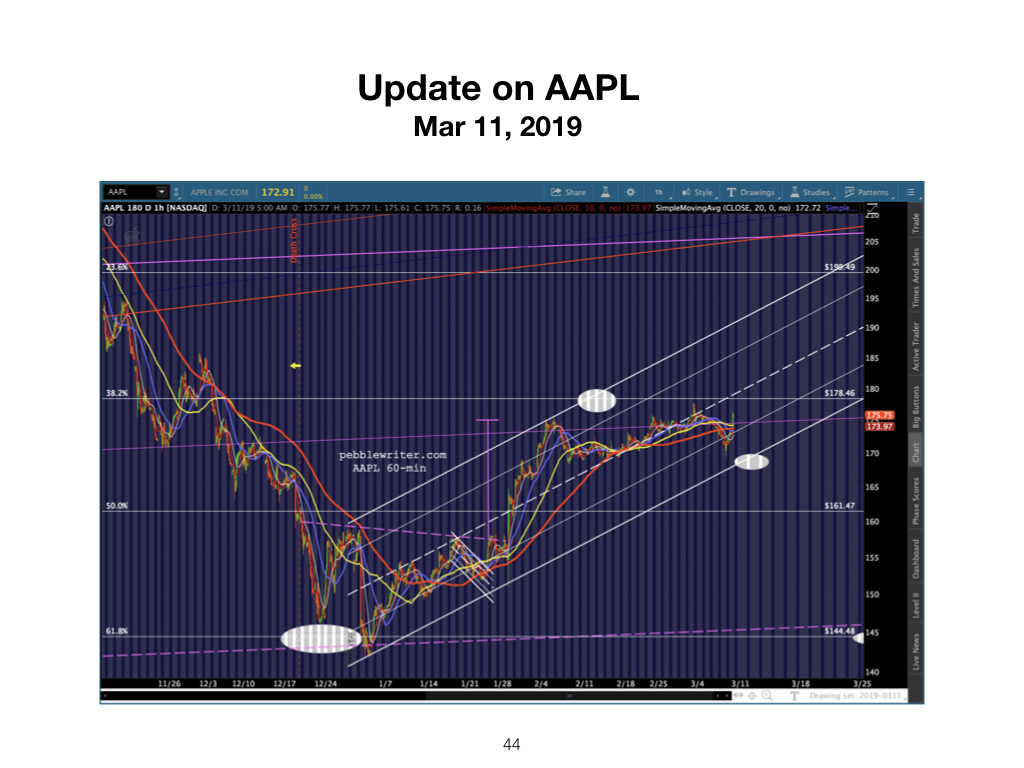

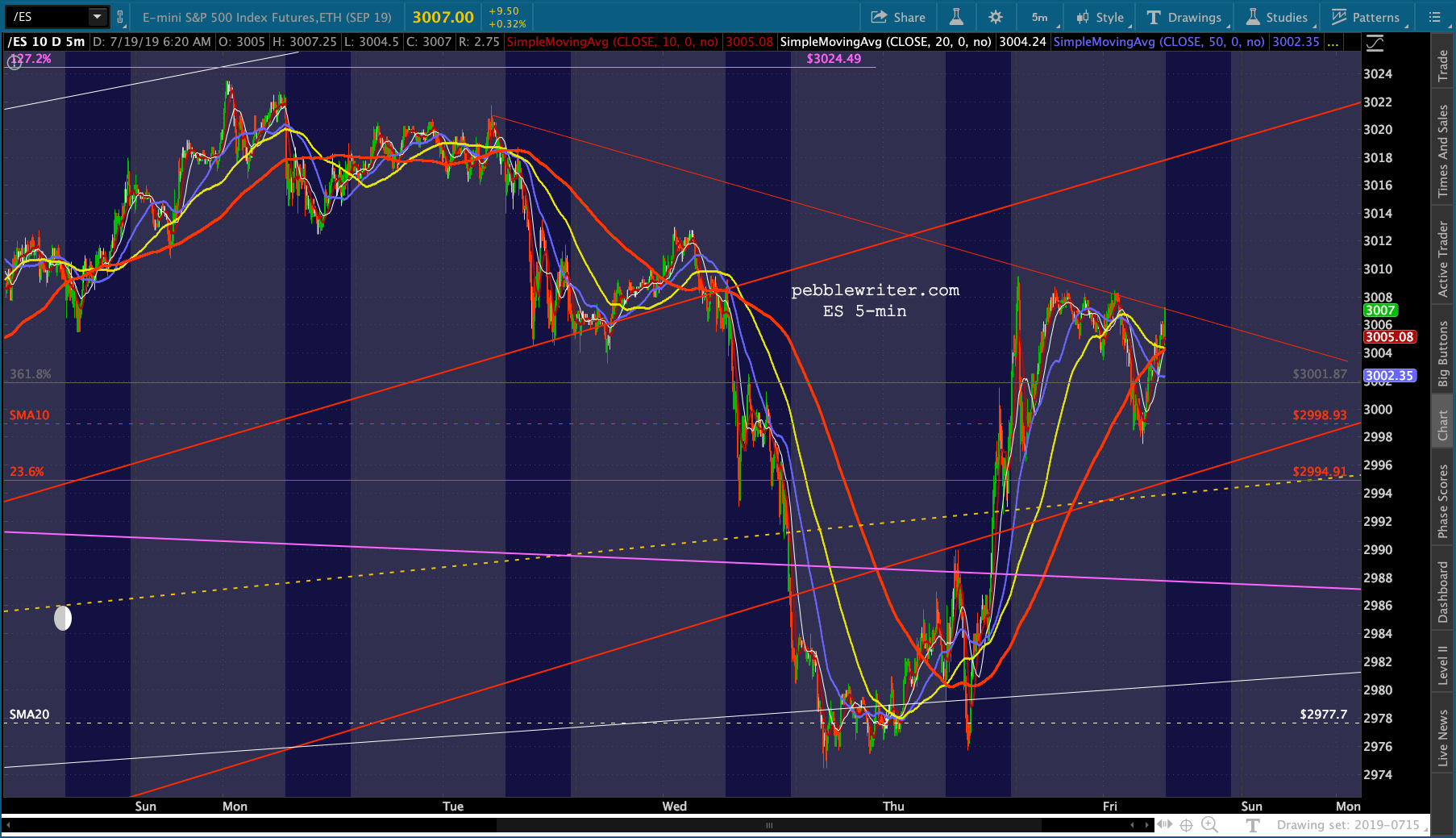

Many of the stocks and indices I follow are sitting right at resistance, as is ES this morning. AAPL has reached our target at the top of its falling channel…

AAPL has reached our target at the top of its falling channel… …DB is bumping up against the TL from Jan 2018…

…DB is bumping up against the TL from Jan 2018… …and BA is within striking distance of the channel top at which it failed yesterday.

…and BA is within striking distance of the channel top at which it failed yesterday. With VIX having reversed yesterday’s breakout and slumped back below its SMA10, the writing is on the wall — but, ES hasn’t yet broken out. Why not?

With VIX having reversed yesterday’s breakout and slumped back below its SMA10, the writing is on the wall — but, ES hasn’t yet broken out. Why not? continued for members… (more…)

continued for members… (more…)

Author: pebblewriter

-

Resistance: Futile?

-

Can Boeing Take Off?

A reminder: our current membership promotion — which slashes the price of a quarterly subscription from $399 to only $299 — is slated to expire tomorrow, July 23. For details and to sign up now, CLICK HERE.

* * *

BA has just about reached our channel top target from Jul 3. From Algos to VIX:

BA’s [chart] indicates another interim bottom.

It has now bounced over 12% since our Jun 3 bottom call signaled by ES’s 2.24 tag and has nearly reached the top of the new, gentler falling purple channel, now at about 380. It’s an important test for the stock — boosted by a monumental PR and its on-again off-again stock repurchase plan.

Note that the current forecast page has been updated for all major charts including

continued for members… (more…)

-

Boston CFA Society Presentation

Thanks to everyone who attended our Boston CFA Society presentation on chart patterns and technical analysis. As promised, here are the slides used in the presentation. Please contact me with any questions.

