Over the last 20 years, we’ve seen two yield curve (2s10s) inversions: essentially all of 2000 and Dec 2005-May 2007. The inversions themselves posed no issues for equity markets. It was the dramatic unwinding of those inversions that produced crashes. Eight months ago, we almost had another. 2s10s had fallen to a trend line connecting those two previous curve lows. Instead of bouncing, however, 2s10s continued falling — reaching a low of .18 on Aug 27.

Eight months ago, we almost had another. 2s10s had fallen to a trend line connecting those two previous curve lows. Instead of bouncing, however, 2s10s continued falling — reaching a low of .18 on Aug 27.

Unfortunately, the optics of this approach to an inversion are troublesome. It is commonly believed that inversions presage recessions. So, the brain trust in the Eccles Building has a little tightrope walking to do.

They need to increase the short end of the curve to stave off (understated) inflation and build some cushion for the next financial calamity. But, to avoid an inversion, they must scale back their intervention in the 10Y — at least enough so it can keep pace with the rapidly rising 2Y.

Eagle-eyed observers might note that both recently out above the trend line connecting previous highs. Not so coincidentally, this occurred as the above-referenced trend line connecting the 2s10s lows was breached and equities began their Jan-Feb swoon.

Eagle-eyed observers might note that both recently out above the trend line connecting previous highs. Not so coincidentally, this occurred as the above-referenced trend line connecting the 2s10s lows was breached and equities began their Jan-Feb swoon. Can the Fed keep the plates spinning a little longer? Without question. Especially if Powell is successful in convincing

Can the Fed keep the plates spinning a little longer? Without question. Especially if Powell is successful in convincing investors algos that the economy is strong but there is no wage pressure and inflation poses no real threat.

Should that narrative fail, however, the spectre of higher rates alongside soaring debt levels might finally awaken equity and bond investors to the elephant in the room.

* * *

* * *

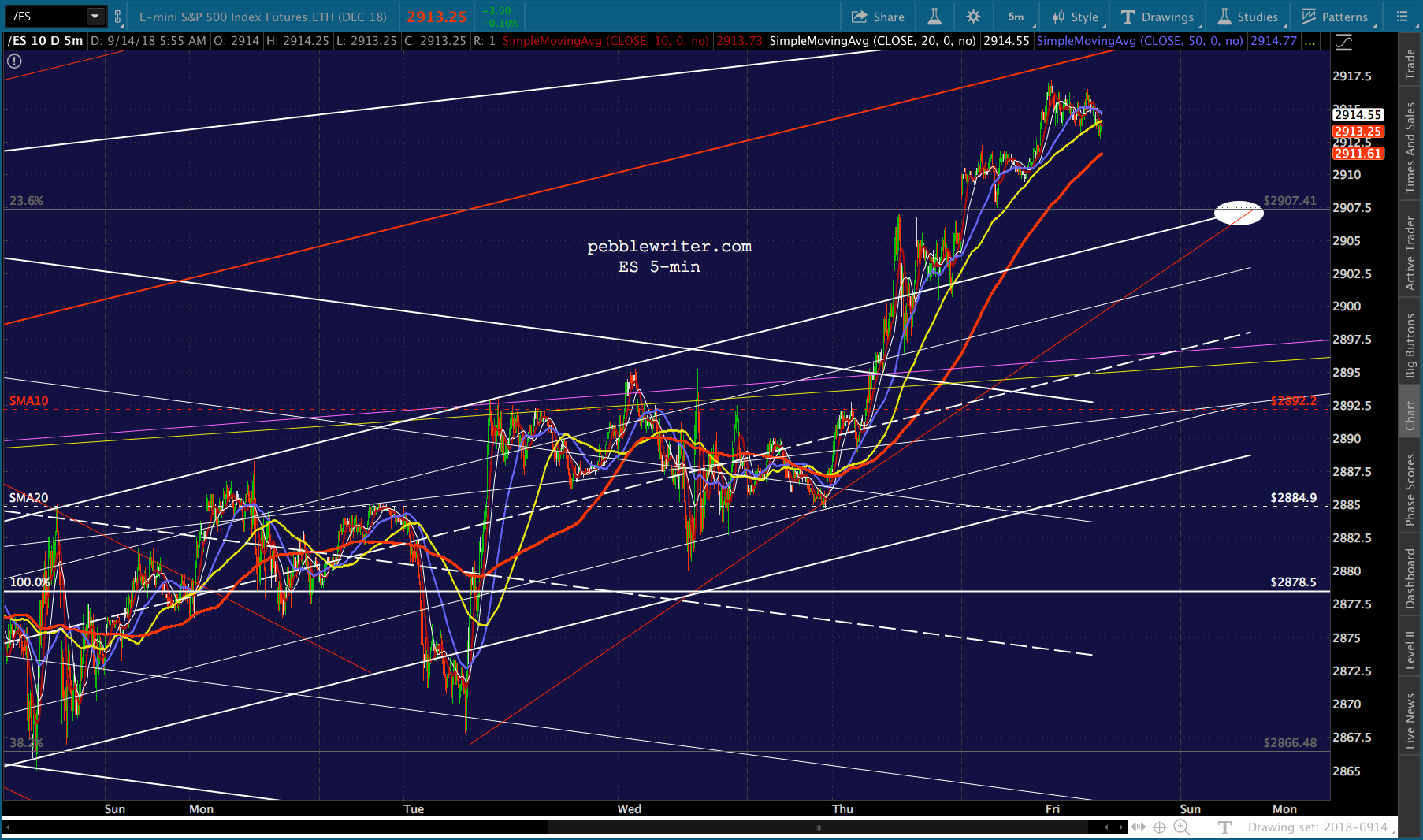

So far, the damage resulting from Friday’s channel breakdown has been contained to the August highs.

But, still ahead, EIA inventory reports and the FOMC statement and press conference.

But, still ahead, EIA inventory reports and the FOMC statement and press conference.

continued for members… (more…)