ZN broke down from its rising red channel back on the 6th. Since then, it has found support in a falling channel – from which it is now threatening to break down. This is a moment of truth for bonds and the many correlated assets such as GC, shown above. Stocks might not be amused.

This is a moment of truth for bonds and the many correlated assets such as GC, shown above. Stocks might not be amused.

continued for members…

continued for members…

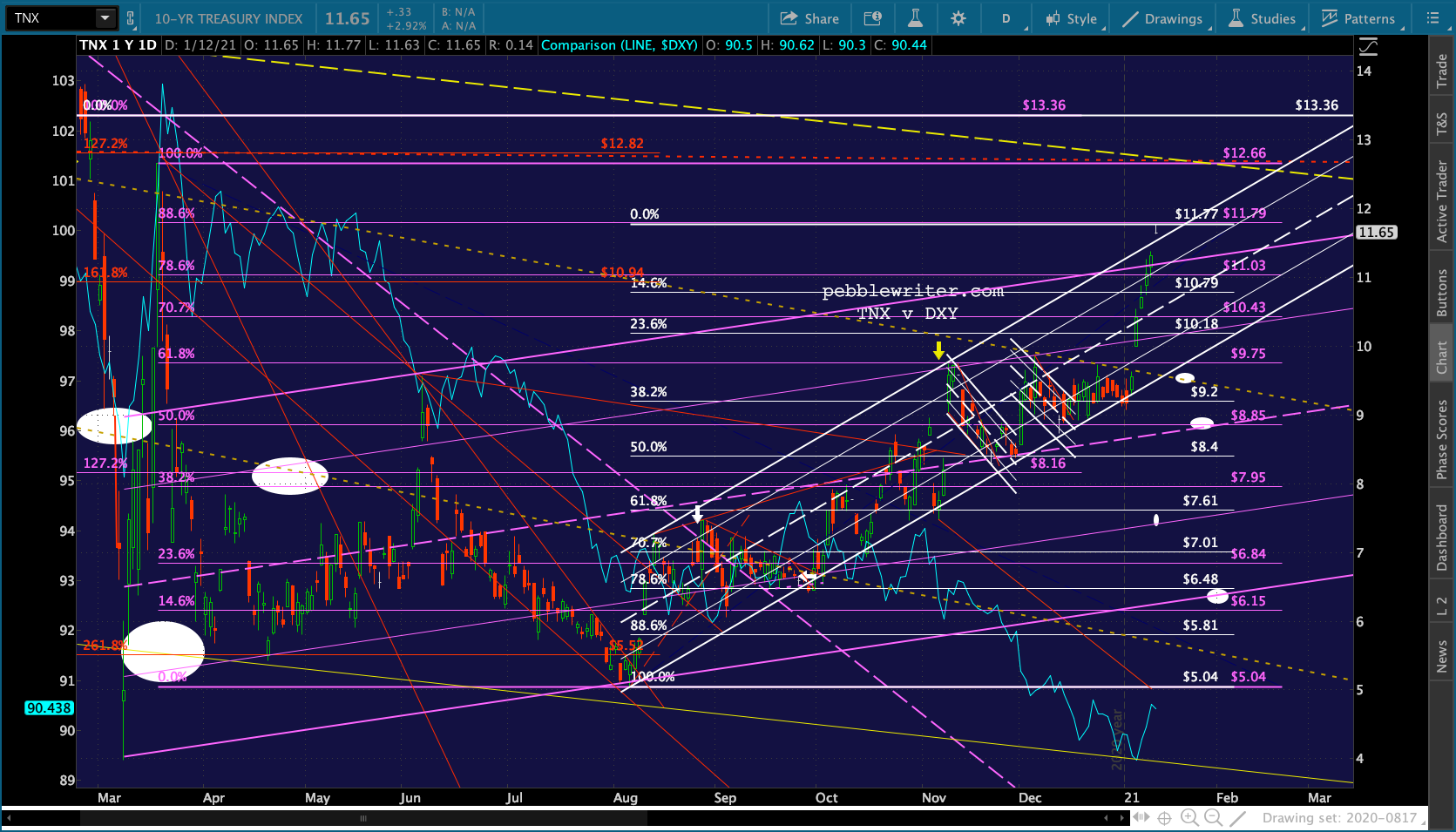

TNX broke out of its rising white channel and purple channel – but to tag a potential reversal at the purple .886 Fib (off the Mar 18, 2020 highs at 1.266.) ZN and DXY have at times been negatively correlated, but they both started bouncing on/around Jan 4.

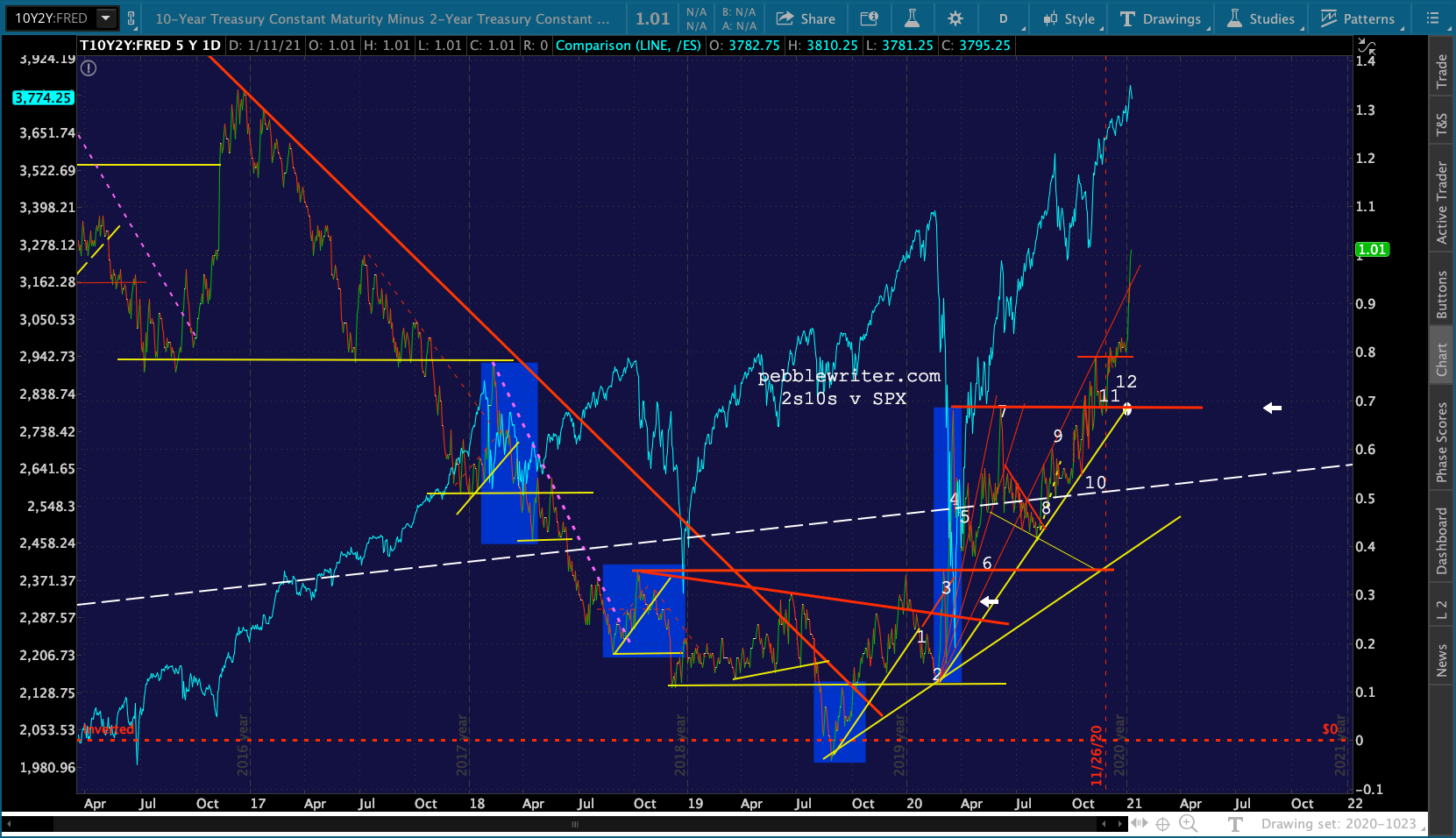

ZN and DXY have at times been negatively correlated, but they both started bouncing on/around Jan 4. Note that our yield curve model is still sounding the alarm – even more so than last week.

Note that our yield curve model is still sounding the alarm – even more so than last week.

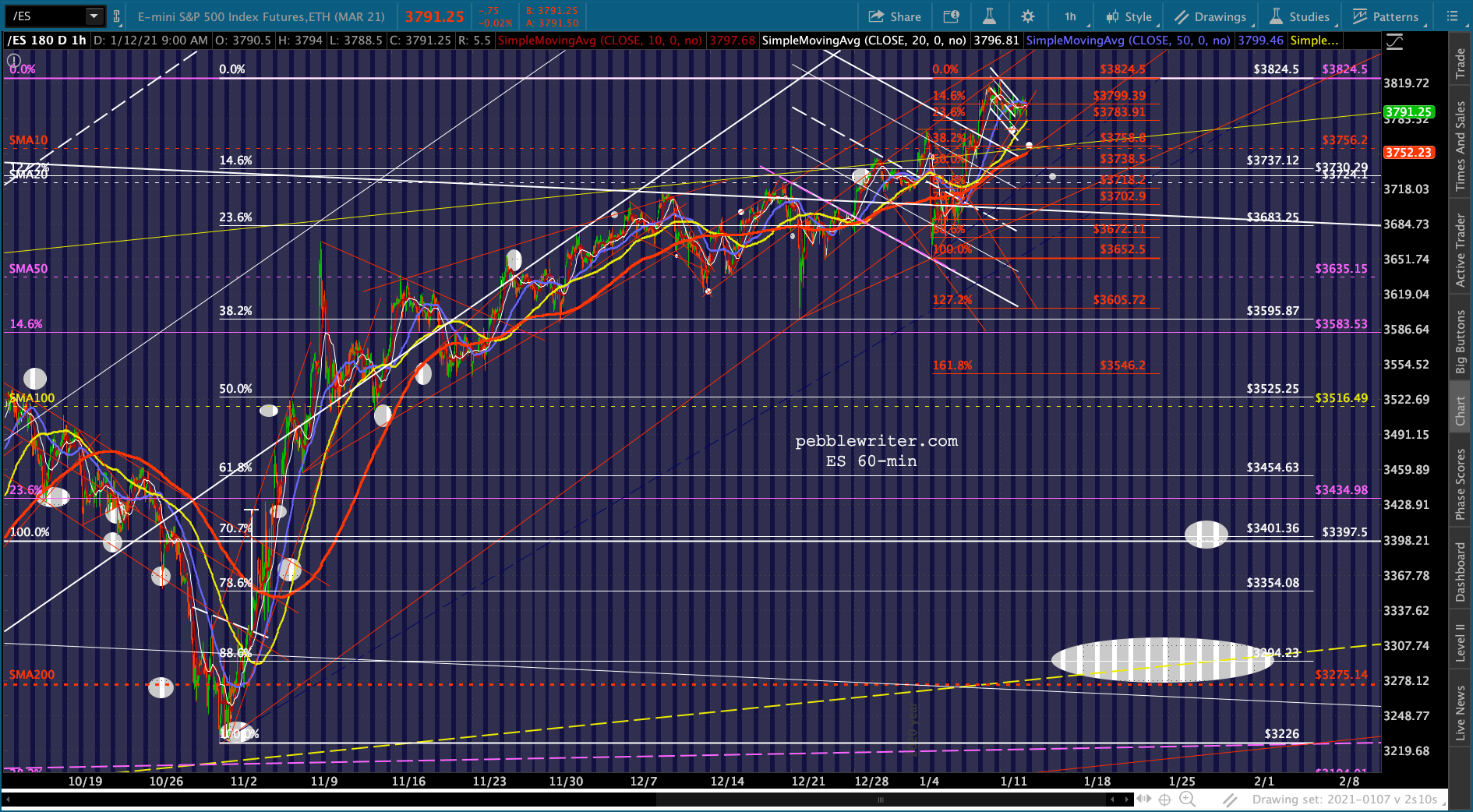

The picture for equities…

ES is threatening to break down, but has plenty of support to break through before any of these lower targets is a reality.

