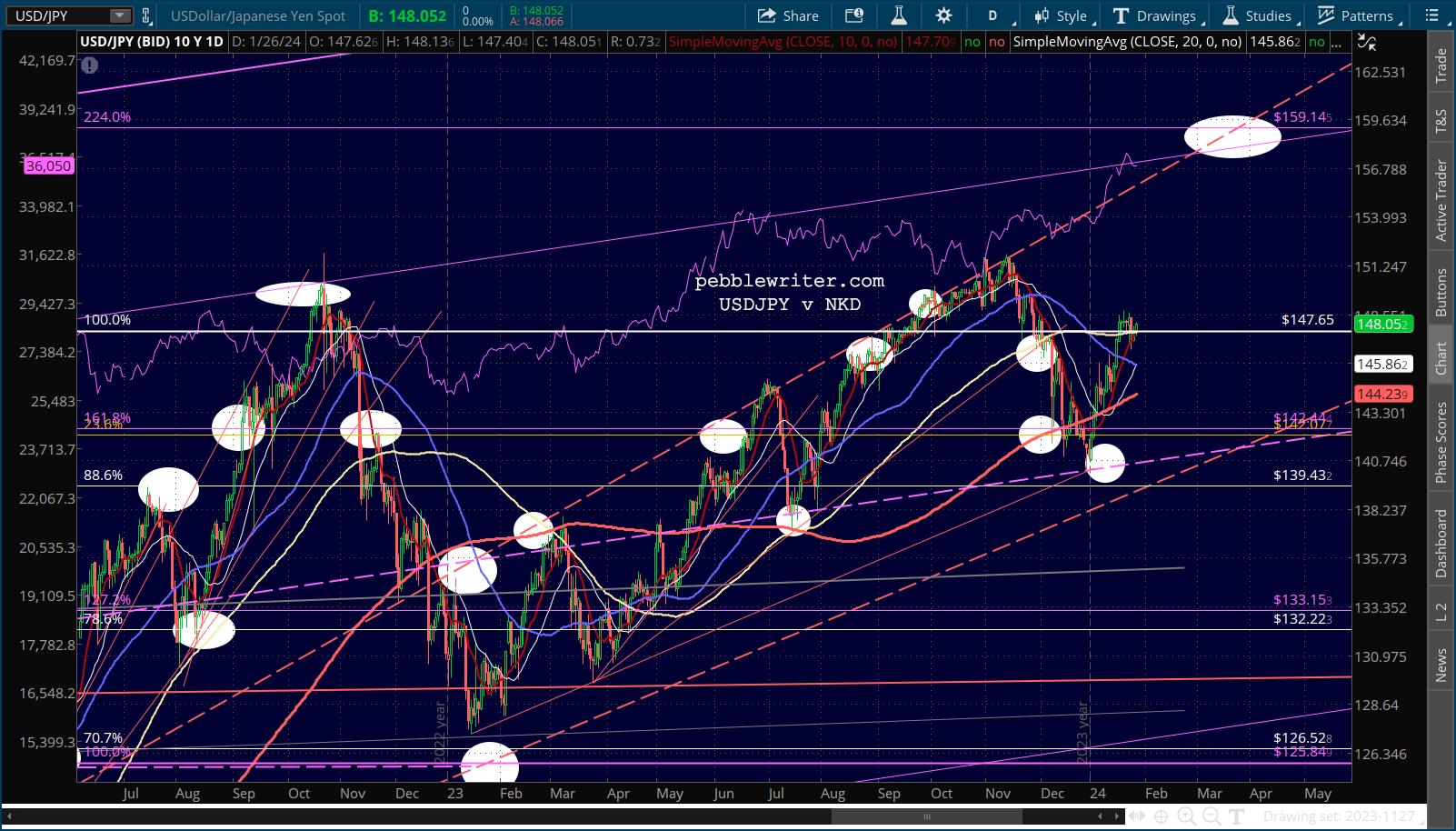

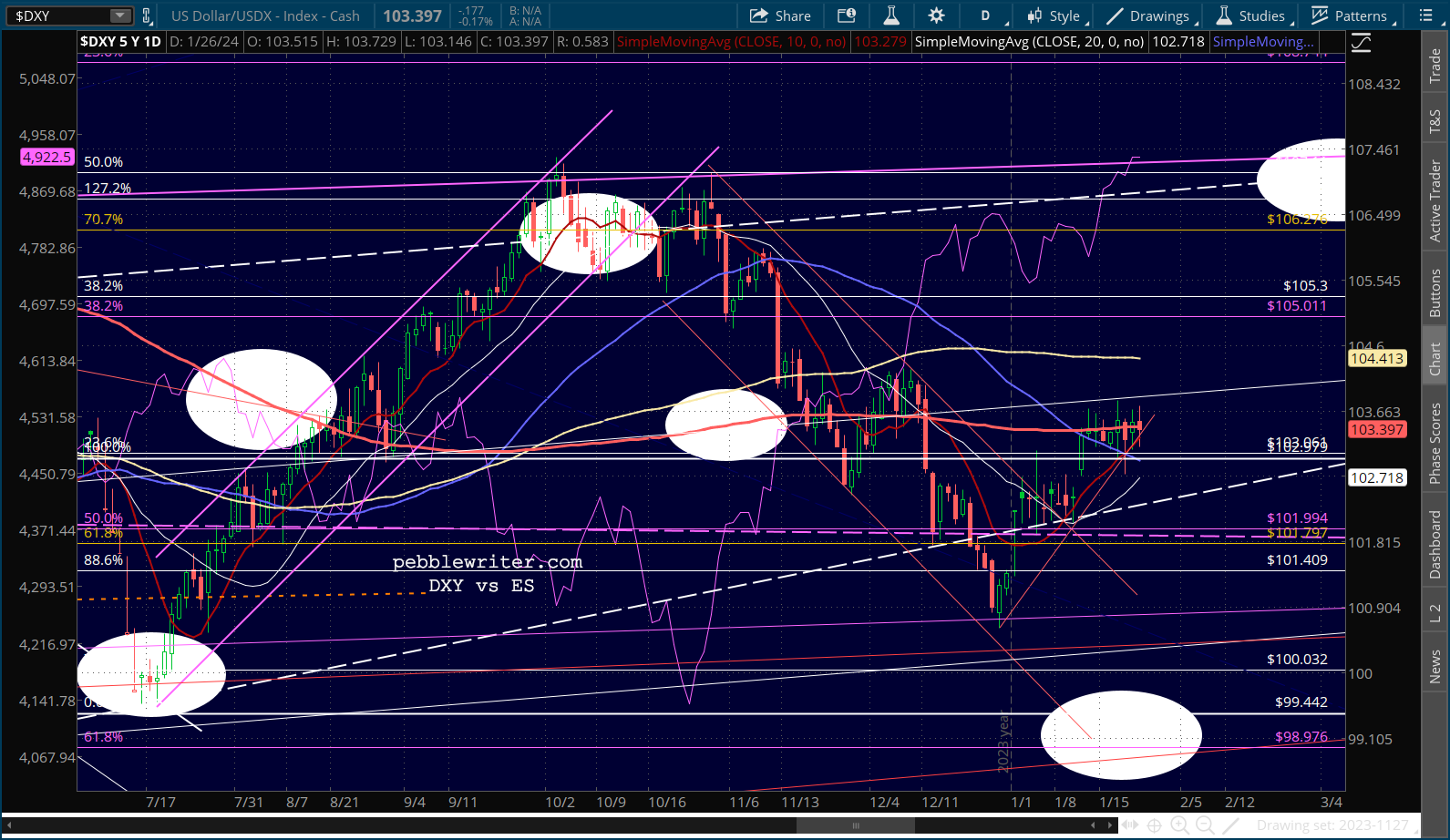

Likewise, VIX is above all its short-term moving averages, which are positively aligned, but is up only slightly on the session. Currencies are no help at all in solving the directional question, as EURUSD and DXY remain glued to their SMA200s and USDJPY is still going sideways.

Currencies are no help at all in solving the directional question, as EURUSD and DXY remain glued to their SMA200s and USDJPY is still going sideways.

Currencies are no help at all in solving the directional question, as EURUSD and DXY remain glued to their SMA200s and USDJPY is still going sideways.

