“If you give a mouse a cookie, he’s going to ask for a glass of milk. When you give him the milk, he’ll probably ask you for a straw. When he’s finished, he’ll ask you for a napkin. Then he’ll want to look in a mirror to make sure he doesn’t have a milk mustache.”

“If you give a mouse a cookie, he’s going to ask for a glass of milk. When you give him the milk, he’ll probably ask you for a straw. When he’s finished, he’ll ask you for a napkin. Then he’ll want to look in a mirror to make sure he doesn’t have a milk mustache.”

And, the familiar children’s classic goes on from there – one amusing unintended consequence after another.

One parallel in the investment world is oil. If you ramp up oil futures in order to convince investors that demand and profitability are coming back, you run the risk of those higher prices showing up in some unfortunate places — such as PPI.

And, if PPI rises, say, the most in three years, investors will come to fear higher interest rates from central banks. And, if they fear higher interest rates, they’ll start dumping bonds — which are bid up to impossibly high levels by those same central banks. If investors start dumping bonds, you will get those higher interest rates of which they were afraid.

If governments can’t sell bonds at 0-2%, then their budgets — which have been balanced on the back of zero interest rate policy — go belly up. And, if government budgets go belly up, we might just have a financial crisis that spirals out of control.

Wouldn’t that be an amusing unintended consequence?

Crude light is up 37% since its March lows — largely to mask the fact that the all-important yen carry trade is faltering.

The yen carry trade is faltering because the yen basically squatted at 120 for over 5 months. USDJPY finally broke out at the end of May, only to be talked back down two days ago by Kuroda himself [see: Did Kuroda Just Kill the Bull Market?]

The yen carry trade is faltering because the yen basically squatted at 120 for over 5 months. USDJPY finally broke out at the end of May, only to be talked back down two days ago by Kuroda himself [see: Did Kuroda Just Kill the Bull Market?]

“The yen is unlikely to weaken further in real effective terms if you think with common sense, given how far it has come.”

In a “market” that has thrived on zero interest rates, investor complacency and central bank manipulation, we have to wonder how much longer the free lunch can last?

In a “market” that has thrived on zero interest rates, investor complacency and central bank manipulation, we have to wonder how much longer the free lunch can last?

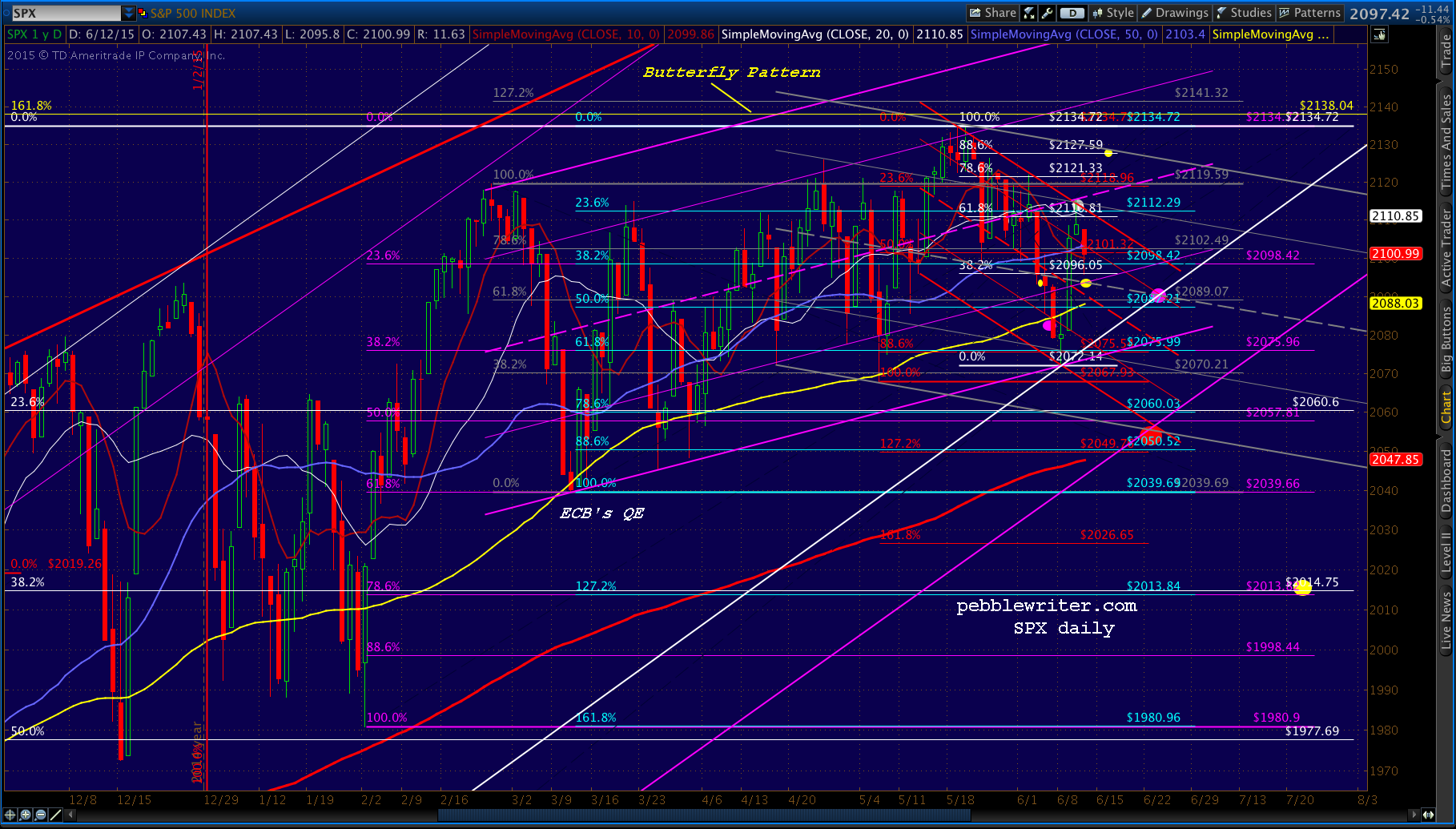

Yesterday, SPX slightly overshot our upside target (2112, later revised to 2115 in the member section.) Our downside targets remain in place. But, watch out for those Greece rumors, which can send prices soaring or plunging regardless of their veracity.

continued for members…Recall that our first downside target was a test of the intersection between the falling gray channel midline and the rising purple channel .236 line.