-

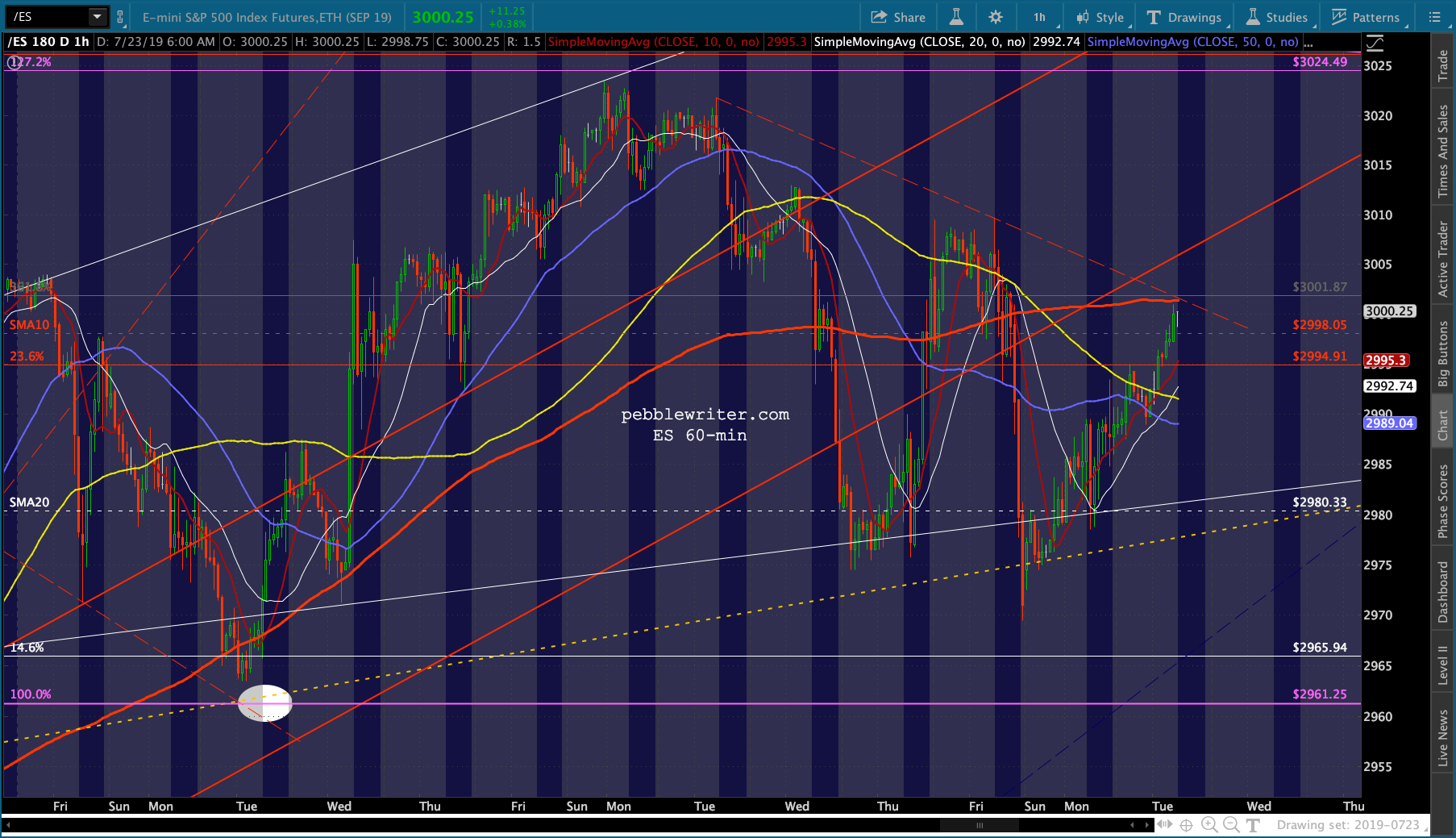

Almost There

Conditions continue to look good for our current analog officially kicking off in 7 sessions. VIX reversed (again) at the fan line off the May 9 highs and backtested an alternate channel bottom — nudging ES higher after a fairly ugly Wednesday.

Oil and gas are closing in on our next downside targets — confounding the “experts.” But, for now, futures are leaking higher and about to test the latest minor obstacle in hopes that the Fed will make everything better. Spoiler alert: it won’t.

Oil and gas are closing in on our next downside targets — confounding the “experts.” But, for now, futures are leaking higher and about to test the latest minor obstacle in hopes that the Fed will make everything better. Spoiler alert: it won’t. Speaking of spoilers…DB has punted on its latest opportunity to break out.

Speaking of spoilers…DB has punted on its latest opportunity to break out. And, BA somehow continues to remain aloft. The real test would be at the purple channel top. Note that it still “owes” us a dip to 325.42.

And, BA somehow continues to remain aloft. The real test would be at the purple channel top. Note that it still “owes” us a dip to 325.42.

continued for members… (more…)

-

Stranger Things at Netflix

First, a confession. In 2004 I sat next to a guy at a Sundance Film Fesitval screening who was very excited about his company that would someday be able to play movies on your computer or even your cell phone. “Why won’t this guy shut up?” I asked myself as I scanned the theater for an empty chair.

Netflix: Looking for more subscribers? The “guy,” of course, was Reed Hastings. At the time, they were barely profitable, having just posted their first net profit ever (a whopping $7 million in 2003.) The stock was hovering around $5/share.

