PPI was expected to tick 0.3% (0.1% core) higher in July. Instead, headline PPI soared 0.6% and core popped a stunning 0.5% – the highest since October 2018.

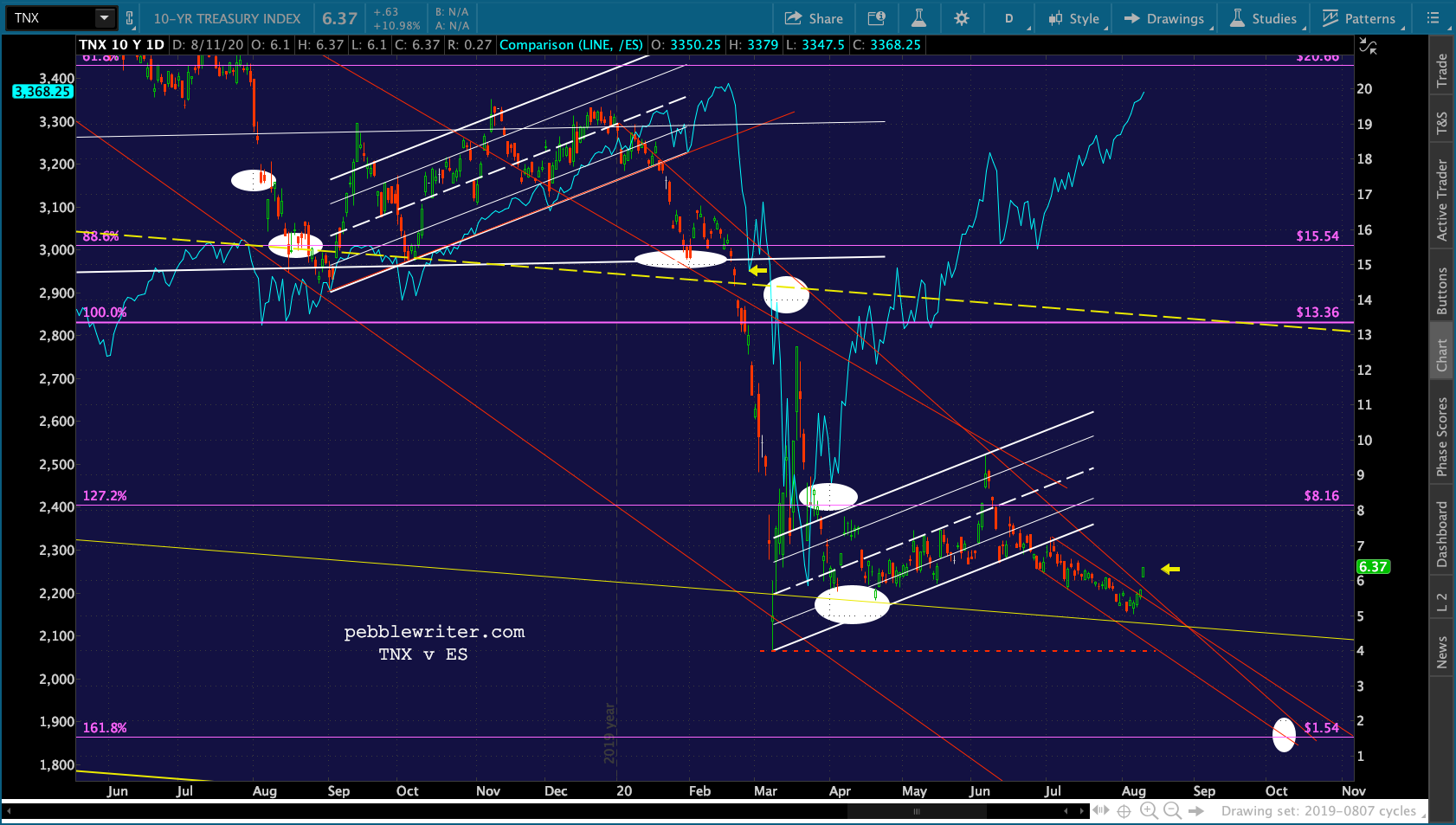

The impact on stocks has been muted so far, as the market is still giddy over the potential release of what is essentially a Phase 1 vaccine out of Russia. The impact on bonds, however, has been significant. 10Y yields have broken out of a long, slow decline.

The impact on stocks has been muted so far, as the market is still giddy over the potential release of what is essentially a Phase 1 vaccine out of Russia. The impact on bonds, however, has been significant. 10Y yields have broken out of a long, slow decline.

When you’re piling on debt (with record-setting duration) the way the US is, higher interest rates are not good news.

When you’re piling on debt (with record-setting duration) the way the US is, higher interest rates are not good news.

continued for members…

The bigger picture shows ZN is backtesting its white channel .786 line. …while TNX has clearly broken trend.

…while TNX has clearly broken trend.