Currencies are no help at all in solving the directional question, as EURUSD and DXY remain glued to their SMA200s and USDJPY is still going sideways.

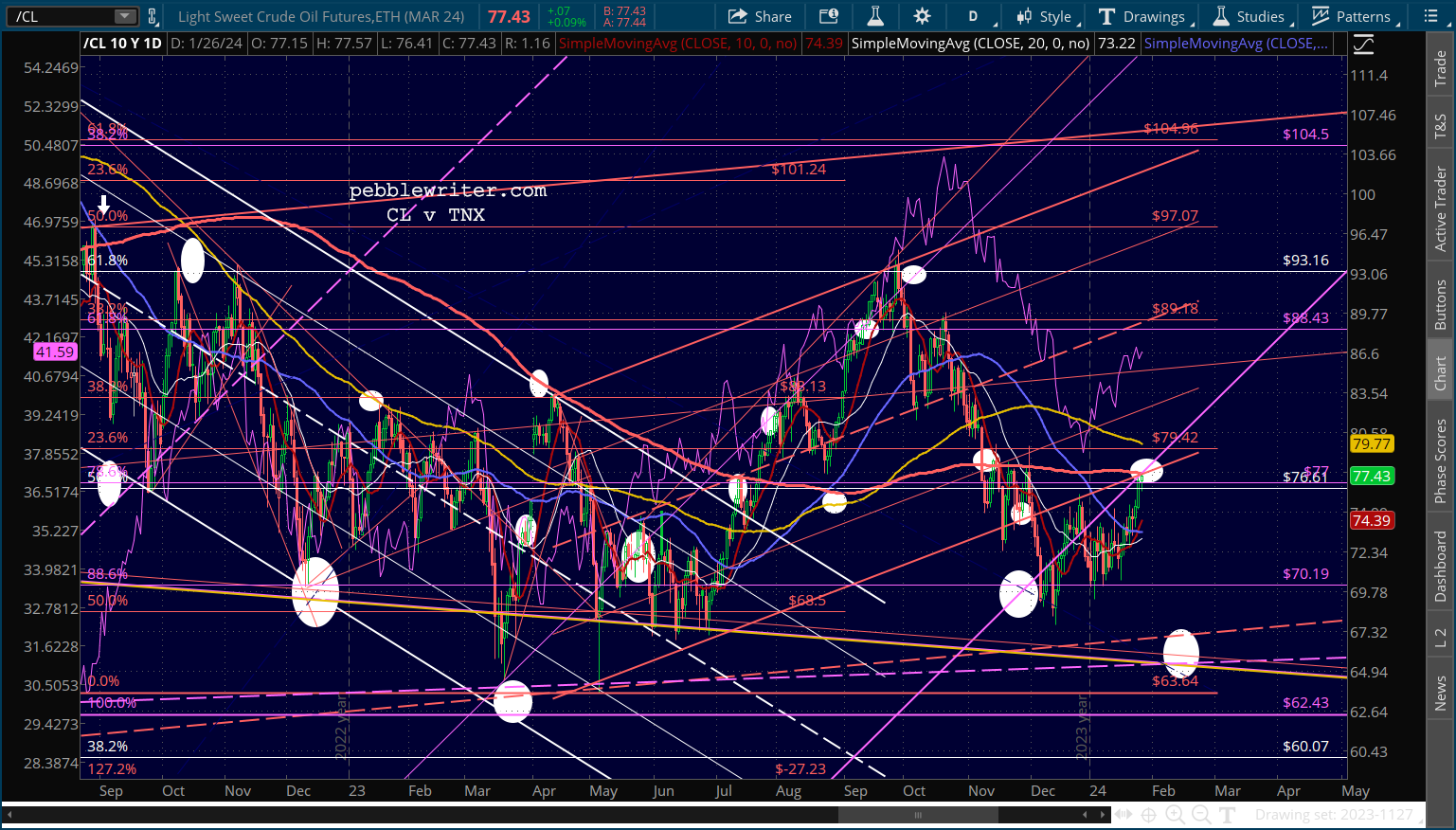

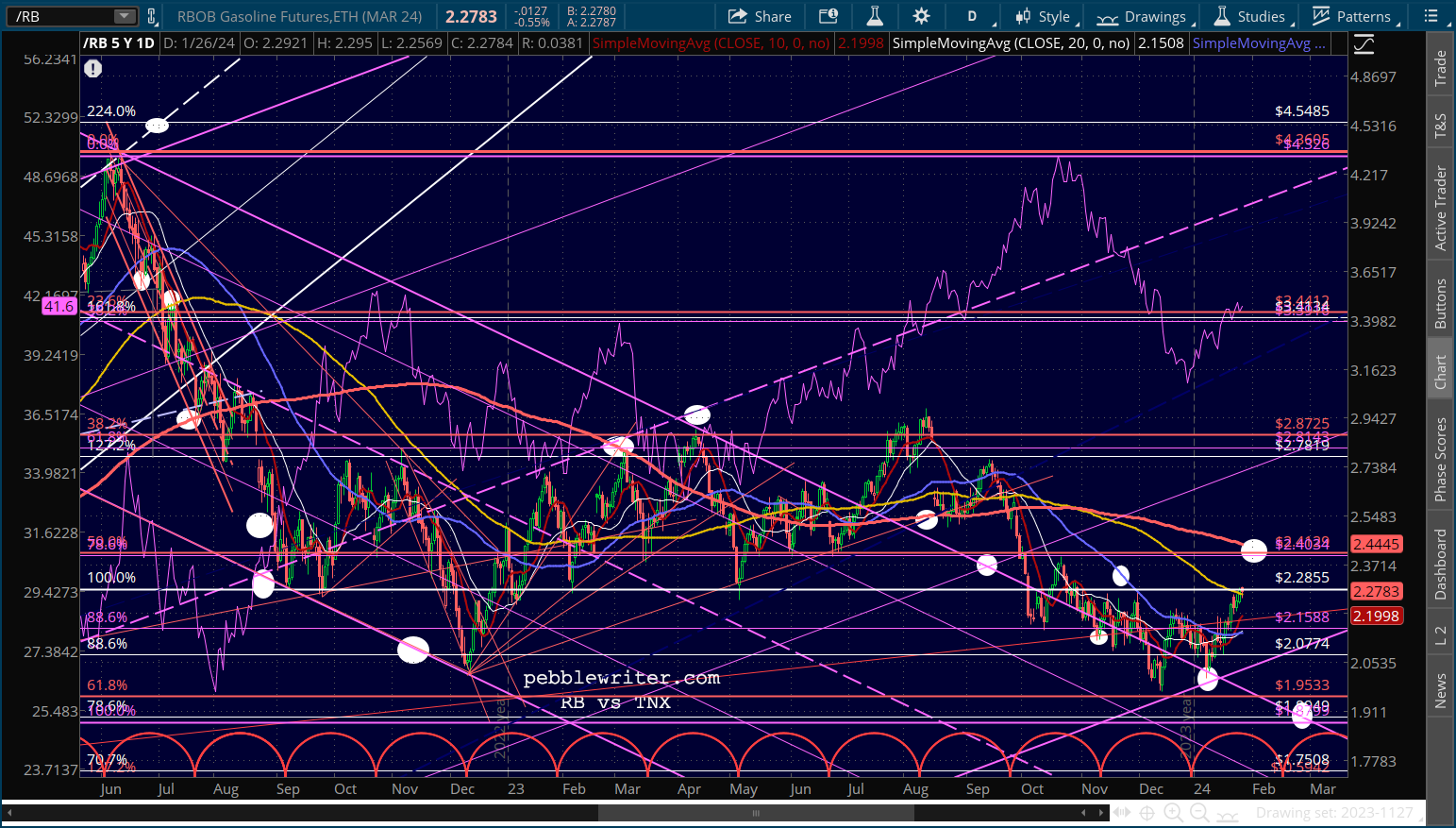

CL has officially reached its SMA200, so could be expected to pull back here. RB is still some way away from its SMA200, but has reached a level of some horizontal resistance.

CL has officially reached its SMA200, so could be expected to pull back here. RB is still some way away from its SMA200, but has reached a level of some horizontal resistance.

