For months we’ve been warning about the coming inflation problem, wondering when the bond market would notice and/or care. The immediate problem in a nutshell:

One of the most highly correlated components of CPI with the headline rate is the price of energy, and gasoline in particular. If prices were to remain where they are now, the base effect will result in a 40% increase YoY in April. Historically, this has produced headline CPI in excess of 2.5%. The Fed points out this base effect bump will be transitory and should be ignored, but the recent rise in interest rates tells us that the bond market is not ignoring it. In fact, recent beats in economic data and sharp price increases across the commodity complex underscore the notion that the rise in inflation will not be transitory. The pop we could see in April would be only the beginning.

The Fed points out this base effect bump will be transitory and should be ignored, but the recent rise in interest rates tells us that the bond market is not ignoring it. In fact, recent beats in economic data and sharp price increases across the commodity complex underscore the notion that the rise in inflation will not be transitory. The pop we could see in April would be only the beginning.

As we approach $30 trillion in debt with more stimulus on the way, markets have to wonder what to make of CPI of 2.5-3.0% or higher. In our opinion, the US has no choice but to follow in the BoJ’s and ECB’s footsteps and repudiate higher rates until the end of time.

10Y note futures reached a level at which we have felt would represent critical support. A drop below this level, we reasoned, would sound loud alarm bells. As we wrote yesterday: “This is quite possibly the Fed’s last chance to avoid a real mess in the bond market.”

Bottom line, don’t be fooled by the Fed’s ability to repeatedly bail out equities at the last minute.

Bottom line, don’t be fooled by the Fed’s ability to repeatedly bail out equities at the last minute.

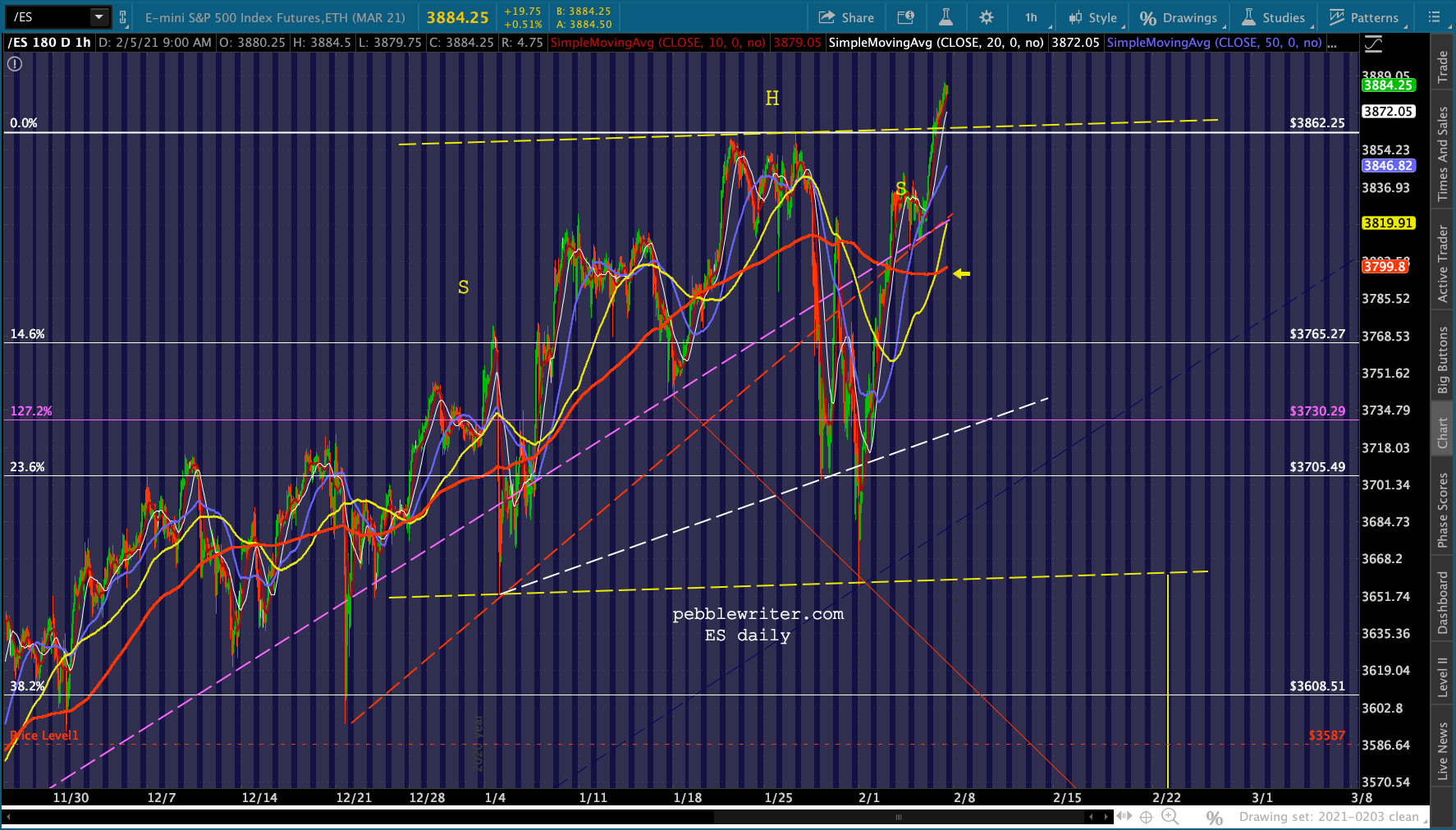

The algos have learned well to respond to moves in VIX, currencies and oil/gas when they are so instructed. It’s no surprise that yesterday’s plunge was arrested at our previous SMA downside target.

The algos have learned well to respond to moves in VIX, currencies and oil/gas when they are so instructed. It’s no surprise that yesterday’s plunge was arrested at our previous SMA downside target.

The problem is bigger and more difficult to cope with than most – including, apparently, the Fed – can imagine.

The problem is bigger and more difficult to cope with than most – including, apparently, the Fed – can imagine.

continued for members…

(more…)

The one we’ve been waiting on for what feels like forever, though, is silver. SI broke out of the falling white channel twice before it managed to tag our 30.35 target in January. But, as we discussed at the time [see: Hi Ho Silver]:

The one we’ve been waiting on for what feels like forever, though, is silver. SI broke out of the falling white channel twice before it managed to tag our 30.35 target in January. But, as we discussed at the time [see: Hi Ho Silver]: We’ll update the prognosis for silver and gold and also sneak in a discussion of EURUSD, which officially reached our next downside target yesterday.

We’ll update the prognosis for silver and gold and also sneak in a discussion of EURUSD, which officially reached our next downside target yesterday.