I couldn’t, for the life of me, figure out how they’d ever compete against Blockbuster — which had turned down an offer to acquire the company for $50 million a few years earlier.

The 2004 annual report cover, to the left, illustrated the problem. Why wait for a movie to arrive in the mail when you could run down to the local Blockbuster and grab a copy (along with some tasty Goobers) right now?

Reed was obviously on to something and soon figured out online delivery — though he still hasn’t cracked the eGoober challenge. A $10,000 investment in the common at that time would be worth around $1 million now. Live and learn, right?

* * *

The stock is under pressure this morning as subscriber growth fell short of Street expectations and the company’s guidance. But, I’ll leave that to my fundamental brethren to suss out. My concern is that the stock will test critical support.

Last year we took a look at the chart and noted that at 400.48, it looked particularly vulnerable. From Netflix: Watch It! on July 16, 2018:

A quick glance at NFLX’s daily chart shows it has significant downside potential. The most obvious downside target is the 100-DMA at 338.73. But, the 200-DMA is approaching the white channel midline and should cross it at around 298-300 on or about August 6. It makes for a nice downside target if the SMA100 doesn’t hold. Should the SMA200 and channel midline fail, the bottom of the white channel is currently around 200 and (obviously) rising.

The stock soon tested then failed at the 100-DMA, but bounced just before reaching the midline and popped out of the falling white channel. It thus postponed the midline/200-DMA test until October 11 where it bounced yet again before plunging through to the channel bottom which, by then, was up to 230.

There are a lot of things that could happen to the stock, which has traded as low as 313 in after-hours. But, the critical level to watch is 295-300 where it would drop through the 200-DMA and test the channel bottom as well as backtest the broadening wedge (aka megaphone pattern.)

There are a lot of things that could happen to the stock, which has traded as low as 313 in after-hours. But, the critical level to watch is 295-300 where it would drop through the 200-DMA and test the channel bottom as well as backtest the broadening wedge (aka megaphone pattern.)

Anything lower would be very problematic for a stock which has been locked in the same rising channel for 6 1/2 years.

One note to those focused on the fundamentals. The observations I made last year still apply:

One note to those focused on the fundamentals. The observations I made last year still apply:As an aside… I’ve been mystified as to the value ascribed to the company based on its ability to produce original content. What about the risk? Anyone who has worked in film or television can tell you that most productions don’t turn a profit.

I don’t want to get into production. There are passionate, talented filmmakers out there and I would pollute the craft.

Reed Hastings, Inc Magazine: Dec 1, 2005

Netflix has clearly hit some home runs with House of Cards, Stranger Things, etc. And, theoretically, producing content in-house can lower acquisition cost and diversify revenues.

But, extrapolating an unending string of popular and profitable productions is just plain silly. Some would say borrowing $1.8 billion to fund said productions is downright reckless.

Think New Line, which followed up the hugely successful Lord of the Rings trilogy with the expensive flop The Golden Compass. Investors would do well to remember that beta works in both directions.

* * *

It’s been ages since we offered a discount on memberships. For the next several days, quarterly subscriptions – normally $399 – will be discounted to only $299 for the first quarter. That’s 3 months for less than the price of two on a monthly subscription.

Click here to join now.

Update for members… (more…)

-

Charts I’m Watching: Jul 17, 2019

The conditions remain constructive for our analog. Both RB and CL have broken down and USDJPY is conspicuously not coming to the rescue. In fact, the only thing keeping SPX on the rise is VIX’s repeated threats to make new lows — threats that, so far, have been hollow.

continued for members… (more…)

continued for members… (more…) -

Analog Watch: Jul 15, 2019

We’ve only done five analogs over the years. One worked out spectacularly, three were fairly accurate, and one just plain fizzled.

Ideally, an analog provides exceptionally accurate forecasts of a very significant move. I think this could be one of those and that stocks are on the cusp of the biggest drop since the Great Financial Crisis.

Ideally, an analog provides exceptionally accurate forecasts of a very significant move. I think this could be one of those and that stocks are on the cusp of the biggest drop since the Great Financial Crisis.For more on analogs, click here.

continued for members… (more…)

-

Why Interest Rates Must Not Rise

In May 2014 many of us were shocked by a report that Ben Bernanke, who had recently departed the Fed, told a group of wealthy investors that he did “not expect the federal funds rate…to rise back to its long-term average of around 4%” in his lifetime.

I remember feeling Bernanke’s statement represented both extraordinary hubris and wishful thinking. Surely, the trillions being pumped into the financial system would drive inflation to levels that would produce higher rates. After all, I reasoned, the bond market isn’t as easily manipulated as is the stock market.

