UPDATE: 6:00 PM

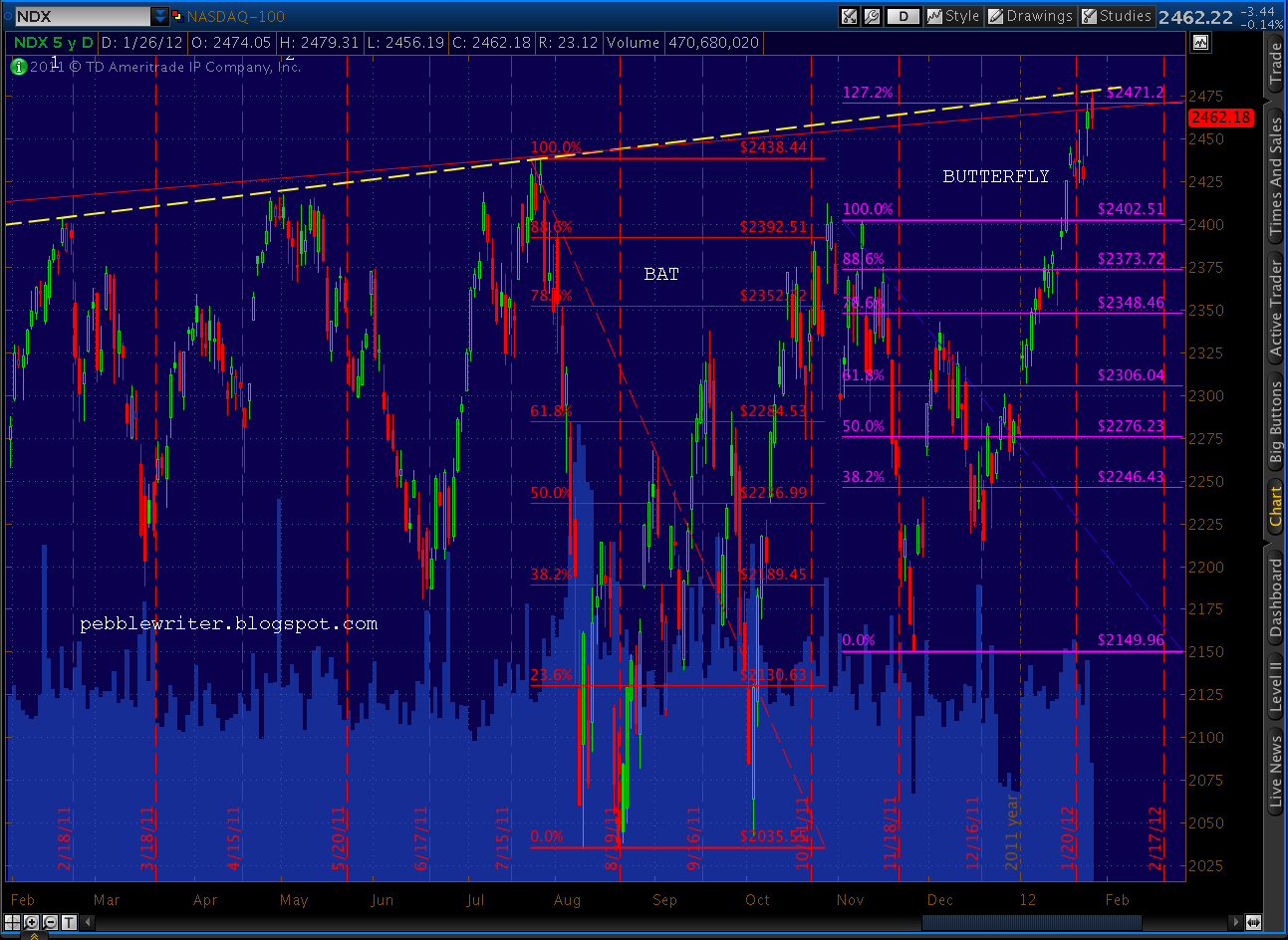

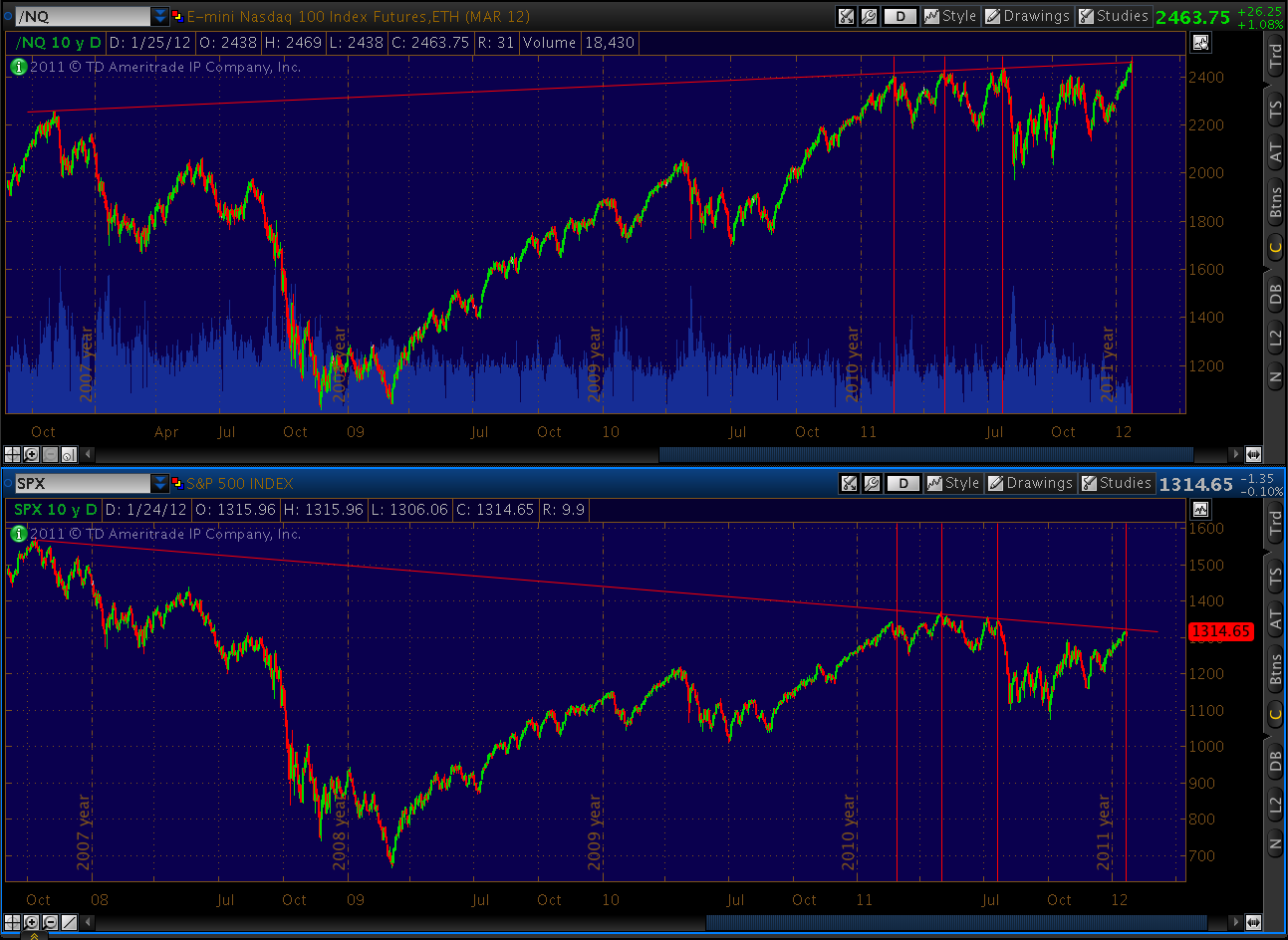

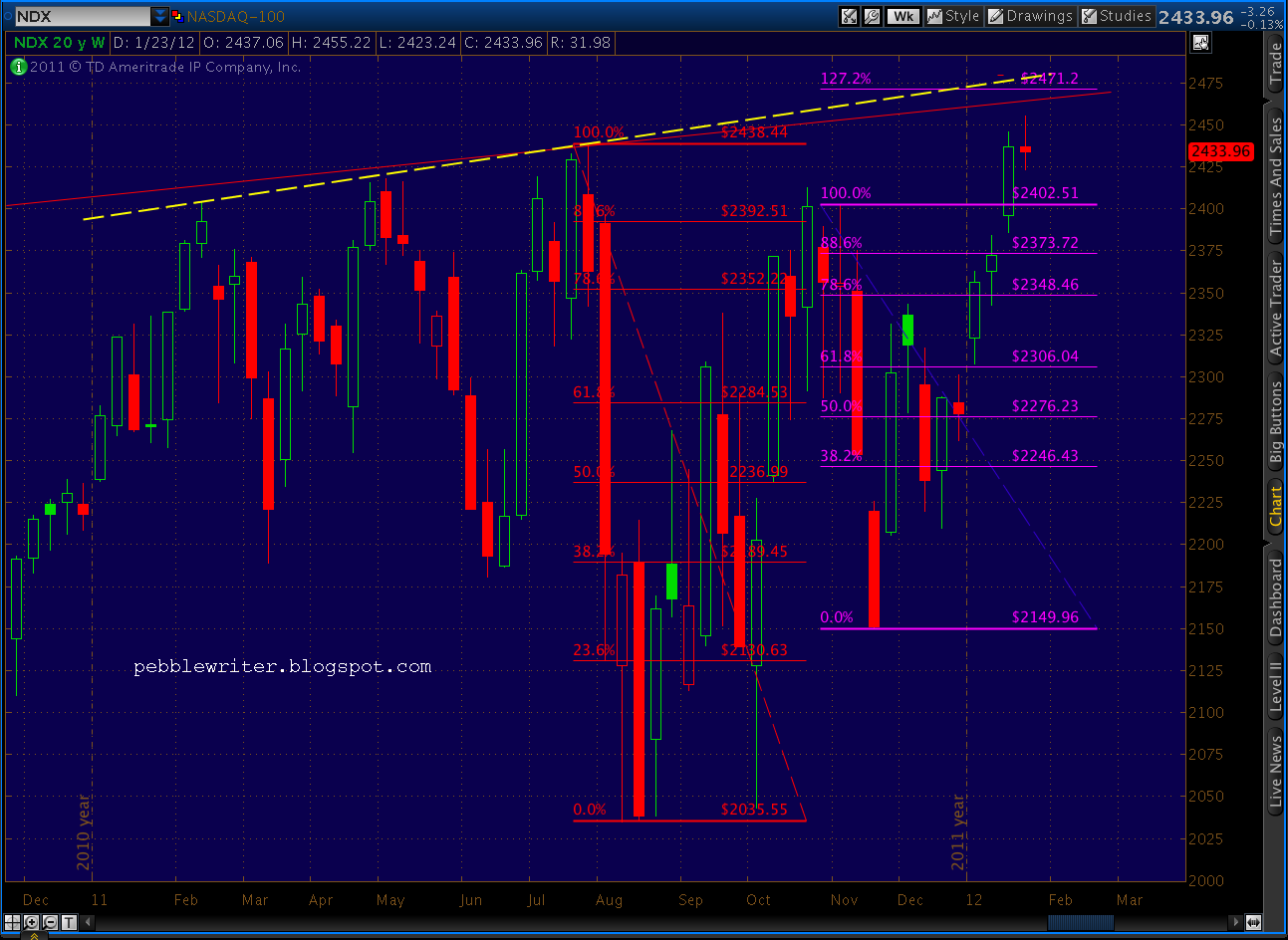

NDX is suggesting an imminent plunge in stocks. I started watching NDX last summer, and found it to be a great confirmation of SPX activity. On July 25, I wrote about it tagging a trend line of previous highs, and how previous tags had led to market corrections [Tale of Two Tops.] A few days later, SPX began an 18% plunge. Here’s the chart from back then:

And, here’s the chart from today, showing us right back at that same trend line — which also happens to be a fan line off the Oct 2007 highs.

There’s a little wiggle room on the precise price level, because the TL connecting all four differs ever so slightly from the fan line. It allows for another 30 points up to 2471, but it’s already close enough that a turn could come at any minute.

What’s significant about 2471? Remember, we had that great reversal off a Bat pattern in October. It then jumped right into another pattern — this time a perfectly shaped Butterfly whose 1.272 extension intersects with the trend line and fan line right at (drum roll please) 2471.