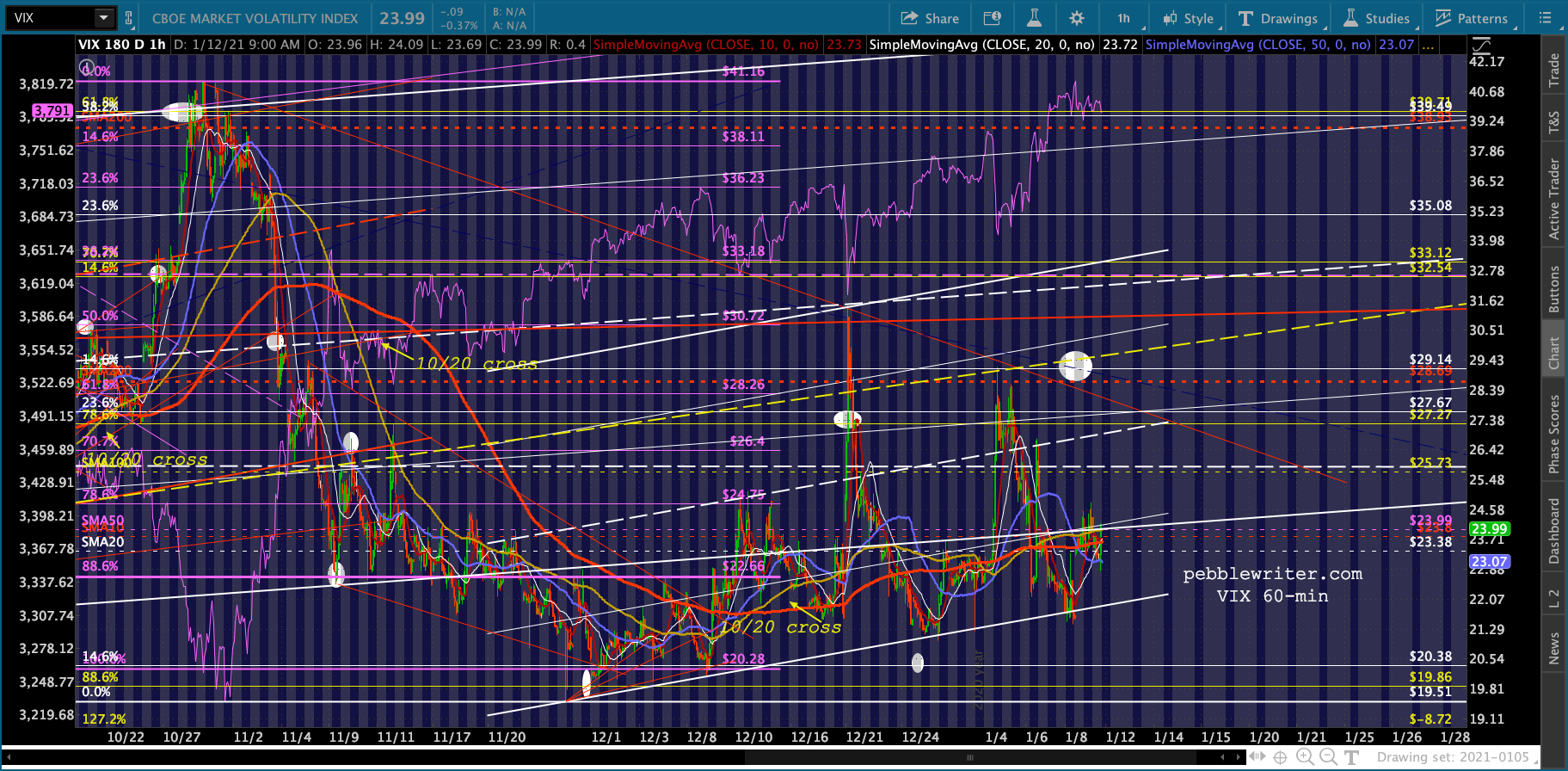

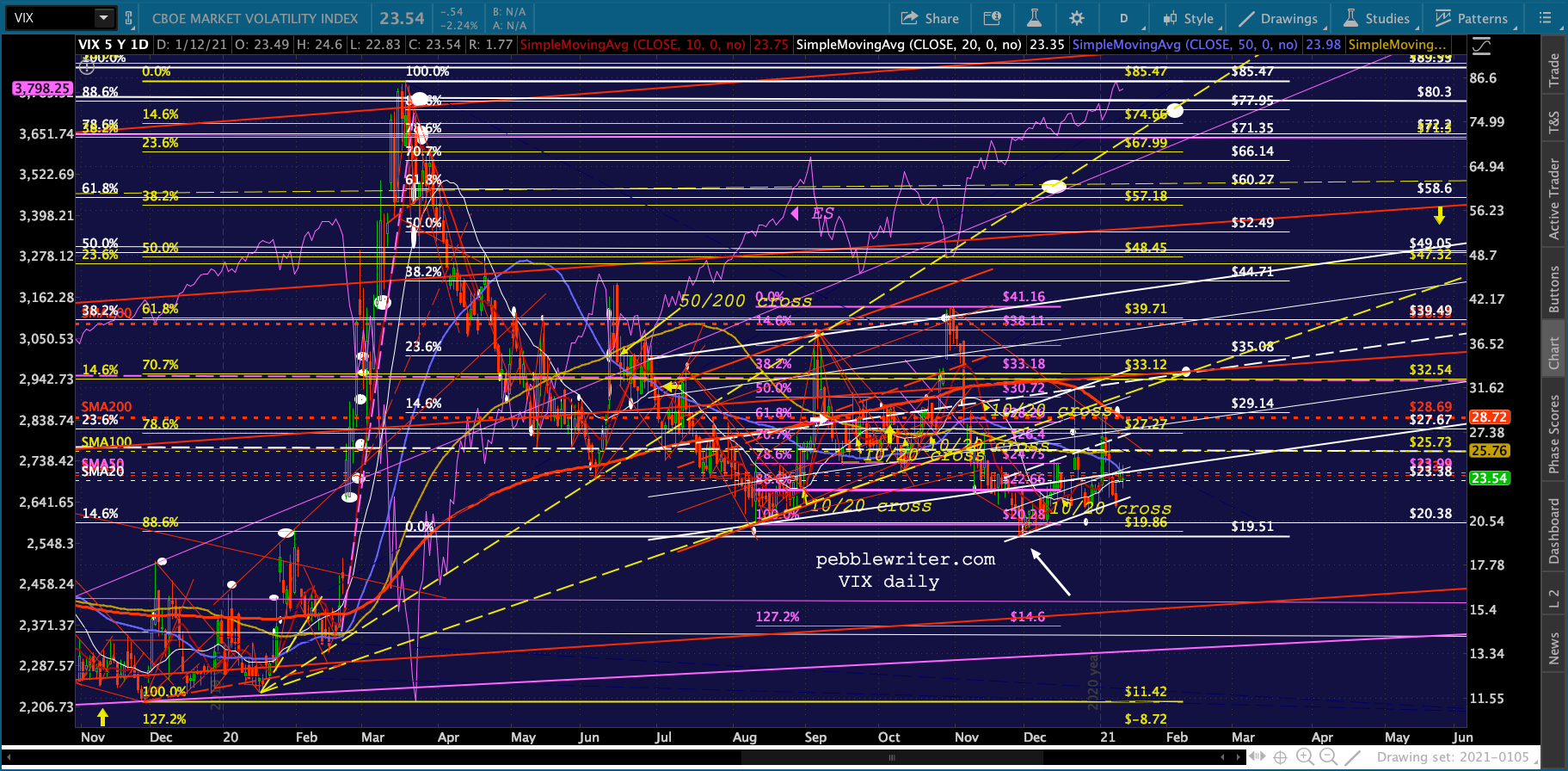

VIX continues to play an outsized role in directing the algos. By reversing at the red TL from Oct 29, sitting right at/below the SMA10, and the narrow margin by which the 10/20 remains bullish (bearish for stocks), VIX is sending a strong signal to the algos: don’t get (too) bearish.

VIX continues to play an outsized role in directing the algos. By reversing at the red TL from Oct 29, sitting right at/below the SMA10, and the narrow margin by which the 10/20 remains bullish (bearish for stocks), VIX is sending a strong signal to the algos: don’t get (too) bearish.