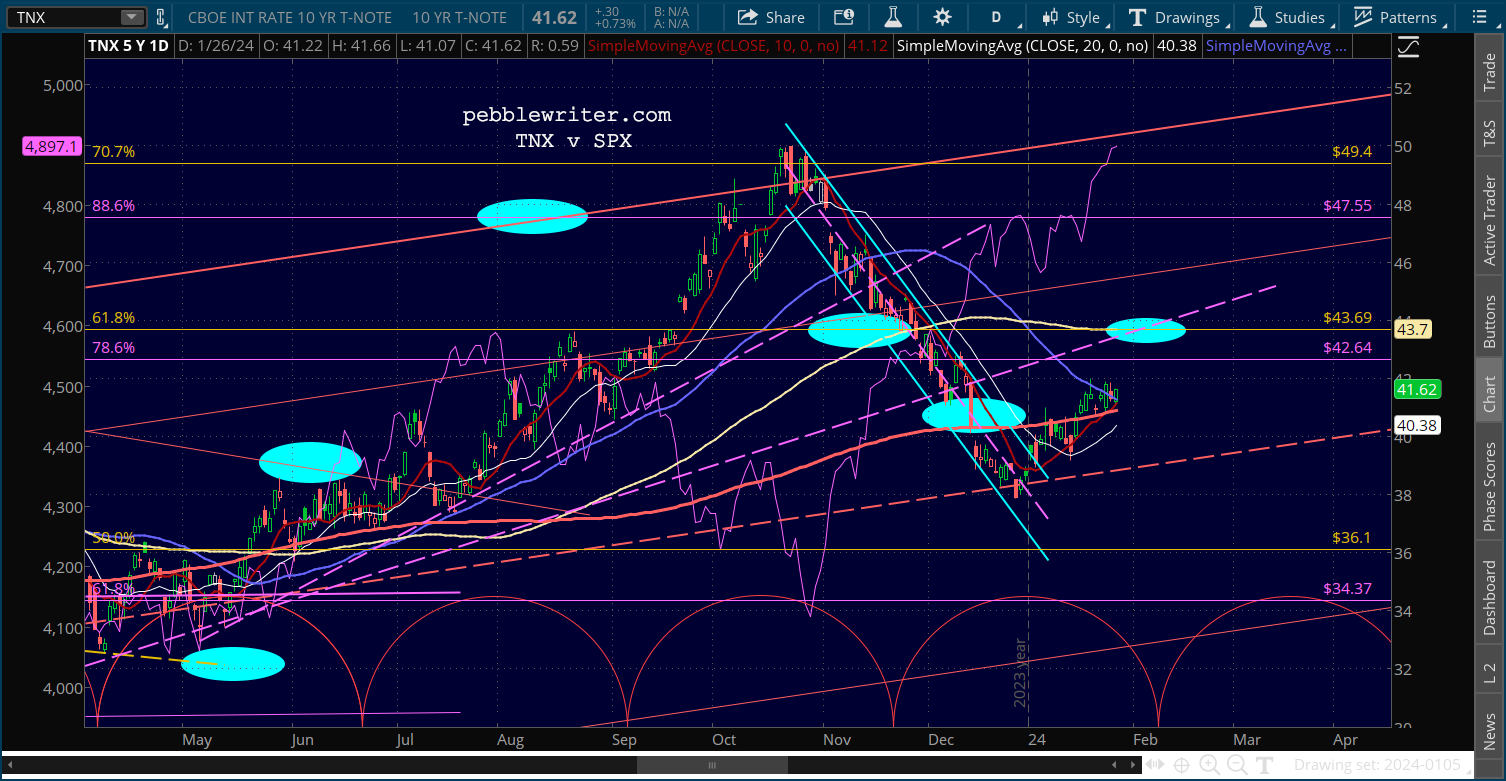

The 10Y continues to go sideways just above its SMA200, with a backtest at 4.37 still a good possibility.

