SPX and ES had no trouble reaching our initial downside targets — a backtest of their January highs. We wondered, however, whether the SMA20s, loitering just below, might come into play.

SPX and ES had no trouble reaching our initial downside targets — a backtest of their January highs. We wondered, however, whether the SMA20s, loitering just below, might come into play.

Sure enough, ES tagged its SMA20 with ease. But, emini traders strongly resisted a drop through the SMA20 – bad mojo, don’t you know.

So, SPX only reached 2867.29, just shy of the SMA20 at 2866.27. And, faster than you can shout “help me Clarence!” SPX bounced the 16 points we anticipated, just like it did on Wednesday.

It was a near miss..or, was it? As we discussed on Tuesday…

One little trick we often see on days when it’s difficult to convince the machines to sell/short down to an obvious bounce point such as the SMA10 is to drive the price merely to where the SMA10 will be tomorrow. The SMA10 will likely increase by another 5 points tomorrow, so getting within 2-3 points is potentially “good enough.”

As luck the algos would have it, today’s SMA20 came in at…wait for it…2866.27. January highs and SMA20 were both tagged.  So, all is well, right? Not so fast. Futures are currently off 10 points, banks are tanking, oil and gas are slipping, FB is scurrying toward the basement and TSLA has tumbled 15% since Tuesday’s short call.

So, all is well, right? Not so fast. Futures are currently off 10 points, banks are tanking, oil and gas are slipping, FB is scurrying toward the basement and TSLA has tumbled 15% since Tuesday’s short call.

In the distance, sirens. A mob of nervous investors crowds the door. Might the Building & Loan actually be in trouble?

Thanks to overeager algos, the S&P 500 has thus far ignored the threats of tariffs, political turmoil, emerging market meltdowns, rising interest rates and historically high multiples. None of that matters as long as corporations can borrow cheap and repurchase their own shares, VIX can be hammered when necessary, the dollar continues rising and oil/gas prices don’t crash.

If any of those support mechanisms falters, however… Well, we’ve seen what can happen. Keep an eye on 2867.29.

continued for members… (more…)

…and, VIX finally breaking down, is it just possible we’ll see a rally this morning?

