I suspect today will be another one of those days, like yesterday, when every little dip in SPX is met with a corresponding dip in VIX, i.e. more melting up.  The 5-point gain in the futures came courtesy of the rising VIX channel “breaking down” at 7:15 ET (the white arrows.) Sadly, that’s all it takes these days.

The 5-point gain in the futures came courtesy of the rising VIX channel “breaking down” at 7:15 ET (the white arrows.) Sadly, that’s all it takes these days.

FWIW, I’ll leave yesterday’s downside targets for SPX and USDJPY in place just in case the VIX bashing lets up.

* * *

Instead of tracking those squiggles, I’m going to take the day and make some sense of yesterday’s word salad that started out as an update on oil. In analyzing oil, I was able to solve some puzzles regarding the relationships between oil, equities, currencies, interest rates, debt and inflation that been nagging me for quite some time.

Did you know, for instance, that although interest rates have been sliced in half since 2008, we’ll spend more servicing the federal debt in 2017? At the current run rate, we’ll spend over $500 billion for the first time in history — more than Medicaid and almost as much as on Medicare or the military. Some of the projections for future growth are downright frightening. From a central banker’s perspective, it must be terrifying — particularly if you take inflation into account. Traditionally, higher inflation has been countered with higher interest rates. But, how does that pencil out when debt and interest expenses are already past the point of no return?

From a central banker’s perspective, it must be terrifying — particularly if you take inflation into account. Traditionally, higher inflation has been countered with higher interest rates. But, how does that pencil out when debt and interest expenses are already past the point of no return?

This quandary helps explain many of the zigs and zags in the markets over the past 10 years. I suspect it will become even more important in the year ahead as we forecast the Fed’s actions and their likely outcome on markets.

continued for members…

UPDATE: 10:02 AM

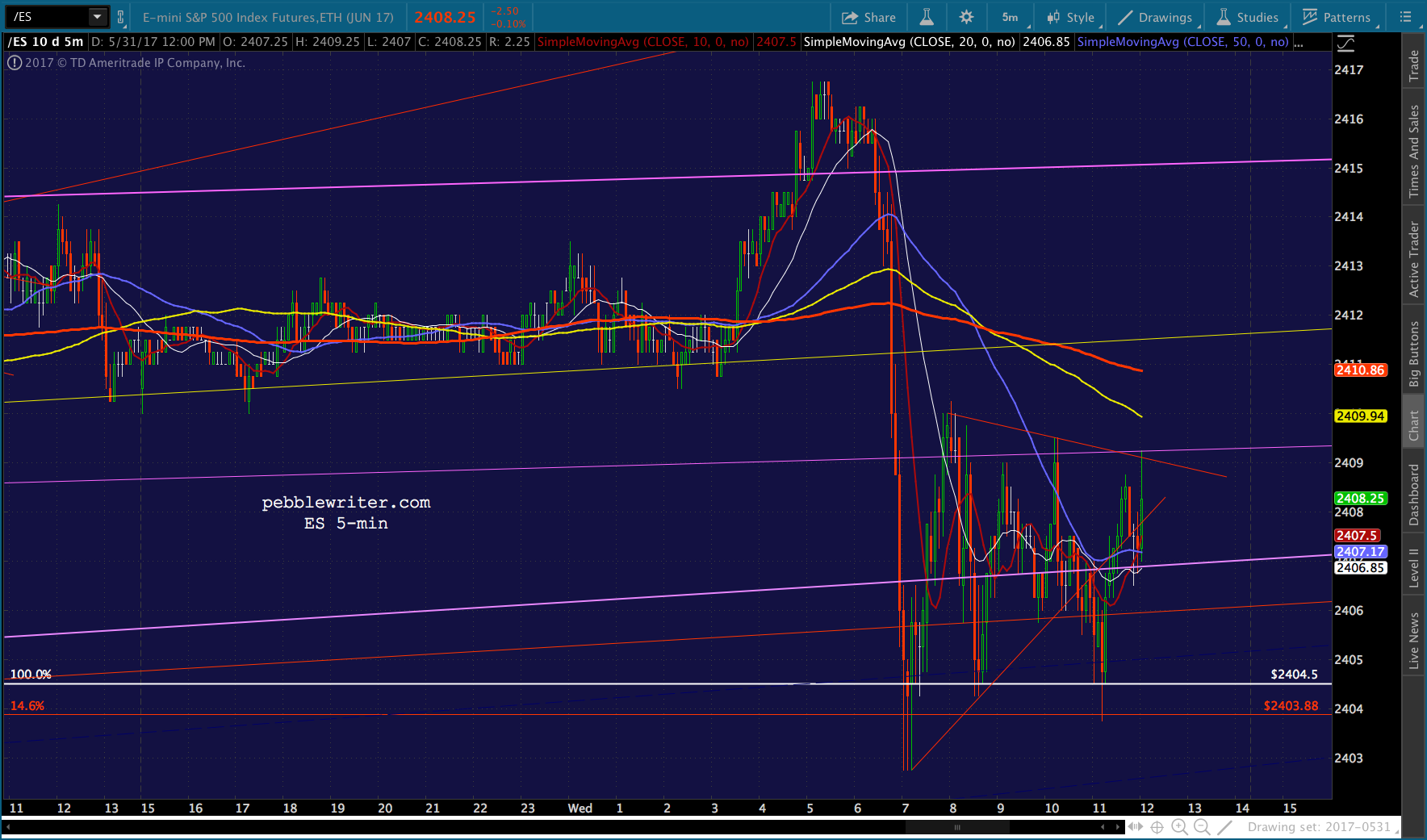

SPX just tagged the bottom of the falling white channel, so I’d cover here but be prepared to re-short if it decides to try for the SMA10/20 at 2395ish. VIX potentially has further to go, with the white channel intersecting with the yellow channel bottom at 11.26ish.

