On June 10, in Did Kuroda Just Kill the Bull Market? we highlighted Bank of Japan head Haruhiko Kuroda’s surprising announcement to the Japanese parliament:

On June 10, in Did Kuroda Just Kill the Bull Market? we highlighted Bank of Japan head Haruhiko Kuroda’s surprising announcement to the Japanese parliament:

“The yen is unlikely to weaken further in real effective terms if you think with common sense, given how far it has come.”

After a massive (sarc) 3% slide in the Nikkei in the ensuing week, Kuroda has had second thoughts. Last night:

““I didn’t say that I’m not seeking a weak yen in nominal terms, nor did I say that it’s unlikely that the yen will fall further.”

Say what??? He further “clarifies:”

“I didn’t mean to evaluate the current nominal exchange rate or forecast the outlook. I just gave a theoretical explanation in response to a question about real effective rates.”

The “question” isn’t on the record — at least that I can find. And, though I have no video to support this, I’m pretty sure that last comment was accompanied by a well-timed wink. Consider the Nikkei 225, of which the BOJ has a sizable and growing position.

The yen’s last major deflating — reflected as a rise in USDJPY — came amidst the October 2014 market scare. The S&P 500 had fallen 9.8% in less than a month (the Nikkei 12.3%.) The Fed and the BOJ swung into action.

The yen’s last major deflating — reflected as a rise in USDJPY — came amidst the October 2014 market scare. The S&P 500 had fallen 9.8% in less than a month (the Nikkei 12.3%.) The Fed and the BOJ swung into action.

Fed President Bullard hinted at QE4, and the BoJ immediately monkey-hammered the yen — followed a few days later by a massive increase in QE and direct stock buying by the BOJ itself and the government pension plan. The impact was dramatic.

NKD spiked 21% in just two weeks (SPX by 11%.) But, it wasn’t quite enough for the NKD to top its nosebleed 2007 highs.

