I’ve glanced wistfully over the years at announcements of runs I’ve enjoyed in the past: countless 5Ks, 10Ks and a handful of marathons. Together with high school football, college rugby and too many pickup basketball games to count, they had bestowed me with the knees of a senior citizen well before any gray hair clocked in.

But, 2020 was a transformative year. I had one knee replaced, then the other – which of course made my shoulders jealous. Two shoulder surgeries later, I felt better than I had in years – racking up 40-50 miles per week during which I occasionally snuck in a few miles of running (okay, shuffling.)

When the UCLA Anderson School of Management email arrived announcing a virtual run for charity, I figured it was time to put my surgeons’ handiwork to the test and signed up for the half marathon. Though it was 24 degrees when I laced up the Sauconys Saturday morning, I felt fantastic.

The knees were rock solid, barely raising a fuss. The most recently repaired shoulder – still in a sling – grumbled a bit under its breath, but acquiesced. At the halfway mark, I even picked up my pace. That, as it turns out, was a mistake.

The known risks weren’t a problem. It was the known unknown ones – the Morton’s neuromas I had forgotten about because they stopped hurting years ago when I was forced to stop running – that blew up my performance. I walked the final five miles, wincing with every step.

So it was with the Archegos fiasco. Without a doubt, someone at Credit Suisse and Nomura had given at least some thought to the size of the virtual position Archegos might have amassed and the possibility that it might have made similar bets at rival banks. Certainly they had done the math on their own position. So why the billions in losses?

Could it have anything to do with this guy?

For the past 12 years, the Fed has offered an implicit (and often explicit) assurance that nothing bad will happen to equity investors. That’s the carrot. The stick is that bond returns have been pounded into the proverbial dirt, offering negative nominal yields in many cases and negative real yields in even more.

For the past 12 years, the Fed has offered an implicit (and often explicit) assurance that nothing bad will happen to equity investors. That’s the carrot. The stick is that bond returns have been pounded into the proverbial dirt, offering negative nominal yields in many cases and negative real yields in even more.

Together with other central bankers, treasuries, and their proxies, they have backed up that assurance with intervention that was once considered unthinkable except under the most extreme circumstances. Consider the March 2020 lows. Is it a coincidence that the Dow bottomed out at 18,213.65, a meager 39 points (0.2%) from the lows registered on Nov 9, 2016, the day after the presidential election?

And, while we’re talking about November 9, 2016…how is it that VIX suddenly collapsed even as the futures screamed southward, off 4.5% in the wake of the news that Trump had won? This would be tantamount to calling your insurance agent to cancel your flood insurance as a hurricane is bearing down on your beachfront cottage.

And, while we’re talking about November 9, 2016…how is it that VIX suddenly collapsed even as the futures screamed southward, off 4.5% in the wake of the news that Trump had won? This would be tantamount to calling your insurance agent to cancel your flood insurance as a hurricane is bearing down on your beachfront cottage.

VIX had spiked 55% within an hour or so. But, it suddenly reversed and gave up all that and more even as ES was still melting down. It even managed to break down from the rising channel it had established 4 months before.

After a few weeks of being mercilessly hammered at every turn, VIX would reach levels not seen since February 2007. Its “breakdowns” would eventually become commonplace whenever stocks reached significant resistance or needed help in the face of inconvenient news or economic data.

After a few weeks of being mercilessly hammered at every turn, VIX would reach levels not seen since February 2007. Its “breakdowns” would eventually become commonplace whenever stocks reached significant resistance or needed help in the face of inconvenient news or economic data. The Fed’s message is clear, and the algorithms have taken it to heart. But, it is not without consequences. Many stocks have risen well above their Feb 2020 highs even though their earnings are nowhere close to where they were a year ago. The prices of many commodities have also soared, spawning a coming spike in inflation to over 3%. Ultra-low mortgage rates have driven housing prices out of reach for many.

The Fed’s message is clear, and the algorithms have taken it to heart. But, it is not without consequences. Many stocks have risen well above their Feb 2020 highs even though their earnings are nowhere close to where they were a year ago. The prices of many commodities have also soared, spawning a coming spike in inflation to over 3%. Ultra-low mortgage rates have driven housing prices out of reach for many.

