The currency crisis in Turkey is finally spilling over into the euro, which is finally breaking down. Not to worry, as we’ve been here before. The complication, of course, is that CPI remains stubbornly high at 2.9%. This is dangerous territory and greatly exacerbates the difficulty the Fed faces in threading the needle of interest rate hikes.

The complication, of course, is that CPI remains stubbornly high at 2.9%. This is dangerous territory and greatly exacerbates the difficulty the Fed faces in threading the needle of interest rate hikes.

As a net importer, the US needs dollar strength to keep inflation under control. But, continuing dollar strength could do untold damage to euro zone banks which are grappling not only with dollar-denominated obligations but with Turkish lira exposure.

Witness Deutsche which, try as it might to recover, is off over 6% today.

By working to establish a buffer for the next financial crisis, the Fed might have hastened its arrival.

continued for members…

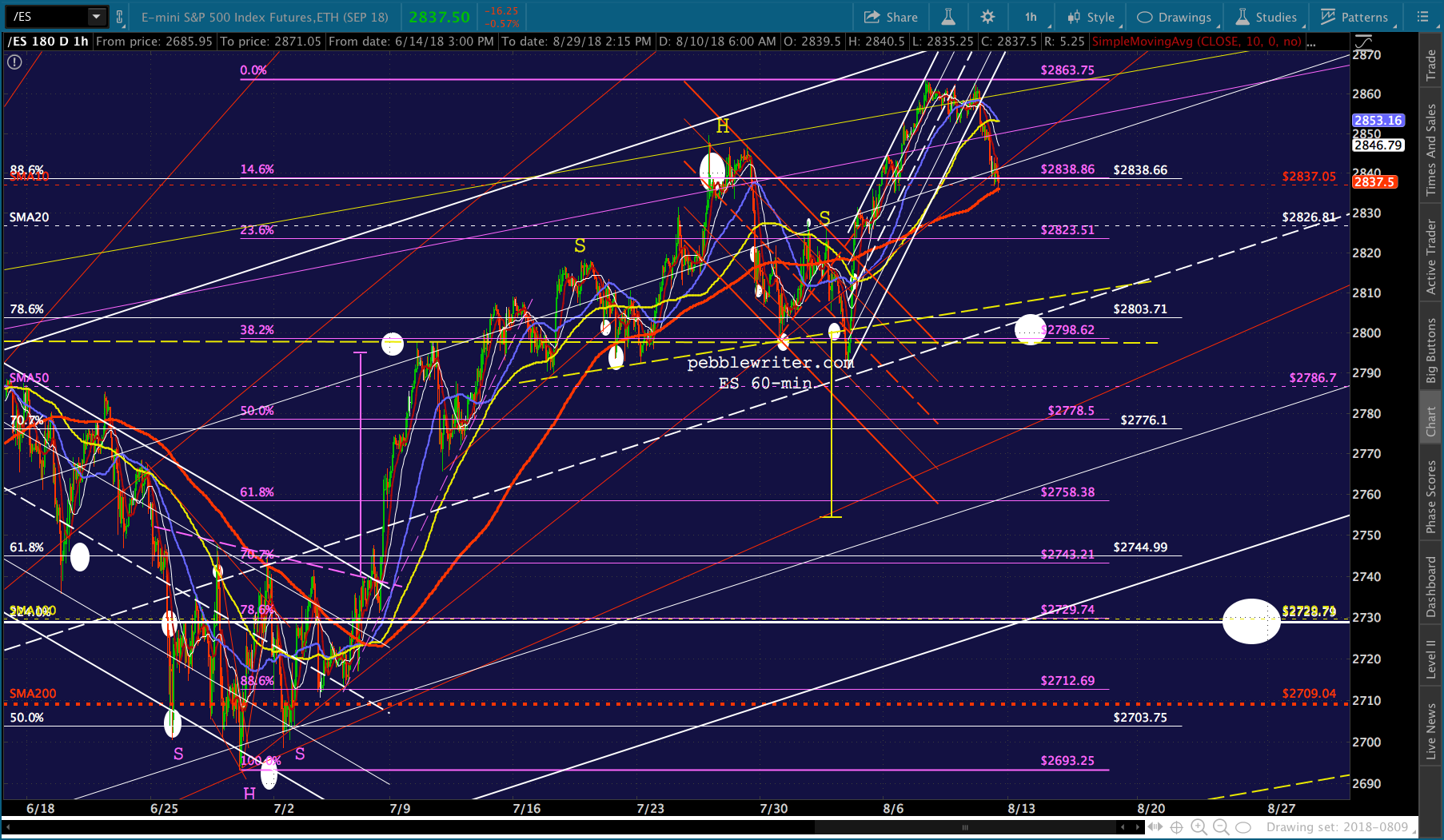

The turmoil is spilling over into the yen, which is strengthening against the dollar and doing a number on equities. If the USDJPY drops back into the falling white channel it recently broke out of, it will make for a big mess for stocks. Futures are currently off about 17 points. If the SMA10 and .886 can’t hold the backtest, we could see ES backtest the busted neckline or .786 at around 2803 – 2810.

Futures are currently off about 17 points. If the SMA10 and .886 can’t hold the backtest, we could see ES backtest the busted neckline or .786 at around 2803 – 2810.