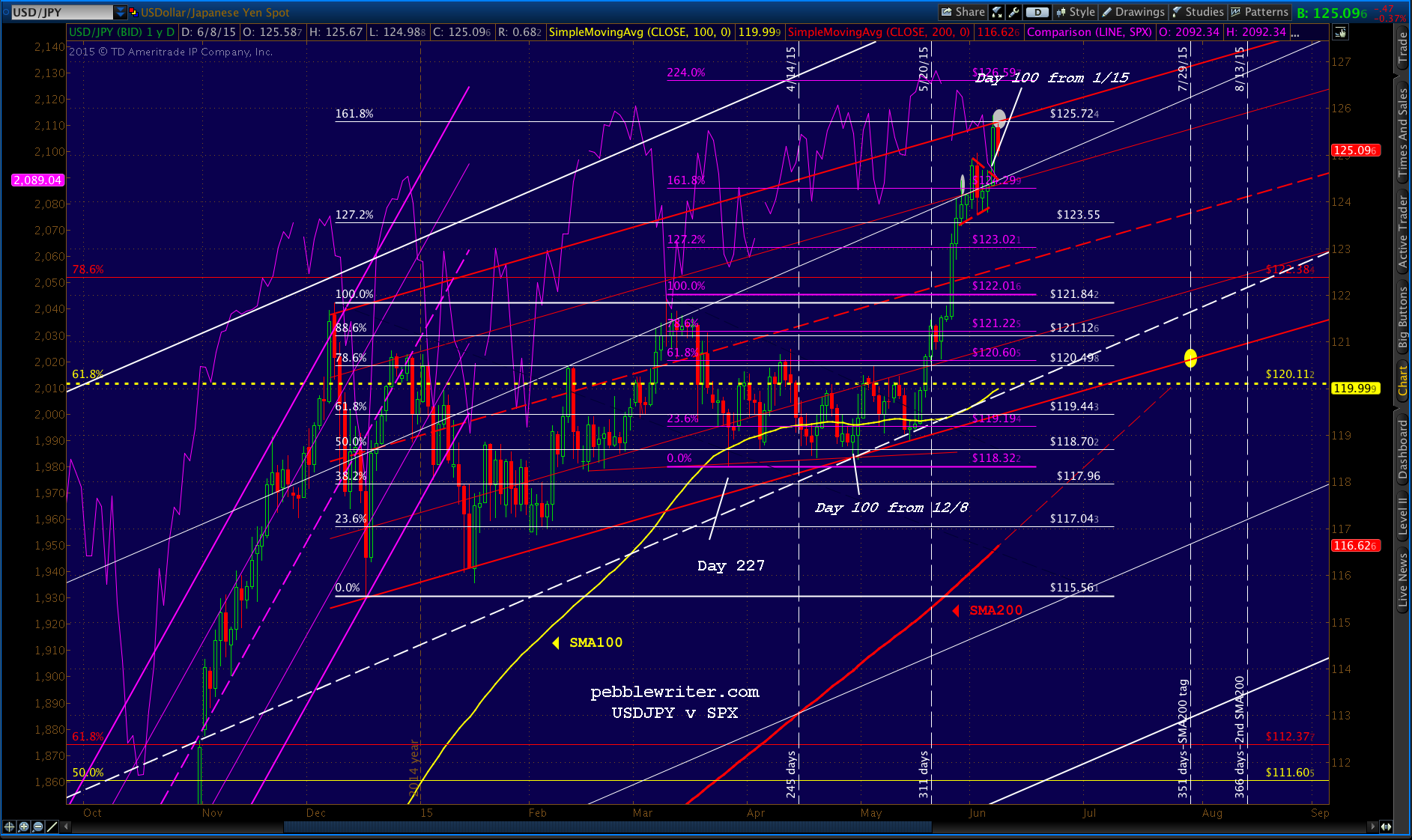

Why not? On Dec 4, the USDJPY reached a major Fibonacci level: the 61.8% retracement of the drop from 147.65 in 1998 to its 2011 lows of 75.56. Big investors who depend on the lucrative yen carry trade for huge profits [see: The Yen Carry Trade Explained] reined in their equity exposure — as is illustrated below.

Why not? On Dec 4, the USDJPY reached a major Fibonacci level: the 61.8% retracement of the drop from 147.65 in 1998 to its 2011 lows of 75.56. Big investors who depend on the lucrative yen carry trade for huge profits [see: The Yen Carry Trade Explained] reined in their equity exposure — as is illustrated below.

The .618 Fib is shown as the dotted yellow line (at 120.11), and the daily SPX values are plotted as a thin purple line on the chart below. Note the wild swings in SPX that began right after USDJPY reached 120.11.

Every time stocks started selling off, the USDJPY would magically make a bee line for 120.11 — typically landing just above it in order to reassure carry trade investors that all was well (producing a series of new highs for SPX.)

Every time stocks started selling off, the USDJPY would magically make a bee line for 120.11 — typically landing just above it in order to reassure carry trade investors that all was well (producing a series of new highs for SPX.)

In late May, when SPX completed the last major Fibonacci Pattern on the its chart [see: The Last Big Butterfly] and was threatened with a major reversal, what happened? USDJPY suddenly shot from below 120.11 to 125.84.

On the other side of the Pacific, the manipulation was even more obvious. NKD approached its 2007 highs in December exactly as USDJPY reached the .618 Fib at 120.11. They both peaked on Dec 5.

Every time since then that NKD needed a boost, USDJPY would shoot up past 120.11 — if only temporarily. The objective? Maintain the rising red acceleration channel that offers an opportunity to break out of the rising white channel from 2009.

Note that Kuroda’s initial comment talking up the yen (down the USDJPY) came as NKD had reached the top of its white channel and the midline of the red — natural reversal points in chart pattern theory.

Note that Kuroda’s initial comment talking up the yen (down the USDJPY) came as NKD had reached the top of its white channel and the midline of the red — natural reversal points in chart pattern theory.