Perhaps most concerning, the Fed is playing a dangerous game of chicken with the bond market in the midst of an unprecedented explosion of debt. New issuance is running about $650 billion per quarter. Who’s going to buy all those treasuries, knowing that they’ll receive negative real yields now and face substantial interest rate risk as inflation spikes higher and the Fed has to taper or even [he shudders] raise rates?

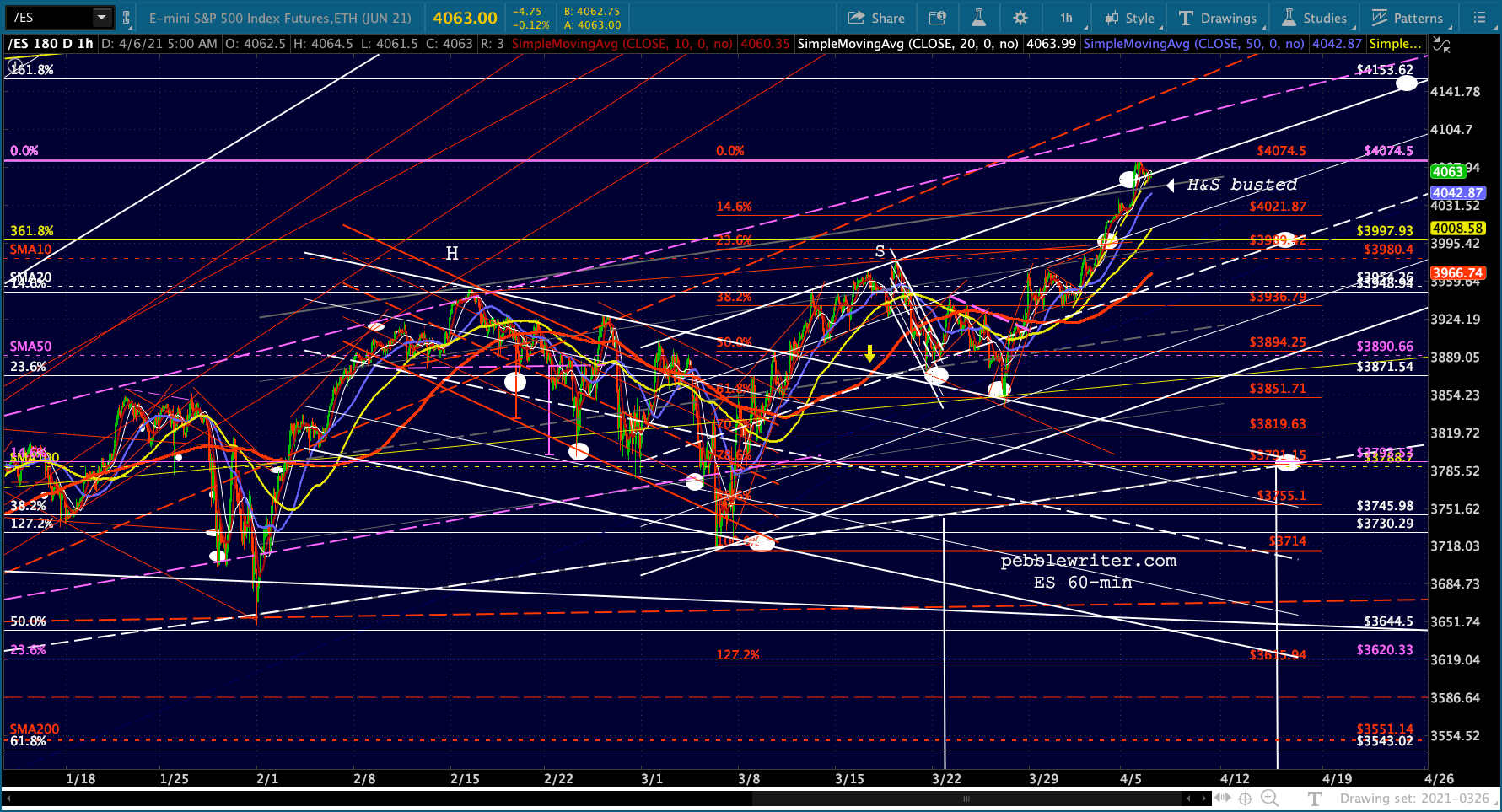

continued for members…The big picture hasn’t changed much, though the ceiling has obviously moved higher since yesterday morning. VIX is still in the driver’s’ seat.

