Many seasoned investors are surprised to see how positively correlated stock returns have been to oil prices. Energy stocks make up 8% of the overall market, so you’d expect them to have some influence. But, thanks to the increasing prominence of algorithms and quantitative trading, the impact has grown well beyond what 8% should contribute – with most of the market’s significant highs and lows perfectly aligned with oil’s over the years. A 2017 study by JP Morgan estimated that only 10% of trading volume is by discretionary investors who focus on fundamentals. This means that 90% of all volume is driven by passive and quantitative techniques including everything from index funds and ETFs to high-frequency trading and corporate buybacks.

A 2017 study by JP Morgan estimated that only 10% of trading volume is by discretionary investors who focus on fundamentals. This means that 90% of all volume is driven by passive and quantitative techniques including everything from index funds and ETFs to high-frequency trading and corporate buybacks.

The tail that wags the quantitative dog is algorithmic trading, where hundreds or even thousands of factors are constantly monitored and provide instant input for trading decisions. While these factors include big picture economic data such as interest rates, inflation or employment figures, the Big Three that consistently drive big moves on a daily basis are VIX, the USDJPY and the price of oil – specifically WTI futures [CL.]

Oil is the only one of the Big Three which has an almost immediate and substantial impact on the US economy. So, when prices are manipulated higher or lower, we see a change in inflation data, interest rates and, of course, stock prices.

This is why we were able to call the top on October 3, 2018:

CL and RB…not only reached overhead resistance by our measure, but must deal with inflation that’s too high, bearish API data, another round of Trump tweeting, and a large build in EIA inventory. I think the time has finally come to revert to short…

CPI had recently reached almost 3%, dragging interest rates higher as well. The 10-YR reached 3.25% on Oct 5, threatening to break out of a channel dating back over 20 years at a time when debt was exploding higher.

Trump had been jawboning and tweeting his desire for lower oil prices. But, his entreaties had fallen on deaf ears until Oct 3, when journalist Jamal Khashoggi was brutally murdered and dismembered by agents of Saudi Arabia for criticizing Saudi Crown Prince Mohammad Bin Salman (MBS.)

Trump had been jawboning and tweeting his desire for lower oil prices. But, his entreaties had fallen on deaf ears until Oct 3, when journalist Jamal Khashoggi was brutally murdered and dismembered by agents of Saudi Arabia for criticizing Saudi Crown Prince Mohammad Bin Salman (MBS.)

As details emerged and MBS’ complicity became evident, Saudi Arabia suddenly needed friends in high places. Trump was happy to oblige, but had one condition: oil prices needed to decline immediately – which they did. CL plunged 45% over the next 11 weeks. The YoY drop in oil and gas prices was immediately reflected in inflation. CPI dropped from 2.52% in October to 2.18% in November and a low of 1.52% by February 2019.

The YoY drop in oil and gas prices was immediately reflected in inflation. CPI dropped from 2.52% in October to 2.18% in November and a low of 1.52% by February 2019.

The 10-YR dropped from 3.25% in October 2018 to 2.36% by March 2019. Prices at the pump plunged as well, and Americans rejoiced at more affordable commuting costs.

The 10-YR dropped from 3.25% in October 2018 to 2.36% by March 2019. Prices at the pump plunged as well, and Americans rejoiced at more affordable commuting costs.

Remember, oil is one of the Big Three drivers of stock prices. So stocks plunged as well – shedding about 20% by December, when Treasury Secretary Mnuchin convened the Plunge Protection Team to prop up the market – enabling stocks to reach new highs while CL merely enjoyed an extended bounce.

Remember, oil is one of the Big Three drivers of stock prices. So stocks plunged as well – shedding about 20% by December, when Treasury Secretary Mnuchin convened the Plunge Protection Team to prop up the market – enabling stocks to reach new highs while CL merely enjoyed an extended bounce. Saudi Arabia needed the bounce every bit as much as did stocks. The troubled Aramco share offering had been delayed time and again, and higher oil prices made a larger raise possible. The plunge resumed within a few weeks of the IPO.

Saudi Arabia needed the bounce every bit as much as did stocks. The troubled Aramco share offering had been delayed time and again, and higher oil prices made a larger raise possible. The plunge resumed within a few weeks of the IPO. Then came the slowdown. Demand had already been ebbing and prices had been settling lower for weeks. But, after a very brief bounce, oil prices plunged when COVID-19 came onto the scene. Suddenly, fundamentals mattered again.

