Last week, both SPX and ES reached Inverted Head & Shoulders targets we established nearly a year ago [see: CIW July 11, 2016.] Not too surprisingly, they topped those targets on Friday, then spent the day defending them. This pattern of slicing through upside resistance and then defending the hell out of it has been a constant over the past several years. But, it’s been ever more blatant since last year’s election.

We’ve covered the whys, wherefores and hows extensively. Consider, for instance, how VIX continues to test all-time lows, constructing arbitrary channels and trend lines which it can then “break down” through at key moments.

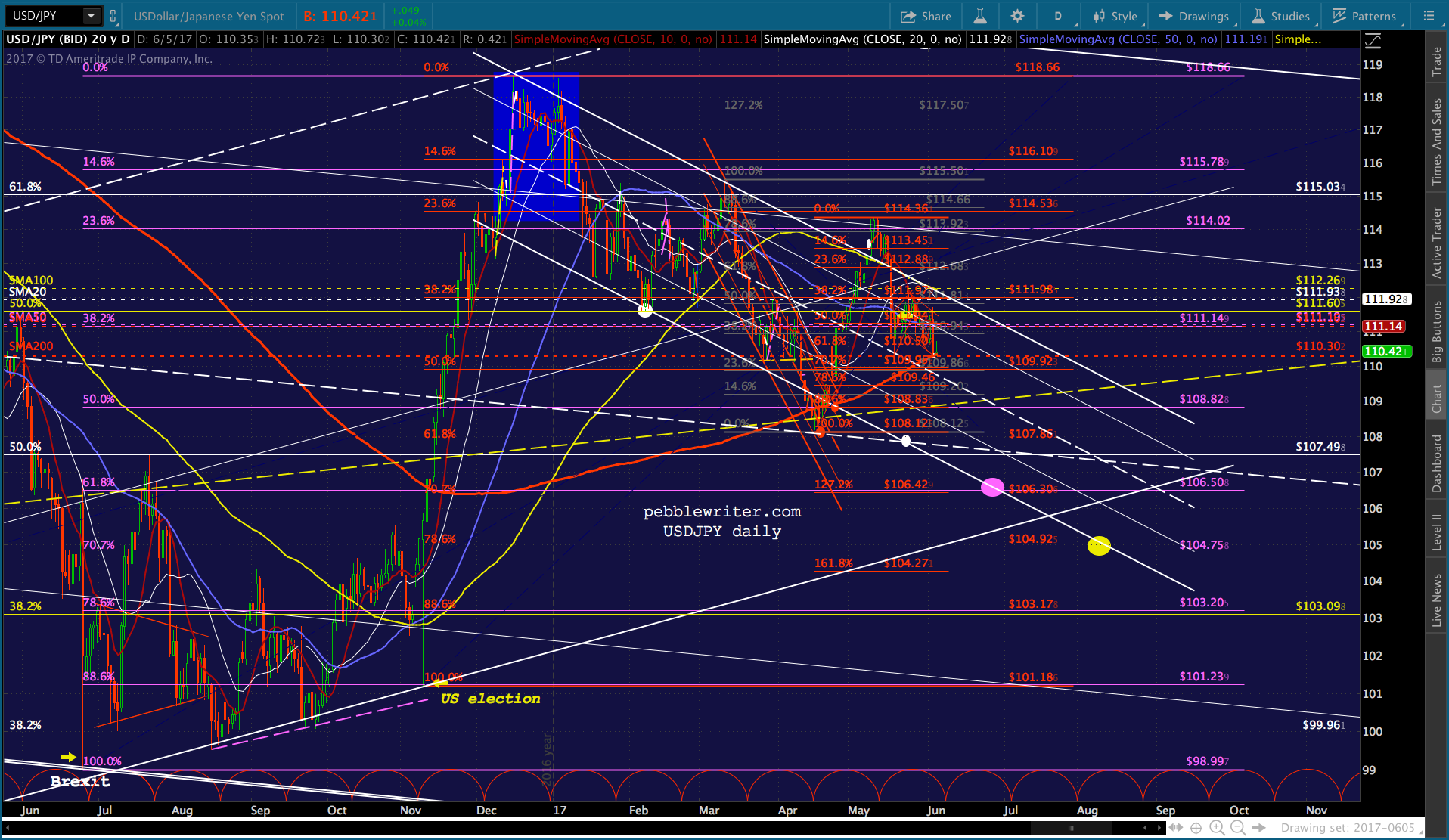

Another favorite trick is ramping higher overnight, when futures are easily supported, only to plunge during the session when stocks need a boost. With futures currently off a couple of points, we should see it play out this morning. Another common occurence we’ve examined at length is the use of well-timed rallies in oil and USDJPY. On May 19, I identified a trade opportunity for USDJPY, noting that it was likely to drop from 111.40 to its SMA200 — then at 109.76. It was a nice short with a modest but healthy payoff. All it had to do was continue lower in the red channel shown below.

Another common occurence we’ve examined at length is the use of well-timed rallies in oil and USDJPY. On May 19, I identified a trade opportunity for USDJPY, noting that it was likely to drop from 111.40 to its SMA200 — then at 109.76. It was a nice short with a modest but healthy payoff. All it had to do was continue lower in the red channel shown below. Instead, it constructed a series of bounces and sharp rallies which boosted stocks and, ultimately, enabled it delay the tag until it constituted a higher low. Instead of dropping to 109.76, it waited until the SMA200 had risen to 110.30. When the tag finally occurred, it was at 8pm on a Sunday night.

Instead, it constructed a series of bounces and sharp rallies which boosted stocks and, ultimately, enabled it delay the tag until it constituted a higher low. Instead of dropping to 109.76, it waited until the SMA200 had risen to 110.30. When the tag finally occurred, it was at 8pm on a Sunday night. In the time it took to write the above, VIX has “broken down” through TL support, presumably because SPX’s 3.42-pt drop was getting out of hand. Somewhere, someone is calculating how much further it would need to be hammered in order to get stocks back to green.