It’s common knowledge that many in Japan are not happy with the yen’s demise. In a country where almost everything is imported, it places a real burden on consumers and manufacturers alike. Despite Kuroda and Abe’s insistence to the contrary, inflation is already a problem.

Oil, which was deliberately crashed for a plethora of reasons [see: Those Wacky Central Bankers], has rebounded strongly — up 37% in yen terms since we called the bottom on March 17 [see: Update on Oil.]

Aluminum has soared in yen terms, up 64% since its 2012 lows and easily outpacing the growth in sales a cheaper yen promised to deliver the auto manufacturers.

Aluminum has soared in yen terms, up 64% since its 2012 lows and easily outpacing the growth in sales a cheaper yen promised to deliver the auto manufacturers.

On the consumer side, fresh food prices are hitting new highs.

On the consumer side, fresh food prices are hitting new highs.

And, meat prices are through the roof.

And, meat prices are through the roof.

In short, a plunging yen places an very real and onerous tax on the very consumers and businesses who are already being bled dry by rising taxes. Kuroda knows this, and started talking up the yen on June 8. The Nikkei 225 immediately plunged 4%.

In short, a plunging yen places an very real and onerous tax on the very consumers and businesses who are already being bled dry by rising taxes. Kuroda knows this, and started talking up the yen on June 8. The Nikkei 225 immediately plunged 4%.

The USDJPY found channel support (red mid-line), which allowed NKD (thin purple line above) to recover (a Fibonacci) .886 of its losses. But, its failure to retake the Jun 9 lows and subsequent failure of a short-term trend line has left NKD vulnerable to additional losses.

The USDJPY found channel support (red mid-line), which allowed NKD (thin purple line above) to recover (a Fibonacci) .886 of its losses. But, its failure to retake the Jun 9 lows and subsequent failure of a short-term trend line has left NKD vulnerable to additional losses.

Enter Kuroda again, helping us better understand his comments of last week. NKD’s decline was arrested, just in time to preserve the rising red channel discussed above.