Then came the slowdown. Demand had already been ebbing and prices had been settling lower for weeks. But, after a very brief bounce, oil prices plunged when COVID-19 came onto the scene. Suddenly, fundamentals mattered again.

Prices plunged to the bottom of a falling channel from 2008 over 3 years ahead of schedule per the cycle study we first posted in March 2019 [see: Macro Cycles and Regime Shifts.] This added fuel to the fire for stocks, which already had plenty of reason to plunge as global economic activity screeched to a halt. Algos, which might normally have been employed to prop up stocks, were pressuring them lower. At the same time, the USDJPY was falling as the Japanese yen rallied and VIX spiked higher on greatly increased volatility.

This added fuel to the fire for stocks, which already had plenty of reason to plunge as global economic activity screeched to a halt. Algos, which might normally have been employed to prop up stocks, were pressuring them lower. At the same time, the USDJPY was falling as the Japanese yen rallied and VIX spiked higher on greatly increased volatility.

Note that long-term trends in gasoline prices were also in danger of breaking down.

Perhaps more alarming to Team Trump, the Dow had fallen to levels not seen since the 2016 election.

Perhaps more alarming to Team Trump, the Dow had fallen to levels not seen since the 2016 election.  The energy industry is vitally important to the US, with millions of jobs and billions in loans dependent on prices stabilizing. It’s no surprise that the federal government would support it as it has many other industries which have been decimated by the global pandemic. Many majors oppose price supports, perhaps hoping to scoop up highly-leveraged players at a bargain price when they failed.

The energy industry is vitally important to the US, with millions of jobs and billions in loans dependent on prices stabilizing. It’s no surprise that the federal government would support it as it has many other industries which have been decimated by the global pandemic. Many majors oppose price supports, perhaps hoping to scoop up highly-leveraged players at a bargain price when they failed.

However, instead of making low or no-interest loans available to tide the industry over as it has with every other affected industry, Trump has focused on artificially inflating prices — first with a series of Tweets and lately with a threat to impose tariffs on imported oil.

As a result, oil has spiked over 50% higher in a mere 4 sessions…

As a result, oil has spiked over 50% higher in a mere 4 sessions…

…facilitating a 24% bounce in the Dow.

…facilitating a 24% bounce in the Dow.

While some are thrilled with the outcome, there are winners and losers. The biggest losers are those who can least afford it: consumers. Higher oil and gas prices are a regressive tax on those consumers who must still drive (disproportionately those less affluent) or buy heating oil or natural gas to keep their families warm during the waning days of cold weather.

While some are thrilled with the outcome, there are winners and losers. The biggest losers are those who can least afford it: consumers. Higher oil and gas prices are a regressive tax on those consumers who must still drive (disproportionately those less affluent) or buy heating oil or natural gas to keep their families warm during the waning days of cold weather.

It’s important to recognize that Trump’s insistence on higher oil prices might be partly about saving oil industry jobs, but it’s really about saving the stock market which has learned to take its cues from oil prices.

If Trump’s “friend” Mohammad Bin Salman — a “man of the people” — still owes any chits from 2018, oil prices could be well supported going forward. But, of course, it will require the assistance of Trump’s other friend, Vladimir Putin, whose willingness to cut back production involves slightly different priorities.

With COVID-19 deaths in the US topping 10,000, Putin’s response will be important in crafting the next headline-stealing development. But, most studies I’ve seen indicate that supply now exceeds demand by at least 25 million bpd. So, even the 10-15 million cut suggested by Trump would do nothing to erase the massive oversupply but would merely slow the rate at which the excess is building.

Rumor has it that Russia will play ball as long as every other oil producing nation is willing to share the pain – including US shale producers, many of were already on life support before COVID-19 (and expect a decent return on their political donations.)

If I sell you 100 barrels at $30 instead of 200 at $15, have I made any more money? Will I now be able to pay back that overdue loan? Will the market reward my stock? Unfortunately, it only works if the pain is borne by the other guys — which will likely boil down to good, old-fashioned horse trading. Trump’s opening ante is throwing down-and-out Americans under the bus. We’ll see if it’s enough.

continued for members…

My position remains the same: either remain on the sidelines or play any gain above CL 26 and RB .75 with very tight stops. I don’t trust this “breakout” and would rather sit on the nice gains we’ve made over the past 18 months than risk it on a political stunt with uncertain promise in the midst of a pandemic with highly variable outcomes.