In the time it took to write the above, VIX has “broken down” through TL support, presumably because SPX’s 3.42-pt drop was getting out of hand. Somewhere, someone is calculating how much further it would need to be hammered in order to get stocks back to green. I remember chuckling in 2014 when Bernanke said that rates would never normalize during his lifetime. How could he be so certain? His economic forecasting skills had certainly fared poorly. Apparently, his hubris had emerged unscathed.

I remember chuckling in 2014 when Bernanke said that rates would never normalize during his lifetime. How could he be so certain? His economic forecasting skills had certainly fared poorly. Apparently, his hubris had emerged unscathed.

JP Morgan now calculates that one-third of the world’s $54 trillion in tradable bonds are currently owned by central banks, confirming what we chartists have observed for years: interest rates are too important to be left to the vagaries of unpredictable investors and traders.

The same can obviously be said for equities. As trading volume continues to drop and passive strategies attract an ever-larger share of assets, entire markets have become more easily manipulated by central banks. The BoJ and SNB buy shares outright. The ECB and Fed intervene indirectly by manipulating the primary inputs to algorithms that drive so much of the daily price action.

The same can obviously be said for equities. As trading volume continues to drop and passive strategies attract an ever-larger share of assets, entire markets have become more easily manipulated by central banks. The BoJ and SNB buy shares outright. The ECB and Fed intervene indirectly by manipulating the primary inputs to algorithms that drive so much of the daily price action.

I had an interesting chat with a fellow student of the markets yesterday. He posed the question: “is this 1995 or 1999?” I think that’s the most important question investors can be asking themselves right now.

I had an interesting chat with a fellow student of the markets yesterday. He posed the question: “is this 1995 or 1999?” I think that’s the most important question investors can be asking themselves right now.