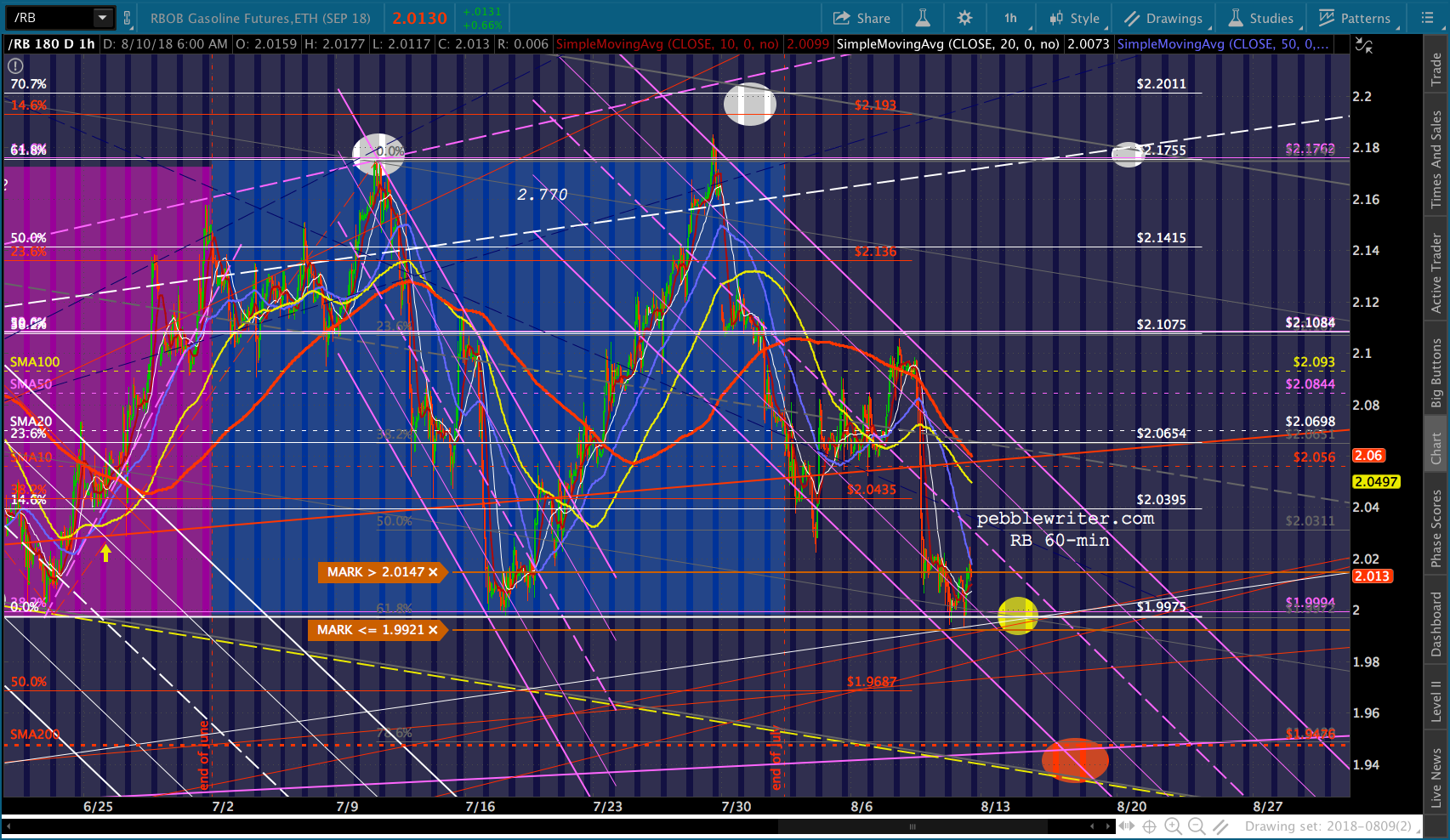

The fallback position for SPX is also its SMA10 (2833.88) which also overlaps the .886. One factor that could help is CL and RB, which are currently up about 1%. But, of course, higher oil and gas prices have limited appeal when inflation is on the rise. Will the algos care? Hard to say.

One factor that could help is CL and RB, which are currently up about 1%. But, of course, higher oil and gas prices have limited appeal when inflation is on the rise. Will the algos care? Hard to say.

