The headlines have been coming fast and furious over the last 24 hours. First, Trump’s tweet yesterday morning regarding trade negotiations with China touched off a rumor, declared false this morning, that a trade deal was imminent. But, SPX soared yesterday anyway.

Then AAPL’s earnings came out. The numbers were underwhelming; and, the company’s announcement that they’d no longer report unit data was very poorly received.

The chart we put up yesterday prior to the close [see: All Eyes on AAPL] showed substantial downside potential… …which after-hours trading is confirming.

…which after-hours trading is confirming. Then there was this morning’s payrolls data: a 250K increase with a 3.1% increase in average hourly earnings. While no doubt It’s exactly the sort of data the Fed needs to justify further rate increases in the face of the collapse in oil and gas prices — the last piece of the puzzle.

Then there was this morning’s payrolls data: a 250K increase with a 3.1% increase in average hourly earnings. While no doubt It’s exactly the sort of data the Fed needs to justify further rate increases in the face of the collapse in oil and gas prices — the last piece of the puzzle.

Gasoline has now fallen over 20% since our Oct 3 short call and tagged another downside target yesterday. Oil is off over 16% and just broke beneath horizontal and channel support. To be sure, it will keep October’s CPI low and will delight voters driving to the polls on Tuesday. But, like the employment data, there are repercussions.

Oil is off over 16% and just broke beneath horizontal and channel support. To be sure, it will keep October’s CPI low and will delight voters driving to the polls on Tuesday. But, like the employment data, there are repercussions. By the way, I have updated our oil and gas forecasting results, available at the links below.

By the way, I have updated our oil and gas forecasting results, available at the links below.

I hope to post currencies, VIX and gold later today or this weekend.