I’ve maintained since March that a June rate hike was problematic. In April, I started incorporating it into our big picture forecasts. And, on May 12 I made it official with the post Bye Bye Rate Hikes. Ten years since the onset of the Great Financial Crisis (and over four years since the S&P 500 recovered enough to make new, all-time highs), markets have never been more dependent on the activities of central bankers.

continued for members…

continued for members…

I think currencies are now almost completely captive — that is, very few major moves will occur without the express consent of the Fed, BoJ and ECB. As such, we will probably continue to see them move in a fairly tight range for the foreseeable future.

Likewise, I think oil is being fairly well controlled — though geopolitical events still have the ability to shock them into sizable moves.

VIX is the ace in the hole — completely manipulable, though with an obvious limit as to how much lower it can go (negative VIX, anyone?)

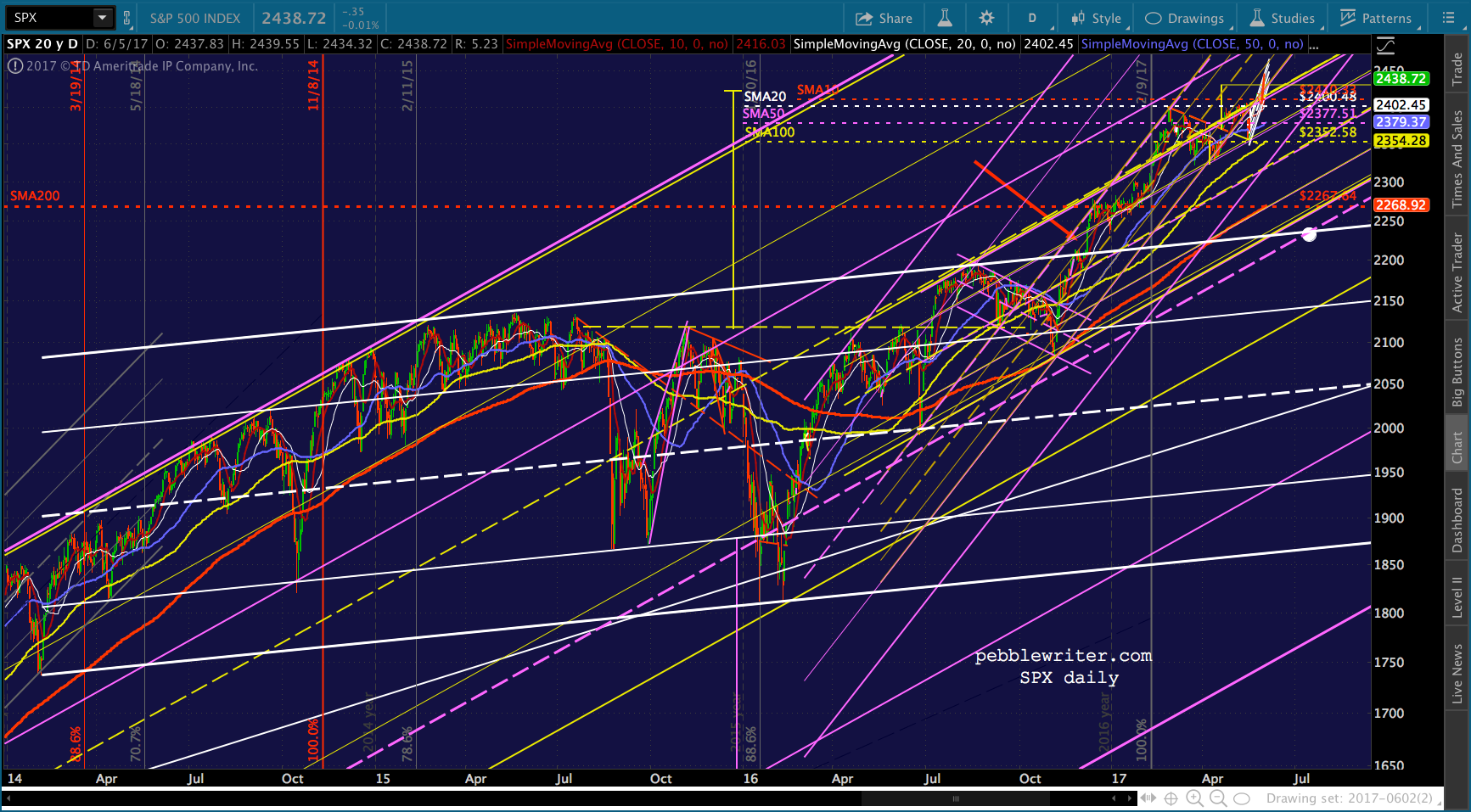

Given the above, I think we’ll see stocks continue to defend the recent breakout. If something alarming occurs, we might see a drop to major support such as the SMA100 (2354) or 200 (2268), a channel bottom, etc. And, if something undeniably bearish occurs, we’ll see the rising channels get fleshed out and major Fib lines backtested.

As we pointed out last week, this could produce some very large drops. As such, I believe the odds of such an occurrence are quite low.