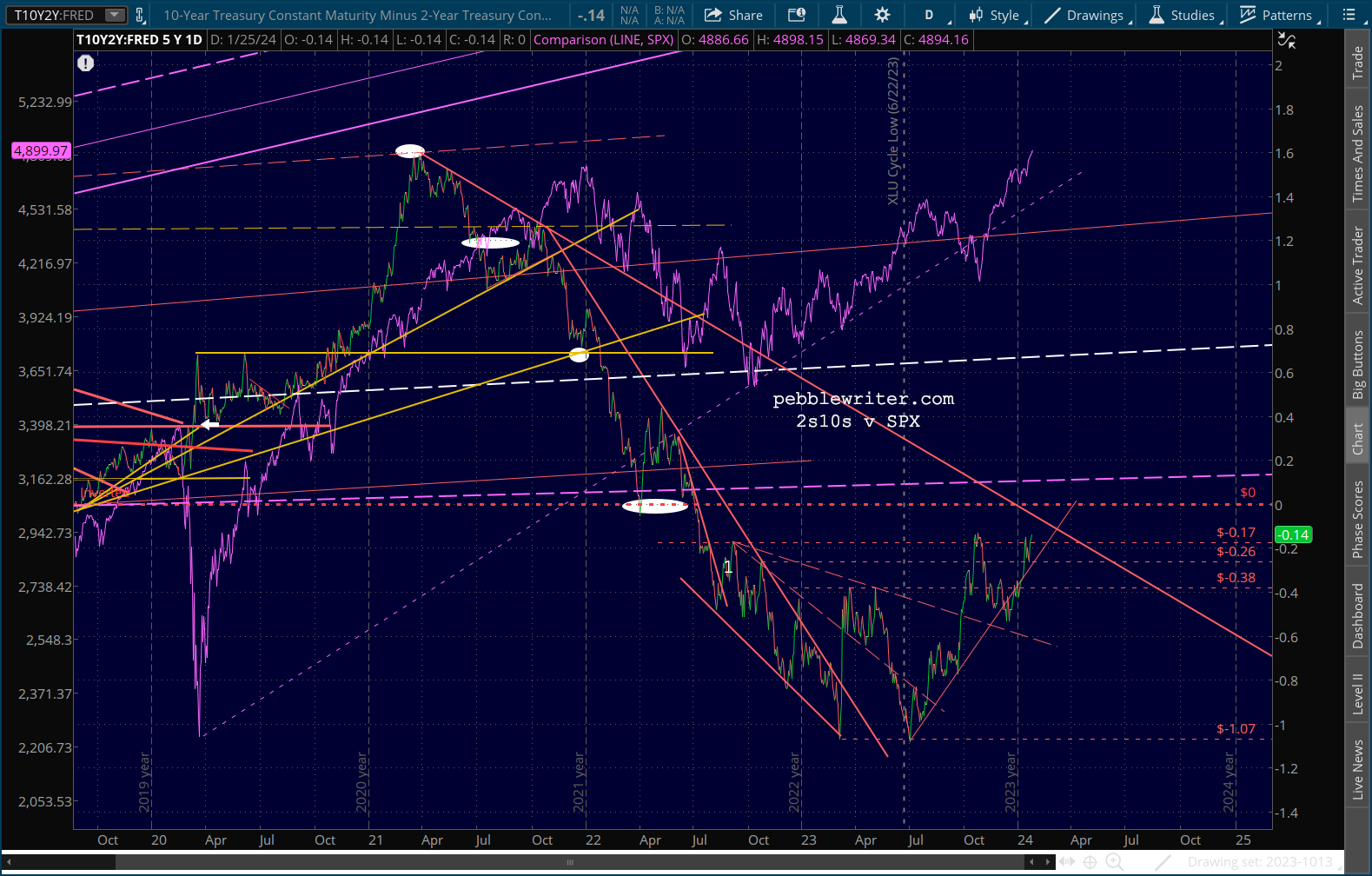

The 10Y continues to go sideways just above its SMA200, with a backtest at 4.37 still a good possibility. The 2s10s has resumed its climb back into positive territory. Remember, a push back above zero has traditionally meant a big downturn for stocks. Can this one be any different?

The 2s10s has resumed its climb back into positive territory. Remember, a push back above zero has traditionally meant a big downturn for stocks. Can this one be any different?The past crashes have typically featured sharp downturns in the 2Y while the 10Y has dropped less sharply.

