CPI rose 0.2% MoM in September, half the August rate. It rose 1.4% YoY, slightly higher than September’s 1.3%. Without the outsized gains in used cars and the minor gains in energy (conflicting with the official EIA data), MoM CPI would likely have been negative.

This is hardly supportive of the reflation narrative driving equity prices lately. This should be the last straw for the 10Y’s bounce, with the resulting breakdown a significant headwind for stocks.

This is hardly supportive of the reflation narrative driving equity prices lately. This should be the last straw for the 10Y’s bounce, with the resulting breakdown a significant headwind for stocks.

continued for members…

continued for members…

Note that ZN is getting a nice boost after holding horizontal support. And, the 2s10s is continuing its reversal off of overhead resistance. A breakdown through the latest TL should accelerate equities losses.

And, the 2s10s is continuing its reversal off of overhead resistance. A breakdown through the latest TL should accelerate equities losses. Note that the reversal was really just an extended backtest of the broken yellow TL. A drop to .35 or so won’t be helpful for equity values.

Note that the reversal was really just an extended backtest of the broken yellow TL. A drop to .35 or so won’t be helpful for equity values. Though DXY is holding yesterday’s lows, it shouldn’t last.

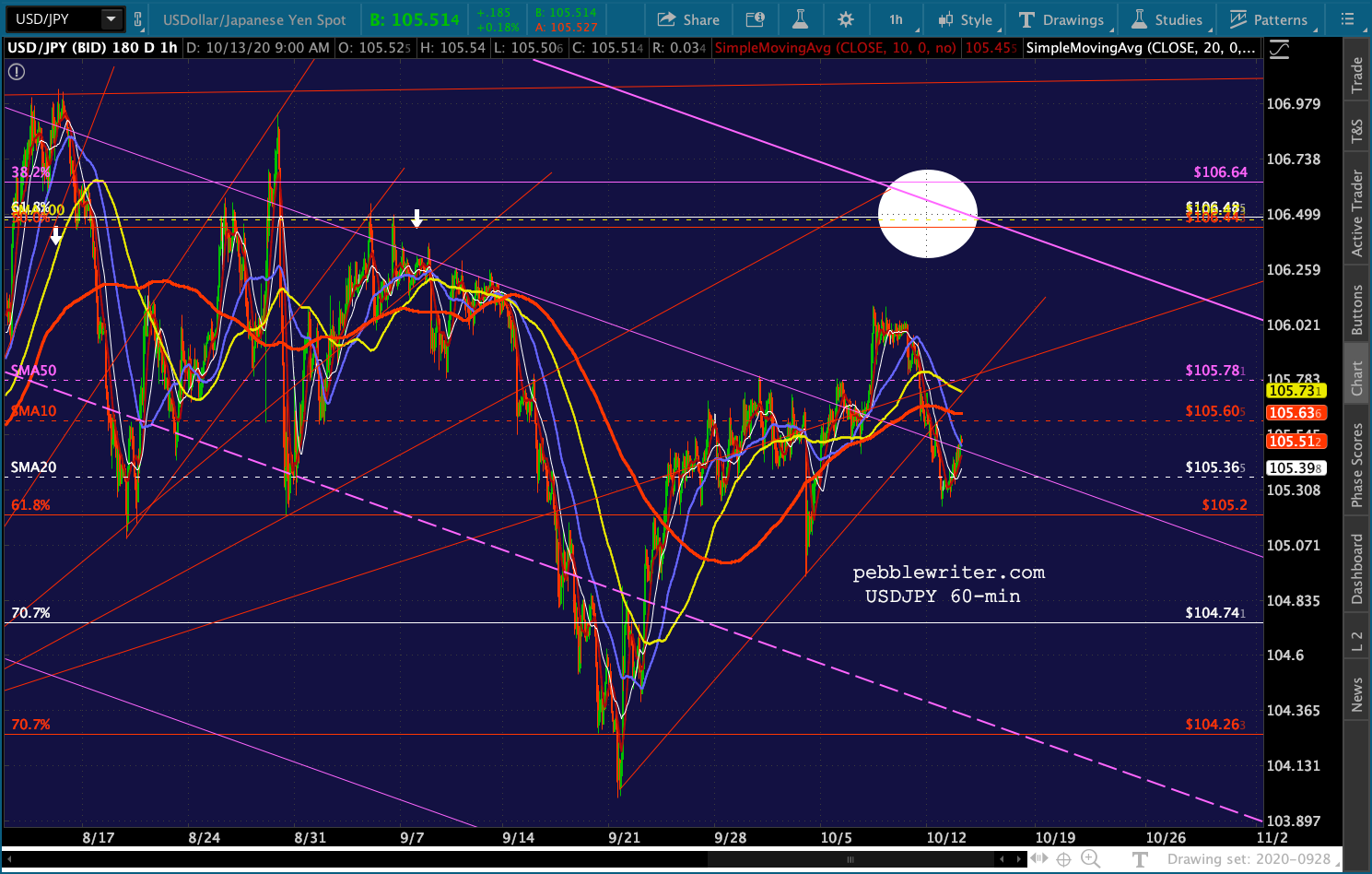

Though DXY is holding yesterday’s lows, it shouldn’t last.  It’s currently due to USDJPY’s equity-supporting bounce…

It’s currently due to USDJPY’s equity-supporting bounce… …and EURUSD’s failure to break out.

…and EURUSD’s failure to break out. It couldn’t have come at a worse time for silver, which was already struggling in an attempt to break out.