Piece it back together, and it looks like this, with a pullback here at 2115 to the SMA50 at 2102 or, secondarily, the purple channel .236 line where it intersects the gray channel midline at 2093ish.

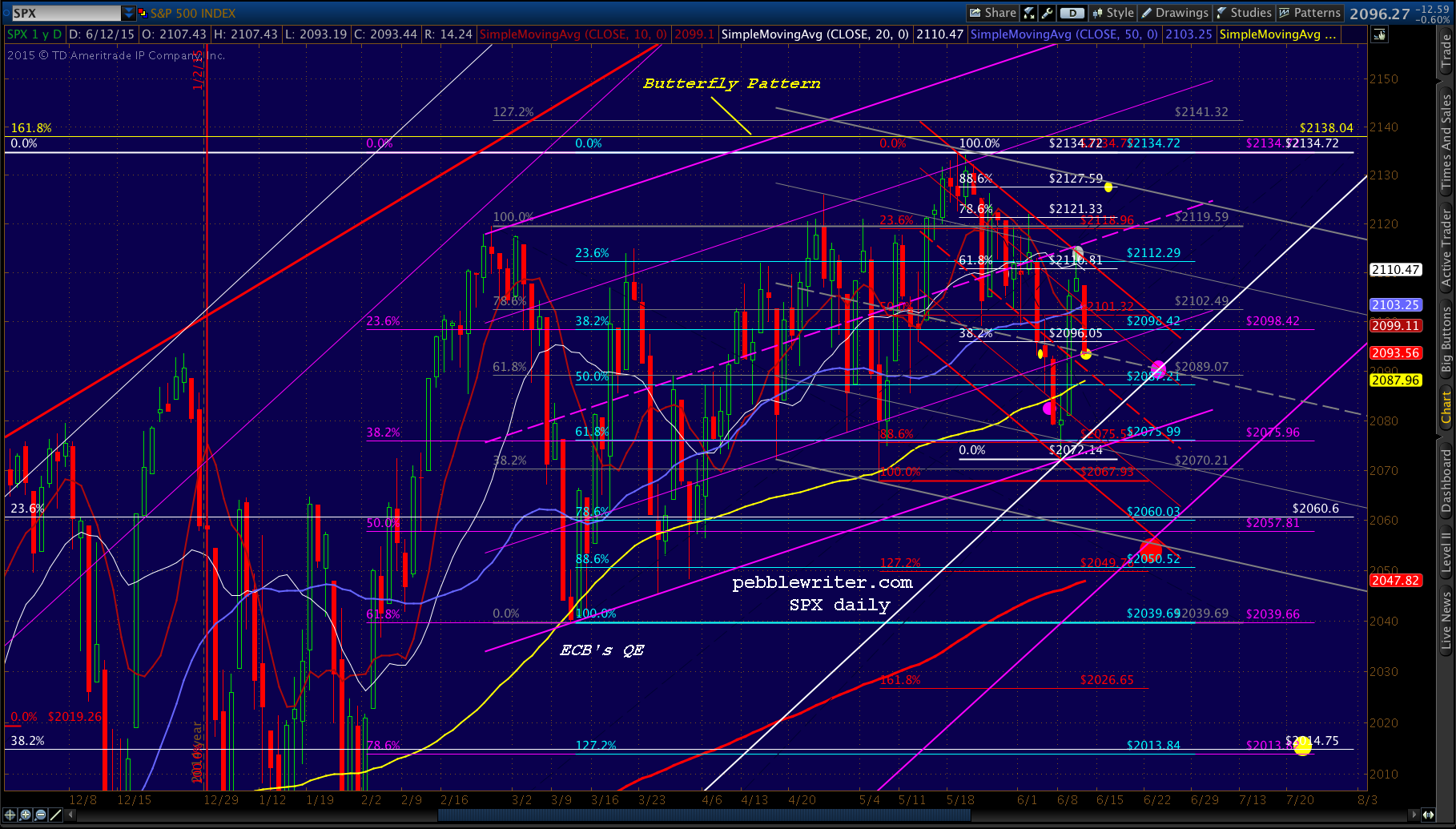

UPDATE: 10:37 AM

UPDATE: 10:37 AM

SPX just reached 2093 and should (60:40?) reverse. I wouldn’t necessarily switch to a long position here (though nimble traders might give it a shot), as the SMA100 is just below at 2088. But, anyone who’s considering holding on to a short position should at least consider placing stops.

Where do we go from here? A bounce keeps the rising purple channel from the March lows intact, with 2138 then a matter of time. A failure of the falling gray channel midline indicates (at least) another test of the SMA100 and — should that fail — the big white channel bottom at around 2077. Ultimately, as we’ve discussed before, I like the SMA200 which should arrive at 2050 next week.

Where do we go from here? A bounce keeps the rising purple channel from the March lows intact, with 2138 then a matter of time. A failure of the falling gray channel midline indicates (at least) another test of the SMA100 and — should that fail — the big white channel bottom at around 2077. Ultimately, as we’ve discussed before, I like the SMA200 which should arrive at 2050 next week.

Stay tuned.