Last year, I called attention to the fact that the cost of servicing the US debt had broken out to new highs [see: Why Rising Rates are a Problem This Time.] Even though interest rates had fallen dramatically, the spiraling debt had send annual interest expense on that debt to roughly $450 billion in FY 2017.

Bernanke’s 2014 words came back to me as I did the math.

Bernanke’s 2014 words came back to me as I did the math.Clearly, if rates were to normalize the interest expense would be unmanageable… Between 2000 and 2007, the average interest rate was 4.84%. On the current $20.6 trillion balance, that would mean an annual interest expense of roughly $1 trillion.

Of course he was confident in his prediction! He understood that rates could never be allowed to rise. A return to normalcy — and, I don’t believe this to be an exaggeration — would absolutely destroy the economy.

I had always found the Treasury’s increasing dependence on short-term, floating rate and inflation-indexed borrowings a bit unsettling. Why not lock in a boatload of 30-yr bonds at 2.1%? Now we know.

In their wisdom (or desperation…time will tell) the central bankers and those maxing out America’s Gold Card have bet our very futures that Bernanke was right — that everything will be okay in the end…as long as the end never gets here.

By the way, here’s an update of the above chart…which has been appropriately renamed.

-

The Inflation Problem

It’s great sport to criticize the Fed for what seem like bone-headed moves. Yesterday wasn’t one of them. What Powell knew and rest of us had guessed was that June CPI was headed significantly lower and would continue to widen its divergence with core CPI.

While the futures were ramping higher thanks to Powell’s dovish prepared remarks (which were conveniently released prior to the open)…

While the futures were ramping higher thanks to Powell’s dovish prepared remarks (which were conveniently released prior to the open)…  …few stopped to question why the Fed should ease amidst the most accommodative monetary conditions since 2013.

…few stopped to question why the Fed should ease amidst the most accommodative monetary conditions since 2013. The fact is that Powell was boxed in. Everybody knows that the official inflation data woefully understates actual inflation. This comes in handy when trying to keep a lid on interest rates — a necessity when you’ve got $22 trillion in debt and a $1 trillion budget deficit.

The fact is that Powell was boxed in. Everybody knows that the official inflation data woefully understates actual inflation. This comes in handy when trying to keep a lid on interest rates — a necessity when you’ve got $22 trillion in debt and a $1 trillion budget deficit.But, even flawed CPI is an important signal. It goes a long way toward explaining why oil and gas prices magically decline every time inflation starts to get out of hand…

…and inflation magically declines every time interest rates threaten to get out of hand.

…and inflation magically declines every time interest rates threaten to get out of hand. Put them together and RBOB’s 42% Oct-Dec 2018 plunge (which began only 2 days prior to the 10Y topping out) suddenly makes a whole lot of sense.

Put them together and RBOB’s 42% Oct-Dec 2018 plunge (which began only 2 days prior to the 10Y topping out) suddenly makes a whole lot of sense. Unfortunately, understating inflation is not convenient at all when investors start worrying about deflation — as the current interest rate environment suggests they do.

Unfortunately, understating inflation is not convenient at all when investors start worrying about deflation — as the current interest rate environment suggests they do.Trump & Co. say they want low interest rates and a cheap dollar. Plunging oil and gas prices are the best way to get there. The latest CPI print at 1.65% is testament to how well the mechanism worked. Score one for the White House.

Sure, the trade war, real estate bubble and rising health care costs are bumping Core CPI higher. But, the average voter couldn’t tell you what “CPI” stands for, let alone the difference between the various inflation measures. And, the average investor only cares about inflation if the Dow should happen to slide more than a few percent which, if it occurs, is easily negated by a breathless update on the excellent progress of the trade

warnegotiations.Bottom line, the Fed would face heavy criticism if they stood pat with CPI at 1.6% and falling. The White House is no doubt well aware of this, and is also well aware that YoY comparisons will be pressured by oil and gas’s recent rallies — particularly when October arrives.

This is why oil and gas prices are very unlikely to continue to rise — as the charts confirm.

continued for members… (more…)

-

Powell Placates

Powell’s prepared remarks, released in advance of his testimony before the House Financial Services Committee, confirmed the FOMC is likely to deliver a 25 bps rate cut at the end of the month. This is what almost everybody

demandedexpected, so the algos have found their happy place.S&P futures, which lagged all night, are currently showing a 24 pop off the overnight lows — nearly enough to send the cash index to new all-time highs.

continued for members… (more…)

continued for members… (more…)