Note also the RSI trend line tag right at 70 — just like the previous tops. All in all, I’d say we’re getting very, very close.

UPDATE: 3:25 PM

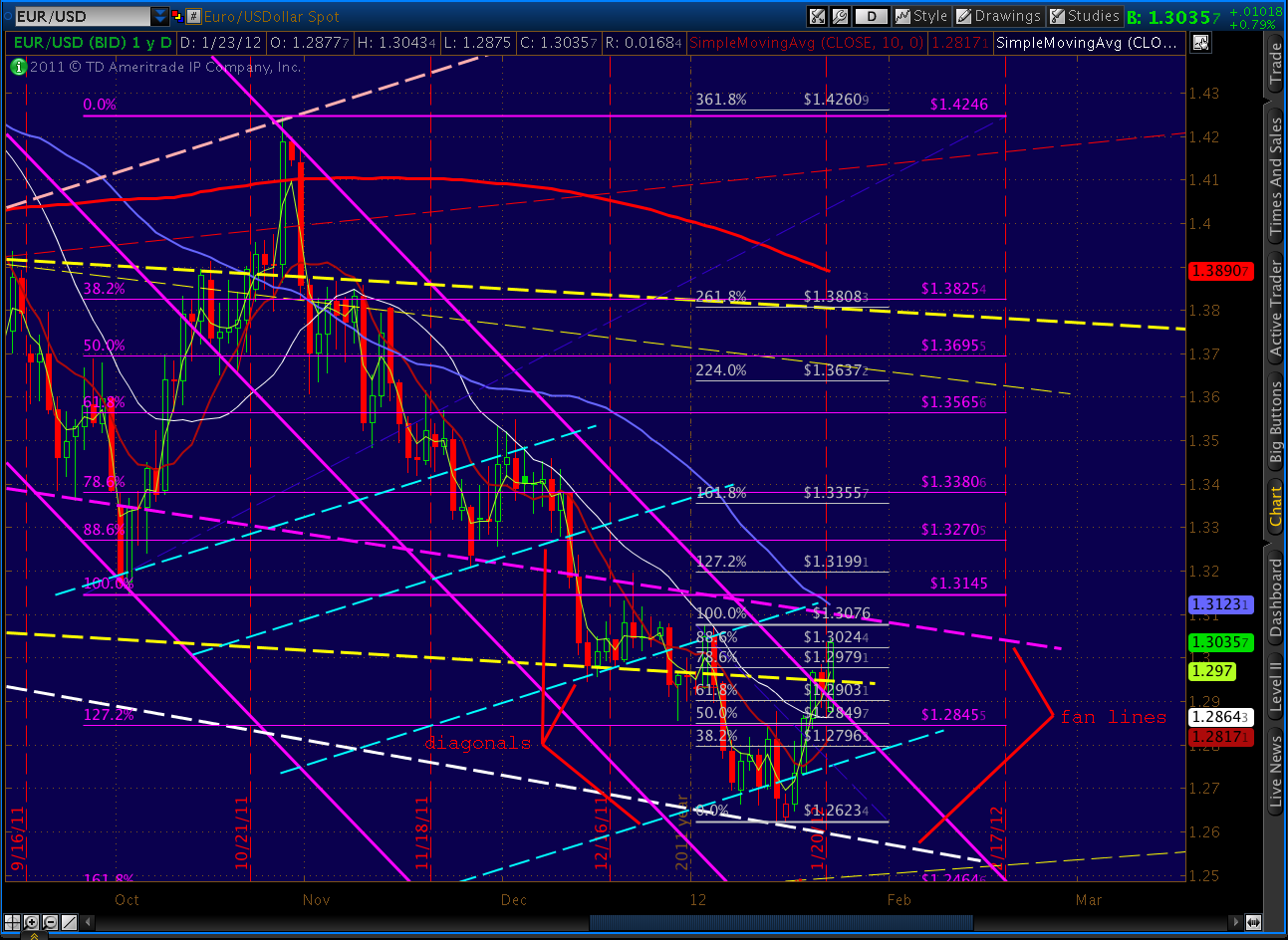

EURUSD has not only tagged the boundary of the channel it’s been following since October, it’s completed a bearish Butterfly at the 1.272 extension. This should be the end of the run (although an overshoot to the 1.618 is always a possibility – use stops!)

A reminder, we’re shooting for at least 1.2464 (Crab pattern), and the slope of this channel line has been proven time and again over the past few years. Note the purple channel lines on the weekly and daily charts below. We’re also backtesting one of our channel lines (yellow, dashed) which have done a nice job of guiding intermediate moves. A decline to 1.2464 from today’s high is a 3.9% drop.