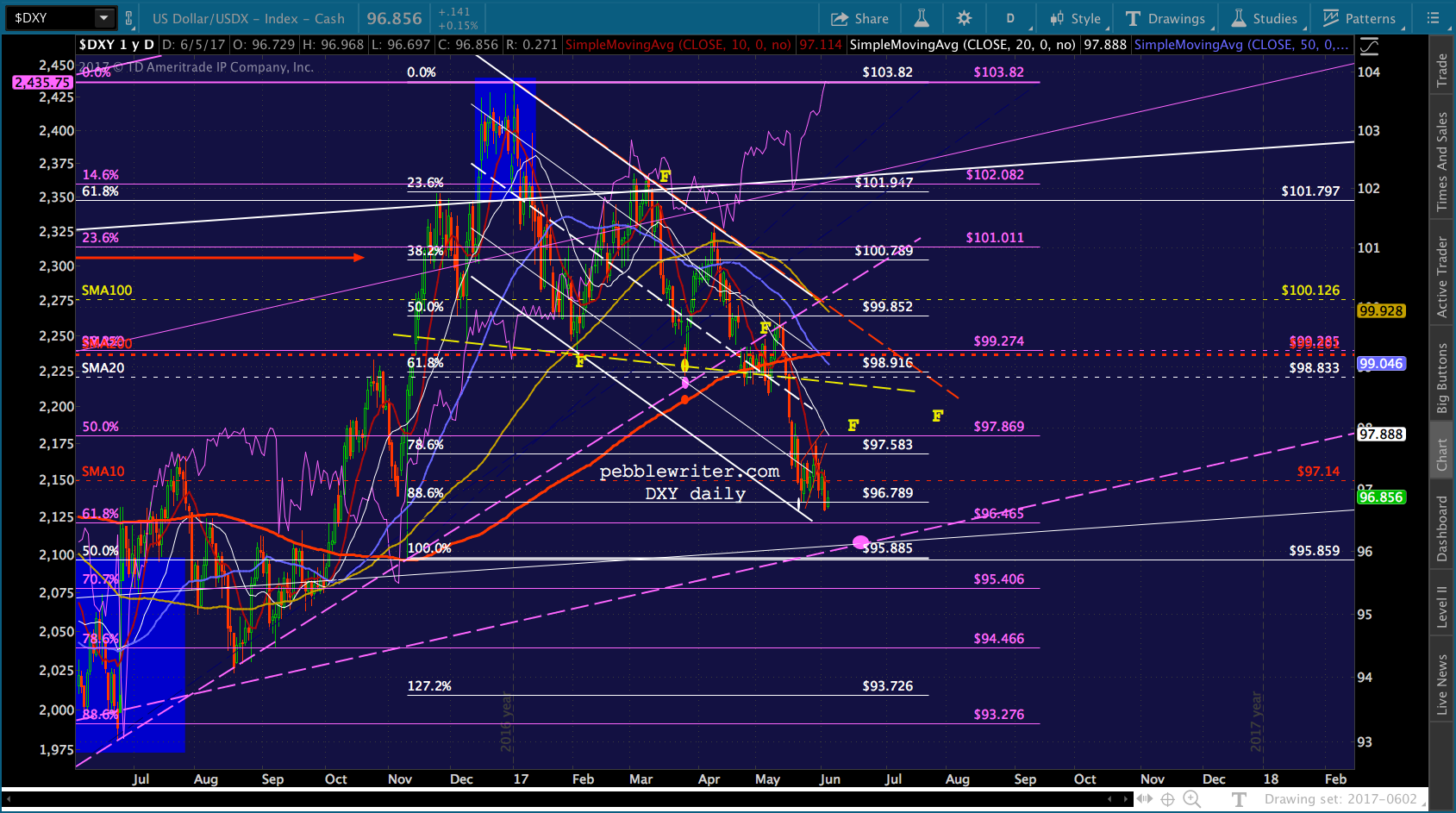

Until something breaks, I think the key to successfully trading equities will be to retain a long bias, but look for situations where they are likely to backtest something significant and/or situations where they have broken down. With DX still falling, we’re likely to see some downside opportunities between now and Jun 21 or so.

We’ve seen several opportunities over the past week or two where we were able to pick up 2-3% in a day or two when SPX round-tripped back to where it started. It’s not anything to write home about, but a few times each month and you’ve got yourself a 10% month.

The other option, of course, is to find good trades in VIX, USDJPY, EURUSD and CL. Our USDJPY experience aside, I continue to believe it’s easier to trade the drivers of algos than it is the resulting equity moves.

Next moves:

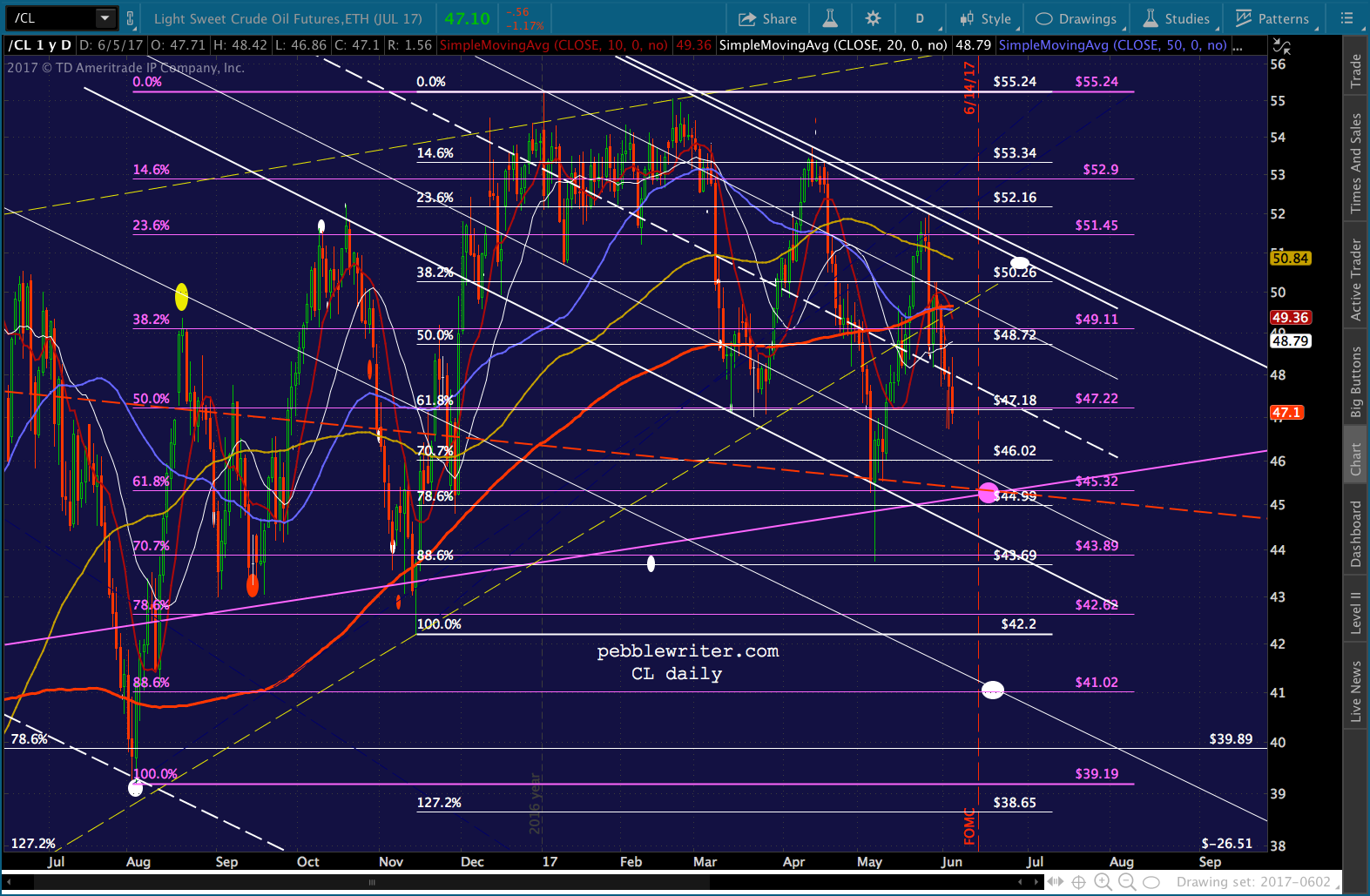

For now, I see DX continuing to drop to the purple channel midline — probably around 96.11 on June 21. If this doesn’t hold, then the USD is in real trouble, with the next not-so-strong support at 94.466. CL broke down through the white midline and, unless it rebounds back above 48, has additional downside potential to 45.22 and, below that, to 41.02.