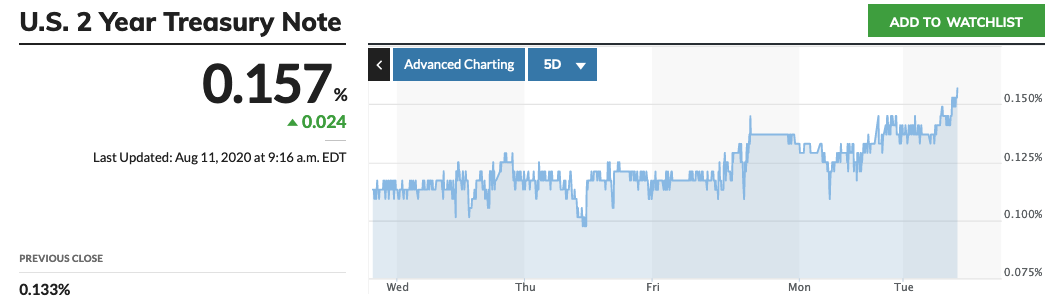

This resulted in a pop in the 2s10s to nearly 49bps. It was at 39 bps just last week. The 2Y has bounced from below 10 bps to above 15.

The 2Y has bounced from below 10 bps to above 15. Suddenly, folks are starting to wonder how CPI might look. Remember, it includes imports, while PPI does not. Imports are more expensive when your currency is plunging as the USD is.

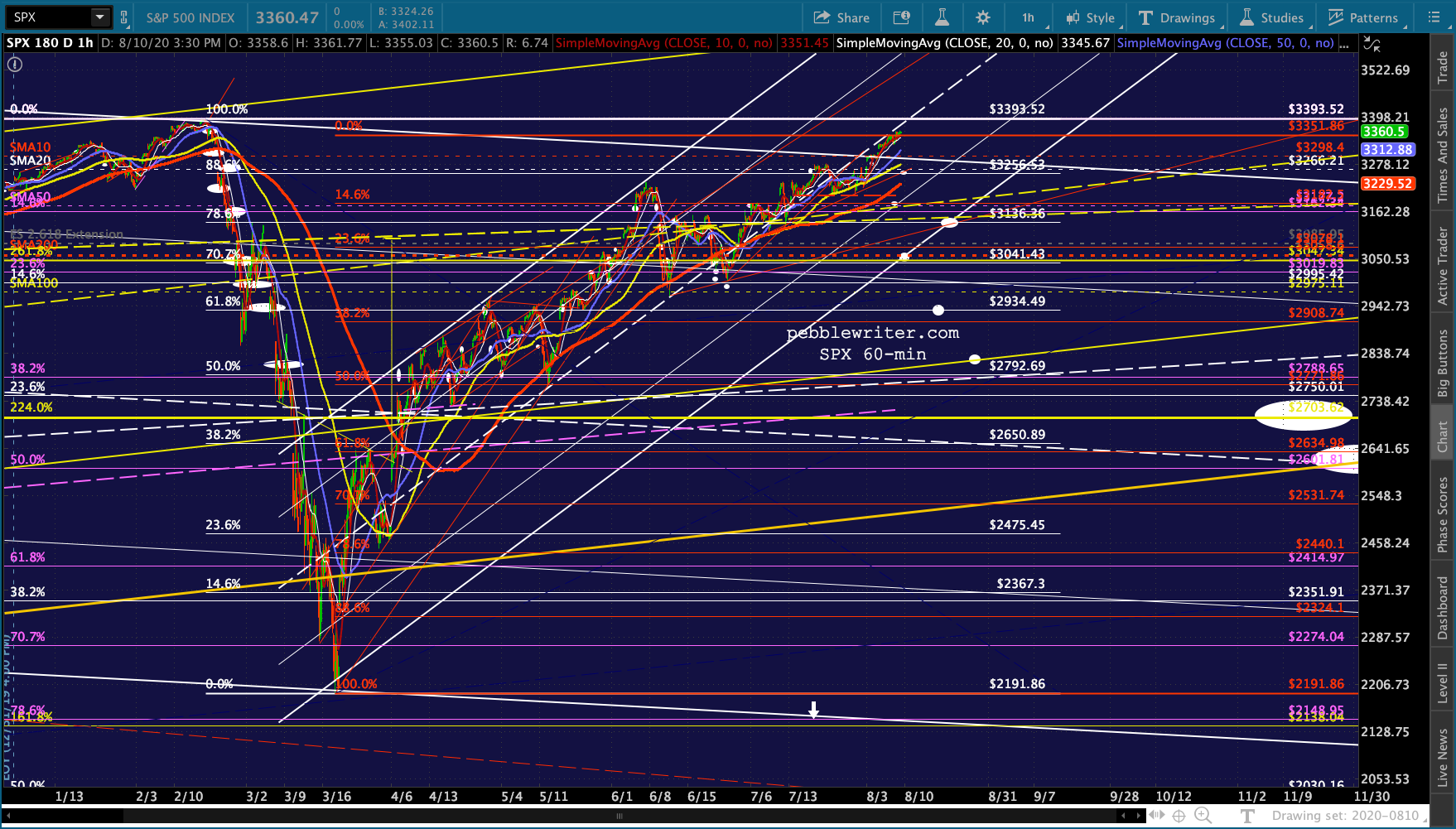

Suddenly, folks are starting to wonder how CPI might look. Remember, it includes imports, while PPI does not. Imports are more expensive when your currency is plunging as the USD is. The move has unnerved futures, which have given up some of their earlier gains.