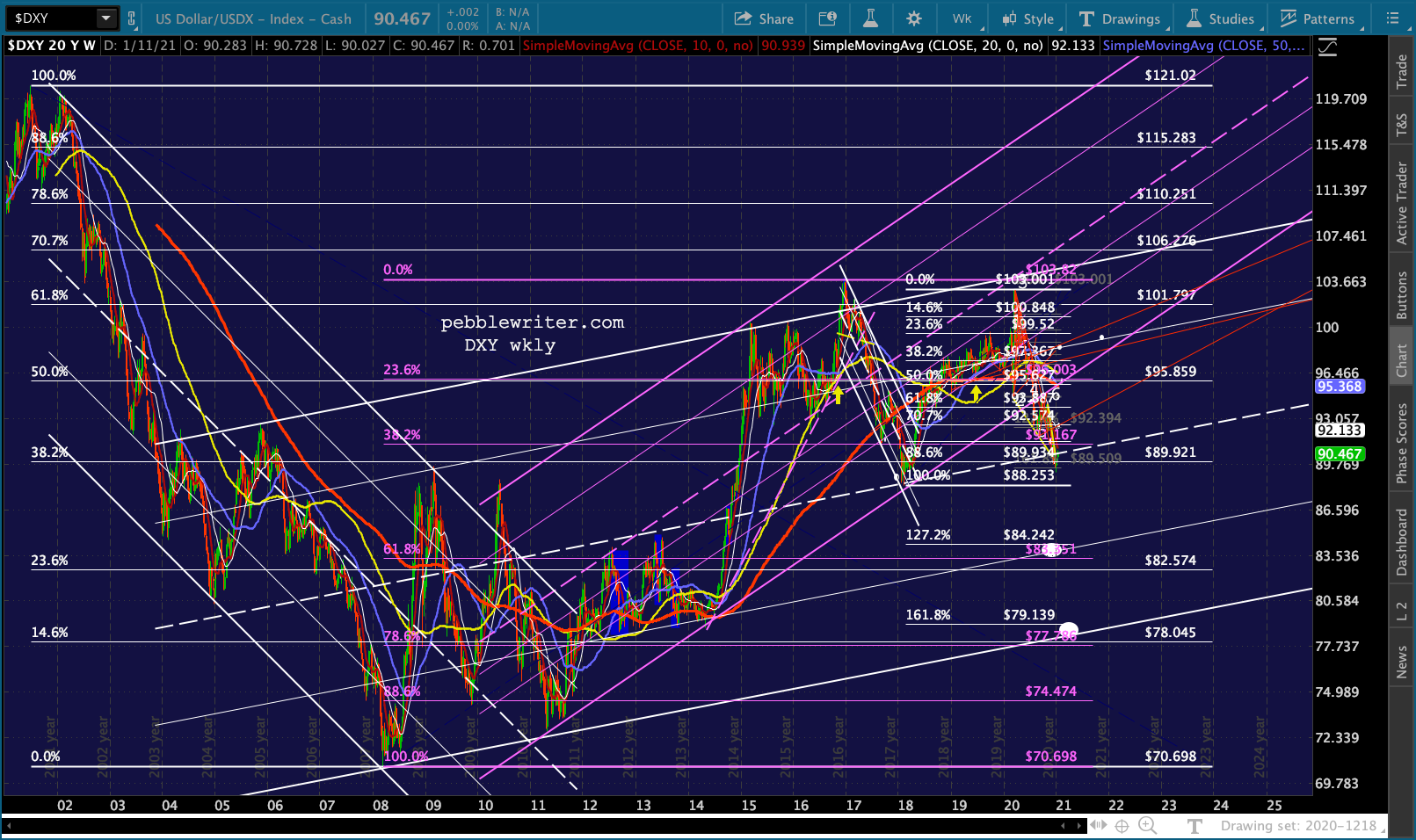

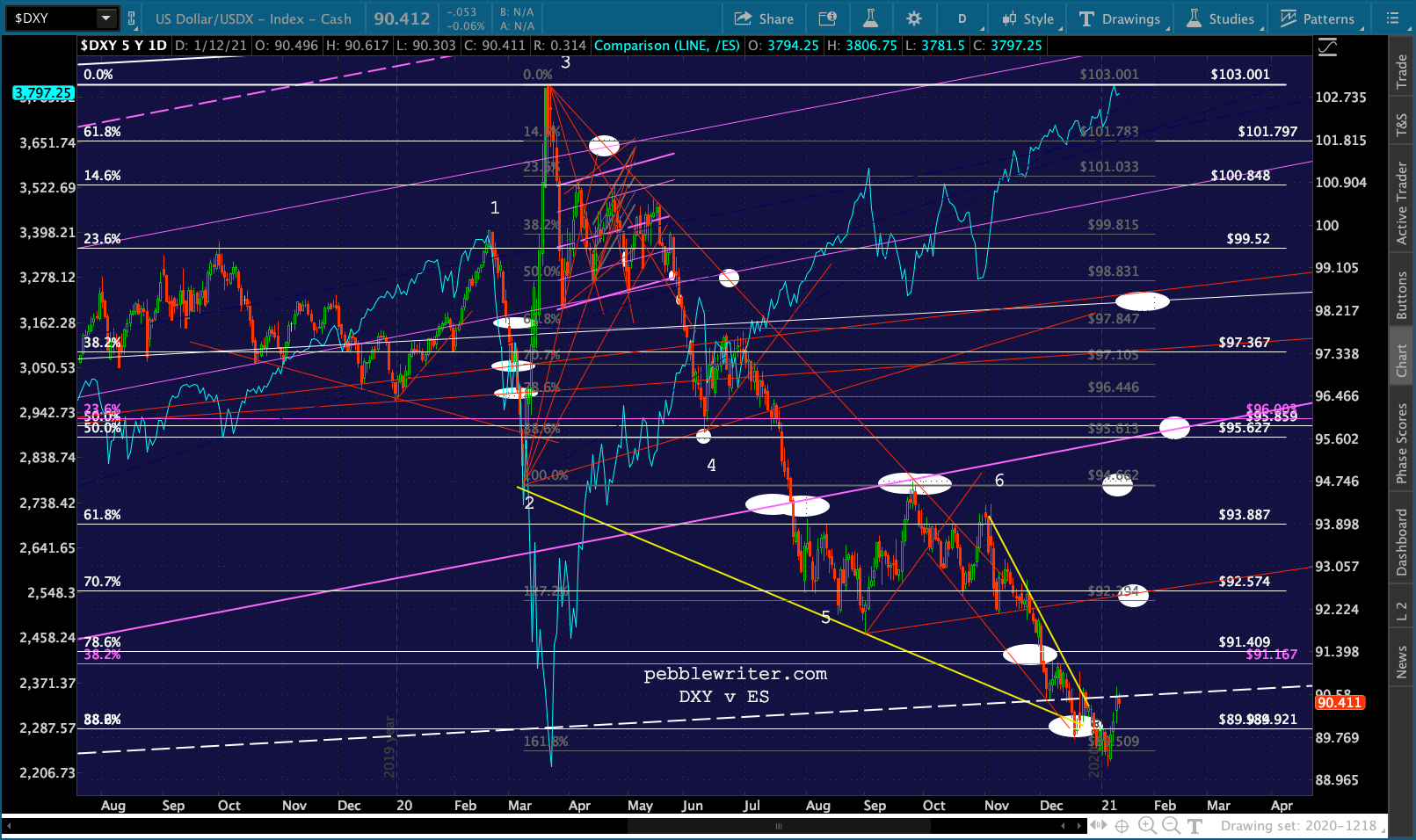

And, DXY has yet to get out of its own way…despite a good start.

And, DXY has yet to get out of its own way…despite a good start.  It is now backtesting the white channel midline from its 2008 lows. If it hovers in this area or goes lower, that would presumably be supportive of stocks.

It is now backtesting the white channel midline from its 2008 lows. If it hovers in this area or goes lower, that would presumably be supportive of stocks.

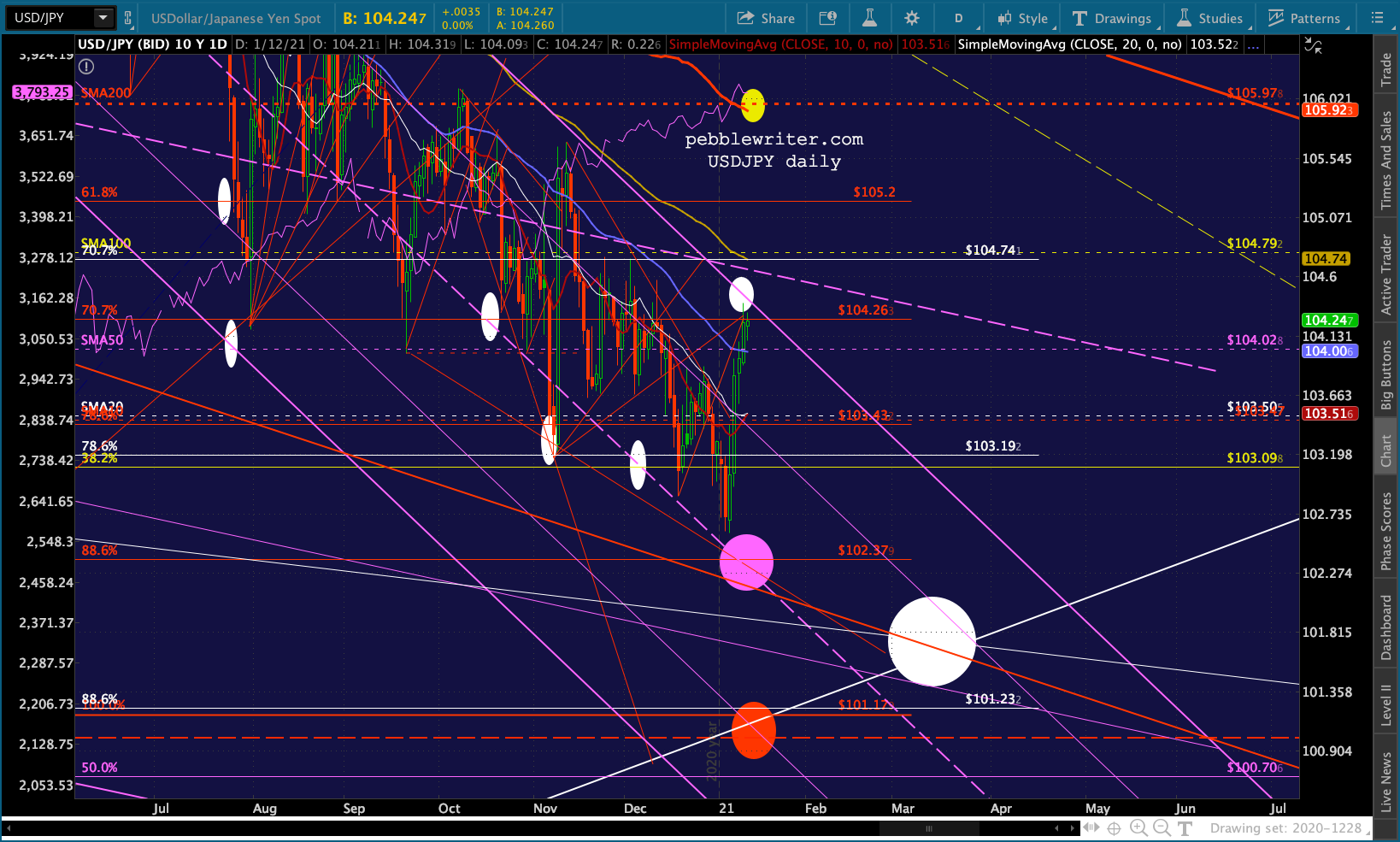

USDJPY continues to threaten a breakout from the falling purple channel – which would also at the very least provide some downside protection. The presence of the SMA200 is a reminder of its history of performing such actions.

USDJPY continues to threaten a breakout from the falling purple channel – which would also at the very least provide some downside protection. The presence of the SMA200 is a reminder of its history of performing such actions.

Let’s talk algos for a minute.

Let’s talk algos for a minute.

The falling US dollar was obviously an important element of stocks’ recovery post Mar 2020. The algos readily incorporate info like this.

They don’t much care why the dollar was falling, only that it was highly negatively correlated to stocks. Falling dollar = buy stocks.