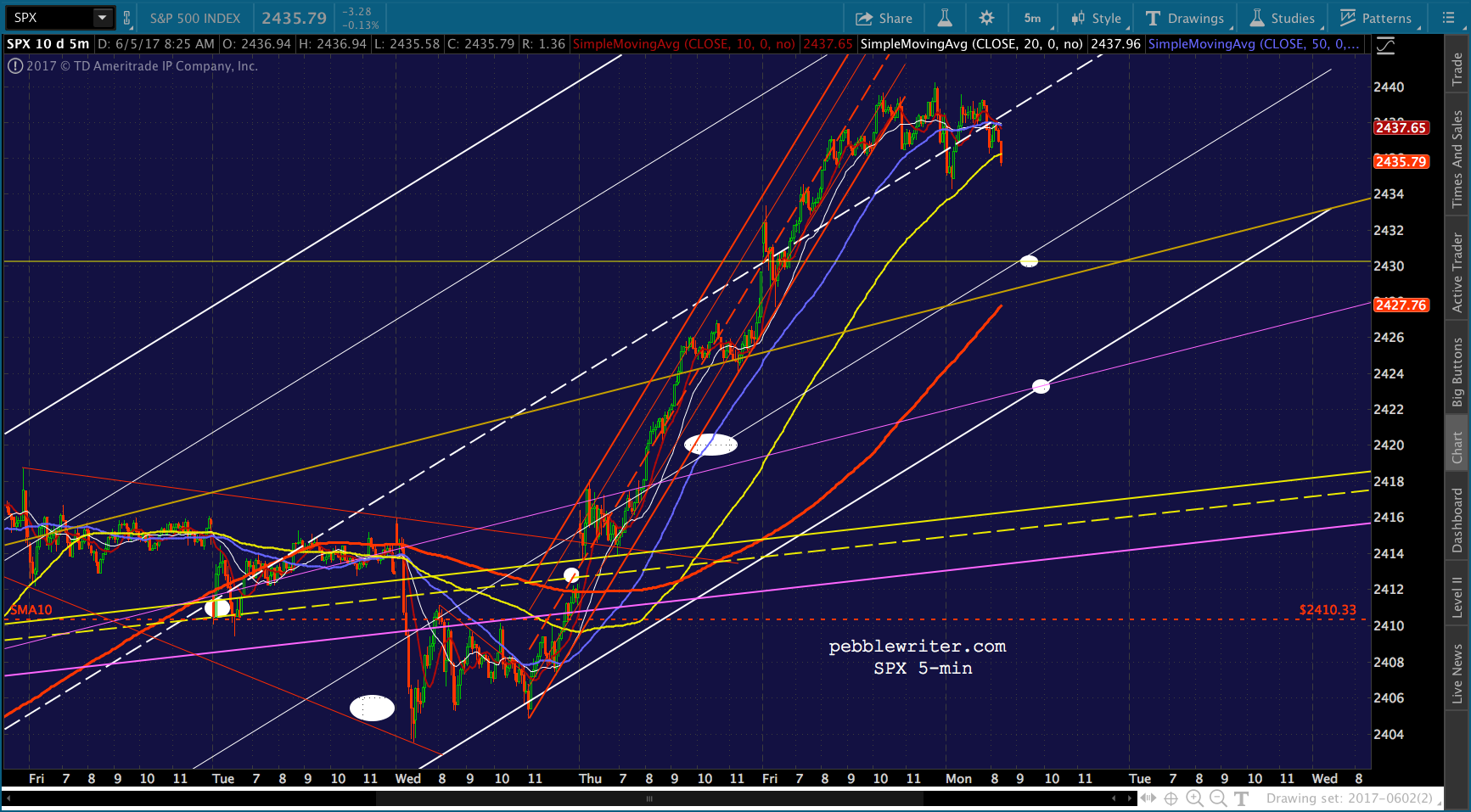

CL broke down through the white midline and, unless it rebounds back above 48, has additional downside potential to 45.22 and, below that, to 41.02. SPX has support back at 2430 (with the arrival of the SMA5 200) and, below that, at 2423-2424 (only if it hurries.)

SPX has support back at 2430 (with the arrival of the SMA5 200) and, below that, at 2423-2424 (only if it hurries.)

If things really get ugly, we could even backtest the broken white channel at 2233 in July.

If things really get ugly, we could even backtest the broken white channel at 2233 in July.