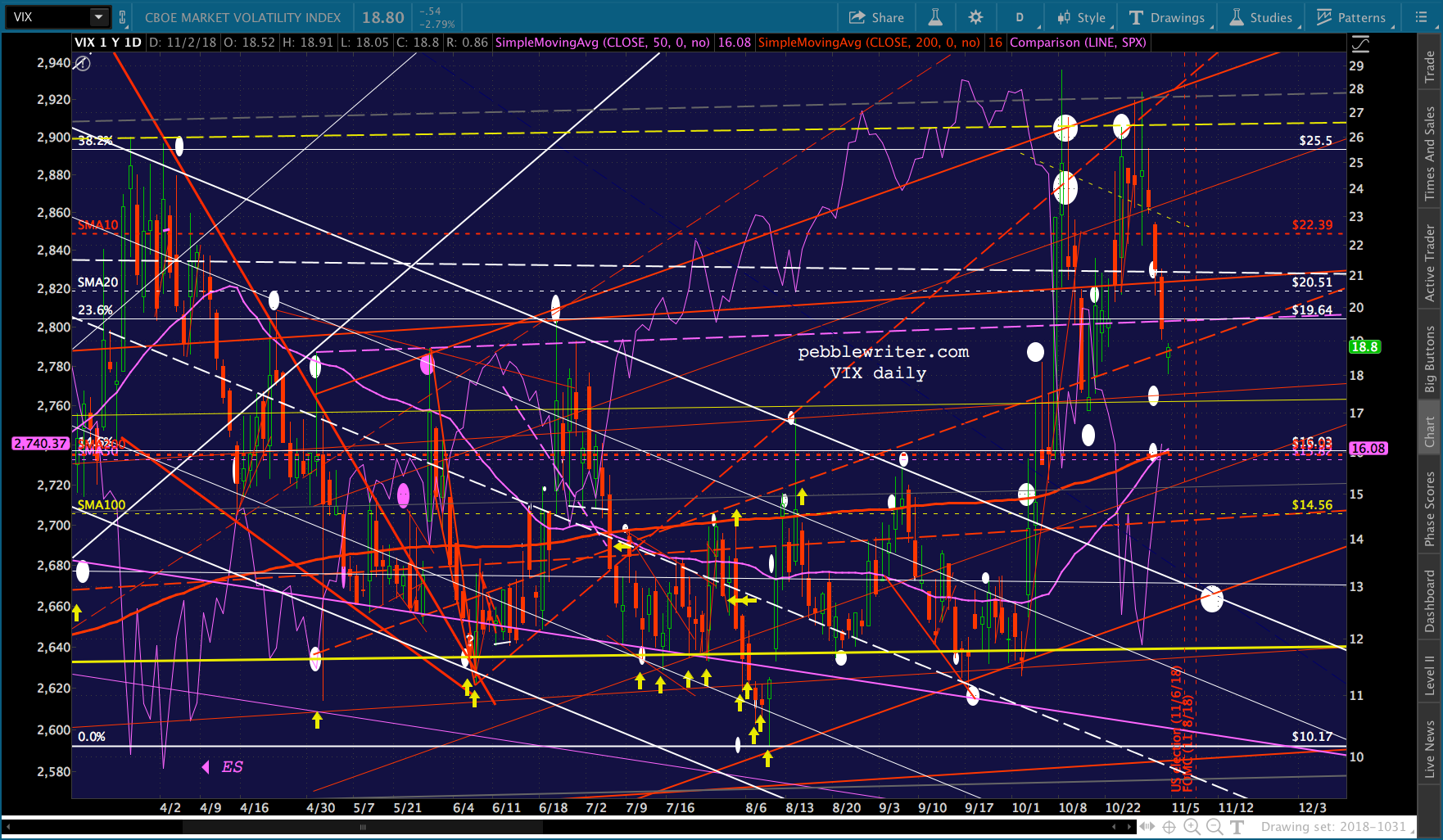

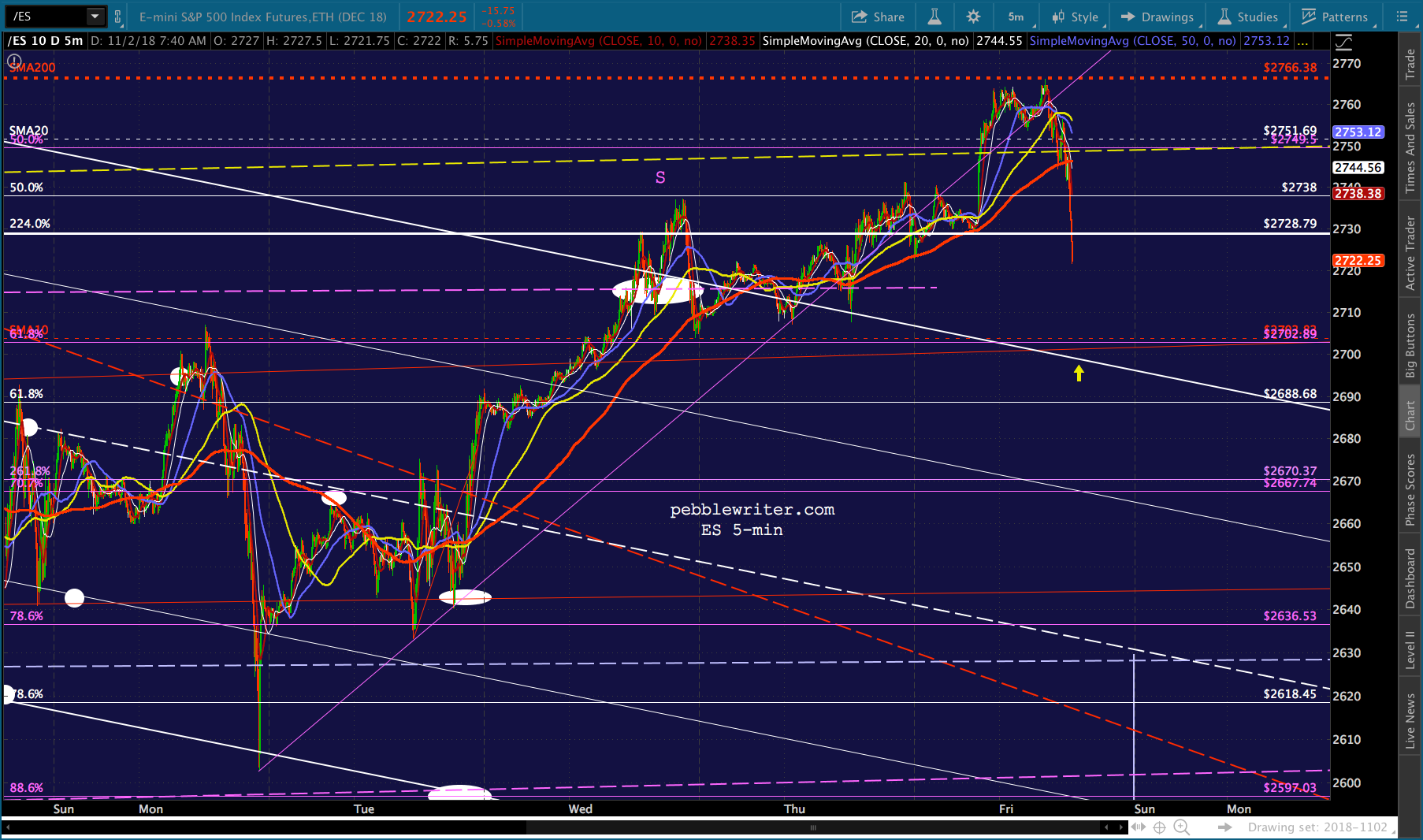

Futures melted up to backtest the SMA200 early this morning and have since fallen 16 points to the algo-darling SMA5 200. It remains to be seen how the mixed messages being sent up from Washington and Cupertino will play out. But, for now, I’m leaving our targets in place. For the moment, at least, VIX’s 50/200 cross is on again.