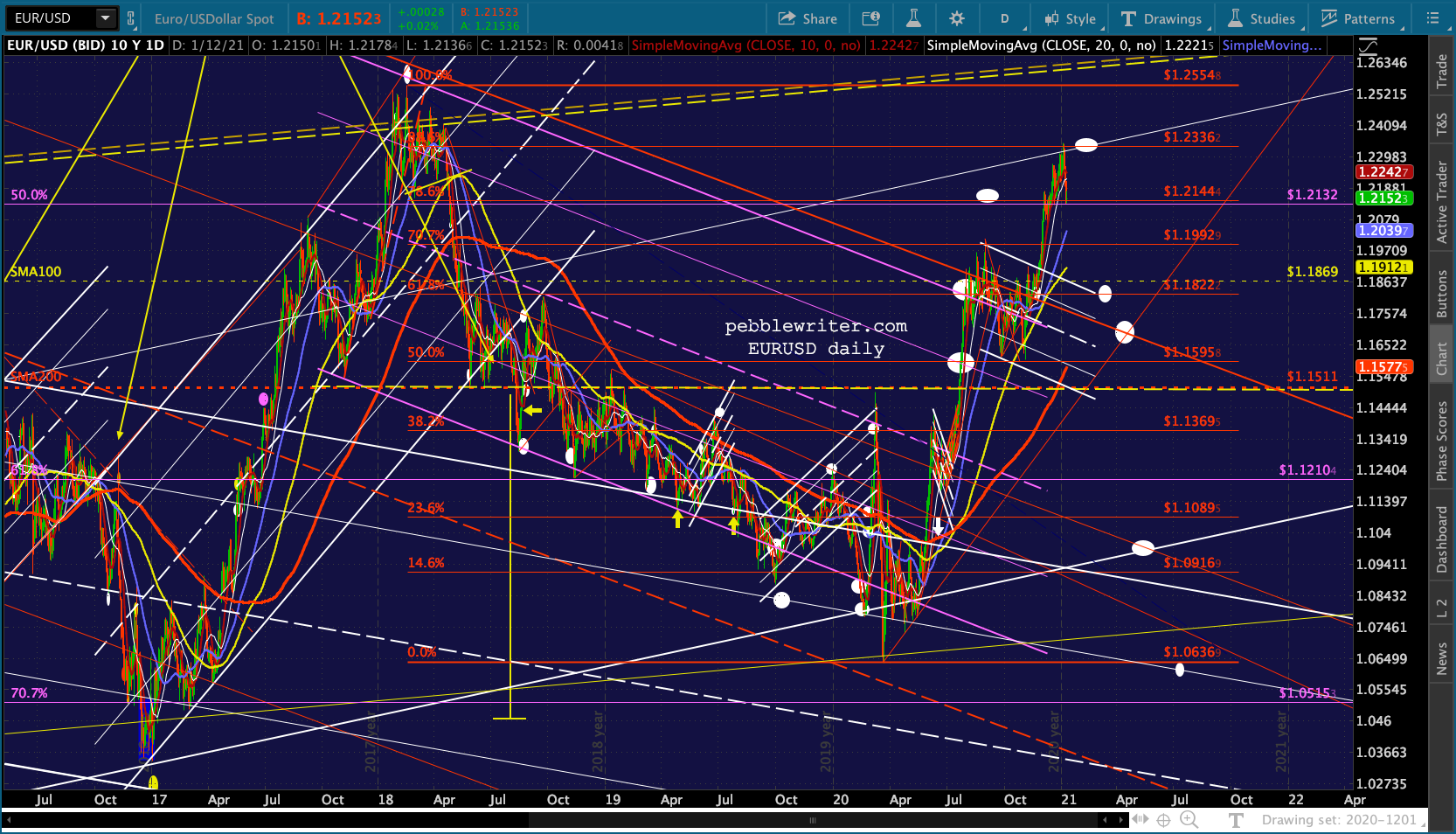

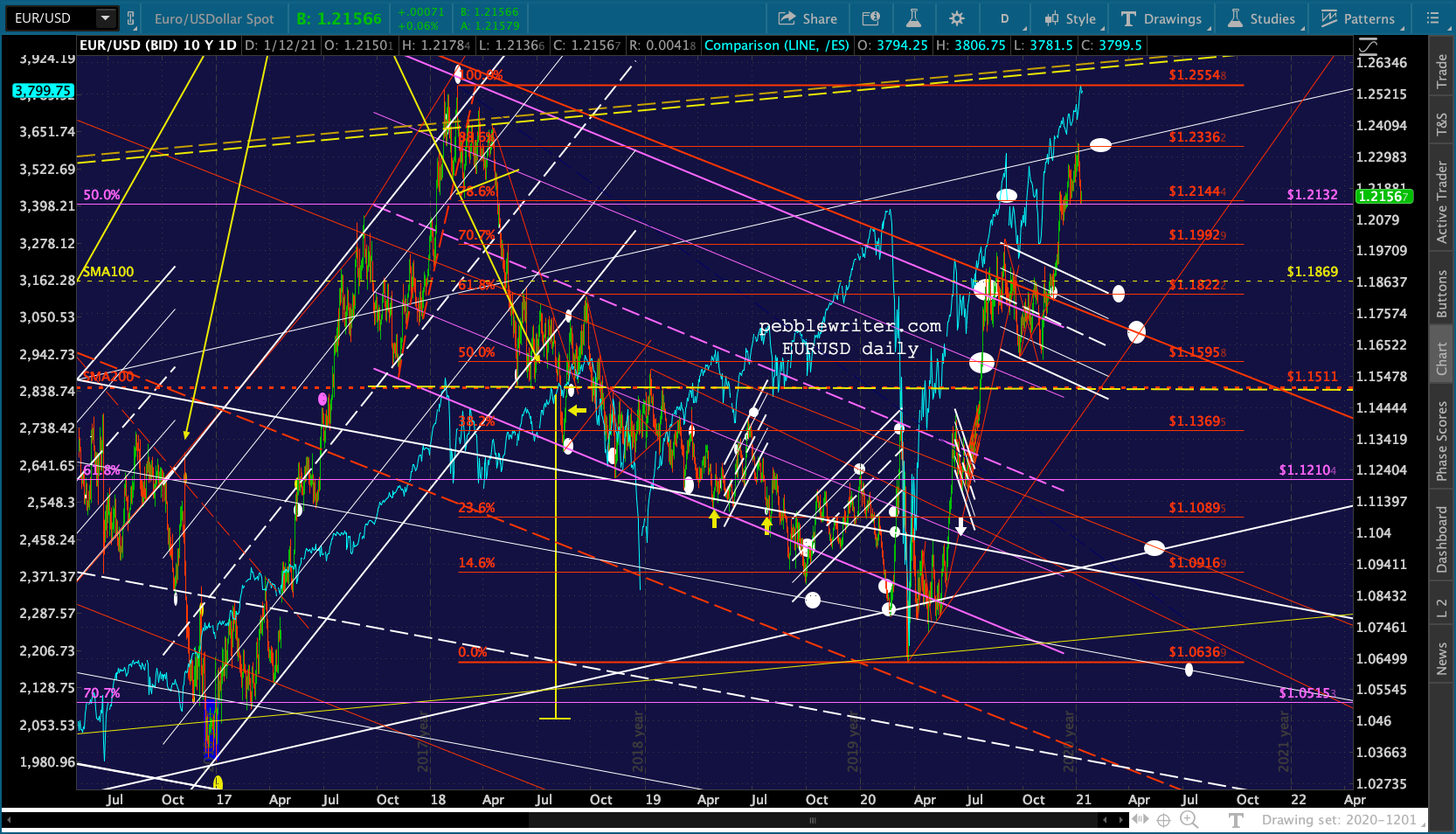

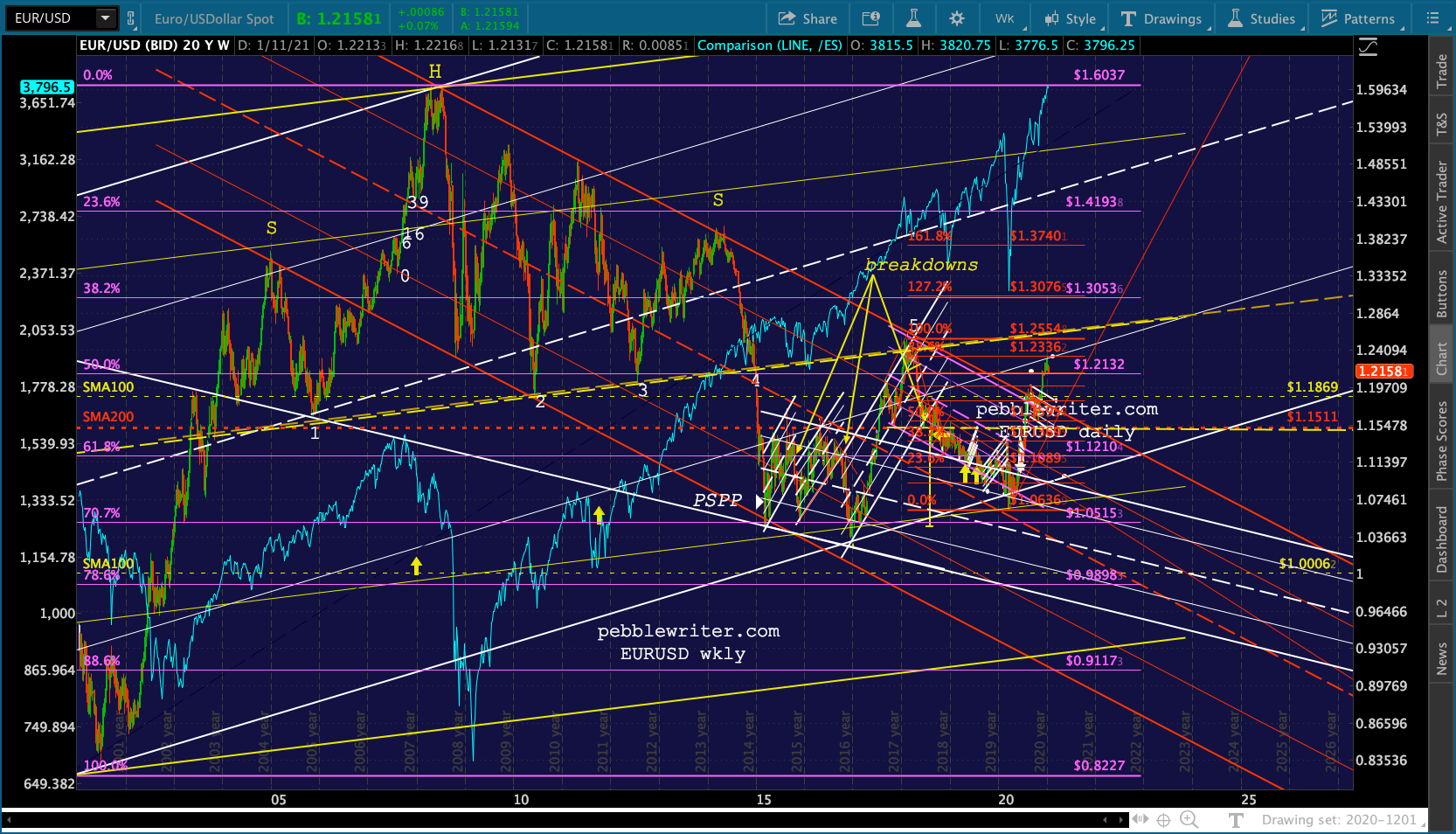

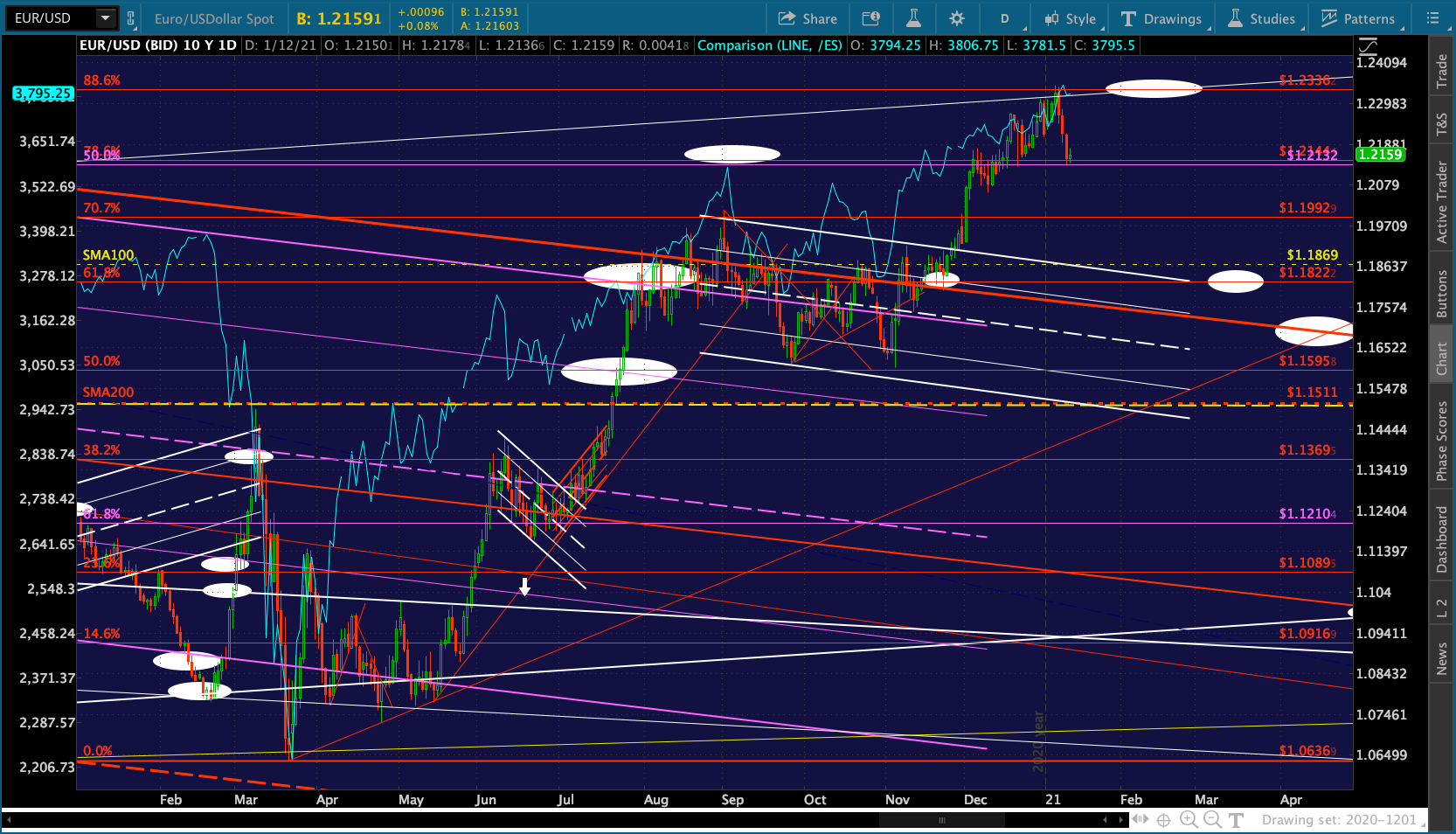

There were, however, fundamental reasons that a drop in DXY was beneficial: (1) it reflected the huge expansion of stimulus and QE; (2) it caused/facilitated the rapid rise in CL prices; (3) it made owning US assets cheaper for foreign buyers. The primary reason for the falling dollar was its relationship with the euro. Note that every time the EURUSD has broken down or reversed lower by a substantial amount, stocks have followed suit.

The primary reason for the falling dollar was its relationship with the euro. Note that every time the EURUSD has broken down or reversed lower by a substantial amount, stocks have followed suit. If you were in charge of propping up stocks for the Fed, you’d certainly notice this and would be hesitant to bring it to a halt. Therefore, you enabled a breakout of the red channel going all the way back to 2005 around Dec 1, 2020.

