Single-family home starts continued to gain from rock bottom interest rates and the exodus from urban, multifamily housing amid the pandemic. September residential starts grew 1.9%, while permits rose 5.2%, the fastest since the 2007 peak.

Single-family inventory dipped to 3.3 months, the smallest since 1963, while multifamily starts cratered by 16.3%.

Single-family inventory dipped to 3.3 months, the smallest since 1963, while multifamily starts cratered by 16.3%.

It was a bright spot of economic news following an ugly day of losses across all indices yesterday that saw ES tumble to our next downside target.

continued for members…Futures are up modestly after giving up much of their overnight gains.

continued for members…Futures are up modestly after giving up much of their overnight gains.

VIX didn’t quite make it to the SMA200, leaving room for additional downside in equities.

VIX didn’t quite make it to the SMA200, leaving room for additional downside in equities.

The major factor driving equities higher overnight was the USDJPY, which spiked up through its SMA10 and SMA20 to its SMA50.

The major factor driving equities higher overnight was the USDJPY, which spiked up through its SMA10 and SMA20 to its SMA50. The channel top and SMA100 remain in play until we get another breakdown.

The channel top and SMA100 remain in play until we get another breakdown.  Meanwhile, EURUSD bounced a little more and DXY settled lower…

Meanwhile, EURUSD bounced a little more and DXY settled lower…

…despite more levitation in the 10Y…

…despite more levitation in the 10Y… …which continues to hold important price support.

…which continues to hold important price support.  Gold and silver continue to eek out just enough gains to maintain upside potential – but unlikely to break out until we get more stimulus. Both remain in a bullish 10/20 cross.

Gold and silver continue to eek out just enough gains to maintain upside potential – but unlikely to break out until we get more stimulus. Both remain in a bullish 10/20 cross.

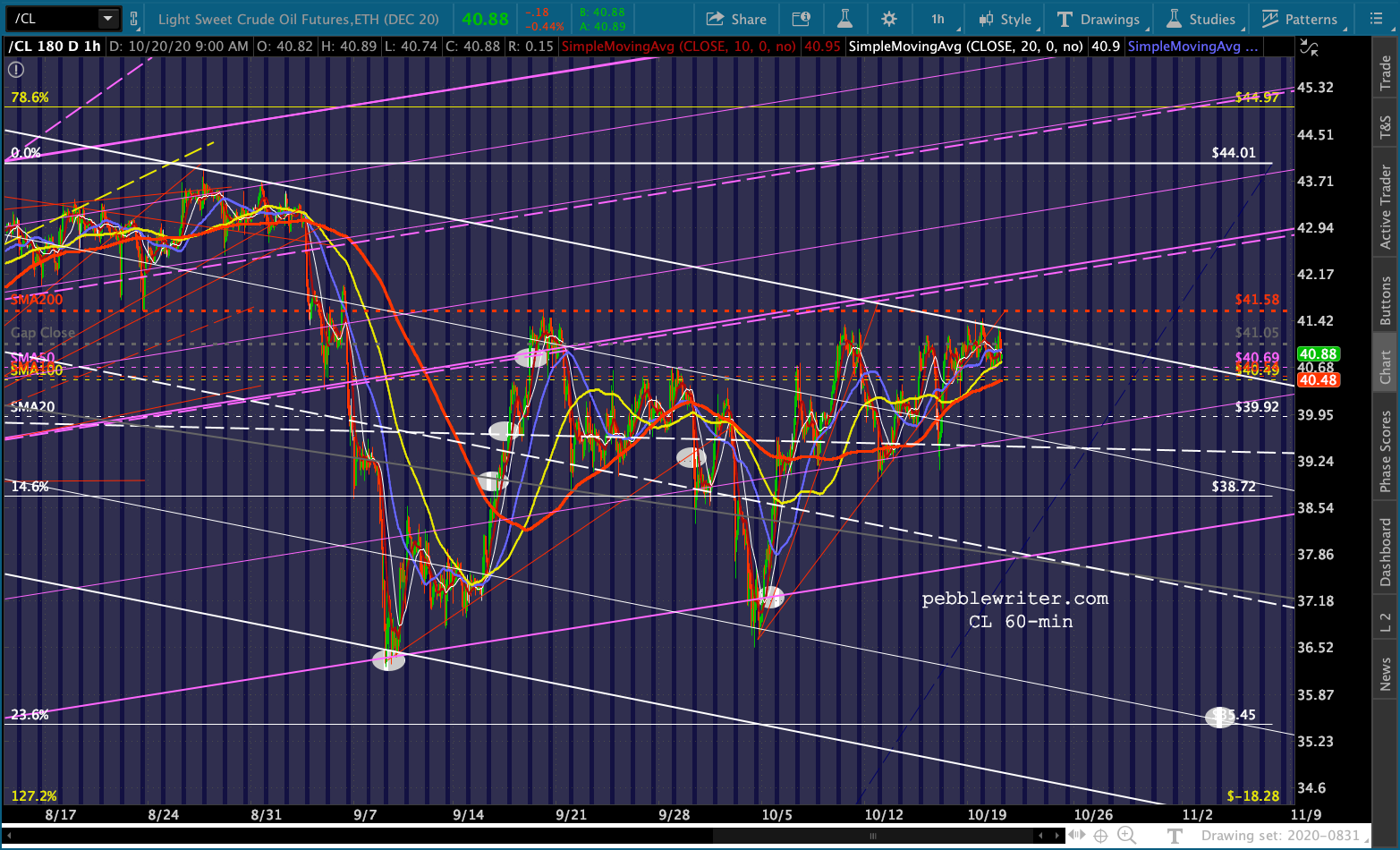

Oil and gas continue to be supportive, not breaking down yet (but not breaking out.) They also remain in a bullish 10/20 cross.

Oil and gas continue to be supportive, not breaking down yet (but not breaking out.) They also remain in a bullish 10/20 cross.

Bottom line, the factors are acting just strong enough to buy a little time. If VIX and CL join in and USDJPY can push above 105.60, we could see an extended bounce. Likewise, a breakthrough on stimulus would obviously boost stocks. Otherwise, SPX’s SMA10 at 3463.32 should prove effective resistance.

Bottom line, the factors are acting just strong enough to buy a little time. If VIX and CL join in and USDJPY can push above 105.60, we could see an extended bounce. Likewise, a breakthrough on stimulus would obviously boost stocks. Otherwise, SPX’s SMA10 at 3463.32 should prove effective resistance.

More later…

UPDATE: 3:50 PM

We almost got down to ES 3400, but VIX and USDJPY have been constrained. Maybe after the close or first thing in the morning…