The move has unnerved futures, which have given up some of their earlier gains.

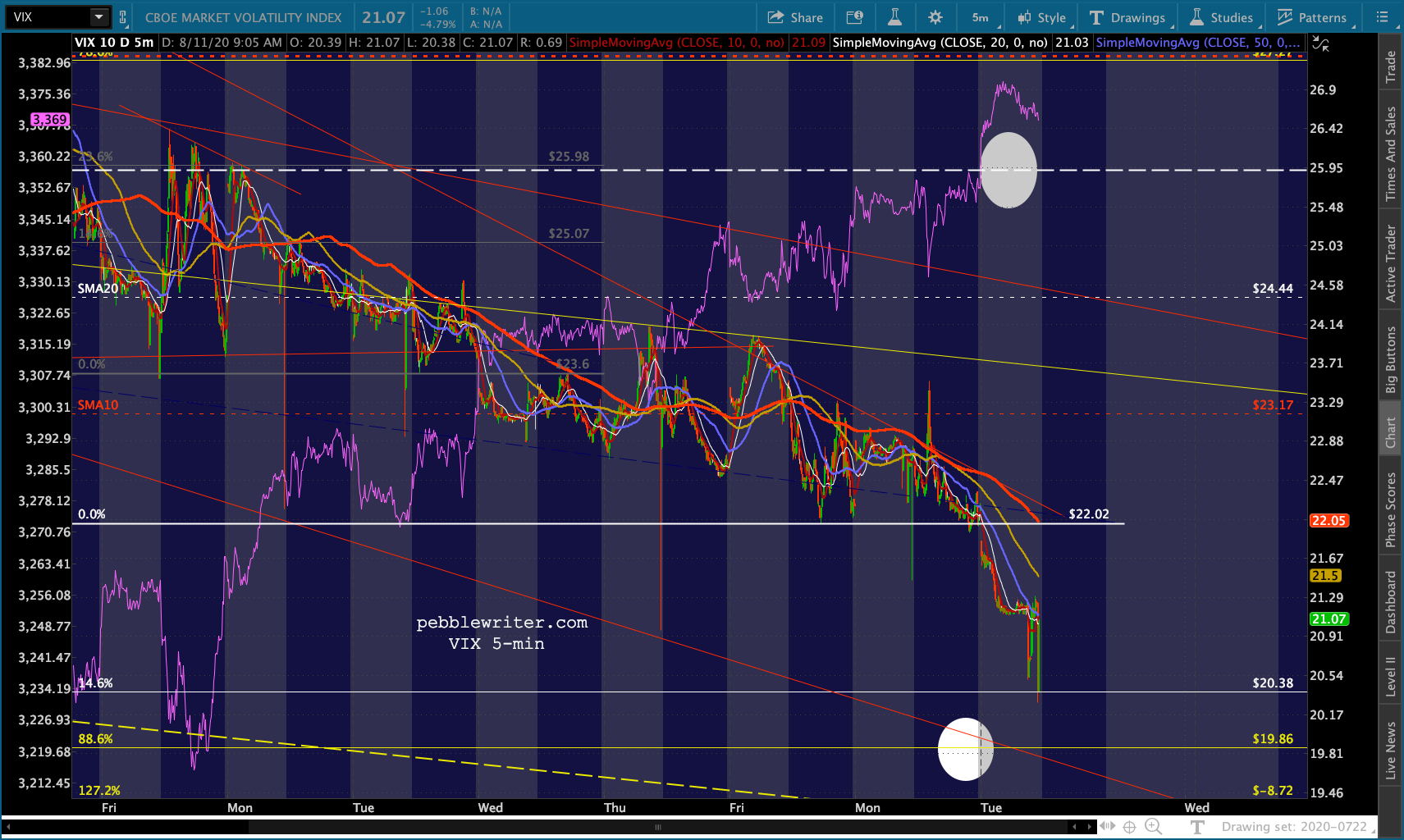

VIX was seemingly on its way to the .886 at 19.86 when the news hit.

