Let’s face it. The reflation trade is dead. It’s not that we don’t have inflation. It’s just that the way in which inflation is reported in the US makes it appear not to be a problem.

Not only does this save mountains of moola on cost of living increases, it makes it much easier for the Fed to keep interest rates at historic lows (very important when you’re in hock to the tune of $20 trillion.)

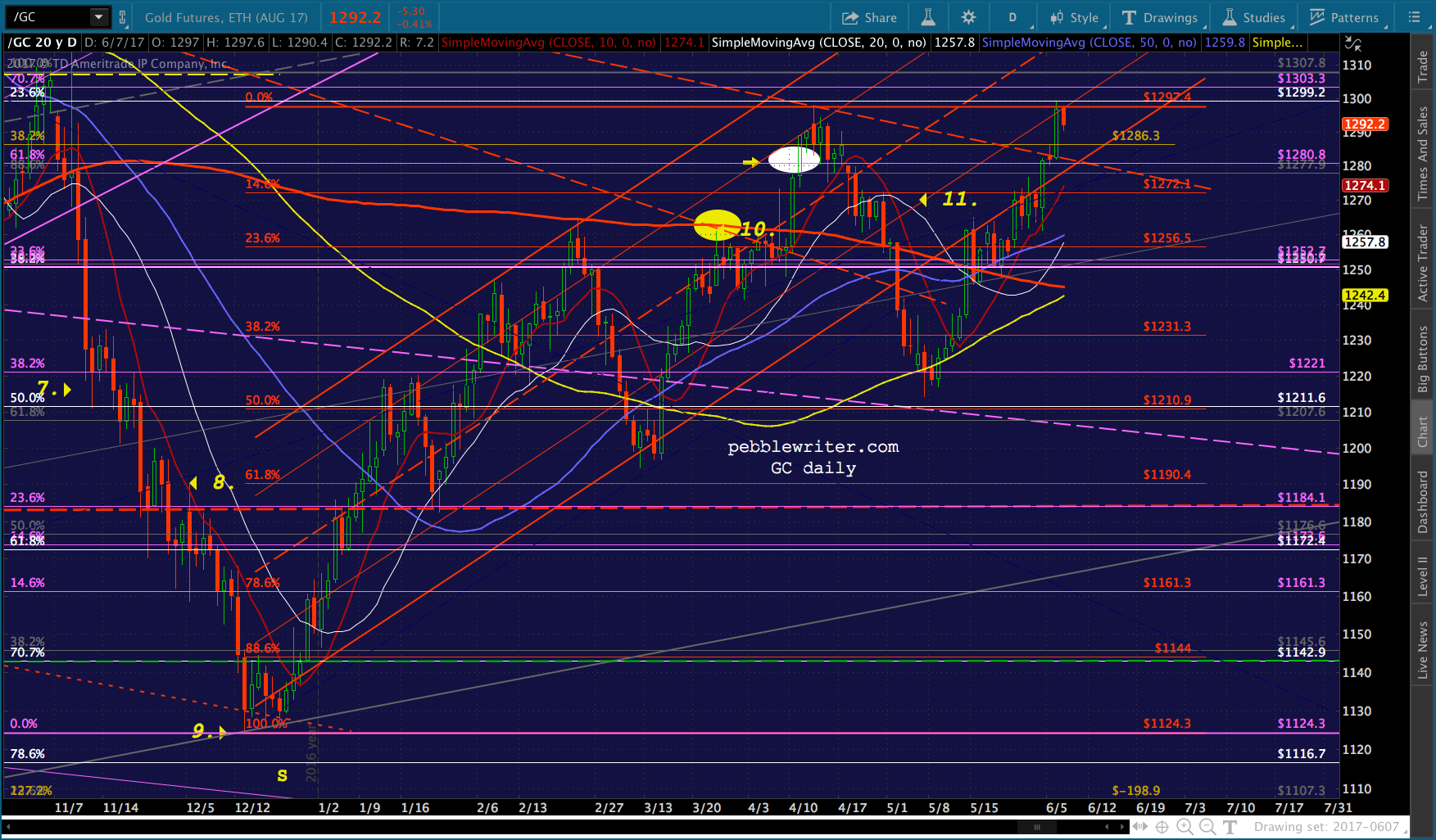

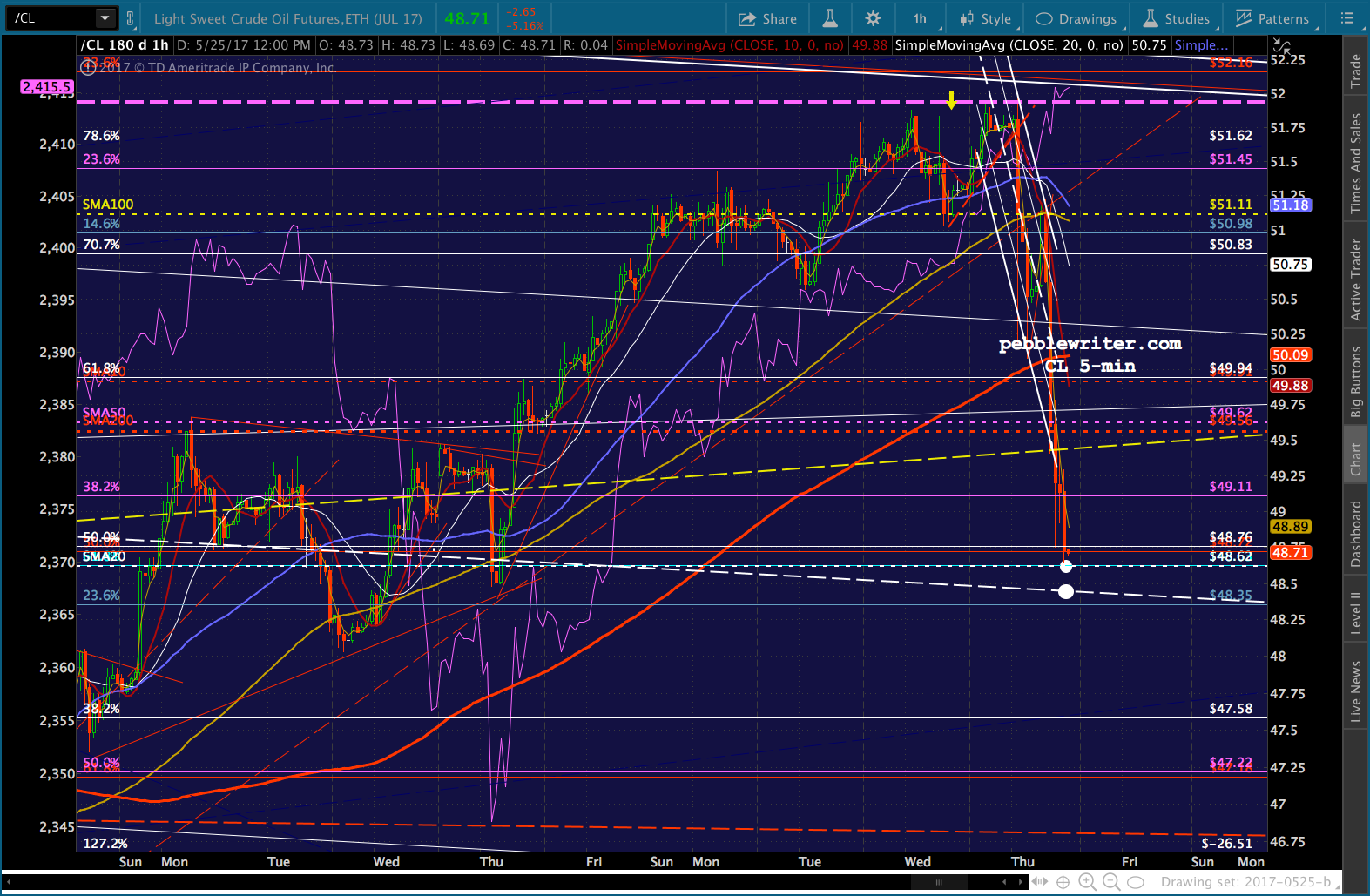

Keeping this thought in mind is important when it comes to predicting what the Fed is going to do, say, next week. And, it has sure come in handy when forecasting the price of oil, gold, the USD, etc. (oil nailed our next downside target overnight.)

Now, the $64 trillion question: if the reflation trade is dead, what about the Trump Rally? It seems stocks have been operating in another universe — where earnings, geopolitical events, and macroeconomics no longer apply.

Now, the $64 trillion question: if the reflation trade is dead, what about the Trump Rally? It seems stocks have been operating in another universe — where earnings, geopolitical events, and macroeconomics no longer apply.

Regular readers know that I’ve poo-pooed the Trump Rally from the start [see: Why the Trump Rally is a Fraud and Central Banks and Markets for starters.] It was built on a foundation of a historic crash in VIX and spike in USDJPY.

No doubt, some fundamental investors piled on, buying the idea that Trump could bend the laws of mathematics to his will (lower taxes and increased spending without increasing the debt/deficit.) Others correctly reasoned that such an exercise would produce inflation, which is usually a good thing for at least nominal, if not real, returns.

And, a considerable number of trend followers jumped on board once key technical levels were taken out. But, the fundamental crowd has probably realized, by now, that there’s a difference between campaign promises and signed legislation.

If reflation isn’t, and the fundamentalists lose faith in Trump’s magic, what’s to keep markets ratcheting higher?

continued for members…

(more…)