For the moment, at least, VIX’s 50/200 cross is on again. continued for members…

continued for members…

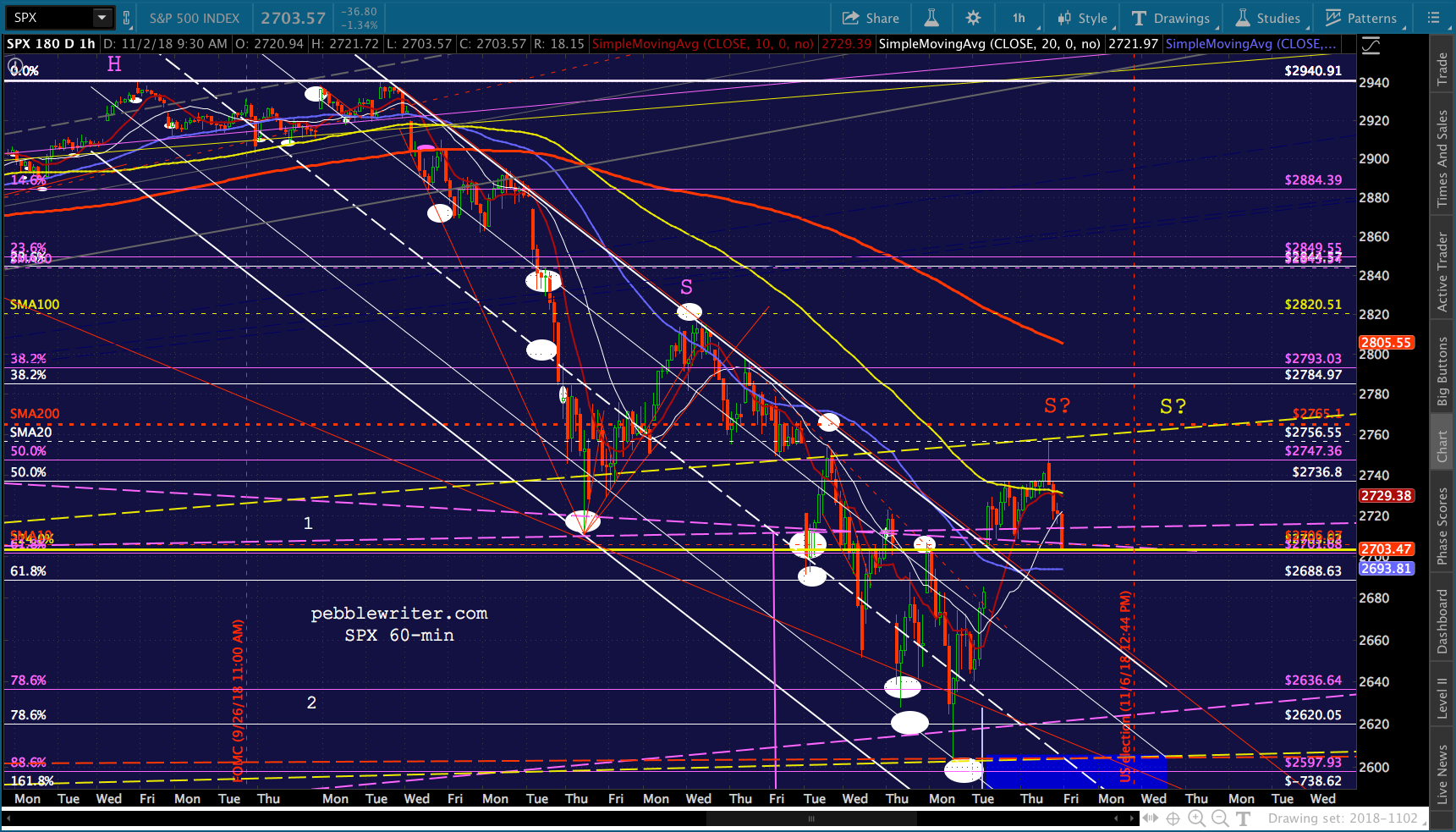

SPX’s various H&S Patterns. Note that it is backtesting the yellow channel midline and potentially its SMA200. And, VIX’s precarious hold on support:

And, VIX’s precarious hold on support: The currency picture: USDJPY is obviously in PPT mode…

The currency picture: USDJPY is obviously in PPT mode… …while EURUSD continues its bounce off the white channel top.

…while EURUSD continues its bounce off the white channel top. The overall effect on DXY is still negative, though the stronger than expected payrolls data might offset this somewhat.

The overall effect on DXY is still negative, though the stronger than expected payrolls data might offset this somewhat.  It will interesting to see if TNX’s mini-breakout will hold. ZN’s rally depends on it.

It will interesting to see if TNX’s mini-breakout will hold. ZN’s rally depends on it.

One last chart I should put up. AAPL isn’t the only big name with downside potential today. Note that AMZN is backtesting its SMA200.

One last chart I should put up. AAPL isn’t the only big name with downside potential today. Note that AMZN is backtesting its SMA200. More later.

More later.

UPDATE: 10:45 AM

ES has dropped through its 2.24 extension and is suggesting at least a backtest of the white channel from which it broke out on Wednesday — about 25 or so points south. It’s an important level of support, as it would align with SPX’s backtest of its own 2.24 at 2703.

It’s an important level of support, as it would align with SPX’s backtest of its own 2.24 at 2703. So far, USDJPY is hanging in there…

So far, USDJPY is hanging in there… …while VIX has gotten a nice bounce off the red midline. I’ve drawn in a more sharply rising channel in case this morning’s low holds.

…while VIX has gotten a nice bounce off the red midline. I’ve drawn in a more sharply rising channel in case this morning’s low holds. AAPL is hanging on to its SMA100…

AAPL is hanging on to its SMA100… …while COMP seems more open to a downdraft.

…while COMP seems more open to a downdraft. RB and CL have gone nowhere since the open.

RB and CL have gone nowhere since the open.

Am I confident of a big drop? Absolutely not. The ramps experienced the last several days are ample proof that TPTB can usually prop up stocks. It remains to be seen how the chess game between the Fed and the White House plays out.

I’ll be on conference calls for the next couple of hours. More later.

UPDATE: 12:55 PM

Quick update on SPX, which just reached its 2.24. Needless to say, important support – as is ES’s white channel backtest. The selloff will either pause here and retreat or pause and plunge lower. I feel that that the oil and gas selloff should end by next Tuesday, given that it’s election day.

AAPL has more downside, but could easily spread it out if they like. VIX isn’t clearly going to bounce here, but my gut tells me it will and that SPX will continue lower. For those intending to hold short, especially over the weekend, watch your stops.