* * *

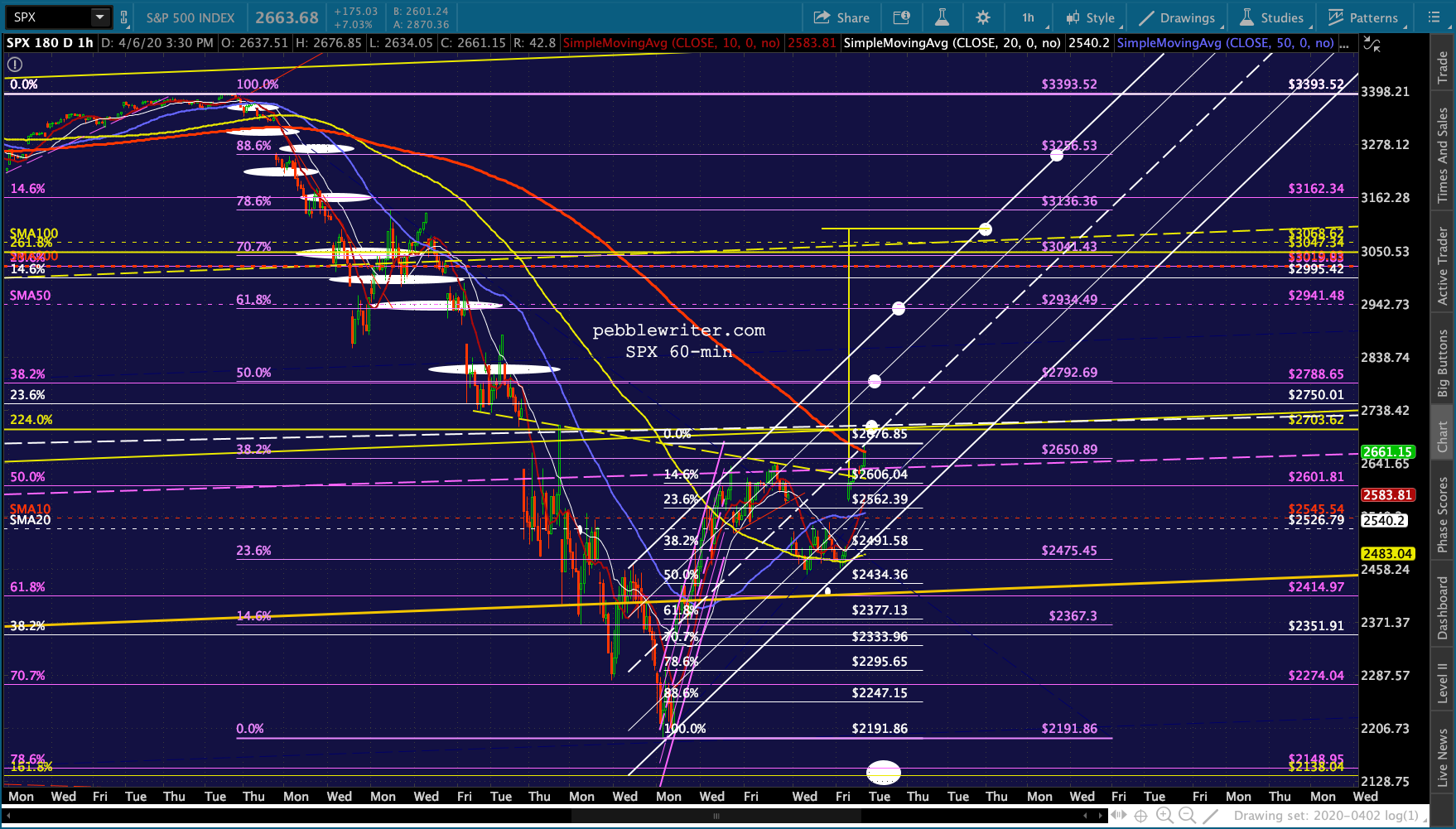

Now, a quick review of equity markets. SPX and ES are both testing (yes, again) the same purple trend line from 2016 that we discussed last week.

First, ES has pushed above that IH&S neckline a third time…but, it has faltered before.

SPX should reach its on or near the open, but must also contend with the red TL from its Feb highs.

SPX should reach its on or near the open, but must also contend with the red TL from its Feb highs.