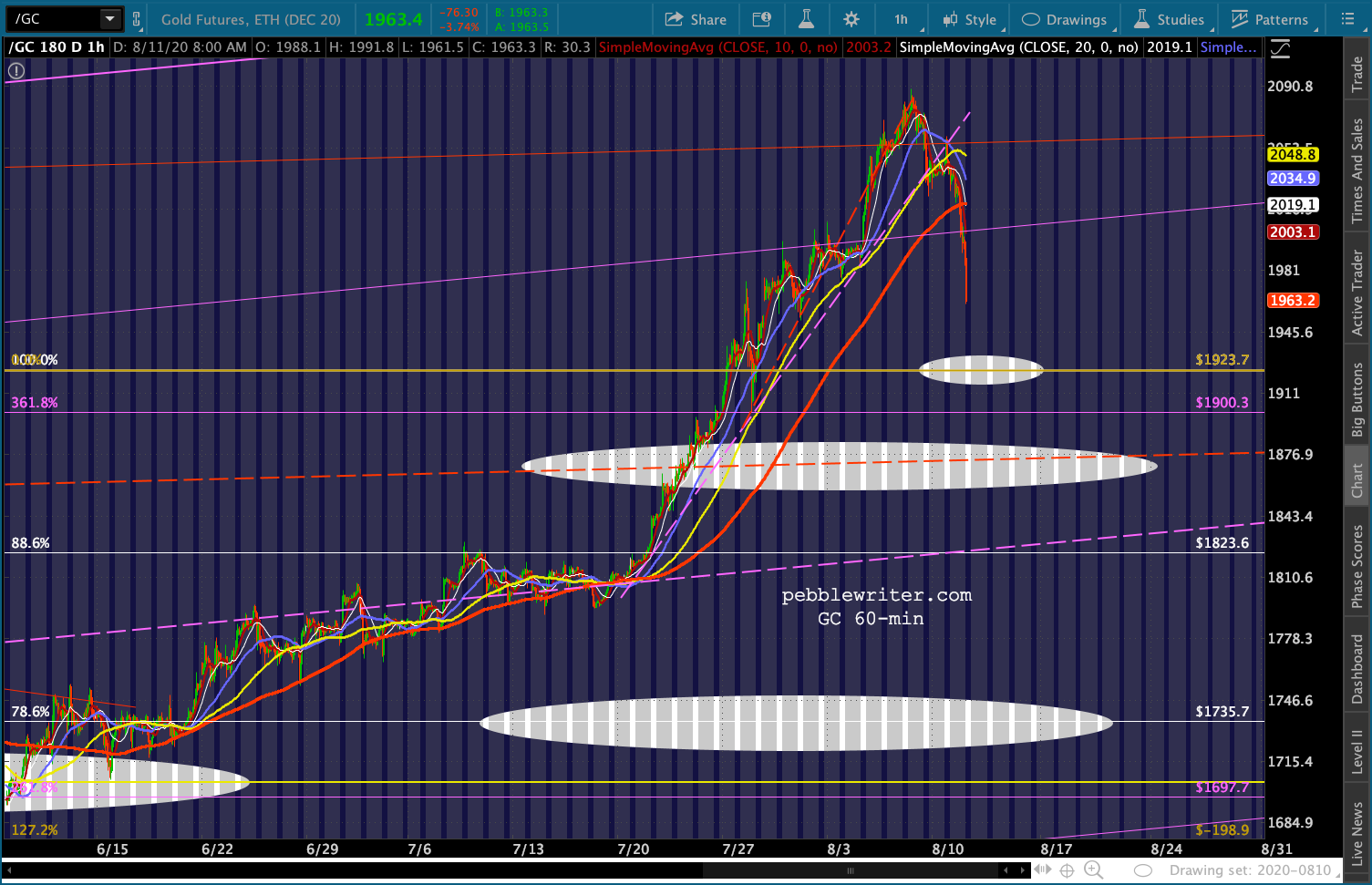

VIX was seemingly on its way to the .886 at 19.86 when the news hit. Gold, which broke below the latest trend line of support yesterday…

Gold, which broke below the latest trend line of support yesterday… …is tumbling. The 1923 backtest we’ve been expecting is looking pretty likely. Note that the SMA20 just broke above the former high.

…is tumbling. The 1923 backtest we’ve been expecting is looking pretty likely. Note that the SMA20 just broke above the former high. Silver is also backtesting – in this case the channel midline it ignored on the way up.