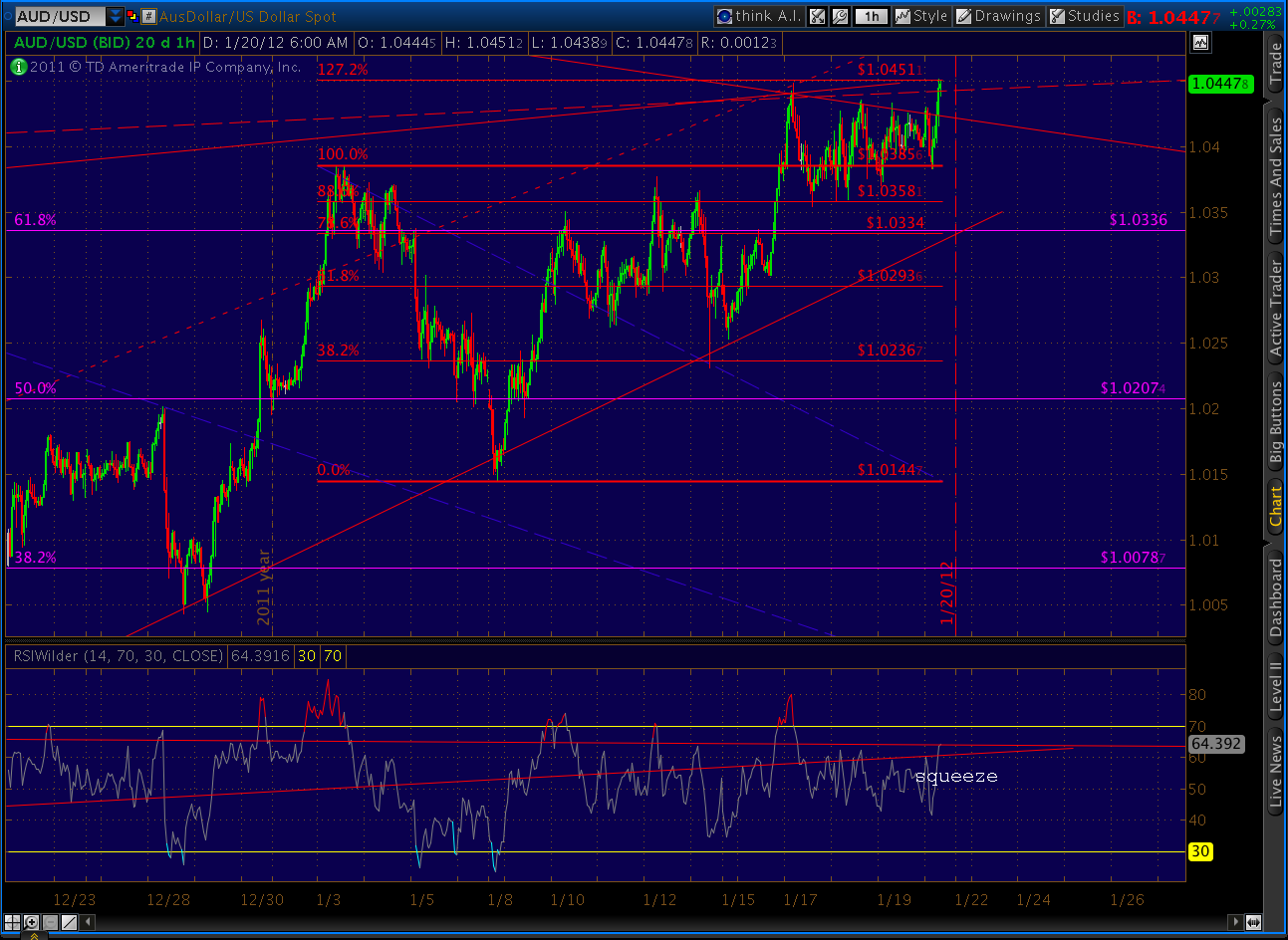

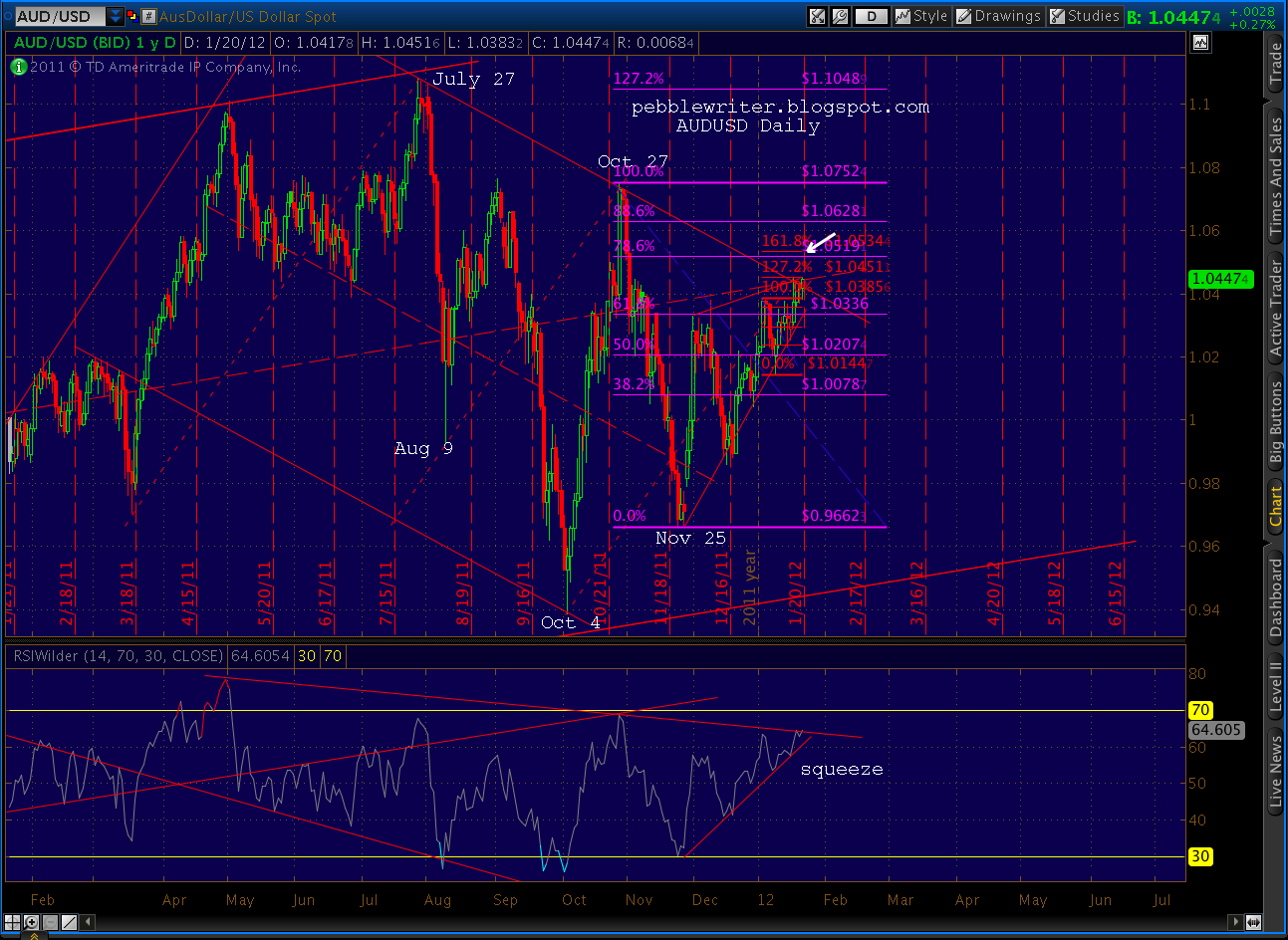

The AUDUSD has tried to push above its channel boundary to complete the Gartley/Crab, but no joy so far. A failure to complete it, along with a firm hold here at the boundary would be extremely bearish for it and for equities in general.