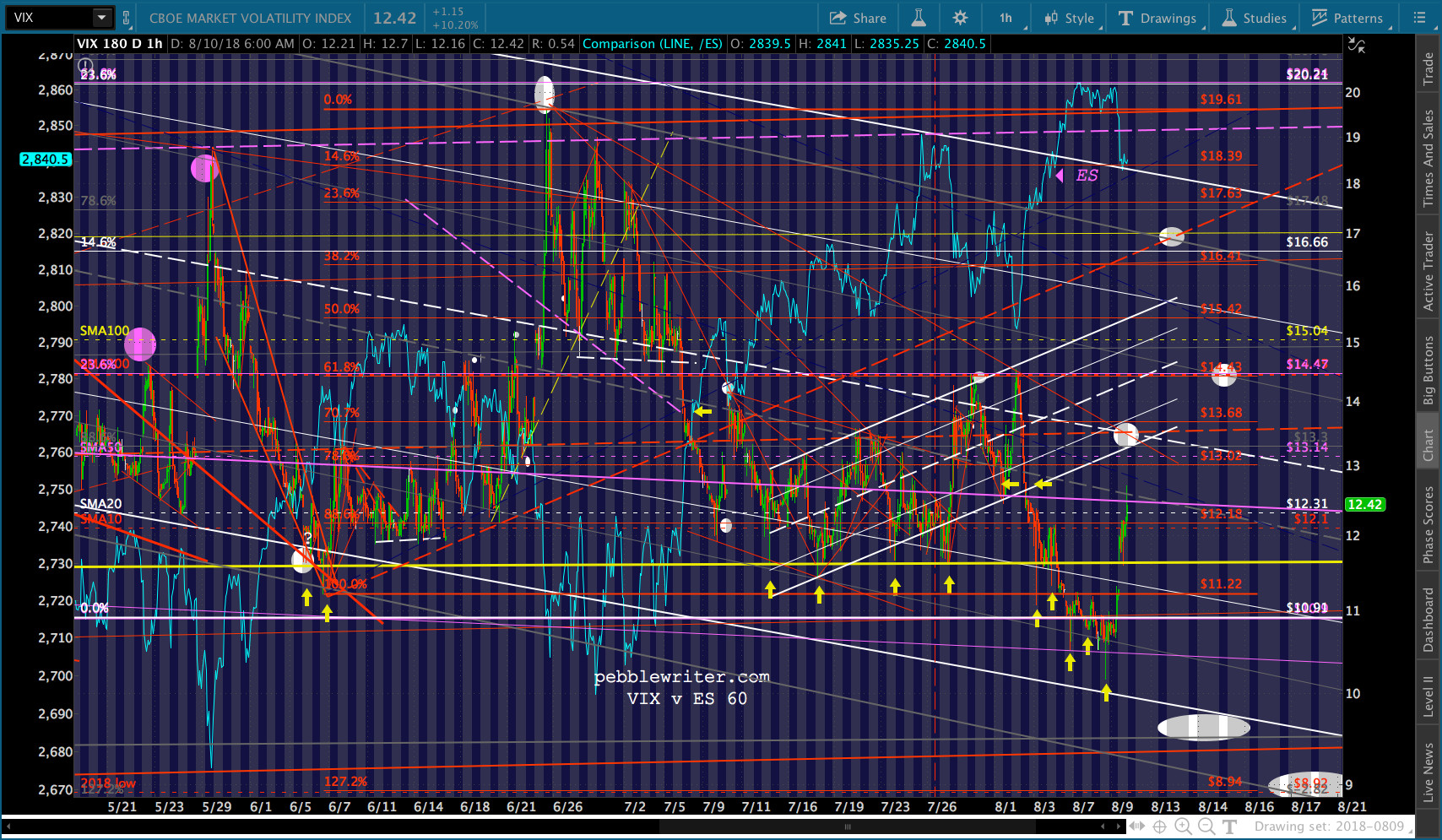

VIX isn’t much help this morning as it’s under buying pressure. It almost reached a 9 handle yesterday, but is bouncing strongly. There are multiple upside targets, with the first being the purple channel bottom around 12.7. If it breaks higher, we’re looking at 13.35, the SMA200 at 14.43, 17 and 17.63.

VIX isn’t much help this morning as it’s under buying pressure. It almost reached a 9 handle yesterday, but is bouncing strongly. There are multiple upside targets, with the first being the purple channel bottom around 12.7. If it breaks higher, we’re looking at 13.35, the SMA200 at 14.43, 17 and 17.63. Back to currencies. The dollar index is where things get very messy. It broke above horizontal resistance today and is closing in on the gray .618 at 96465. This is also the top of an aggressively rising channel.

Back to currencies. The dollar index is where things get very messy. It broke above horizontal resistance today and is closing in on the gray .618 at 96465. This is also the top of an aggressively rising channel. Let’s put ourselves in the Fed’s shoes. Worried about inflation, we hike twice more, further propping up the dollar and sending currency markets into chaos and doing grievous damage to systemically important global banks. In the process, the yield curve inverts and kills off business confidence. Stocks decline, especially if we crash oil and gas prices to keep inflation under control.

Let’s put ourselves in the Fed’s shoes. Worried about inflation, we hike twice more, further propping up the dollar and sending currency markets into chaos and doing grievous damage to systemically important global banks. In the process, the yield curve inverts and kills off business confidence. Stocks decline, especially if we crash oil and gas prices to keep inflation under control.