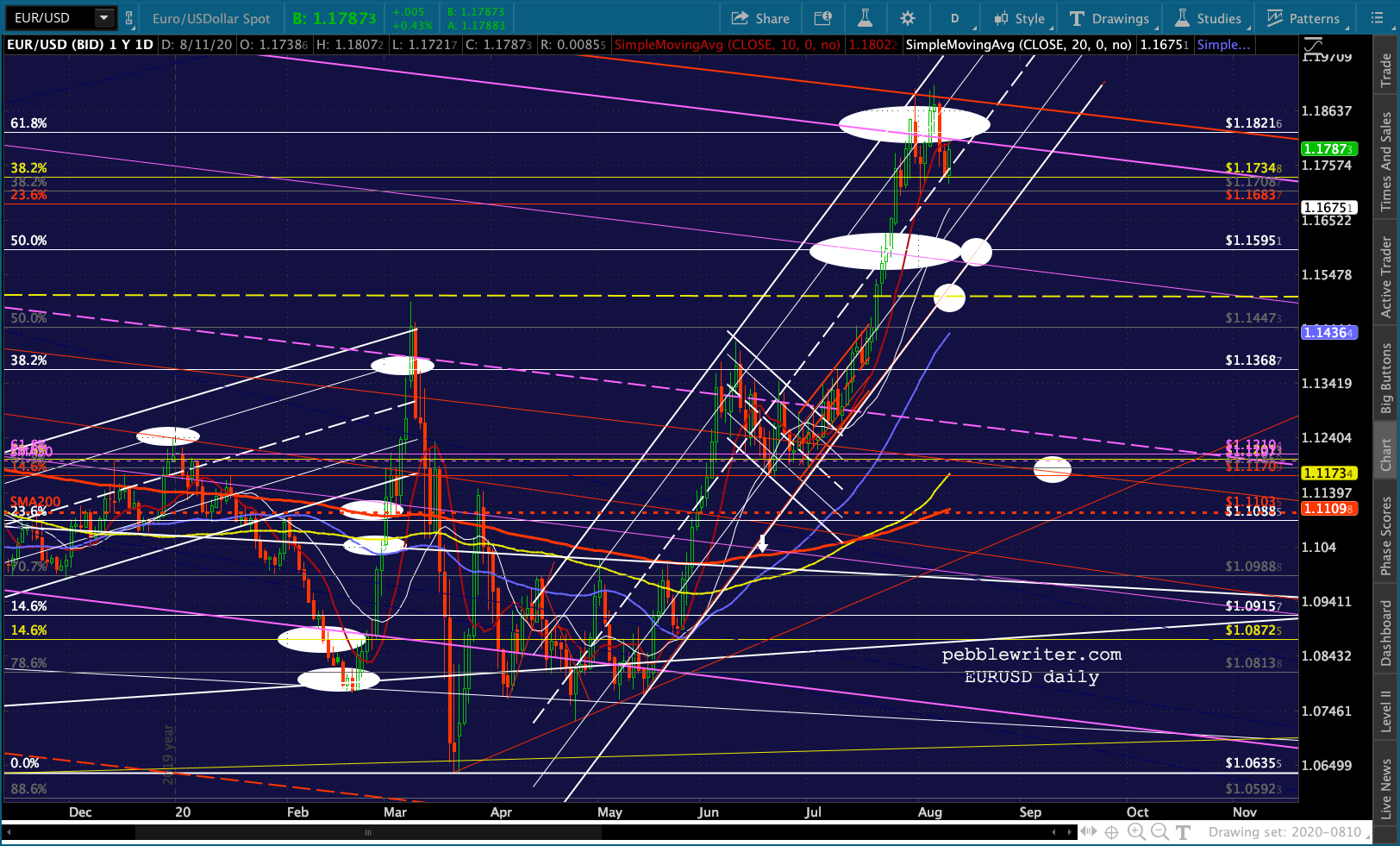

Silver is also backtesting – in this case the channel midline it ignored on the way up. Elsewhere in the currency world, EURUSD is getting a slight bounce…