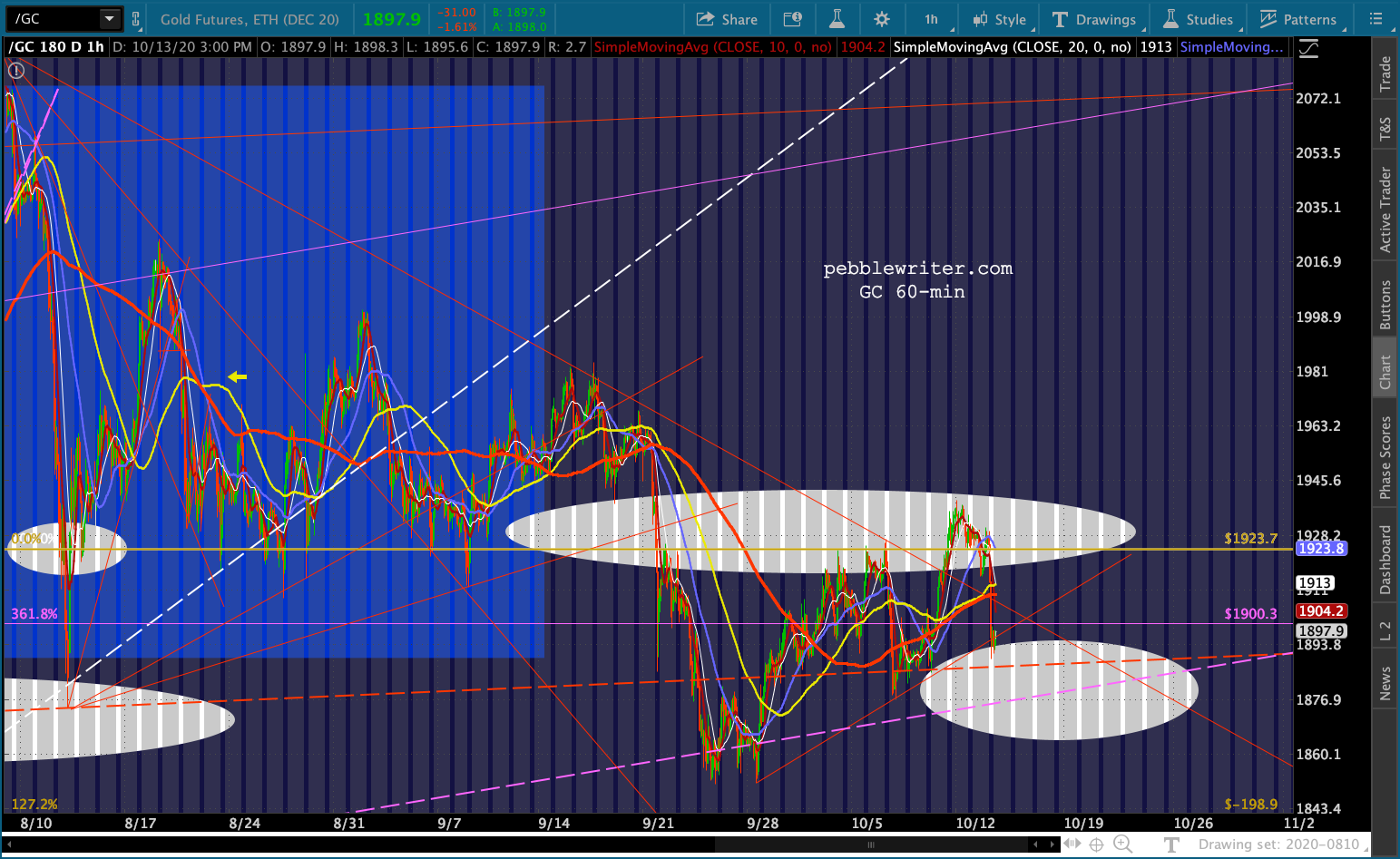

It couldn’t have come at a worse time for silver, which was already struggling in an attempt to break out. While gold has an opportunity to backtest its breakout TL and its SMA10 and SMA20.

While gold has an opportunity to backtest its breakout TL and its SMA10 and SMA20.