Note that DJI is still shy of its 3.618 – though it has bumped up against the top of its rising channel.

Note that DJI is still shy of its 3.618 – though it has bumped up against the top of its rising channel.

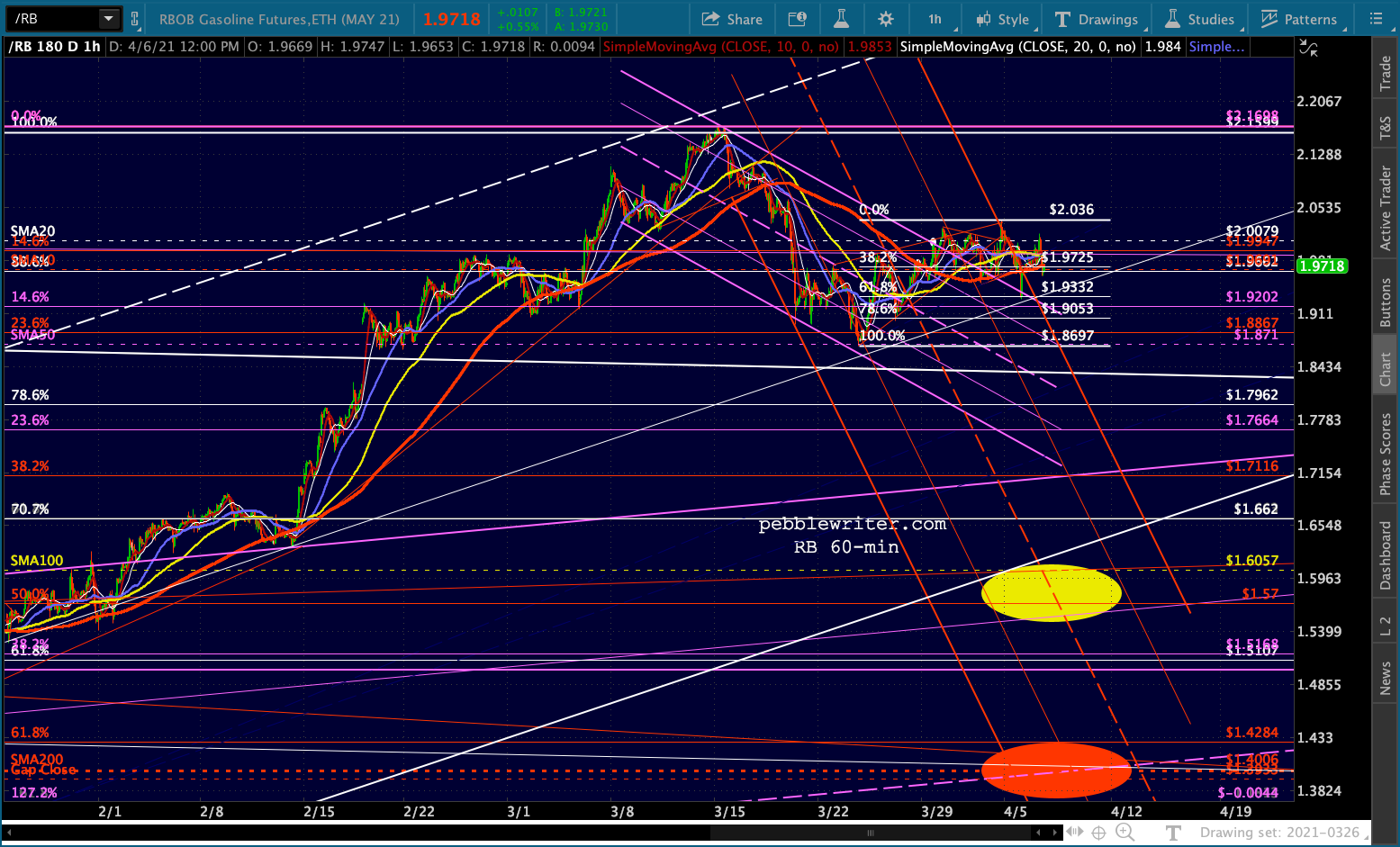

FWIW, USDJPY is breaking down a little bit…

FWIW, USDJPY is breaking down a little bit…

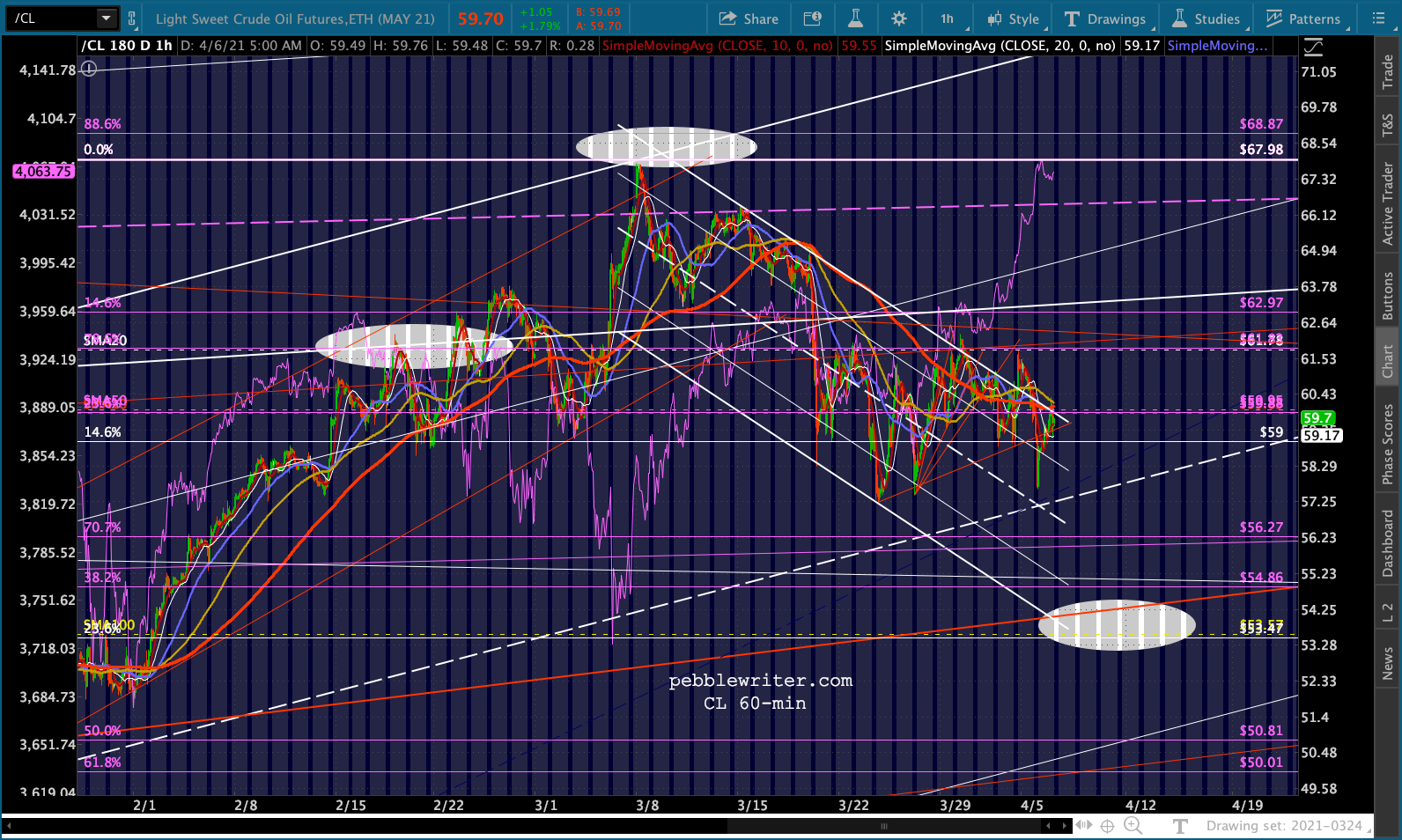

and NKD continues to suggest a decent selloff to backtest its SMA200.