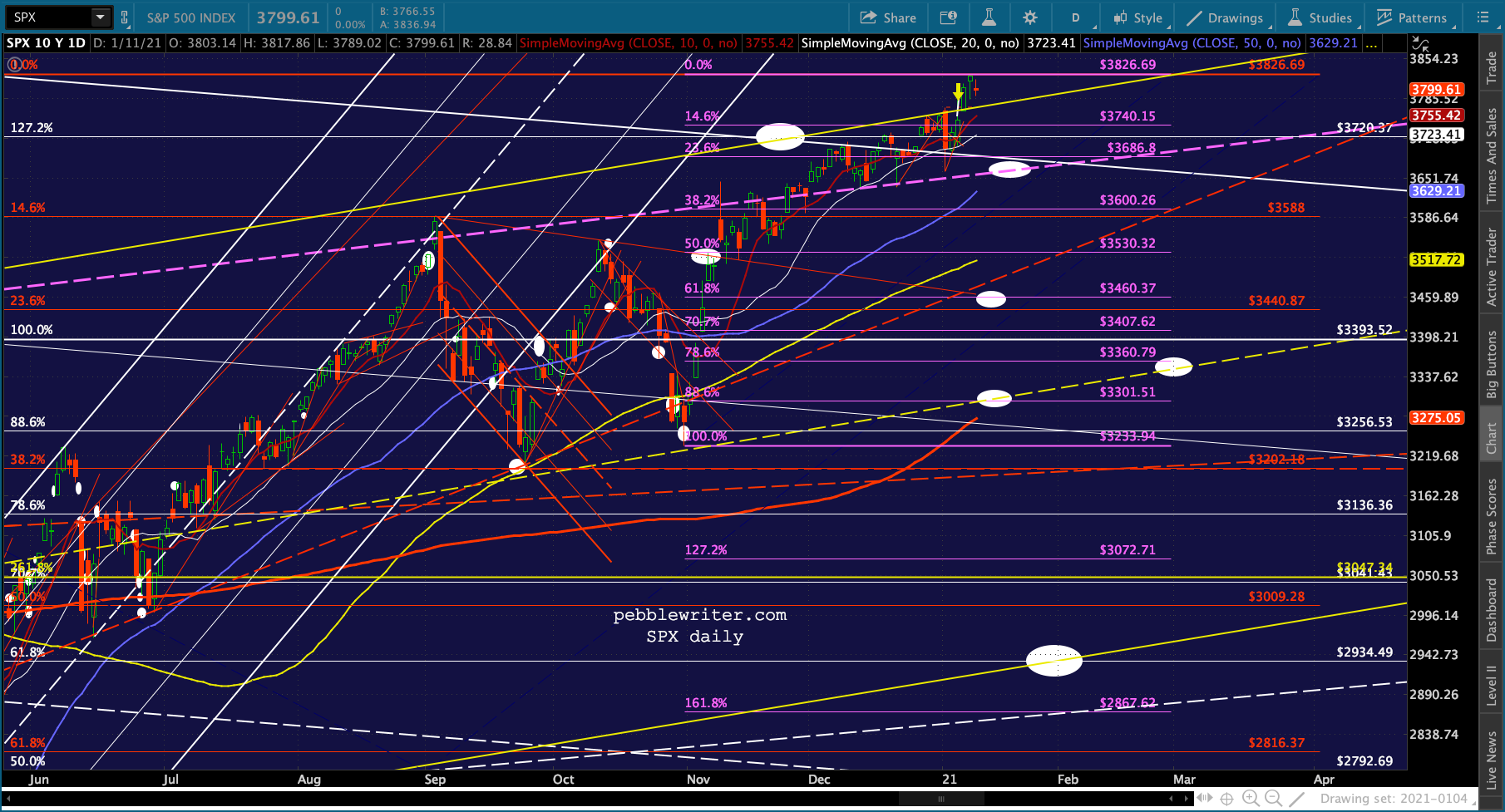

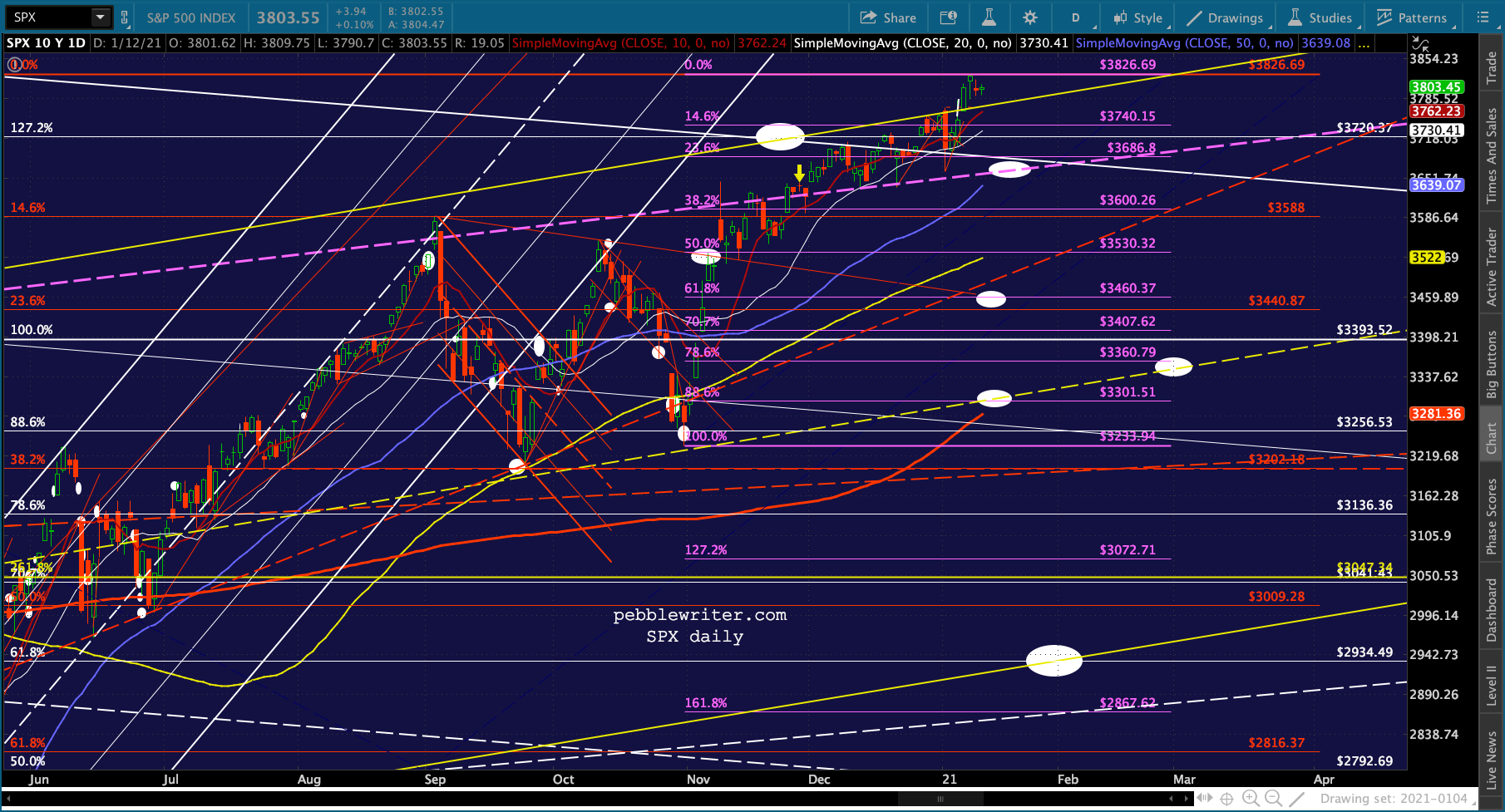

If you were in charge of propping up stocks for the Fed, you’d certainly notice this and would be hesitant to bring it to a halt. Therefore, you enabled a breakout of the red channel going all the way back to 2005 around Dec 1, 2020. This enabled SPX to break out above the purple TL connecting the previous highs (the yellow arrow below)…

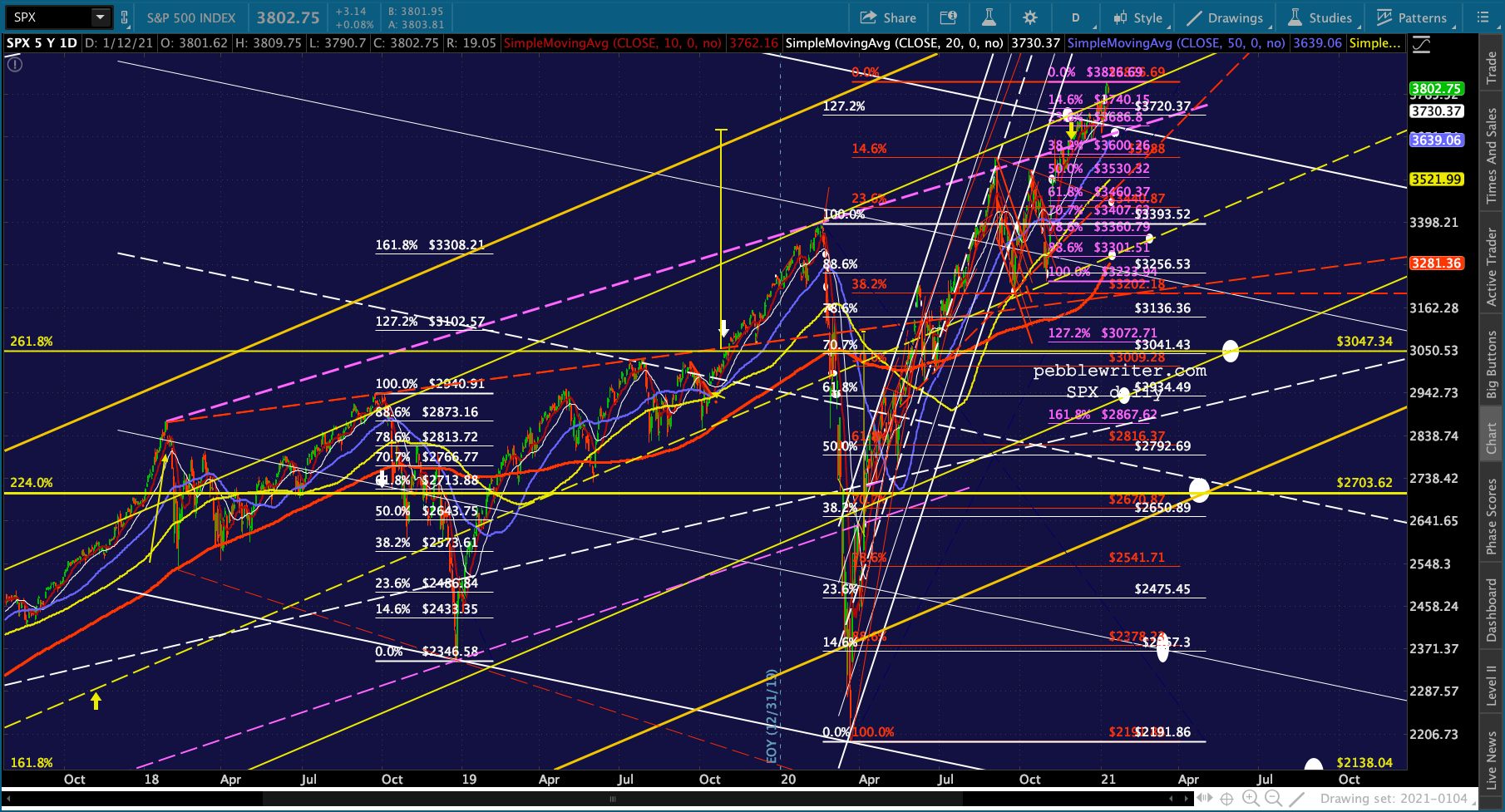

This enabled SPX to break out above the purple TL connecting the previous highs (the yellow arrow below)… …seen more easily on this chart…

…seen more easily on this chart… …and was bolstered by VIX making a lower low (white arrow) at the same time.

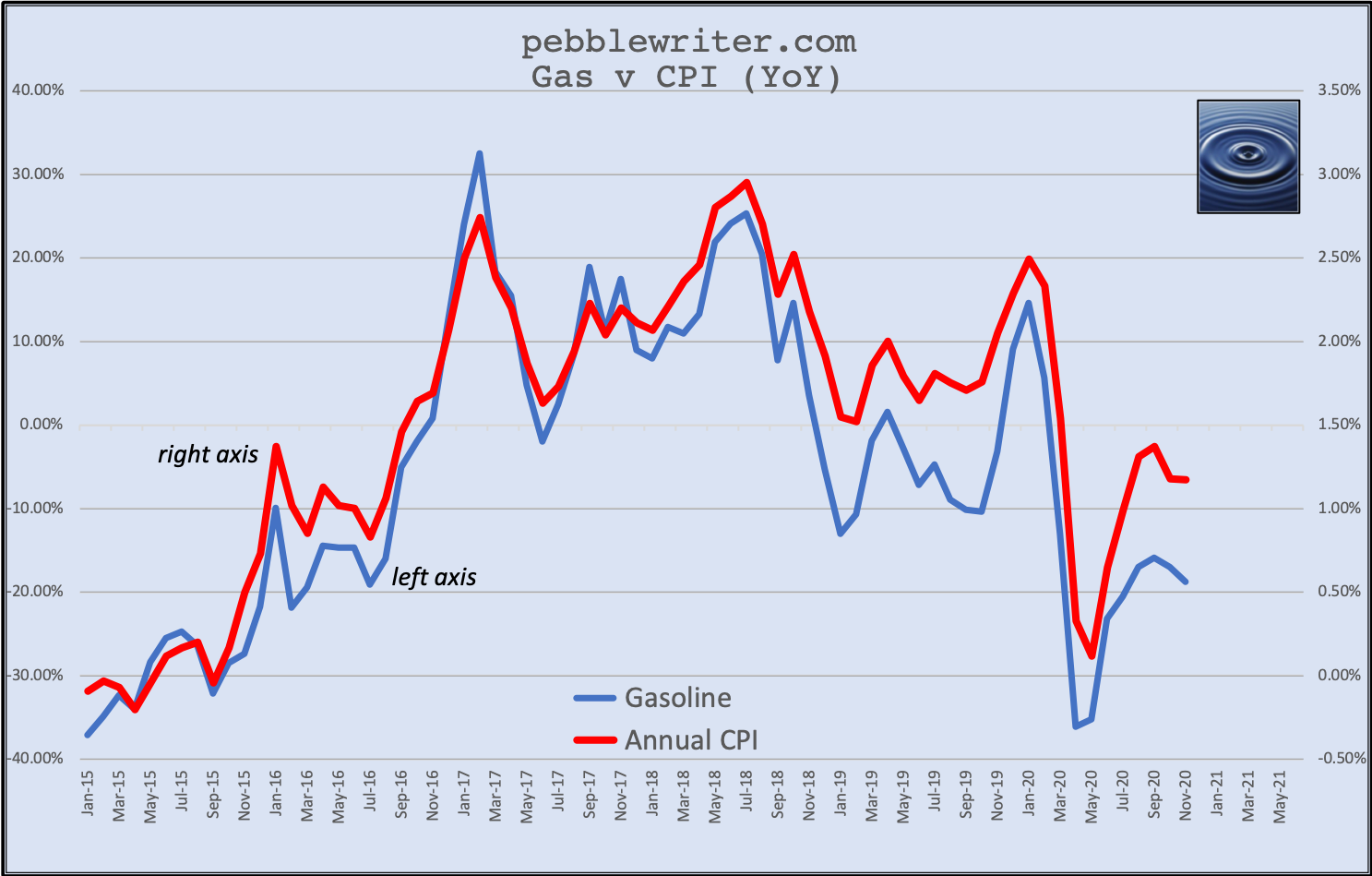

…and was bolstered by VIX making a lower low (white arrow) at the same time. There are repercussions of such maneuvers, though. Since the US is a net importer and imports plenty from Europe, this would eventually cause inflation pressure to build. Given the oil/gas inflation problem coming in April (potentially 2%+ CPI, 2.5% 10Y unless gas prices crater), I believe they saw the writing on the wall and decided it was time to rein it in.