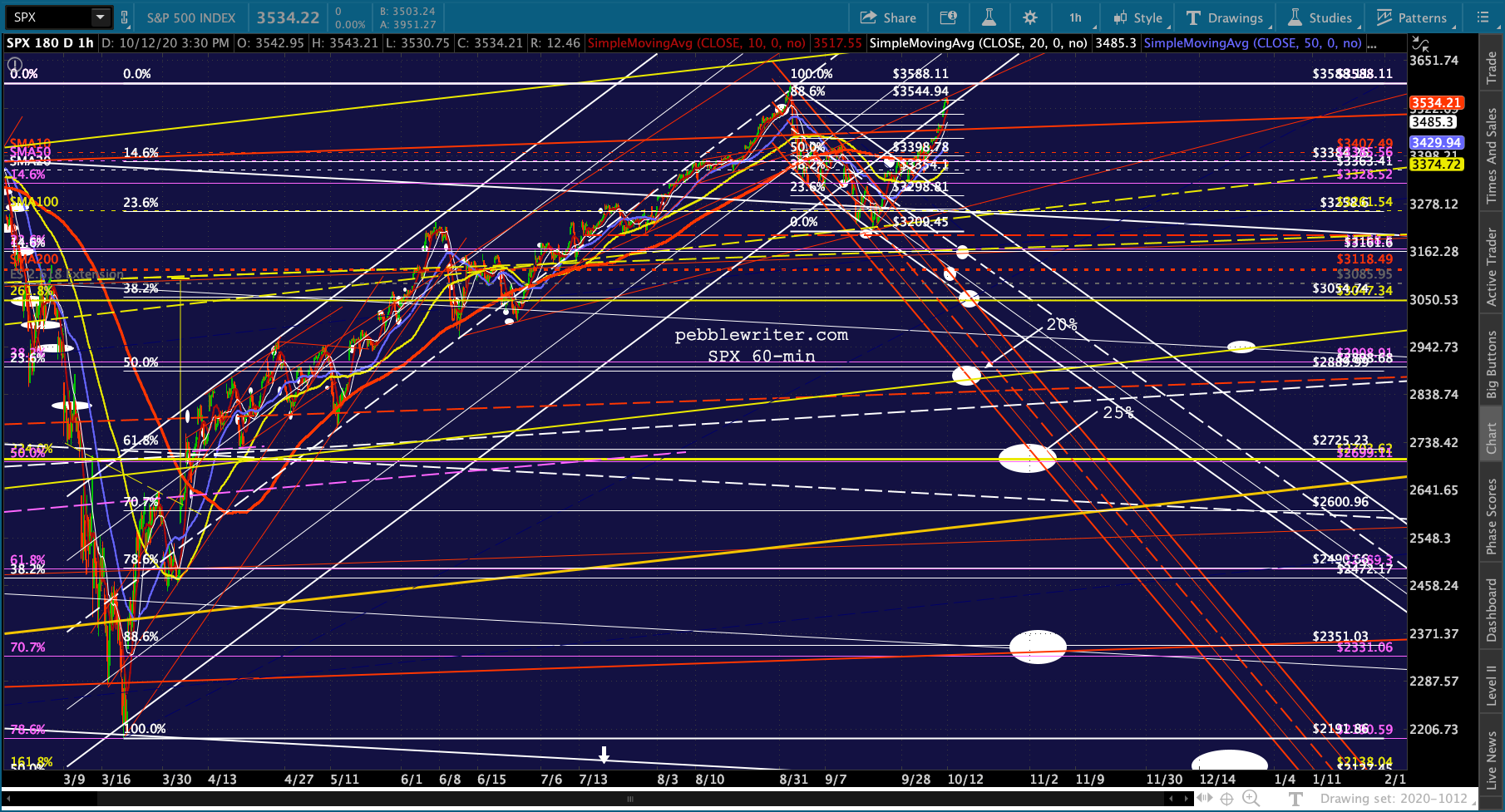

The equity markets aren’t all that pleased, with ES continuing its decline after reaching its .886 as we discussed yesterday.

The equity markets aren’t all that pleased, with ES continuing its decline after reaching its .886 as we discussed yesterday. SPX reached its as well…

SPX reached its as well… ..and backtested its broken white channel.

..and backtested its broken white channel.  This was the first morning since Thursday in which VIX didn’t test or break below support at 24.84. The SMA10 currently stands slightly lower than the SMA10 – a bearish cross which would be undone by a bounce to at least 26.

This was the first morning since Thursday in which VIX didn’t test or break below support at 24.84. The SMA10 currently stands slightly lower than the SMA10 – a bearish cross which would be undone by a bounce to at least 26. As mentioned above, CPI didn’t reflect the EIA’s gas price data. In August, the MoM decrease of -0.3% and YoY decrease of -16.9% resulted in CPI of 0.4%/1.3%. Gasoline came in at a 2.0% MoM increase according to the BLS – an obvious overstatement which supported the higher inflation data reported.

As mentioned above, CPI didn’t reflect the EIA’s gas price data. In August, the MoM decrease of -0.3% and YoY decrease of -16.9% resulted in CPI of 0.4%/1.3%. Gasoline came in at a 2.0% MoM increase according to the BLS – an obvious overstatement which supported the higher inflation data reported.

This month, the MoM increase of 0.1% and a YoY decrease of -15.8% produced CPI of 0.2%/1.4%. The BLS reported a 0.1% increase, in line with EIA data. This contributed to headline CPI that is more in line with where the Fed/Treasury need it to be.

We could quibble over the BLS’ faulty/disingenuous methodology, but in this era of ever expanding trillion dollar deficits, it’s crucial to keep interest rates low. Therefore, it’s crucial to keep inflation low (or, at least reported inflation.)

Of course, the idea that it would remain so low in the face of trillions in stimulus and added liquidity could be viewed as somewhat alarming. There has clearly been no widespread “lift off” as viewed through the prism of official inflation data – though pockets of price inflation can easily be seen in financial assets, single-family residential real estate, used cars and food.

UPDATE: 3:55 PM

Coming up on the close, and stocks have recovered some of their earlier losses.  VIX looks like it’ll unwind the bearish 10/20 cross.