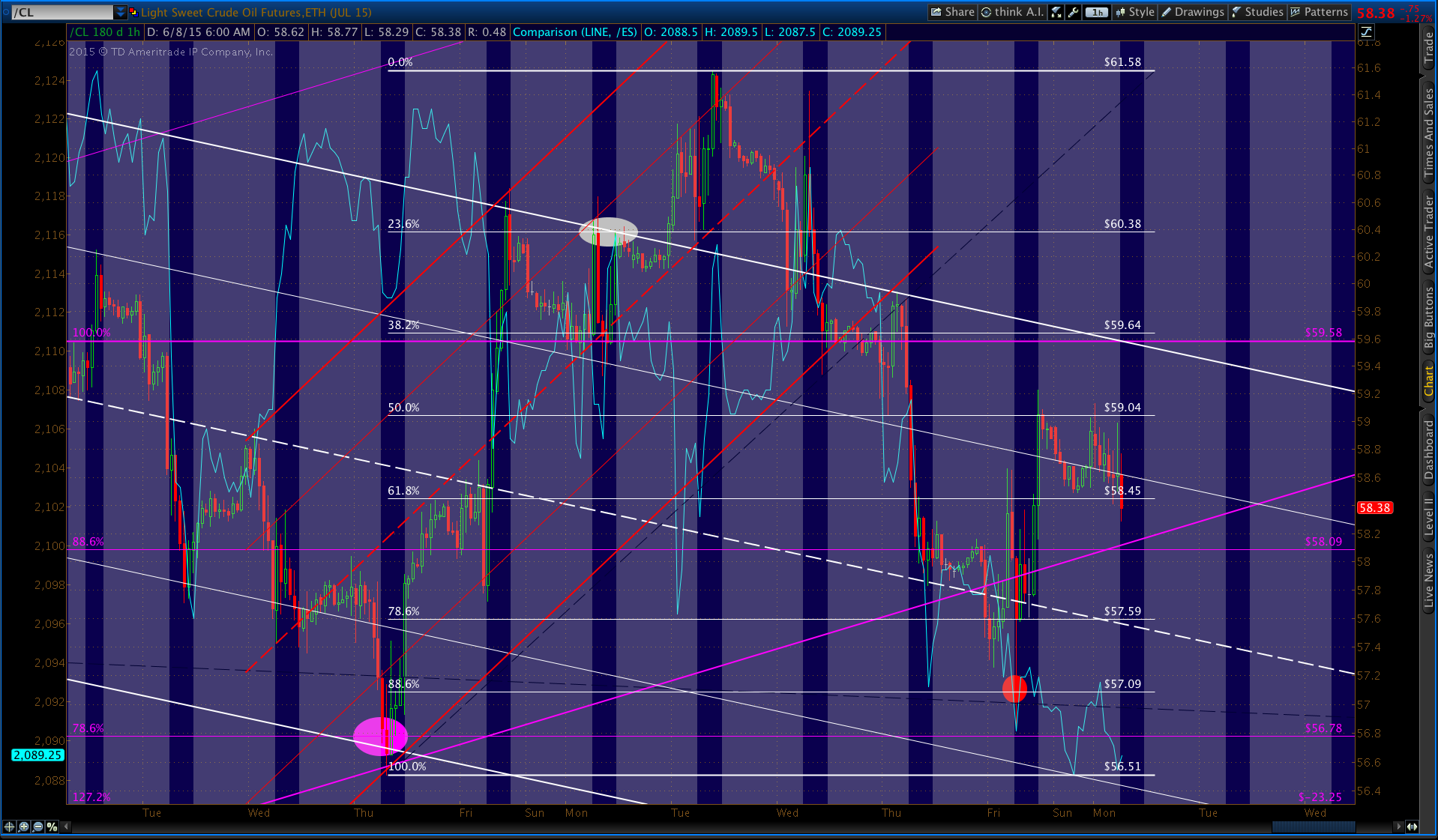

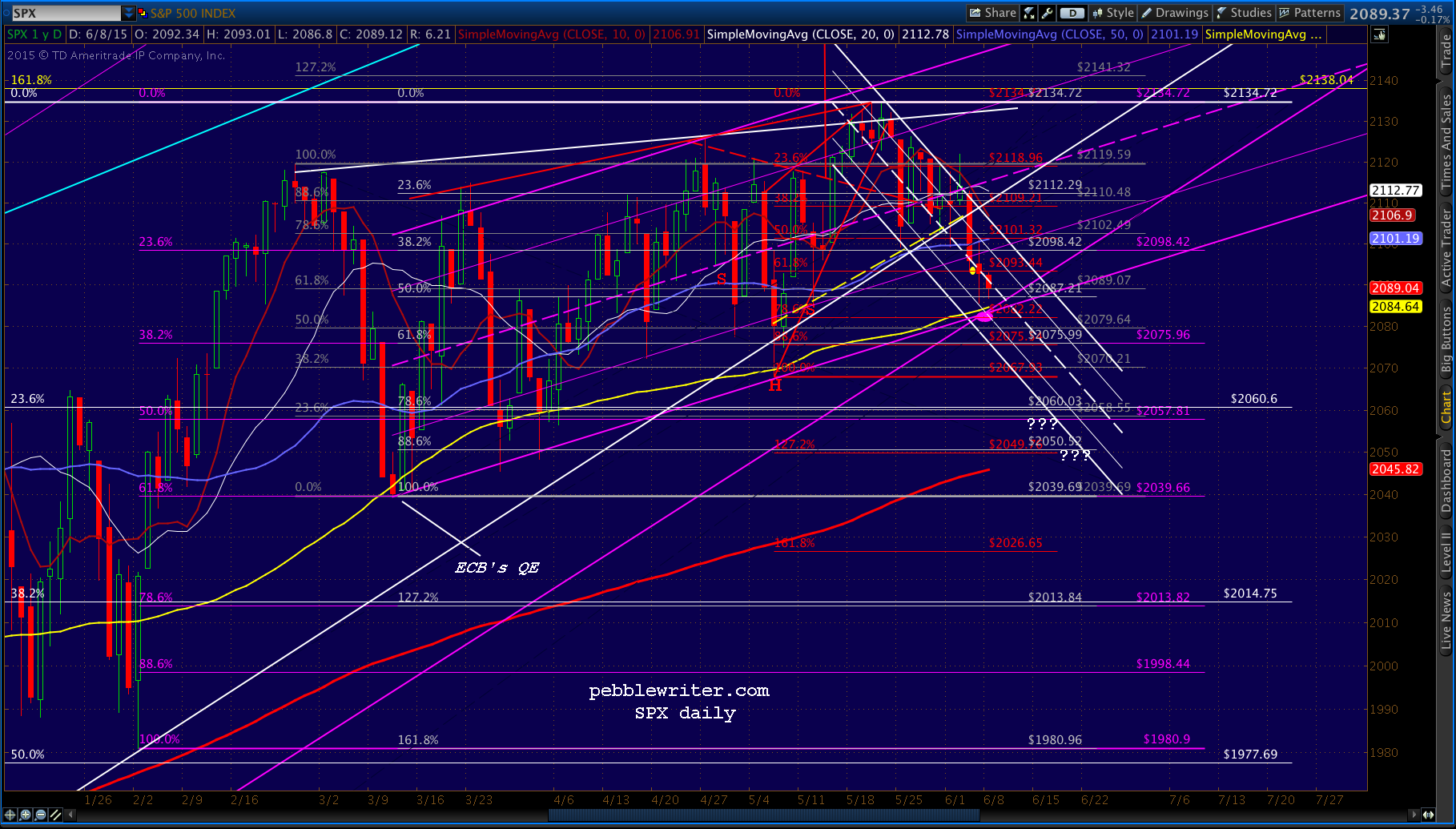

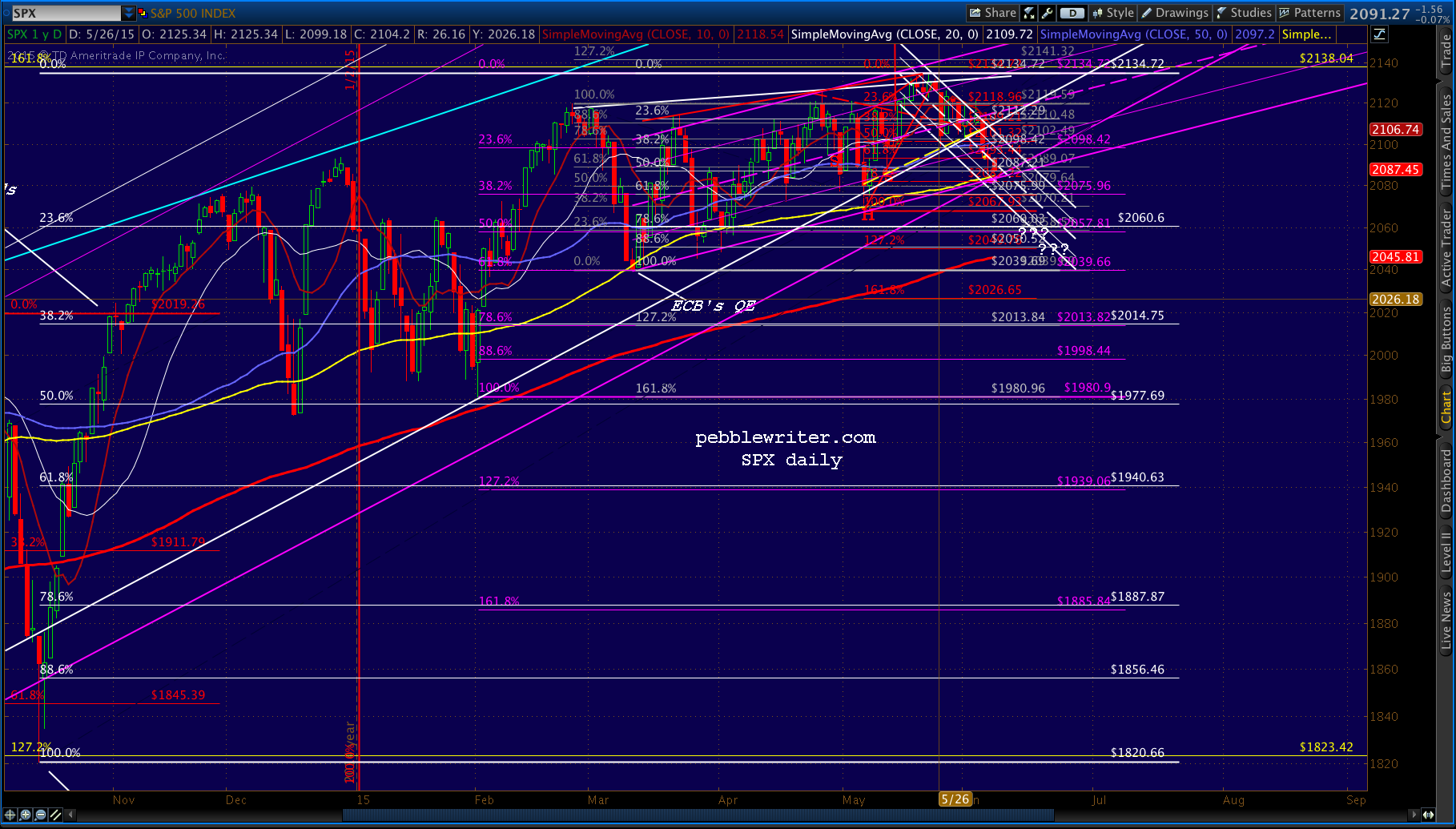

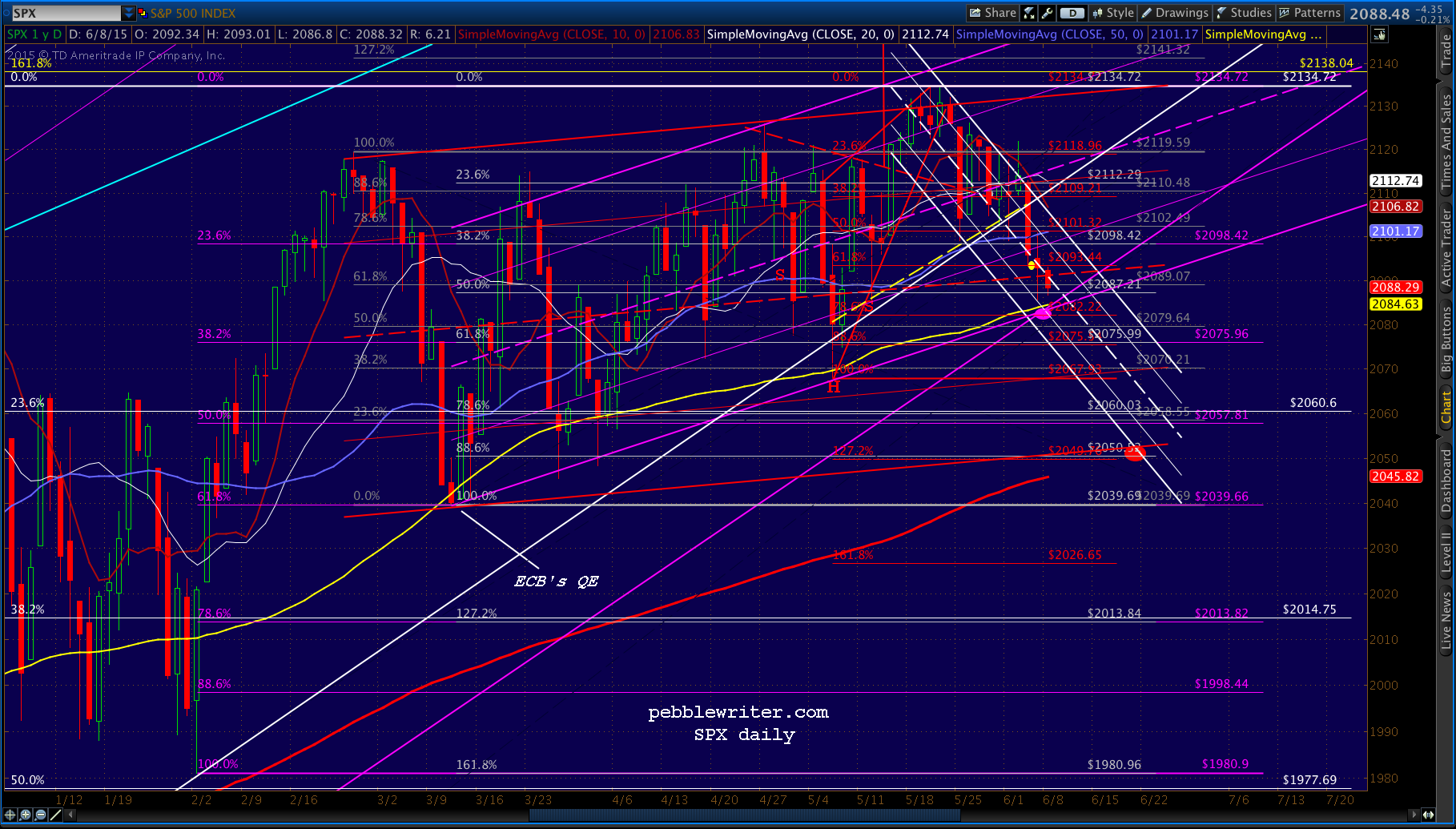

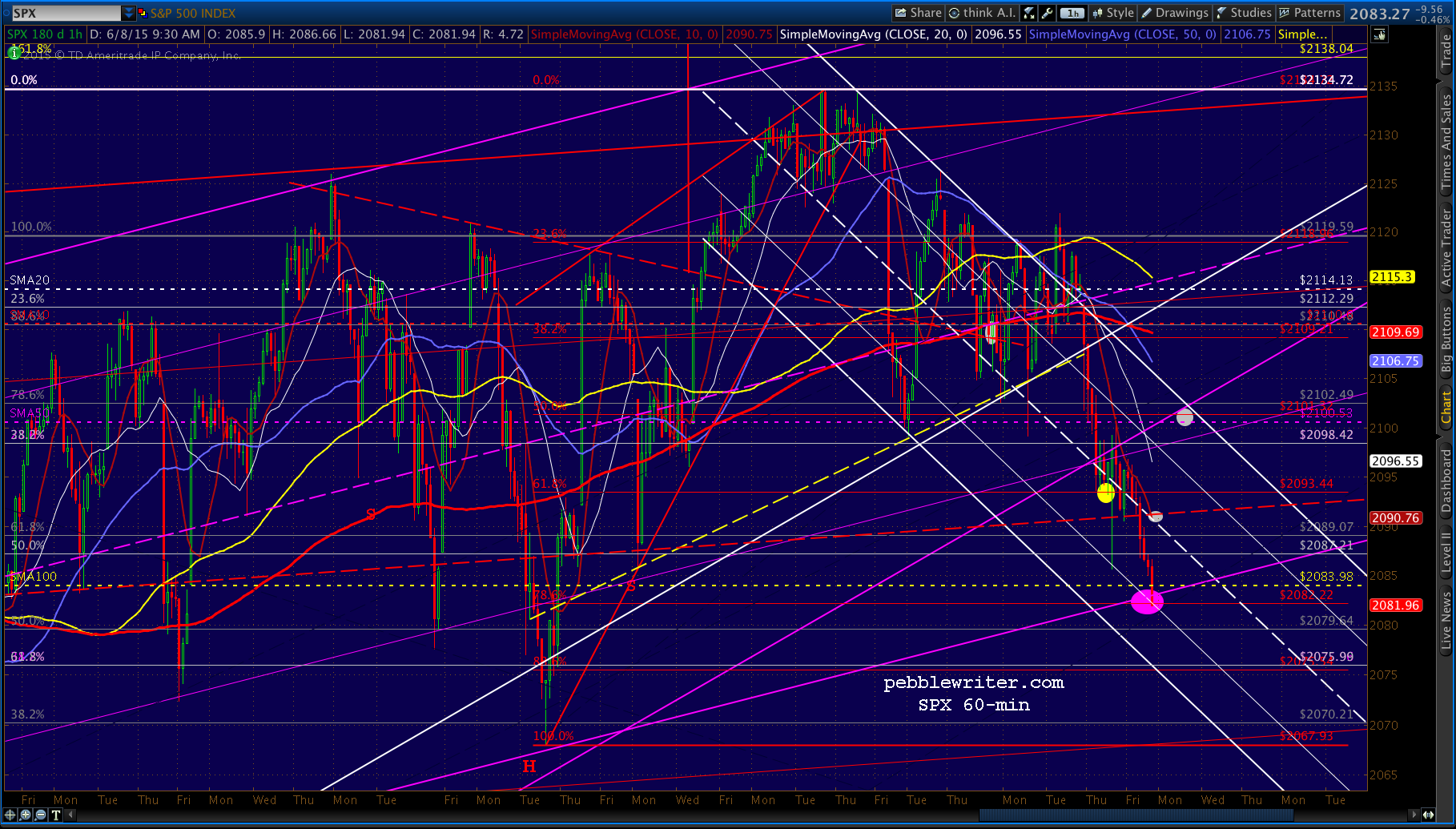

SPX is up about 8 points and, in fact, just nailed our secondary bounce target posted in yesterday’s members section.

SPX just tagged our next downside target, reaching 2074.26… An ideal bounce spot would be back to the SMA100 at 2088 or even the gray midline around 2092.

With the “markets” subject not only to made up news stories (what’s the latest tweet re Greece?) but the constant manipulations unleashed by politicians and central bankers, is there much value in economic analysis or charting anymore?