The alternative is to back off of rate hike talk, blaming it on currency chaos. The dollar crashes back to 89-90. Inflation would increase, but we could put pressure on oil and gas prices to offset it. The combination of a falling USDJPY and falling oil and gas prices would probably be too much for stocks.

It’s a difficult situation for the central banks. Even if they cooperate to the fullest extent possible, the rise of inflation — caused primarily by rising oil and gas prices — is a problem. If oil and gas prices decline, inflation is reduced by quite a bit. But, the latest rally in stocks was greatly bolstered by the breakout in oil and gas. If the breakout goes away, would the rally?

The trick, I think, is to keep oil and gas prices high enough to keep deflation at bay but low enough to keep inflation and interest rates under control — all with an eye toward maintaining the equity rally.

UPDATE: 3:50 PM

Quick update as we head into the close. ES and SPX are at their SMA20s, while VIX reached the white midline. In other words, could go either way on Monday. As always, only hold short if you can handle the gap risk.

Note that TNX fell pretty sharply today.

Note that TNX fell pretty sharply today. But, if we zoom in, we can see that it has formed a small triangle within the larger one. In other words, this might be all we get at this time.

But, if we zoom in, we can see that it has formed a small triangle within the larger one. In other words, this might be all we get at this time.

But, the price chart says there’s more to come.

EURUSD still looks plenty weak.

Though the DXY is pushing up against channel resistance.