The situation is pretty clear. By raising rates, the FOMC could continue to fight inflation but would also exacerbate the banking crisis. By pausing, the FOMC could give banks a little relief but would loosen financial conditions – thereby making it tougher to reduce inflation to target.

The seldom discussed situation is what impact the Fed’s decision would have on equity markets. This unspoken third mandate often weighs more heavily on decisions than do full employment and price stability.

From that standpoint, we look for the Fed to either: (a) pause but stress that the pause is due to rapidly tightening financial conditions which are inherently disinflationary; or, (b) raise 25 bps but stress that this could be the last hike for a while because they believe inflation is headed significantly lower due to tightening financial conditions.

Our own research indicates that this is true. Gas prices, which are very highly correlated with CPI, are slated to fall 18.6% YoY in March. The last time the YoY delta hit this level was in Nov 2021 when CPI registered 1.17%.

Obviously, other stickier factors have usurped the inflation narrative: wages, real estate, cars, etc. But, as we’ve discussed often in these pages, many of these other categories have been fairly flat or have declined over the past year – meaning that their YoY deltas are also falling rapidly.

Obviously, other stickier factors have usurped the inflation narrative: wages, real estate, cars, etc. But, as we’ve discussed often in these pages, many of these other categories have been fairly flat or have declined over the past year – meaning that their YoY deltas are also falling rapidly.

Consider food prices, still elevated at 9.5% YoY in Feb.

Underlying prices, as reflected in the DBA agricultural ETF, have fallen 11.3% over the past year. As long as it remains in the very tight trading range it’s been in since Jun 2022, the YoY decline will reduce inflationary pressures just as oil/gas have.

Underlying prices, as reflected in the DBA agricultural ETF, have fallen 11.3% over the past year. As long as it remains in the very tight trading range it’s been in since Jun 2022, the YoY decline will reduce inflationary pressures just as oil/gas have.

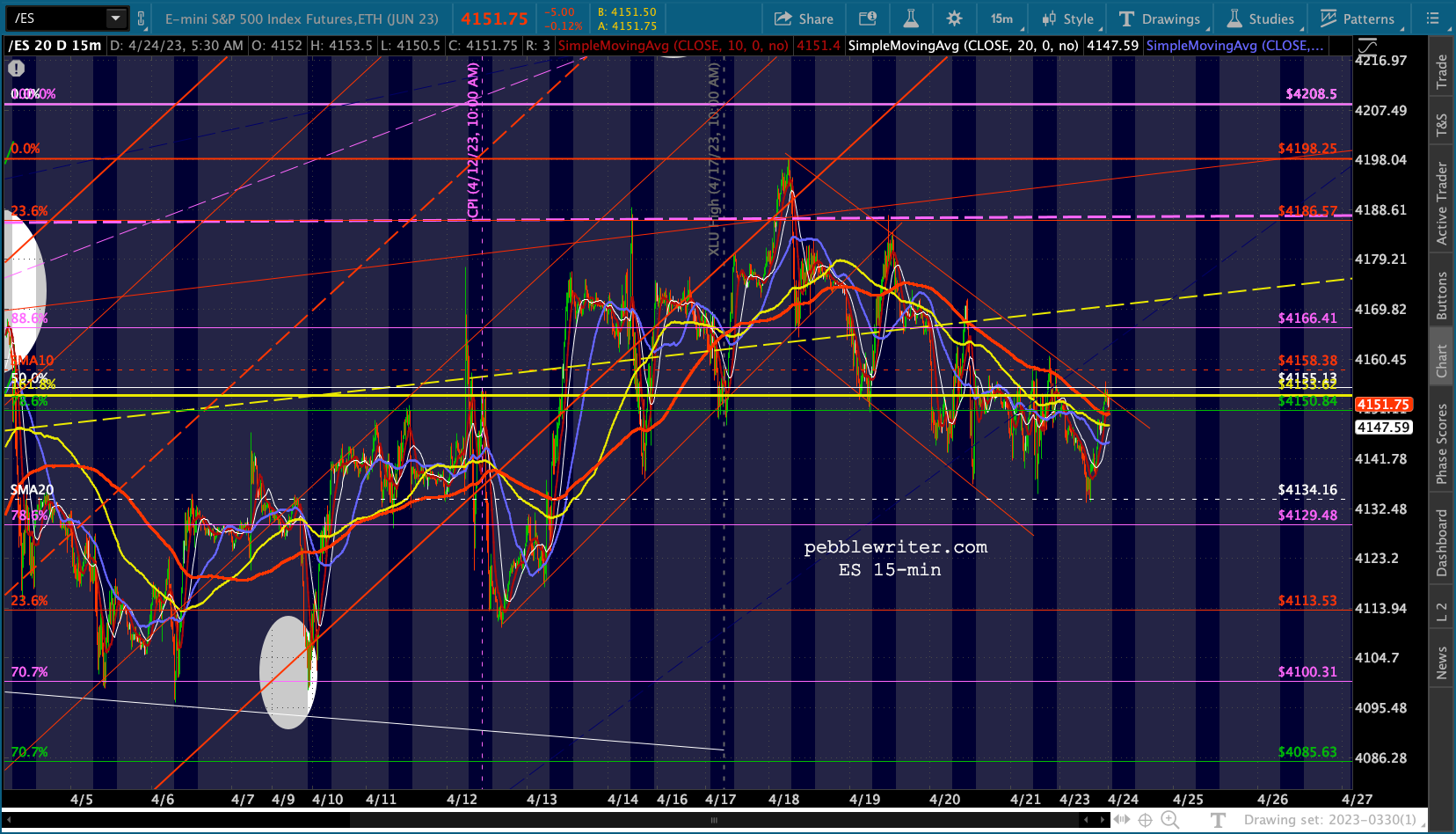

Futures have been vacillating around unch all night. The real action should start at 2PM with the announcement, followed by Powell’s press conference at 2:30.

Futures have been vacillating around unch all night. The real action should start at 2PM with the announcement, followed by Powell’s press conference at 2:30.

continued for members… (more…)

continued for members… (more…)

Utilities, a bond proxy for some, have taken a big hit this week as investors shift into shorter-term, less volatile treasuries.

Utilities, a bond proxy for some, have taken a big hit this week as investors shift into shorter-term, less volatile treasuries.