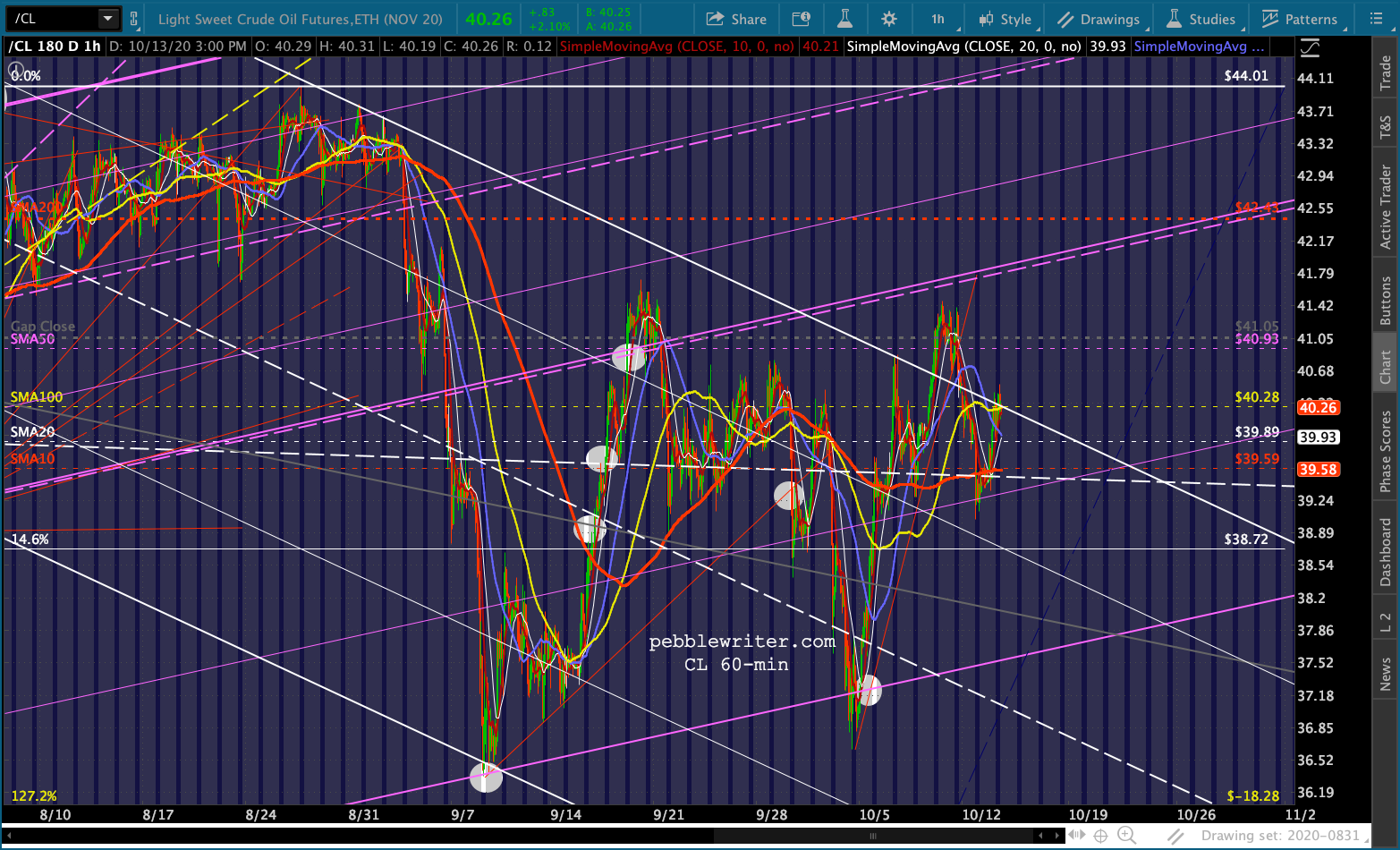

VIX looks like it’ll unwind the bearish 10/20 cross. Everything else is iffy. CL is threatening a breakout of the falling white channel. This remains an important question: which channel to follow.

Everything else is iffy. CL is threatening a breakout of the falling white channel. This remains an important question: which channel to follow.

And, USDJPY has broken below the red TL but is sitting atop the purple channel .786 line with a tag of the falling purple channel top still a possibility.