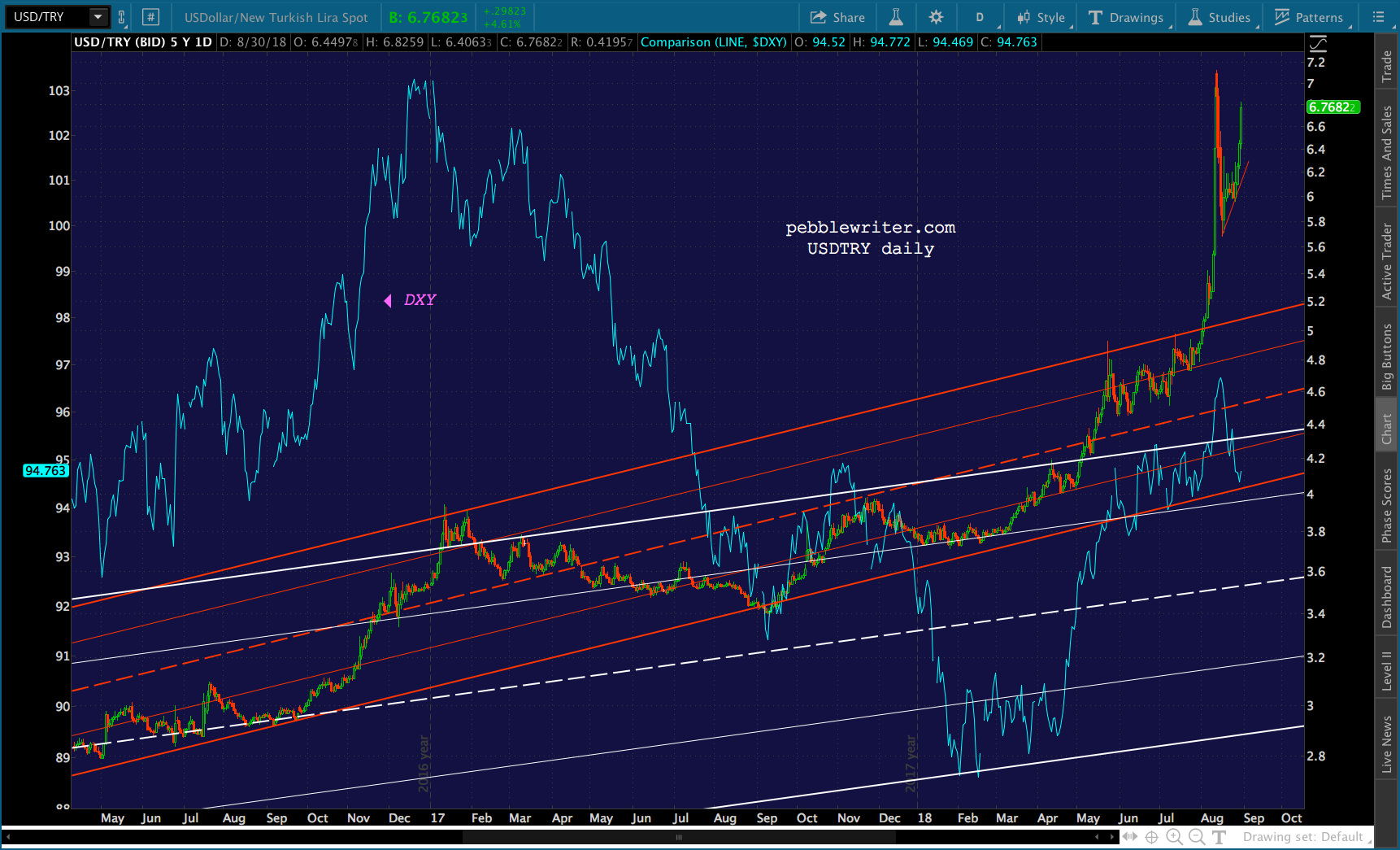

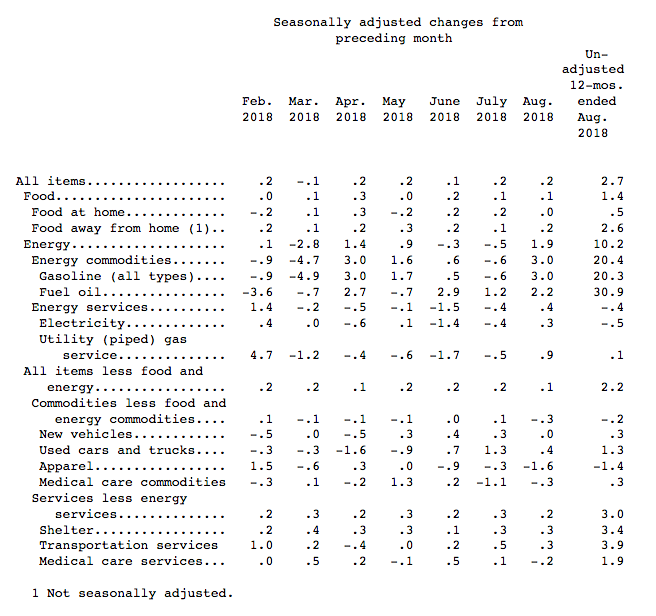

…and, VIX finally breaking down, is it just possible we’ll see a rally this morning? And, why not? Thanks to the timely dip in oil and gas prices (and, some creative accounting over at the BLS), CPI came in at an annual rate of 2.7% — down from last month’s 2.9%.

And, why not? Thanks to the timely dip in oil and gas prices (and, some creative accounting over at the BLS), CPI came in at an annual rate of 2.7% — down from last month’s 2.9%. Toss in a bullish (sp?) statement from Draghi [announcing the end of QE as the ECB trims its growth forecast …yeah, right] and the algos are loving it.

Toss in a bullish (sp?) statement from Draghi [announcing the end of QE as the ECB trims its growth forecast …yeah, right] and the algos are loving it.