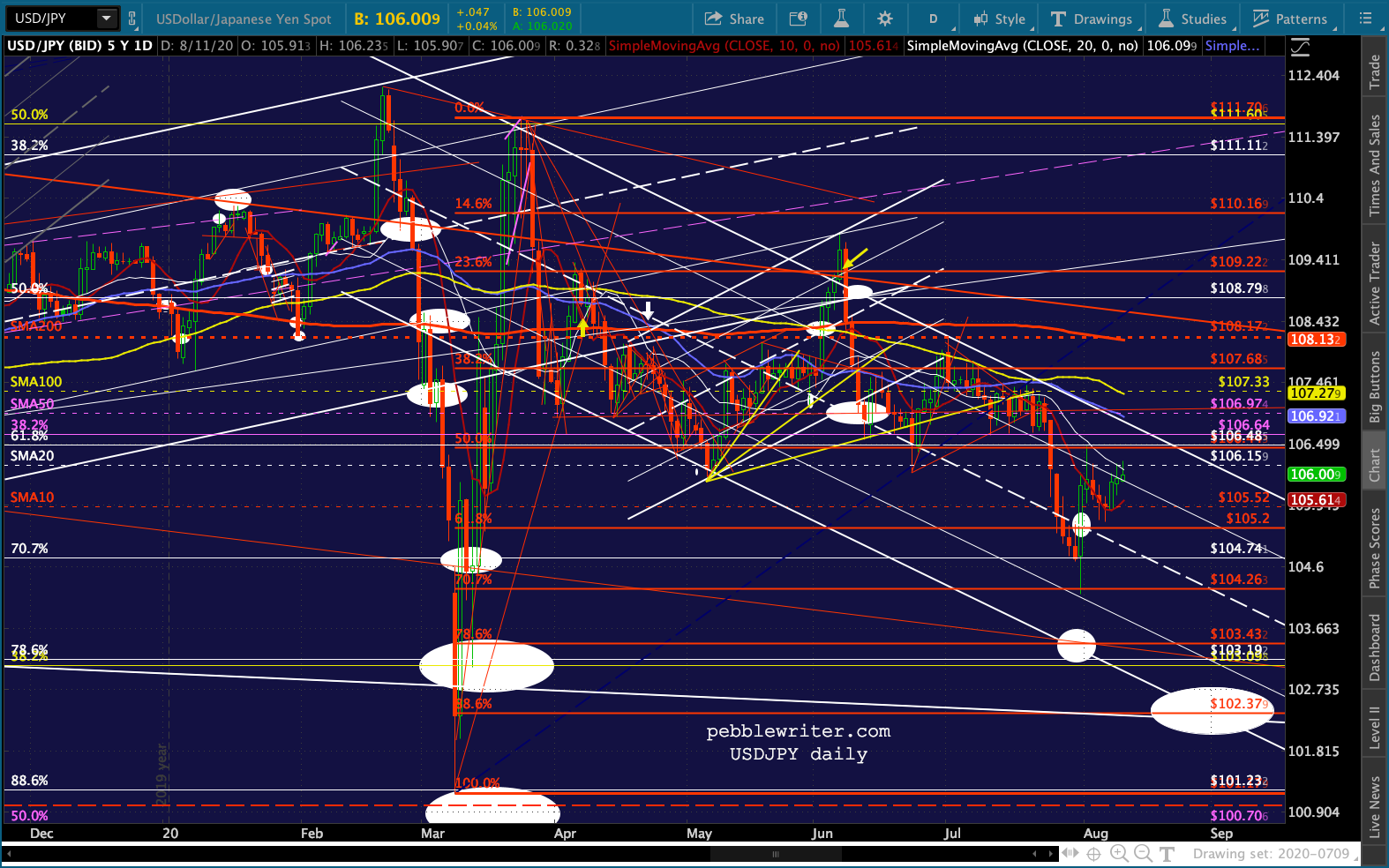

Elsewhere in the currency world, EURUSD is getting a slight bounce…  while USDJPY is pushing up through a channel line.