USDJPY continues to aid stocks, most recently pushing above its SMA100. It remains a huge wild card for stocks, as a breakout could enable the next leg up, while a breakdown would put an end to any further rally.

USDJPY continues to aid stocks, most recently pushing above its SMA100. It remains a huge wild card for stocks, as a breakout could enable the next leg up, while a breakdown would put an end to any further rally.

…which, together with the euro’s continued meltdown…

…which, together with the euro’s continued meltdown…

…has allowed DXY to continue bouncing. And VIX continues to slump lower, most recently dropping through the TL from the Mar 3 lows.

And VIX continues to slump lower, most recently dropping through the TL from the Mar 3 lows.

While the 10Y has been rising…

While the 10Y has been rising…

…the 2Y has held fairly steady.

…the 2Y has held fairly steady.

…allowing the 2s10s to remain below the breakout level at 48 bps.

…allowing the 2s10s to remain below the breakout level at 48 bps.

As we discussed last week, SPX’s SMA10 has crossed above its SMA20 – a bullish cross. By the end of the day, ES will have followed suit. DJIA already has.

As we discussed last week, SPX’s SMA10 has crossed above its SMA20 – a bullish cross. By the end of the day, ES will have followed suit. DJIA already has. It’s impossible to ignore the fact that the DJIA’s bounce has been well-supported for obvious reasons. The bond market has settled down as the Fed has assumed control of the whole shebang. And, oil is presumably well-supported at these levels.

It’s impossible to ignore the fact that the DJIA’s bounce has been well-supported for obvious reasons. The bond market has settled down as the Fed has assumed control of the whole shebang. And, oil is presumably well-supported at these levels.

It would be tempting to go full bullish and sleep soundly. But, as we’ve discussed for the past two weeks, this feels more like an interim bounce and is based on hope and supposition more so than cold hard data – the worst of which is yet to come.

A continuing rally from this point would simply mean that the algos have beat the fundamentals. It has happened many times in the past and might happen again. But, I’d respect the purple TL from the 2016 lows, now at SPX 2635ish.

If SPX breaks above it, then the next significant overhead resistance is the yellow channel bottom at SPX 2712ish — not much of a reward for taking on potentially huge gap risk to the downside. Everybody has their own risk appetite. But, it’s not a bet I’d be excited about making.

For those inclined to follow the Fed’s lead, the safe strategy is to keep your stops reasonably close and to watch out for a drop back through the SMA10 and/or channel bottom. Either one is a signal for traders to sell and for buy-and-hold types to rein in risk.

More later.

UPDATE: 3:55 PM

There goes SPX – right through the old highs. Although it has upside potential at 2712 as mentioned earlier, note that the last time it made a higher high – on Mar 31, it dropped 195 points (7.4%) the very next session.