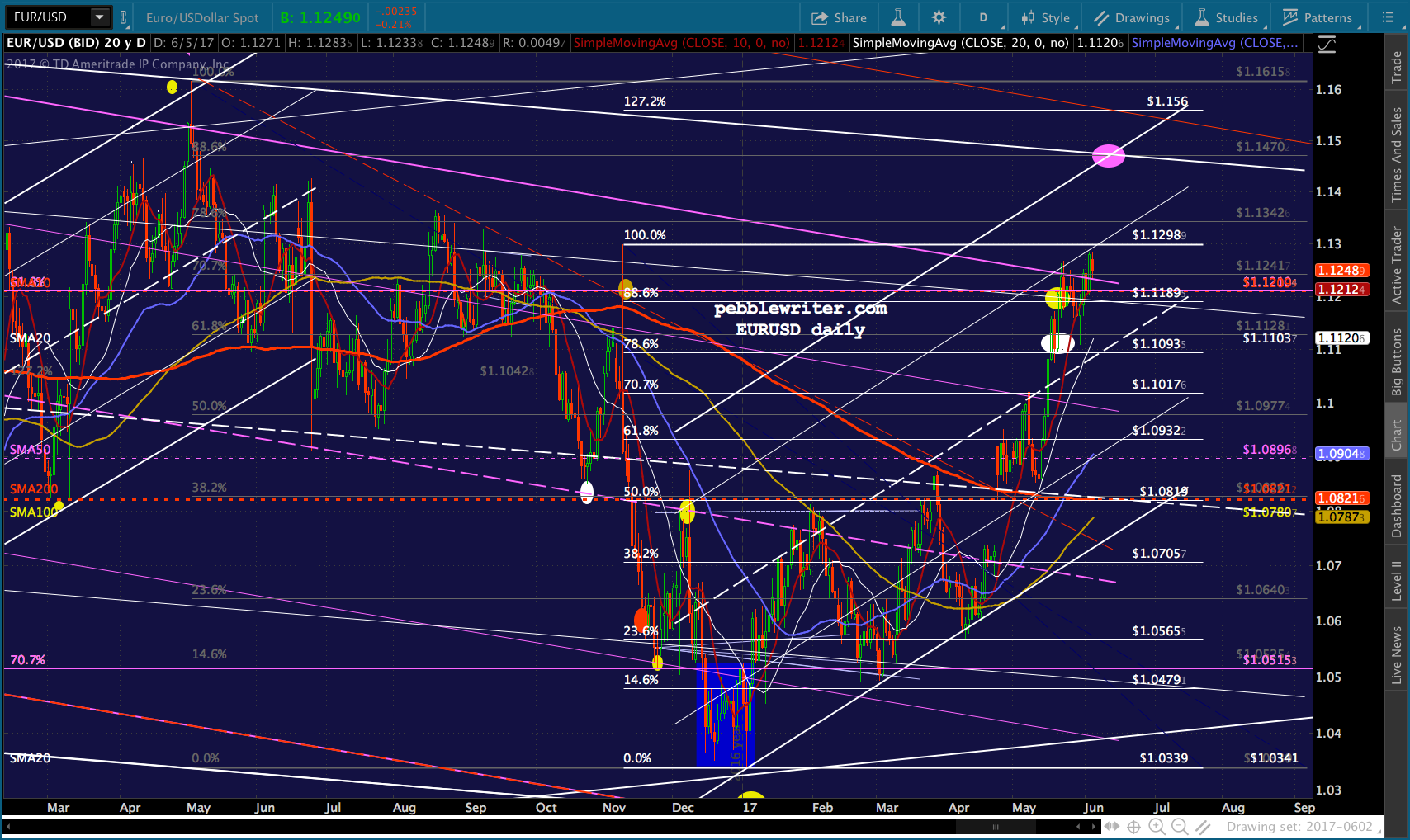

If USDJPY should drop through its SMA200 when, as I expect, the Fed punts on a June rate hike, it has potential to 107.86, followed by 106.50 and 104.92. And, as we discussed last week, EURUSD seems destined for 114.72ish.

And, as we discussed last week, EURUSD seems destined for 114.72ish. With the exception of SPX, these are all big-picture, swing moves that will rely greatly on the dollar continuing to drop. If members are amenable, I’d like to focus more on them over the coming weeks and see how they play out.

With the exception of SPX, these are all big-picture, swing moves that will rely greatly on the dollar continuing to drop. If members are amenable, I’d like to focus more on them over the coming weeks and see how they play out.

In looking at the summer ahead, I’ve decided to get some R&R here and there — starting with this week. It’ll be a “stay-cation” for us, which means I’ll continue to post my general thoughts each morning while getting caught up on some neglected indices, currency pairs, etc.

If anyone has any urgent requests, please pass them along and I’ll get to them as best I can. And, for those who would appreciate more frequent FX setups or who have other suggestions, please let me know.

GLTA.