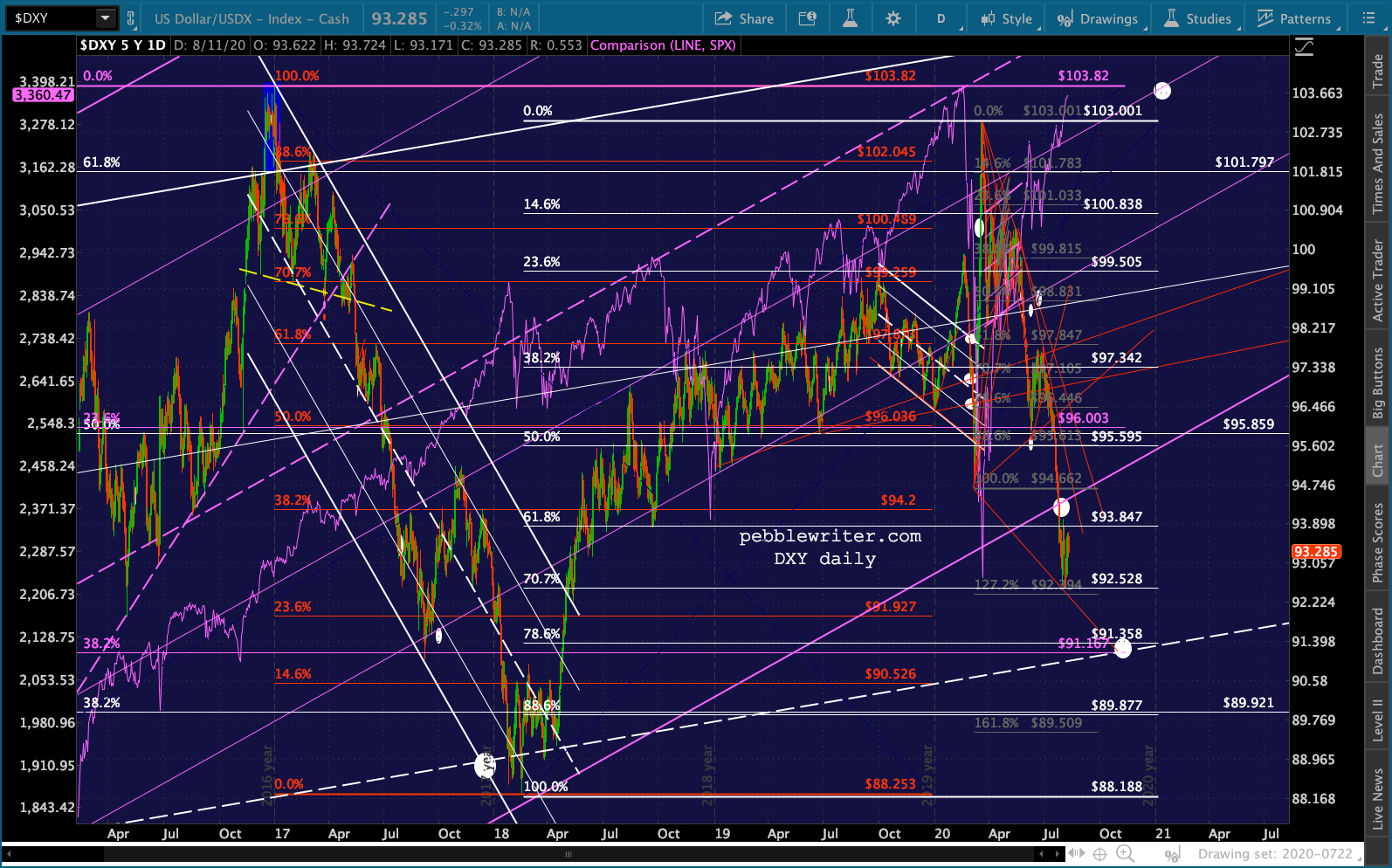

while USDJPY is pushing up through a channel line.  The net result in DXY is roughly neutral – which makes GC’s move all the more interesting.