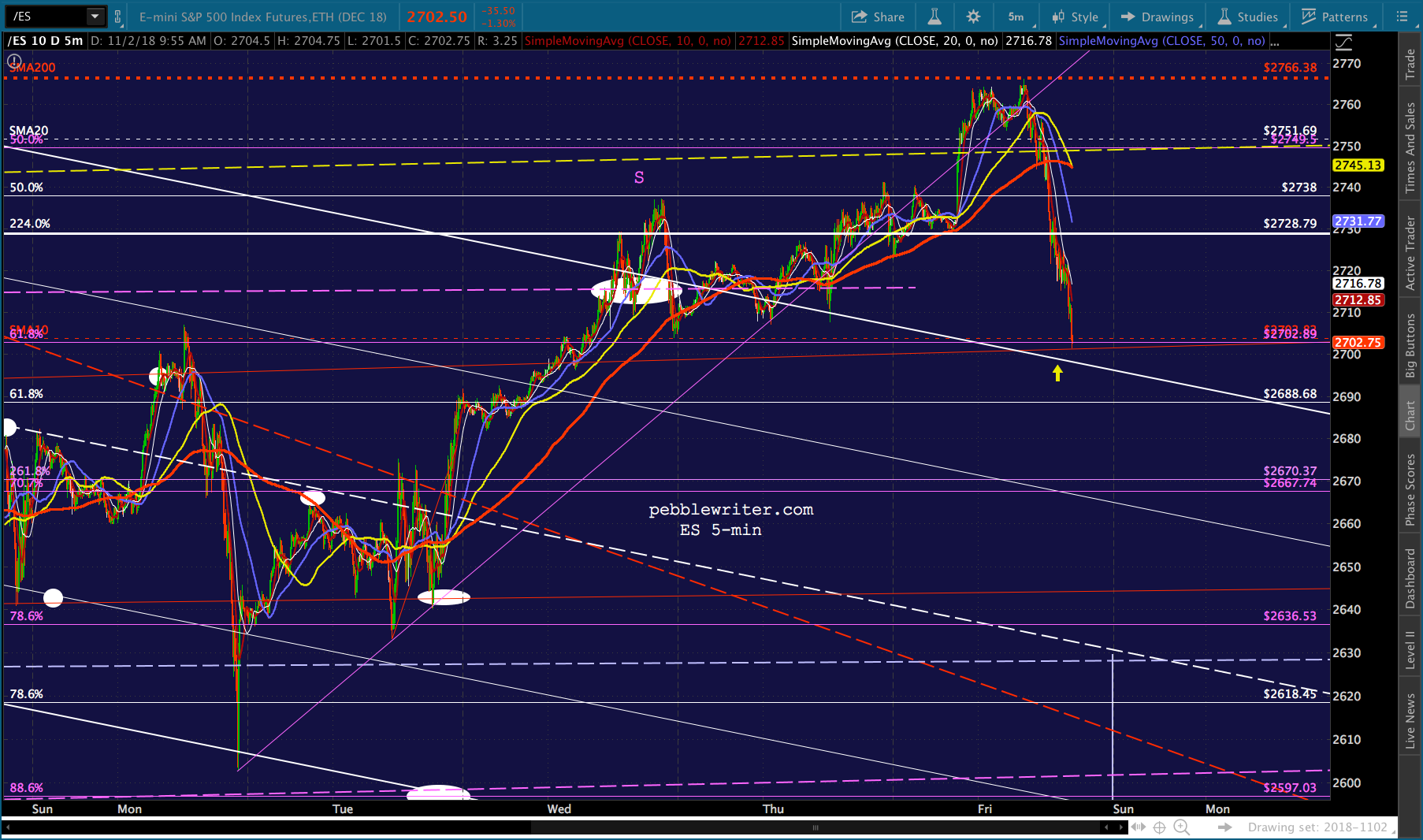

ES’ backtest is closer to 2700 – still a few points away.

ES’ backtest is closer to 2700 – still a few points away. I’m going to sign off for a while and get busy with the rest of the performance data. More later.

I’m going to sign off for a while and get busy with the rest of the performance data. More later.

UPDATE: 3:50 PM

ES and SPX keep inching higher, but nothing resembling a breakout just yet. Clearly, the “market” has become a key battleground for election day referendums. As discussed earlier, only hold short if you can hedge or deal with the gap risk.

GLTA.

GLTA.

Comments

3 responses to “Mixed Messages”

Interesting close

US 10YR closed at high 3.22%

And even better, the intraday high was officially 3.222%

sounds like a moment of truth early in November

What a day so far !

You can say that again!