There are repercussions of such maneuvers, though. Since the US is a net importer and imports plenty from Europe, this would eventually cause inflation pressure to build. Given the oil/gas inflation problem coming in April (potentially 2%+ CPI, 2.5% 10Y unless gas prices crater), I believe they saw the writing on the wall and decided it was time to rein it in.

But, how, without also cratering stocks? That’s why VIX is lurking in the basement, USDJPY is bouncing, the 10Y is spiking higher, etc. If stocks don’t correct as EURUSD does, it’ll be quite a feat. The official explanation is that the economy is recovering, the market is forward looking. But, as the pandemic worsens and we learn that the vaccine rollout is going badly, it’s really the algos that are keeping stocks from tanking even as EURUSD drops and DXY rises.

The official explanation is that the economy is recovering, the market is forward looking. But, as the pandemic worsens and we learn that the vaccine rollout is going badly, it’s really the algos that are keeping stocks from tanking even as EURUSD drops and DXY rises.

I heard Atlanta Fed president Bostic interviewed yesterday. The one comment that stuck in my craw was in response to a question about whether, given all the stimulus and $120 billion/month bond buying, he was worried about inflation. He wasn’t worried, as “we have tools to deal with that.”

What tools!? Officially, they can expand or contract the money supply and they can drive interest rates higher or lower. The only other thing they can do to limit inflation is to manipulate the prices of assets that feed into CPI.

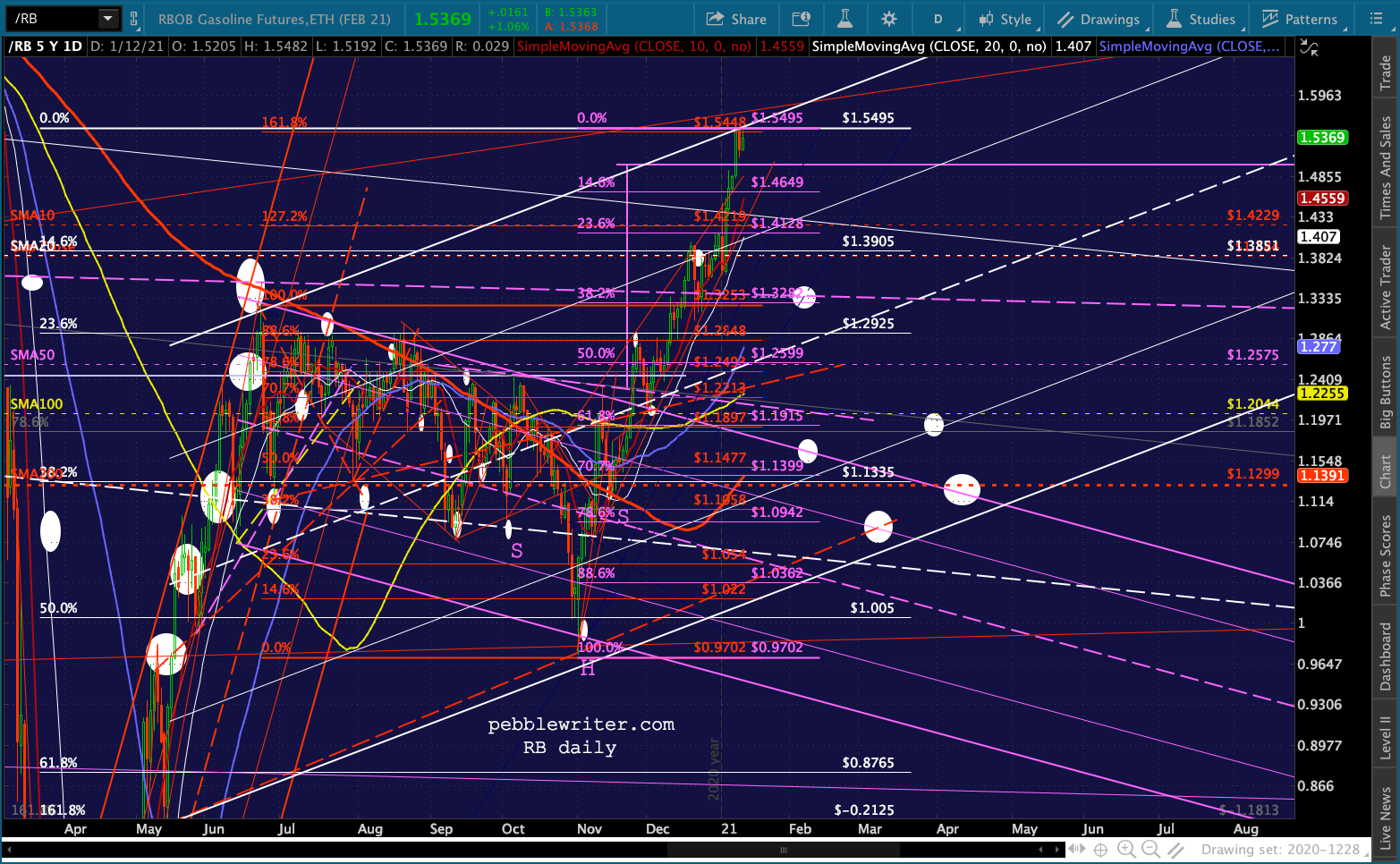

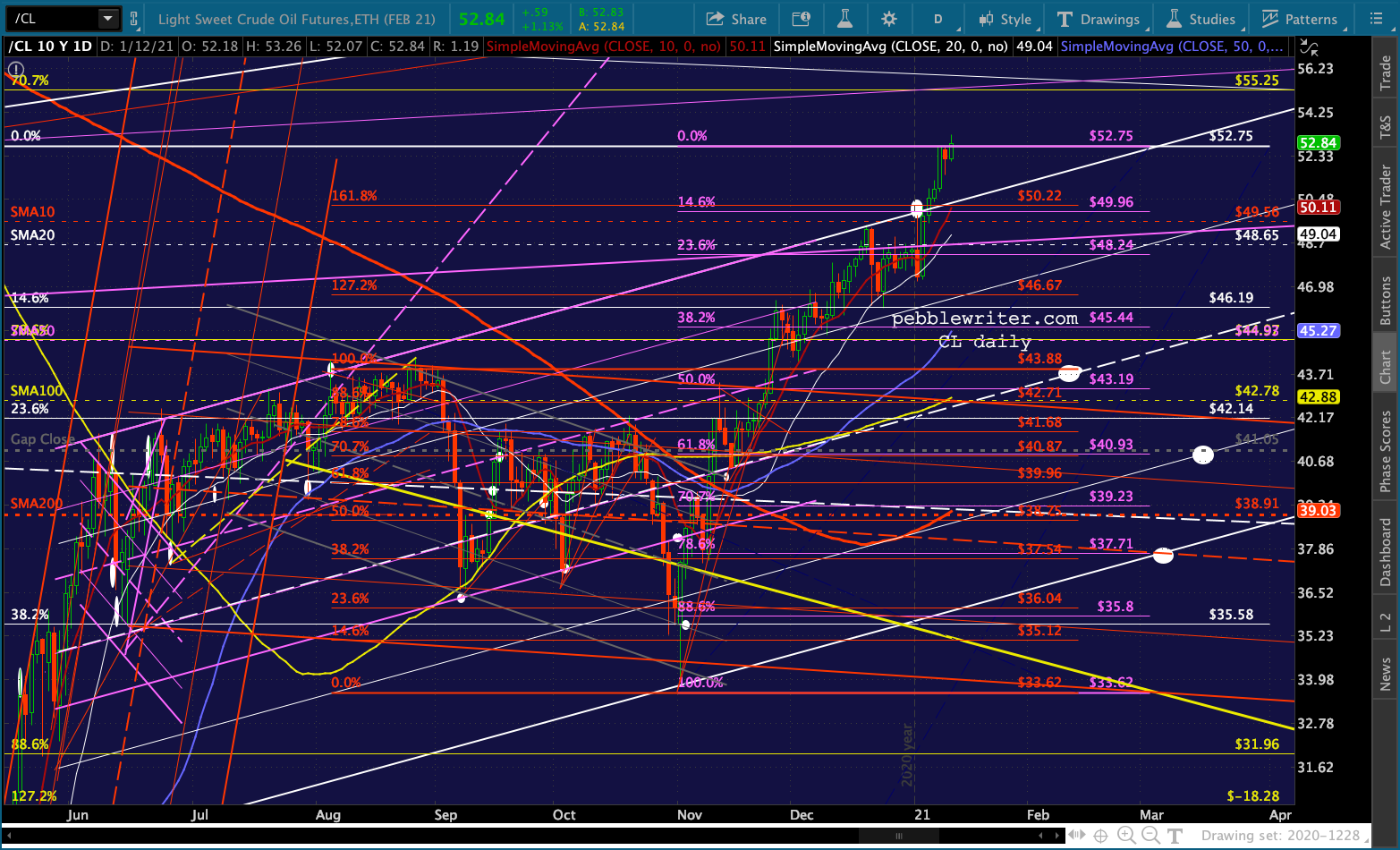

This is why I’m pretty certain that, come April, RB will be considerably lower. It’s the one thing they have consistently manipulated when necessary in order to reign in CPI and, thus, interest rates.