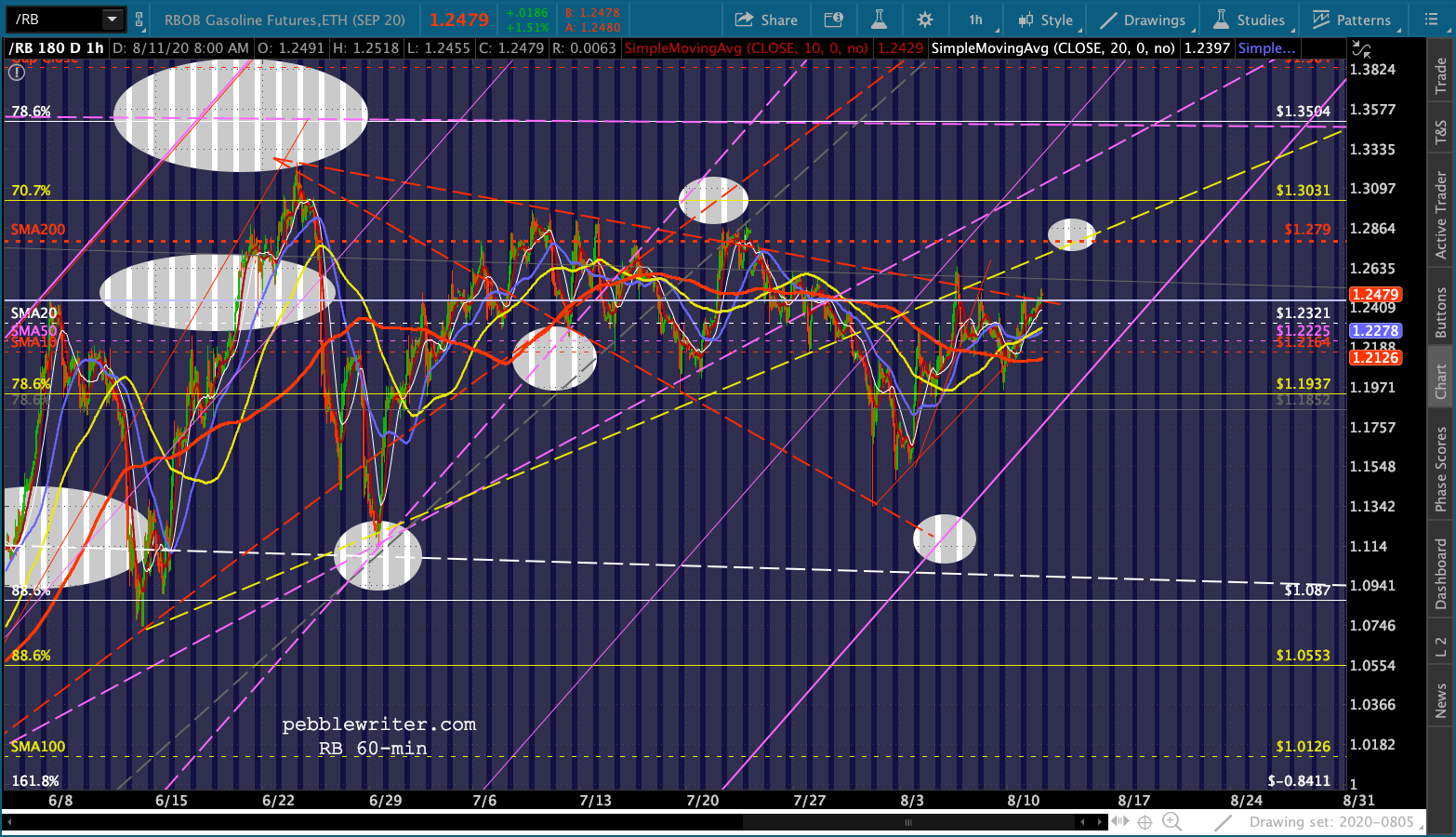

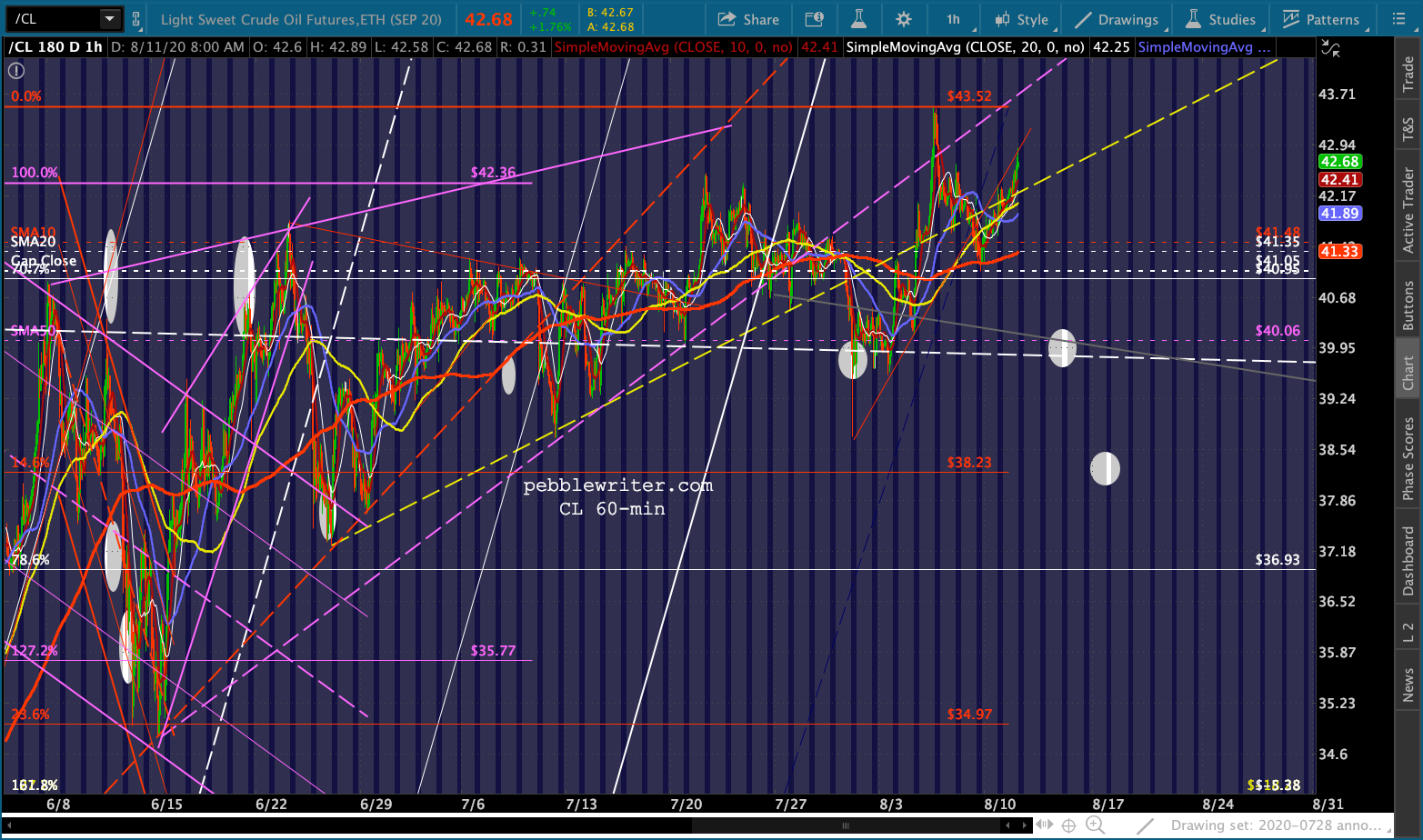

The net result in DXY is roughly neutral – which makes GC’s move all the more interesting.  Oil and gas are making noises about breakouts, but I’m not convinced that they will last. RB has the better chance from a charting standpoint. It has yet to actually tag its falling SMA200.

Oil and gas are making noises about breakouts, but I’m not convinced that they will last. RB has the better chance from a charting standpoint. It has yet to actually tag its falling SMA200.

Meanwhile, AMZN continues to languish…which got me to thinking about COMP. Update coming shortly.

Meanwhile, AMZN continues to languish…which got me to thinking about COMP. Update coming shortly.