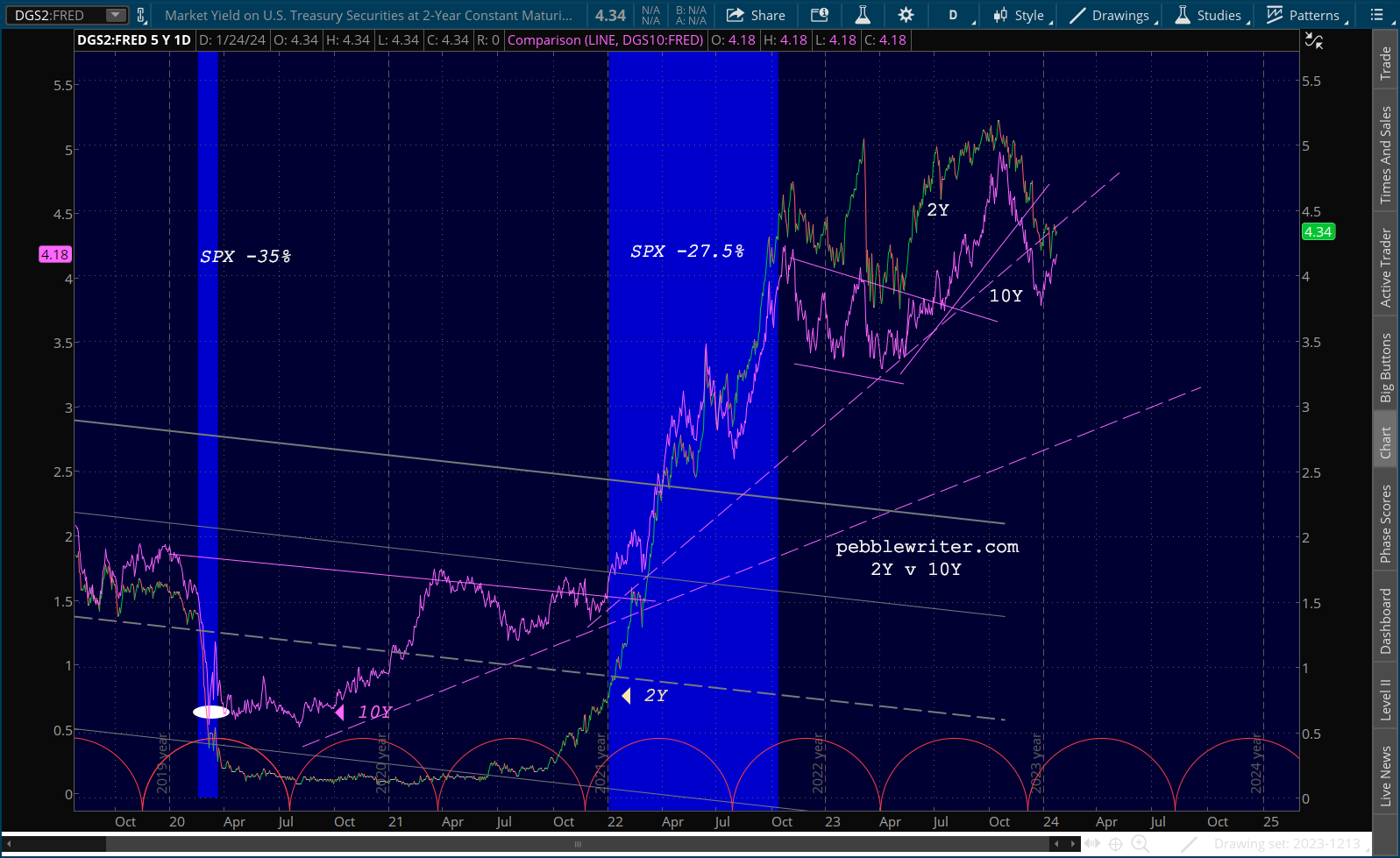

The 2Y has obviously been weaker than the 10Y, but the drop hasn’t been very dramatic yet.

My apologies for the late post this morning. My internet is finally back up and seems to be working better than before.

My apologies for the late post this morning. My internet is finally back up and seems to be working better than before.Stay tuned…