More after the close.

ORIGINAL POST:

First, thanks for all the emails yesterday regarding taking this blog private. I haven’t read all of them yet, but about 80-90% of those I’ve read so far support the idea — particularly if it comes with a steady stream of info on a variety of securities.

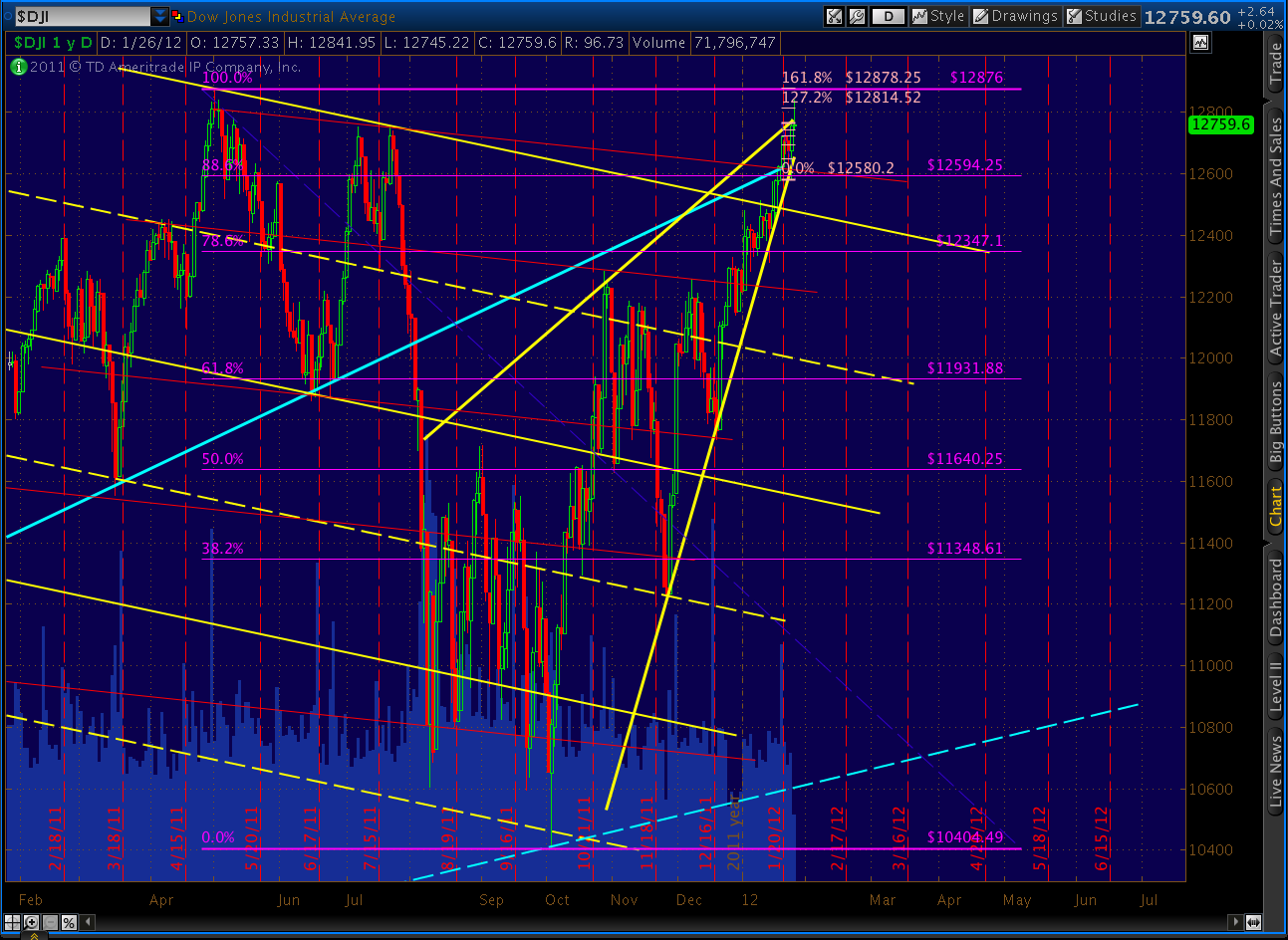

I focus primarily on SPX, but I was thinking (updated daily) charts for SPX, RUT, DJI, NDX, COMP, VIX, EURUSD, DX, GC, SI and maybe a few stocks everyone watches like AAPL. I could run three sets for each: (1) long term — weekly or monthly, (2) medium term – daily, (3) intra-day. I would detail the chart and hamonic patterns I see, and provide a guide to finding and understanding harmonic patterns that many of you have been requesting.

I think the guide could help everyone be more knowledgeable about the patterns, so we could use a shorthand that would allow me to increase the volume of info rather than spending time on prose describing what I see. So, for example:

“rw on SPX, apex @ 1324 intersecting with FL from Oct ’07, May and Jul ’11; .886 of pseudo-Bat (1370-1074) @ 1331.“

instead of:

“With today’s push, the rising wedge has expanded and points to an apex of around 1325. Note that 1325 intersects with a fan line coming off the Oct 07 highs and connecting with the May and July 2011 highs. It’s also with a few points of the Fibonacci .886 (1331) of the distance between the May highs (1370) and the October lows (1074.) Recall that it’s not technically a Bat pattern because our Point C (1074) is lower than Point A (1101 on Aug 9.)“

I’d also like to establish a more robust commenting capability to increase the communication among readers. There are at least 2,000 of you on a daily basis now. But, these emails are the first I’ve heard from most of you, and I’ll bet you have something to say — even if it’s only about how badly I blew a particular call.

And, last, I’d like to set up an email or twitter feed for timely stuff that comes out during the day — maybe my take on a bogus earnings report, a fib target being hit, a trend line broken, etc.

As some of you have pointed out, I announced a few months ago that I’d be scaling back. Well, let’s just say I tried. I really did. But, with another big whoosh on the way, it seemed like bad timing. And, I must admit, I enjoy blogging. I just have to figure out a way to make it more valuable but require less time… and somehow compensate for the tradeoff between spending time with family and being able to support both said family and my charitable giving.