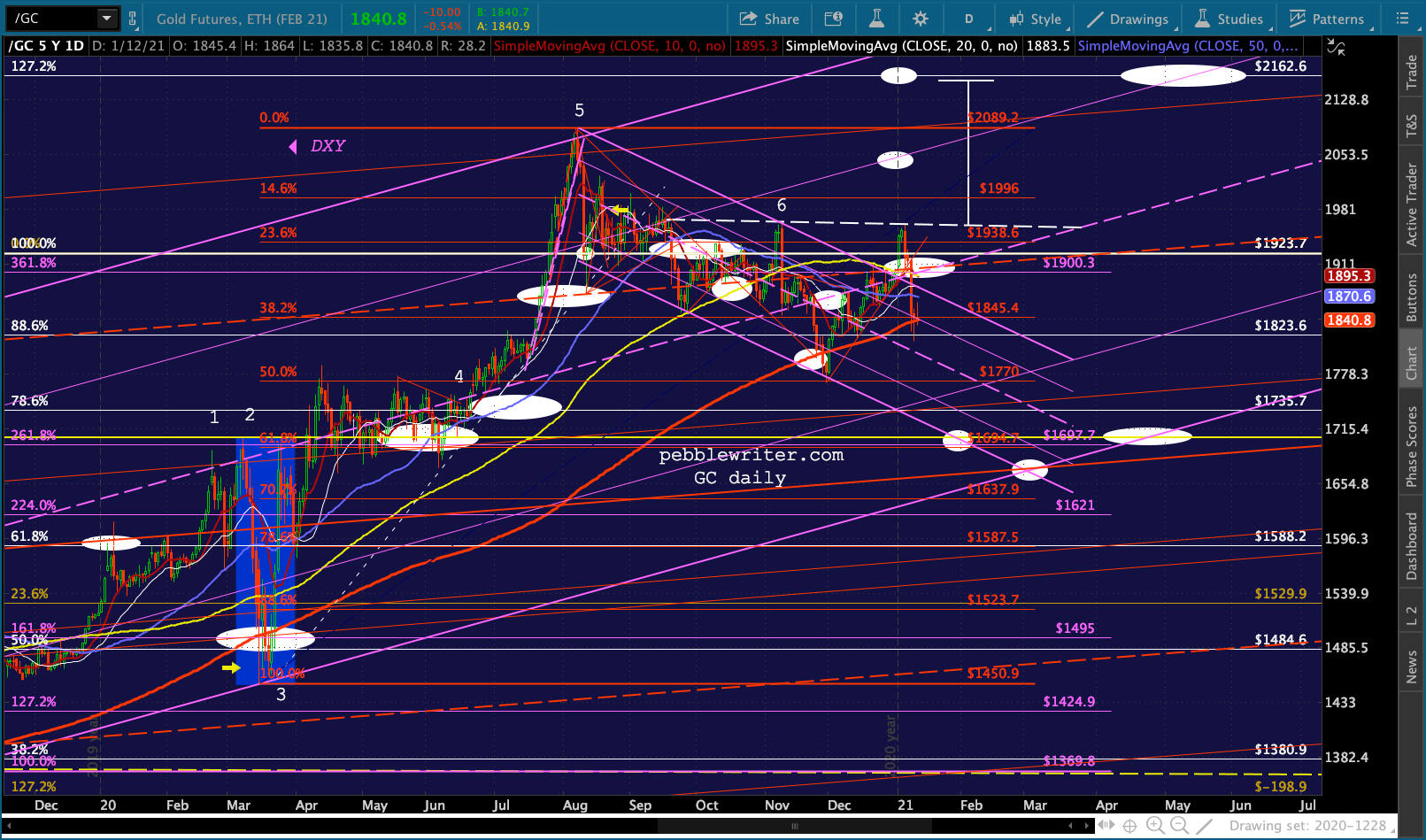

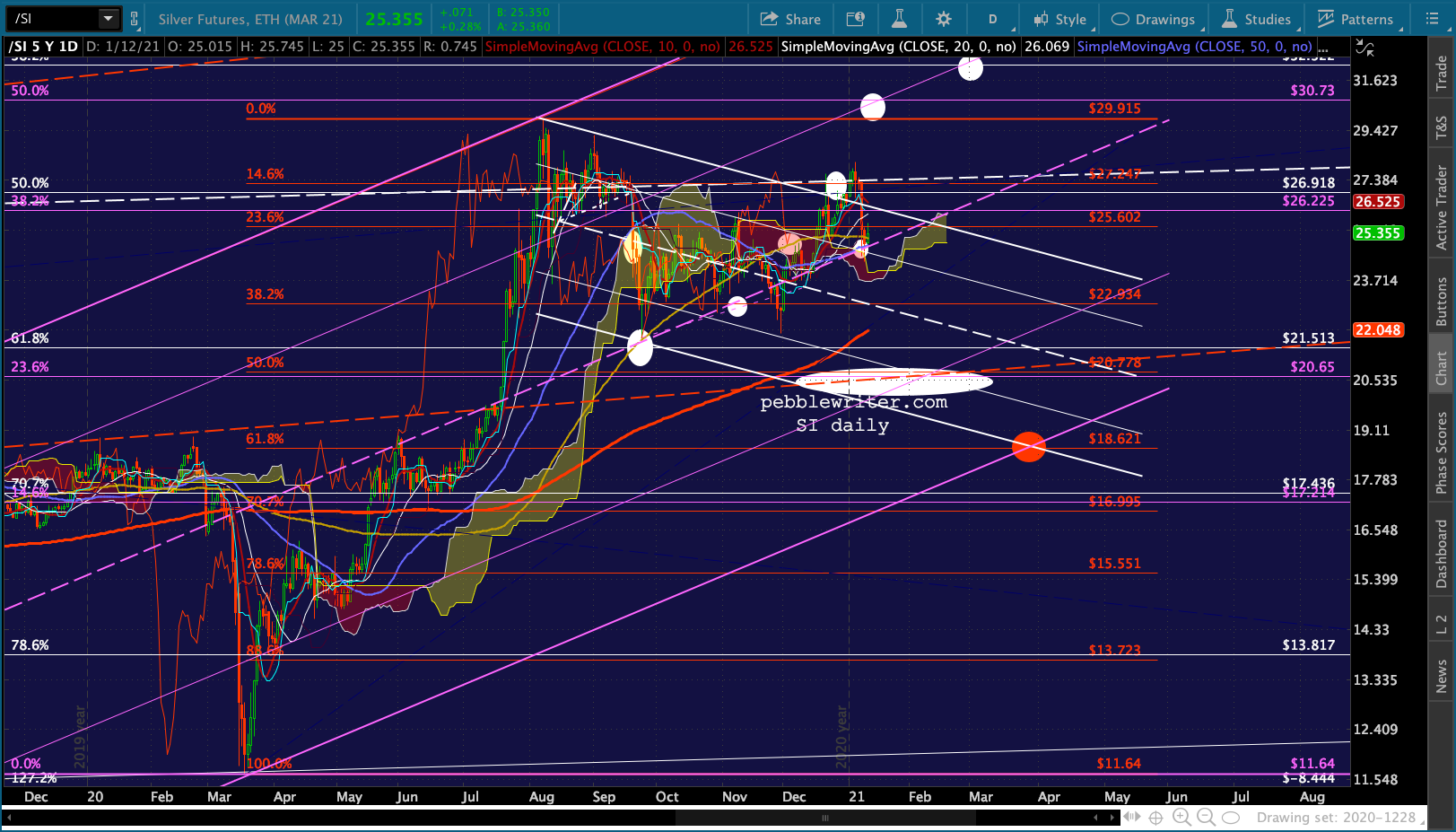

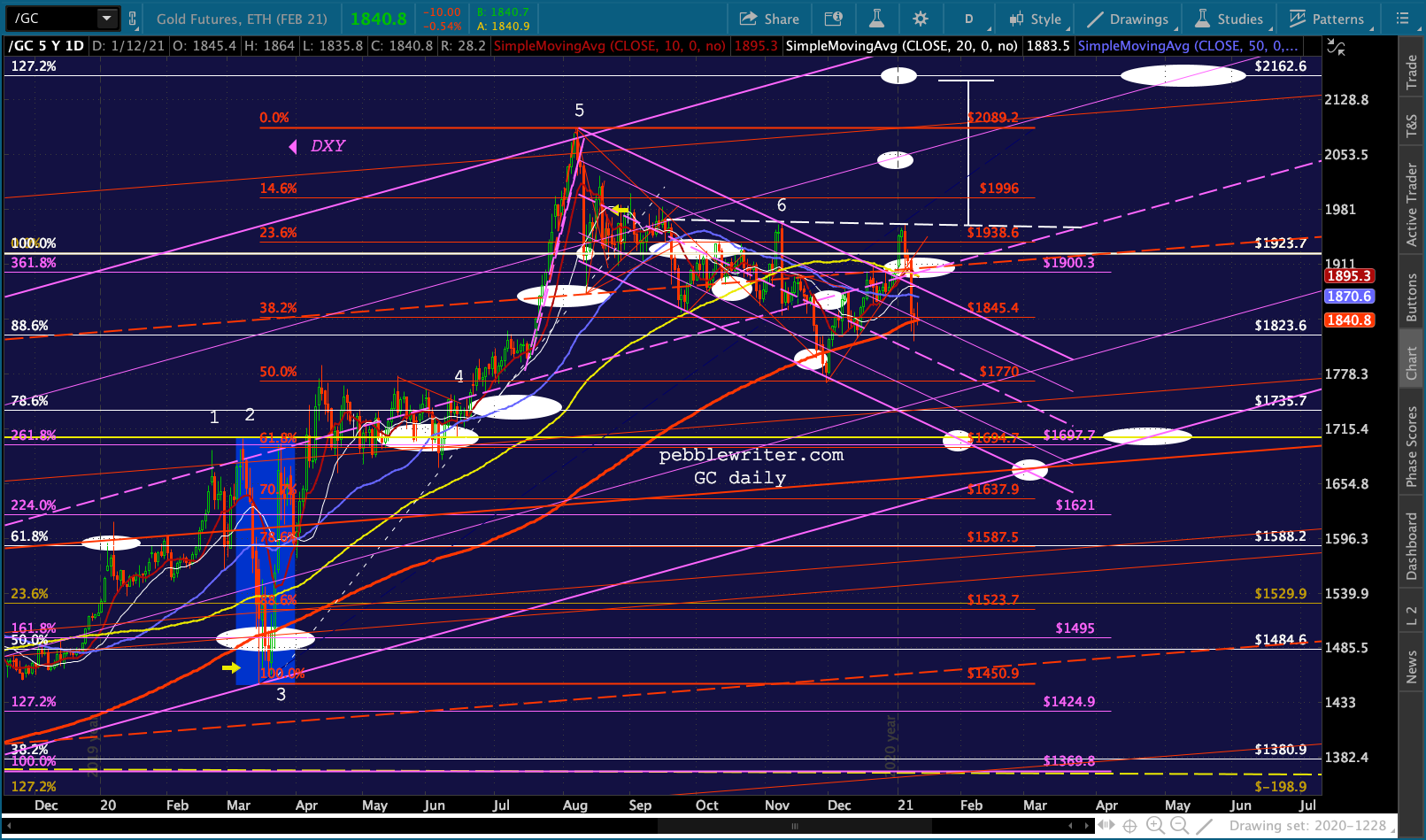

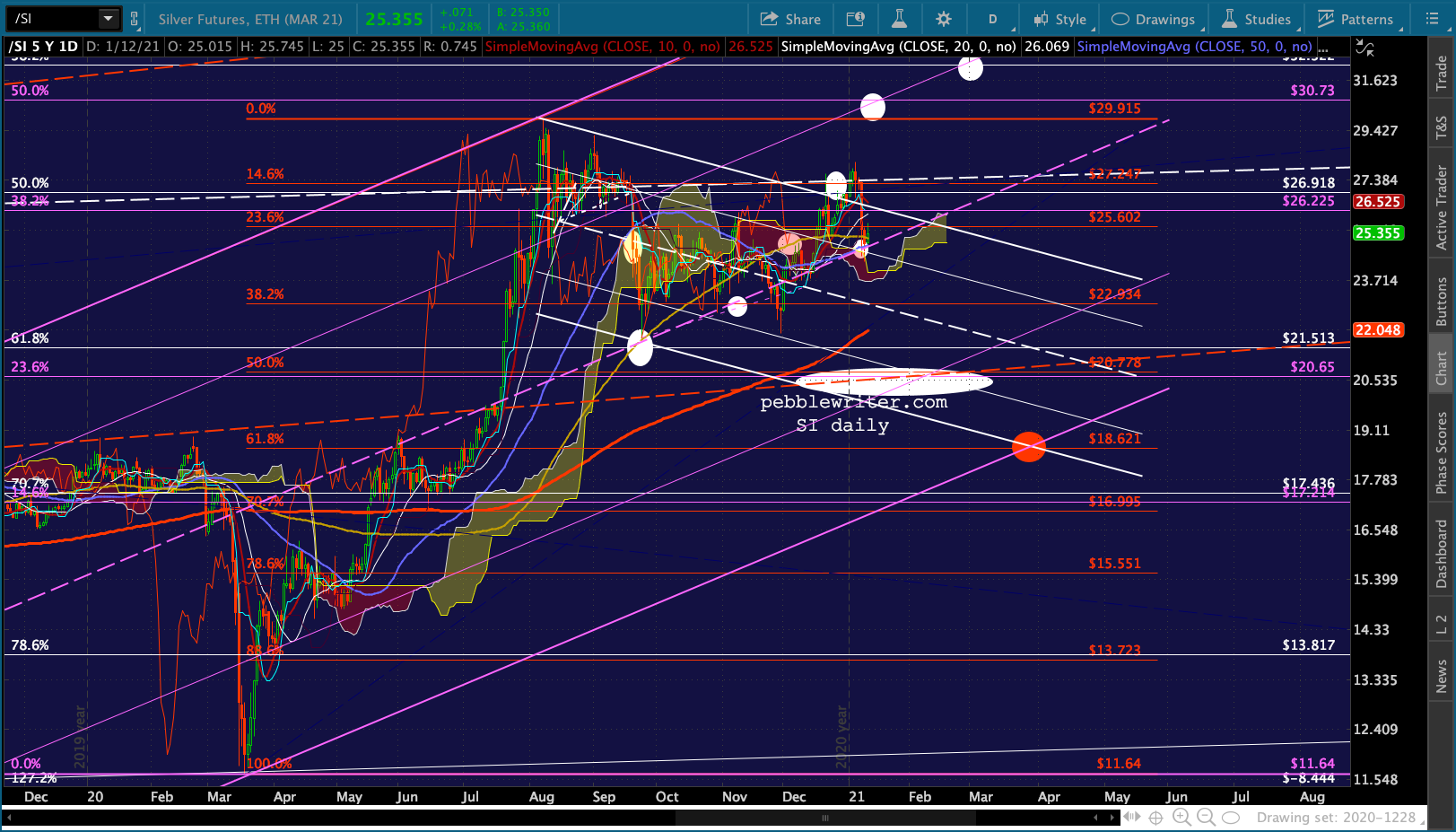

Despite all the talk about the reflation trade and Fed’s supposed desire to get back to 2% CPI, everyone knows the Fed will do whatever it takes to keep inflation under control. Perhaps that’s why GC and SI can’t seem to make any headway.