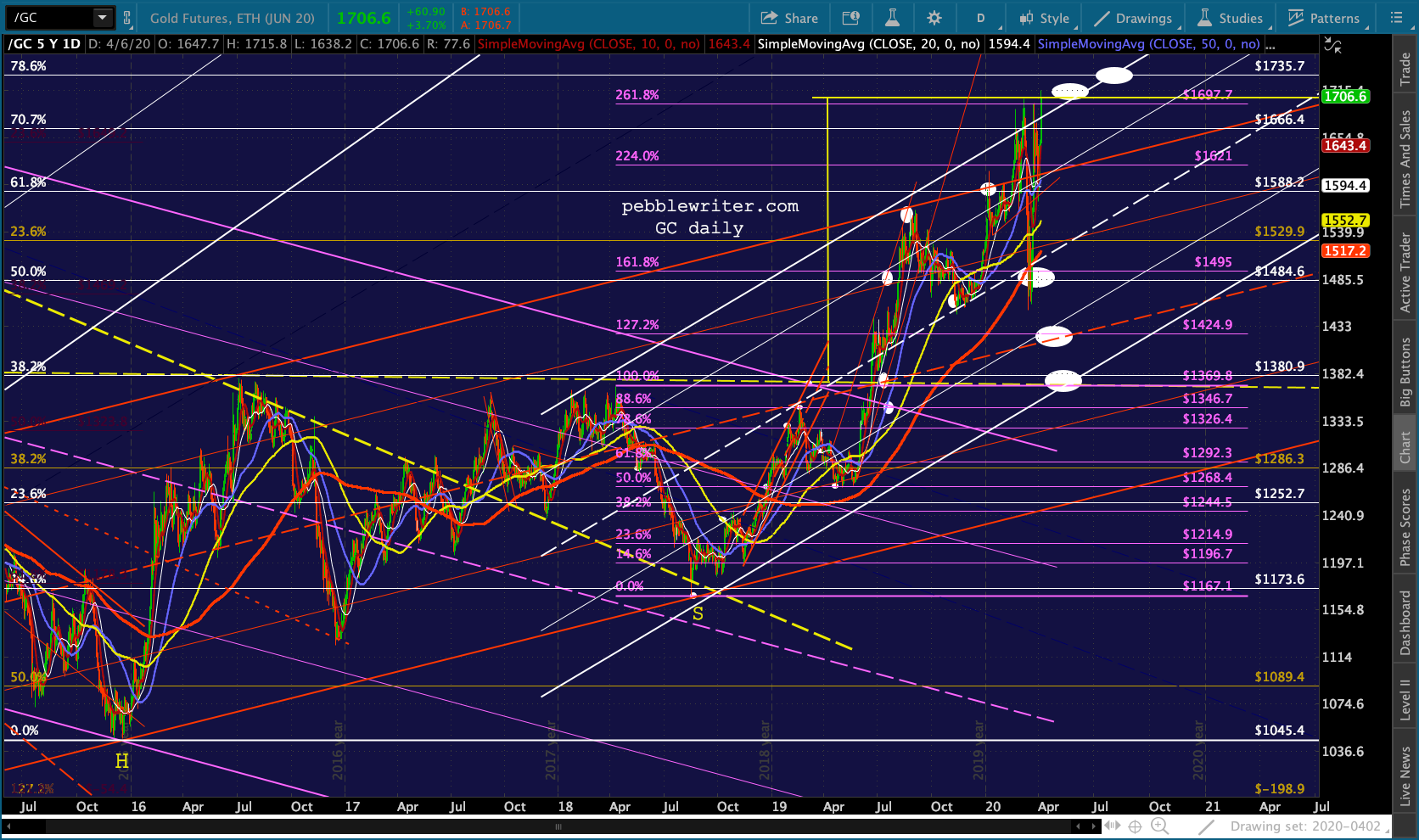

For those who have been waiting for GC to reach its 1708 IH&S target, it did so earlier today. The next upside target is 1735.70 – the .786 Fib of the drop from 1923.70 to 1045.40.

For those who have been waiting for GC to reach its 1708 IH&S target, it did so earlier today. The next upside target is 1735.70 – the .786 Fib of the drop from 1923.70 to 1045.40. UPDATE: 6:30 PM

UPDATE: 6:30 PM

Thanks for member “Reeodd” for pointing out the cup and handle pattern in SPX. In addition, SPX completed its own Inverted H&S Pattern shown below in yellow and targeting 3097.

Coincidentally (or maybe not) this is almost exactly the same level as the yellow trend line connecting the Jan 2018, Oct 2018 and Jul 2019 highs.

Coincidentally (or maybe not) this is almost exactly the same level as the yellow trend line connecting the Jan 2018, Oct 2018 and Jul 2019 highs. ES has a similar setup targeting 3099…

ES has a similar setup targeting 3099… …and its own yellow TL.

…and its own yellow TL.

There are numerous potential upside targets: .500, .618, .786 and .886 Fibs, various moving averages, etc. But, any time we get a meltup of this sort in the face of the worst economic news in 12 (or maybe 90) years and a pandemic that could kill millions – not to mention the most aggressive Fed response ever, we have to take all patterns with a grain of salt.

There are numerous potential upside targets: .500, .618, .786 and .886 Fibs, various moving averages, etc. But, any time we get a meltup of this sort in the face of the worst economic news in 12 (or maybe 90) years and a pandemic that could kill millions – not to mention the most aggressive Fed response ever, we have to take all patterns with a grain of salt.

I believe that at some point the headlines will outweigh the Fed’s and White House’s actions and manipulation and we’ll get a lower low that tests at least SPX 2138. This feels very much like a ramp job that is designed for one purpose only: to get SPX as high as possible before the shit truly hits the fan — which could be tomorrow, 3 weeks from now, or never.

Wouldn’t it be something if a depression, a 30-50% decline in GDP merely produced a brief 35% V-shaped recovery? I wonder if folks would start to believe that markets are manipulated?

GLTA.