With the “markets” subject not only to made up news stories (what’s the latest tweet re Greece?) but the constant manipulations unleashed by politicians and central bankers, is there much value in economic analysis or charting anymore?

Clearly, Japan is in deep, deep trouble. They’ve gone all in on the yen carry trade and are, effectively, holding a very large heavily margined position in stocks and bonds that would absolutely crater were the yen to strengthen significantly.

Caught in between the rock of protecting their balance sheet and the hard place of screwing over the Japanese people, they’re apparently going with the rock. When push comes to shove, Kuroda explains, the yen can absolutely go even lower.

As long as it does, the yen carry trade needn’t unwind — much like in 1995-2000 and 2003-2007. If it should reverse, however, run — don’t walk — to the nearest exit.

We won’t know until it happens how effectively central bankers can stave off a true market crash once it gets started. We’ve had several warning signs already — including the Big Butterfly Pattern completion on May 20. I for one, would rather remain aware of the danger zones ahead instead of cruising blithely along, assuming they won’t bite me as long as I ignore them.

Coming up: today’s market update and forecast.

Note: We’ll be updating and automating the mailing list this weekend. If you didn’t get an email this morning advising you of this post, take a moment to enter your email address in the subscription box to the right.

continued for members… (more…)

Remember, at least 75% of the time, FOMC announcements/press conferences have led to a frenzy of algo activity that drives prices higher into the close. It’s part of the “FOMC has got our back” meme that investors have come to accept/expect.

Remember, at least 75% of the time, FOMC announcements/press conferences have led to a frenzy of algo activity that drives prices higher into the close. It’s part of the “FOMC has got our back” meme that investors have come to accept/expect. My preference is to stay on the sidelines on days like today. The algo-driven rallies don’t always last, and there are often sharp spikes in either direction.

My preference is to stay on the sidelines on days like today. The algo-driven rallies don’t always last, and there are often sharp spikes in either direction. Updated targets and currency charts coming up in a few.

Updated targets and currency charts coming up in a few.