Right now, the information is spread far and wide and is all too often posted on other sites that charge big bucks for my ideas (if the shoe fits, RP…) It’s one thing to give away valuable info, but quite another to provide free product to a “competitor.” It makes more sense to deliver valuable info to those who value it and cut out the middle man.

For those of you who have affordability concerns, rest assured that the cost will be reasonable — about the cost of the commission on a round trip trade on which you stand to make many times the fee. I might even do a special deal of some sort for current followers.

Please let me know what you think. This site is for you and I want it to be something you’re excited about. Again, the address is: pebblescribe at gmail dot com.

*****

Lots of stuff going on today. I’ll post some charts shortly. First, thanks to Dillzs99 for this comment on yesterday’s post. I thought it was important to bring it current for all to see as it raises some good questions:

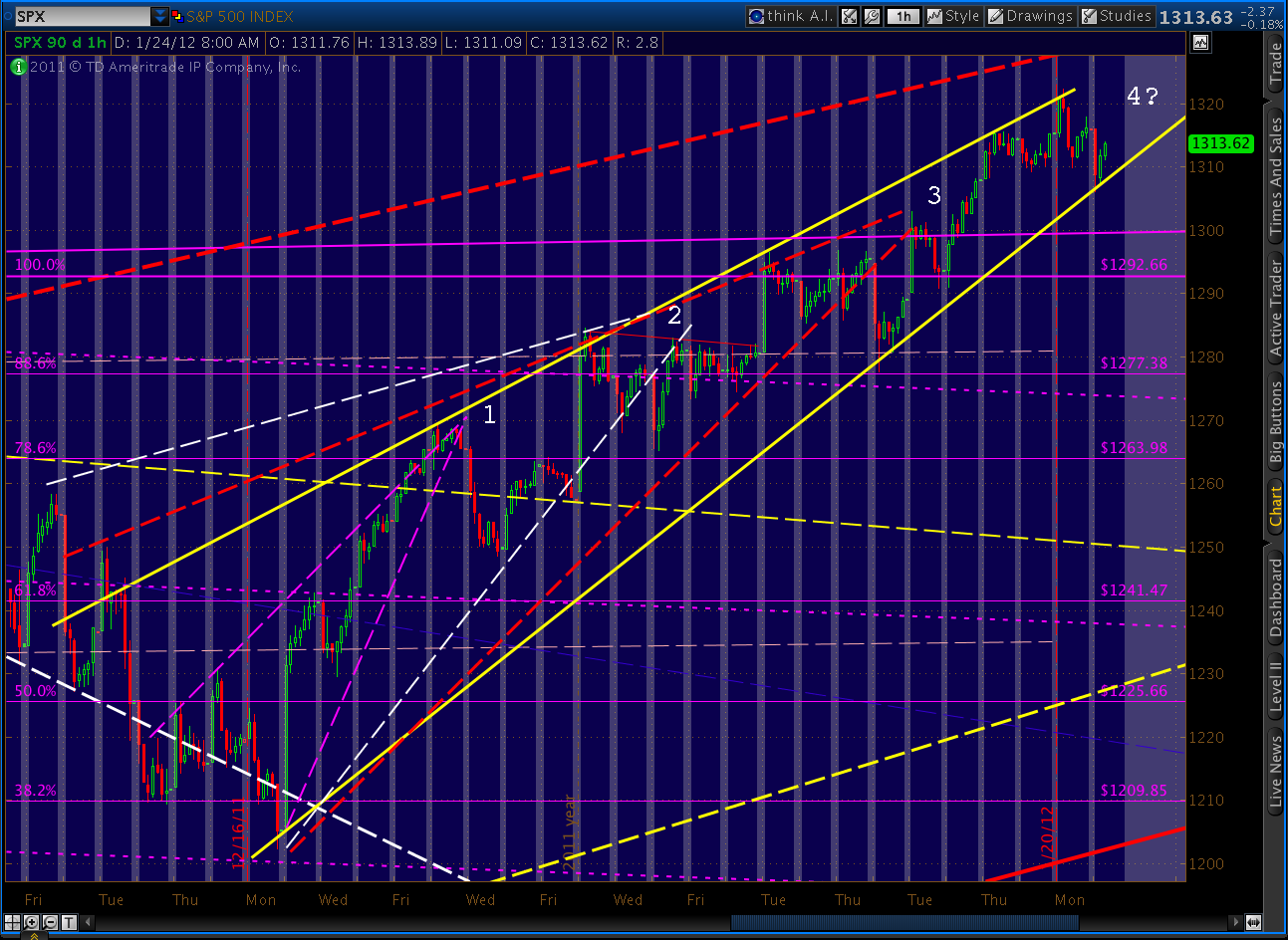

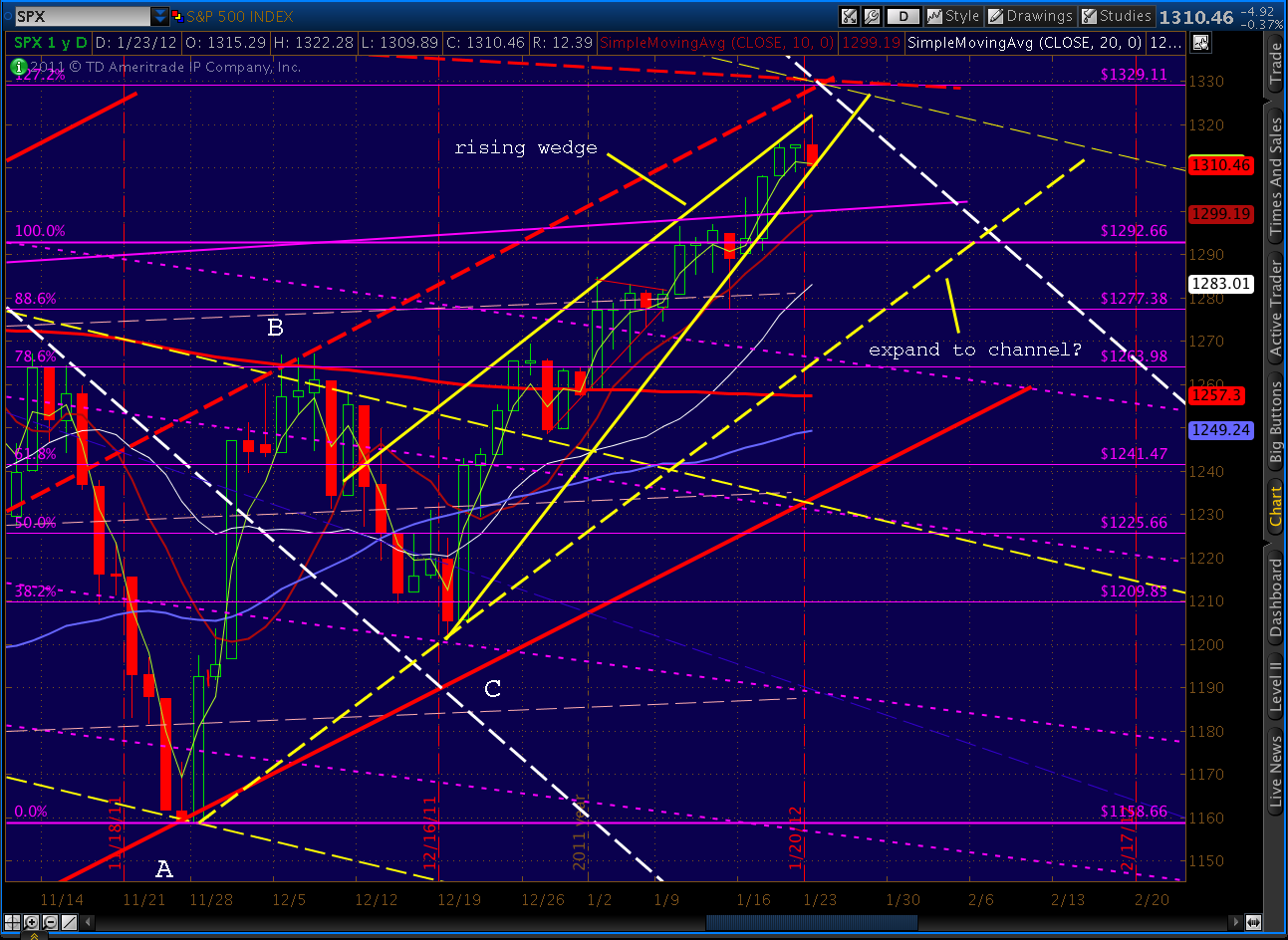

It looks like SPX may be working on completing a bat pattern at 1336. Using X as the May high and A as the October low, you can make a case that B was hit on 10/12 just below the 50 retracement and C @ the 38.2 was hit on the next day 10/13. The target for D in this case is 1336. 1336 also is almost smack on the descending trend line from the 2007 high.

I also have been watching the harmonics on the RSI. It seems as though the daily RSI is in the last leg of a butterfly. X in this case is the 10/28/11 peak and A is the 11/23/11 low.

Additionally, the RSI weekly looks to be finishing a gartley. X in this case is the 2/14/11 peak and A is the 8/8/11 low.

In my opinion, a final push to 1336 would complete the bat pattern, and finalize the harmonics in the daily and weekly RSI. It also would correspond well with the last push up the harmonics are expecting in the AUD/USD (as you noted above).

Here’s a chart of the relevant Fib levels involved in the Bat he’s suggesting:

I agree with 1370 as a Point X. It’s right up top, where we like X’s to be — major turning points. Likewise, Point A is at an important low. My only concern is Points B and C. It’s entirely possible these two are the right ones, but I’m not thrilled with using them because it means ignoring some otherwise more remarkable turns.

If we hadn’t seen C go below A, for instance, we might have something like this. I’d be willing to ignore a point or two and call it a 100% retrace, but not 27.

We could fix the C versus A problem and go with something like this, but then we have a Point B at the .786, which means Butterfly instead of Bat. That would spell an extension to the 1.272 @ 1433 — which I just don’t see in the cards — for a variety of non-harmonic reasons.