Despite all the talk about the reflation trade and Fed’s supposed desire to get back to 2% CPI, everyone knows the Fed will do whatever it takes to keep inflation under control. Perhaps that’s why GC and SI can’t seem to make any headway.

Bottom line, they have to accommodate a drop in oil but especially gas prices during the months March – May.

Bottom line, they have to accommodate a drop in oil but especially gas prices during the months March – May.

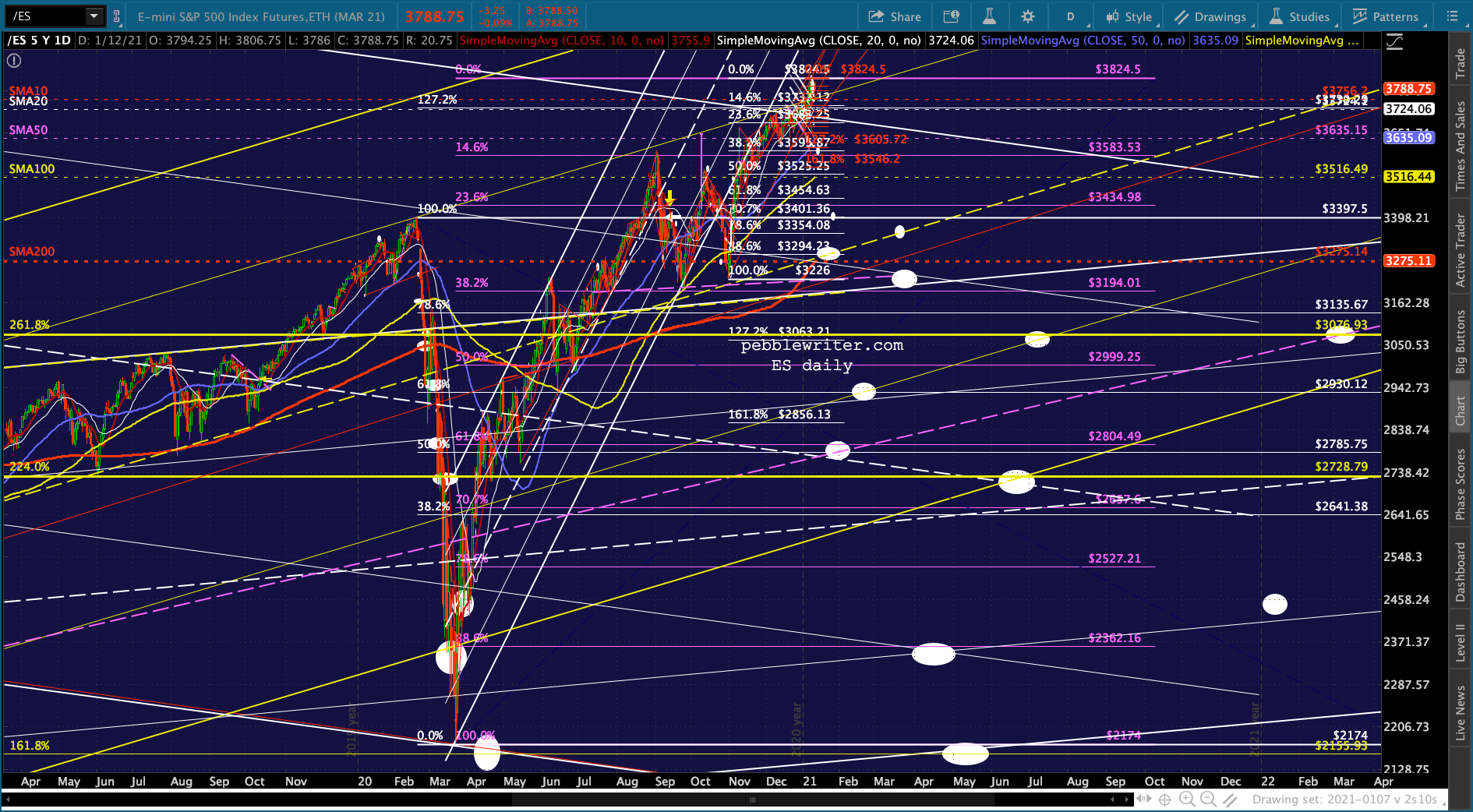

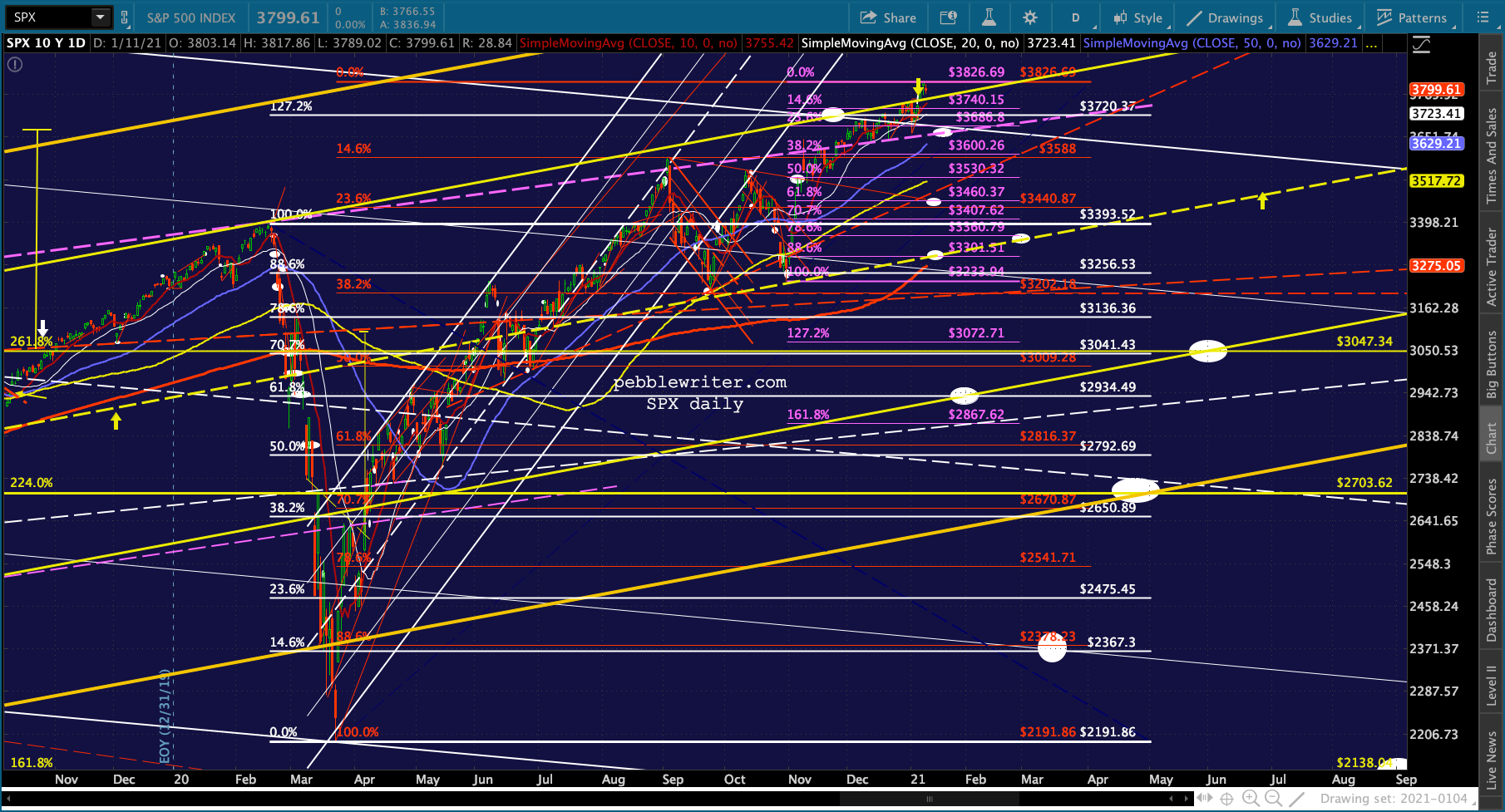

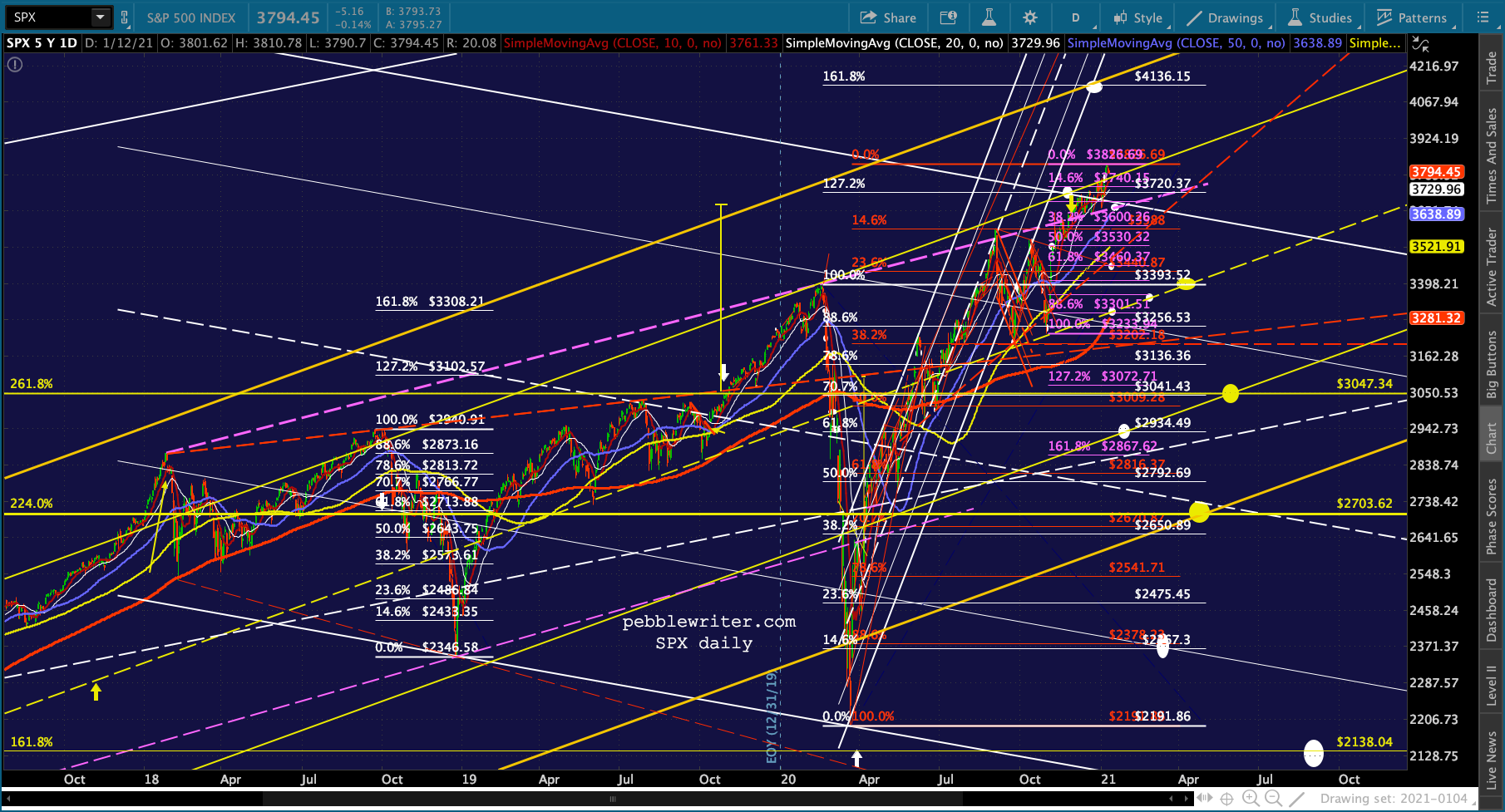

They want to do so without killing stocks – which, in this case, probably means holding an important level of support: ideally the Feb 2020 SPX 3393 highs, with alternatives being the 2.618 at 3047 or the 2.24 at 2703. Their intersections with important channel lines are marked below in yellow. Note that they all fall around the middle of April to the end of May.

They want to do so without killing stocks – which, in this case, probably means holding an important level of support: ideally the Feb 2020 SPX 3393 highs, with alternatives being the 2.618 at 3047 or the 2.24 at 2703. Their intersections with important channel lines are marked below in yellow. Note that they all fall around the middle of April to the end of May.

The 1.618 at 4136.15 would have been a good target, but the optimal timing would have been when it intersected with the yellow channel top on Dec 22. We’re past that now. In case you’re wondering, the inability to hold the yellow channel opens the door to SPX 2138 — which was narrowly missed on Mar 23.

In case you’re wondering, the inability to hold the yellow channel opens the door to SPX 2138 — which was narrowly missed on Mar 23.

I have several calls and a doctor’s appointment this afternoon, so will post more after the close if anything surprising happens.

GLTA.