VIX potentially has further to go, with the white channel intersecting with the yellow channel bottom at 11.26ish. USDJPY has broken down, but might backtest/bounce here in an effort to contain SPX’s decline.

USDJPY has broken down, but might backtest/bounce here in an effort to contain SPX’s decline. Okay, with that bit of drama out of the way, let’s get back to big picture stuff. Look for SPX to erase these losses and return to test the SMA5 200 and yellow channel top around 2413-2414.

Okay, with that bit of drama out of the way, let’s get back to big picture stuff. Look for SPX to erase these losses and return to test the SMA5 200 and yellow channel top around 2413-2414.

If you’d like to know all the details behind the following, please refer back to yesterday’s post on oil. If you just want to know what time it is without having to understand how the watch works, read on.

The view from 30,000 feet:

- we have way too much debt, and it will very likely continue to expand

- higher interest rates would ultimately bankrupt the US as they have Japan

- interest rates must be kept low

- inflation must be kept low

- the primary drivers of inflation, such as oil, must be kept low

- but, w/ current correlations, equities typically decline when oil declines

- and, the USD declines with lower interest rates

- a declining USDJPY means a declining USDJPY

- given current correlations, equities typically decline when USDJPY does

- the only other currently effective algo driver is lower VIX – it’s “victimless”

Given the above, it’s clear that the Fed and other central bankers are effectively boxed in. But, that doesn’t mean they’ll sit on their hands. It simply means they have to be creative in how they manipulate markets.

We’ve seen a lot of this already in the cycling of algo influences: oil gooses stocks while USDJPY resets; then, USDJPY gooses stocks while oil resets; and, finally, VIX gooses stocks when nothing else seems to be working or when CL or USDJPY are unable to respond.

Another tactic we’ve seen more and more of is the simple bashing of VIX. It got down to 9.59 on May 9 — only 17 cents from its pre-2007-2009 crash levels and 25 cents from its all-time lows. Should it go lower? Of course not. Can it go lower? Of course, it can!

More importantly, those controlling it have become quite adept at ramping it up after-hours in order to bash it the following morning. This same game is sometimes played with USDJPY and CL, too (hammered overnight so they can “recover” during the session.

These activities, alone, should be able to continue supporting stocks’ continued rise — even if the data doesn’t. So, what could go wrong?

First, those same algos that support stocks can turn against them when investors/traders get nervous. Oil, for instance, fell below its SMA200 and the falling white channel midline this morning.  This is making it tough for SPX to stage its usual snapback rally.

This is making it tough for SPX to stage its usual snapback rally.  Also, since interest rates have to stay low, the USD and, therefore, USDJPY will find it tougher to rally. It can certainly be propped up as it has been the past several days. But, that costs money — which means bigger CB balance sheets at a time when folks are already focused on them.

Also, since interest rates have to stay low, the USD and, therefore, USDJPY will find it tougher to rally. It can certainly be propped up as it has been the past several days. But, that costs money — which means bigger CB balance sheets at a time when folks are already focused on them. FWIW, it appears as though the SMA200 will finally exceed the May 18 lows (110.232.) So, it’ll be possible to tag it without a lower low (it was 109.717 on the 18th when USDJPY began its breakout.)

FWIW, it appears as though the SMA200 will finally exceed the May 18 lows (110.232.) So, it’ll be possible to tag it without a lower low (it was 109.717 on the 18th when USDJPY began its breakout.)

Where does all this leave us? I suspect that trading equities will continue to be difficult, with frequent overnight gap risk. We should be able to continue to earn an extra 1-2% here and there, which adds up over the course of a month.

But, I think the more interesting opportunities will continue to be in VIX, CL and USDJPY as they take turns trying to support stocks. Their efforts are simply more predictable.

More later.

UPDATE: 1:27 PM

For those playing the bounce in SPX, be aware that it is struggling. A drop below current prices would represent a breakdown. As it now stands, VIX faces its last clean opportunity to tag 11.26.

I’m going to take the rest of the day and catch up on some other charts. Keep an eye on the white channel, and don’t be afraid to ditch the long position if the channel breaks down.

I’m going to take the rest of the day and catch up on some other charts. Keep an eye on the white channel, and don’t be afraid to ditch the long position if the channel breaks down.

GLTA.

UPDATE: 3:03 PM

Hanging in there… Note that VIX reached our upside target, the intersection of the red channel top and yellow channel bottom. This knocked SPX out of its rising white channel, but it barged back in — only to run into the SMA5 100.

Probably not a bad place to call it a day, though a big dump by VIX into the close (10.25ish) could get SPX up to the SMA5 200 (two more points to 2412ish) or back to green at 2412.88. Note that ES has run into TL resistance, and has roughly the same distance up to its own SMA5 200.

With targets…

With targets…

UPDATE: 3:50 PM

UPDATE: 3:50 PM

This ought to do it. Cash for the night unless you can hedge or otherwise deal with the gap risk of a short position overnight.