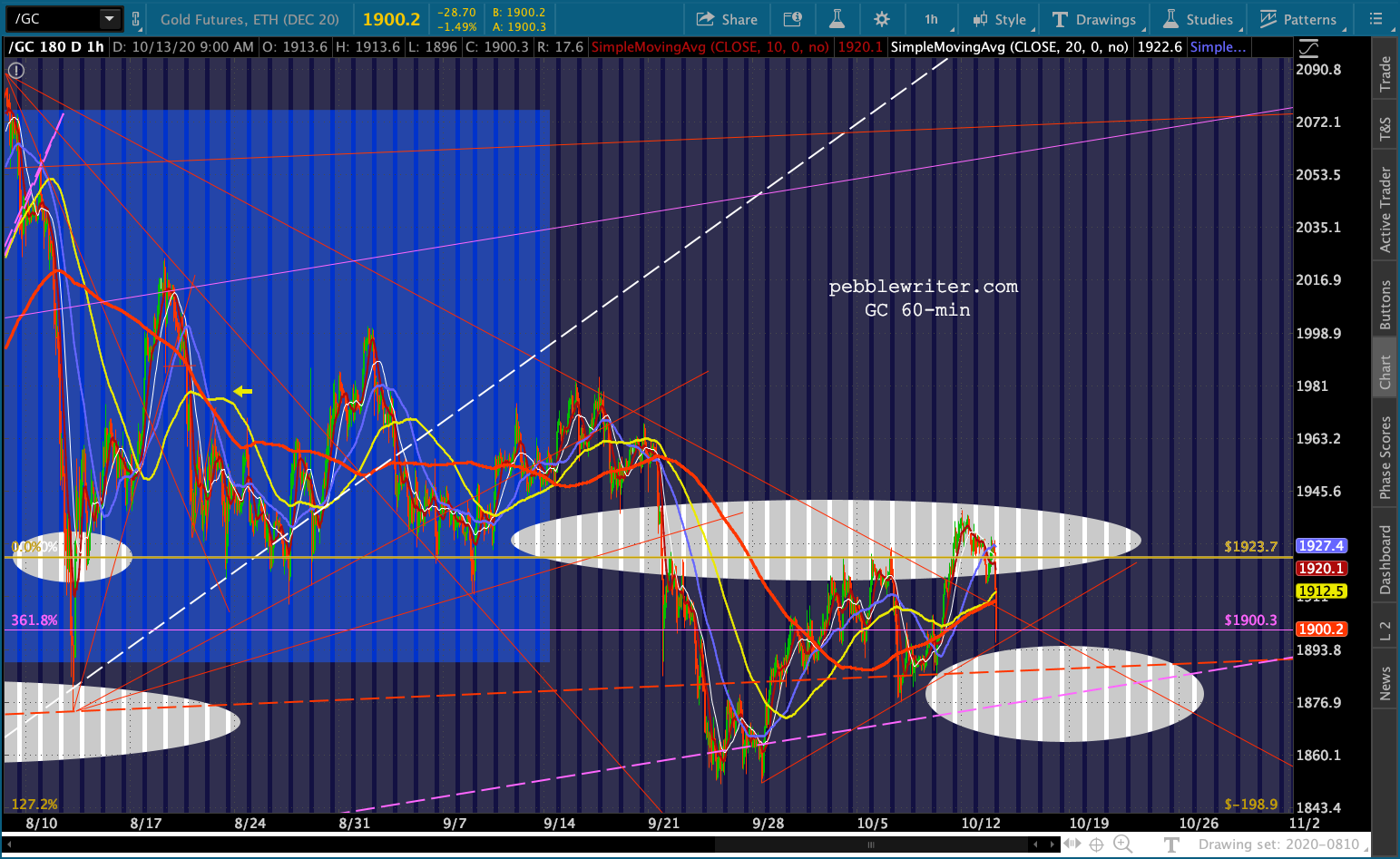

And, USDJPY has broken below the red TL but is sitting atop the purple channel .786 line with a tag of the falling purple channel top still a possibility.  GC managed to hold on to support – both the red TL and the purple and red midlines. The SMA100 is coming up fast, currently at 1870.60.

GC managed to hold on to support – both the red TL and the purple and red midlines. The SMA100 is coming up fast, currently at 1870.60.