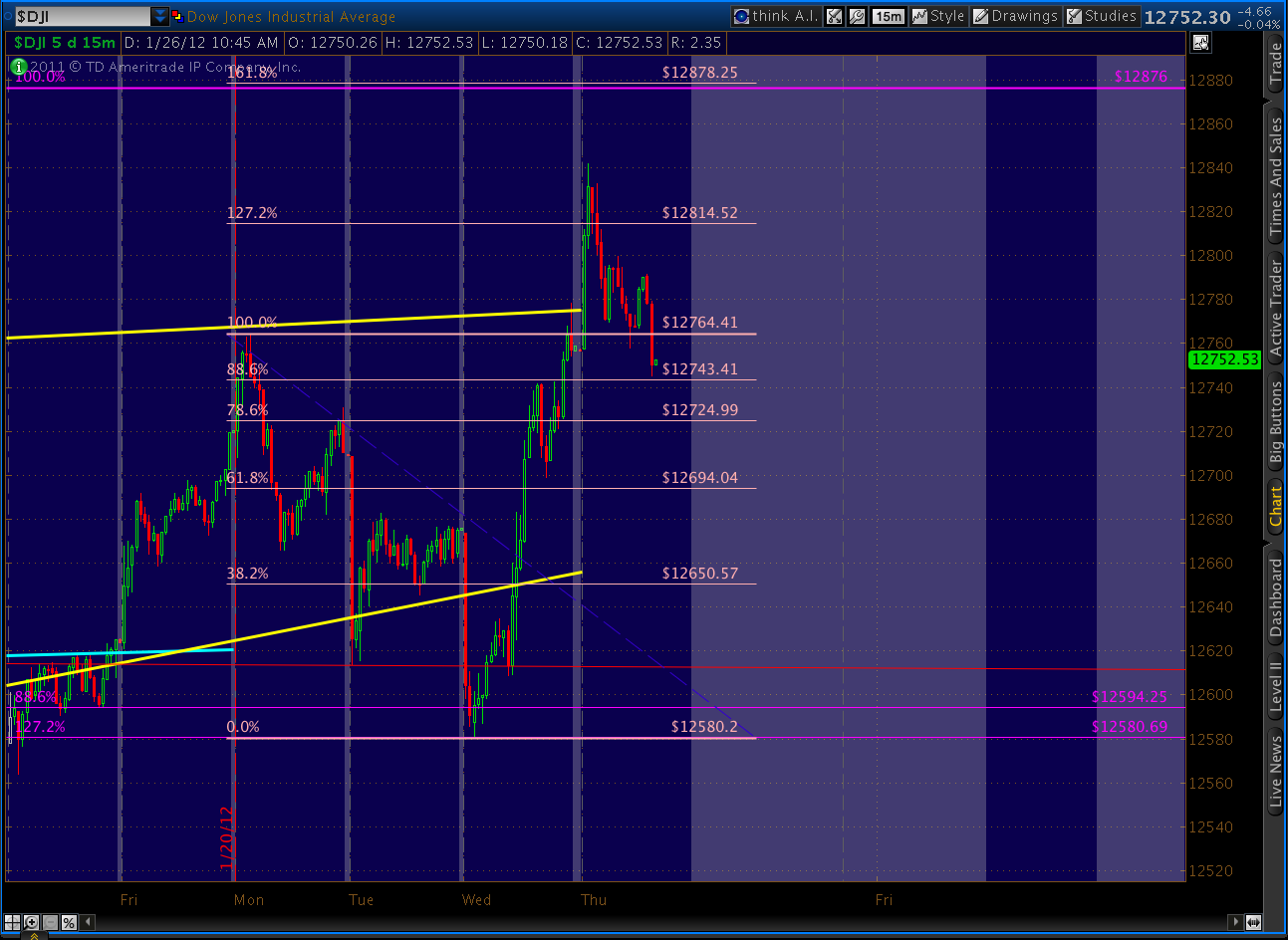

The only pattern that I really like it this one. It turns right at the .786 so it’s (so far) a perfectly formed Butterfly that calls for a Point D at the 1.272 extension of 1329. This fits with your RSI harmonics observation, Dillzs, and it’s one I’m really comfortable with. It also happens to be darned close to your 1336.

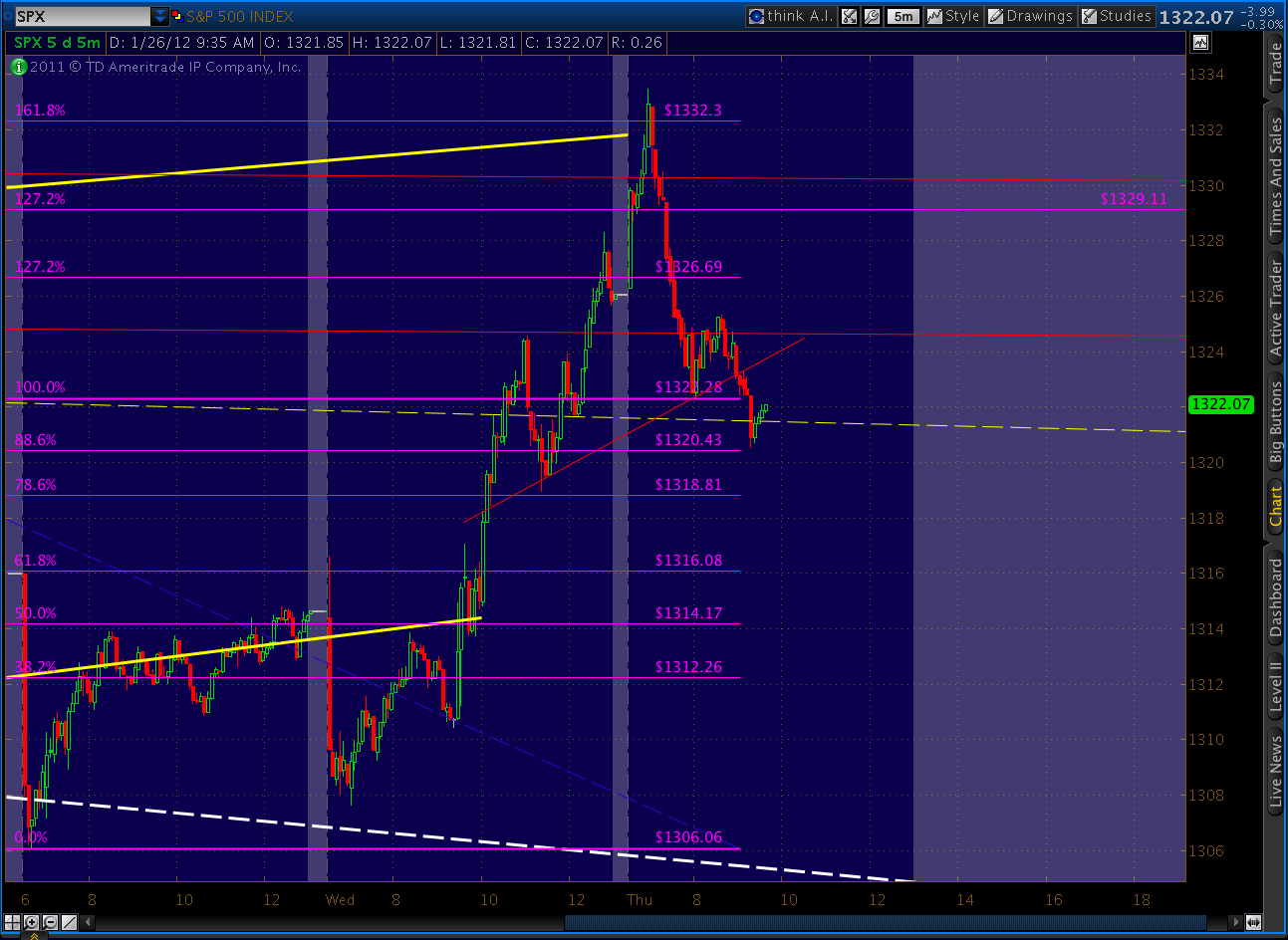

I’ve drawn the fan line off Oct 2007 as precisely as TOS allows, and I think 1329 is a little closer to 1325 or 1331 (current values, depending on whether you count the May 2 shadow) than 1336. Here’s a close up.

Having said all that, we could easily hit 1336. This rise has a head of steam on it, and Wall Street is pumping the living crap out of it. I think bears, who have been beat down so many times over the past few months, are licking wounds and picking a place to take a stand. The fan line from 2007 seems like a good one, and OPEX will no longer be an issue in about 26 hours.

Whether we turn down from here, 1329 or 1336 isn’t terribly important. It would be downright silly to try to catch the absolute top within pennies when we’re talking about a potential 300+ point drop (if this is, indeed, P3.)

More later.